- Analytics

- News and Tools

- Market News

Analytics, News, and Forecasts for CFD Markets: stock news — 26-07-2017.

(index / closing price / change items /% change)

Nikkei +94.96 20050.16 +0.48%

TOPIX +3.81 1620.88 +0.24%

Hang Seng +88.97 26941.02 +0.33%

CSI 300 -14.17 3705.39 -0.38%

Euro Stoxx 50 +17.65 3491.19 +0.51%

FTSE 100 +17.50 7452.32 +0.24%

DAX +40.80 12305.11 +0.33%

CAC 40 +29.09 5190.17 +0.56%

DJIA +97.58 21711.01 +0.45%

S&P 500 +0.70 2477.83 +0.03%

NASDAQ +10.57 6422.75 +0.16%

S&P/TSX -30.98 15171.39 -0.20%

The main stock indexes of Wall Street finished the session above the zero mark, receiving a boost from confident corporate profits.

In addition, some influence on the dynamics of trading was provided by data on the US housing market and the results of a two-day meeting of the Federal Reserve.

The Commerce Department reported that in June, sales of new homes in the US rose for the second consecutive month, as purchases in the West rose to nearly a 10-year high, but a serious shortage of real estate remains an obstacle to a robust recovery in the housing market. Sales of new buildings rose by 0.8% to a seasonally adjusted annual level of 610,000 units. The pace of sales for May was revised to 605,000 units from 610,000 units.

As for the Fed meeting, as expected, the Central Bank left the range of interest rates on federal funds unchanged, between 1.00% and 1.25%. This decision was taken unanimously (9 members of the FOMC voted "for"). The FOMC Accompanying Statement reported that the process of reducing the balance will begin "pretty soon." In general, the Fed management did not make it clear that weak inflation data changed their plans for another rate increase this year. "The situation on the labor market continued to improve. The growth of jobs is "strong", the unemployment rate has declined, "the FOMC statement said. - Economic activity "is growing at a moderate pace." The costs of households and companies also continued to grow. Short-term risks for the economy, in general, are "balanced". "

Oil prices rose by more than 1.5%, reaching an almost 8-week high, as a significant drop in US oil inventories reinforced expectations that the long-oversaturated market is moving toward a balance of supply and demand. The US Energy Ministry reported that US oil inventories fell sharply last week, as refineries increased their workload. In addition, there was a reduction in gasoline stocks and distillate stocks.

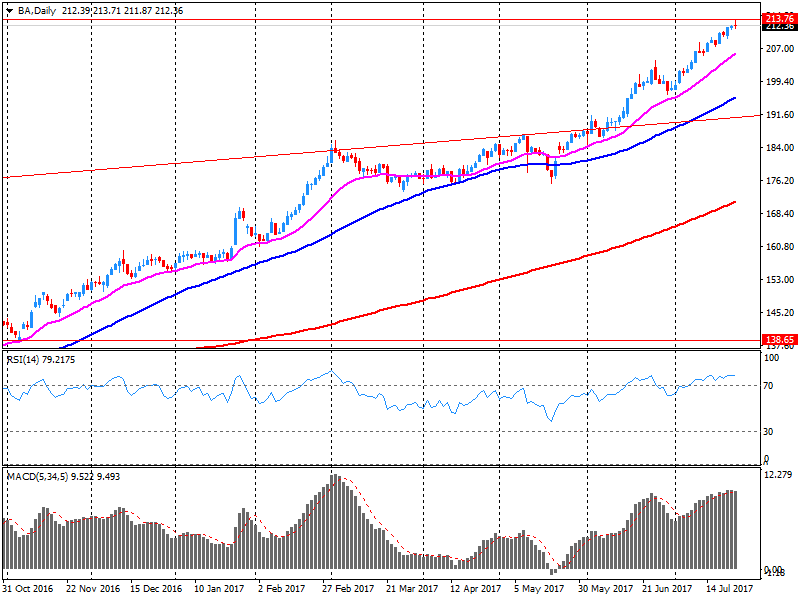

Components of the DOW index finished trades in different directions (17 in negative territory, 13 in positive territory). The leader of growth was the shares of The Boeing Company (BA, + 9.56%). Outsider were the shares of Cisco Systems, Inc. (CSCO, -1.75%).

Most sectors of the S & P recorded a rise. The utilities sector grew most (+ 0.5%). The health sector showed the greatest decline (-0.3%).

At closing:

DJIA + 0.45% 21,710.12 +96.69

Nasdaq + 0.16% 6,422.75 +10.58

S & P + 0.03% 2.477.83 + 0.70

U.S. stock-index futures were higher as investors digested another batch of earnings and awaited the Fed's latest policy decision.

Global Stocks:

Nikkei 20,050.16 +94.96 +0.48%

Hang Seng 26,941.02 +88.97 +0.33%

Shanghai 3,247.58 +3.89 +0.12%

S&P/ASX 5,776.63 +50.03 +0.87%

FTSE 7,466.44 +31.62 +0.43%

CAC 5,188.24 +27.16 +0.53%

DAX 12,299.68 +35.37 +0.29%

Crude $48.38 (+1.02%)

Gold $1,247.10 (-0.40%)

(company / ticker / price / change ($/%) / volume)

| 3M Co | MMM | 200.8 | 1.41(0.71%) | 2117 |

| ALCOA INC. | AA | 37.42 | 0.12(0.32%) | 212 |

| Amazon.com Inc., NASDAQ | AMZN | 1,045.00 | 5.13(0.49%) | 11717 |

| Apple Inc. | AAPL | 153.35 | 0.61(0.40%) | 38884 |

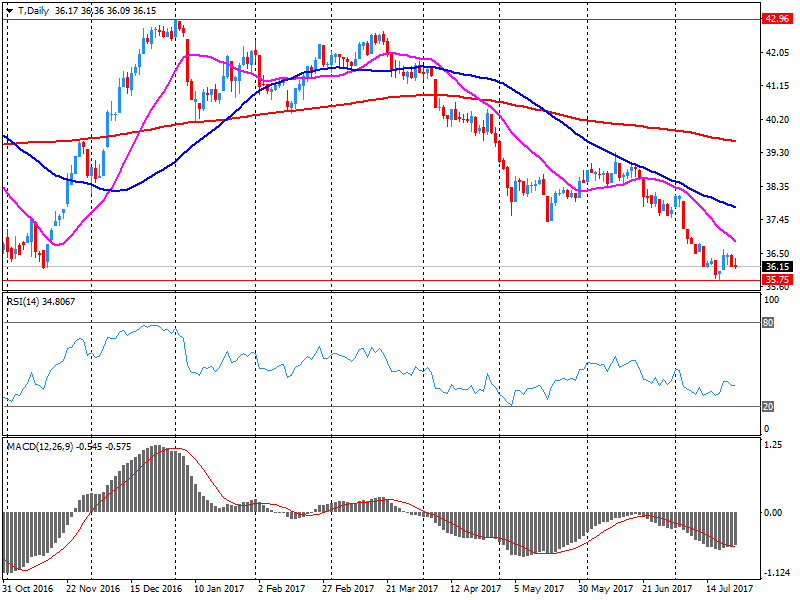

| AT&T Inc | T | 37.48 | 1.26(3.48%) | 734345 |

| Barrick Gold Corporation, NYSE | ABX | 15.94 | -0.10(-0.62%) | 67443 |

| Boeing Co | BA | 219.85 | 7.39(3.48%) | 123088 |

| Caterpillar Inc | CAT | 114.23 | -0.31(-0.27%) | 4568 |

| Chevron Corp | CVX | 104.79 | 0.40(0.38%) | 553 |

| Cisco Systems Inc | CSCO | 32.1 | -0.02(-0.06%) | 1755 |

| Citigroup Inc., NYSE | C | 68.25 | 0.22(0.32%) | 18531 |

| Deere & Company, NYSE | DE | 128.45 | 0.55(0.43%) | 2503 |

| Exxon Mobil Corp | XOM | 80.68 | 0.41(0.51%) | 2727 |

| Facebook, Inc. | FB | 165.85 | 0.57(0.34%) | 98195 |

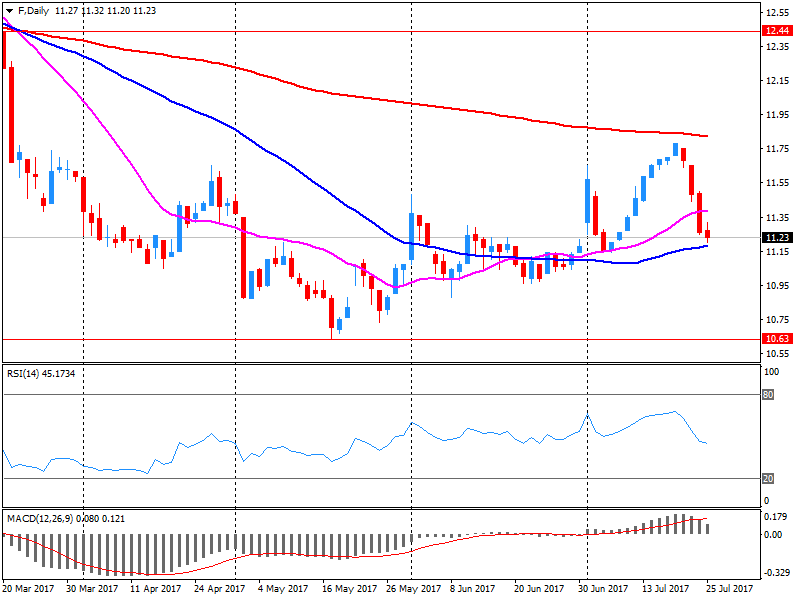

| Ford Motor Co. | F | 11.11 | -0.16(-1.42%) | 2541142 |

| Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 14.61 | -0.26(-1.75%) | 127164 |

| General Electric Co | GE | 25.55 | 0.11(0.43%) | 20711 |

| General Motors Company, NYSE | GM | 35.5 | -0.07(-0.20%) | 2680 |

| Goldman Sachs | GS | 222.24 | 0.66(0.30%) | 1253 |

| Google Inc. | GOOG | 952.78 | 2.08(0.22%) | 2773 |

| Home Depot Inc | HD | 146.72 | -0.25(-0.17%) | 555 |

| Intel Corp | INTC | 34.73 | 0.06(0.17%) | 1949 |

| International Business Machines Co... | IBM | 147 | 0.81(0.55%) | 342 |

| JPMorgan Chase and Co | JPM | 93 | 0.20(0.22%) | 4228 |

| McDonald's Corp | MCD | 158.92 | -0.15(-0.09%) | 1788 |

| Microsoft Corp | MSFT | 74.31 | 0.12(0.16%) | 13722 |

| Starbucks Corporation, NASDAQ | SBUX | 58.85 | 0.30(0.51%) | 1206 |

| Tesla Motors, Inc., NASDAQ | TSLA | 340.91 | 1.31(0.39%) | 29093 |

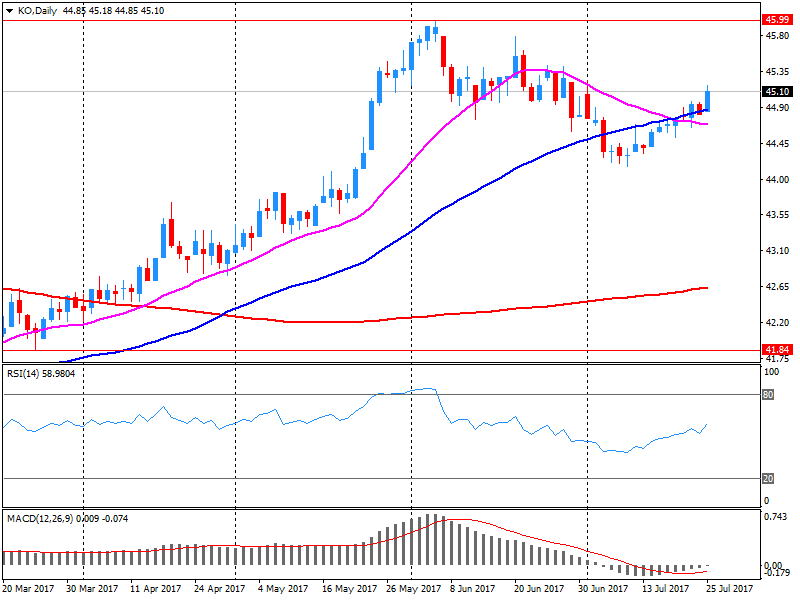

| The Coca-Cola Co | KO | 45.2 | -0.04(-0.09%) | 22763 |

| Twitter, Inc., NYSE | TWTR | 19.9 | -0.07(-0.35%) | 25788 |

| United Technologies Corp | UTX | 120.5 | 0.08(0.07%) | 655 |

| Verizon Communications Inc | VZ | 44.89 | 0.91(2.07%) | 205317 |

| Wal-Mart Stores Inc | WMT | 78.54 | 0.02(0.03%) | 801 |

Boeing (BA) reported Q2 FY 2017 earnings of $2.55 per share (versus -$0.44 in Q2 FY 2016), beating analysts' consensus estimate of $2.31.

The company's quarterly revenues amounted to $22.739 bln (-8.1% y/y), missing analysts' consensus estimate of $22.972 bln.

The company also issued guidance for FY 2017, raising EPS to $9.80-10.00 from $9.20-9.40 (versus analysts' consensus estimate of $9.40) and reaffirming FY 2017 revenues of $90.5-92.5 bln (versus analysts' consensus estimate of $92 bln).

BA rose to $219.47 (+3.30%) in pre-market trading.

Coca-Cola (KO) reported Q2 FY 2017 earnings of $0.59 per share (versus $0.60 in Q2 FY 2016), beating analysts' consensus estimate of $0.57.

The company's quarterly revenues amounted to $9.702 bln (-15.9% y/y), generally in-line with analysts' consensus estimate of $9.618 bln.

KO rose to $45.50 (+0.57%) in pre-market trading.

Ford Motor (F) reported Q2 FY 2017 earnings of $0.51 per share (versus $0.52 in Q2 FY 2016), beating analysts' consensus estimate of $0.43.

The company's quarterly revenues amounted to $36.932 bln (-0.5% y/y), generally in-line with analysts' consensus estimate of $37.219 bln.

The company also issued upside guidance for FY 2017, projecting EPS of $1.65-1.85 versus analysts' consensus estimate of $1.51.

F fell to $11.25 (-0.18%) in pre-market trading.

AT&T (T) reported Q2 FY 2017 earnings of $0.79 per share (versus $0.72 in Q2 FY 2016), beating analysts' consensus estimate of $0.74.

The company's quarterly revenues amounted to $39.837 bln (-1.6% y/y), in-line with analysts' consensus estimate of $39.838 bln.

The company also said it continued to expect the Time Warner (TWX) deal to close by year-end and further transform the company.

T rose to $37.25 (+2.84%) in pre-market trading.

European stocks closed higher Tuesday, with bank stocks gaining ground as investors assessed upbeat developments from Germany and Greece. The Stoxx Europe 600 SXXP, +0.41% tacked on 0.4% to finish at 380.77, rebounding after the benchmark on Monday closed lower by 0.2%. In Frankfurt, the DAX 30 DAX, +0.45% was higher by 0.5% at 12,264.31, holding to gains after the closely watched Ifo Institute described German companies as "euphoric". The widely watched Ifo index of business sentiment in Europe's largest economy surged to a record high of 116.0 in July.

Asian shares gave up earlier gains Wednesday, though Japanese and Australian stocks outperformed, helped by an improvement in appetite for risk, which pushed the U.S. dollar and commodity prices higher overnight. Commodities led the charge in European and U.S. trading on Tuesday, with copper prices jumping 4% and oil rising more than 3%. That's particularly good for Australian stocks, where a big market segment is mining and energy companies.

The S&P 500 and Nasdaq on Tuesday notched fresh all-time highs as Wall digested an array of better-than-expected corporate-results. The Dow Jones Industrial Average DJIA, +0.47% closed up 100 points, or 0.5%, but the blue-chip average's advance was limited by a plunge in shares of component 3M Co. MMM, -5.05% which marked its sharpest-ever net drop on a dollar-basis on record, off $10.61, or down 5.1%, according to WSJ Market Data Group, tracking data going back to 1972.

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers