- Analytics

- News and Tools

- Market News

Analytics, News, and Forecasts for CFD Markets: stock news — 30-08-2016.

(index / closing price / change items /% change)

Nikkei 225 16,725.36 -12.13 -0.07%

Shanghai Composite 3,076.20 +6.17 +0.20%

S&P/ASX 200 5,478.29 +9.07 +0.17%

FTSE 100 6,820.79 -17.26 -0.25%

CAC 40 4,457.49 +33.24 +0.75%

Xetra DAX 10,657.64 +113.20 +1.07%

S&P 500 2,176.12 -4.26 -0.20%

Dow Jones Industrial Average 18,454.30 -48.69 -0.26%

S&P/TSX Composite 14,684.85 +2.88 +0.02%

Major stock indexes in Wall Street declined slightly, as investors are waiting for a catalyst that will move the markets, while maintaining a focus on the timing of the next rate hike.

Investors expect the monthly data on the number of jobs on Friday to assess whether they are comparable to the statements by the Fed. According to forecasts, the number of people employed in non-agricultural sectors of the economy increased in August by 185 thousand. After increasing by 255 thousand. In July. The unemployment rate is likely to decline to 4.8% from 4.9%. Meanwhile, the growth rate of the average hourly rate is estimated to have slowed to 0.2% from 0.3%.

However, today's report from S & P / Case-Shiller showed that the national index of housing prices in the US rose by 5.1% annually in June, unchanged from the previous month. A composite index for the 10 megacities US reported an annual growth of 4.3%, compared with 4.4% in the previous month.

In addition, it was reported that the consumer confidence index from the Conference Board, which decreased slightly in July, increased in August. The index is currently 101.1 compared to 96.7 in July. the present situation index rose to 118.8 from 123.0, while the expectations index rose to 82.0 last month to 86.4.

Most components of the DOW index finished trading in negative territory (24 of 30). Outsider were shares of The Boeing Company (BA, -1.60%). More rest up shares The Goldman Sachs Group, Inc. (GS, + 1.16%).

Most of the S & P sectors showed a decline. Most utilities sector fell (-0.9%). The leader turned out to be the financial sector (+ 0.6%).

At the close:

Dow -0.26% 18,454.30 -48.69

Nasdaq -0.18% 5,222.99 -9.34

S & P -0.19% 2,176.13 -4.25

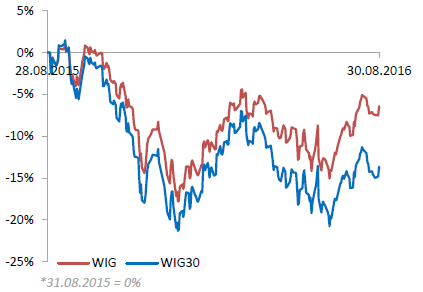

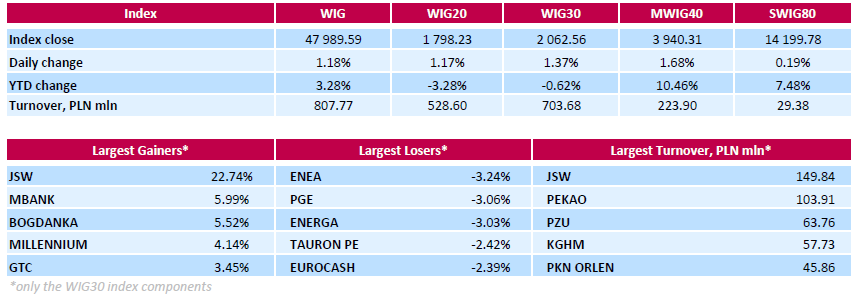

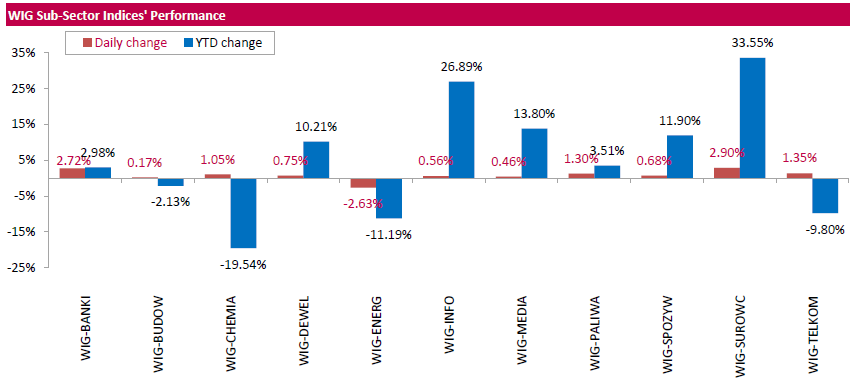

Polish equity market closed higher on Tuesday. The broad market measure, the WIG Index, rose by 1.18%. Utilities sector (-2.63%) was sole decliner within the WIG Index, while materials (+2.90%) outpaced.

The large-cap stocks' measure, the WIG30 Index, surged by 1.37%. Coking coal miner JSW (WSE: JSW) was the standout performer in the WIG30 Index basket, skyrocketing by 22.74% on announcement the company had agreed with its bondholders to extend the payments from JSW's bond by five years until 2025. The agreement concerns two JSW bonds worth PLN 700 mln and $164 mln, respectively. Other notable gainers were three banking names MBANK (WSE: MBK), MILLENNIUM (WSE: MIL) and PEKAO (WSE: PEO), thermal coal miner BOGDANKA (WSE: LWB) and property developer GTC (WSE: GTC), advancing by 3.35%-5.99%. On the other side of the ledger, four utilities names ENEA (WSE: ENA), PGE (WSE: PGE), ENERGA (WSE: EMG) and TAURON PE (WSE: TPE) recorded the biggest declines, tumbling by 2.42%-3.24%.

Major U.S. stock-indexes little changed on Tuesday morning as investors looked for catalysts to drive the markets while keeping one eye on clues for the timing of the next interest rate hike. Federal Reserve Chair Janet Yellen painted a rosy picture of the U.S. economy at an economic symposium on Friday and said the case for a rate hike was strengthening, but gave little indication on when the central bank could move. Investors are awaiting a report on monthly payrolls data due on Friday to assess whether it supports the hawkish tone that Fed officials have taken.

Most of Dow stocks in negative area (23 of 30). Top gainer - JPMorgan Chase & Co. (JPM, +0.28%). Top loser - The Boeing Company (BA, -1.51%).

Most of S&P sectors also in negative area. Top gainer - Conglomerates (+0.4%). Top loser - Utilities (-0.7%).

At the moment:

Dow 18447.00 -42.00 -0.23%

S&P 500 2174.75 -4.50 -0.21%

Nasdaq 100 4778.00 -15.25 -0.32%

Oil 46.45 -0.53 -1.13%

Gold 1321.40 -5.70 -0.43%

U.S. 10yr 1.57 +0.00

Increases in indices of the Warsaw Stock Exchange as for now persist, which goes hand in hand with more or less the same behavior of European markets. However, while an increase of more than 1% of the WIG20 index after two weeks of weakness is not surprising, as much similar achievements of medium companies, which for the last two months were not practically down, it is an admirable result. In the afternoon phase of the session was a noticeable weakening in the market of the zloty, which began to weaken against major currencies.

The opening of trading in the US was held at neutral, and at the moment, has no influence into the picture of the situation on the Warsaw market. An hour before the end of listing the WIG 20 index rising by 1.28% (1,800 pts).

U.S. stock-index futures were little changed as investors awaited jobs data due this week for further clues on the path of Federal Reserve policy.

Global Stocks:

Nikkei 16,725.36 -12.13 -0.07%

Hang Seng 23,016.11 +194.77 +0.85%

Shanghai 3,076.20 +6.17 +0.20%

FTSE 6,836.58 -1.47 -0.02%

CAC 4,461.66 +37.41 +0.85%

DAX 10,649.07 +104.63 +0.99%

Crude $47.34 (+0.77%)

Gold $1322.80 (-0.32%)

(company / ticker / price / change ($/%) / volume)

| 3M Co | MMM | 180.5 | 0.00(0.00%) | 65021 |

| ALCOA INC. | AA | 10.24 | -0.02(-0.1949%) | 4800 |

| ALTRIA GROUP INC. | MO | 66.25 | 0.15(0.2269%) | 250 |

| Amazon.com Inc., NASDAQ | AMZN | 770.89 | -0.40(-0.0519%) | 4236 |

| American Express Co | AXP | 65.67 | 0.15(0.2289%) | 201 |

| AMERICAN INTERNATIONAL GROUP | AIG | 59.43 | 0.00(0.00%) | 49499 |

| Apple Inc. | AAPL | 105.65 | -1.17(-1.0953%) | 783832 |

| AT&T Inc | T | 41.1 | 0.10(0.2439%) | 1030 |

| Barrick Gold Corporation, NYSE | ABX | 18.23 | -0.16(-0.87%) | 90918 |

| Boeing Co | BA | 132.9 | 0.00(0.00%) | 32734 |

| Caterpillar Inc | CAT | 83.15 | 0.05(0.0602%) | 700 |

| Chevron Corp | CVX | 102.05 | 0.00(0.00%) | 92351 |

| Cisco Systems Inc | CSCO | 31.69 | 0.11(0.3483%) | 3378 |

| Citigroup Inc., NYSE | C | 47.26 | -0.00(-0.00%) | 8913 |

| Deere & Company, NYSE | DE | 87.1 | 0.17(0.1956%) | 550 |

| E. I. du Pont de Nemours and Co | DD | 70.45 | 0.00(0.00%) | 23195 |

| Exxon Mobil Corp | XOM | 87.84 | 0.00(0.00%) | 1322210 |

| Facebook, Inc. | FB | 126.48 | -0.06(-0.0474%) | 70677 |

| FedEx Corporation, NYSE | FDX | 165.17 | 0.00(0.00%) | 63982 |

| Ford Motor Co. | F | 12.5 | 0.03(0.2406%) | 15700 |

| Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 10.98 | -0.00(-0.00%) | 47225 |

| General Electric Co | GE | 31.37 | 0.01(0.0319%) | 3997 |

| General Motors Company, NYSE | GM | 31.81 | 0.00(0.00%) | 115012 |

| Goldman Sachs | GS | 166.36 | 0.14(0.0842%) | 456 |

| Google Inc. | GOOG | 771.7 | -0.45(-0.0583%) | 992 |

| Hewlett-Packard Co. | HPQ | 14.4 | -0.03(-0.2079%) | 700 |

| Home Depot Inc | HD | 134.73 | 0.18(0.1338%) | 260 |

| HONEYWELL INTERNATIONAL INC. | HON | 117.17 | 0.00(0.00%) | 30476 |

| Intel Corp | INTC | 35.55 | -0.00(-0.00%) | 1025 |

| International Business Machines Co... | IBM | 159.72 | 0.00(0.00%) | 157285 |

| International Paper Company | IP | 48.9 | 0.00(0.00%) | 16161 |

| Johnson & Johnson | JNJ | 119.92 | 0.00(0.00%) | 160 |

| JPMorgan Chase and Co | JPM | 67 | 0.05(0.0747%) | 2251 |

| McDonald's Corp | MCD | 115.5 | 0.98(0.8557%) | 24260 |

| Merck & Co Inc | MRK | 63.01 | 0.00(0.00%) | 82910 |

| Microsoft Corp | MSFT | 58.1 | -0.00(-0.00%) | 14506 |

| Nike | NKE | 58.5 | -0.13(-0.2217%) | 950 |

| Pfizer Inc | PFE | 35.05 | -0.06(-0.1709%) | 407 |

| Procter & Gamble Co | PG | 88.3 | 0.00(0.00%) | 113281 |

| Starbucks Corporation, NASDAQ | SBUX | 56.6 | -0.20(-0.3521%) | 119 |

| Tesla Motors, Inc., NASDAQ | TSLA | 215.5 | 0.30(0.1394%) | 3064 |

| The Coca-Cola Co | KO | 43.54 | 0.00(0.00%) | 388855 |

| Travelers Companies Inc | TRV | 118.48 | 0.00(0.00%) | 11316 |

| Twitter, Inc., NYSE | TWTR | 18.57 | 0.10(0.5414%) | 18930 |

| United Technologies Corp | UTX | 107.97 | 0.00(0.00%) | 24409 |

| UnitedHealth Group Inc | UNH | 137.27 | 0.00(0.00%) | 83486 |

| Verizon Communications Inc | VZ | 52.62 | 0.12(0.2286%) | 620 |

| Visa | V | 80.82 | -0.05(-0.0618%) | 520 |

| Wal-Mart Stores Inc | WMT | 71.4 | 0.00(0.00%) | 1000 |

| Walt Disney Co | DIS | 94.9 | 0.03(0.0316%) | 447 |

| Yahoo! Inc., NASDAQ | YHOO | 42.31 | 0.05(0.1183%) | 1500 |

| Yandex N.V., NASDAQ | YNDX | 22.22 | 0.00(0.00%) | 200 |

Upgrades:

McDonald's (MCD) upgraded to Outperform from Neutral at Robert W. Baird; target raised to $128 from $126

Downgrades:

Other:

The positive hero of today's session on the Warsaw market is the coal company JSW. After yesterday's quotations, the company announced an agreement with bondholders vs. repayment of the securities at PLN 1.3 billion. Today, the company's management presented the main assumptions of the restructuring of the JSW group and its results for the first half of the year. Till 2025, through the implementation of about 130 savings initiatives, the group is expected to reduce operating costs by a total of approx. PLN 1.6 billion (excluding the effects of the agreements with the bondholders in February and September 2015). As a result, the company's shares rise more than 18%. In conjunction with the good behavior of companies Sanok (WSE: SNK) and Forte (WSE: FTE) after the publication of the results it leads to rise of the mWIG40 to the new year's maximum. The index of blue chips supported today by stronger behavior of exchanges in Euroland and return to the game of investors from London also presents much better itself, reaching in the halfway point of today's trading the level of 1,800 points (+1,29%) with the turnover of PLN 286 mln.

European stocks are rising and can finish in positive territory for the second month in a row. Investors continue to assess the chances of a rate hike by the Federal Reserve.

According CME Group fed futures point to a 33% probability of a hike in September and 61% in December.

On Tuesday and Wednesday, market participants are waiting for statements by Stanley Fischer, who is a "hawk" among the leaders of the US Central Bank.

The composite index of the largest companies in the region Stoxx Europe 600 rose during trading 0,6% - to 345.13 points.

Shares of mining companies become cheaper amid lower prices for metals and strengthening of the US dollar. Stock prices of Antofagasta Plc, Randgold Resources Ltd. and Glencore Plc fell more than 3% in London trading, Rio Tinto - 4%.

The market value of Bunzl Plc increased by 1.5% due to an increase in quarterly revenue and operating profit margin.

Shares of the German sporting goods manufacturer Adidas and Dutch retailer Ahold Delhaize rose by 0.6%. In an estimated by LBBW analysts, both companies can be included in the index of the largest enterprises in the euro zone, replacing Carrefour and Unicredit.

Shares of German Wirecard rose by 4.1% as Barclays raised their rating.

Thyssenkrupp AG shares rose 0.6% on reports that the German company signed a contract for the manufacture, supply, installation and maintenance of more than 500 elevators and escalators for Qatar Doha Metro.

At the moment:

FTSE 6850.42 12.37 0.18%

DAX 10653.02 108.58 1.03%

CAC 4466.45 42.20 0.95%

WIG20 index opened at 1776.41 points (-0.05%)*

WIG 47442.34 0.03%

WIG30 2033.16 -0.07%

mWIG40 3886.26 0.28%

*/ - change to previous close

The futures market opened with an increase of 0.23% to 1,778 points.

The beginning of the session on the cash market (the WIG20 index) was without any major deviations of both the index and its components. At the same time, the European markets are gaining, indicating that is extremely hard to break our spot market out of stagnation.

Over the time we will probably also see something more about the turnover that after today's London return to the game should already be noticeably higher in relation to yesterday's level of activity. The beginning of trading is under the sign of continuing of improvement in sentiment after a little worse Friday on the Warsaw Stock Exchange.

Yesterday's trading on Wall Street ended with a rise in the broad S&P500 index by 0.5%. Most of this increase took place during the European session and will not be surprising for the early morning on these exchanges. It seems that investors are waiting for Friday's data from the US labor market, which will determine the likelihood of interest rate increases, however good behavior of the banking sector on Wall Street indicated that investors are betting a rate hike scenario.

Asian markets, excluding Japan, are dominated by the green color. The Japanese Nikkei, as well as contracts in the US, are currently traded on the light-cons, which should lead to a peaceful start of the European session.

Today's macro calendar is once again not too rich. More attention could attract only the consumer confidence index in the US, the Conference Board.

Today's morning trading on the currency market brings to maintain light pressure on the valuation of the zloty against foreign currency. The Polish zloty is valued by the market as follows: PLN 4,3407 per euro, PLN 3.8873 against the US dollar.

European stocks on Monday finished in negative territory, kicking off the week lower as rising expectations the U.S. Federal Reserve will lift interest rates later this year poked the air out of a recent rally.

The Stoxx Europe 600 index SXXP, -0.15% lost 0.2% to close at 343.20, pulling back after a 1.1% climb last week.

The pan-European benchmark settled 0.5% higher on Friday, after Fed Chairwoman Janet Yellen, at a closely watched speech at Jackson Hole, Wyo., said the U.S. economy is improving, seen as a sign of confidence in economic growth world-wide. However, the central-bank boss also hinted a rate increase is on the cards in coming months, which weighed on U.S. markets on Friday and dragged stocks in most of Asia and Europe lower on Monday.

U.S. stocks closed higher Monday, led higher by financial stocks as investors warmed up to the possibility of a Federal Reserve rate hike this year. The Dow Jones Industrial Average [ s: djia] closed up 107.59 points, or 0.6%, at 18,502.99, with Travelers Cos. TRV, +1.14% American Express Co AXP, +1.13% J.P. Morgan Chase & Co. JPM, +1.10% and DuPont DD, +1.15% all finishing up more than 1%. The S&P 500 Index SPX, +0.52% finished up 11.34 points, or 0.5%, at 2,180.38, as the financial sector gained 1%, followed by a rise in materials stocks. The Nasdaq Composite Index COMP, +0.26% rose 13.41 points, or 0.3%, to close at 5,232.33.

Asian shares bounced on Tuesday as doubts the Federal Reserve really would hike interest rates as soon as September restrained the dollar, while investors continued to count on more policy stimulus elsewhere in the world.

Japan's Nikkei .N225 went flat as the yen stopped falling following a sharp drop late last week.

A raft of Japanese data, from unemployment to retail sales, mostly beat analysts' forecasts but did nothing to change expectations the Bank of Japan would eventually have to ease further.

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers