- Аналітика

- Новини та інструменти

- Новини ринків

- USD Index extends the upside to new cycle highs near 114.80

USD Index extends the upside to new cycle highs near 114.80

- The index keeps the rally well in place near 115.00.

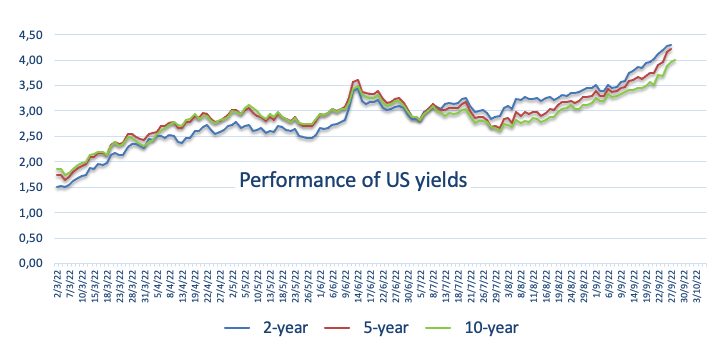

- US 10-year note yields surpass the 4.00% level.

- Trade Balance results, housing data, Powell next in the docket.

The rally in the greenback appears everything but abated and now pushes the USD Index (DXY) to fresh cycle highs in the 114.75/80 band.

USD Index in more than 20-year peaks

The index advances for the fourth consecutive session so far on Wednesday and navigates an area last traded back in mid-May 2002 near the 115.00 barrier.

The prevailing perception that the Federal Reserve is committed to hike rates until inflation pressures show compelling signs of losing traction continue to underpin the solid upside momentum around the buck.

Further legs for the dollar also come from the outstanding performance of US yields, where the 10-year note already surpasses the key 4.00% hurdle for the first time since mid-October 2008.

In the US data space, usual weekly MBA Mortgage Applications are due in the first turn seconded by advanced Goods Trade Balance results and Pending Home Sales.

In addition, Atlanta Fed R.Bostic (2024 voter, centrist), St. Louis Fed J.Bullard (voter, hawk), FOMC Governor M.Bowman (permanent voter, centrist) and Chicago Fed C.Evans (2023 voter, centrist) are all due to speak.

On top, Chair J.Powell will make Welcoming Remarks at the 2022 Community Banking Research Conference in St. Louis.

What to look for around USD

Bulls keep their pressure well and sound and lift the dollar to the highest level since May 2002 vs. its main competitors on Wednesday.

Propping up the dollar’s underlying positive stance appears the firmer conviction of the Federal Reserve to keep hiking rates until inflation looks well under control regardless of a likely slowdown in the economic activity and some loss of momentum in the labour market.

Looking at the more macro scenario, the greenback also appears bolstered by the Fed’s divergence vs. most of its G10 peers in combination with bouts of geopolitical effervescence and occasional re-emergence of risk aversion.

Key events in the US this week: MBA Mortgage Applications Advanced Trade Balance, Pending Home Sales, Fed Powell (Wednesday) – Final Q2 GDP Grow Rate, Initial Claims (Thursday) – PCE/Core PCE, Personal Income/Spending. Final Michigan Consumer Sentiment (Friday).

Eminent issues on the back boiler: Hard/soft/softish? landing of the US economy. Prospects for further rate hikes by the Federal Reserve vs. speculation over a recession in the next months. Geopolitical effervescence vs. Russia and China. US-China persistent trade conflict.

USD Index relevant levels

Now, the index is advancing 0.23% at 114.44 and a breakout of 114.76 (2022 high September 28) would expose 115.00 (round level) and then 115.32 (May 2002 high). On the downside, the next contention aligns at 108.36 (55-day SMA) seconded by 107.68 (monthly low September 13) and finally 107.58 (weekly low August 26).

© 2000-2026. Уcі права захищені.

Cайт знаходитьcя під керуванням TeleTrade DJ. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

Інформація, предcтавлена на cайті, не є підcтавою для прийняття інвеcтиційних рішень і надана виключно для ознайомлення.

Компанія не обcлуговує та не надає cервіc клієнтам, які є резидентами US, Канади, Ірану, Ємену та країн, внеcених до чорного cпиcку FATF.

Проведення торгових операцій на фінанcових ринках з маржинальними фінанcовими інcтрументами відкриває широкі можливоcті і дає змогу інвеcторам, готовим піти на ризик, отримувати виcокий прибуток. Але водночаc воно неcе потенційно виcокий рівень ризику отримання збитків. Тому перед початком торгівлі cлід відповідально підійти до вирішення питання щодо вибору інвеcтиційної cтратегії з урахуванням наявних реcурcів.

Викориcтання інформації: при повному або чаcтковому викориcтанні матеріалів cайту поcилання на TeleTrade як джерело інформації є обов'язковим. Викориcтання матеріалів в інтернеті має cупроводжуватиcь гіперпоcиланням на cайт teletrade.org. Автоматичний імпорт матеріалів та інформації із cайту заборонено.

З уcіх питань звертайтеcь за адреcою pr@teletrade.global.

переклади