- Analiza

- Novosti i instrumenti

- Vesti sa tržišta

Forex-novosti i prognoze od 07-09-2023

- EUR/USD trades at 1.0696, up 0.01%, but remains below the pivotal 1.0700 mark, signaling potential for further downside.

- For a bullish reversal, the pair needs to clear 1.0700 and aim for September 6 daily high of 1.0748 as an intermediate resistance.

- Most likely scenario sees EUR/USD targeting May 31 low of 1.0635, with a breach potentially exposing the 1.0600 psychological level.

The EUR/USD begins the Asian session almost flat but below the 1.0700 figure, seen as a bearish signal, after printing losses of 0.29% on Thursday, which could open the door to test May lows. At the time of writing, the major trades at 1.0696, up 0.01%.

EUR/USD Price Analysis: Technical outlook

The daily chart portrays a continuation of the downtrend, as the pair achieved a new lower-low and trades near the bottom of the weekly range. However, being the 1.0700 figure that usually keeps the EUR/USD seesawing in the top/bottom of the double zero mark, buyers and sellers need to take action to win the battle.

For buyers, the EUR/USD must climb above 1.0700 and reclaim the September 6 daily high of 1.0748, an intermediate resistance level. Once cleared, the pair's next ceiling level would be the September 5 high at 1.0798 before challenging the 200-day Moving Average (DMA) at 1.0822.

On the flip side, and the most likely scenario, due to recent economic data and the EUR/USD breaking decisively below the 200-DMA, the first support would be the May 31 daily low of 1.0635. A breach of the latter will expose the psychological 1.0600 figure, followed by the March 15 swing low of 1.0516.

EUR/USD Price Action – Daily chart

- NZD/USD remains on the defensive around 0.5875 amid the cautious mood.

- US Initial Jobless Claims declined to 216,000; Continuing Claims totaled 1.679 million, beating market estimates.

- US economic data lends support to the higher for longer interest rate narrative.

- The concern over of Chinese economic slowdown might exert some selling pressure on the Kiwi.

The NZD/USD pair remains under pressure below the 0.5900 barrier during the early Asian session on Friday. The US Dollar (USD) gains momentum as investors price in a quarter basis point (bps) hike in interest rates by the Federal Reserve (Fed) for the rest of the year. The pair currently trades near 0.5875, gaining 0.03% on the day.

Data released by the US Department of Labor on Thursday showed that the US Initial Jobless Claims totaled 216,000 in the week ending of September 2. This figure surpassed the market's forecast of 234,000 and followed the previous week's revised figure of 229,000 (from 228,000). Meanwhile, Nonfarm Productivity rose by 3.5%, below the 3.8% market expectation and revised from the first estimate of 3.7%. In response to the data, the US Dollar Index (DXY) edged higher to the highest level since early March above the 105.00 area,

New York Federal Reserve (Fed) President John Williams stated that inflation is heading in the right direction while adding that he requires additional information before making a decision. Chicago’s Fed President Austan Goolsbee said the Fed may achieve the golden path, where inflation erases but a recession is avoided. Along with The Federal Reserve (Fed) Governor Christopher Waller last week, he said that there is further room to increase interest rates, but the data will determine whether the Fed needs to hike rates again and if it is done hiking rates.

Nevertheless, the US economic data lends support to the "higher for longer" interest rate narrative, which boosts the Greenback across the board. According to the CME FedWatch Tool, markets have priced in 93% odds of holding the interest rate at the September meeting, while the probability of raising rates in its November meeting is around 51%.

On the Kiwi front, Statistics New Zealand showed on Thursday that the nation’s Manufacturing Sales for the second quarter improved to 2.9% versus a 2.1% drop in the previous reading. Earlier this week, the ANZ Commodity Price for August dropped to 2.9% from a 2.6% decline in July. The New Zealand Terms of Trade Index improved to 0.4% in the second quarter, compared to a decline of 1.5% in the previous reading and an expected drop of 1.3%. Apart from the data, the fear of the economic slowdown in China and the property debt crisis might exert some selling pressure on the China-proxy New Zealand Dollar (NZD).

Moving on, market participants will digest the data and wait for fresh impetus. In the absence of top-tier economic figures from both New Zealand and the US, risk sentiment will be a key factor for the pair movement. On Saturday, the Chinese Consumer Price Index (CPI) YoY for August will be released and it might trigger volatility in the next sessions. These figures could give a clear direction for NZD/USD.

- AUD/USD trades flat at 0.6375 as Australia posts a trade surplus of A$8 billion in July, missing estimates and sparking risk-off sentiment.

- US jobless claims of 216K beat estimates, reinforcing the Fed’s ‘higher for longer’ stance and putting downward pressure on AUD/USD.

- Traders eye upcoming economic indicators from Australia and the US, including Westpac Consumer Confidence and US inflation figures.

The Aussie Dollar (AUD) pared its losses versus the US Dollar (USD) on Thursday after US economic data showed the US Federal Reserve (Fed) work is far from done, while weakness in China’s exports weighed the market mood. At the time of writing, the AUD/USD is trading at 0.6375, flat as Friday’s Asian session commences.

The Aussie Dollar remains flat against the US Dollar as strong US jobless claims and China’s export slowdown create a mixed trading environment

Australia’s economic docket showed that Imports surpassed Exports, but still, it showed a surplus on its Trade Balance of A$8 billion in July. Although the data is encouraging, missed estimates. That, alongside a weaker improvement of China’s exports, spurred a risk-off impulse that carried on throughout the whole trading day, with Wall Street finishing with losses, except for the Dow Jones, witnessing decent gains of 0.22%.

Aside from this, US economic data revealed by the US Department of Labor reinforced the Federal Reserve’s need to hold rates higher for longer, as said by its Chairman Jerome Powell. Unemployment claims for the last week rose by 216K, below estimates, while Continuing Claims gave signals that conditions are tightening.

The data bolstered the US Dollar (USD), which, as shown by the US Dollar Index, printed gains of 0.20%, standing near yearly highs above 105.000. Therefore, the AUD/USD was downward pressure near the 0.6350s area.

Meanwhile, US Treasury bond yields retreated somewhat, as money market futures slashed bets the US Federal Reserve would continue to tighten monetary policy, past the current Federal Funds Rate (FFR) at 5.25%-5.50%, Odds for a 25 bps rate hike in November, are at 43.4%.

Recently, Federal Reserve officials have kept their options open regarding deciding the forward path of monetary policy. John Williams from the New York Fed said that policy is “restrictive” but refrained from commenting on his decision. Of late, Chicago’s Fed President Austan Goolsbee said the Fed could reach the “golden path” where inflation falls but recession is avoided.

AUD/USD traders should be attentive to next week’s data. The Australian economic docket would feature the Westpac Consumer Confidence, NAB Business Confidence, and employment data. On the US front, inflation figures, Retail Sales, Industrial Production, unemployment claims and Consumer Sentiment would shed some light regarding the Fed’s future decision.

AUD/USD Price Analysis: Technical outlook

The daily chart portrays the pair subdued at around the year lows of 0.6357, printing back-to-back sessions of spinning tops, suggesting that neither buyers nor sellers are in charge. However, the trend remains downward, and if the AUD/USD drops below 0.6357, expect a challenge of the 0.6300 figure. Once cleared, the major would test the November 22 low of 0.6272. On the flip side, upside risks emerge above the September 6 high of 0.6405, with the next resistance at the September 5 high at 0.6464.

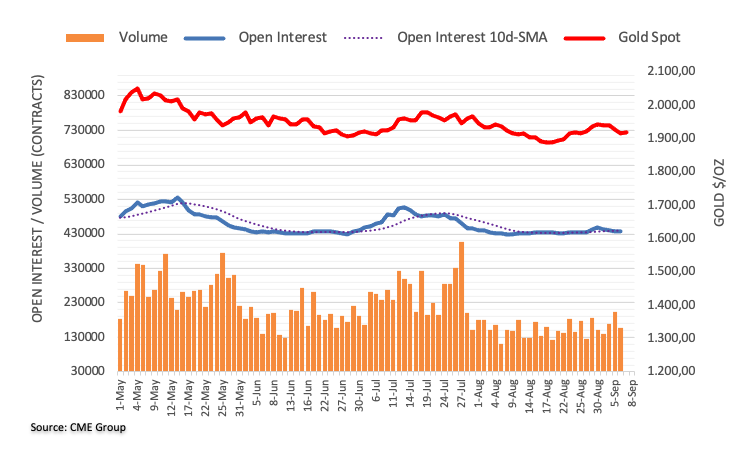

- XAU/USD found support at the convergence of the 20 and 200-day SMAs at $1,915.

- Jobless Claims for the first week of September from the US came in lower than expected.

- Tightening expectations for the Fed and US yields remain high.

The Gold Spot price XAU/USD recovered some ground after finding support at the $1,915 area, jumping towards $1,920. However, the upside is limited as the expectations of one last Federal Reserve (Fed) hike grow in the markets.

During the American session, it was reported that Initial Jobless Claims for the first week of September came in lower than expected. The figure came in at 216,000, lower than the expected figure of 234,000 and declining from the previous 228,000.

The US Treasury yields, often seen as the opportunity cost of holding non-yielding metals, declined on Thursday and allowed the yellow metal to gather momentum. That being said, they still remain high as markets are placing bets on the Federal Reserve (Fed) hiking again in this tightening cycle, in November or in December, as the US is showing evidence of its economic activity remaining strong despite the Fed's aggressive moves. The focus shifts to next week's Consumer Price Index (CPI) data from the US in order for markets to continue modelling their expectations.

XAU/USD Levels to watch

Based on the daily chart, XAU/USD maintains a neutral to bearish technical perspective, suggesting that the bears are gradually gaining momentum but are not yet in total control. The Relative Strength Index (RSI) exhibits a positive slope below its midline, while the Moving Average Convergence (MACD) lays out decreasing green bars.

Support levels: $1,915 (Convergence of 20 and 200-day SMA), $1,900, $1,880.

Resistance levels: $1,930, $1,950, $1,970.

XAU/USD Daily Chart

-638297203807772297.png)

- USD/CHF rose to 0.8925, up by 0.20% daily.

- Switzerland Unemployment data from August didn’t show any surprises.

- Hawkish bets on the Fed boosts the USD

On Thursday, the USD/CHF continued to gain ground, driven by a strong USD whose DXY index traded at highs since March above 105.00.

On the data front, the US reported that Initial Jobless Claims came in lower than expected in the first week of September, with the headline figure at 216,000, lower than the expected figure of 234,000 and decelerating from the previous 229,000. On the Swiss side, the Unemployment rate came in at 2.1% in August, matching the consensus.

What’s strengthening the USD seems to be investors placing hawkish bets on the Federal Reserve (Fed) due to the continuing favourable reports of the US economic activity. Despite US Treasury yields decreasing, the CME FedWatch tool suggests that swaps markets are pricing in higher probabilities of nearly 40% of a 25 basis point (bps) hike by the Fed in the November and December meetings.

USD/CHF Levels to watch

The daily chart analysis shows that the short-term outlook for USD/CHF appears bullish. The Relative Strength Index (RSI) and Moving Average Convergence Divergence (MACD) maintain favourable positions, with the RSI above its midline and displaying an upward trend and the MACD exhibiting green bars. In addition, the pair is above the 20 and 100-day Simple Moving Averages (SMAs), but below the 200-day SMA, pointing towards the prevailing strength of the bulls in the larger context.

Support levels: 0.8900, 0.8877 (100-day SMA), 0.8850.

Resistance levels: 0.8950, 0.9000, 0.9030.

USD/CHF Daily Chart

-638297162038382097.png)

- Polish central bank cuts interest rates deeper than expected, draws criticisms.

- Politics appear to be influencing central bank action rather than the economy.

- Polish inflation is still in double-digit territory despite recent declines.

The USD/PLN is pushing higher following an interest rate cut from the National Bank of Poland (NBP), sending the Polish Zloty (PLN) into a tailspin. The NBP cut their reference rate from 6.75% to 6% on Wednesday, and the move is sending the PLN to five-month lows, erasing much of 2023’s gains.

Polish annual inflation remains slightly above 10%, far below the peak of 18% from earlier this year but still well above the NBP’s target of 2.5%. The Polish economy is also showing signs of a deepening slowdown, and too much movement from the NBP could exacerbate problems for the Polish economy.

Polish central bank accused of political motivations

NBP Governor Adam Glapinski, an open supporter of the governing Law and Justice conservative party, has been criticized for the poorly timed rate cut. Marek Tatala, vice president of the Economic Freedom Foundation, publicly stated that the central bank has “joined the election campaign” using his position at the NBP to try and stoke popularity for the ruling party by easing borrowing costs.

Reductions to the inflation rate will help to make lending rates cheaper in the short term, but Polish politician Ryszard Petru noted in a statement that cutting rates will be “pro-inflationary”, which could make life harder for the Polish population moving forward.

USD/PLN technical outlook

The USD/PLN has broken well above the 100-day EMA on the daily candles and appears set to continue breezing past the 4.3000 psychological level as the PLN eats away at the progress made through the year. The USD peaked against the Zloty in late 2022 near 5.000, reaching a floor of 3.9354 in July.

Technical resistance currently rests at the upper bound of April’s consolidation zone, just below 4.5000, and any bearish resurgence will face dynamic support from the 100-day EMA that is beginning to rotate bullish from 1.4500.

USD/PLN Daily chart

- Eurostoxx closes down on weak European data releases.

- DAX manages to hold steady as the German economy leads the EU group.

- FTSE saw a hesitant step upward as BoE signals a possible end of rate hikes.

Thursday’s European market session ended with a mixed bag thanks to the United Kingdom’s (UK) Financial-Times Stock Exchange 100 Share Index (FTSE 100) managing to hang onto intraday gains and close the day up around 0.35% near £7,430.

UK FTSE lifts on dovish BoE Gov Bailey

UK stock markets were potentially relieved to hear from the Bank of England’s (BoE) Governor Andrew Bailey that the peak of the rate hike cycle may have been achieved. Dovish comments from both Governor Bailey and policymaker Swati Dhingra helped to prop up the UK indexes, but the action came at the expense of the Pound Sterling (GBP), which broadly stepped lower on the news.

On the European Union (EU) side of The Channel, the Eurostoxx 50 closed lower, down -0.24% for Thursday. European equities continue to struggle under the weight of consistently underperforming economic data for the region, and growing fears of a slowdown are beginning to sap buying strength across the indexes. The Eurostoxx 50 closed out the day near €4,220.

German DAX holds steady for Thursday

Germany’s DAX index managed to avoid any losses, closing mostly flat on the day near €15,700. With economic data for the broad EU region beginning to show signs of weakness, Germany enjoys the benefit of having the least weak data. Still not good enough to spark confident rallies in the equity indexes, but enough to stave off further moves to the bearish side.

FTSE Technical outlook

The FTSE 100 will be the index to watch as equities grapple with possible policy stance changes from the BoE. Inflation may be bedding back down for the UK, but the technical positioning still leans bearish for the moment.

Current price action is struggling to make a clean break from the declining pattern from August’s start near £7,700, and bullish momentum remains limited from the £7,450 level. Continued short action will see support from August’s lows near £7,250, a level that saw similar technical support back in July.

- The GBP/JPY can’t find a decent boost from near-term bottom.

- BoE Governor Bailey warns rate hike cycle could be approaching the end.

- Japan GDP data to determine JPY flows heading into the end of the week.

The GBP/JPY pairing is on the downside as the Pound Sterling (GBP) stumbles on comments from the Bank of England (BoE) Governor Andrew Bailey suggesting the rate hike cycle could be nearing its end. It’s been up-and-down action for the Guppy chart as the GBP struggles to find a foothold against the Yen (JPY). The week’s early near 185.75 couldn’t hold and now the pair is swamped near the bottom of a three-week channel near the 183.50 level.

Dovish BoE saps Pound Sterling momentum, sends GBP lower

BoE Governor Bailey hit the wires early Thursday with dovish comments about the BoE rate hike cycle, implying September’s rate call could see the end of interest rate increases from the United Kingdom’s central bank. Policymaker Swati Dhingra also hit the airwaves, echoing Governor Bailey’s dovish rate sentiment.

Japan GDP figures are on the docket, mild contraction expected

It's a data-light week for the GBP, and JPY traders will be keeping an eye out for Japanese Gross Domestic Product (GDP) figures due during Tokyo’s Friday market session. Japan’s GDP grew by 1.5% during the first quarter of 2023, and Q2 GDP is expected to show a minor reduction in the headline figure to 1.3%.

Technical outlook

The GBP/JPY sees contracting resistance from late August’s peak near 186.75, with lower highs tapping out a descending trendline. The near-term floor has been priced in near 183.60, and 4-hour chart technical indicators are beginning to flash oversold conditions.

On the daily candles, 184.00 is developing into a significant level for the Guppy, and while the overall trend remains decidedly bullish from the year’s lows near 156.00, upside momentum has been evaporating steadily. Bearish momentum from this level will see the GBP/JPY running into support from the 180.00 to 181.00 region.

GBP/JPY, 4-hour chart

The US Dollar remains firm, and on Friday, it will attempt to defend or extend the weekly gains. During the Asian session, Japan will release Q2 GDP data. Later in the day, the highlight will be the Canadian jobs report.

Here is what you need to know on Friday, September 8:

Wall Street finished mixed, with the Dow Jones gaining 0.17% and the Nasdaq falling 0.89%. Caution still prevails in the markets. US Treasury yields jumped initially after the release of US economic data but later pulled back. The US 10-year yield settled around 4.25%.

Data released in the US on Thursday revealed a decline in Initial Jobless Claims to 216K and Continuing Claims to 1.679 million, surpassing market estimates. Following the report, the US Dollar Index reached a peak of 105.15, its highest level since March, before retracing slightly to 105.05. Economic figures bolster the "higher for longer" interest rates narrative and provide support for the US Dollar.

EUR/USD posted its lowest daily close in three months, just below 1.0700. The Euro appears vulnerable, moving with a clear downward bias and showing no signs of stabilization. The final release of Germany's Consumer Price Index is upcoming, and no surprises are anticipated. Looking ahead, the European Central Bank (ECB) will hold its monetary policy meeting next week, and there is currently no clear consensus on what actions it may take regarding interest rates.

Analysts at Danske Bank on ECB meeting:

The worsened economic outlook and markets turning more dovish, we expect the ECB to deliver a 25bp hike at the September meeting, marking a peak in the deposit rate of 4.00%. After all, the ECB has an inflation mandate rather than facilitating economic activity.

USD/JPY pulled back modestly after reaching fresh multi-month highs just below 148.00. The reversal in US yields provided support to the Japanese Yen on Thursday. Japan is set to release Q2 GDP growth data on Friday.

The British Pound registered its fifth daily decline out of the last six days, against the US Dollar. GBP/USD hit a three-month low at 1.2445, close to the 200-day Simple Moving Average (1.2425), before paring losses and rising to 1.2470.

Despite signs of stabilization in China's trade data, the Australian Dollar continues to face pressure from commodity prices and a stronger US Dollar. AUD/USD remains range-bound between 0.6360 and 0.6400, near monthly lows, with a downside bias.

The Canadian Dollar underperformed during the Americas session, despite upbeat Building Permits and Ivey PMI data. Following the Bank of Canada's decision to keep interest rates unchanged at 5%, Governor Macklem explained the decision and mentioned that there is little downward momentum in underlying inflation. USD/CAD rose to its highest level since March and is eyeing the 1.3700 area. Canada will release the August employment report on Friday.

TD Securities on Canadian jobs data:

We look for the economy to add 20k jobs in August, slightly below the 6m trend and well below levels required to keep up with population growth, with a partial rebound in construction helping to drive the headline print. A 20k print would leave the UE rate stable at 5.5%, while softer wage growth should give the report a dovish tone even if jobs print slightly above consensus.

Like this article? Help us with some feedback by answering this survey:

In an interview with Bloomberg, New York Federal Reserve President John Williams mentioned that inflation is moving in the right direction. Regarding the September FOMC meeting, he said he needs more data before deciding.

Williams added that labor market imbalances are evening out and that demand is coming down. According to him, the question before the Fed is whether monetary policy needs to be more restrictive.

He sees the risk of stronger-than-expected growth and projects the unemployment rate to edge up over the next year.

Market reaction

The US dollar pulled back marginally after the beginning of Williams' comments. The US Dollar Index is hovering around 105.00.

- Silver falls 0.83% despite a pause in US Treasury bond yield uptrend, as strong US jobless claims data hints at further Fed action.

- Money markets currently rule out rate hikes for the remainder of the year, but upcoming CPI data could reignite discussions.

- Traders eye US real yields and upcoming inflation data, as any upward revisions could signal headwinds for precious metals.

Silver price plunged 0.83%, although US Treasury bond yields paused their uptrend after data from the United States (US) sponsored speculations the US Federal Reserve is not done raising interest rates. Despite this, the Greenback (USD) is rising a headwind for the white metal. The XAG/USD is trading at $22.97 per troy ounce after hitting a daily high of $23.18.

XAG/USD drops BELOW $23.00 amid robust US jobless claims, putting precious metals under pressure as rate hike talks resurface

The precious metals segment, mainly the white metal, is under pressure, as Gold remains steady at $1,920.00 a troy ounce, gaining 0.18%. Solid data revealed by the US Department of Labor showed that Americans filling for unemployment claims was below expectations of 229K in the last week, with data coming at 216K. Although weekly measures tend to be volatile, Continuing Claims fell by 40K to 1.679 million in the week ending August 26, the lowest level since the week ended on July 15.

Given that the latest US Nonfarm Payrolls report for August was solid, despite seeing an uptick in the Unemployment Rate from 3.5% to 3.8%, it appears the Fed still has work to do.

However, after today’s data, money markets do not expect any rate hikes from the US central bank for the remainder of the year. Even though chances of a 25 bps rate hike are still below 50%, next week’s data could spark discussions about November’s meeting.

Next week, the US Department of Labor will reveal inflation in the country. The Consumer Price Index (CPI) for August is expected to come at 3.4% YoY, while core CPI, which excludes volatile items, is foreseen at 4.5% YoY. The former is projected to increase compared to July’s data, contrarily to core CPI.

Upward revisions on the data would add to already high inflationary pressures in the US and trigger action by the Federal Reserve. Traders should be aware that policymakers will enter its blackout period on Saturday. So, any signals must be viewed with a pinch of salt, as next week’s data could trigger a change of direction in the US central bank.

If US data suggests further tightening is needed, that would be a headwind for precious metals, as US Treasury bond yields would likely advance. Traders must follow the direction of US real yields, which are US nominal bond yields minus inflation expectations. Currently, the US 10-year TIPS, seen as a proxy for real yields, stands at 1.955%, three bps below its opening price.

XAG/USD Price Analysis: Technical outlook

Silver price is set to extend its losses after decisively clearing the 200-day Moving Average (DMA) at $23.46, while the 50-DMA closes into the former, threatening to form a death-cross, seeing as a bearish signal. If XAG/USD achieves a daily close below $23.00, expect further downside, with the August 15 daily low of $22.23 seen as the next support before it tumbles toward the June 23 swing low of $22.11. Conversely, buyers’ initial resistance would be seen at the 200-DMA, followed by the 50-DMA at $23.71.

The US Dollar can exhibit more strength through the end of the current year than previously expected, argue analysts at Wells Fargo. They point out that China's slowdown and a resilient US economy can support the Greenback. However, longer term, they see dollar depreciation.

Key quotes:

We are now more optimistic on the dollar's prospects over our entire investment horizon. Given our view for a deteriorating macroeconomic backdrop amid a sharp China deceleration, we believe the dollar could attract safe haven flows that boost the greenback through the end of this year.

We also believe the resilience of the U.S. economy and the possibility of additional Fed rate hikes should also attract investors toward dollar-denominated assets and support the greenback through the end of 2023.

Longer term, we continue to forecast a weaker dollar; however, we now believe the greenback will experience a slower pace of depreciation than previously. We still expect Fed rate cuts to weigh on the dollar next year, but with a U.S. “soft landing” a real possibility and inflation likely to hover above the Fed's target in 2024, sharp rate cuts are now less likely.

With the Fed likely to deliver a version of a “higher for longer” stance on interest rates, the dollar can now exhibit more resilience over the course of 2024.

- GBP/USD declined for a third consecutive day towards the 1.2470 area.

- Initial Jobless Claims from the US from the first week of September come in lower than expected.

- Investors await next week's CPI figures from the US from August.

- Market’s bet on a less aggressive BoE after Monetary Policy hearings on Wednesday.

On Thursday, the GBP/USD turned south and seems to be heading to the 200-day Simple Moving Average (SMA) at 1.2420 for a restest. A resilient USD and falling British yields are responsible for the pair’s movements.

On the data front, Jobless Claims from the week ending on September 1 came in slightly lower at 216,000 vs. the 234,000 expected, decelerating from the previous weekly reading of 229,000. The initial reaction boosted the USD, and the DXY increased to nearly 105.10.

The US Treasury yields are retreating but remain high, suggesting investors are gearing up for another Federal Reserve (Fed) hike this cycle. The 2-year consolidated Wednesday’s upward movements and declined below 5%, while the 5 and 10-year yields stand at 4.38% and 4.26%. Regarding expectations, economic activity in the US remains robust and doesn’t show signs of cooling, which would give the Fed the green light to consider one last hike. In that sense, the CME FedWatch tool suggests that the odds of one more 25 basis point (bps) hike stand near 40%, keeping the USD afloat.

On the GBP’s side, the 2,5 and 10-year rates are seeing more than 1% declines and may reflect that investors foresee a less aggressive Bank of England (BoE). On Wednesday, Andrew Bailey commented that the bank would remain data-dependent and didn’t commit to further hikes. At the same time, Swati Dhingra pointed out that the policy is “sufficiently restrictive”.

GBP/USD Levels to watch

The technical analysis of the daily chart points to a neutral to bearish outlook for GBP/USD, indicating the potential for further bearish movement. The Relative Strength Index (RSI) is getting nearer to oversold conditions, while the Moving Average Convergence (MACD) histogram presents rising red bars. Moreover, the pair is below the 20 and 100-day Simple Moving Averages (SMAs), but above the 200-day SMA, suggesting that despite the recent bearish sentiment, the bulls are still resilient, holding some momentum.

Support levels: 1.2420 (20-day SMA), 1.2400, 1.2380.

Resistance levels: 1.2470, 1.2500, 1.2550.

GBP/USD Daily Chart

-638297092469356213.png)

- EUR/USD trades at 1.0707, down 0.19%, as US jobless claims of 216K outperform the expected 229K, fueling a Fed rate hike speculation.

- Eurozone Q2 GDP grows a meager 0.1%, missing market expectations of 0.3%, raising concerns of a potential economic contraction.

- Despite high inflation, traders expect the ECB to maintain rates, though a hawkish statement from Lagarde is anticipated.

The Euro (EUR) caps its fall against the Greenback (USD) but remains trading with losses of 0.19% after data from the Eurozone shows the bloc grew at a marginal pace. Contrarily, the United States (US) labor market remains robust, as demonstrated by data. The EUR/USD is trading at 1.0700 after hitting a daily high of 1.0731.

Euro struggles against a resilient US Dollar as Eurozone GDP disappoints and US jobless claims beat expectations

Data revealed from the US Burea of Labor Statistics (BLS) showed the jobs market remains resilient amidst 525 basis points of tightening by the Fed, as Initial Jobless Claims for the last week printed 216K new fillings for unemployment, well below the 229K foreseen by analysts. This data spurred a repricing of further tightening by the US Federal Reserve, with chances for a 25 bps hike in November ticking up to 43%. Regarding September’s meeting, money market futures have priced in the Fed would stay put.

Consequently, the EUR/USD pair edged lower and hit a low of 1.0688. Since then, the pair has recovered territory and the 1.0700 figure, sponsored by US Treasury bond yields, registering modest losses. At the same time, the Greenback lost some ground, as the US Dollar Index (DXY) fell below the 105.000 mark but clung to gains of 0.11%.

Earlier in the European session, Eurostat revealed the Gross Domestic Product (GDP) for the second quarter (Q2) in the bloc grew by just 0.1%, lower than the 0.3% expected by the markets. Although the EU had missed a recession, recently revealed data showing that business activity is slowing, Industrial Production is dropping, and hawkish stances by European Central Bank (ECB) policysetters could pave the way for an economic contraction in the Eurozone.

Given the backdrop, the EUR/USD pair is set to continue to weaken despite the ECB’s hawkish commentary. Although inflation remains high, downside risks in the EU compared to the United States (US) paint a gloomy scenario for Europe. At the upcoming September meeting, traders expect the ECB to keep rates unchanged, though Lagarde and Co are foreseen to deliver a hawkish statement.

EUR/USD Price Analysis: Technical outlook

The pair’s fall below 1.0700 has opened the door for further losses, with sellers eyeing the next intermediate support at 1.0635, the May 31 swing low. Once cleared, there’s no demand area until the EUR/USD drops towards the March 15 daily low at 1.0516. Conversely, buyers can remain hopeful of higher prices if the major prints a daily close above 1.0700. First resistance would be September 7 high at 1.0731, followed by the September 6 high at 1.0748 and 1.0800.

Tiff Macklem, Governor of the Bank of Canada mentioned on Thursday that monetary policy “may be sufficiently restrictive to restore price stability” but warned the Governing Council “is concerned about the persistence of underlying inflation.” On Wednesday, the BoC kept its key interest rate unchanged at 5%.

Speaking before the Calgary Chamber of Commerce, Macklem added that they are prepared to raise rates further, if they have to, in order to “restore price stability”. After reading his remarks, the Governor will take questions from reporters.

Key takeaways from the speech:

We’ve come a long way in the past year. Monetary policy is working, and inflation is coming down. But we still have some way to go to restore price stability. With past interest rate increases still working their way through the economy, monetary policy may be sufficiently restrictive to restore price stability. However, Governing Council is concerned about the persistence of underlying inflation. Inflation is still too high, and there is little downward momentum in underlying inflation.

We will be carefully assessing the balance between demand and supply and underlying inflation to gauge progress toward price stability. If we need to raise interest rates further to restore price stability, we are prepared to take further action. But we don’t want to raise our policy rate more than we have to.

We know higher interest rates are hitting some Canadians hard, and we don’t want this to be any harder than necessary. But letting too-high inflation persist would be worse. We are confident that 2% is the right target. The target is now in sight. We need to stay the course.

Market reaction

The USD/CAD remained relatively steady hovering around 1.3670, on its way to the highest daily close in months.

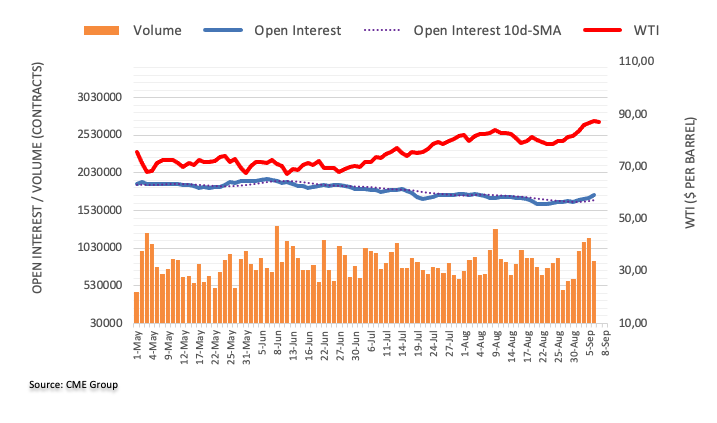

- WTI decreased by more than 0.80%, below $87.00.

- Global tighter supply amid further extensions of voluntary cuts on OPEC+ countries limits the downside for WTI.

- US Crude Oil stockpiles decreased in the first week of September, above expectations.

In Thursday's session, the West Texas Intermediate (WTI) retreated below $87.00, near $86.30, after releasing the Energy Information Administration (EIA) stock data. On the USD side, despite falling yields, it stays resilient and contributed to the WTI’s decline.

On the data front, the Energy Information Administration (EIA) reported that Crude Oil stocks decreased by 6.37M in the first week of September, higher than the expected 2.06M, but failed to trigger a reaction on the WTI. Furthermore, as Oil contracts are denominated in USD, a stronger Greenaback limits the upside potential in the session, and the expectations of one last hike of the Federal Reserve (Fed) give the Greenback traction. On Thursday's session, it was reported that the number of people filling for unemployment benefits increased but was lower than expected, suggesting that the labour market remains resilient.

As for now, the odds of a hike in November or December by the Fed, according to the CME FedWatch tool, increased to 40%. High rates tend to cool down the economies, so solid economic figures may allow the Fed to continue hiking, limiting the WTI’s potential in the short term.

On a positive note, Saudi Arabia, the biggest Oil exporter in the world, is set to extend its voluntary production cuts throughout the rest of 2023 by 1.66 million barrels per day (bpd) after announcing a 1 million reduction in July. In that sense, supply forces may limit the downside for the WTI.

WTI Levels to watch

Analyzing the daily chart, the WTI's technical outlook is bullish in the short term, but indicators still flash overbought signals meaning that the price may correct in the next sessions. The Relative Strength Index (RSI) is above 70 with a negative slope, while the Moving Average Convergence Divergence (MACD) displays stagnant green bars. In the larger context, the pair is above the 20,100,200-day Simple Moving Average (SMA), suggesting that the bulls are firmly in control..

Support levels: $86.00, $85.50, $84.00

Resistance levels: $87.00, $87.50, $88.00

WTI Daily Chart

-638297048967901278.png)

- The EUR has managed to climb up the charts against the GBP, but upside momentum remains limited.

- Eurozone data continues to miss expectations but hasn’t turned negative yet.

- Data-light GBP leaves the calendar open for the Euro.

The Euro (EUR) has managed to claw back some ground from the Pound Sterling (GBP) as of late, but the chart action has been middling for Thursday as the neighboring currencies play tug-of-war for chart momentum. It’s been a data-light week for the GBP, leaving the economic calendar decidedly Euro-centric for scheduled data events.

Gross Domestic Product (GDP) figures for the broader European Union (EU) came in slightly below expectations early Thursday, printing a meager 0.5%. Market forecasts expected the headline figure to match the previous period’s reported figure of 0.6%. The miss caused the Euro to sag briefly against the Pound Sterling, but a continued bump in German Bunds helped to bolster the EUR to a session high just beyond the 0.8600 handle before market sentiment dragged the EUR/GBP back towards the middle.

Upcoming on the economic data docket will be Germany’s Harmonized Index of Consumer Prices for August. The report is the Final version of the data point, with the Preliminary version released a week ago, so any wild deviations in the printing are not anticipated. The market forecast is for an annual rate of 6.4%, in line with the preliminary reading.

EUR/GBP Levels to watch

On the technical side, the EUR/GBP has caught a bump to lift away from the week’s low of 0.8524, but the challenge for Euro bulls will be to overcome late August’s swing high near 0.8610. Continued selling pressure will put the EUR/GBP back into August’s lows near 0.8580, but near-term support is being provided by the recent inflection point around 0.8570.

EUR/GBP 1-hour chart

- NZD/USD remains trapped as Kiwi bulls seek upside momentum.

- Broader market remains very much a USD game.

- Upcoming Japan data could provide a bump for the Antipodeans if numbers deviate.

The NZD/USD finds itself range-bound as the week continues, trapped between yesterday’s high and low as the US Dollar (USD) refuses to give up ground against most of its major competitors. US Initial Jobless Claims came in better than expected, providing support for the Greenback, and a notable lack of recovery momentum leaves the Antipodeans in a slump after the USD’s bumper start to the week.

US Initial Jobless claims printed at 216K, below the previous period’s 229K, reversing the market’s forecasted increase to 234K. Several speaking notes are expected from members of the Federal Reserve (Fed) over the remainder of the day, and traders will want to keep an eye out for any fresh comments about monetary policy that could shift USD sentiment.

Things are notably light on the Kiwi (NZD) side. During the Asian session, traders will want to keep an eye on upcoming Japanese data that could produce some volatility if the numbers have any surprises. Japan's quarterly Gross Domestic Production figures are expected to show a slight decline; market forecasts are calling for a printing of 1.3%, down from the previous reading of 1.5%.

NZD/USD: 0.5900 is the new resistance

Looking out over the longer-term horizon, the Kiwi is tapping into the lowest prices for the year, touching ten-month lows near 0.5880. Continued selling pressure will see the NZD/USD pair at risk of free-falling to 2022’s lows near 0.5560, and the upside looks resistance-heavy as the NZD has clocked losses against the Greenback for six of the past seven trading weeks.

With the Kiwi’s recent slump to the downside of the sideways channel from the last three weeks, there’s a risk the previous support from 0.5900 could now act as a near-term resistance level.

NZD/USD 4-hour chart

- USD/MXN drops 0.30% to 17.5300 as Mexico’s inflation falls to 4.64%, meeting market expectations and signaling a cooling economy.

- US jobless claims below forecasts at 216K, but the Mexican Peso gains ground, challenging the Fed’s neutral stance on rate hikes.

- USD/MXN faces strong resistance at 18.0000, with potential triggers for volatility, including Fed surprises and Mexico’s 2024 general election.

The Mexican Peso (MXN) recovered some ground against the US Dollar (USD) on Thursday, although Mexico’s economy deflates while the US jobs market remains tight. Hence, the USD/MXN is trading at 17.5300, a loss of 0.30%, after hitting a daily high of 17.7074.

Mexican Peso gains against the US Dollar despite a strong US labor market, as inflation in Mexico drops

The Instituto Nacional de Estadistica Geografia e Informatica (INEGI) revealed that inflation in Mexico dropped to its lowest level since March 2021, at 4.64%, as expected by market analysts. Core inflation, which excludes volatile items, slowed sharply to a 20-month low in August at 6.08%, below the foreseen 6.12%.

Jonathan Heath, a Deputy Governor of the Bank of Mexico (Banxico), said in social media X that core inflation was “good news” while adding, “There is still a long way to go.” Recently, some Banxico officials stressed the need to maintain higher rates as the central bank curbs inflation.

Across the border, the US Bureau of Labor Statistics (BLS) revealed that unemployment claims rose by 216K, beneath 229K forecasts on the week ending September 2, flashing a tight labor market. Even though the Greenback (USD) appreciated against most G8 currencies on the news release, the Mexican Peso outweighed the former, as the USD/MXN continued to trend downwards.

Fed officials have become more neutral, as data suggests prices are cooling down. But the resilience of the US jobs market puts the US central bank at a crossroads between doing too much and triggering a recession or perhaps under-tightening and suffering the consequences of an acceleration of inflation.

Meanwhile, the CME FedWatch Tool depicts money markets have fully priced in the Fed will keep rates unchanged in September. But for November, chances of a 25 bps increase lie at 43.5%.

Given the recent developments in both economies, the USD/MXN is set to print more gains, though it would face strong resistance at 18.0000. Any hawkish surprises by the Fed and next year’s Mexico general election could trigger outflows from the emerging market currency.

USD/MXN Price Analysis: Technical outlook

From a technical standpoint, the USD/MXN is neutral to upward biased. Still, today’s pause could spur some consolidation as bulls recharge batteries to challenge the 18.0000 psychological figure. Even though a pin-bar is forming, a daily close below September’s 6 low of 17.3912 could pave the way for a deeper correction. Otherwise, a break above 17.7074 and the pair could reach 18.0000.

- USD/JPY declined more than 0.30% towards 147.20.

- Initial Jobless Claims for the first week of September came in lower than expected.

- Masato Kanda didn’t rule out an intervention to stop JPY’s weakness.

On Thursday’s session, the USD/JPY slightly fell towards the 147.20 area, driven by the growing expectations of the Bank of Japan (BoJ) taking action to stop the JPY’s decline. On the other hand, the USD is consolidating, but hawkish bets on the Federal Reserve (Fed) limit the downside for the Greenback.

The US Bureau of Labour Statistics reported that the number of people filing for unemployment benefits increased but was lower than expected. The actual figure came in at 216,000 vs. the 234,000 expected and was lower than the previous weekly reading of 229,000.

Meanwhile, the USD measured by the DXY index holds above the 105.00 zone, its highest level since March. On the other hand, US Treasury yields slightly retreated but remained in weekly highs after yesterday’s rally following the strong ISM PMI figures from the US from August. In that sense, the CME FedWatch tool suggests that markets still bet on higher odds of one last hike by the Federal Reserve (Fed) in this cycle, and the odds of a 25 basis point in November and December stan near 40%.

However, those expectations may change after next week’s Consumer Price Index (CPI) figures from the US from August.

On the Bank of Japan's (BoJ) front, Reuter reported that Japan's top currency diplomat, Masato Kanda, stated that the Japanese banking authorities are considering an intervention to end “speculative” movements. In that sense, in case the BoJ steps in, the JPY may see some upside, but monetary policy divergences seem to be the main reason for Yen’s weakness. Furthermore, on Friday, investors will see Japan's Gross Domestic Product (GDP) Q2 revision figures.

USD/JPY Levels to watch

Observing the daily chart, the USD/JPY displays signs of bullish exhaustion, leading to a neutral to bearish technical perspective. The Relative Strength Index (RSI) displays a negative slope in the bullish territory, hinting at a potential shift in momentum, while the Moving Average Convergence (MACD) exhibits shorter green bars. In the broader context, the pair is above the 20,100,200-day Simple Moving Average (SMA), highlighting the continued dominance of bulls on the broader scale.

Support levels: 147.00, 146.50, 146.10 (20-day SMA).

Resistance levels: 147.50, 148.00, 148.50.

USD/JPY Daily Chart

-638296986911906841.png)

- USD/CAD rises 0.35% to 1.3675 after US jobless claims fall below estimates, pressuring the Fed to focus on its 2% inflation target.

- Market anticipates a 43.5% chance of a 25 bps Fed rate hike in November, as per CME FedWatch Tool, bolstering the US Dollar.

- Loonie stumbles as crude oil prices dip and Canadian GDP contracts, diminishing prospects of a Bank of Canada rate hike.

The US Dollar (USD) extends its advance against the Loonie (CAD) as data from both countries, although it remains positive, favors the Greenback. Powell’s saying “higher for longer” in his speeches continues to impact the markets, which remain wary of further tightening, boosting the USD. The USD/CAD is trading at 1.3675 and gains 0.35% after hitting a daily low of 1.3631.

USD/CAD gains momentum amid favorable jobless claims and Fed rate hike speculation despite stable Canadian business activity.

The US Department of Labor showed that Initial Jobless Claims for the week ending September 2 rose by 216K, below estimates of 229K, indicating the jobs market is yet to loosen. This puts pressure on the US Federal Reserve (Fed), which focuses on bringing inflation towards its 2% goal.

Although Fed policymakers have begun to adopt a more cautious stance, the market’s reaction suggests the Fed could increase rates in the future. The CME FedWatch Tool depicts money markets have fully priced in the US central bank would keep rates unchanged in September. But for November, chances of a 25 bps increase lie at 43.5%.

The USD/CAD pair reacted to the upside on the data, even though US Treasury bond yields are unchanged. In the meantime, the US Dollar Index (DXY), a gauge of the buck’s value against a basket of peers, prints modest gains of 0.18

Another reason behind Loonie’s fall is crude oil prices are under pressure, down 0.31%, at $87.27, as the market awaits EIA inventories.

Recently, data from Canada showed that business activity expanded in August following a contraction of 48.6 in July. The Ivey PMI came at 53.5, indicating expansion, as shown by data on Thursday. Some subcomponents of the PMI showed an improvement, like employment and supplier deliveries. Although it paints an improved scenario, the latest Gross Domestic Product (GDP) report for the second quarter contracted -0.2%, denting the Bank of Canada (BoC) of a possible rate hike yesterday as the economy cools down.

What to watch?

The Canadian economic docket would feature employment data, while the US will release Wholesale Inventories and Fed speakers.

USD/CAD Price Analysis: Technical outlook

The pair resumed its uptrend, challenging a major resistance area at 1.3667, April’s 28 daily high. A daily close above the latter would expose the 1.3700 figure and then the March 24 high at 1.3804. Conversely, sellers could remain hopeful of lower prices if USD/CAD ends Thursday’s session below 1.3667. A breach of the latter would expose September’s 6 low of 1.3622 before diving towards September 4 low of 1.3586.

Analysts at Wells Fargo have moved up the commencement of interest rate cuts from the Federal Reserve from May 2024 to March. They look for the FOMC to cut rates by 225 basis points next year.

US economy has remained resilient, but growth outlook appears to be subpar

Last month, we anticipated that the FOMC would begin cutting rates in May 2024. We now look for the Committee to cut rates by 25 bps at its March 2024 meeting.

In total, we look for the FOMC to cut rates by 225 bps next year, a bit less than the 250 bps of easing we had projected last month. This would bring the fed funds target range down to 3.00%-3.25% by the end of 2024.

Increased prospects of a "soft landing," although still not our base-case view, have led us to modestly pare back our forecasted amount of policy easing.

We believe that the Fed's tightening cycle has come to an end. The probability of another rate hike at the Sept. 20 FOMC meeting appears to be low. We acknowledge the FOMC could raise rates again at its meeting on Nov. 1, but we anticipate that the Committee will remain on hold as inflation continues to ease and as the economy decelerates.

- Silver price plummets to $23 as the US labor market remains resilient.

- US Q2 Unit Labor Costs jumped to 2.2% vs. expectations and the former release of 1.6%.

- Silver price corrects vertically to near the 200-day EMA, which trades around $23.30.

Silver price (XAG/USD) corrected significantly to near $23.00 as United States labor market indicators outperformed expectations. The white metal faces selling pressure as the US Department of Labor reported that individuals claiming jobless benefits for the first time dropped to 216K for the week ending September 01 vs. expectations of 234K and the former release of 229K.

Meanwhile, Q2 Unit Labor Costs jumped to 2.2% vs. expectations and the former release of 1.6%. Decent wage growth would keep households’ disposable income higher and might eventually keep inflationary pressures stubborn.

The S&P500 opens on a negative note as the tight US labor market would allow the Federal Reserve (Fed) to keep doors open for further policy tightening. The Fed is widely expected to keep interest rates unchanged in September monetary policy. As per the CME Fedwatch Tool, traders see a 93% chance for interest rates to remain unchanged at 5.25%-5.50% in the September policy meeting.

The US Dollar Index (DXY) edges marginally lower from its five-month high of 105.10. However, the upside bias is still solid as the market mood is quite cautious. For further action, investors will focus on the Consumer Price Index (CPI) for August, which will be released next week.

Silver technical analysis

Silver price corrects vertically to near the 200-day Exponential Moving Average (EMA), which trades around $23.30. The white metal forms a Head and Shoulder chart pattern, which is a bearish reversal pattern. The neckline of the aforementioned formation is placed from June 22 low at $22.18.

The Relative Strength Index (RSI) (14) drops to near 40.00. A bearish impulse would be activated if it breaks below the same.

Silver daily chart

-638296915233165909.png)

- EUR/USD breaks below the key 1.0700 support.

- Next on the downside aligns the May low in the 1.0630 zone.

EUR/USD retreats further and breaches the key support at 1.0700 the figure on Thursday.

The underlying bearish sentiment remains unchanged and leaves the door open to extra pullbacks in the short-term horizon. Against that backdrop, the pair could now embark on a probable visit to the May low of 1.0635 (May 31) ahead of the March low of 1.0516 (March 15).

In the meantime, further losses remain in the pipeline while below the key 200-day SMA, today at 1.0821.

EUR/USD daily chart

- DXY advances further and trespasses 105.00.

- The continuation of the march now targets the YTD highs.

DXY finally manages to surpass the key 105.00 hurdle, up for the third consecutive session on Thursday.

The continuation of the multi-week rally is now expected to shift its attention to the 2023 high of 105.88 (March 8) prior to the round level at 106.00.

While above the key 200-day SMA, today at 103.02, the outlook for the index is expected to remain constructive.

DXY daily chart

Analysts at Danske Bank project a minor contraction in the European economy during the second half of 2023. They argue that the disinflationary process is underway, but not enough for the European Central Bank (ECB) to be confident in the timely return to the 2% target.

Bye-bye two speed economy. Hello contraction

The August PMIs painted a gloomy picture following the also weak July print. Service PMI dropped to a 30-month low of 48.3, entering contractionary territory, while the manufacturing sector continued to register declining activity. The releases conclude the end of the two-speed economy with the service sector paving the way for benign growth, while the manufacturing sector struggled.

The drag in European business activity mainly attributes to the downturn in Europe’s largest economy – Germany - where activity declined at a 3-year high pace. The worsening of euro area activity should be seen as a feature rather than a bug given the ECB’s tightening mode the last year.

The risk is that activity suddenly declines too fast. Going forward, we expect a small contraction in the euro area GDP in H2 2023, partly driven by the gloomy Chinese outlook, persisting monetary headwinds, and the recent service sector weakness signs.

The disinflationary process is underway, but not enough for the ECB to be confident to the timely return to the 2% target.

The worsened economic outlook and markets turning more dovish, we expect the ECB to deliver a 25bp hike at the September meeting, marking a peak in the deposit rate of 4.00%

- EUR/JPY halts a three-day positive streak and drops to 157.50.

- The vicinity of 160.00 continues to cap the upside so far.

EUR/JPY comes under some marked selling pressure and recedes to the area of weekly lows in the mid-157.00s.

In the meantime, the cross could move into a consolidative phase ahead of the potential resumption of the uptrend. That said, immediate hurdle emerges at the recent 2023 peak at 159.76 (August 30) prior to the key round level at 160.00. The surpass of the latter should not see any resistance level of note until the 2008 high at 169.96 (July 23).

So far, the longer term positive outlook for the cross appears favoured while above the 200-day SMA, today at 148.33.

EUR/JPY daily chart

The US Bureau of Labor Statistics reported that Unit Labor Cost (ULC) rose 2.2% during the second quarter, a revision from the previous estimate of 1.6%. ULC rose 3.3% during the first quarter (revised from 4.2%).

Nonfarm Productivity increased 3.5%, below the 3.8% of market consensus, and revised from the 3.7% of the preliminary estimate.

Key takeaways from the report:

Unit labor costs in the nonfarm business sector increased 2.2 percent in the second quarter of 2023, reflecting a 5.7-percent increase in hourly compensation and a 3.5-percent increase in productivity. Unit labor costs increased 2.5 percent over the last four quarters.

In the second quarter of 2023, nonfarm business sector productivity increased 3.5 percent--a 0.2-percentage point downward revision from the preliminary estimate of a 3.7-percent increase--reflecting a 0.5-percentage point downward revision to output and a 0.2-percentage point downward revision to hours worked.

In the first quarter of 2023, nonfarm business sector productivity and unit labor costs were not revised. Manufacturing sector productivity was revised down 0.2 percentage point to a decrease of 2.0 percent. As a result, unit labor costs were revised up 0.2 percentage point to an increase of 2.6 percent.

Market reaction

The US Dollar Index rose further above 105.00 after the release of US data that also included the weekly Jobless Claims report.

- Initial Jobless Claims in the US decreased by 13,000 in the week ending September 2.

- US Dollar Index climbed to fresh multi-month highs above 105.00 after the data.

There were 216,000 initial jobless claims in the week ending September 2, the weekly data published by the US Department of Labor (DOL) showed on Thursday. This print followed the previous week's print of 229,000 (revised from 228,000) and came better than the market expectation of 234,000.

Further details of the publication revealed that the advance seasonally adjusted insured unemployment rate edged lower to 1.1% from 1.2% and the 4-week moving average stood at 229,250, a decrease of 8,500 from the previous week's revised average.

"The advance number for seasonally adjusted insured unemployment during the week ending August 26 was 1,679,000, a decrease of 40,000 from the previous week's revised level," the publication further read.

Market reaction

The US Dollar Index continues to push higher after this data and was last seen trading at its highest level since early March at 105.12, rising 0.27% on a daily basis.

- USD/CHF stabilized above 0.8900 due to the strength of the US Dollar.

- European and Asian economies are struggling to sustain economic prospects due to stubborn inflation and higher interest rates.

- The Swiss economy remained stagnant in Q2 while investors anticipated a growth rate of 0.1%.

The USD/CHF pair shifted auction above the round-level resistance of 0.8900 on Thursday, inspired by strength in the US Dollar. The Swiss Franc asset is expected to extend upside as the US Dollar remains resilient due to the risk-off market mood.

S&P500 futures generated significant losses, carry forwarded sell-off propelled on Wednesday due to outperforming service sector. US ISM reported that Services PMI jumped significantly to 54.5 vs. expectations of 52.5 and July’s reading of 52.7. Also, the New Orders Index soared to 57.5 against the former reading of 55.0, which indicates an upbeat demand outlook.

The US Dollar Index (DXY) aims to climb above the crucial resistance of 105.00 as investors continue to pump money due to deepening global uncertainties. European and Asian economies are struggling to sustain economic prospects due to stubborn inflation and higher interest rates by their respective central banks.

Going forward, investors will focus on the April-June quarter Unit Labor Costs data. The economic data is seen unchanged at 1.6%. Stable wage growth would allow the Federal Reserve (Fed) to keep interest rates higher for a longer period. Currently, investors hope that the Fed is done with hiking interest rates due to cooling inflation and higher Unemployment Rate. Apart from the Q2 Unit Labor Costs, commentaries from various Fed policymakers are due, which will bring action to the US Dollar.

On the Swiss Franc front, the currency remained in action due to the release of the Swiss Gross Domestic Product (GDP) data for the April-June quarter. The Swiss economy remained stagnant in Q2 while investors anticipated a growth rate of 0.1%. In the January-March quarter, the Swiss economy grew by 0.3%.

UOB Group’s Senior Economist Julia Goh and Economist Loke Siew Ting assess the latest publication of inflation figures in the Philippines.

Key Takeaways

The Philippines’ headline inflation reverted higher to 5.3% y/y in Aug after easing for six straight months to 4.7% y/y in Jul. The reading defied our expectation of a slowdown to 4.6% and Bloomberg consensus of a steady rate at 4.7%. This outturn was particularly due to a sharp jump in prices of food and fuels following the transitory effects of two super typhoons (Egay and Falcon) striking the country last month. Costlier recreation, sports & culture related goods and secondary education services also contributed to the acceleration in Aug’s headline inflation.

New circumstances such as the event of super typhoons, a further acceleration in global oil price above USD90/bbl, and emerging staple food supply shocks have posed a material change in the near-term inflation trajectory. This is in addition to lingering concerns about additional transport fare hikes, higherthan-expected minimum wage adjustments in other regions, and possible knock-on effects of higher toll rates on prices of key agricultural goods on the local front. Hence, we revise our full-year inflation forecasts back to our initial projections made in Feb, at 6.0% for 2023 (from 5.3% previously, BSP est: 5.6%, 2022: 5.8%) and 3.5% for 2024 (from 2.5% previously, BSP est: 3.3%). This upward revision also pushes back our earlier expectation of inflation returning to BSP’s 2.0%-4.0% medium target range to 1Q24 from 4Q23.

- The US Dollar keeps pressing after upbeat ISM data on Wednesday.

- Surprise rate cuts out of Poland make the ECB, BoE weaker against Fed.

- The US Dollar Index breaks above 105 but takes a small step back on Thursday.

The US Dollar (USD) has another go on Wednesday as markets tremble and crack in every pillar. The bond market sees its yields surge again, with the US 10-year yield on a trajectory to break the monthly high at 4.36%.

Equites took a short nosedive move on Wednesday with the S&P 500 breaking below the 55-day Simple Moving Average (SMA). With the surprise 0.75% rate cut from the Polish Central Bank, analysts are further increasing the rate divergence trade where US rates will remain elevated for longer and Europe, the United Kingdom and Central European countries will have to cut quicker and more aggressively in order to avoid a crashing economy.

While the macroeconomic data points from Wednesday were key and pivotal, there is nothing really important to expect this Thursday. Possibly the Initial and Continuing Jobless Claims might be worth watching in case there is a sudden uptick. Instead, gear up for the afternoon with no less than five US Federal Reserve speakers that might move the needle on making an end to this Indian Summer rally in the US Dollar Index.

Daily digest: US Dollar faces Fed speech

- Around 12:30 GMT, the data calendar for the US kicks off with the Weekly Initial and Continuing Jobless Claims. Expectations are for the Initial claims to jump from 228,000 to 234,000. The Continuing segment is expected to decline from 1,725,000 to 1,715,000.

- At that same time, the Nonfarm Productivity number for Q2 will be published. Expectations are for a small increase from 3.7% to 3.8%. The Unit Labor Costs are not expected to rise any further and should remain steady at 1.6%.

- A chunky batch of US Federal Reserve speakers: Patrick Harkers from Philadelphia is to kick off the headlines at 14:00 GMT. Next Fed member Austan Gooldsbee from Chicago will speak at 15:45 GMT. At 19:30 GMT, John Williams from New York will speak together with Raphael Bostic from Atlanta. Michelle Bowman will deliver the last remarks from Fed members this Thursday around 20:55 GMT.

- Equities in Asia are taking over the negative mood in which the US closed on Wednesday: The Hang Seng Index has fallen over 1% near its closing bell on Thursday. Meanwhile, European equities are firmly in the red but containing losses.

- The CME Group FedWatch Tool shows that markets are pricing in a 93% chance that the Federal Reserve will keep interest rates unchanged at its meeting in September.

- The benchmark 10-year US Treasury bond yield trades at 4.29% and keeps heading higher after the US Treasury issued quite a lot of debt paper on Tuesday. The auctions flooded the markets with supply and saw yields ramping up.

US Dollar Index technical analysis: shifting reality

Taking a step back to the recent turn of events, it becomes clear that this week has already been a seismic shift from this year’s monetary policy for several big central banks. The clear shift in stance can be witnessed with the US Federal Reserve and the Bank Of Canada sticking to the higher for longer timeline concerning interest rates, while Poland and the European Central Bank are seeing EU data signaling distress. This only adds to more fuel in the rate divergence between the two big geographical blocks. Expect to see more gains in the US Dollar Index (DXY) in the fall once the ECB and other Central-European countries start to cut, while the Fed keeps rates steady throughout 2023.

All eyes stay on 105.00 after the DXY briefly broke the level on Wednesday. Only a few cents to go and the DXY will be at a new six-month high. The next levels are at 105.88, the high of March 2023, which would make a new yearly high. If the index reaches this last level, some resistance might kick in.

On the downside, the 104.30 figure is vital to keep the US Dollar Index sustained at these elevated levels. Some room lower, the 200-day Simple Moving Average (SMA) at 103.06 comes into play, which could bring substantially more weakness once the DXY starts trading below it. The double belt of support at 102.42, with both the 100-day and the 55-day SMA, are the last lines of defence before the US Dollar sees substantial and longer-term depreciation.

US Dollar FAQs

What is the US Dollar?

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022.

Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

How do the decisions of the Federal Reserve impact the US Dollar?

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

What is Quantitative Easing and how does it influence the US Dollar?

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

What is Quantitative Tightening and how does it influence the US Dollar?

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

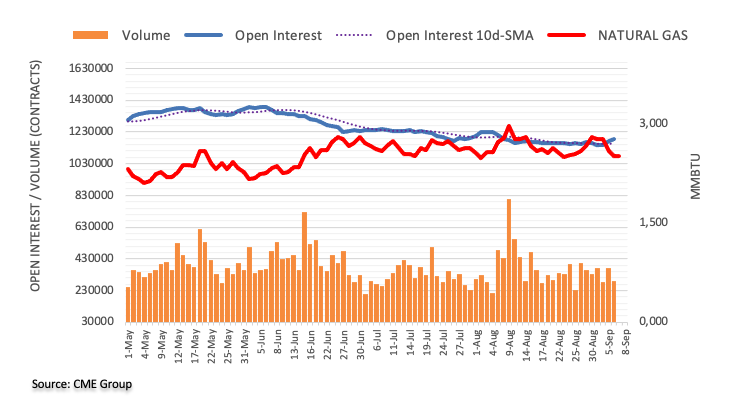

- Natural Gas is in the green on Thursday, putting an end to this week's decline.

- The US Dollar strengthens as a substantial monetary shift unfolds in Western and Central Europe.

- Natural gas price could extend upward momentum after support at $2.71 triggered a bounce.

Natural Gas price is trying to push up after its steady three-day decline this week, with benchmark futures rising 2.7% on Thursday. Traders are in the dark on what the current situation is in Australia at Chevron’s LNG facilities. Union representatives are holding discussions on whether to delay partial strike actions by another day later this Thursday. Any headline around that might turn into a headwind (or tailwind) and send Natural Gas futures substantially higher or lower.

Meanwhile, the US Dollar is gaining strength as it turns its summer rally into an extended one. A surprise 0.75% rate cut from the Polish central bank is a telling sign of the monetary policy divergence between the United States and the European bloc. Whereas recent economic US data confirmed good health, data out of the Eurozone and several Central European countries signals distress and an increased chance of a hard landing, forcing local central banks to start cutting interest rates quicker than expected. These moves depreciate local currencies against the Greenback.

At the time of writing, Natural Gas is trading at $2.746 per MMBtu.

Natural Gas news and market movers

- Another sharp drop in Russian gas flows to Europe keeps market supply very tight.

- The elevated level of gas storages in Europe remains a headwind for Natural Gas prices, head of gas and power at Trafigura Richard Holtum said during a Gastech conference in Singapore earlier this Thursday. Holtum said that both the European and global LNG markets have lost flexibility, which means prices are very receptive for sudden and violent price spikes in case of sudden hiccups or shortages caused by either unforeseen bigger demand or supply reductions.

- A Bloomberg analyst report mentioned that China will be jacking up its demand for LNG as it will ramp up its reserves for the winter. The report also mentioned that the country might take in more stockpiles, taking advantage of the current favorable prices in Gas futures and the better-than-expected growth projections.

- In the US, the weekly numbers from the Energy Information Administration (EIA) are due at 14:30 GMT for the Natural Gas Storage Changes. Expectations are for an increase from 32 billion cubic feet to 43 billion cubic feet. The range is for 33 as the lowest and 47 for the highest. Should the number be below 33, expect a firm squeeze higher in Natural Gas prices, where a jump above 47 will likely cause a severe downturn.

Natural Gas Technical Analysis: bounce needs to break higher

Natural Gas is erasing this week all the gains from the previous one. Some support is coming in in the form of the 55-day Simple Moving Average (SMA), which caught the break lower on Wednesday and has been triggering a bounce. In order to confirm the bounce, the high of Wednesday needs to be broken for this turnaround to be viable.

On the upside, $2.83 needs to be taken out in order for this bounce to gain momentum. Once this rebound materialises, look for the the 200-day Simple Moving Average (SMA) near $2.96. In case price starts to break above there and head higher, $3 will be crucial with the high of September at stake.

On the downside, the trend channel has done a massive job underpinning the price action. The 55-day SMA already provided support ahead of any test on the lower end of the trend channel. In case the 55-day SMA breaks, look for support near $2.65.

-638296774371945314.png)

XNG/USD (Daily Chart)

Natural Gas FAQs

What fundamental factors drive the price of Natural Gas?

Supply and demand dynamics are a key factor influencing Natural Gas prices, and are themselves influenced by global economic growth, industrial activity, population growth, production levels, and inventories. The weather impacts Natural Gas prices because more Gas is used during cold winters and hot summers for heating and cooling. Competition from other energy sources impacts prices as consumers may switch to cheaper sources. Geopolitical events are factors as exemplified by the war in Ukraine. Government policies relating to extraction, transportation, and environmental issues also impact prices.

What are the main macroeconomic releases that impact on Natural Gas Prices?

The main economic release influencing Natural Gas prices is the weekly inventory bulletin from the Energy Information Administration (EIA), a US government agency that produces US gas market data. The EIA Gas bulletin usually comes out on Thursday at 14:30 GMT, a day after the EIA publishes its weekly Oil bulletin. Economic data from large consumers of Natural Gas can impact supply and demand, the largest of which include China, Germany and Japan. Natural Gas is primarily priced and traded in US Dollars, thus economic releases impacting the US Dollar are also factors.

How does the US Dollar influence Natural Gas prices?

The US Dollar is the world’s reserve currency and most commodities, including Natural Gas are priced and traded on international markets in US Dollars. As such, the value of the US Dollar is a factor in the price of Natural Gas, because if the Dollar strengthens it means less Dollars are required to buy the same volume of Gas (the price falls), and vice versa if USD strengthens.

- AUD/USD defends the 0.6360 support as China opens for business with Australia.

- The market mood remains cautious as global economies have been exposed to economic turmoil.

- The resilient US service sector indicates a stable consumer spending momentum that might make inflation more stubborn.

The AUD/USD pair attempts recovery after defending the crucial support of 0.6360 after China’s Premier Li Qiang cited that the economy is willing to work with Australia to jointly safeguard peace, and stability in Asia-Pacific. Opening of the Chinese economy to Australia will provide it with a larger market to expand operations.

S&P500 futures demonstrate some losses generated in Europe, portraying a risk-off market mood. US equities were heavily sold on Wednesday after upbeat ISM Services PMI indicates that the Federal Reserve (Fed) is expected to keep interest rates higher for a very long period. In spite of US economic resilience, the Fed is widely expected to keep the monetary policy unchanged for the remaining year.

As per the CME Group’s FedWatch Tool, traders see a 93% chance for interest rates to remain unchanged at 5.25%-5.50% in the September policy meeting.

The US Dollar Index (DXY) trades inside Wednesday’s range but is expected to deliver more gains amid a dampened market mood. Investors are funding into the US Dollar to avoid risks of global economic turmoil. The US service sector which accounts for two-thirds of the economy turned out resilient, which indicates a stable consumer spending momentum that might make inflation more stubborn.

Meanwhile, investors await the April-June quarter Unit Labor Costs data, which will provide more clarity about wage growth. The economic data is seen unchanged at 1.6%. Apart from that, commentaries from Fed policymakers are also due.

The Australian Dollar remains in the spotlight this week as the Reserve Bank of Australia (RBA) keeps its Official Cash Rate (OCR) unchanged at 4.10%. Also, the Australian growth rate in Q2 remained better than expectations. The economy grew at a steady pace of 0.4%, a higher-than-expected growth rate of 0.3%. On an annualized basis, Q2 GDP dropped to 2.1% from the Q1 growth rate of 2.4% but remained higher than expectations of 1.7%.

Economist Lee Sue Ann at UOB Group reviews the latest GDP figures in Australia.

Key Takeaways

Australia’s GDP came in at 0.4% q/q in 2Q23, in line with expectations. This marked the seventh consecutive rise in quarterly GDP. From a year earlier, the economy expanded by 2.1% y/y, above expectations of 1.8% y/y.

The latest GDP print remains in line with our view of growth turning softer. We continue to expect growth to be well below trend at 1.6% in 2023 and 1.2% in 2024. As the economy slows, softening labour demand should see the unemployment rate rise back to 3.8% by end-2023 and around 4.5% by end2024.

Today’s GDP data comes a day after the Reserve Bank of Australia (RBA) held its cash rate target steady at 4.10% for the third consecutive time. Our view remains for the RBA to keep policy unchanged at the next meeting on 3 Oct.

- Gold price stabilizes near a six-day low as the appeal for the US Dollar strengthens.

- The US economy remains resilient while other nations are going through the consequences of restrictive monetary policy.

- Strong demand for the US service sector could allow the Fed to keep doors open for further policy tightening.

Gold price (XAU/USD) consolidates near a six-day low and remains exposed to more falls as investors keep funding the US Dollar due to an infirm global economy. The precious metal fails to capitalize on a widely anticipated unchanged interest rate decision by the Federal Reserve (Fed), which will be announced on September 20. Meanwhile, investors await Q2 US Unit Labor Costs data, which will be published at 12:30 GMT.

With economies like the UK and the Eurozone struggling due to tight monetary policy and high inflationary pressures and China facing deflation risks, the US economy remains resilient. The US economy is expected to avoid recession as inflation starts cooling due to the strict interest rate policy by the Fed, while job growth and consumer spending remain broadly stable.