- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 28-03-2019

| Time | Country | Event | Period | Previous value | Forecast |

|---|---|---|---|---|---|

| 00:01 | United Kingdom | Gfk Consumer Confidence | March | -13 | -14 |

| 00:30 | Australia | Private Sector Credit, m/m | February | 0.2% | 0.3% |

| 00:30 | Australia | Private Sector Credit, y/y | February | 4.3% | |

| 05:00 | Japan | Construction Orders, y/y | February | 19.8% | |

| 05:00 | Japan | Housing Starts, y/y | February | 1.1% | 0.5% |

| 07:00 | Germany | Retail sales, real unadjusted, y/y | February | 2.6% | 2.8% |

| 07:00 | Germany | Retail sales, real adjusted | February | 3.3% | -0.9% |

| 07:45 | France | CPI, m/m | March | 0% | 0.9% |

| 07:45 | France | Consumer spending | February | 1.2% | 0.2% |

| 07:45 | France | CPI, y/y | March | 1.3% | |

| 08:00 | Switzerland | KOF Leading Indicator | March | 92.4 | 93.9 |

| 08:55 | Germany | Unemployment Rate s.a. | March | 5% | 4.9% |

| 08:55 | Germany | Unemployment Change | March | -21 | -10 |

| 09:30 | United Kingdom | Net Lending to Individuals, bln | February | 4.8 | 4.6 |

| 09:30 | United Kingdom | Consumer credit, mln | February | 1.095 | 0.9 |

| 09:30 | United Kingdom | Mortgage Approvals | February | 66.77 | 65 |

| 09:30 | United Kingdom | Business Investment, y/y | Quarter IV | -1.9% | -3.7% |

| 09:30 | United Kingdom | Business Investment, q/q | Quarter IV | -1.2% | -1.4% |

| 09:30 | United Kingdom | Current account, bln | Quarter IV | -26.5 | -23 |

| 09:30 | United Kingdom | GDP, q/q | Quarter IV | 0.6% | 0.2% |

| 09:30 | United Kingdom | GDP, y/y | Quarter IV | 1.6% | 1.3% |

| 09:45 | Eurozone | ECB's Benoit Coeure Speaks | |||

| 12:30 | Canada | Industrial Product Price Index, y/y | February | 1% | |

| 12:30 | Canada | Industrial Product Price Index, m/m | February | -0.3% | |

| 12:30 | Canada | GDP (m/m) | January | -0.1% | 0% |

| 12:30 | U.S. | Personal Income, m/m | February | -0.1% | 0.3% |

| 12:30 | U.S. | PCE price index ex food, energy, Y/Y | January | 1.9% | 1.9% |

| 12:30 | U.S. | PCE price index ex food, energy, m/m | January | 0.2% | 0.2% |

| 12:30 | U.S. | Personal spending | January | -0.5% | 0.3% |

| 13:25 | U.S. | FOMC Member Williams Speaks | |||

| 13:45 | U.S. | Chicago Purchasing Managers' Index | March | 64.7 | 61 |

| 14:00 | U.S. | New Home Sales | February | 0.607 | 0.62 |

| 14:00 | U.S. | Reuters/Michigan Consumer Sentiment Index | March | 93.8 | 97.8 |

| 14:30 | U.S. | FOMC Member Kaplan Speak | |||

| 16:05 | U.S. | FOMC Member Quarles Speaks | |||

| 17:00 | U.S. | Baker Hughes Oil Rig Count | March | 824 |

| Time | Country | Event | Period | Previous value | Forecast |

|---|---|---|---|---|---|

| 00:01 | United Kingdom | Gfk Consumer Confidence | March | -13 | -14 |

| 00:30 | Australia | Private Sector Credit, m/m | February | 0.2% | 0.3% |

| 00:30 | Australia | Private Sector Credit, y/y | February | 4.3% | |

| 05:00 | Japan | Construction Orders, y/y | February | 19.8% | |

| 05:00 | Japan | Housing Starts, y/y | February | 1.1% | 0.5% |

| 07:00 | Germany | Retail sales, real unadjusted, y/y | February | 2.6% | 2.8% |

| 07:00 | Germany | Retail sales, real adjusted | February | 3.3% | -0.9% |

| 07:45 | France | CPI, m/m | March | 0% | 0.9% |

| 07:45 | France | Consumer spending | February | 1.2% | 0.2% |

| 07:45 | France | CPI, y/y | March | 1.3% | |

| 08:00 | Switzerland | KOF Leading Indicator | March | 92.4 | 93.9 |

| 08:55 | Germany | Unemployment Rate s.a. | March | 5% | 4.9% |

| 08:55 | Germany | Unemployment Change | March | -21 | -10 |

| 09:30 | United Kingdom | Net Lending to Individuals, bln | February | 4.8 | 4.6 |

| 09:30 | United Kingdom | Consumer credit, mln | February | 1.095 | 0.9 |

| 09:30 | United Kingdom | Mortgage Approvals | February | 66.77 | 65 |

| 09:30 | United Kingdom | Business Investment, y/y | Quarter IV | -1.9% | -3.7% |

| 09:30 | United Kingdom | Business Investment, q/q | Quarter IV | -1.2% | -1.4% |

| 09:30 | United Kingdom | Current account, bln | Quarter IV | -26.5 | -23 |

| 09:30 | United Kingdom | GDP, q/q | Quarter IV | 0.6% | 0.2% |

| 09:30 | United Kingdom | GDP, y/y | Quarter IV | 1.6% | 1.3% |

| 09:45 | Eurozone | ECB's Benoit Coeure Speaks | |||

| 12:30 | Canada | Industrial Product Price Index, y/y | February | 1% | |

| 12:30 | Canada | Industrial Product Price Index, m/m | February | -0.3% | |

| 12:30 | Canada | GDP (m/m) | January | -0.1% | 0% |

| 12:30 | U.S. | Personal Income, m/m | February | -0.1% | 0.3% |

| 12:30 | U.S. | PCE price index ex food, energy, Y/Y | January | 1.9% | 1.9% |

| 12:30 | U.S. | PCE price index ex food, energy, m/m | January | 0.2% | 0.2% |

| 12:30 | U.S. | Personal spending | January | -0.5% | 0.3% |

| 13:25 | U.S. | FOMC Member Williams Speaks | |||

| 13:45 | U.S. | Chicago Purchasing Managers' Index | March | 64.7 | 61 |

| 14:00 | U.S. | New Home Sales | February | 0.607 | 0.62 |

| 14:00 | U.S. | Reuters/Michigan Consumer Sentiment Index | March | 93.8 | 97.8 |

| 14:30 | U.S. | FOMC Member Kaplan Speak | |||

| 16:05 | U.S. | FOMC Member Quarles Speaks | |||

| 17:00 | U.S. | Baker Hughes Oil Rig Count | March | 824 |

Major US stock indices rose moderately, aided by reports of progress in trade negotiations between the US and China.

However, further increases were limited by revised US GDP data, which heightened concerns about a slowdown in economic growth. A report by the Department of Commerce showed that US economic growth slowed more than initially reported in the fourth quarter of 2018, due to a revision of consumer and government spending. According to the report, the US GDP grew by 2.2% year on year, which was below the initial value of 2.6% and the forecast of experts 2.4%. Consumer spending, which constitutes a large part of the economy, grew by 2.5% (revised downwards), which also turned out to be lower than expected. In the third quarter of 2018, the US economy grew by 3.4%.

With regard to trade negotiations, the US delegation, led by Trade Representative Robert Lighthizer and Finance Minister Stephen Mnuchin, arrived in Beijing for a two-day meeting on Thursday. Reuters reported yesterday evening that China made unprecedented proposals on a number of controversial issues, including the forced transfer of technology by US companies when entering the PRC market. The message is encouraging, but it should be remembered that the market has already expressed hope for a final deal, which has never been reached. Trump's economic adviser Larry Cudlow said that negotiations are not time-dependent.

Most of the components of DOW finished trading in positive territory (25 out of 30). The growth leader was NIKE Inc. (NKE, + 1.15%). The outsider was Verizon Communications Inc. (VZ; -2.95%).

Almost all sectors of the S & P recorded an increase. The service sector grew the most (+ 0.6%). The largest decline was shown by the utility sector (-0.8%).

At the time of closing:

Dow 25,717.46 +91.87 +0.36%

S & P 500 2,815.44 +10.07 +0.36%

Nasdaq 100 7,669.17 +25.79 +0.34%

Spanish business confidence index rose to -2.3 in March from a downwardly revised -4.7 in February (originally -4.9). It was the highest reading since November of 2018.

Expectations for production rose significantly (5.4 in March from -2.1 in February) and new orders improved (-6.1 from -6.7). At the same time, the current level of output decreased (-3.0 from -0.3) and employment expectations dropped slightly (2.5 from 2.6).

The National Association of Realtors (NAR) announced on Thursday its seasonally adjusted pending home sales index (PHSI) fell 1.0 percent m-o-m to 101.9 in February, down from 102.9 in January.

Economists had expected pending home sales to raise 0.7 percent m-o-m in February.

On y-o-y basis, the index tumbled 4.9 percent. That was the 14th consecutive month of annual declines.

According to the report, the pending home sales rose in in two of the four regions in m-o-m terms but fell in most regions compared to February 2018. Pending home sales in the South inched up 1.7 percent m-o-m to an index of 121.8 in February, which is 2.9 percent lower than this time last year. The PHSI in the West increased 0.5 percent m-o-m in February to 87.5 and fell 9.6 percent below a year ago. The index in the Northeast decreased 0.8 percent m-o-m to 92.1 in February, and is now 2.6 percent below a year ago. In the Midwest, the index dropped 7.2 percent m-o-m to 93.2 in February, 6.1 percent lower than February 2018.

The chief economist for the NAR, Lawrence Yun, said February’s pending home sales decline is coming off a solid gain in the prior month. “In January, pending contracts were up close to 5 percent, so this month’s 1 percent drop is not a significant concern,” he noted. “As a whole, these numbers indicate that a cyclical low in sales is in the past but activity is not matching the frenzied pace of last spring.”

The Federal Statistical Office (Destatis) reported on Thursday that the inflation rate in Germany is expected to slow to 1.3 percent y-o-y in March from 1.5 percent in February.

Economists expect the rate of inflation to be 1.6 percent y-o-y.

According to the report, energy inflation accelerated to 4.5 percent y-o-y this month from 2.9 percent y-o-y in February, while food price growth slowed to 0.7 percenty-o-y from 1.4 percent y-o-y.

Compared to the previous month, the CPI is seen to increase by 0.4 percent in March, the same pace as in February.

Economists forecast a 0.6 percent m-o-m gain.

The harmonised index of consumer prices for Germany, which is calculated for European purposes, is estimated to increase by 1.5 prercent y-o-y and 0.6 percent m-o-m.

- U.S. is more exposed to global shock due to integration

- Fed can be patient amid global risks, muted inflation

- Risks include Brexit, trade and slower global growth

U.S. stock-index were flat on Wednesday as investors awaited more details on the progress in the U.S.-China trade talks amid lingering concerns of slowing economic growth.

Global Stocks:

Index/commodity | Last | Today's Change, points | Today's Change, % |

Nikkei | 21,033.76 | -344.97 | -1.61% |

Hang Seng | 28,775.21 | +46.96 | +0.16% |

Shanghai | 2,994.94 | -27.78 | -0.92% |

S&P/ASX | 6,176.10 | +40.10 | +0.65% |

FTSE | 7,221.99 | +27.80 | +0.39% |

CAC | 5,305.57 | +4.33 | +0.08% |

DAX | 11,445.70 | +26.66 | +0.23% |

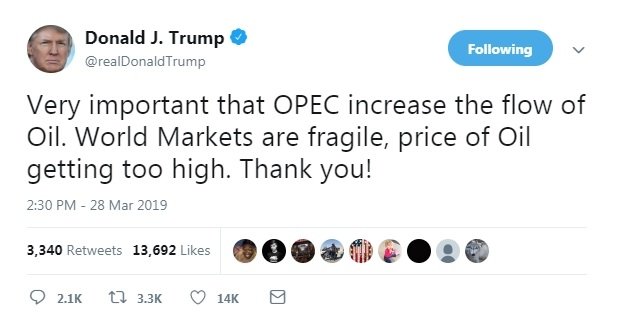

Crude oil | $58.49 | -1.55% | |

Gold | $1,305.40 | -0.87% |

The data from the Labor Department revealed the number of applications for unemployment benefits fell to a two-month low last week, pointing to still strong labor market conditions.

According to the report, the initial claims for unemployment benefits decreased 5,000 to 211,000 for the week ended March 23.

Economists had expected 225,000 new claims last week.

Claims for the prior week were revised downwardly to 216,000 from the initial estimate of 221,000.

Meanwhile, the four-week moving average of claims dropped 3,250 to 217,250 last week.

(company / ticker / price / change ($/%) / volume)

ALCOA INC. | AA | 27.9 | -0.01(-0.04%) | 300 |

Amazon.com Inc., NASDAQ | AMZN | 1,766.55 | 0.85(0.05%) | 37852 |

American Express Co | AXP | 108.8 | -0.18(-0.17%) | 201 |

Apple Inc. | AAPL | 188.12 | -0.35(-0.19%) | 108572 |

AT&T Inc | T | 31.47 | 0.07(0.22%) | 28780 |

Boeing Co | BA | 375.11 | 0.90(0.24%) | 28453 |

Caterpillar Inc | CAT | 131.07 | -0.13(-0.10%) | 1726 |

Chevron Corp | CVX | 122.08 | -0.71(-0.58%) | 5049 |

Cisco Systems Inc | CSCO | 53.1 | -0.04(-0.08%) | 7795 |

Citigroup Inc., NYSE | C | 60.71 | -0.02(-0.03%) | 3906 |

Exxon Mobil Corp | XOM | 80 | -0.34(-0.42%) | 1663 |

Facebook, Inc. | FB | 164 | -1.87(-1.13%) | 140350 |

FedEx Corporation, NYSE | FDX | 174 | -2.09(-1.19%) | 847 |

Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 12.7 | -0.01(-0.08%) | 5998 |

General Electric Co | GE | 9.97 | 0.01(0.10%) | 86405 |

Goldman Sachs | GS | 190.21 | 0.18(0.09%) | 10374 |

Hewlett-Packard Co. | HPQ | 19.01 | 0.08(0.42%) | 306 |

Home Depot Inc | HD | 189.55 | 0.30(0.16%) | 818 |

Intel Corp | INTC | 53.15 | -0.01(-0.02%) | 4261 |

Johnson & Johnson | JNJ | 139.05 | 0.35(0.25%) | 682 |

JPMorgan Chase and Co | JPM | 99.9 | 0.32(0.32%) | 7254 |

McDonald's Corp | MCD | 187.3 | -0.21(-0.11%) | 361 |

Microsoft Corp | MSFT | 117.08 | 0.31(0.27%) | 45366 |

Nike | NKE | 83.26 | 0.17(0.20%) | 2818 |

Pfizer Inc | PFE | 42.15 | 0.13(0.31%) | 307 |

Tesla Motors, Inc., NASDAQ | TSLA | 275.77 | 0.94(0.34%) | 40223 |

Twitter, Inc., NYSE | TWTR | 32.21 | -0.07(-0.22%) | 40930 |

UnitedHealth Group Inc | UNH | 242.5 | 0.79(0.33%) | 678 |

Wal-Mart Stores Inc | WMT | 97.17 | -0.04(-0.04%) | 901 |

Walt Disney Co | DIS | 110.32 | 0.04(0.04%) | 2214 |

Yandex N.V., NASDAQ | YNDX | 35 | 0.16(0.46%) | 1900 |

Boeing (BA) Buy rating reiterated at Tigress Research

FedEx (FDX) downgraded to Neutral from Positive at Susquehanna

A report from the Commerce Department showed on Thursday that the U.S.

economy grew slower than initially thought in the fourth quarter of 2018, as personal

consumption expenditures (PCE), state and local government spending, and

nonresidential fixed investment were revised down, but the general picture of

economic growth remains the same.

According to the third estimate, the U.S. gross domestic product (GDP)

grew at a 2.2 percent annual rate in the fourth quarter, lower than 2.6 percent

reported in the second estimate.

Economists had expected the growth rate to be revised down to 2.4

percent.

In the third quarter of 2018, the economy expanded by 3.4 percent.

The increase in real GDP in the fourth quarter reflected positive

contributions from personal consumption expenditures (PCE), nonresidential

fixed investment, exports, private inventory investment, and federal government

spending. Those were partly offset by negative contributions from residential

fixed investment and state and local government spending. Imports, which are a

subtraction in the calculation of GDP, increased in the fourth quarter.

Meanwhile, the deceleration in real GDP growth in the fourth quarter

reflected decelerations in private inventory investment, PCE, and federal

government spending and a downturn in state and local government spending.

These movements were partly offset by an upturn in exports and an acceleration

in nonresidential fixed investment. Imports increased less in the fourth

quarter than in the third quarter.

- PM's deal, if supported, is best path to leaving EU on May 22

- May's views on merits of a customs union have not changed

- Theresa May meeting with colleagues throughout the day

- Government talks with DUP are ongoing

- Clear both sides in talks with DUP believe discussions have taken place in a constructive spirit

- I would support a certain mitigation, consider the topic as relevant

German exports will grow by up to 3% this year and hit a record high of nearly 1.4 trillion euros, the BGA trade association said, suggesting that companies are able to expand foreign business despite trade disputes and Brexit.

Imports are expected to increase by 5% to reach an all-time high of 1.14 trillion euros in 2019, BGA head Holger Bingmann told.

Bingmann criticised Economy Minister Peter Altmaier's new industrial strategy, which envisages a shift towards a more interventionist policy to tackle an assertive China. Bingmann adding that the government should fight efforts in Europe to weaken competition and the free flow of market forces.

Jakob Christensen, chief analyst at Danske Bank, notes that EUR actually proved rather resilient to ECB hints of a tiered deposit system yesterday notwithstanding the significant drop seen in euro rates across the curve.

“On the one hand, to the extent that tiered deposits allow ECB to keep rates lower for longer it is clearly a EUR negative. On the other hand, to the extent that this leaves the impression of an ECB that is severely challenged on its toolbox and that low inflation risks becoming entrenched (like has happened for SNB and BoJ) it is a EUR positive down the road. ECB will have to stick to a soft stance near term, and this may fuel a larger easing risk premium on EUR/USD, but we are not in for a break of 1.10 in our view.”

According to the report from European Commission, in March 2019, the Economic Sentiment Indicator (ESI) decreased slightly in both the euro area (by 0.7 points to 105.5) and the EU (by 0.4 points to 105.0).1

The deterioration of euro-area sentiment resulted from markedly lower confidence in industry and, to a lesser extent, services, while confidence improved in retail trade and construction and remained broadly stable among consumers.

The marked decrease in industry confidence (−1.3) resulted from managers' more pessimistic views on all three components, i.e. production expectations, the current level of overall order books and the stocks of finished products. The decline in services confidence (−0.8) was driven by managers' significantly more pessimistic views on past and expected demand, while their assessment of the past business situation held up. The stability of consumer confidence (+0.2) resulted from households’ more positive assessments of their past financial situation and their expectations about the general economic situation, partly offset by a slight decrease in their intentions to make major purchases.

Consumers’ expectations of their future financial situation remained broadly stable. The strong increase in retail trade confidence (+1.5) resulted from more positive views on all its components: the present and expected business situation, and managers’ assessment of the adequacy of the volume of stocks. Increasing construction confidence (+0.9) was fuelled by managers' more optimistic views on the level of order books, while their employment expectations worsened. Finally, financial services confidence (not included in the ESI) increased sharply (+9.2), reflecting strong improvement in all its components (i.e. managers' appraisals of past and future demand and their assessment of the past business situation).

Jakob Christensen, chief analyst at Danske Bank, points out that in the UK, in yesterday’s indicative votes, the House of Commons rejected all eight Brexit options, which is not a big surprise.

“Next step is likely more indicative votes on Monday 1 April, where members of parliament may vote again but on fewer options. Within the Conservative Party more Brexiteers are now backing May’s deal after she promised to resign soon after Brexit has been delivered, but unfortunately for May, the supporting party DUP from Northern Ireland remains against. May’s deal will likely be dead on arrival if brought forward for a vote tomorrow. With just about two weeks to go, uncertainty is high. In our view, there seems to be four possible ways forward now: May’s deal, no deal, second EU referendum or May’s deal including a permanent customs union. Risk of snap election might have gone up, though.”

According to the report from European Central Bank, annual growth rate of broad monetary aggregate M3 increased to 4.3% in February 2019 from 3.8% in January. Economists had expected a 3.9% increase

Annual growth rate of narrower monetary aggregate M1, comprising currency in circulation and overnight deposits, increased to 6.6% in February from 6.2% in January

Annual growth rate of adjusted loans to households stood at 3.3% in February, compared with 3.2% in January

Annual growth rate of adjusted loans to non-financial corporations increased to 3.7% in February from 3.4% in January

The European Central Bank’s chief economist says there needs to be a solid monetary-policy case before officials act to mitigate side effects of negative interest rates on banks.

ECB staff are examining the issue of tiering -- where some of banks’ excess reserves are exempt from the lowest rate -- but action isn’t a done deal, Peter Praet said.

“For tiering, we need to be convinced that it would address a monetary-policy question in an efficient way,’’ he said. “We have to be ready for all the possible instruments that we could use.’’

“The perspective of low rates for longer has triggered the debate about the side effects of a negative rates,” Praet said. “When you look at the economy today and the lending channel, we don’t see any particular problem,” but “with the weakening economy, it may happen in the future. So you have to be ready.”

According to the flash estimate issued by the INE, the annual inflation of the CPI in March 2019 was 1.3%. This indicator provides a preview of the CPI that, if confirmed, would imply an increase of two tenths in the annual rate, since in February this change was 1.1%. This behaviour highlights the increase in the prices of fuels. Also influences that the prices of electricity decrease this month less than in 2018.

In turn, the annual variation of the flash estimate of the HICP in March stands at 1.3%. If confirmed, the annual rate of the HICP would increase two tenths with respect to the previous month. According to the flash estimate of the CPI, consumer prices registered a variation of 0.4% as compared with February.

Karen Jones, analyst at Commerzbank, notes that the GBP/USD pair continues to hold steady as the pair has held over the 3 month uptrend at 1.3055 and 200 day ma at 1.2980 and for now they will continue to favour the topside.

“The market recently challenged the 1.3363 July 2018 high, reaching 1.3382 before failing. Provided that dips lower are contained by the 200 day ma, our overall target remains the 1.3563 200 week ma. Below the 200 day ma lies the double Fibo retracement at 1.2900/1.2895. This guards the recent low at 1.2772. Below 1.2772 we would allow for losses to the 1.2669/62 15th January low and August low and possibly the 1.2609/78.6% retracement.”

The talks are expected to last for a full day on Friday, ministry spokesman Gao Feng told reporters at a regular briefing.

Gao said both sides have achieved some progress during previous phone calls, but there remains much work to do.

China will sharply expand market access for foreign banks and securities and insurance companies, especially in its financial services sector, Premier Li Keqiang said.

The government will also work on more favourable policies for foreign investors to trade Chinese bonds, Li said in a speech at the annual Boao forum.

"We are quickening the full opening of market access for foreign investors in banking, securities and insurance sectors," he said.

Li's remarks add to speculation that China may soon announce new rules that will allow foreign banks and insurance firms to increase their presence in China, as senior officials from China and the United States are due to meet in Beijing this week for the next round of trade negotiations.

The U.S. and China have no choice but to conclude ongoing trade negotiations, most likely in the next month or so, former U.S. ambassador to China Max Baucus said.

"The talks will conclude. They have to," Baucus told. "U.S, China, we're so closely joined at the hip economically, we got to get this thing done."

"There's some feeling here maybe — by the end of April, maybe a little longer — but we'll get it done," Baucus said, noting that otherwise, U.S. stock markets and China's already slowing economy would be negatively impacted.

For those reasons, Baucus said there is greater impetus for the U.S. to make a deal with China. He also said the near-term fallout of nuclear talks between Trump and North Korean leader Kim Jong Un in late February should not be used as an example for how trade negotiations between the world's two largest economies might end.

According to Karen Jones, analyst at Commerzbank, EUR/USD remains on the defensive following its rejection last week from the 200 day ma at 1.1471 and has sold off to the February low at 1.1234.

“The intraday Elliott waves counts are conflicting and it is possible that we retest the 1.1176 recent low. We suspect that it is trying to base but needs to do more work. Once above the 200 day ma, the cross should target the 1.1570 January high, together with the 55 week ma at 1.1609. We view 1.1176 as an interim low in place. Initial support lies at 1.1216 November low ahead of 1.1176 low. Long term trend (1-3 months): Completed a falling wedge – target the 55 week ma. Then the 1.1815 September 2018 high on route to 1.2000.”

EUR/USD

Resistance levels (open interest**, contracts)

$1.1423 (2248)

$1.1392 (1283)

$1.1370 (409)

Price at time of writing this review: $1.1257

Support levels (open interest**, contracts):

$1.1236 (3363)

$1.1193 (3165)

$1.1146 (4602)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date April, 5 is 73095 contracts (according to data from March, 27) with the maximum number of contracts with strike price $1,1350 (4785);

GBP/USD

Resistance levels (open interest**, contracts)

$1.3399 (1473)

$1.3372 (465)

$1.3341 (752)

Price at time of writing this review: $1.3190

Support levels (open interest**, contracts):

$1.3150 (1439)

$1.3118 (769)

$1.3083 (568)

Comments:

- Overall open interest on the CALL options with the expiration date April, 5 is 26846 contracts, with the maximum number of contracts with strike price $1,3400 (4260);

- Overall open interest on the PUT options with the expiration date April, 5 is 31158 contracts, with the maximum number of contracts with strike price $1,2500 (5057);

- The ratio of PUT/CALL was 1.16 versus 1.18 from the previous trading day according to data from March, 27

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

| Raw materials | Closed | Change, % |

|---|---|---|

| Brent | 67.18 | -0.3 |

| WTI | 59.39 | -0.95 |

| Silver | 15.27 | -0.91 |

| Gold | 1309.67 | -0.41 |

| Palladium | 1446.87 | -6.12 |

| Index | Change, points | Closed | Change, % |

|---|---|---|---|

| NIKKEI 225 | -49.66 | 21378.73 | -0.23 |

| Hang Seng | 161.34 | 28728.25 | 0.56 |

| KOSPI | -3.18 | 2145.62 | -0.15 |

| ASX 200 | 5.4 | 6136 | 0.09 |

| FTSE 100 | -2.1 | 7194.19 | -0.03 |

| DAX | -0.44 | 11419.04 | -0 |

| Dow Jones | -32.14 | 25625.59 | -0.13 |

| S&P 500 | -13.09 | 2805.37 | -0.46 |

| NASDAQ Composite | -48.14 | 7643.38 | -0.63 |

| Pare | Closed | Change, % |

|---|---|---|

| AUDUSD | 0.70854 | -0.68 |

| EURJPY | 124.265 | -0.32 |

| EURUSD | 1.12508 | -0.17 |

| GBPJPY | 145.337 | -0.5 |

| GBPUSD | 1.31576 | -0.35 |

| NZDUSD | 0.67971 | -1.52 |

| USDCAD | 1.34106 | 0.21 |

| USDCHF | 0.99393 | -0.04 |

| USDJPY | 110.444 | -0.15 |

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers