- Analytics

- News and Tools

- Market News

Analytics, News, and Forecasts for CFD Markets: currency news — 29-11-2016.

(pare/closed(GMT +3)/change, %)

EUR/USD $1,0648 +0,34%

GBP/USD $1,2490 +0,60%

USD/CHF Chf1,0115 -0,14%

USD/JPY Y112,38 +0,40%

EUR/JPY Y119,65 +0,71%

GBP/JPY Y140,35 +0,98%

AUD/USD $0,7482 +0,03%

NZD/USD $0,7124 +0,73%

USD/CAD C$1,343 +0,15%

00:00 New Zealand ANZ Business Confidence November 24.5

00:05 United Kingdom Gfk Consumer Confidence November -3 -4

00:30 Australia Private Sector Credit, m/m October 0.4% 0.4%

00:30 Australia Private Sector Credit, y/y October 5.4%

00:30 Australia Building Permits, m/m October -8.7% 1.5%

05:00 Japan Construction Orders, y/y October 16.3%

05:00 Japan Housing Starts, y/y October 10% 11.2%

07:00 United Kingdom BOE Financial Stability Report

07:00 Germany Retail sales, real adjusted October -1.4% 1%

07:00 Germany Retail sales, real unadjusted, y/y October 0.4% 1%

07:00 Switzerland UBS Consumption Indicator October 1.59

08:00 Switzerland KOF Leading Indicator November 104.7 104

08:55 Germany Unemployment Change November -14 -5

08:55 Germany Unemployment Rate s.a. November 6% 6%

10:00 Eurozone Harmonized CPI, Y/Y (Preliminary) November 0.5% 0.6%

10:00 Eurozone Harmonized CPI ex EFAT, Y/Y (Preliminary) November 0.8% 0.8%

12:30 Eurozone ECB President Mario Draghi Speaks

13:15 U.S. ADP Employment Report November 147 165

13:30 Canada Industrial Product Price Index, m/m October 0.4% 0.6%

13:30 Canada Industrial Product Price Index, y/y October -0.5%

13:30 Canada GDP (m/m) September 0.2% 0.1%

13:30 Canada GDP QoQ Quarter III -0.4%

13:30 Canada GDP (YoY) Quarter III -1.6% 3.4%

13:30 U.S. Personal spending October 0.5% 0.5%

13:30 U.S. Personal Income, m/m October 0.3% 0.4%

13:30 U.S. PCE price index ex food, energy, m/m October 0.1% 0.1%

13:30 U.S. PCE price index ex food, energy, Y/Y October 1.7%

14:45 U.S. Chicago Purchasing Managers' Index November 50.6 52

15:00 U.S. Pending Home Sales (MoM) October 1.5% 0.4%

15:30 U.S. Crude Oil Inventories November -1.255

16:45 U.S. FOMC Member Jerome Powell Speaks

19:00 U.S. Fed's Beige Book

22:30 Australia AIG Manufacturing Index November 50.9

23:50 Japan Capital Spending Quarter III 3.1%

The Conference Board Consumer Confidence Index, which had declined in October, increased significantly in November. The Index now stands at 107.1 (1985=100), up from 100.8 in October. The Present Situation Index increased from 123.1 to 130.3, while the Expectations Index improved from 86.0 last month to 91.7.

"Consumer confidence improved in November after a moderate decline in October, and is once again at pre-recession levels," said Lynn Franco, Director of Economic Indicators at The Conference Board. (The Index stood at 111.9 in July 2007.) "A more favorable assessment of current conditions coupled with a more optimistic short-term outlook helped boost confidence. And while the majority of consumers were surveyed before the presidential election, it appears from the small sample of post-election responses that consumers' optimism was not impacted by the outcome. With the holiday season upon us, a more confident consumer should be welcome news for retailers."

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, surpassed the peak set in July 2006 as the housing boom topped out. The National index reported a 5.5% annual gain in September, up from 5.1% last month. The 10-City Composite posted a 4.3% annual increase, up from 4.2% the previous month.

The 20-City Composite reported a yearover-year gain of 5.1%, unchanged from August. Seattle, Portland, and Denver reported the highest year-over-year gains among the 20 cities over each of the last eight months. In September, Seattle led the way with an 11.0% year-over-year price increase, followed by Portland with 10.9%, and Denver with an 8.7% increase. 12 cities reported greater price increases in the year ending September 2016 versus the year ending August 2016.

EURUSD 1.0620-30 (EUR 947m) 1.0640 (653m)

USDJPY 110.00 (USD 400m)

GBPUSD 1.2655 (GBP 433m)

USDCNY 6.9000 (USD 580m) 6.9300 (602m)

USDCAD 1.3400 (USD 1.03bln) 1.3600 (890m)

Canada's current account deficit (on a seasonally adjusted basis) narrowed $0.7 billion in the third quarter to $18.3 billion, following three straight quarterly increases.

In the financial account (unadjusted for seasonal variation), strong foreign investment in Canadian corporate bonds led the inflow of funds in the quarter.

The deficit on international trade in goods narrowed $2.7 billion to $8.3 billion in the third quarter, following a record deficit of $11.1 billion in the second quarter. Exports outpaced imports as exports saw the highest growth since the first quarter of 2014.

otal exports of goods increased $5.9 billion to $130.1 billion in the third quarter. Energy products were the major contributor with exports up $2.3 billion on higher prices and volumes. In addition, exports of metal and non-metallic mineral products increased by $1.0 billion, mostly from higher prices. Consumer goods were up $0.7 billion on higher volumes, following a $1.6 billion reduction in the second quarter.

Real gross domestic product increased at an annual rate of 3.2 percent in the third quarter of 2016, according to the "second" estimate released by the Bureau of Economic Analysis. In the second quarter, real GDP increased 1.4 percent.

The GDP estimate released today is based on more complete source data than were available for the "advance" estimate issued last month. In the advance estimate, the increase in real GDP was 2.9 percent. With the second estimate for the third quarter, the general picture of economic growth remains the same; the increase in personal consumption expenditures was larger than previously estimated.

The inflation rate in Germany as measured by the consumer price index is expected to be +0.8% in November 2016. Based on the results available so far, the Federal Statistical Office (Destatis) also reports that the consumer prices are expected to increase by 0.1% on October of the year.

The harmonised index of consumer prices for Germany calculated for European purposes is expected to be up 0.7% year on year.However, it is not expected to change from October 2016. The final results for November 2016 will be released on 13 December 2016.

EUR/USD

Offers 1.0620-25 1.0650 1.0685 1.0700 1.0730 1.0750 1.0780 1.0800

Bids 1.0580-85 1.0560 1.0530 1.0515 1.0500

GBP/USD

Offers 1.2420-25 1.2440-45 1.2475 1.2500 1.2520 1.2530-35 1.2550-55 1.2570 1.2585 1.2600

Bids 1.2400 1.2380 1.2360 1 .2340 1.2315-20 1.2300 1.2285 1.2250

EUR/GBP

Offers 0.8560 0.8575-80 0.8600 0.8630-35 0.8650

Bids 0.8520 0.8500 0.8475-80 0.8450 0.8420 0.8400

EUR/JPY

Offers 119.30 119.50 119.80-85 120.00 120.45-50 121.00 121.50

Bids 118.80 118.50 118.00 117.80 117.60 117.30 117.00

USD/JPY

Offers 112.50 112.80 113.00 113.25-30 113.60 113.80 114.00

Bids 112.00 111.80-85 111.50 111.30-35 111.00 110.85 110.50 110.30 110.00

AUD/USD

Offers 0.7500-05 0.7520 0.7545-50 0.7580 0.7600

Bids 0.7460 0.7450 0.7430 0.7400 0.7370 0.7355-60 0.7325-30 0.7300

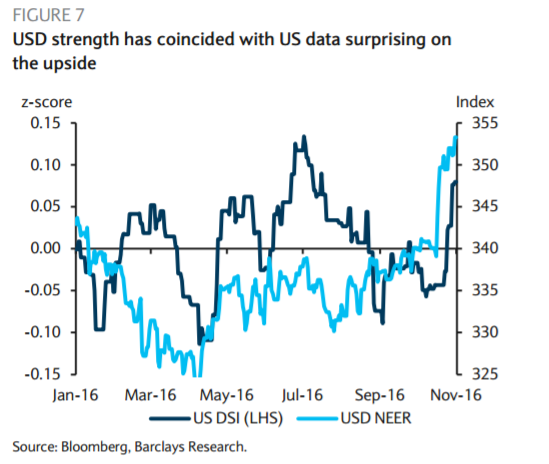

"We see asymmetric risks to the USD this week as the employment report (Friday) takes central stage. A number close to our expectation of 175k or even lower would keep the Fed on track as it is assumed that a deceleration in job creation is normal as the labour market is near full employment. On the other hand, a higher number (closer to 200k) would signal that the momentum is still strong, and that additional stimulus would probably lead the Fed to act faster, accelerating USD trend. We expect the unemployment rate to decline to 4.8% from 4.9%, average hourly earnings to rise 0.2% m/m and 2.8% y/y, and the average workweek to remain unchanged at 34.4 hours.

In addition, we expect the ISM manufacturing (Thursday) to remain soft and decreasing slightly from 51.9 to 51.5 as employment in the manufacturing sector remained weak through October.

Next Sunday's Italian referendum on Senate reform is an important event for markets this week but a "no" outcome appears largely priced in EURUSD, in our view. Polls suggest that most voters oppose PM Renzi's proposal and should that be realised, we expect him to step down. While recent EURUSD depreciation has largely been driven by USD strength, we think a portion of recent EUR weakness reflects a discount to various political risks over the coming year, including elections in the Netherlands, France and Germany. Given these residual risks we think any sustained EURUSD appreciation is unlikely. The reaction to a surprise "yes" vote is uncertain with, bi-modal implications: it simultaneously increases the likelihood of Prime Minister Renzi's reform agenda (if the PD, Mr. Renzi's party, wins the next election) and the likelihood of radical change and rejection of the euro if 5SM wins.

On the data front, November euro area headline/core inflation (Wednesday) is expected to remain unchanged at 0.5%/0.8%, while euro area final November manufacturing PMI (Thursday) is expected to be confirmed at 53.7".

Copyright © 2016 Barclays Capital, eFXnews™

At the moment the yield on Italian 10-year bonds shows a decline of 5 basis points, to 2.02 per cent.

Eurozone economic confidence improved to a 11-month high in November, survey data from the European Commission showed Tuesday, cited by rttnews.

The industrial confidence index dropped unexpectedly to -1.1 November from -0.6 points in October. The reading was forecast to rise to -0.5.

At the same time, the consumer sentiment indicator improved to -6.1, as initially estimated, from -8 in October. The increase in confidence was fueled by significantly brighter expectations regarding the future general economic situation and future unemployment.

After two months of sharp increases, the Economic Sentiment Indicator (ESI) in November moved broadly sideways in the euro area (+0.1 points to 106.5) and edged up only slightly in the EU (+0.4 points to 107.3), the European Comision says.

UK broad money, M4ex, is defined as M4 excluding intermediate other financial corporations (OFCs). M4ex increased by £11.7 billion in October, compared to the average monthly increase of £14.5 billion over the previous six months. The three-month annualised and twelve-month growth rates were 6.9% and 7.8% respectively.

Households' holdings of M4 increased by £5.0 billion in October, compared to the average monthly increase of £7.5 billion over the previous six months. The three-month annualised and twelve-month growth rates were 5.4% and 6.7% respectively. M4 lending to households increased by £4.2 billion in October, compared to the average monthly increase of £3.5 billion over the previous six months. The three-month annualised and twelve-month growth rates were 3.9% and 4.0% respectively.

Loans to financial and non-financial businesses decreased by £8.2 billion in October, compared to the average monthly increase of £2.3 billion over the previous six months. The decrease was mainly in loans to businesses in the financial services industry (£10.5 billion). The twelve-month growth rate was 1.0%.

The number of loan approvals for house purchase was 67,518 in October, compared to the average of 63,914 over the previous six months. The number of approvals for remortgaging was 43,513, compared to the average of 42,115 over the previous six months. The number of approvals for other purposes was 13,427, compared to the average of 12,726 over the previous six months

EUR/USD 1.0620-30 (EUR 947m) 1.0640 (653m)

USD/JPY 110.00 (USD 400m)

GBP/USD 1.2655 (GBP 433m)

USD/CNY 6.9000 (USD 580m) 6.9300 (602m)

USD/CAD 1.3400 (USD 1.03bln) 1.3600 (890m)

According to the flash estimate published by the INE, the annual inflation of the CPI in November 2016 is 0.7%.

This indicator provides a preview of the CPI that, if confirmed, would imply the maintenance of its annual change, given that in October this change was 0.7%. In this behavior, it is noteworthy the drop in the prices of fuels (gasoil and gasoline).

In turn, the annual change of the HICP flash estimate in November stands at 0.5%. If confirmed, the annual change of the HICP would remain the same as in the previous month.

"USD has entered its last leg within a secular bull market. We expect USD to be driven by widening rate and investment return differentials.

USD strength should be front-loaded against low-yielding currencies, particularly JPY and KRW.

Later in the cycle we see USD strength broadening out with the help of rising US real rates, specifically hitting high-yielding currencies. Higher real rates should eventually tighten financial conditions, increasing the headwinds for the US economy and marking the turning point for USD after 1Q18.

1) Long USD/JPY: Yield differentials driving outflows from Japan and higher inflation expectations.

Copyright © 2016 Morgan Stanley, eFXnews

-

At 10:00 GMT Italy will place 10-year bonds

-

At 14:15 GMT FOMC member William Dudley will make a speech

-

At 17:40 GMT FOMC member Jerome Powell will deliver a speech

-

At 20:00 GMT RBNZ Financial Stability Report

In October 2016, household consumption expenditure on goods bounced back in volume*: +0.9% after −0.4%. In particular, spendings on energy and purchases of household durables and of clothing picked up markedly.

Energy consumption bounced back sharply (+3.6% after −1.8%). Expenditure on heating in gas and electricity surged owing to relatively cool temperatures for October, after a mild climate for the season in September. Likewise, the consumption of refined products recovered (+2.6% after −3.1%), in part due to oil consumption.

EUR/USD

Resistance levels (open interest**, contracts)

$1.0831 (4510)

$1.0759 (1653)

$1.0704 (1176)

Price at time of writing this review: $1.0592

Support levels (open interest**, contracts):

$1.0501 (4333)

$1.0440 (4970)

$1.0365 (1969)

Comments:

- Overall open interest on the CALL options with the expiration date December, 9 is 78550 contracts, with the maximum number of contracts with strike price $1,1400 (6390);

- Overall open interest on the PUT options with the expiration date December, 9 is 68290 contracts, with the maximum number of contracts with strike price $1,0500 (4970);

- The ratio of PUT/CALL was 0.87 versus 0.88 from the previous trading day according to data from November, 28

GBP/USD

Resistance levels (open interest**, contracts)

$1.2701 (2033)

$1.2603 (1393)

$1.2505 (1822)

Price at time of writing this review: $1.2403

Support levels (open interest**, contracts):

$1.2296 (4036)

$1.2198 (1107)

$1.2099 (1184)

Comments:

- Overall open interest on the CALL options with the expiration date December, 9 is 35197 contracts, with the maximum number of contracts with strike price $1,3400 (2560);

- Overall open interest on the PUT options with the expiration date December, 9 is 36758 contracts, with the maximum number of contracts with strike price$1,2300 (4036);

- The ratio of PUT/CALL was 1.04 versus 1.05 from the previous trading day according to data from November, 28

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

During a press conference, Steven Poloz said that he is confident in the economy's prospects. "We expect that the economy will reach full capacity utilization by mid-2018". He added that the economic recovery will contribute to growth in the service sector. Contributing to the economic recovery monetary and fiscal policy.

According to data published by Ministry of Internal Affairs and Communications, household expenditures in October fell by 0.4% year on year. In September, expenses decreased by -2.1%. Economists had expected a decrease of 0.6% in October compared with the same period of the previous year. Household spending is an indicator that assesses the total expenditure of households and used as an indicator of consumer optimism.

Retail sales increased in October by 2.5% after rising 0.3% in September. The increase marked the second consecutive month, and points to some improvement of the trend in recent years. However, on an annualized basis, this indicator continues to decrease for the eighth month in a row. According to published data, retail sales decreased by -0.1% compared to the same period of the previous year. Sales of Japan's major stores also fell by -1.0% compared with the same period last year.

The report of the Ministry of Economy and Trade says that consumers were cautious in their spending in the conditions of slow growth in wages, although the decline was less significant than in previous months.

As reported by the Federal Statistical Office (Destatis), the index of import prices decreased by 0.6% in October 2016 compared with the corresponding month of the preceding year. In September and in August 2016 the annual rates of change were -1.8% and -2.6%, respectively. From September to October 2016 the index rose by 0.9%.

The index of import prices, excluding crude oil and mineral oil products, decreased by 0.7% compared with the level of a year earlier.

The index of export prices decreased by 0.1% in October 2016 compared with the corresponding month of the preceding year. In September and in August 2016 the annual rates of change were -0.6% and -0.9%, respectively. From September to October 2016 the export price index rose by 0.3%

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers