- Analytics

- News and Tools

- Market News

Analytics, News, and Forecasts for CFD Markets: currency news — 24-05-2011.

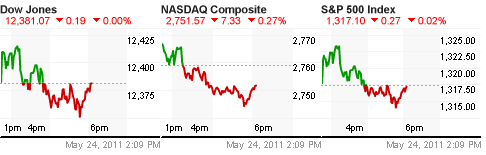

Stocks have made a slight upturn in recent trade. Both the Dow and the S&P 500 now face possible resistance at the flat line. The Nasdaq continues to lag its counterparts, though.

Ian Shepherdson of High Frequency Economics says "A 7.3% increase in sales sounds impressive, but it was nowhere near large enough to be statistically significant." He reminds that the Census Bureau says the margin of error is plus or minus 16.6% so "the trend in new home sales is still broadly flat, at an extraordinarily depressed level."

- non-standard exit depends on market conditions and Greek restructuring would be a disaster.

The euro rose versus the dollar for the first time in three days as German business confidence unexpectedly held near a record high, fueling bets the European Central Bank will resume boosting interest rates even as the region’s debt crisis intensifies.

The dollar remained lower versus most peers as purchases of new houses rose in April to the highest level this year. Sales increased 7.3% to a 323,000 annual pace last month, Commerce Department data showed today

“Ifo is a timely reminder that the most important economy in Europe is still motoring along,” said Richard Franulovich, a senior currency strategist at Westpac Banking Corp. in New York. “It’s probably enough to confirm the ECB’s own thinking that the core of Europe is still strong and they need to move away from some of that accommodative policy.”

“This can probably run to $1.42 to $1.4250 in the next 24 to 48 hours, and that wouldn’t alter the fundamental story that ultimately the euro is going to trade lower,” said Franulovich.

- Fed is 'keeping a close eye on sign of inflation';

- Without price stability the economy can't sustain maximum employment;

- Now is the 'opportune time' for an explicit 2% inflation target.

The major equity averages remain mired near the neutral line. The muddled action comes even though the dollar is trading with a 0.4% loss near its session low.

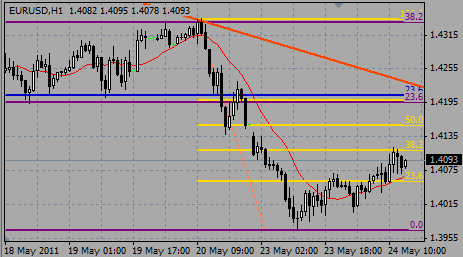

The rate gained higher around the London fixing event, extending the ride to $1.4130 area but with little fresh momentum. Area of $1.4145/50 seen to hold further offers but a few stops also cited in the $1.4130/40 zone, to make for some chop.

Commodities are trading higher except for a select few including natural gas (-0.3%), lean hogs (-0.6%).

Crude oil has been in positive territory all session. The energy component hit session highs of $99.97/barrel minutes ago and is now up 1.9% at $99.51/barrel.

Natural gas has been the laggard in the energy markets after it sold-off when pit trading began. During its morning sell-off, it fell into negative territory, dropped ~2% and hit new session lows of $4.35/MMBtu. In current activity, it's down 0.3% at $4.38/MMBtu.

Both gold and silver has been trading in positive territory all session and are showing a similar chart to crude oil. Gold hit new session highs of $1527.90/oz. about five minutes ago and is now up 0.7% at $1526.50/oz. Silver just hit new session highs as well and is now trading just under that level at $36.23/oz. up 3.8%.

Grain markets just opened and popped higher. Corn futures are 2 cents higher at $7.56/bu, wheat is still down 3 cents at $8.00, even after popping higher at the open, and soybeans are up 10 cents at $13.84/bu.

U.S. stocks were headed for modest gains Tuesday, looking to recoup losses after eurozone debt jitters sparked a global sell-off in the previous session.

Economy: Traders will be looking for government data on April new home sales, due shortly after the opening bell.

Economists expect the report to show new homes slugged along at prior month's levels, with 300,000 units being sold in April. The housing market remains weak, even though a few recent indicators have started to suggest a gradual recovery.

Companies: Shares of doughnut maker Krispy Kreme (KKD) continued to gain Tuesday, rising 2% in premarket trading. On Monday, Krispy Kreme shares surged more than 20%, after the company posted better-than-expected earnings.

Shares of entertainment products maker Sony (SNE) rebounded, ticking up more than 4% before the opening bell. Shares slipped nearly 4% in the previous session following disappointing quarterly results due to the earthquake and tsunami in Japan.

Commodities: Oil for July delivery gained $1.20, or more than 1%, to $98.90 a barrel.

Gold futures for June delivery rose $6 to $1,521.40 an ounce.

EUR/USD holds around $1.4088 when US hours open. The focus remain on Eurozone periphery with no major data for now. Offers eyed at $1.4120 area, just above the overnight high, bids back at $1.4060.

Data released:

06:00 Germany GDP (Q1) revised 1.5% 1.5% 1.5%

06:00 Germany GDP (Q1) revised Y/Y 4.9% 4.9% 4.9%

06:45 France Business confidence (May) 107 109 109 (110)

08:00 Germany IFO business climate index (May) 114.2 110.0 114.2 (110.4)

08:30 UK PSNCR (April), bln 3.3 2.0 24.8

08:30 UK PSNB (April), bln 7.7 5.0 16.4

09:00 EU(17) Industrial orders (April) -1.8% -1.0% 0.5 (0.9)%

09:00 EU(17) Industrial orders (April) Y/Y 14.1% 12.9% 21.5 (21.3)%

11:30 UK CBI retail sales volume balance (May) 18% 12% 21%

The euro rose against the dollar as German business confidence unexpectedly stayed near a record in May, fueling bets that the European Central Bank will resume raising interest rates even as the debt crisis intensifies.

The Ifo institute said its business climate index held at 114.2 from April after economists forecast a decline to 113.7.

Europe’s common currency has dropped about 6% from its 2011 high against the dollar on May 4, amid concern that Greece may have to restructure its debt.

A restructuring would be a “horror story” that the central bank cannot accept, ECB Governing Council member Christian Noyer told reporters today.

The euro pared gains against the yen as a report showed European industrial orders declined more than economists forecast in March. Orders in the euro area slipped 1.8% from February, when they increased 0.5%. Economists had forecast a drop of 1.1%.

The pound fell versus the euro after Moody’s Investors Service placed U.K. financial institutions on review for downgrades and Britain posted a larger budget deficit than predicted.

Lloyds Banking Group Plc (LLOY) and Royal Bank of Scotland Group Plc are among 14 U.K. lenders whose debt Moody’s is considering downgrading as withdrawal of government support may increase their credit risk. The outlook on Barclays Plc (BARC)’s senior debt and deposit ratings was changed to negative from stable, Moody’s said in a statement today.

Britain had net borrowing of 10 billion pounds ($16 billion) last month, the largest for any April since at least 1993, data showed today. The median of forecasts was for a shortfall of 6.5 billion pound.

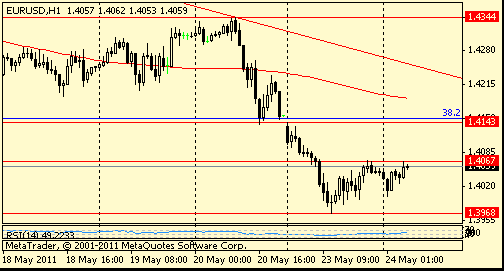

EUR/USD tested highs on $1.4115, but failed to hold above the figure and retreated to $1.4070. But decline was weak and there is a room for a second test of highs.

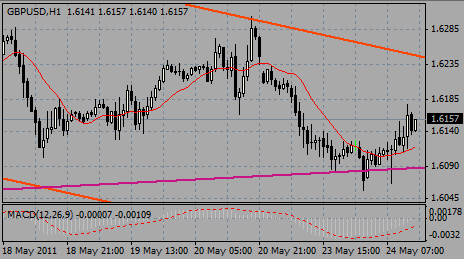

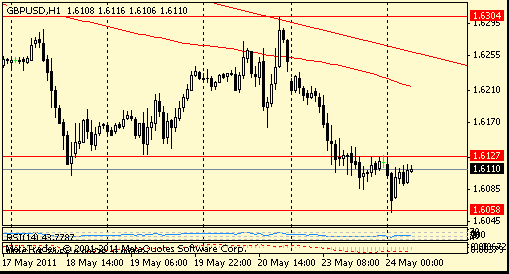

GBP/USD tested $1.6180 after the release of stronger than forecast CBI data, but the report fails to prompt any further rally and rate retreats. Back under $1.6140 to open a deeper move toward $1.6120/15 ahead of $1.6105/00.

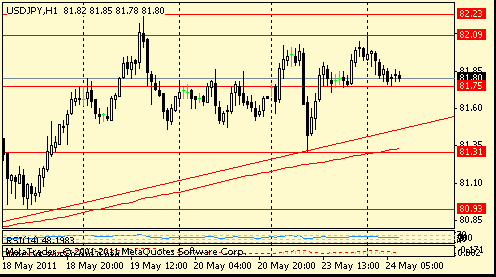

USD/JPY challenges Y82.00, correcting from Asian lows around Y81.60.

US data come at 1400GMT with report on New home sales.

GBP/USD tested $1.6180 after the release of stronger than forecast CBI data, but the report fails to prompt any further rally and rate retreats. Back under $1.6140 to open a deeper move toward $1.6120/15 ahead of $1.6105/00. Resistance remains toward earlier rally highs at $1.6180.

EUR/USD holds tight amid some fresh demand interest following Greek opposition leader rejection of austerity plan. However, plan can pass without their support and that caps the losses. Rate trades around $1.4090. Offers remain into $1.4120, more at $1.4145/50. Support $1.4055/50.

Goldman Sachs has changed its oil forecasts and now expect $130/bbl as 2012 average and $140/bbl year-end forecast for 2012. In addition, GS is also raising its Brent crude oil price forecast to $115/bbl, $120/bbl, and $130/bbl on a 3, 6, and 12 month horizon.

- Will do what needed to keep inflation low

- ECB must make sure not to overreact

- Will do what needed to keep inflation low

- ECB must make sure not to overreact

EUR/GBP extends recovery to stg0.8752, but sellers capped the rise further. A clear above stg0.8755 to open a move toward stg0.8780. Cross currently holds around stg0.8727.

The dollar held firm near a seven-week high against a basket of currencies and the euro remained on the defensive on Tuesday amid worries that the euro zone's debt crisis could spread to countries like Spain.

Standard & Poor's cut its outlook for Italy to "negative" from "stable" on Saturday, while a crushing defeat for Spain's ruling socialists in local elections raised worries about Prime Minister Jose Luiz Rodrigo Zapatero's ability to meet fiscal targets.

But euro buying from Asian central banks helped stem the euro's decline, with some traders saying that in the near-term there might be a small rebound for the single currency.

"The amount of the euro selling in the past few days has been huge. So I suspect a lot of euro long positions have been cleared. Some may be probably caught in short positions," said a trader at a U.S. bank. "I expect the euro to rebound in the near term, though I still think it's still in a downtrend in the longer run," he said.

The euro has also been suffering from a lack of consensus among European policy-makers on how to deal with Greece, as many opposed the idea of debt restructuring while some market players think it is inevitable.

As worries about the euro zone's debt problems spread, other European currencies also came under pressure. The pound slipped to an eight-week low before erasing gains.

The Swiss currency was hurt by comments from Swiss National Bank Vice Chairman Thomas Jordan that he is "very worried" about the rise in the franc and that the bank will take action if deflationary pressure emerges as a result of a higher franc.

But the New Zealand dollar gained after a quarterly survey on behalf of the Reserve Bank of New Zealand (RBNZ) showed inflation expectations in New Zealand rose in the second quarter.

July WTI crude extends through $99.00 to $99.13, largely driven by a firmer euro, weaker dollar and a Goldman Sachs forecast of higher Brent Crude prices.

EUR/USD lifts above $1.4100, despite reports of Asian sales. rate also rided on speculation we could see some positive statements coming out of Greece. Stops remain in place above $1.4110. Offers then at $1.4120, more at $1.4145/50.

EUR/JPY Y114.00, Y115.70, Y116.20, Y117.00

GBP/USD $1.6125

AUD/USD $1.0500, $1.0600

The euro weakened for a third day against the yen on speculation Europe’s sovereign-debt crisis is worsening and as the region’s industrial expansion slows.

Nikkei + 0.17% 9477.17

The European Central Bank will accept Greece’s government bonds as collateral in its refinancing operations as long as the country’s consolidation program stays on track, Ewald Nowotny, an ECB Governing Council member, told reporters today. Officials said last week it may not be able to take Greek sovereign debt as collateral if bond maturities are extended.

Australia’s dollar was among the worst performers against the greenback after a Chinese manufacturing gauge fell to a 10-month low amid concern the global economic recovery will falter.

The preliminary purchasing managers’ index for China compiled by HSBC Holdings Plc and Markit Economics fell to 51.1 in May. It was 51.8 in April.

China is the nation’s biggest trading partner.

at 121.0 and the expectations index slipping to a reading of 106.5 from 107.7. EMU industrial orders data is due at 0900GMT, although the data is for March and is expected to post a decline at -1.8% m/m.

England's Paul Fisher speaks at 1100GMT, while at 1130GMT, the CBI Distributive Trades data for May is expected to see the reported sales balance post a decline to 12 from a reading of 21.

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers