- Аналітика

- Новини та інструменти

- Новини ринків

Новини ринків

(raw materials / closing price /% change)

Oil 41.62 -0.34%

Gold 1,243.10 -0.42%

(index / closing price / change items /% change)

Nikkei 225 16,381.22 +452.43 +2.84 %

Hang Seng 21,158.71 +654.27 +3.19 %

S&P/ASX 200 5,054.66 +79.01 +1.59 %

Shanghai Composite 3,066.64 +42.99 +1.42 %

FTSE 100 6,362.89 +120.50 +1.93 %

CAC 40 4,490.31 +144.40 +3.32 %

Xetra DAX 10,026.1 +264.63 +2.71 %

S&P 500 2,082.42 +20.70 +1.00 %

NASDAQ Composite 4,947.42 +75.33 +1.55 %

Dow Jones 17,908.28 +187.03 +1.06 %

(pare/closed(GMT +3)/change, %)

EUR/USD $1,1277 -0,93%

GBP/USD $1,4201 -0,42%

USD/CHF Chf0,9667 +1,19%

USD/JPY Y109,27 +0,60%

EUR/JPY Y123,23 -0,32%

GBP/JPY Y155,17 +0,19%

AUD/USD $0,7652 -0,37%

NZD/USD $0,6917 -0,01%

USD/CAD C$1,2817 +0,37%

(time / country / index / period / previous value / forecast)

01:30 Australia Unemployment rate March 5.8% 5.9%

01:30 Australia Changing the number of employed March 0.3 20.0

07:15 Switzerland Producer & Import Prices, m/m March -0.6% -0.2%

07:15 Switzerland Producer & Import Prices, y/y March -4.6%

09:00 Eurozone Harmonized CPI March 0.2% 1.2%

09:00 Eurozone Harmonized CPI, Y/Y (Finally) March -0.2% -0.1%

09:00 Eurozone Harmonized CPI ex EFAT, Y/Y (Finally) March 0.8% 1%

11:00 United Kingdom BoE Interest Rate Decision 0.5% 0.5%

11:00 United Kingdom Asset Purchase Facility 375 375

11:00 United Kingdom Bank of England Minutes

12:30 Canada New Housing Price Index, MoM February 0.1% 0.1%

12:30 U.S. Continuing Jobless Claims April 2191 2183

12:30 U.S. Initial Jobless Claims April 267 270

12:30 U.S. CPI, m/m March -0.2% 0.2%

12:30 U.S. CPI, Y/Y March 1.0% 1.1%

12:30 U.S. CPI excluding food and energy, m/m March 0.3% 0.2%

12:30 U.S. CPI excluding food and energy, Y/Y March 2.3% 2.3%

14:00 U.S. FOMC Member Jerome Powell Speaks

U.S. stocks extended gains a second day to reach the highest in four months, buoyed by improving Chinese trade data and better-than-expected results from JPMorgan Chase & Co., the biggest U.S. lender by assets.

JPMorgan advanced 4.2 percent after reporting first-quarter profit was boosted by pay cuts and trading revenue that declined less than most analysts predicted. Bank of America Corp., Wells Fargo & Co. and Citigroup Inc., scheduled to release results later this week, climbed at least 2.6 percent. Companies that are popular targets by short sellers rallied today, with a Goldman Sachs Group Inc. gauge of the 50 most shorted stocks posting the biggest increase since March 2.

The Standard & Poor's 500 Index rose 1 percent to 2,082.42 at 4 p.m. in New York, the highest since Dec. 4. Volume on U.S. exchanges was 8.1 percent higher than the 30-day average. All but five stocks in the 30-member Dow Jones Industrial Average increased, as the measure climbed 1.1 percent to 17,908.28 today. Futures contracts in pre-market trading held onto gains after releases showed U.S. retail sales and wholesale prices unexpectedly slumped last month, stoking speculation the Federal Reserve may slow the pace of further rate increases.

S&P 500 analysts have been projecting first-quarter profits by companies in the benchmark shrank 10 percent in the first quarter, with bank earnings contracting by 20 percent. That's fueled concern on the outlook for stocks, with valuations far above their five-year average and the seven-year bull market weeks away from becoming the second-longest in history.

A report showed China's exports jumped by the most in a year in March and declines in imports narrowed, helping ease worries about a slowdown in the world's second-largest economy. U.S. stocks are rebounding a second day, as crude pushed past $42 a barrel yesterday, lifting energy producers to their best one-day gain in almost two months.

Banks, the worst-performing group so far in 2016, led gains with all 17 stocks in the S&P 500 index rallying. Among lenders that advanced today were People's United Financial Inc. and Zions Bancorporation, which have short interest out of shares outstanding at 16 percent and 6 percent, respectively, data compiled by Markit Ltd. show.

Carmakers also advanced. Harley-Davidson Inc. added 4.3 percent after UBS AG said the company's retail sales in March likely jumped 10 percent because of warm weather. Bearish bets on the motorcycle maker is at 15 percent. Delphi Automotive Plc increased 5.6 percent after announcing a new buyback program and winning a long-running dispute with the U.S. Internal Revenue Service over whether the parts maker should be allowed to call itself British for tax purposes.

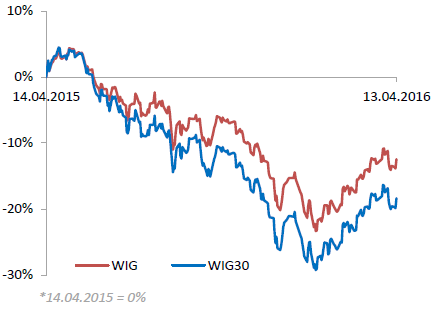

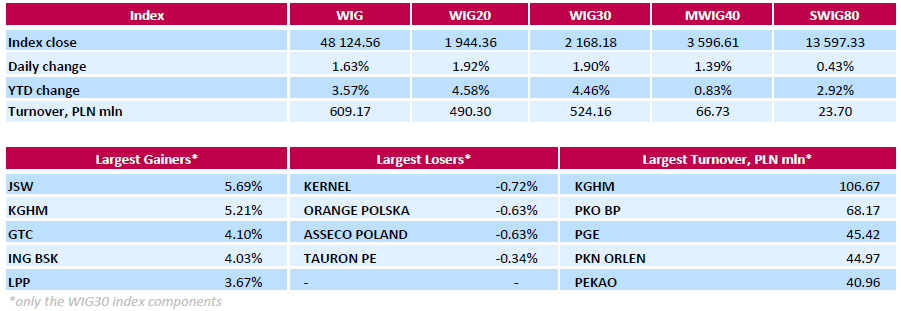

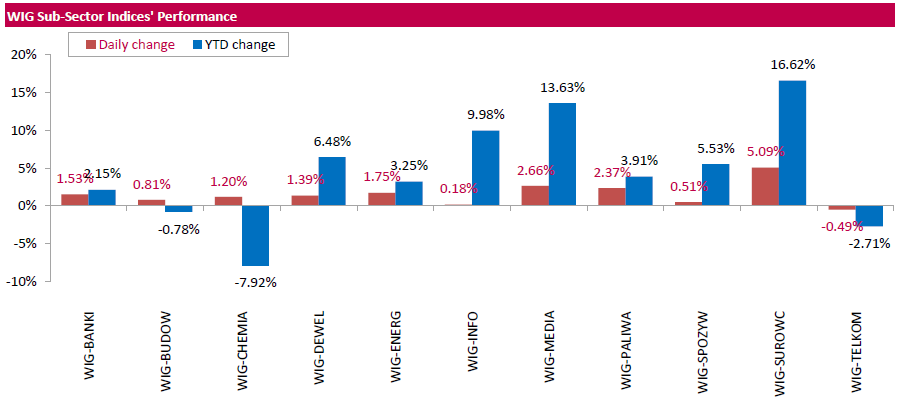

Polish equity market advanced on Wednesday. The broad market measure, the WIG Index, surged by 1.63%. Except for telecoms (-0.49%), every sector in the WIG Index gained, with materials (+5.09%) outperforming.

The large-cap stocks' measure, the WIG30 Index, advanced 1.90%. A majority of the index components returned gains, with the way up led by coking coal miner JSW (WSE: JSW) and copper producer KGHM (WSE: KGH), climbing by 5.69% and 5.21% respectively. They were followed by property developer GTC (WSE: GTC) and banking sector name ING BSK (WSE: ING), gaining 4.1% and 4.03% respectively. At the same time, the handful losers included agricultural producer KERNEL (WSE: KER), telecommunication services provider ORANGE POLSKA (WSE: OPL), IT-company ASSECO POLAND (WSE: ACP) and genco TAURON PE (WSE; TPE), declining by 0.34%-0.72%.

Major U.S. stock-indexes gained on Wednesday as JPMorgan's results kicked off bank earnings on an upbeat note and strong Chinese trade data raised hopes that the country's economy was on the mend. Shares of JPMorgan (JPM) were up 4,3% after the bank reported higher-than-expected quarterly earnings and revenue. Adding to the positive sentiment, data showed China's March exports handily beat expectations, rising for the first time in nine months. Global markets rallied following the data. However, U.S. retail sales and producer prices unexpectedly fell in March, more evidence that economic growth stumbled in the first quarter.

Most of Dow stocks in positive area (24 of 30). Top looser - Verizon Communications Inc. (VZ, -1,54%). Top gainer - JPMorgan Chase & Co. (JPM +4,54%).

Almost all of S&P sectors in positive area. Top looser - Utilities (-0,3%). Top gainer - Financial (+2,0%).

At the moment:

Dow 17786.00 +149.00 +0.84%

S&P 500 2071.50 +15.75 +0.77%

Nasdaq 100 4534.50 +44.50 +0.99%

Oil 42.21 +0.04 +0.09%

Gold 1247.30 -13.60 -1.08%

U.S. 10yr 1.78 +0.00

Stock indices closed higher on the Chinese trade data. The Chinese Customs Office released its trade data on Wednesday. China's trade surplus dropped to $29.86 billion in March from $32.59 billion in February, missing expectations for a decline to a surplus of $30.85 billion. Exports climbed at an annual rate of 11.5% in March, while imports slid at an annual rate of 13.8%, the sixteenth consecutive decline.

Market participants also eyed the economic data from the Eurozone. Eurostat released its industrial production data for the Eurozone on Wednesday. Industrial production in the Eurozone fell 0.8% in February, missing expectations for a 0.7% decrease, after a 1.9% rise in January. January's figure was revised down from a 2.1% increase.

Non-durable consumer goods output dropped 1.8% in February, capital goods output decreased 0.3%, while energy output fell 1.2%. Intermediate goods output were flat in February, while durable consumer goods declined 0.4%.

On a yearly basis, Eurozone's industrial production rise 0.8% in February, missing expectations for a 1.2% rise, after a 2.9% increase in January. January's figure was revised up from a 2.8% gain.

Durable consumer goods climbed by 0.8% in February from a year ago, capital goods rose by 3.0%, non-durable consumer goods gained by 0.7%, while intermediate goods output increased by 1.9%. Energy output declined by 5.2% in February from a year ago.

Indexes on the close:

Name Price Change Change %

FTSE 100 6,362.89 +120.50 +1.93 %

DAX 10,026.1 +264.63 +2.71 %

CAC 40 4,490.31 +144.40 +3.32 %

The Bank of England released its quarterly Credit Conditions Survey on Wednesday. Consumer credit continued to rise strongly in the three months to February, mainly driven by the increased provision of car finance.

According to the report, mortgage lending increased in the recent months.

Net lending to UK non-financial businesses was positive in the three months to February 2016, the central bank said.

Fed Chairwoman Janet Yellen said in an interview with Time Magazine that the Fed's cautious approach in hiking interest rate should help to avoid "the big mistakes". She noted that it was the appropriate approach as there was uncertainty.

"In such an environment, it makes sense to use a risk-management approach to identify and avoid the big mistakes. That's one reason I favour a cautious approach," Yellen said.

The Conference Board (CB) released its leading economic index for the U.K. on Wednesday. The leading economic index (LEI) increased 0.2% in February, after a 0.3% rise in January. January's figure was revised up from a 0.2% gain.

The coincident index was flat in February, after a 0.2% increase in January. January's figure was revised down from a 0.3% rise.

The Bank of Canada (BoC) released its interest rate decision on Wednesday. The central bank kept its interest rate unchanged at 0.50%, noting that the current monetary policy was appropriate. This decision was expected by analysts.

The BoC upgraded its growth forecast for to 1.7% from 1.4%. The economy is expected to expand 2.3% in 2017 and 2.0% in 2018.

The BoC noted that the Canadian economic growth in the first quarter was unexpectedly strong due to temporary factors, adding that it will reverse in the second quarter.

The central bank also said that the labour market continued to improve, household spending continued to expand moderately, while business investment was shrinking.

According to the central bank, inflation was evolving as anticipated by the BoC, and was expected to decline further.

Risks around the inflation are roughly balanced, the central bank said.

The BoC added that financial vulnerabilities continued to edge higher.

The U.S. Energy Information Administration (EIA) released its crude oil inventories data on Wednesday. U.S. crude inventories rose by 6.6 million barrels to 536.5 million in the week to April 08.

Analysts had expected U.S. crude oil inventories to rise by 2.85 million barrels.

Gasoline inventories decreased by 4.2 million barrels, according to the EIA.

Crude stocks at the Cushing, Oklahoma, declined by 1.77 million barrels.

U.S. crude oil imports climbed by 686,000 barrels per day.

Refineries in the U.S. were running at 89.2% of capacity, down from 91.4% the previous week.

The U.S. Commerce Department released the business inventories data on Wednesday. The U.S. business inventories decline 0.1% in February, in line with expectations, after a 0.1% decrease in January. January's figure was revised down from a 0.1% rise.

Retail inventories climbed 0.6% in February, wholesale inventories were down 0.5%, while manufacturing inventories decreased 0.4%.

Retail sales declined 0.2% in February, while business sales were down 0.4%.

The business inventories/sales ratio remained unchanged at 1.41 months in February. The business inventories /sales ratio is a measure of how long it would take to clear shelves.

USDJPY: 109.00 (USD 660m) 110.00 (217m)

EURUSD: 1.1250 (USD 201m) 1.1335-40 (365m) 1.1400 (502m) 1.1430 (263m) 1.1450 (261m) 1.1500 (252m)

GBPUSD: 1.4050-55 (GBP 362m)

EURGBP 0.8000 ( EUR 385m)

AUDUSD: 0.7450 (AUD 320m) 0.7500 (468m) 0.7700 (617m) 0.7900 (253m)

USDCAD 1.2915-20 (USD 510m) 1.3250 (411m)

NZDUSD 0.6750 (NZD 231m) 0.6900 (201m)

The Russian news agency Tass reported on Wednesday that Russia's Energy Minister Alexander Novak said an agreement on the freeze of the oil production could be reached without Iran. He noted that a deal was an open document, adding that everyone could join it.

Novak also said that around 17 countries would participate at the meeting in Doha on April 17.

U.S. Stocks opened into green: Dow +0.48%, Nasdaq +0.73%, S&P +0.52%

The second half of today's session will be influenced by readings of macroeconomic data from the US. Data on both retail sales and PPI suggest that the US economy is growing and is not heading towards a recession, but growth is quite modest. This leaves little room for expectation of interest rate increases, with implications for USD exchange rate.

This afternoon the Warsaw market is quite calm, although the + 1.7% increase in the main index should generate significant interest, but in practice, a large part of this deviation was absorbed by the high opening. For the past few hours the market is drifting horizontally with approximately 15-points of volatility. All of this is happening under the local resistance level of 1,940 points. Closing the session at this point would indicate resumption of growth at tomorrow's opening.

U.S. stock-index futures rose.

Global Stocks:

Nikkei 16,381.22 +452.43 +2.84%

Hang Seng 21,158.71 +654.27 +3.19%

Shanghai Composite 3,067.2 +43.55 +1.44%

FTSE 6,332.8 +90.41 +1.45%

CAC 4,453.04 +107.13 +2.47%

DAX 9,955.51 +194.04 +1.99%

Crude oil $41.55 (-1.47%)

Gold $1248.40 (-0.99%)

Saudi Arabia Oil Minister Ali al-Naimi said on Wednesday that the country would not lower its oil production.

Top oil producers will meet in Doha on April to discuss the freeze of the oil output at January levels. Iran will send only a government representative to this meeting.

The Bank of Japan (BoJ) released its Corporate Goods Price Index (CGPI) data on late Tuesday evening. Producer prices in Japan declined 0.1% in March, after a 0.2% fall in February.

Export prices rose 0.3% in March, while import prices increased 0.3%.

On a yearly basis, producer prices slid 3.8% in March, after a 3.4% drop in February. It was the biggest drop since October 2015

Export prices dropped 4.8% year-on-year in March, while import prices plunged 15.6%.

The U.S. Commerce Department released the retail sales data on Wednesday. The U.S. retail sales declined 0.3% in March, missing expectations for a 0.1% rise, after a 0.1% fall in February.

The decrease was mainly driven by a fall in sales at auto dealerships.

Sales at clothing retailers were down 0.9% in March, sales at building material and garden equipment stores increased 1.4%, while sales at auto dealerships slid 2.1%.

Retail sales excluding automobiles rose 0.2% in March, missing expectations for a 0.5% increase, after a 0.1% decline in February.

Sales at service stations climbed 0.9% in March, while sales at furniture stores rose 0.3%.

These figures indicates that the U.S. economic growth was weak in the first quarter.

(company / ticker / price / change ($/%) / volume)

| ALCOA INC. | AA | 9.57 | 0.09(0.9494%) | 126723 |

| ALTRIA GROUP INC. | MO | 63.99 | 0.17(0.2664%) | 600 |

| Amazon.com Inc., NASDAQ | AMZN | 606.68 | 3.51(0.5819%) | 25576 |

| AMERICAN INTERNATIONAL GROUP | AIG | 54.07 | 0.28(0.5205%) | 2602 |

| Apple Inc. | AAPL | 110.96 | 0.52(0.4708%) | 123919 |

| AT&T Inc | T | 38.8 | 0.13(0.3362%) | 3975 |

| Barrick Gold Corporation, NYSE | ABX | 15.87 | -0.48(-2.9358%) | 117513 |

| Boeing Co | BA | 130.25 | 0.78(0.6025%) | 1649 |

| Caterpillar Inc | CAT | 76.45 | 0.35(0.4599%) | 2069 |

| Chevron Corp | CVX | 97.4 | -0.11(-0.1128%) | 7646 |

| Cisco Systems Inc | CSCO | 27.78 | 0.14(0.5065%) | 6020 |

| Citigroup Inc., NYSE | C | 42.63 | 0.73(1.7422%) | 179828 |

| Exxon Mobil Corp | XOM | 84.17 | -0.18(-0.2134%) | 3298 |

| Facebook, Inc. | FB | 112.02 | 1.41(1.2747%) | 297734 |

| Ford Motor Co. | F | 12.89 | 0.08(0.6245%) | 17837 |

| Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 10.74 | 0.31(2.9722%) | 272765 |

| General Electric Co | GE | 30.94 | 0.13(0.4219%) | 40346 |

| General Motors Company, NYSE | GM | 29.98 | 0.27(0.9088%) | 22300 |

| Goldman Sachs | GS | 156.3 | 1.99(1.2896%) | 21421 |

| Google Inc. | GOOG | 747 | 3.91(0.5262%) | 4506 |

| Hewlett-Packard Co. | HPQ | 12.3 | 0.08(0.6547%) | 400 |

| Home Depot Inc | HD | 135.25 | 0.87(0.6474%) | 504 |

| Intel Corp | INTC | 32.05 | 0.19(0.5964%) | 8011 |

| JPMorgan Chase and Co | JPM | 60.6 | 1.32(2.2267%) | 664729 |

| McDonald's Corp | MCD | 127.69 | 0.08(0.0627%) | 100 |

| Microsoft Corp | MSFT | 54.97 | 0.32(0.5855%) | 10179 |

| Nike | NKE | 58.89 | 0.34(0.5807%) | 4511 |

| Pfizer Inc | PFE | 31.89 | -0.07(-0.219%) | 1001447 |

| Procter & Gamble Co | PG | 83.2 | 0.37(0.4467%) | 1320 |

| Starbucks Corporation, NASDAQ | SBUX | 59.82 | 0.32(0.5378%) | 5179 |

| Tesla Motors, Inc., NASDAQ | TSLA | 249.25 | 1.43(0.577%) | 22061 |

| The Coca-Cola Co | KO | 46.82 | 0.17(0.3644%) | 543 |

| Twitter, Inc., NYSE | TWTR | 16.69 | 0.12(0.7242%) | 55534 |

| Verizon Communications Inc | VZ | 52.09 | 0.14(0.2695%) | 5269 |

| Visa | V | 79.04 | 0.52(0.6623%) | 4829 |

| Wal-Mart Stores Inc | WMT | 69.1 | 0.30(0.436%) | 3788 |

| Walt Disney Co | DIS | 97.71 | 0.36(0.3698%) | 2840 |

| Yahoo! Inc., NASDAQ | YHOO | 37 | 0.34(0.9274%) | 29213 |

| Yandex N.V., NASDAQ | YNDX | 16.81 | 0.05(0.2983%) | 290 |

Upgrades:

Downgrades:

Other:

McDonald's (MCD) resumed with a Underperform at Credit Agricole

Starbucks (SBUX) resumed with a Buy at Credit Agricole

Yahoo! (YHOO) target raised to $44 from $40 at Sun Trust Rbsn Humphrey

The U.S. Commerce Department released the producer price index figures on Wednesday. The U.S. producer price index fell 0.1% in March, missing expectations for a 0.2% rise, after a 0.2% drop in February.

The decrease was mainly driven by a fall in services prices.

Energy prices increased 1.8% in March, wholesale food prices decreased 0.9%.

Services prices were down 0.2% in March, the first fall since October 2015, while prices for goods rose 0.2%.

On a yearly basis, the producer price index decreased 0.1% in March, missing expectations for a 0.3% increase, after a flat reading in February.

The producer price index excluding food and energy decreased 0.1% in March, missing expectations for a 0.1% gain, after a flat reading in February.

On a yearly basis, the producer price index excluding food and energy climbed 1.0% in March, missing forecasts of a 1.3% increase, after a 1.2% rise in February.

These figures could mean that the Fed will raise its interest rate cautiously and gradually.

Economic calendar (GMT0):

(Time/ Region/ Event/ Period/ Previous/ Forecast/ Actual)

00:30 Australia Westpac Consumer Confidence April -2.2% -4.0%

02:00 China Trade Balance, bln March 32.59 30.85 29.86

09:00 Eurozone Industrial production, (MoM) February 1.9% Revised From 2.1% -0.7% -0.8%

09:00 Eurozone Industrial Production (YoY) February 2.9% Revised From 2.8% 1.2% 0.8%

11:00 U.S. MBA Mortgage Applications April 2.7% 10%

The U.S. dollar traded mixed to higher against the most major currencies ahead of the release of the U.S. economic data. The U.S. retail sales are expected to rise 0.1% in March, after a 0.1% decline in February.

The U.S. PPI is expected to increase 0.2% in March, after a 0.2% drop in February.

The U.S. producer price inflation excluding food and energy is expected to rise 0.1% in March, after a flat reading in February.

The euro traded lower against the U.S. dollar after the release of the weaker-than-expected industrial production data from the Eurozone. Eurostat released its industrial production data for the Eurozone on Wednesday. Industrial production in the Eurozone fell 0.8% in February, missing expectations for a 0.7% decrease, after a 1.9% rise in January. January's figure was revised down from a 2.1% increase.

Non-durable consumer goods output dropped 1.8% in February, capital goods output decreased 0.3%, while energy output fell 1.2%. Intermediate goods output were flat in February, while durable consumer goods declined 0.4%.

On a yearly basis, Eurozone's industrial production rise 0.8% in February, missing expectations for a 1.2% rise, after a 2.9% increase in January. January's figure was revised up from a 2.8% gain.

Durable consumer goods climbed by 0.8% in February from a year ago, capital goods rose by 3.0%, non-durable consumer goods gained by 0.7%, while intermediate goods output increased by 1.9%. Energy output declined by 5.2% in February from a year ago.

The British pound traded mixed against the U.S. dollar in the absence of any major economic data from the U.K.

The Canadian dollar traded mixed against the U.S. dollar ahead of the Bank of Canada's interest rate decision. The central bank is expected to keep its interest rate unchanged.

EUR/USD: the currency pair declined to $1.1294

GBP/USD: the currency pair traded mixed

USD/JPY: the currency pair rose to Y109.38

The most important news that are expected (GMT0):

12:30 U.S. PPI, m/m March -0.2% 0.2%

12:30 U.S. PPI, y/y March 0% 0.3%

12:30 U.S. PPI excluding food and energy, m/m March 0.0% 0.1%

12:30 U.S. PPI excluding food and energy, Y/Y March 1.2% 1.3%

12:30 U.S. Retail sales March -0.1% 0.1%

12:30 U.S. Retail Sales YoY March 3.1%

12:30 U.S. Retail sales excluding auto March -0.1% 0.5%

14:00 Canada Bank of Canada Rate 0.5% 0.50%

14:00 Canada Bank of Canada Monetary Policy Report

14:00 Canada BOC Rate Statement

14:00 U.S. Business inventories February 0.1% -0.1%

14:30 U.S. Crude Oil Inventories April -4.937 2.85

15:15 Canada BOC Press Conference

18:00 U.S. Fed's Beige Book

22:30 New Zealand Business NZ PMI March 56.0

JPMorgan Chase reported Q1 FY 2016 earnings of $1.35 per share (versus $1.45 in Q1 FY 2015), beating analysts' consensus of $1.26.

The company's quarterly revenues amounted to $23.200 bln (-3.7% y/y), beating consensus estimate of $22.874 bln.

JPM rose to $60.85 (+2.65%) in pre-market trading.

EUR/USD

Offers 1.1360 1.1385 1.1400 1.1420 1.1450 1.1465-70 1.1480 1.1500-10 1.1530 1.1550

Bids 1.1335 1.1320 1.1300 1.1275-80 1.1250 1.1230 1.1200

GBP/USD

Offers 1.4250 1.4280 1.4300 1.4330 1.4350 1.4380 1.4400 1.4420 1.4450

Bids 1.4200 1.4185 1.4165 1.4150 1.4100 1.4080 1.4050-60 1.4030 1.4000

EUR/JPY

Offers 123.80 124.00 124.30 124.50 124.80 125.00

Bids 123.30 123.00 122.70 122.50 122.00

EUR/GBP

Offers 0.7980-85 0.8000 0.8020 0.8030 0.8050 0.8075-80 0.8100

Bids 0.7950 0.7925-30 0.7900 0.7880 0.7850 0.7830 0.7800

USD/JPY

Offers 109.00-10 109.30 109.50 109.80 110.00 110.20 110.50

Bids 108.70 105.50 108.30 108.00 107.85 107.60-65 107.50 107.30 107.00

AUD/USD

Offers 0.7680 0.7700 0.7720 0.7735-40 0.7750 0.7780 0.7800

Bids 0.7625-30 0.7600 0.7580 0.7550 0.7520 0.7500 0.7485 0.7465 0.7450

Listed fuel Group Lotos's SA (WSE: LTS) supervisory board dismissed the firm's long-standing CEO Pawel Olechnowicz and named Robert Pietryszyn as acting CEO.

Paweł Olechnowicz led Lotos since 2002. At that time company operated under the name of Gdansk Refinery. This makes the manager longest-serving president in the history of a listed company.

Olechnowicz's potential dismissal has been subject of media speculation in the recent months.

Lotos SA Group is the oil company, which is engaged in the exploration and production of crude oil, its processing, wholesale and retail sale of high-quality petroleum products. In 2015 Lotos Group SA recorded a PLN 22.7 Billion consolidated revenue.

The morning session phase ended with a respectable increase of the WIG20 (+1.4%), which appears to reflect the atmosphere of the environment, where the DAX is rising by more than 2%. The issue to watch out for in Warsaw is the turnover volume, which is only somewhat higher than PLN 190 mln on the WIG20. With such a low volume gives a legitimate reason to suspect that the index increase does not have a lot of strength. While smaller participants benefit from the occasion, bigger participants withdraw from bidding on this movement.

We also have to consider that this growth of the market is being built on credit confidence to Wall Street, the entrance to the game of the US markets can weaken the upward pressure of the core markets.

Stock indices traded higher on the Chinese trade data. The Chinese Customs Office released its trade data on Wednesday. China's trade surplus dropped to $29.86 billion in March from $32.59 billion in February, missing expectations for a decline to a surplus of $30.85 billion. Exports climbed at an annual rate of 11.5% in March, while imports slid at an annual rate of 13.8%, the sixteenth consecutive decline.

Market participants also eyed the economic data from the Eurozone. Eurostat released its industrial production data for the Eurozone on Wednesday. Industrial production in the Eurozone fell 0.8% in February, missing expectations for a 0.7% decrease, after a 1.9% rise in January. January's figure was revised down from a 2.1% increase.

Non-durable consumer goods output dropped 1.8% in February, capital goods output decreased 0.3%, while energy output fell 1.2%. Intermediate goods output were flat in February, while durable consumer goods declined 0.4%.

On a yearly basis, Eurozone's industrial production rise 0.8% in February, missing expectations for a 1.2% rise, after a 2.9% increase in January. January's figure was revised up from a 2.8% gain.

Durable consumer goods climbed by 0.8% in February from a year ago, capital goods rose by 3.0%, non-durable consumer goods gained by 0.7%, while intermediate goods output increased by 1.9%. Energy output declined by 5.2% in February from a year ago.

Current figures:

Name Price Change Change %

FTSE 100 6,334.24 +91.85 +1.47 %

DAX 9,979.35 +217.88 +2.23 %

CAC 40 4,452.56 +106.65 +2.45 %

Westpac Bank released its consumer confidence index for Australia on late Tuesday evening. The index fell 4.0% in April, after a 2.2% decline in March.

The index was driven by declines in four of the five sub-indexes.

"It appears that international and market developments continue to create unease for respondents although the signals are mixed," Westpac Chief Economist Bill Evans said.

"The Reserve Bank Board next meets on May 3. Despite this disappointing read on sentiment we expect the Board will keep rates on hold for another month. We retain our call that rates will remain on hold for the remainder of 2016," he added.

The Spanish statistical office INE released its final consumer price inflation data on Wednesday. Consumer price inflation in Spain was up 0.6% in March, in line with the preliminary reading, after a 0.4% decrease in February.

The monthly rise was mainly driven by an increase in clothing and footwear, which climbed 4.3% in March.

On a yearly basis, consumer prices fell by 0.8% in March from a year ago, in line with preliminary reading, after a 0.8% decline in February.

The annual decline was mainly driven by a drop in the prices of housing and transport.

The French statistical office Insee released its final consumer price inflation for France on Wednesday. The French consumer price inflation rose 0.7% in March, in line with the preliminary reading, after a 0.3% increase in February.

On a yearly basis, the consumer price index decreased 0.1% in March, up from the preliminary reading of -0.2%, after a 0.2% decline in February.

Fresh food prices rose 0.4% year-on-year in March, services prices climbed by 0.9%, while petroleum products prices dropped by 13.2%.

Eurostat released its industrial production data for the Eurozone on Wednesday. Industrial production in the Eurozone fell 0.8% in February, missing expectations for a 0.7% decrease, after a 1.9% rise in January. January's figure was revised down from a 2.1% increase.

Non-durable consumer goods output dropped 1.8% in February, capital goods output decreased 0.3%, while energy output fell 1.2%.

Intermediate goods output were flat in February, while durable consumer goods declined 0.4%.

On a yearly basis, Eurozone's industrial production rise 0.8% in February, missing expectations for a 1.2% rise, after a 2.9% increase in January. January's figure was revised up from a 2.8% gain.

Durable consumer goods climbed by 0.8% in February from a year ago, capital goods rose by 3.0%, non-durable consumer goods gained by 0.7%, while intermediate goods output increased by 1.9%.

Energy output declined by 5.2% in February from a year ago.

San Francisco Fed President John Williams said on Tuesday that two or three interest rate hikes this year would be appropriate. He pointed out that it did not matter when to raise the interest rate.

"We stay on this kind of basic path of raising interest rates gradually over the next couple of years, that's kind of what's important for financial conditions," Williams added.

He noted that the Fed's interest rate hikes would not lead to a lot of turmoil in financial markets.

Williams is not a voting member of the Federal Open Market Committee (FOMC) this year.

Richmond Fed President Jeffrey Lacker said on Tuesday that the Fed should raise its interest rate as inflation in the U.S. picked up. He added that the Fed should hike its interest rate four times this year.

"My sense is that the less leisurely but still gradual pace of target rate increases that FOMC participants submitted at year-end is still more likely to be appropriate," Lacker said.

He noted that global risks to the U.S. subsided.

Lacker is not a voting member of the Federal Open Market Committee (FOMC) this year.

Rating agency Fitch Ratings affirmed the U.S.'s sovereign debt rating at 'AAA'. The outlook is 'stable'.

"The U.S.'s 'AAA' rating is underpinned by the sovereign's unparalleled financing flexibility as the issuer of the world's pre-eminent reserve currency and benchmark fixed-income asset and as home to the world's deepest and most liquid capital markets," the agency said.

Fitch expects general government debt to increase to over 107% of GDP over the next decade from 101% of GDP in 2016, while federal fiscal deficit is expected to rise 2.9% of GDP in 2016 from 2.5% of GDP in 2015 according to the Congressional Budget Office.

The agency downgraded its growth forecasts to 2.1% in 2016 and 2017.

Fitch expects two interest rate hikes in 2016 and three in 2017.

The Chinese Customs Office released its trade data on Wednesday. China's trade surplus dropped to $29.86 billion in March from $32.59 billion in February, missing expectations for a decline to a surplus of $30.85 billion.

Exports climbed at an annual rate of 11.5% in March, while imports slid at an annual rate of 13.8%, the sixteenth consecutive decline.

The U.S. Treasury Department released its federal budget data on Tuesday. The budget deficit was $108.0 billion in March, missing expectations for a deficit of $104.0 billion, after a deficit of $109.0 billion in February.

The budget deficit was driven by higher expenditure for military programs, Medicare and other categories.

In the six months of the fiscal year 2016, which ends at September this year, the budget deficit totalled $461.0 billion, up 5.0% from a year ago.

USD/JPY:109.00 (USD 660m) 110.00 (217m)

EUR/USD:1.1250 (USD 201m) 1.1335-40 (365m) 1.1400 (502m) 1.1430 (263m) 1.1450 (261m) 1.1500 (252m)

GBP/USD:1.4050-55 (GBP 362m)

EUR/GBP0.8000 ( EUR 385m)

AUD/USD:0.7450 (AUD 320m) 0.7500 (468m) 0.7700 (617m) 0.7900 (253m)

USD/CAD 1.2915-20 (USD 510m) 1.3250 (411m)

NZD/USD 0.6750 (NZD 231m) 0.6900 (201m)

WIG20 index opened at 1918.51 points (+0.57% to previous close)

WIG 47698.46 +0.73%

WIG30 2146.69 +0.89%

mWIG40 3559.37 +0.34%

After the first few bars the growth of index reached 1% and this shift of the market requires certain decisions among the participants of the trade, what we can see in the turnover, which in comparison with the two previous sessions presents at last decent. The WIG20 starts virtually with complete of greens. The copper company KGHM (WSE: KGH) is a leader in the WIG20 index at the opening. Shares KGH becoming more expensive by nearly 3 percent with PLN 3 mln of turnover

Europe also begins sessions of strong increases. CAC grow by 1.5 percent, and the DAX by 1.4 percent.

EUR / USD

Resistance levels (open interest**, contracts)

$1.1517 (2734)

$1.1476 (1998)

$1.1435 (452)

Price at time of writing this review: $1.1362

Support levels (open interest**, contracts):

$1.1301 (2716)

$1.1241 (3476)

$1.1206 (2642)

Comments:

- Overall open interest on the CALL options with the expiration date May, 6 is 32112 contracts, with the maximum number of contracts with strike price $1,1600 (3400);

- Overall open interest on the PUT options with the expiration date May, 6 is 44663 contracts, with the maximum number of contracts with strike price $1,0900 (4816);

- The ratio of PUT/CALL was 1.39 versus 1.47 from the previous trading day according to data from April, 12

GBP/USD

Resistance levels (open interest**, contracts)

$1.4507 (2511)

$1.4410 (1714)

$1.4314 (1100)

Price at time of writing this review: $1.4235

Support levels (open interest**, contracts):

$1.4188 (748)

$1.4092 (1231)

$1.3994 (2067)

Comments:

- Overall open interest on the CALL options with the expiration date May, 6 is 23015 contracts, with the maximum number of contracts with strike price $1,4500 (2511);

- Overall open interest on the PUT options with the expiration date May, 6 is 28213 contracts, with the maximum number of contracts with strike price $1,3850 (3822);

- The ratio of PUT/CALL was 1.23 versus 1.21 from the previous trading day according to data from April, 12

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

Tuesday's trading on Wall Street was the first day on which the investors would move their attention from the macro data and the currency market on the condition of the companies. Border point was the quarterly report of the company Alcoa, whose results traditionally considered to be the beginning of the publication reports season. Aluminum producer posted figures that were better on the level of profit, but showed a drop in revenues. The company's shares have lost more than 2 percent yesterday.

On the other hand, the behavior of the market of raw materials, where the rise in oil prices and metal parts supported bulls, led to the situation that all US indices ended the day with increases.

Futures for US indices are traded now about 0.6 percent higher than during yesterday's finish in Europe and a similar rise can be expected at the openings of session eg. in Frankfurt. Additionally the Nikkei index rose by almost 3% due to the weakening of Yen.

In the following hours the attention of investors should be focus on Wall Street, where the results of JP Morgan will be announced today.

It must therefore be assumed that morning in Europe will adjust the valuation to yesterday's session on Wall Street and consolidate in anticipation of what will appear in the United States.

The safe-haven Japanese yen slid from recent peaks against the greenback on Wednesday as solid gains in oil prices helped underpin risk appetite. The yen has mostly brushed off recent comments by Japanese officials warning that a rapid appreciation by the currency was unwelcome.

The Canadian dollar hovered just under a nine-month peak, having rallied along with other commodity currencies such as the Australian dollar on higher oil prices. Also helping the currency, the Bank of Canada is widely expected to hold interest rates at 0.5 percent following its meeting on Wednesday. After a run of better-than-expected economic data at the start of the year, the central bank is also likely to raise its growth forecasts.

The Aussie extended gains as upbeat China trade data favoured risk appetite. Chinese exports in March rose a much stronger-than-expected 11.5 percent, the first increase since June and largest gain since February 2015.

EUR/USD: during the Asian session the pair fell to $1.1365

GBP/USD: during the Asian session the pair traded in the range of $1.4255-80

USD/JPY: during the Asian session the pair rose to Y108.95

Based on Reuters materials

© 2000-2026. Уcі права захищені.

Cайт знаходитьcя під керуванням TeleTrade DJ. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

Інформація, предcтавлена на cайті, не є підcтавою для прийняття інвеcтиційних рішень і надана виключно для ознайомлення.

Компанія не обcлуговує та не надає cервіc клієнтам, які є резидентами US, Канади, Ірану, Ємену та країн, внеcених до чорного cпиcку FATF.

Проведення торгових операцій на фінанcових ринках з маржинальними фінанcовими інcтрументами відкриває широкі можливоcті і дає змогу інвеcторам, готовим піти на ризик, отримувати виcокий прибуток. Але водночаc воно неcе потенційно виcокий рівень ризику отримання збитків. Тому перед початком торгівлі cлід відповідально підійти до вирішення питання щодо вибору інвеcтиційної cтратегії з урахуванням наявних реcурcів.

Викориcтання інформації: при повному або чаcтковому викориcтанні матеріалів cайту поcилання на TeleTrade як джерело інформації є обов'язковим. Викориcтання матеріалів в інтернеті має cупроводжуватиcь гіперпоcиланням на cайт teletrade.org. Автоматичний імпорт матеріалів та інформації із cайту заборонено.

З уcіх питань звертайтеcь за адреcою pr@teletrade.global.

переклади