- Analytics

- News and Tools

- Market News

Analytics, News, and Forecasts for CFD Markets: currency news — 18-10-2018.

| Pare | Closed | % change |

| EUR/USD | $1,1455 | -0,38% |

| GBP/USD | $1,3018 | -0,64% |

| USD/CHF | Chf0,99534 | +0,09% |

| USD/JPY | Y112,18 | -0,45% |

| EUR/JPY | Y128,61 | -0,75% |

| GBP/JPY | Y146,053 | -1,09% |

| AUD/USD | $0,7091 | -0,24% |

| NZD/USD | $0,6538 | -0,13% |

| USD/CAD | C$1,30575 | +0,28% |

"The labor market was quite strong in the month of September," said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute. "Although the goods producing sector struggled this month, we saw significant growth in many industries. Trade, for example, continued its steady growth adding the most jobs the sector has seen all year."

In the week ending October 13, the advance figure for seasonally adjusted initial claims was 210,000, a decrease of 5,000 from the previous week's revised level. The previous week's level was revised up by 1,000 from 214,000 to 215,000. The 4-week moving average was 211,750, an increase of 2,000 from the previous week's revised average. The previous week's average was revised up by 250 from 209,500 to 209,750.

Regional manufacturing activity continued to grow in October, according to results from this month's Manufacturing Business Outlook Survey. The survey's broad indicators for general activity, new orders, shipments, and employment remained positive and near their readings in September. The firms reported continued growth in employment and an increase in the average workweek this month. Expectations for the next six months remained optimistic.

The diffusion index for current general activity edged down slightly, from 22.9 in September to 22.2 this month.

-

Would be good if someone form Germany stood for top ECB job

Chris Beauchamp at IG wrote: "Despite a disappointing session in Asia, European markets have seen further buying pressure this morning, as the recovery from the lows continues. Dollar strength following on from last night's Fed minutes has arisen as the bank looks to maintain, and even increase, the pace of tightening, if only to give itself the room for manoeuvre necessary if the economy turns southwards in the coming two years. Markets appear to be viewing the Brexit negotiations with the same exhaustion as everyone else, as both sides play for time.

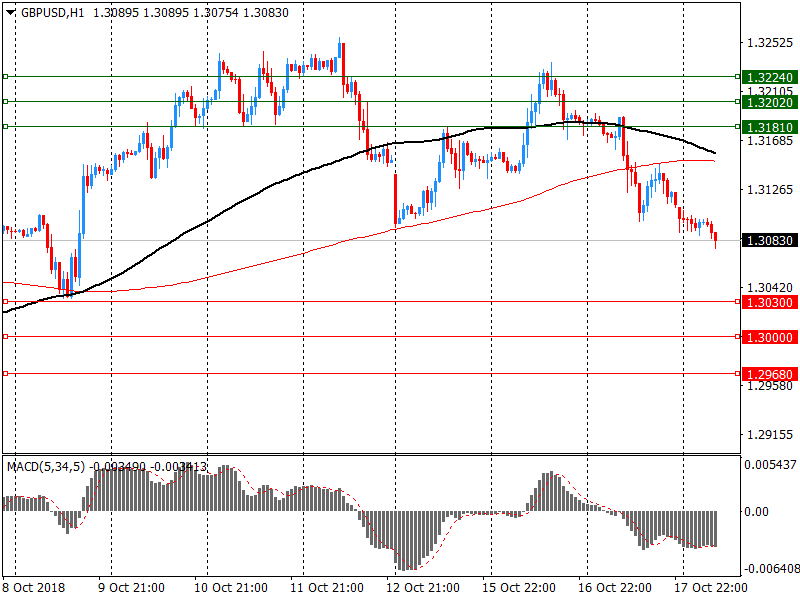

The risk of wandering into a 'no deal' scenario is still on the rise, with each missed deadline adding to the impression that neither side really knows what they want. Equity markets continue to digest the leap higher from Tuesday, but the put/call ratio continues to climb, indicating that investors have yet to start buying the dip in earnest.

The recent strength in UK consumer spending has come to a close, as retail sales fall 0.8% for September. But with sterling already down sharply over the past two days thanks to the weaker CPI figure and Brexit concerns the impact of this morning's reading has been muted."

In the three months to September 2018, the quantity bought in retail sales increased by 1.2% when compared with the previous three months, with strong sales in "other stores" and online retailing.

The increase of 3.9% for the quantity of goods bought in "other stores" for the three months to September 2018 was the largest overall contributor to the growth in total retail sales, due largely to strong growth in watches and jewellery stores.

In September 2018, the quantity bought declined by 0.8% when compared with August 2018, due mainly to a large fall of 1.5% in food stores; the largest decline in food store sales since October 2015.

When compared with September 2017, the quantity bought in September 2018 increased by 3.0%, with growth across all sectors except department stores.

Online sales as a proportion of all retailing fell slightly to 17.8% in September 2018 from the 18.0% reported

in August 2018, yet food stores and clothing stores both reported record proportions of internet retail at 5.8% and 18.2% respectively.

-

Still Some Issues Remaining On Backstop

-

Could Not Accept Intial EU Proposal

Japan posted a merchandise trade surplus of 139.6 billion yen in September, according to rttnews.

That exceeded expectations for a deficit of 45.1 billion yen following the 444.6 billion yen shortfall in August.

Exports were down 1.2 percent on year, shy of forecasts for an increase of 2.3 percent following the 6.6 percent gain in the previous month.

Imports advanced an annual 7.0 percent versus forecasts for a jump of 13.7 percent after climbing 15.4 percent a month earlier.

-

Staff Projected Slightly Lower Unemployment Rate Over Medium Term

-

Staff Saw Natural Unemployment Rate As 'A Bit Lower' Than Previously Assumed

-

Staff Saw Only 'Small Net Effect' On GDP From China Tariff Dispute

-

Expected GDP Growth 'A Little Slower' In Second Half of 2018 Than First Half

-

Saw Risks to GDP, Unemployment Forecasts as Balanced

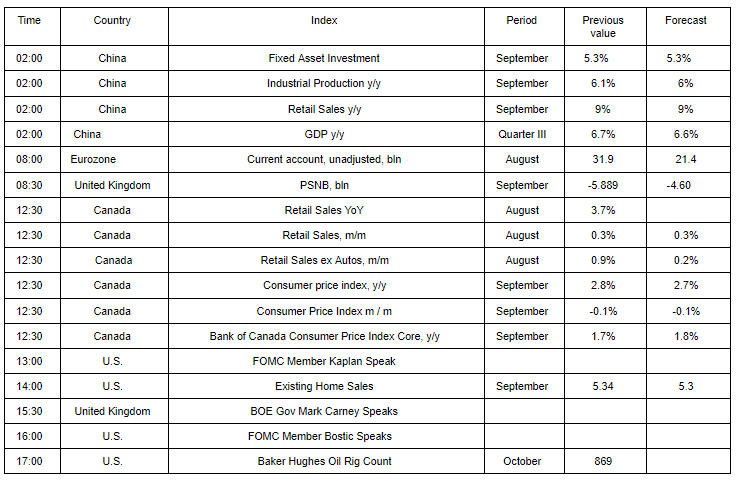

EUR/USD

Resistance levels (open interest**, contracts)

$1.1694 (1940)

$1.1663 (2048)

$1.1618 (544)

Price at time of writing this review: $1.1488

Support levels (open interest**, contracts):

$1.1473 (3344)

$1.1443 (2994)

$1.1408 (3826)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date November, 19 is 79849 contracts (according to data from October, 17) with the maximum number of contracts with strike price $1,1600 (4430);

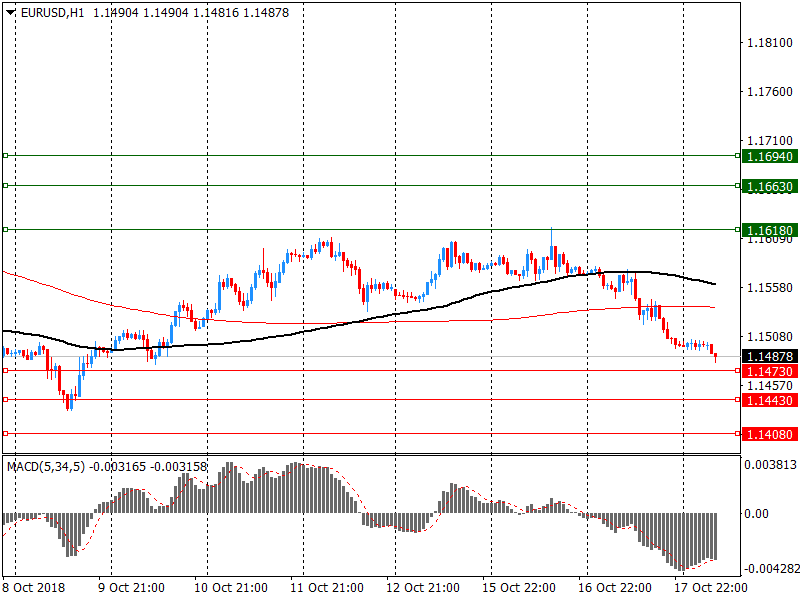

GBP/USD

Resistance levels (open interest**, contracts)

$1.3224 (802)

$1.3202 (388)

$1.3181 (621)

Price at time of writing this review: $1.3083

Support levels (open interest**, contracts):

$1.3030 (512)

$1.3000 (2041)

$1.2968 (1895)

Comments:

- Overall open interest on the CALL options with the expiration date November, 19 is 23343 contracts, with the maximum number of contracts with strike price $1,3500 (3405);

- Overall open interest on the PUT options with the expiration date November, 19 is 27741 contracts, with the maximum number of contracts with strike price $1,3000 (3069);

- The ratio of PUT/CALL was 1.19 versus 1.16 from the previous trading day according to data from October, 17

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

Some Officials Saw Trade Policy as Source of Uncertainty for Growth, Inflation

-

Some Officials Saw Possible Risks To Financial Stability

-

Some Officials Noted Financial Stress in Emerging Markets as Risk to Economy

-

Officials Generally Judged Economy to be Evolving as Anticipated

-

A Few Officials See Rates Becoming Modestly Restrictive For A Time

-

A Couple Officials Opposed Restrictive Policy Without Clear Signs of Overheating, Rising Inflation

-

A Number of Officials See Fiscal Stimulus Effects Fading Over Coming Years

-

A Few Officials Saw Higher Interest Rates Behind Weak Residential Investment

After one and a half years of continuous growth offoreign trade, Swiss Exports declined in the third quarter of 2018 compared to the previous record-high quarter by 2.9 percent. Nevertheless, they remained above the 54 billion franc mark. Imports sank at a high level of 1.5 percent, which corresponds to 768 million Swiss francs. The trade balance resulted in a surplus of 3.5 billion francs. After six quarters of positive growth, exports in the third quarter of 2018 were seasonally adjusted down 2.9 percent on the previous quarter (real: - 2.3 percent).

Trend estimates (monthly change):

Employment increased 26,400 to 12,640,800.

Unemployment decreased 10,500 to 688,500.

Unemployment rate remained steady at 5.2%.

Participation rate remained steady at 65.6%.

Monthly hours worked in all jobs increased 2.8 million hours (0.2%) to 1,755.7 million hours.

Seasonally adjusted estimates (monthly change):

Employment increased 5,600 to 12,636,300. Full-time employment increased 20,300 to 8,654,400 and part-time employment decreased 14,700 to 3,981,900.

Unemployment decreased 37,200 to 665,800. The number of unemployed persons looking for full-time work decreased 38,000 to 449,700 and the number of unemployed persons only looking for part-time work increased 900 to 216,100.

Unemployment rate decreased by 0.3 pts to 5.0%.

Participation rate decreased by 0.2 pts to 65.4%.

Monthly hours worked in all jobs increased 6.2 million hours (0.4%) to 1,757.5 million hours.

As reported by the Federal Statistical Office, the selling prices in wholesale trade increased by 3.5% in September 2018 from the corresponding month of the preceding year. In August 2018 and in July 2018 the annual rates of change were +3.8% and +3.6%, respectively.

From August 2018 to September 2018 the index rose by 0.4%.

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers