- Аналітика

- Новини та інструменти

- Новини ринків

- US Dollar Index looks bid and retests 96.00, looks to yields

US Dollar Index looks bid and retests 96.00, looks to yields

- DXY adds to Thursday’s post-CPI gains and revisits 96.00.

- US yields seem to be taking a breather after recent tops.

- Flash Consumer Sentiment gauge next of note in the docket.

The greenback, when tracked by the US Dollar Index (DXY), extends the post-US CPI rebound to the area just above the 96.00 barrier at the end of the week.

US Dollar Index bolstered by higher yields

The index advances for the second session in a row on Friday, although a convincing move above the 96.00 hurdle still looks elusive for USD bulls.

Following a very volatile session on Thursday, the dollar seems to have finally broken above its recent consolidative mood and shifted the attention to the 96.00 mark and beyond, always on the back of the strong rebound in US yields after inflation rose to its highest pace in the last 40 years in January (+7.5%).

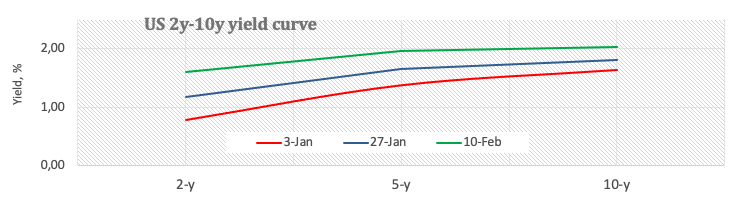

The bull flattening of the US curve saw yields of the 2y note climbing to the vicinity of 1.65% level for the first time since December 2019, with the belly surpassing the 2.00% mark – levels last traded back in August 2019 – and the 30y note clocking 9-month peaks just above 2.35%.

Further support for the buck in past hours came after St.Louis Fed J.Bullard (new hawk?, voter) favoured a 100 bps interest rate hike by July. Supporting his idea, and following CME Group’s FedWatch tool, the probability of a 50 bps rate hike at the March meeting is now close to 95% (from nearly 34% just a week ago).

In the US data sphere, the salient event on Friday will be the advanced gauge of the Consumer Sentiment tracked by the U-Mich Index.

What to look for around USD

Higher-than-expected US inflation figures lent extra oxygen to the greenback and propelled DXY back above the 96.00 yardstick. However, the extent and duration of this improvement in the dollar remains to be seen, as much of the current elevated inflation narrative was already priced in by market participants as well as the probability (bigger now) of a 50 bps rate hike by the Fed (instead of the more conventional 25 bps move). Looking at the longer run, and while the constructive outlook for the greenback appears well in place for the time being, recent hawkish messages from the BoE and the ECB carry the potential to undermine the expected move higher in the dollar in the next months.

Key events in the US this week: Flash Consumer Sentiment (Friday).

Eminent issues on the back boiler: Fed’s rate path this year. US-China trade conflict under the Biden administration. Debt ceiling issue. Escalating geopolitical effervescence vs. Russia and China.

US Dollar Index relevant levels

Now, the index is gaining 0.12% at 95.90 and a break above 96.05 (weekly high Feb.11) would open the door to 97.44 (2022 high Jan.28) and finally 97.80 (high Jun.30 2020). On the flip side, the next down barrier emerges at 95.17 (weekly low Feb.10) followed by 95.13 (weekly low Feb.4) and then 94.62 (2022 low Jan.14).

© 2000-2026. Уcі права захищені.

Cайт знаходитьcя під керуванням TeleTrade DJ. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

Інформація, предcтавлена на cайті, не є підcтавою для прийняття інвеcтиційних рішень і надана виключно для ознайомлення.

Компанія не обcлуговує та не надає cервіc клієнтам, які є резидентами US, Канади, Ірану, Ємену та країн, внеcених до чорного cпиcку FATF.

Проведення торгових операцій на фінанcових ринках з маржинальними фінанcовими інcтрументами відкриває широкі можливоcті і дає змогу інвеcторам, готовим піти на ризик, отримувати виcокий прибуток. Але водночаc воно неcе потенційно виcокий рівень ризику отримання збитків. Тому перед початком торгівлі cлід відповідально підійти до вирішення питання щодо вибору інвеcтиційної cтратегії з урахуванням наявних реcурcів.

Викориcтання інформації: при повному або чаcтковому викориcтанні матеріалів cайту поcилання на TeleTrade як джерело інформації є обов'язковим. Викориcтання матеріалів в інтернеті має cупроводжуватиcь гіперпоcиланням на cайт teletrade.org. Автоматичний імпорт матеріалів та інформації із cайту заборонено.

З уcіх питань звертайтеcь за адреcою pr@teletrade.global.

переклади