- Analytics

- News and Tools

- Market News

- EUR/USD remains bid above 1.0600, albeit down from daily highs

EUR/USD remains bid above 1.0600, albeit down from daily highs

- EUR/USD gives away part of the initial bull run to 1.0670.

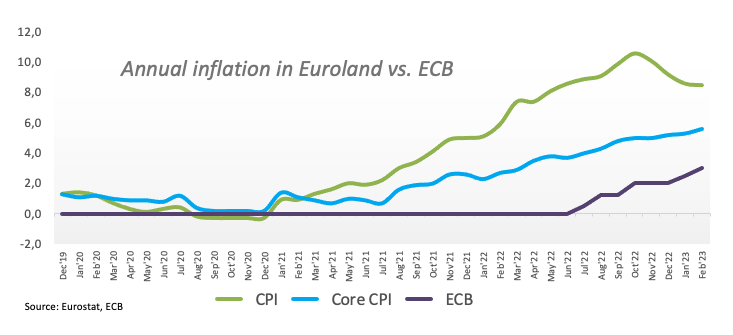

- EMU Final Inflation Rate rose 8.5% YoY in February.

- US advanced Consumer Sentiment worsens to 63.4 in March.

EUR/USD maintains the bid bias well in place around the 1.0640 region at the end of the week. Despite the bounce in the last couple of sessions, the pair’s weekly performance falls into the negative territory.

EUR/USD: Weekly upside appears capped around 1.0760

The recovery in the risk complex – mainly on the back of alleviated concerns surrounding the banking system on both sides of the ocean – keeps the buying pressure unchanged around EUR/USD, which adds to Thursday’s advance past 1.0600 the figure at the end of the week.

On the USD-side of the equation, the knee-jerk in the buck comes amidst the resumption of the downtrend in US and German yields, all following the 50 bps rate hike by the ECB on Thursday and conviction of a 25 bps rate raise at the Fed’s gathering on March 22.

Data wise in the euro area, final inflation figures showed the CPI rose 8.5% in the year to February and 5.6% when it came to the Core inflation.

In the US, Industrial Production came flat on a monthly basis in February and contracted 0.2% vs. the same month of 2022. In addition, Manufacturing Production expanded 0.1% MoM and contacted 1.0% over the last twelve months. Finally, the CB Leading Index dropped 0.3% MoM during last month and the advanced Michigan Consumer Sentiment is expected to have deflated to 63.4 in March.

What to look for around EUR

EUR/USD manages to leave behind some of the recent weakness and retakes the 1.0600 hurdle and above at the end of the week. The rebound seen so far in the second half of the week faltered near 1.0670.

In the meantime, price action around the European currency should continue to closely follow dollar dynamics, as well as the potential next moves from the ECB in a context still dominated by elevated inflation, although amidst dwindling recession risks.

Key events in the euro area this week: EMU Final Inflation Rate (Friday).

Eminent issues on the back boiler: Continuation of the ECB hiking cycle amidst dwindling bets for a recession in the region and still elevated inflation. Impact of the Russia-Ukraine war on the growth prospects and inflation outlook in the region. Risks of inflation becoming entrenched.

EUR/USD levels to watch

So far, the pair is advancing 0.20% at 1.0629 and the breakout of 1.0759 (monthly high March 15) would target 1.0804 (weekly high February 14) en route to 1.1032 (2023 high February 2). On the other hand, the next support emerges at 1.0516 (monthly low March 15) seconded by 1.0481 (2023 low January 6) and finally 1.0324 (200-day SMA).

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers