- Analytics

- News and Tools

- Market News

Analytics, News, and Forecasts for CFD Markets: stock news — 22-08-2016.

(index / closing price / change items /% change)

Nikkei 225 16,598.19 +52.37 +0.32%

Shanghai Composite 3,084.76 -23.34 -0.75%

S&P/ASX 200 5,515.06 -11.63 -0.21%

FTSE 100 6,828.54 -30.41 -0.44%

CAC 40 4,389.94 -10.58 -0.24%

Xetra DAX 10,494.35 -50.01 -0.47%

S&P 500 2,182.64 -1.23 -0.06%

Dow Jones Industrial Average 18,529.42 -23.15 -0.12%

S&P/TSX Composite 14,748.19 +60.73 +0.41%

Major U.S. stock-indexes little changed on Monday as oil prices fell and investors remained cautious ahead of Federal Reserve Chair Janet Yellen's speech this week. With the earnings season coming to an end, investor focus will shift to Yellen's speech on Friday at the annual central bankers' meeting in Jackson Hole, Wyoming to see whether the Fed is keen on raising interest rates in the coming months.

Most of Dow stocks in negative area (21 of 30). Top gainer - The Boeing Company (BA, +0.61%). Top loser - Apple Inc. (AAPL, -1.23%).

Most of S&P sectors also in negative area. Top gainer - Utilities (+0.3%). Top loser - Conglomerates (-2.9%).

At the moment:

Dow 18540.00 0.00 0.00%

S&P 500 2182.25 +0.50 +0.02%

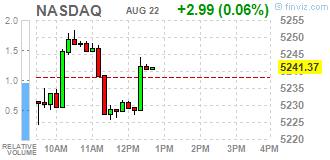

Nasdaq 100 4809.50 +2.50 +0.05%

Oil 47.68 -1.43 -2.91%

Gold 1343.80 -2.40 -0.18%

U.S. 10yr 1.54 -0.04

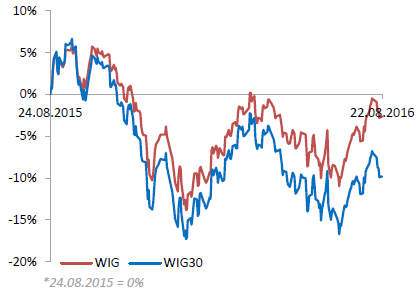

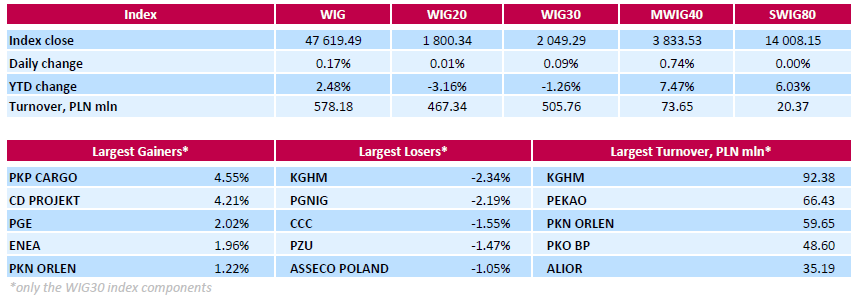

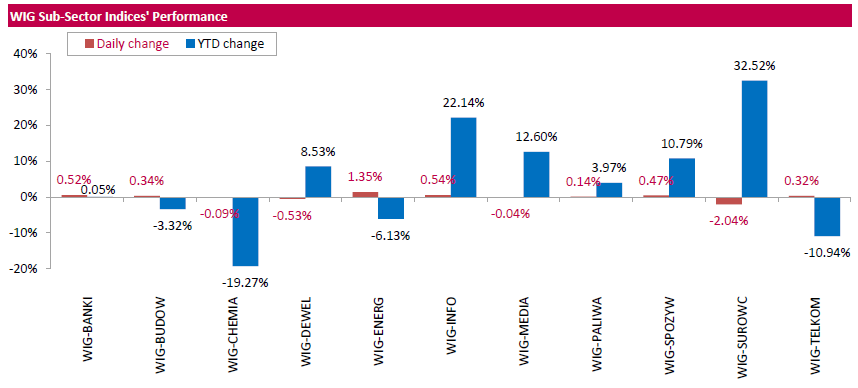

Polish equity market closed higher on Monday. The broad market measure, the WIG index, advanced by 0.17%. Sector performance within the WIG Index was mixed. Utilities (+1.35%) outperformed, while materials (-2.04%) lagged behind.

The large-cap stocks' measure, the WIG30 Index, inched up 0.09%. In the index basket, railway freight transport operator PKP CARGO (WSE: PKP) and videogame developer CD PROJEKT (WSE: CDR) generated the biggest advances, soaring by 4.55% and 4.21% respectively. Other major gainers were oil refiner PKN ORLEN (WSE: PKN), two gencos ENEA (WSE: ENA) and PGE (WSE: PGE) as well as two banking sector names ING BSK (WSE: ING) and ALIOR (WSE: ALR), adding between 1.11% and 2.02%. On the other side of the ledger, copper producer KGHM (WSE: KGH) led the decliners, dropping by 2.34% on news Poland's 2017 draft budget envisages that mining tax, paid almost solely by the state-controlled KGHM, will stay in place next year. It was followed by oil and gas producer PGNIG (WSE: PGN), footwear retailer CCC (WSE: CCC) and insurer PZU (WSE: PZU), sliding by 2.19%, 1.55% and 1.47% respectively.

Afternoon trading phase brought a deeper decline in Euroland and the bulls on the Warsaw market may boast relative strength to the European stock exchanges where the German DAX clearly went under the line, going directly to the support area 10,400-10,500 points.

Thus begins to materialize the negative scenario of evolving in the environment correction, even though the session is not over yet.

At the beginning of the US session the mood generated by European investors has prompted Americans to start trading with somewhat lower levels.

U.S. stock-index futures slipped with crude oil, amid increased speculation that interest rates may rise this year after Federal Reserve Vice Chairman Stanley Fischer said the economy was close to meeting the central bank's goals.

Global Stocks:

Nikkei 16,598.19 +52.37 +0.32%

Hang Seng 22,997.91 +60.69 +0.26%

Shanghai 3,084.76 -23.34 -0.75%

FTSE 6,831.03 -27.92 -0.41%

CAC 4,394.17 -6.35 -0.14%

DAX 10,487.54 -56.82 -0.54%

Crude $48.08 (-2.10%)

Gold $1341.40 (-0.36%)

(company / ticker / price / change ($/%) / volume)

| 3M Co | MMM | 179.61 | 0.00(0.00%) | 65986 |

| ALCOA INC. | AA | 10.22 | -0.05(-0.4869%) | 95529 |

| ALTRIA GROUP INC. | MO | 66.57 | 0.24(0.3618%) | 978 |

| Amazon.com Inc., NASDAQ | AMZN | 756.75 | -0.56(-0.0739%) | 4287 |

| American Express Co | AXP | 65.53 | 0.00(0.00%) | 161700 |

| AMERICAN INTERNATIONAL GROUP | AIG | 58.74 | -0.12(-0.2039%) | 6100 |

| Apple Inc. | AAPL | 109.35 | -0.01(-0.0091%) | 23161 |

| AT&T Inc | T | 40.95 | -0.06(-0.1463%) | 5955 |

| Barrick Gold Corporation, NYSE | ABX | 20.3 | -0.31(-1.5041%) | 83088 |

| Boeing Co | BA | 134.44 | 0.00(0.00%) | 24683 |

| Caterpillar Inc | CAT | 83.5 | -0.34(-0.4055%) | 937 |

| Chevron Corp | CVX | 101.26 | -1.06(-1.036%) | 686 |

| Cisco Systems Inc | CSCO | 30.47 | -0.05(-0.1638%) | 3790 |

| Citigroup Inc., NYSE | C | 46.4 | -0.13(-0.2794%) | 6765 |

| Deere & Company, NYSE | DE | 86.79 | -0.53(-0.607%) | 13635 |

| E. I. du Pont de Nemours and Co | DD | 69.9 | 0.12(0.172%) | 150 |

| Exxon Mobil Corp | XOM | 87.3 | -0.50(-0.5695%) | 7337 |

| Facebook, Inc. | FB | 123.57 | 0.01(0.0081%) | 65209 |

| FedEx Corporation, NYSE | FDX | 168.63 | 0.00(0.00%) | 464 |

| Ford Motor Co. | F | 12.4 | 0.01(0.0807%) | 29200 |

| Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 11.73 | -0.24(-2.005%) | 111783 |

| General Electric Co | GE | 31.23 | -0.02(-0.064%) | 12977 |

| General Motors Company, NYSE | GM | 31.9 | 0.07(0.2199%) | 1200 |

| Goldman Sachs | GS | 166.07 | -0.16(-0.0962%) | 9447 |

| Google Inc. | GOOG | 775.42 | 0.00(0.00%) | 641 |

| Hewlett-Packard Co. | HPQ | 14.47 | 0.05(0.3467%) | 121099 |

| Home Depot Inc | HD | 135.47 | 0.01(0.0074%) | 255 |

| HONEYWELL INTERNATIONAL INC. | HON | 116.04 | -0.07(-0.0603%) | 41128 |

| Intel Corp | INTC | 35.15 | -0.09(-0.2554%) | 3917 |

| International Business Machines Co... | IBM | 160 | -0.04(-0.025%) | 1016 |

| International Paper Company | IP | 47.15 | -0.31(-0.6532%) | 132 |

| Johnson & Johnson | JNJ | 119.92 | 0.00(0.00%) | 3602 |

| JPMorgan Chase and Co | JPM | 66 | 0.14(0.2126%) | 5735 |

| McDonald's Corp | MCD | 114.81 | -0.20(-0.1739%) | 490 |

| Merck & Co Inc | MRK | 63.44 | 0.08(0.1263%) | 400 |

| Microsoft Corp | MSFT | 57.5 | -0.12(-0.2083%) | 726 |

| Nike | NKE | 58.92 | 0.02(0.034%) | 655206 |

| Pfizer Inc | PFE | 34.64 | -0.34(-0.972%) | 74852 |

| Procter & Gamble Co | PG | 87.3 | -0.01(-0.0114%) | 194119 |

| Starbucks Corporation, NASDAQ | SBUX | 54.86 | -0.08(-0.1456%) | 5362 |

| Tesla Motors, Inc., NASDAQ | TSLA | 224.35 | -0.65(-0.2889%) | 4789 |

| The Coca-Cola Co | KO | 44 | 0.08(0.1821%) | 859 |

| Travelers Companies Inc | TRV | 117.47 | 0.00(0.00%) | 173163 |

| Twitter, Inc., NYSE | TWTR | 18.99 | 0.01(0.0527%) | 17893 |

| United Technologies Corp | UTX | 109.14 | 0.00(0.00%) | 79089 |

| UnitedHealth Group Inc | UNH | 142.04 | 0.00(0.00%) | 36927 |

| Verizon Communications Inc | VZ | 52.48 | 0.03(0.0572%) | 218838 |

| Visa | V | 80.63 | 0.16(0.1988%) | 147684 |

| Wal-Mart Stores Inc | WMT | 72.89 | 0.08(0.1099%) | 5050 |

| Walt Disney Co | DIS | 96.39 | -0.00(-0.00%) | 1593 |

| Yahoo! Inc., NASDAQ | YHOO | 42.94 | -0.08(-0.186%) | 1550 |

| Yandex N.V., NASDAQ | YNDX | 22.42 | -0.06(-0.2669%) | 1900 |

Upgrades:

Downgrades:

Other:

HP (HPQ) target raised to $14 from $12 at RBC Capital Mkts

Deere (DE) target raised to $80 from $72 at RBC Capital Mkts

In the first hour of trading the WIG20 index defended the level of support and started up inspired by similar attitude of surrounding. Unfortunately, the next trading hours brought the return of part of earlier gains. A similar situation took place on the European markets. The Warsaw market easily gave a large part of the morning gains and the index WIG20 moved down at around the level of 1,800 points, which only briefly managed to halt the process of withdrawal. At the halfway point of the session the index of the largest companies stood at the level of 1,797 points (-0,18%) with the turnover close to PLN 200 mln.

European stocks mostly rise, getting support from the corporate news and a rise in price of shares of exporters in response to the weakening of the euro against the US dollar.

The dollar strengthened on recent statements by Fed Vice Chairman Stanley Fischer that the central bank is still considering the possibility of a rate hike in 2016. He also noted that the US economy is already close to objectives and will continue to gain momentum. "I look forward to at the accelerating growth of GDP in the coming quarters on the background of recovery in investment after unexpectedly weak performance, as well as reducing the effect of the strengthening of the dollar which occurred earlier," - said Fisher, but did not give precise forecasts on rates. Later this week, the focus will be the speech of the Fed's Janet Yellen at Jackson Hole. In her statement may signal whether the economy is strong enough and could afford a rate hike in September or in the coming months. According to the futures market, the probability of a Fed rate hike is 12% in September and in December is estimated at 39.1%.

The composite index of Europe's largest enterprises, Stoxx 600 added 0.4 percent. Recall, at the end of last week, the index recorded the biggest drop since the beginning of June. The trading volume today is 37 percent lower than the average for the last 30 days. Strategists expect the index to bring its annual decline to 8.6 percent. Meanwhile, the report of Bank of America Corp. showed that investors continued to withdraw money from funds in the region, extending this series to 28 consecutive weeks.

Bank shares rebounded after the bigest fall in two weeks, while the shares of exporters, including automakers, rose against the euro weakness. Shares of mining companies shows a negative trend, due to the fall in commodity prices due to the strengthening of the dollar.

Shares of Syngenta AG - a Swiss chemical company - jumped 11 percent, the largest increase in more than a year. Today, China National Chemical Corp reported that the US National Security officials approved the merger with Syngenta AG.

The cost of Teleperformance SA rose 6.5 percent after the call-center operator agreed to buy LanguageLine Solutions LLC for $ 1.5 billion to expand in the US market.

Quotes of Kingspan Group Plc climbed 6.2 percent, as the Irish manufacturer of building insulation panels reported a 19 percent increase in revenues in the first half of the year.

At the moment:

FTSE 100 6827.27 -31.68 -0.46%

DAX +3.11 10547.47 + 0.03%

CAC 40 +2.45 4402.97 + 0.06%

WIG20 index opened at 1799.87 points (-0.02%)*

WIG 47513.29 -0.05%

WIG30 2045.04 -0.12%

mWIG40 3814.26 0.23%

*/ - Change to Previous Close

The futures market (FW20U1620) began a new week from discount of 0.22% to 1,804 points. The contract for the German DAX lost 0.4% at the opening. The cash market (WIG20) opened with a modest discount of -0.02% to 1,799 points at a fairly low turnover. Very little is needed to go down and this is the main risk for today's session. At this stage it means continuation of the direction seen in the past few days.

The moods in the morning are not particularly beneficial, because in Asia dominate declines and contracts in the US lose on the value. These changes are not big, although the situation of the bulls will not be much improved.

On the Warsaw market in the past week, each session brought declines, although the main European indices as well as Wall Street presented a stronger stance. This paints a very disturbing picture indicating a prompt return of local weaknesses as well signaled last week by restatement of energy companies. Investors did not like the results of larger companies of which the latest example was Eurocash (WSE: EUR). It seems that if the correction in the environment will start the WSE may develop the declines of the past week. So far, the market (the WIG20 index) was at 1,800 pts., which means support, prevents access to the next psychological barrier of 1,750 points.

This week will bring more consequential information, but this day will be quiet in this regard. Also macro calendar remains empty and only tomorrow's preliminary PMI readings may somewhat enliven the atmosphere. Investors in recent days live mainly in words of members of the Federal Reserve, who began to signal the possibility of the September rate hike.

Markets news said that the German government encourages citizens to take inventory in the event of a crisis. Of course this is just the kind of exercise, but who knows if some does not see a real threat behind it. Perhaps this message is behind the decline in Eurodollar. A pair of EURUSD lose the morning approx. 0,45%

European stocks fell Friday, with Italian shares leading the charge lower as concerns over the country's banking system sent lenders lower across the eurozone.

The Stoxx Europe 600 SXXP, -0.81% lost 0.8% to close at 340.14, extending its weekly loss to 1.7%.

U.K. stocks and the British pound declined on Friday after a news report suggested Prime Minister Theresa May is "sympathetic: to starting Brexit talks with the European Union by April at the latest.

The FTSE 100 UKX, -0.15% finished 0.2% lower at 6,858.95, erasing a 0.1% gain from Thursday.

U.S. stocks finished lower Friday as investors worried about whether the Federal Reserve will raise interest rates sooner rather than later.

But the Nasdaq Composite managed to notch its eighth consecutive weekly gain, marking the longest such stretch for the tech-laden index since April 23, 2010, according to Dow Jones data.

Few catalysts and the expiration of August options contracts contributed to fairly lackluster moves during a week that has offered little guidance for investors about the Fed's policy plans, following the release on Wednesday of minutes from the central bank's July meeting.

Asian shares slipped on Monday and the dollar pulled away from last week's lows on expectations that a signal might emerge from a Federal Reserve gathering this week in Jackson Hole, Wyoming that the U.S. central bank is gearing up to hike interest rates.

Global central bankers will join the annual mountain retreat that opens on Thursday, with Fed Chair Janet Yellen due to speak the following day.

On Sunday, Fed Vice Chairman Stanley Fischer gave a generally upbeat assessment of the U.S. economy's current strength in prepared remarks, saying the job market was close to full strength and still improving.

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers