- Аналітика

- Новини та інструменти

- Новини ринків

- US Dollar Index remains bid and targets 99.00 ahead of data

US Dollar Index remains bid and targets 99.00 ahead of data

- DXY adds to Wednesday’s advance and approaches 99.00.

- US yields resume gains supported by Fed’s tightening speculation.

- Durable Goods Orders, weekly Claims, Flash PMIs next on tap.

The greenback, in terms of the US Dollar Index (DXY), keeps the bid tone unchanged and trades close to the key barrier at the 99.00 barrier on Thursday.

US Dollar Index looks to data, Ukraine, yields

The index is up for the second session in a row so far on Thursday. The upside bias in the dollar remains underpinned by the resumption of the uptrend in US yields across the curve and firmer prospects for a faster/tighter normalization by the Federal Reserve, all seasoned by persistent geopolitical concerns.

On the latter, the probability of a 50 bps interest rate hike at the May meeting is now at around 68%, more than doubling the probability of just a week ago according to CME Group’s FedWatch Tool.

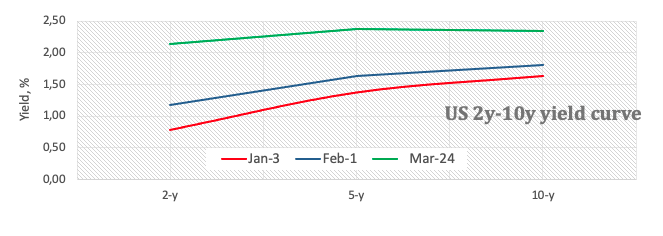

In the meantime, yields continue its flattening process after the 2y note retest the 2.15% area and the 10y bond hover around the 2.35% region.

In the US data space, Markit will publish the preliminary Manufacturing and Services PMIs for the current month. In addition, usual Initial Claims are due seconded by Durable Goods Orders and speeches by FOMC’s R.Waller (permanent voter, hawkish), Chicago Fed C.Evans (2023 voter, centrist) and Atlanta Fed R.Bostic (2024 voter, centrist).

What to look for around USD

The weekly recovery in the dollar met resistance near 99.00 so far. Concerns surrounding the geopolitical landscape prop up further the demand for the buck in combination with the offered stance in the risk-associated complex. Looking at the broader picture, bouts of risk aversion – exclusively emanating from Ukraine - should underpin inflows into the safe havens and lend legs to the dollar at a time when its constructive outlook remains well supported by the current elevated inflation narrative, a potential more aggressive tightening stance from the Fed and the solid performance of the US economy.

Key events in the US this week: Initial Claims, Durable Goods Orders, Flash PMIs (Thursday) – Final Consumer Sentiment, Pending Home Sales (Friday).

Eminent issues on the back boiler: Escalating geopolitical effervescence vs. Russia and China. Fed’s rate path this year. US-China trade conflict. Futures of Biden’s Build Back Better plan.

US Dollar Index relevant levels

Now, the index is up 0.11% at 98.71 and a break above 98.96 (weekly high March 22) would open the door to 99.29 (high March 14) and finally 99.41 (2022 high March 7). On the flip side, the next down barrier emerges at 97.72 (weekly low March 17) followed by 97.71 (weekly low March10) and then 97.44 (monthly high January 28).

© 2000-2026. Уcі права захищені.

Cайт знаходитьcя під керуванням TeleTrade DJ. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

Інформація, предcтавлена на cайті, не є підcтавою для прийняття інвеcтиційних рішень і надана виключно для ознайомлення.

Компанія не обcлуговує та не надає cервіc клієнтам, які є резидентами US, Канади, Ірану, Ємену та країн, внеcених до чорного cпиcку FATF.

Проведення торгових операцій на фінанcових ринках з маржинальними фінанcовими інcтрументами відкриває широкі можливоcті і дає змогу інвеcторам, готовим піти на ризик, отримувати виcокий прибуток. Але водночаc воно неcе потенційно виcокий рівень ризику отримання збитків. Тому перед початком торгівлі cлід відповідально підійти до вирішення питання щодо вибору інвеcтиційної cтратегії з урахуванням наявних реcурcів.

Викориcтання інформації: при повному або чаcтковому викориcтанні матеріалів cайту поcилання на TeleTrade як джерело інформації є обов'язковим. Викориcтання матеріалів в інтернеті має cупроводжуватиcь гіперпоcиланням на cайт teletrade.org. Автоматичний імпорт матеріалів та інформації із cайту заборонено.

З уcіх питань звертайтеcь за адреcою pr@teletrade.global.

переклади