- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 23-08-2011

Gainers:

Symb Last Change Chg %

PMC.N 13.97 +3.04 +27.81

VG.N 3.04 +0.42 +16.03

BID.N 34.38 +4.25 +14.11

IVN.N 19.74 +2.43 +14.04

HEI.N 49.57 +5.23 +11.80

Losers:

Symb Last Change Chg %

TIN.N 20.48 -4.34 -17.49

AIB.N 0.72 -0.07 -8.88

CMM.N 1.04 -0.09 -7.96

DL.N 2.35 -0.20 -7.84

HRZ.N 0.68 -0.05 -6.85

Stocks remain near session highs. Treasuries are still generally flat following results from an auction of 2-year Notes. The auction drew a bid-to-cover of 3.44, dollar demand of $120.4 billion, and an indirect bidder participation rate of 31.6%. For comparison, the prior auction produced a bid-to-cover of 3.14, dollar demand of $109.9 billion, and an indirect bidder rate of 27.7%. An average of the past six auctions results in a bid-to-cover ratio of 3.16, dollar demand of $110.5 billion, and an indirect bidder rate of 30.5%.

The dollar weakened against most of its major counterparts as speculation that Federal Reserve Chairman Ben S. Bernanke may signal further steps to boost the U.S. economy damped demand for safer assets.

The New Zealand and Australian dollars led gains versus the greenback after reports showed manufacturing from China to Europe exceeded economists’ forecasts and before Bernanke’s speech on Aug. 26 in Jackson Hole, Wyoming. The euro trimmed an advance versus the dollar as European stocks pared increases. The yen rose versus the greenback even amid speculation officials will act to curb the Japanese currency’s appreciation.

“You have an overall trend of a weaker dollar,” said Fabian Eliasson, head of U.S. currency sales at Mizuho Financial Group Inc. in New York. “The whole market is just waiting for the Jackson Hole meeting. We might not have seen the last of the Federal Reserve putting more liquidity in the market.”

The Standard & Poor’s 500 Index advanced 1.5 percent. The Stoxx Europe 600 Index was up 0.6 percent after rising earlier as much as 2.2 percent.

Demand for higher-yielding assets gained today as a preliminary gauge of Chinese manufacturing in August slipped to 49.8, according to a reading of the Purchasing Managers’ Index reported by HSBC Holdings Plc and Markit Economics today. The figure was better than the “rumored” number of 45 and may provide some relief to the market, Bank of America Merrill Lynch’s Ting Lu said. A number below 50 shows a contraction.

Germany’s manufacturing purchasing managers’ index was 52 in August, exceeding the 50.6 median forecast in a Bloomberg survey, Markit Economics said separately today. A composite index of euro-area purchasing managers in services and manufacturing also exceeded estimates.

Stocks have rallied back from a recent slip. The effort has taken the broader market up to a gain of more than 2%. Buying action has been broad based, but newfound strength among financials has been a primary impetus for the move.

Financial stocks had been lagging all session as participants applied pressure to diversified banks and financial services providers, but the overall financial sector has since climbed to a 2.0% gain. The move comes as the likes of JPMorgan Chase (JPM 34.27, +0.86) and Citigroup (C 26.90, +0.84) rally to heady gains.

weekly retail sales reports "signaled a purchasing pause in the week ending 20 Aug." Could be that "weak consumer sentiment is constraining spending" for back-to-school.

"Despite the decline this month, the pace of new home sales remains squarely within the 281-331k range that new home sales have registered over the past year, so we characterize today's reading as suggesting that little has changed.

The dollar index remains in negative territory, which has provided some strength to the CRB Commodity Index. Energy markets are mixed, while precious metals are lower.

Crude oil lost steam almost two hours ago and fell $2 to new session lows of $83.40/barrel. Crude has recovered above the $84 level and moved back into positive territory and is now up 0.1% at $84.53/barrel. Natural gas has been in positive territory all morning and just hit new session highs of $3.96/MMBtu and is currently up 1.7% at $3.95/MMBtu.

Gold and silver have been trading with modest losses this morning. In recent trade, silver pushed off of new session lows of $42.60/oz and momentarily moved into the black. However, it's currently down 0.2% at $43.25/oz. Gold is down 0.6% at $1880.40/oz.

"-0.7% Jul new home sales to an 8-month low of

EUR/USD: $1.4200, $1.4230, $1.4250, $1.4300, $1.4500.

USD/JPY: Y75.00, Y76.00, Y77.00

GBP/USD: $1.6500

EUR/CHF: Chf1.1300, Chf1.1400

AUD/USD: $1.0395, $1.0435

US data include New Home Sales at 14:00 GMT.

"We still expect weak but positive GDP growth for the remainder of this year and into 2012. But recession risks are clearly rising. We also est mfg ISM may print below 50 but say this isn't a recession signal - a number in the 46-42 area might be instead."

Data released:

02:30 China HSBC Manufacturing PMI 49.8 49.3

03:00 New Zealand RBNZ Inflation Expectations (YoY) (Q3) 2.9% 3.0%

Asian currencies advanced on speculation policy makers will continue to raise borrowing costs to fight inflation and the Federal Reserve will unveil stimulus measures to revive the U.S. economy.

Central bankers from around the world will meet at Jackson Hole, Wyoming this week, where Fed Chairman Ben S. Bernanke foreshadowed the second round of quantitative easing last year.

GBP/USD follows the euro higher - up from the lows around $1.6450 to highs on $1.6570.

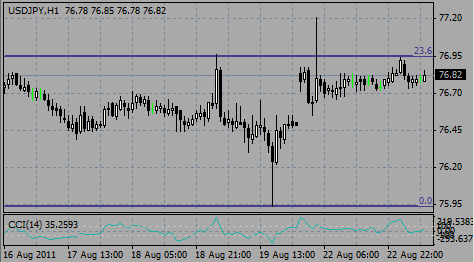

USD/JPY weakened from Y76.94 to Y76.55/60.

In Europe attention will be on ZEW index at 09:00 GMT.

The UK CBI Industrial Trends Survey will announce its orders data for August at 10:00 GMT.

US data include New Home Sales at 14:00 GMT.

EUR/USD

Offers: $1.4400, $1.4415/20

Bids: $1.4340

GBP/USD

Offers: $1.6520/25

Bids: $1.6450/40

NZD/USD

Offers: $0.8300/10

AUD/USD

Offers: $1.0475/85

EUR/GBP:

Offers: stg0.8745/55

Bids: stg0.8725/20, stg0.8700

EUR/USD: $1.4200, $1.4230, $1.4250, $1.4300, $1.4500.

USD/JPY: Y75.00, Y76.00, Y77.00

GBP/USD: $1.6500

EUR/CHF: Chf1.1300, Chf1.1400

AUD/USD: $1.0395, $1.0435

Majors close

Nikkei 225 -91.11 -1.04% 8,628.13

FTSE 100 +54.54 +1.08% 5,095.30

CAC 40 +34.37 +1.14% 3,051.36

DAX -6.22 -0.11% 5,473.78

Dow +37.00 +0.34% 10,854.65

Nasdaq +3.54 +0.15% 2,345.38

S&P 500 +0.29 +0.03% 1,123.82

10 Year Yield 2.09% +0.02 --

Commodities Oil $84.30 +0.18 +0.21%

Gold $1,894.70 +2.80 +0.15%

The Nikkei 225 (NKY) Stock Average slipped 1%, erasing earlier gains. The exporter-heavy index advanced briefly after Japanese Finance Minister Yoshihiko Noda said today he’s prepared to take decisive steps to curb the yen’s appreciation after it rose last week to a post-World War II high against the dollar.

Exporters slid on concern global economic growth is slowing.

Toyota Motor Corp. dropped 2.5%.

Fanuc Corp. fell 4.1%.

Hino Motors Ltd. slumped 4.8% after Deutsche Bank AG. cut its investment rating on the truckmaker.

The Topix slipped 1.2%, falling to the lowest since March 2009. The gauge lost 12% this month amid concern that U.S. growth is sputtering and Europe’s debt crisis will damage the banking system, damping demand in two of Japan’s biggest export markets.

European stocks rebounded from a two-year low amid speculation the Federal Reserve may this week signal additional stimulus measures and as prospects for an end to the war in Libya boosted energy companies.

Eni SpA (ENI) and Petrofac Ltd. (PFC) led a rally in oil companies, both rising more than 3%.

Petropavlovsk Plc (POG) jumped 6.2% as Citigroup Inc. upgraded the gold producer and the precious metal advanced to an all-time high.

Jyske Bank A/S dropped 7.6% as earnings missed estimates.

The benchmark Stoxx Europe 600 Index rose 0.8% to 224.9, having earlier lost the same amount. The gauge retreated 6.1% last week, extending its decline from this year’s high to 23%.

Gains in European stocks were limited as German Chancellor Angela Merkel resisted calls for common euro-area borrowing. Speaking in an interview with ZDF television from the chancellery in Berlin yesterday, she said bringing in euro bonds at this time would further undermine economic stability.

U.S. stocks rose modestly Monday as investors grappled with an uncertain economic outlook ahead of a key speech by Fed chairman Ben Bernanke.

Hewlett-Packard (HPQ, Fortune 500) was the strongest performer on the Dow, with shares rising over 3.5%. HP's stock plunged 20% on Friday amid concerns about the company's turnaround plan.

Shares of big financial institutions were among the biggest decliners. Bank of America (BAC, Fortune 500) sank 7%, near its 52-week low, and JPMorgan (JPM, Fortune 500) slid 2.3%.

Investors are also looking ahead to Friday, when Bernanke will give his keynote speech.

At last year's annual meeting, the Fed chief prepared the market for QE2, a bond-buying program that is widely credited for supporting stocks earlier this year.

Meanwhile, shares of oil companies Exxon (XOM, Fortune 500) and Chevron (CVX, Fortune 500) were in focus as rebel forces swept the Libyan capital of Tripoli, poised to topple Moammar Gadhafi's 42-year rule following six months of civil war.

On Friday, U.S. stocks capped a difficult week, with the S&P 500 posting its biggest four-week drop since March 2009. The Dow, S&P 500 and Nasdaq fell between 4% and 6% last week.

The yen retreated from record against the dollar and the Swiss franc weakened amid speculation policy makers in both countries will seek to curb gains in their currencies that are hurting exporters.

The yen fell the most in two weeks after Japan’s Finance Minister Yoshihiko Noda said he’s ready to take decisive steps after the currency strengthened to 75.95 against the greenback on Aug. 19.

“One of the big drivers for these two currencies has been the heightened speculation of imminent intervention by the Japanese and Swiss authorities,” said Lee Hardman, a currency strategist at Bank of Tokyo-Mitsubishi UFJ Ltd..

Noda told reporters today he’s become “more concerned about the worsening of the yen’s one-sided movements.” The government will take “bold actions if necessary and won’t rule out any possible options,” he said.

Bank of Japan Deputy Governor Hirohide Yamaguchi said yesterday he was “worrying” about the yen’s gains, noting also that a stronger currency won’t “necessarily” damage the economy.

Gains in the dollar were limited amid speculation Federal Reserve Chairman Ben S. Bernanke will signal at an Aug. 26 conference that the Fed will increase monetary stimulus to boost the economy. The central bank bought $600 billion in Treasuries from November through June in a process known as quantitative easing or QE2.

“The market focus is on Bernanke’s speech this week,” Junichi Ishikawa, a Tokyo-based market analyst at IG Markets Securities Ltd. wrote in a note to clients today. “There may be increasing downward pressure for the dollar, should he mention the possibility of QE3.”

GBP/USD remained within the $1.6460/$1.6510 range for some time before refreshed lows.

USD/JPY rallied to Y77.20 before sharply retreated to Y76.70.

In Europe attention will be on ZEW index at 09:00 GMT.

The UK CBI Industrial Trends Survey will announce its orders data for August at 10:00 GMT.

US data include New Home Sales at 14:00 GMT.

- yen's appreciation impacts economy ngatively;

- rapid yen rise reflects both capital and speculative moves;

- doesn't comment on forex rates.

- yen's appreciation impacts economy ngatively;

- rapid yen rise reflects both capital and speculative moves;

- doesn't comment on forex rates.

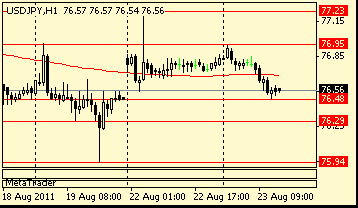

Resistance 3: Y78.20

Resistance 2: Y77.80

Resistance 1: Y77.20

Current price: Y76.77

Support 1:Y75.90

Support 2:Y75.00

Support 3:Y74.30

Nikkei 225 -91.11 -1.04% 8,628.13

FTSE 100 +54.54 +1.08% 5,095.30

CAC 40 +34.37 +1.14% 3,051.36

DAX -6.22 -0.11% 5,473.78

Dow +37.00 +0.34% 10,854.65

Nasdaq +3.54 +0.15% 2,345.38

S&P 500 +0.29 +0.03% 1,123.82

10 Year Yield 2.09% +0.02 --

Commodities Oil $84.30 +0.18 +0.21%

Gold $1,894.70 +2.80 +0.15%

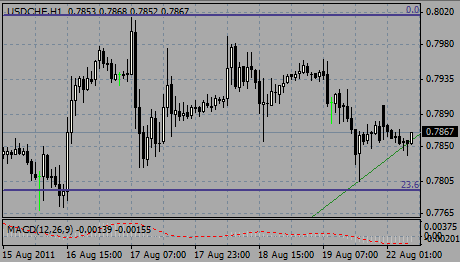

Resistance 3: Chf0.8140

Resistance 2: Chf0.8010/15

Resistance 1: Chf0.7910

Current price: Chf0.7885

Support 1: Chf0.7790

Support 2: Chf0.7660

Support 3: Chf0.7540

Comments: Techs hasn't changed with strong support comes at Chf0.7790 (23.6% Fibo of Chf0.7070 - Chf0.8020). Below losses may widen to Chf0.7660 (38.6%) and Chf0.7540 (Aug 12 lows). Resistance is around yesterday's highs on Chf0.7960, stronger - at Chf0.8010/15 (Aug 17 highs). Further rise may extend Chf0.8140 (channel line from the mid-Feb).

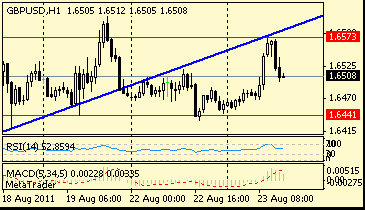

Resistance 3:$1.6660

Resistance 2:$1.6620

Resistance 1: $1.6520

Current price: $1.6476

Support 1: $1.6420

Support 2: $1.6360

Support 3: $1.6300/10

Comments: Rate holds tight today with support is near $1.6420 (38.2% of Friday's high). Below losses may widen to $1.6360 (50%, $1.6350 - Aug 17 low) and $1.6300/10 (61.8%). Resistance is near yesterday's highs on $1.6520, stronger - at $1.6620 (Friday's high). Further rise may extend to $1.6660.

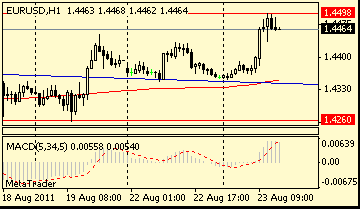

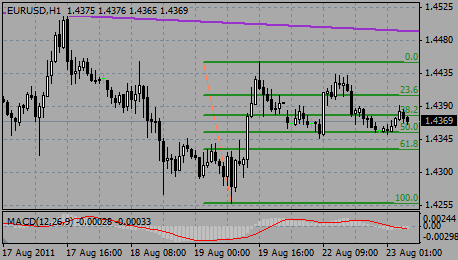

Resistance 3: $1.4580

Resistance 2: $1.4500/20

Resistance 1: $1.4450

Current price: $1.4373

Support 1: $1.4350

Support 2: $1.4330

Support 3: $1.4260

Comments: Techs hasn't changed since yesterday. Support remains at $1.4350 (50% of Friday's rise). Below there is a chance for a test of $1.4330 (61.8%). Stronger level - at $1.4260 (Friday's low). Resistance is around Friday's high on $1.4450. Stronger resistance comes at $1.4500/20 (channel line from May 04, also Aug 17 high). Further rise may extend to $1.4580 (Jul 04 high).

06:58 France PMI (August) flash 49.7 50.5

06:58 France PMI services (August) flash 53.9 54.2

07:28 Germany PMI (August) flash 51.0 52.0

07:28 Germany PMI services (August) flash 52.0 52.9

07:58 EU(17) PMI (August) flash 49.5 50.4

07:58 EU(17) PMI services (August) flash 51.0 51.6

09:00 Germany ZEW economic expectations index (August) -25.0 -15.1

10:00 UK CBI industrial order books balance (August) -13% -10%

10:00 UK CBI industrial output balance (August) - 6%

12:30 Canada Retail sales (June) 0.6% 0.1%

12:30 Canada Retail sales excluding auto (June) 0.3% 0.5%

12:55 USA Redbook (20.08)

14:00 USA New home sales (July) 315K 312K

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers