- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 06-09-2016

(raw materials / closing price /% change)

Oil$44.88+0.11%

Gold$1,354.00-0.07%

(index / closing price / change items /% change)

Nikkei 225 17,081.98 +44.35 +0.26%

Shanghai Composite 3,091.45 +19.35 +0.63%

S&P/ASX 200 5,413.63 -15.95 -0.29%CAC 40

CAC 4,529.96 -11.12 -0.24%

Xetra DAX 10,687.14 +14.92 +0.14%

FTSE 100 6,826.05 -53.37 -0.78%

S&P 500 2,186.48 +6.50 +0.30%

Dow Jones Industrial Average 18,538.12 +46.16 +0.25%

S&P/TSX Composite 14,813.02 +17.32 +0.12%

(pare/closed(GMT +3)/change, %)

EUR/USD $1,1248 +0,91%

GBP/USD $1,3423 +0,87%

USD/CHF Chf0,9699 -1,01%

USD/JPY Y102,09 -1,30%

EUR/JPY Y114,12 -1,02%

GBP/JPY Y137,02 -0,74%

AUD/USD $0,7681 +1,28%

NZD/USD $0,7410 +1,46%

USD/CAD C$1,2846 -0,61%

(time / country / index / period / previous value / forecast)

01:30 Australia Gross Domestic Product (QoQ) Quarter II 1.1% 0.4%

01:30 Australia Gross Domestic Product (YoY) Quarter II 3.1% 3.2%

05:00 Japan Leading Economic Index (Preliminary) July 99.2

05:00 Japan Coincident Index (Preliminary) July 111.1

06:00 Germany Industrial Production s.a. (MoM) July 0.8% 0.2%

06:45 France Trade Balance, bln July -3.4

07:00 United Kingdom Halifax house price index August -1%

07:00 United Kingdom Halifax house price index 3m Y/Y August 8.4%

08:30 United Kingdom Industrial Production (MoM) July 0.1% -0.2%

08:30 United Kingdom Industrial Production (YoY) July 1.6% 1.9%

08:30 United Kingdom Manufacturing Production (MoM) July -0.3% -0.4%

08:30 United Kingdom Manufacturing Production (YoY) July 0.9% 1.7%

14:00 United Kingdom NIESR GDP Estimate Quarter III 0.3%

14:00 Canada Ivey Purchasing Managers Index August 57

14:00 Canada Bank of Canada Rate 0.5% 0.5%

14:00 Canada BOC Rate Statement

14:00 U.S. JOLTs Job Openings July 5.624

18:00 U.S. Fed's Beige Book

23:50 Japan Current Account, bln July 974.4 2090

23:50 Japan GDP, q/q (Finally) Quarter II 0.5% 0%

23:50 Japan GDP, y/y (Finally) Quarter II 2% 0.0%

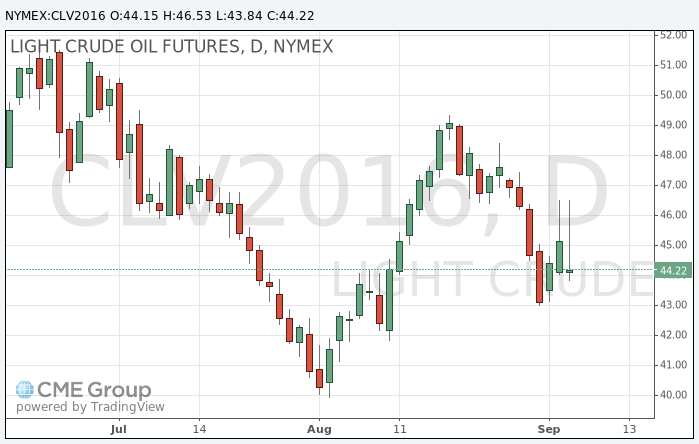

Brent traded in the red zone on skepticism about the likelihood of achieving an effective agreement between the producers, WTI adjusted upward as yesterday's trading on the New York Mercantile Exchange was on hault due to the holiday in the US.

Brent jumped monday more than 5% to $ 49.40 session after Saudi Arabia and Russia pledged to work together to support the market.

However, prices have lost gains during the session and closed well below session highs amid disappointment about the details of the agreement.

The two world's largest oil producer said to establish a working group to monitor the performance of the oil market for joint action to ensure the stability of the market.

Oil Minister of Saudi Arabia Khalid al-Falih and his Russian counterpart Alexander Novak will meet in Algeria in October and November to discuss co-operation in the framework of the new agreement.

OPEC members will discuss potential limitation of production in the course of an informal meeting on the sidelines of the International Energy Conference in Algiers on 26-28 September.

The cost of the October futures for US light crude oil WTI (Light Sweet Crude Oil) rose to 46.53 dollars per barrel on the New York Mercantile Exchange.

October futures price for North Sea petroleum mix of mark Brent fell to 46.29 dollars a barrel on the London Stock Exchange ICE Futures Europe.

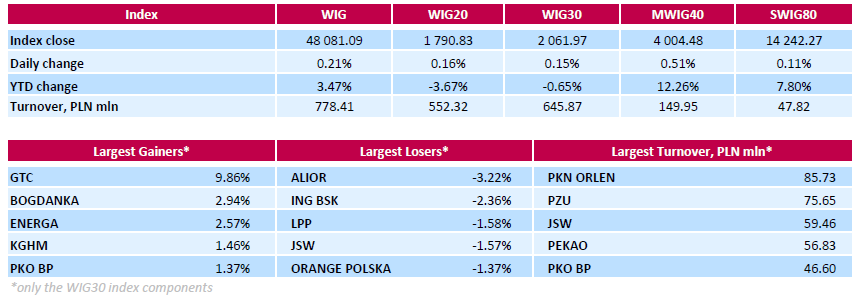

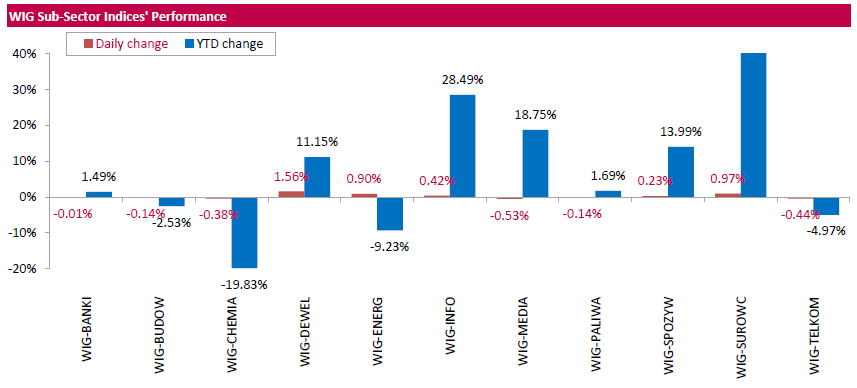

Polish equity market closed higher on Tuesday. The broad market measure, the WIG Index, rose by 0.21%. Sector performance within the WIG Index was mixed. Developing sector (+1.56%) outperformed, while media (-0.53%) lagged behind.

The large-cap stocks' measure, the WIG30 Index, added 0.15%. Within the index components, property developer GTC (WSE: GTC) led the gainers, jumping by 9.86%, supported by an analyst recommendation upgrade. It was followed by thermal coal miner BOGDANKA (WSE: LWB), genco ENERGA (WSE: ENG) and copper producer KGHM (WSE: KGHM), growing by 2.94%, 2.57% and 1.46% respectively. At the same time, the session's largest losers were two banking names ALIOR (WSE: ALR) and ING BSK (WSE: ING), which quotations fell by 3.22% and 2.36% respectively.

Major U.S. stock-indexes little changed on Tuesday as lower chances of an interest rate hike and a host of multi-billion dollar takeover deals boosted investor sentiment. Top Federal Reserve officials, encouraged by a string of strong economic data, had hinted that a rate hike could come as early as this month. However, Friday's disappointing employment numbers dampened those expectations.

Dow stocks mixed (17 in negative area, 13 in positive area). Top gainer - Verizon Communications Inc. (VZ, +1.57%). Top loser - General Electric Company (GE, -1.41%).

S&P sectors also mixed. Top gainer - Utilities (+0.5%). Top loser - Financial (-0.6%).

At the moment:

Dow 18470.00 -10.00 -0.05%

S&P 500 2177.50 -0.50 -0.02%

Nasdaq 100 4812.75 +17.50 +0.36%

Oil 44.30 -0.14 -0.32%

Gold 1344.40 +17.70 +1.33%

U.S. 10yr 1.56 -0.04

Gold prices rose as the dollar fell after weak data from the non-manufaturing sector, calculated by the Institute of Supply Management (ISM).

According to the data, the index fell in August to 51.4 after 55.5 in July, signaling a deterioration of the situation in a key sector of the US economy. Published on Friday,

After the most recent set o economic data the likelihood of a Fed hike this year declines. According to Fed funds futures, the probability of a hike in September is estimated at only 15% against 30% earlier.

"By itself, a possible increase in rates would not have a material adverse effect on the gold in September - said a senior analyst at Danske Bank. Really important for gold is whether the increase in rates this year signal that now the Fed is ready to speed up the cycle, because then again on the agenda will be the final normalization of interest rates. "

The market will be closely watching the release of new data from the US and any speeches by the Fed.

The cost of the October futures for gold on COMEX rose to $ 1342.9 per ounce.

-

Global DairyTrade prices: +7.7%.

-

Milk powder: +3.7%.

NZD/USD up around 50 pips so far.

The report was issued today by Anthony Nieves, CPSM, C.P.M., CFPM, chair of the Institute for Supply Management® (ISM®) Non-Manufacturing Business Survey Committee. "The NMI® registered 51.4 percent in August, 4.1 percentage points lower than the July reading of 55.5 percent. This represents continued growth in the non-manufacturing sector at a slower rate.

The Non-Manufacturing Business Activity Index decreased substantially to 51.8 percent, 7.5 percentage points lower than the July reading of 59.3 percent, reflecting growth for the 85th consecutive month, at a notably slower rate in August.

The New Orders Index registered 51.4 percent, 8.9 percentage points lower than the reading of 60.3 percent in July. The Employment Index decreased 0.7 percentage point in August to 50.7 percent from the July reading of 51.4 percent. The Prices Index decreased 0.1 percentage point from the July reading of 51.9 percent to 51.8 percent, indicating prices increased in August for the fifth consecutive month. According to the NMI®, 11 non-manufacturing industries reported growth in August. The majority of the respondents' comments indicate that there has been a slowing in the level of business for their respective companies."

The market in the US after an extended weekend opened with a slight increase. At the same time the volatility remains at low level, which is supported by a modest amount of information that may influence the prices. Only data from the services sector may slightly affect the behavior of investors.

The Warsaw market started growing after the beginning of trading on Wall Street and an hour before the end of trading the WIG20 index almost touched the level of 1,800 points (1,799 points + 0.63%).

EURUSD 1.0900, 1.0950, 1.0990 1.1000, 1.1050, 1.1095 1.1100/05, 1.1115 (1.75bn), 1.1120/25 (1.35bn), 1.1170 1.1240, 1.1250/55/60 (1.09bn), 1.1275 1.1300, 1.1315/20 (652m)

USDJPY 100.00/05 (1.45bn), 100.40/45/50 101.00 (570m), 101.25/30 102.00 (906m), 102.30 (500m), 102.55 103.00 (1.33bn), 103.30, 103.75 104.00 (925m), 104.20/25, 104.50/55 105.00

GBPUSD 1.3000, 1.3025 1.3300

AUDUSD 0.7395/400 (975m) 0.7520 0.7625/30/34 0.7700, 0.7745/50, 0.7790 0.7800

NZDUSD 0.7075/80 0.7350 (347m)

AUDNZD 1.1050

AUDJPY 81.65

EURGBP 0.8475 0.8675 (401m)

USDCAD 1.2600 1.2800 1.2900, 1.2975 (1.32bn) 1.3000/10 (645m), 1.3050 (569m), 1.3080 1.3220

USDCHF 1.0900

EURJPY 113.50 116.05

U.S. stock-index futures edged higher amid speculation the Federal Reserve will hold off raising interest rates this month.

Global Stocks:

Nikkei 17,081.98 +44.35 +0.26%

Hang Seng 23,787.68 +138.13 +0.58%

Shanghai 3,091.45 +19.35 +0.63%

FTSE 6,852.79 -26.63 -0.39%

CAC 4,548.51 +7.43 +0.16%

DAX 10,715.00 +42.78 +0.40%

Crude $44.17 (-0.61%)

Gold $1338.60 (+0.90%)

(company / ticker / price / change ($/%) / volume)

| ALCOA INC. | AA | 10.15 | 0.02(0.1974%) | 23350 |

| 3M Co | MMM | 181.09 | 0.28(0.1549%) | 177 |

| ALTRIA GROUP INC. | MO | 66.88 | -0.00(-0.00%) | 990 |

| Amazon.com Inc., NASDAQ | AMZN | 774.02 | 1.58(0.2045%) | 9228 |

| Apple Inc. | AAPL | 108.06 | 0.33(0.3063%) | 138047 |

| AT&T Inc | T | 41 | 0.05(0.1221%) | 3670 |

| Barrick Gold Corporation, NYSE | ABX | 18.63 | 0.47(2.5881%) | 107419 |

| Chevron Corp | CVX | 101.1 | 0.17(0.1684%) | 5373 |

| Cisco Systems Inc | CSCO | 31.82 | -0.01(-0.0314%) | 1878 |

| Citigroup Inc., NYSE | C | 47.53 | 0.02(0.0421%) | 600 |

| Deere & Company, NYSE | DE | 84.47 | 0.42(0.4997%) | 200 |

| Exxon Mobil Corp | XOM | 87.6 | 0.18(0.2059%) | 3039 |

| Facebook, Inc. | FB | 126.55 | 0.04(0.0316%) | 67414 |

| Ford Motor Co. | F | 12.49 | -0.01(-0.08%) | 1515 |

| Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 10.61 | 0.13(1.2405%) | 121244 |

| General Electric Co | GE | 31.34 | 0.05(0.1598%) | 21217 |

| General Motors Company, NYSE | GM | 32.2 | 0.04(0.1244%) | 4850 |

| Google Inc. | GOOG | 772.88 | 1.42(0.1841%) | 2512 |

| Home Depot Inc | HD | 135.17 | 0.02(0.0148%) | 303 |

| Intel Corp | INTC | 36.4 | 0.32(0.8869%) | 32395 |

| Johnson & Johnson | JNJ | 119.66 | 0.34(0.285%) | 583 |

| JPMorgan Chase and Co | JPM | 67.6 | 0.11(0.163%) | 1022 |

| McDonald's Corp | MCD | 116.63 | 0.80(0.6907%) | 9716 |

| Microsoft Corp | MSFT | 57.7 | 0.03(0.052%) | 3165 |

| Nike | NKE | 57.87 | -0.15(-0.2585%) | 495 |

| Pfizer Inc | PFE | 34.89 | 0.12(0.3451%) | 630 |

| Procter & Gamble Co | PG | 88.43 | 0.23(0.2608%) | 2496 |

| Starbucks Corporation, NASDAQ | SBUX | 56.46 | 0.28(0.4984%) | 609 |

| Tesla Motors, Inc., NASDAQ | TSLA | 199.31 | 1.53(0.7736%) | 21094 |

| Twitter, Inc., NYSE | TWTR | 19.75 | 0.20(1.023%) | 185075 |

| Verizon Communications Inc | VZ | 53.15 | 0.27(0.5106%) | 2383 |

| Wal-Mart Stores Inc | WMT | 72.56 | 0.06(0.0828%) | 3200 |

| Walt Disney Co | DIS | 94.7 | 0.28(0.2965%) | 1021 |

| Yahoo! Inc., NASDAQ | YHOO | 43.65 | 0.37(0.8549%) | 7476 |

| Yandex N.V., NASDAQ | YNDX | 22.74 | 0.35(1.5632%) | 656 |

Upgrades:

Intel (INTC) upgraded to Buy at Evercore ISI

Downgrades:

Other:

Apple (AAPL) reiterated at an Outperform at Cowen; target $117

The following data was published:

(Time / country / index / period / previous value / forecast)

5:45 Switzerland GDP q / q II quarter 0.3% 0.4% 0.6%

5:45 Switzerland GDP y / y in the II quarter 1.1% 0.9% 2.0%

6:00 Germany Factory Orders m / m in July -0.3% 0.5% 0.2%

7:15 Switzerland Consumer Price Index m / m in August -0.4% -0.1% -0.1%

7:15 Switzerland Consumer Price Index y / y in August -0.2% -0.1% -0.1%

9:00 Eurozone GDP q / q (final data) II quarter 0.5% 0.3% 0.3%

9:00 Eurozone GDP y / y (final data) II quarter 1.7% 1.6% 1.6%

The euro rose against the US dollar, heading to yesterday's high on overall bearish view of the US currency, statistical data on the GDP of the eurozone, as well as the expectations of the ECB meeting scheduled for Thursday.

The final data from Eurostat showed that the euro zone economy continued to expand in the 2nd quarter, helped by the increase in exports and strong internal demand. However, the growth rate slowed down in comparison with the 1st quarter. Gross domestic product increased by 0.3 percent in quarterly terms and by 1.6 per cent y/y, in line with previous estimates and forecasts of experts. In the 1st quarter the economy expanded by 0.5 percent and 1.7 percent respectively. The largest contribution to GDP growth was from net trade - added 0.4 percentage points to the final result. Demand on the part of the population has contributed 0.1 percentage points. Falling inventories took away 0.2 percentage points of GDP, slowing investment, in contrast to previous quarters. In quarterly terms, the economic growth slowed sharply in France - from 0.7 percent to zero and in Italy from 0.3 percent to zero. In Germany, the rate of expansion eased to 0.4 percent from 0.7 percent.

With regard to the ECB meeting, analysts expect the Central Bank to leave its monetary policy unchanged, but may hint at expanding bond purchase program. At the ECB meeting in July, the head of the Central Bank Draghi said that officials have shown that they can adjust the program of quantitative easing (QE) in the case of need, and there should be no doubt that they can extend the life of QE after March 2017.

The pound rose slightly against the dollar, helped by strengthening risk appetite in response to the rising cost of a number of commodities. In addition, support for the pound have the latest data on the UK, signaling a more favorable economic situation than had been expected after Brexit.

Investors also await the publication of new statistics from Britain - tomorrow industrial production and production in the manufacturing sector. Economists predict that both indicators have decreased slightly compared to June, but rose in annual terms. Also in Halifax will present its house price index, which was closely monitoring the market in the hope of receiving signals in regard to how the instability associated with Brexit affect the housing market. However, on Friday, investors will examine data on foreign trade in order to understand whether the weakening of the pound was able to support exports.

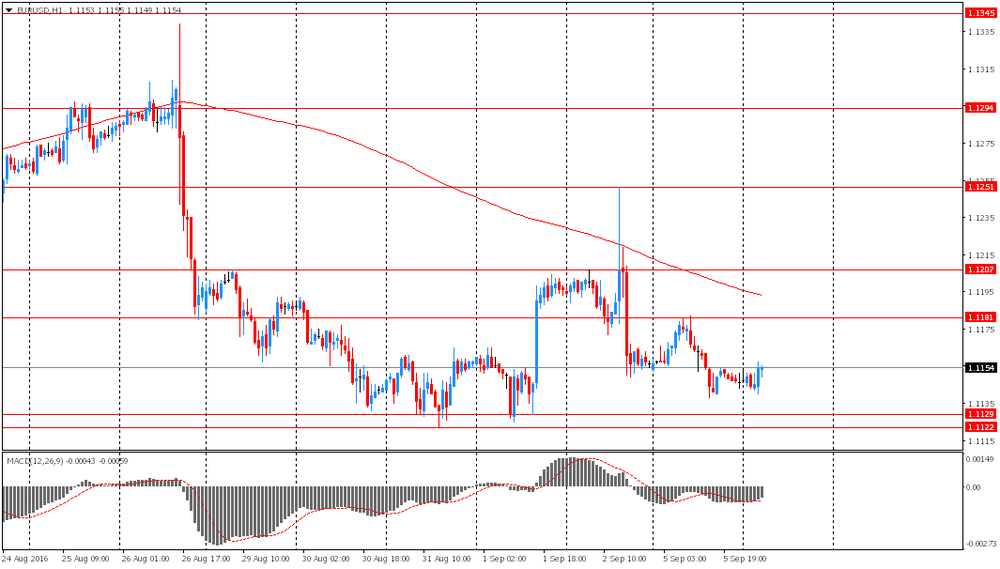

EUR / USD: during the European session, the pair rose to $ 1.1168

GBP / USD: during the European session, the pair has risen to $ 1.3360

USD / JPY: during the European session, the pair fell to Y103.15

EUR/USD

Offers 1.1185 1.1200 1.1225-30 1.1250 1.1280 1.1300 1.1320 1.1350-55

Bids 1.1120 1.1100 1.1080 1.1050 1.1030 1.1000

GBP/USD

Offers 1.3350 1.3370-75 1.3390-1.3400 1.3420 1.3450

Bids 1.3300 1.3275-80 1.3255-60 1.3230 1.3200 1.3175-80 1.3250 1.3120 1.3100

EUR/GBP

Offers 0.8400 0.8420 0.8445-50 0.8480 0.8500 0.8520-25 0.8535 0.8550

Bids 0.8350 0.8330 0.8300

EUR/JPY

Offers 115.65 115.85 116.00 116.20 116.50 117.00

Bids 115.00 114.80 114.50 114.00 113.80 113.50

USD/JPY

Offers 103.80 104.00 104.45-50 104.75 105.00 105.50

Bids 103.00 102.80 102.50 102.20 102.00 101.80 101.65 101.50

AUD/USD

Offers 0.7680 0.7700 0.7730 0.7750

Bids 0.7600 0.7580 0.7560 0.7520 0.7500 0.7485 0.7450 0.7430 0.7400

-

It's not always appropriate to put all cards on the table at the start of negotiations - spokesman

Today, Wall Street is back in the game, however past behavior of contracts for US indices does not indicate any breakthrough.

In the mid-session the WIG20 index was at the level of 1,784 points (-0.22%) and reached the turnover of PLN 187 million.

European stocks traded mostly in positive territory, near 8-month high, as investors awaited the outcome of ECB's meeting.

Analysts expect that the outcome of the September meeting will be a monetary policy unchanged, but the central bank may hint at expanding bond purchase program. At the last ECB meeting in July, the head of the Central Bank Draghi said officials have shown that they can adjust the program of quantitative easing (QE) in the case of need, and there should be no doubt that they can extend the life of QE after March 2017 .

Today's data show that in the second quarter euro-zone's GDP grew in line with expectations, while German manufacturing orders in July rose less than forecast.

Eurostat Statistical Office reported that the gross domestic product of the 19 countries of the eurozone increased by 0.3 percent in quarterly terms and by 1.6 percent over the previous year, in line with previous estimates and forecasts of experts. In the 1st quarter the economy expanded by 0.6 percent and 1.7 percent respectively. The largest contribution to GDP growth was from net trade - it has added 0.4 percentage points to the final result. Falling inventories took away 0.2 percentage points of GDP, slowing investment, in contrast to previous quarters. The data also showed that q/q growth of the economy slowed sharply in France - from 0.7 percent to zero and in Italy from 0.3 percent to zero. In Germany, the rate of expansion eased to 0.4 percent from 0.7 percent.

The composite index of the largest companies in the region Stoxx Europe 600 up 0.1 percent. The trading volume today is 34 percent less than the average over the past 30 days.

Volatility declined by 1.1 percent, reaching a month low.

Fresenius capitalization increased by 3.7 per cent after the pharmaceutical company said it will pay $ 6.42 billion for IDC Holding Salud, the largest network of private hospitals in Spain.

Ingenico Group SA shares fell 13 percent, as the manufacturer of payment terminals downgraded its forecasts for annual profit and revenue growth.

OCI NV cost decreased by 7 percent after the fertilizer producer reported a decline in revenues in the first half.

At the moment:

FTSE -20.77 6858.65 -0.30%

DAX +21.66 10693.88 + 0.20%

CAC 40 +2.06 4543.14 + 0.05%

-

Germany is doing well

-

Employment is at a record high, unemployment at a 25yr low

-

Germany must prove that integration can succeed

-

Will link spending to increases in GDP growth

-

More growth needed to end low rate policy

-

More structural reforms are needed globally

-

Debt must be cut globally

-

Central bank created liquidity is worrying

-

Investment boost should be driven by private sector

-

Junker fund should be expanded if needed

*via forexlive

"Despite the Fed having effectively told us that they will hike this year again, the USD has not been able to rally by much and market positioning is well below last year's levels.

The EUR cannot weaken by much, as the ECB has reached its self-imposed QE constraints and Draghi has to fight relaxing them one-by one. The JPY cannot weaken without a BoJ endorsement of fiscal stimulus in the absence of a long-term fiscal consolidation plan, in our opinion. GBP is actually strengthening, as the market was too short and the data has surprised to the upside. And EM FX still finds support from the Fed's policy put.

If the Fed does not hike ahead of the elections, December is the only real option, but lots of things can happen until then. A number of times this year the Fed thought that the road was clear for the next hike, but unexpected shocks kept it on hold.

We still expect the Fed to hike faster than markets are pricing (Dec this year and two more next year), which would support the USD, but do not expect a sharp USD move higher".

Copyright © 2016 BofAML, eFXnews™

GDP and main aggregates estimate for the second quarter of 2016 GDP up by 0.3% in the euro area and by 0.4% in the EU28 +1.6% and +1.8% respectively compared with the second quarter of 2015.

Seasonally adjusted GDP rose by 0.3% in the euro area (EA19) and by 0.4% in the EU28 during the second quarter of 2016, compared with the previous quarter, according to an estimate published by Eurostat, the statistical office of the European Union.

In the first quarter of 2016, GDP grew by 0.5% in both zones. Compared with the same quarter of the previous year, seasonally adjusted GDP rose by 1.6% in the euro area and by 1.8% in the EU28 in the second quarter of 2016, after +1.7% and +1.9% respectively in the previous quarter.

During the second quarter of 2016, GDP in the United States increased by 0.3% compared with the previous quarter (after +0.2% in the first quarter of 2016). Compared with the same quarter of the previous year, GDP grew by 1.2% (after +1.6% in the previous quarter).

This morning in New York WTI crude oil futures increased by 1.67% to $ 45.19 and Brent oil futures were at $ 47.62 per barrel. Thus, the black gold is gaining on the background of the agreement between Russia and Saudi Arabia on possible joint action to stabilize the market. At the same time, Iran continues to ramp up production to return to desired levels of exports. In October, Russia and Saudi Arabia will hold the first meeting in the in the field of oil and gas. Also, a ministerial meeting is scheduled in Algiers in November.

August saw a rise in eurozone retail sales, led by solid growth in Germany. Retailers in France also recorded an increase in sales, however their Italian counterparts recorded a fall for the eighth consecutive month.

Phil Smith, economist at IHS Markit which compiles the Eurozone Retail PMI survey, said: "Retail sector performances across the euro area remained divided in August, with sales growth in France accelerating to the highest seen for almost five years, but sales down notably again in Italy. Not forgetting Germany, the overall top performer and where sales have now risen for seven months on the bounce. Overall the data point to modest growth in consumer spending in the eurozone, which adds to the picture from the sister manufacturing and services surveys of a moderate pace of expansion in the broader economy."

EURUSD 1.0900, 1.0950, 1.0990, 1.1000, 1.1050, 1.1095, 1.1100/05, 1.1115 (1.75bn), 1.1120/25 (1.35bn), 1.1170, 1.1240, 1.1250/55/60 (1.09bn), 1.1275, 1.1300, 1.1315/20 (652m)

USDJPY 100.00/05 (1.45bn), 100.40/45/50, 101.00 (570m), 101.25/30, 102.00 (906m), 102.30 (500m), 102.55, 103.00 (1.33bn), 103.30, 103.75, 104.00 (925m), 104.20/25, 104.50/55, 105.00

GBPUSD 1.3000, 1.3025, 1.3300

AUDUSD 0.7395/400 (975m), 0.7520, 0.7625/30/34, 0.7700, 0.7745/50, 0.7790, 0.7800

NZDUSD 0.7075/80, 0.7350 (347m)

AUDNZD 1.1050

AUDJPY 81.65

EURGBP 0.8475, 0.8675 (401m)

USDCAD 1.2600, 1.2800, 1.2900, 1.2975 (1.32bn), 1.3000/10 (645m), 1.3050 (569m), 1.3080, 1.3220

USDCHF 1.0900

EURJPY 113.50, 116.05

According to rttnews, Romania's economic growth accelerated in the three months ended June as initially estimated, latest figures from the National Institute of Statistics showed Tuesday.

Gross domestic product advanced an unadjusted 6.0 percent year-over-year in the second quarter, confirming the flash data, faster than previous quarter's 4.3 percent expansion.

On the expenditure side, total final consumption grew 7.6 percent annually in the June quarter and gross fixed capital formation rose by 2.6 percent.

On a seasonally adjusted basis, the annual economic growth quickened to 5.9 percent from 4.2 percent in the first quarter.

Quarter-on-quarter, GDP expanded at a stable pace of 1.5 percent in the three-month period to June, in line with the flash data published on August 12.

WIG20 index opened at 1792.02 points (+0.22%)*

WIG 48140.10 0.33%

WIG30 2067.10 0.40%

mWIG40 3991.03 0.17%

*/ - change to previous close

The futures market (WSE: FW20U1620) started the day with a rise of 0.22% to 1,792 points. The same gained contract on the German DAX.

The cash market by its increase works out only slightly lower yesterday's closing and is close to the psychological resistance level at 1,800 points, which probably will cool a bit appetite to growth.

After higher opening noticeable is growing, stronger since yesterday, the energy sector. For the record, the inspiration was provided by information from the Treasury about change their mind on raising the nominal value of shares of PGE.

At 15:30 GMT the United States will hold an auction of 4, 3 and 6-month bills.

At 09:30 GMT Britain will place 10-year bonds.

At 16:15 GMT The head of the SNB, Thomas Jordan will deliver a speech.

"With a light data schedule for the US week ahead, we see potential for the GBP to rally the most among G10 currencies against the USD.

Firstly, the market is only beginning to acknowledge that the UK economic data may not come in as weakly as expected. Good data prints in services PMI, IP and house prices following other positive prints in manufacturing PMI and retail sales should continue to alleviate market concerns regarding the Brexit result and lead to an asymmetrically large rally in GBP crosses.

This leads directly to the second point - that market positioning is still extremely short and still has some way to unwind.

Finally, while the headline US payrolls number was not particularly weak, slow labor wage growth and a shortened work week should be sufficient (in combination with other weak data prints such as ISM and US political risks) to keep the Fed on hold and progressively price a Sep hike out of the picture over the week.

The main risks to the trade are if the upcoming data print unexpectedly worse, and if UK political developments signal a consensus forming around a "hard Brexit" policy cocktail,"

As a technical trade, CS booked profit today on its GBP/USD long from 1.3064 at 1.3355.

Copyright © 2016 Credit Suisse, eFXnews™

The Australian dollar traded higher after the Reserve Bank of Australia decided to maintain the cash rate unchanged at around 1.5%. It is worth noting that the decision coincided with forecasts of most economists. The Central Bank pointed out that the decision to keep rates unchanged meets the objectives in relation to GDP and inflation. "With regard to the labor market, indicators of employment remain somewhat ambiguous and point to the growth of this sector in the short term," - said the Reserve Bank of Australia. In addition, analysts say that low interest rates are supporting domestic demand in the country. The RBA also commented on the Australian dollar, saying that the strengthening of the national currency may complicate the transition and recovery in the economy. At the same time, a lower rate of the Australian dollar has supported the trade sector.

Previously, data on the balance of payments have been published. Australia's current account deficit amounted to $ 15.54 billion in Q2 vs A -$ 19,75 mlrd forecast. In the first quarter a deficit of A -$ 20.8 was recorded. It also became known that the net external debt of Australia in the second quarter increased by 2.0%. The contribution of net exports to GDP growth fell by 0.2 percentage points in the 2nd quarter

The pound rose slightly despite the publication of weak statistics on retail sales in the UK. According to the poll of the British Retail Consortium (BRC), retail sales in the UK declined in August after rising in July by 0.9% compared to the same period of the previous year. In July, this indicator increased by 1.1%. Total sales decreased by 0.3% vs +0.1% in August 2015.

EUR / USD: during the Asian session, the pair was trading in the $ 1.1140-55 range

GBP / USD: during the Asian session, the pair rose to $ 1.3325

USD / JPY: during the Asian session, the pair was trading in Y103.35-80 range

Yesterday lack of trading on Wall Street caused that this morning we do not refer to changes in these markets. While the behavior of the Asian parquets is tranquil and slightly upward. Contracts in the US are stable and this should also be morning in Europe.

During today's session, there is no important macro publications from the domestic market. On the broad market it is worth to pay attention, among others, to orders in German industry, the final lecture to GDP for the second quarter for the euro zone and the ISM for August in the US service sector, although traditionally it does not cause such reactions, as in case of the industrial sector. The only new event is the end of the two-day G20 summit in China. Although these meetings are virtually ignored by investors, because do not bring anything concrete.

On Tuesday morning, trading on the currency market brings a slight stabilization of the Polish currency. The Polish zloty is valued by the market as follows: PLN 4.3385 per euro, PLN 3.8912 against the US dollar. Yields on domestic debt amounts to 2,879% for 10-year bonds.

The current account deficit, seasonally adjusted, increased $636m (4%) to $15,535m in the June quarter 2016. The deficit on the balance on goods and services decreased $652m (8%) to $7,996m. The net primary income deficit increased $1,351m (23%) to $7,160m.

In seasonally adjusted chain volume terms, the surplus on goods and services decreased $999m (8%) from $11,796m in the March quarter 2016 to $10,797m in the June quarter 2016. This is expected to detract 0.2 percentage points from growth in the June quarter 2016 volume measure of GDP.

"At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

The global economy is continuing to grow, at a lower than average pace. Several advanced economies have recorded improved conditions over the past year, but conditions have become more difficult for a number of emerging market economies. Actions by Chinese policymakers have been supporting growth, but the underlying pace of China's growth appears to be moderating.

Commodity prices are above recent lows, but this follows very substantial declines over the past couple of years. Australia's terms of trade remain much lower than they had been in recent years.

Financial markets have continued to function effectively. Funding costs for high-quality borrowers remain low and, globally, monetary policy remains remarkably accommodative.

In Australia, recent data suggest that overall growth is continuing, despite a very large decline in business investment, helped by growth in other areas of domestic demand and exports. Labour market indicators continue to be somewhat mixed, but suggest continued expansion in employment in the near term" - Statement by Glenn Stevens, Governor.

Switzerland's real gross domestic product (GDP) grew by 0.6% in the 2nd quarter of 2016. Positive contributions to GDP came from foreign trade as well as government consumption, while household consumption expenditure stagnated, and investment in construction and equipment fell slightly. On the production side of GDP, growth was broadly based across sectors. The biggest boosts came from the energy sector, government-related sectors and other services. In comparison to the 2nd quarter of 2015, real GDP grew by 2.0%.

Exports of goods (excluding non-monetary gold, valuables and merchanting) rose by 0.8% in the 2nd quarter of 2016. The chemicals/pharmaceuticals category provided the strongest contribution to growth, while in particular the precision tools/watches/jewellery and machinery/appliances/electronics categories had a negative impact. Imports of goods (excluding non-monetary gold and valuables) rose by 0.5% in the 2nd quarter of 2016, with the chemicals/pharmaceuticals category showing the highest growth. Imports in the vehicles and precision tools/watches/jewellery categories fell.

Based on provisional data, the Federal Statistical Office (Destatis) reports that price-adjusted new orders in manufacturing had increased in July 2016 a seasonally and working-day adjusted 0.2% on June 2016. For June 2016, revision of the preliminary outcome resulted in a decrease of 0.3% compared with May 2016 (primary -0.4%). Price-adjusted new orders without major orders in manufacturing had decreased in July 2016 a seasonally and working-day adjusted 1.3% on June 2016.

In July 2016, domestic orders decreased by 3.0%, while foreign orders increased by 2.5% on the previous month. New orders from the euro area were up 5.9% on the previous month and new orders from other countries increased by 0.6% compared to June 2016.

In July 2016 the manufacturers of intermediate goods saw new orders unchanged in real terms adjusted for seasonally fluctuations and working-day variations compared with June 2016. The manufacturers of capital goods showed increases of 0.8% on the previous month. For consumer goods, a decrease in new orders of 4.3% was recorded.

EUR/USD

Resistance levels (open interest**, contracts)

$1.1308 (4349)

$1.1266 (4926)

$1.1205 (3163)

Price at time of writing this review: $1.1146

Support levels (open interest**, contracts):

$1.1110 (3171)

$1.1078 (4559)

$1.1038 (5710)

Comments:

- Overall open interest on the CALL options with the expiration date September, 9 is 52786 contracts, with the maximum number of contracts with strike price $1,1250 (4926);

- Overall open interest on the PUT options with the expiration date September, 9 is 58292 contracts, with the maximum number of contracts with strike price $1,1000 (5757);

- The ratio of PUT/CALL was 1.10 versus 1.12 from the previous trading day according to data from September, 2

GBP/USD

Resistance levels (open interest**, contracts)

$1.3600 (817)

$1.3501 (1818)

$1.3402 (2234)

Price at time of writing this review: $1.3319

Support levels (open interest**, contracts):

$1.3197 (874)

$1.3099 (1051)

$1.3000 (1856)

Comments:

- Overall open interest on the CALL options with the expiration date September, 9 is 32510 contracts, with the maximum number of contracts with strike price $1,3300 (2716);

- Overall open interest on the PUT options with the expiration date September, 9 is 27378 contracts, with the maximum number of contracts with strike price $1,2800 (2704);

- The ratio of PUT/CALL was 0.84 versus 0.82 from the previous trading day according to data from September, 2

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

U.S. stock futures switched between small gains and small losses on Monday, with markets closed for the Labor Day holiday and investors digesting an oil agreement between Russia and Saudi Arabia.

U.K. stocks retreated Monday, feeling the pinch from ratings downgrades for Royal Bank of Scotland PLC and Lloyds Banking Group PLC, as well as from dampened expectations for more monetary easing from the Bank of England after a stronger-than-expected services-sector update.

Shares in Asia were broadly higher Monday, as weaker-than-expected U.S. jobs data eased worries over an imminent interest-rate increase by the Federal Reserve. The U.S. added about 151,000 jobs in August, a number unlikely to be strong enough for the U.S. Federal Reserve to move toward raising interest rates in September, analysts say. The data helped lift stocks in the U.S. and Europe late Friday.

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers