- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 08-09-2020

| Time | Country | Event | Period | Previous value | Forecast |

|---|---|---|---|---|---|

| 01:30 | China | PPI y/y | August | -2.4% | -2% |

| 01:30 | China | CPI y/y | August | 2.7% | 2.4% |

| 05:45 | Switzerland | Unemployment Rate (non s.a.) | August | 3.2% | 3.3% |

| 06:00 | Japan | Prelim Machine Tool Orders, y/y | August | -31.1% | |

| 12:15 | Canada | Housing Starts | August | 245.6 | 220 |

| 14:00 | U.S. | JOLTs Job Openings | July | 5.889 | 6 |

| 14:00 | Canada | Bank of Canada Rate | 0.25% | 0.25% | |

| 23:50 | Japan | Core Machinery Orders, y/y | July | -22.5% | -18.3% |

| 23:50 | Japan | Core Machinery Orders | July | -7.6% | 1.9% |

FXStreet reports that according to Natixis, wars destroy useful capital. After the war, this capital has to be rebuilt, resulting in an investment and growth boom. The COVID-19 crisis is destroying capital that has become stranded in the sectors permanently affected by the crisis. This capital does not have to be replaced, so investment in these sectors will remain weak and the situation will be very different from that following a war.

“After a war, the capital destroyed during the war is rebuilt, because this capital is necessary (housing, infrastructure, factories, etc.). This leads to a very high level of investment and strong growth. We can look at the examples of the United Kingdom and France after the Second World War. This raises the question of why, after the COVID-19 crisis, which is also going to destroy capital, there will not be this same investment and growth boom as after the war.”

“The COVID-19 crisis is also going to destroy capital since some of the capital of sectors in permanent difficulty can no longer be used. This is the case in the automotive and aerospace sectors, tourism, traditional retail, air transport and oil and gas. In these sectors, a portion of the capital has become unusable due to the permanent loss of revenue. As this capital has become useless, it does not have to be replaced.”

- Says Senate Republicans will introduce a new targeted proposal on Tuesday, focused on health care, education, and economic issues

FXStreet notes that GBP/USD (-0.9%) is weaker for a fifth consecutive day. This comes as Brexit talks resume in London today after a several-week hiatus. The risk of a No-Deal outcome remains, but the base case remains that they will eventually come to a landing. Ahead of this, however, economists at TD Securities are looking for this noisy tone to continue and keep GBP on the defensive near-term.

“We are taking all this with a grain of salt. The risk of a No-Deal outcome by the end of the year remains a possibility and the latest developments are certainly not very helpful in that regard. Despite this, our base case remains that they will eventually come to a landing over the next couple of months. Away from the rhetoric, the reality is that there are only a few core issues that need to be resolved (Fisheries and State Aid foremost among them).”

“The hardening of positions by both sides is likely to keep sterling on the defensive – especially, perhaps, over the next day or two as the talks get underway. Indeed, it may be late Thursday before markets get anything concrete to sink their teeth into. This is likely to be amplified as the UK continues to suffer a more sluggish and prolonged economic recovery than some of its peers. With new coronavirus cases accelerating rapidly and running at their fastest pace since May, we think sentiment toward GBP will remain fragile.”

- We are seeing some good data on the economy

- Germany will need to suspend debt rules in 2021 again

- German budget will be in line with debt rules in 2022

- Recovery measures are the start of a fiscal union

U.S. stock-index futures fell on Tuesday, as investors continued to sell off shares of big tech companies, while worsening U.S.-China tensions and concerns over an unstable economic rebound also weighed on sentiment.

Global Stocks:

Index/commodity | Last | Today's Change, points | Today's Change, % |

Nikkei | 23,274.13 | +184.18 | +0.80% |

Hang Seng | 24,624.34 | +34.69 | +0.14% |

Shanghai | 3,316.42 | +23.83 | +0.72% |

S&P/ASX | 6,007.80 | +63.00 | +1.06% |

FTSE | 5,878.62 | -58.78 | -0.99% |

CAC | 4,935.55 | -118.17 | -2.34% |

DAX | 12,865.29 | -234.99 | -1.79% |

Crude oil | $37.45 | -5.83% | |

Gold | $1,921.90 | -0.64% |

FXStreet notes that the S&P 500 has avoided a bearish “reversal week” but with support from the 13-day average broken, and analysts at Credit Suisse look for a corrective phase to develop for now beneath resistance at 3479/97.

“A bearish ‘reversal week’ was avoided last week but the market did close back below its 13-day exponential average and whilst the core trend stays seen higher, with the market having been to the upper end of its ‘typical’ extreme our bias is for a more protracted consolidation phase within this uptrend.”

“Key as to the severity of a setback remains seen from rates markets and whether we see a more decisive move lower in 10yr US Breakevens and a base in 10yr US Real Yields, neither of which we have yet to see, although the risk is there.”

“Resistance is seen at 3479, then the 61.8% retracement of last week’s fall at 3495/97, which we look to now ideally cap to keep the immediate risk lower.”

(company / ticker / price / change ($/%) / volume)

3M Co | MMM | 165.6 | -0.17(-0.10%) | 4632 |

ALCOA INC. | AA | 14.5 | 0.10(0.69%) | 59413 |

ALTRIA GROUP INC. | MO | 43.5 | 0.01(0.02%) | 26857 |

Amazon.com Inc., NASDAQ | AMZN | 3,158.24 | -136.38(-4.14%) | 116196 |

American Express Co | AXP | 105 | -0.67(-0.63%) | 7733 |

AMERICAN INTERNATIONAL GROUP | AIG | 29.5 | -0.30(-1.01%) | 2339 |

Apple Inc. | AAPL | 114.82 | -6.14(-5.08%) | 4597254 |

AT&T Inc | T | 29.54 | 0.12(0.41%) | 134995 |

Boeing Co | BA | 166.9 | -4.15(-2.43%) | 216264 |

Caterpillar Inc | CAT | 147 | -1.18(-0.80%) | 11527 |

Chevron Corp | CVX | 80.76 | -1.17(-1.43%) | 38054 |

Cisco Systems Inc | CSCO | 40.37 | -0.45(-1.10%) | 123209 |

Citigroup Inc., NYSE | C | 51.89 | -0.63(-1.20%) | 84934 |

E. I. du Pont de Nemours and Co | DD | 58.75 | -0.05(-0.09%) | 962 |

Exxon Mobil Corp | XOM | 38.26 | -0.82(-2.10%) | 195678 |

Facebook, Inc. | FB | 271.63 | -11.10(-3.93%) | 236108 |

FedEx Corporation, NYSE | FDX | 223.46 | -2.66(-1.18%) | 12473 |

Ford Motor Co. | F | 6.86 | -0.04(-0.58%) | 202231 |

Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 15.68 | -0.34(-2.12%) | 68128 |

General Electric Co | GE | 6.33 | -0.09(-1.40%) | 350198 |

General Motors Company, NYSE | GM | 31.9 | 1.90(6.33%) | 1358340 |

Goldman Sachs | GS | 210.4 | -0.54(-0.26%) | 15676 |

Google Inc. | GOOG | 1,544.40 | -46.64(-2.93%) | 21814 |

Hewlett-Packard Co. | HPQ | 18.82 | -0.23(-1.23%) | 5359 |

Home Depot Inc | HD | 266.69 | -2.97(-1.10%) | 13922 |

HONEYWELL INTERNATIONAL INC. | HON | 165 | -1.69(-1.01%) | 6919 |

Intel Corp | INTC | 49.25 | -0.83(-1.66%) | 476600 |

International Business Machines Co... | IBM | 121.9 | -0.40(-0.33%) | 20838 |

International Paper Company | IP | 38.5 | -0.53(-1.36%) | 886 |

Johnson & Johnson | JNJ | 149.5 | 0.91(0.61%) | 16859 |

JPMorgan Chase and Co | JPM | 102.3 | -1.22(-1.18%) | 61490 |

McDonald's Corp | MCD | 210.76 | -0.97(-0.46%) | 7174 |

Merck & Co Inc | MRK | 85.75 | 0.51(0.60%) | 9049 |

Microsoft Corp | MSFT | 206.75 | -7.50(-3.50%) | 582605 |

Nike | NKE | 111.4 | -1.00(-0.89%) | 7990 |

Pfizer Inc | PFE | 36.42 | 0.06(0.17%) | 81088 |

Procter & Gamble Co | PG | 138.7 | 0.74(0.54%) | 9328 |

Starbucks Corporation, NASDAQ | SBUX | 85.01 | -1.26(-1.46%) | 21304 |

Tesla Motors, Inc., NASDAQ | TSLA | 357.27 | -61.05(-14.59%) | 4755078 |

The Coca-Cola Co | KO | 51.27 | 0.23(0.45%) | 36282 |

Travelers Companies Inc | TRV | 115.4 | -1.17(-1.00%) | 6395 |

Twitter, Inc., NYSE | TWTR | 38.5 | -1.37(-3.44%) | 92372 |

UnitedHealth Group Inc | UNH | 311.3 | -0.70(-0.22%) | 7624 |

Verizon Communications Inc | VZ | 60.93 | 0.45(0.74%) | 55614 |

Visa | V | 200.5 | -4.16(-2.03%) | 29873 |

Wal-Mart Stores Inc | WMT | 140.79 | -2.04(-1.43%) | 71211 |

Walt Disney Co | DIS | 131 | -0.99(-0.75%) | 118147 |

Yandex N.V., NASDAQ | YNDX | 62.57 | -1.87(-2.90%) | 127679 |

Alcoa (AA) upgraded to Buy from Neutral at BofA Securities

Walt Disney (DIS) upgraded to Buy from Hold at Deutsche Bank; target raised to $163

- We are fully committed to the Northern Ireland protocol and the Withdrawal Agreement

- We have always sought to honour international obligations

- Our approach guarantees unfettered market access for Northern Ireland

- Bill we will bring forward on Wednesday will live up to manifesto pledges

- Bill will give certainty to people of Northern Ireland

- Bill will ensure businesses in Northern Irelan will have access to UK market without paperwork

- We need to agree on mechanism to resolve any future disputes with EU

- Cabinet was told that government is working closely with business to get ready for Britain leaving EU's customs union and single market on December 31st

- UK is fully committed to implementing Withdrawal Agreement and Northern Ireland protocol

- Government cannot allow damaging situation to arise if UK and EU do not agree on details of Withdrawal Agreement and Northern Ireland protocol

- We must ensure that principle of Northern Ireland being part of UK's customs territory is not compromised

- UK is not going to become high-subsidy regime at end of transition; will set out more on state aid regime in due course

FXStreet reports that economist at UOB Group Ho Woei Chen, CFA, gives her opinion on the Chinese trade outlook.

“China’s exports expanded at a stronger-than-expected pace in August but the contraction in imports weighed on the outlook. In USD-terms, exports rose at 9.5% y/y… However, the contraction in imports worsened to -2.1% y/y… Imports have resumed contractions after a brief rebound in June, casting a pall on the domestic demand outlook… In August, China’s trade surplus narrowed to US$58.93 billion from US$62.33 billion in July.”

“US-China tensions have increasingly shifted into the technology space with US Trump administration’s crackdown on Chinese technology companies. This could dampen bilateral trade even as China may try to ramp up its agricultural purchases before year-end. The US-China tensions, weaker recovery in domestic demand and threats of COVID-19 resurgence are key downside risks to the trade outlook. On the other hand, sustained recovery in global demand supported by reopening of businesses is expected to anchor exports while the CNY strength may boost import demand ahead.”

FXStreet reports that according to strategists at Credit Suisse, USD/CAD has shifted into a near-term range after staying capped at the key 1.3153/67 resistance level. The loonie is trading near daily highs around the 1.3140 mark as of writing.

“The rebound higher in USD/CAD remains capped by the 23.6% retracement the fall from June, price resistance and March downtrend at 1.3153/67, with the market now shifting into a near-term range.”

“Support moves initially to 1.3076, but with a break below 1.3038 needed to reassert a bearish bias again for a fall back to 1.2994, then medium-term support at 1.2952. Beneath here would suggest we are seeing the formation of a significant and long-lasting top, with support seen next at the downward sloping trendline from February 2019, currently seen at 1.2863, with the 78.6% retracement of the 2017/2020 bull trend seen at 1.2620.”

| Time | Country | Event | Period | Previous value | Forecast | Actual |

|---|---|---|---|---|---|---|

| 06:00 | Germany | Current Account | July | 20.4 | 20.0 | |

| 06:00 | Germany | Trade Balance (non s.a.), bln | July | 15.6 | 19.2 | |

| 06:45 | France | Trade Balance, bln | July | -8.06 | -6.99 | |

| 09:00 | Eurozone | Employment Change | Quarter II | -0.2% | -2.9% | |

| 09:00 | Eurozone | GDP (QoQ) | Quarter II | -3.7% | -12.1% | -11.8% |

| 09:00 | Eurozone | GDP (YoY) | Quarter II | -3.2% | -15% | -14.7% |

GBP fell against other major currencies in the European session on Tuesday, as fears of a no-deal Brexit reignited as the latest round of the UK-EU talks started today. On Monday, the UK's PM Boris Johnson stated that, if a trade deal is not reached by 15 October, both sides should "accept that and move on", which would still be "a good outcome for the UK".

Germany's finance minister Olaf Scholz said today that the latest signals from London "do not raise excessive hopes for an agreement". He also warned that "a disorderly Brexit would not be good for Europe, it would be a real disaster for Britain and its citizens".

It was also reported by the FT that the Head of UK’s government legal department Jonathan Jones is leaving his position due to his disagreement with the UK prime minister Boris Johnson's plans to challenge critical parts of the Brexit Withdrawal Agreement, signed in January. According to sources close to Jones, he said he was “very unhappy” about the decision to overwrite parts of the Northern Ireland protocol with new powers in the UK internal market bill, - the new legislation, which was designed by the government to protect trade arrangements between the four parts of the UK and is to be published on Wednesday.

Brussels warned there will be no trade deal if London tries to override parts of the Withdrawal Agreement. "I trust the British government to implement the Withdrawal Agreement, an obligation under international law and prerequisite for any future partnership," the European Commission President Ursula von der Leyen tweeted on Monday. "Protocol on Ireland/Northern Ireland is essential to protect peace and stability on the island & integrity of the single market," she added.

FXStreet reports that FX Strategists at UOB Group note that USD/JPY is still forecasted to trade within a consolidative fashion between 105.50 and 106.90 for the time being.

24-hour view: “We highlighted yesterday USD ‘could consolidate and trade between 106.00 and 106.50’... Momentum indicators are still mostly ‘neutral’ and USD could continue to consolidate for now, likely between 106.05 and 106.50.”

Next 1-3 weeks: “We noted last Thursday (03 Sep, spot at 106.20) that ‘the odds for USD to test the 104.70 have diminished’. We added, ‘a breach of 106.55 would indicate that USD has moved back into a consolidation phase’. While the 106.55 level is still intact, downward momentum has more or less dissipated. In other words, the current price action is likely part of a consolidation phase and USD is expected to trade between 105.50 and 106.90 for a period of time.”

FXStreet notes that GBP/USD weakness has extended on the latest negative Brexit news and the cable is only holding above the 1.31 level. Below 1.3078/54, the pair would mark a top and a more important turn lower, economists at Credit Suisse apprise.

“GBP/USD weakness has extended for a decisive break of its 13-day average and price support at 1.3268/43 and with RSI momentum now not only holding a bearish divergence but now also a top, and with DeMark exhaustion signals also in place the risk for a top is seen growing sharply.”

“Pivotal support is seen starting at the ‘neckline’ to the top at 1.3078, with key price support at 1.3054. Below this latter level is needed to see a top confirmed to mark a more important turn lower with support then seen next and initially at 1.3012/05 – the August low. Whilst we would look for this to hold at first, below in due course should see a move to the 55-day average next at 1.2892.”

The Financial Times (FT) reports, citing two officials with knowledge of the situation, that the UK's Treasury solicitor and permanent secretary of the Government Legal Department, Jonathan Jones, was leaving his position due to his disagreement with the UK Prime Minister Boris Johnson's plans to challenge critical parts of the 2019 Brexit withdrawal agreement.

According to sources, Jones said he was “very unhappy” about the decision to overwrite parts of the Northern Ireland protocol with new powers in the UK internal market bill.

Reuters reports that a disorderly Brexit would be a disaster for Britain and its citizens, German Finance Minister Olaf Scholz told Reuters, adding that the latest signals from London "do not raise excessive hopes for an agreement".

"One thing is clear: a disorderly Brexit would not be good for Europe, it would be a real disaster for Britain and its citizens," Scholz said in an interview ahead of Brexit trade talks on Tuesday.

The European Union told Britain on Monday that there would be no trade deal if it tried to tinker with the Brexit divorce treaty, raising the prospect of a tumultuous end-of-year finale to the saga.

The EU warning came after the Financial Times reported that Prime Minister Boris Johnson's government might simply undercut the Withdrawal Agreement treaty signed in January.

Britain said it would honour the deal and was simply offering clarification to avoid any future legal difficulties.

"Whoever negotiates should always have a good result as their goal," Scholz said. "At any rate, that is the position of the European Union in this matter, which is why I am not even bothering with speculation as to whether or not an agreement will be reached in the end."

FXStreet reports that extra decline in USD/CNH appears to have lost some momentum as of late, suggested FX Strategists at UOB Group.

Next 1-3 weeks: “Our latest narrative was from last Wednesday (02 Sep, spot at 6.8355) wherein ‘oversold short-term conditions could lead to consolidation first but overall risk is for further USD weakness towards 6.8000’. Our view was not wrong as USD traded in a relatively quiet manner for the past few days. While downward momentum has eased somewhat, the negative phase in USD that started in mid-August still has chance to push lower towards the round-number support level of 6.8000. Only a move above 6.8800 (no change in ‘strong resistance’ level) would indicate the negative phase in USD has run its course.”

According to the report from Eurostat, in the second quarter of 2020, still marked by COVID-19 containment measures in most Member States, seasonally adjusted GDP decreased by 11.8% in the euro area and by 11.4% in the EU compared with the previous quarter. These were by far the sharpest declines observed since the time series started in 1995. Economists had expected a 12.1% decrease in the euro area. In the first quarter of 2020, GDP had decreased by 3.7% in the euro area and by 3.3% in the EU.

Compared with the same quarter of the previous year, seasonally adjusted GDP decreased by 14.7% in the euro area and by 13.9% in the EU in the second quarter of 2020, after -3.2% and -2.7% respectively in the previous quarter. These were also by far the sharpest declines since the time series started in 1995. Economists had expected a 15.0% decrease in the euro area.

During the second quarter of 2020, household final consumption expenditure decreased by 12.4% in the euro area and by 12.0% in the EU (after -4.5% in the euro area and -4.2% in the EU in the previous quarter). Gross fixed capital formation decreased by 17.0% in the euro area and by 15.4% in the EU (after -5.2% and -4.6% respectively). Exports decreased by 18.8% in both the euro area and the EU (after -3.9% and -3.2% respectively). Imports decreased by 18.0% in the euro area and by 17.8% in the EU (after -3.2% and -2.8% respectively). Household final consumption expenditure had a very strong negative contribution to GDP growth in both the euro area and the EU (-6.6 and -6.3 percentage points – pp, respectively) and the contribution from gross fixed capital formation was also strongly negative in both zones (-3.8 and -3.4 pp respectively). The contributions from the external balance and government final expenditure were also negative in both zones, while the contribution of changes in inventories was slightly positive in the euro area and slightly negative in the EU.

Reuters reports that the Bank of England's chief economist, Andy Haldane, hailed the recovery so far in Britain's economy after its coronavirus lockdown shock, striking a more upbeat tone than several of his colleagues recently.

Haldane told City A.M. newspaper that the "recovery isn't being given enough credit" and the economy "has bounced back" in large part because consumers had shown themselves to be "incredibly resilient and adaptive and so too have businesses."

Britain suffered its most severe economic contraction on record between March and June when it shrank by 20%, a worse performance than other large industrialised nations.

Haldane has consistently sounded more optimistic about the prospect of a relatively quick recovery.

He also told City A.M. that calls to extend the British government's huge job retention scheme would prevent a "necessary process of adjustment" from taking place in the labour market as some companies looked set to fail.

Haldane told the newspaper in a podcast interview that the pandemic had already delivered "lasting structural change to the economy which does mean, regrettably, some businesses will probably not make it through and some jobs may well not be coming back."

According to the report from Istat, in July 2020 estimates for seasonally adjusted index of retail trade show a monthly contraction, even though levels of total sales confirm recovery after steep falls due to Covid-19 outbreak. When compared with June 2020, value of sales decreased by 2.2%, while volume of retail trade dropped by 3.1%.

Partial recovery after lockdown was confirmed in the three-month on three-month series, as value grew by 12.1% and volume rose by 11.5%.

In July 2020, both value and volume of sales sharply fell in the year on year series, decreasing by 7.2% and 10.2% respectively.

Concerning large-scale distribution and small-scale distribution, the year on year rate dropped for the 5th consecutive month in July, decreasing by 3.8% and 11.7% respectively. Non-store retail sales were down 7.0% when compared with July 2019.

In July 2020, online sales showed a lower year on year growth rate comparing with the strong rise recorded in June 2020 (+52.9%), however internet sales still remained positive year on year (+11.6%).

Looking at the value of sales for non-food products, dramatic falls were reported across all categories besides tools (+3.2%). Similarly to the previous month, in July 2020 the most affected categories of products were clothing (-27.9%) and shoes, leather goods and travel items (-17.3%).

FXStreet reports that the euro strength creates a headache for the European Central Bank (ECB), by tightening financial conditions amid weak growth and deflation. The rhetoric against the common currency strength may ramp up with further ECB easing likely, creating headwinds for additional euro strength, economists at HSBC inform.

“What strikes us is how divergent the EUR’s broad rally is vs. the economic backdrop in the Eurozone. We believe the Eurozone economy will find it incredibly hard to accommodate a strong currency for any sustained period of time. Therefore, the euro strength looks unsustainable. While the markets might be ignoring this for now, at some point, it will matter and the dissonance will be deafening.”

“In the current environment, where EUR strength is much less justified by the economic backdrop than it was in 2017-18, we believe the ECB’s rhetoric on FX is likely to ramp up with further easing likely. With markets preoccupied by the Fed’s policy framework shift to average inflation targeting, the risk of such a shift by the ECB has been completely ignored for now. As and when this happens, further strength in the EUR should be curtailed.”

Reuters reports that the global economy is likely to recover to pre-pandemic levels by early next quarter, about three months earlier than previously expected, economists at Morgan Stanley said.

"The evidence indicates that the virus/economy equation has shifted decisively from the early days of the outbreak," they said in a note to clients, saying that the recovery has continued to gather momentum as countries get better at managing the virus.

The U.S. economy could reach its pre-COVID 19 levels by the second quarter of next year, while the entire developed markets could reach that level by the third quarter of next year, they said.

Coupled with unprecedented levels of fiscal and monetary support and possible disruptions to trade, the prospective recovery is likely to be accompanied by stronger inflation, they said

| Time | Country | Event | Period | Previous value | Forecast | Actual |

|---|---|---|---|---|---|---|

| 01:30 | Australia | National Australia Bank's Business Confidence | August | -14 | -8 | |

| 05:00 | Japan | Eco Watchers Survey: Current | August | 41.1 | 43.9 | |

| 05:30 | France | Non-Farm Payrolls | Quarter II | -2.0% | -0.9% | |

| 06:00 | Germany | Current Account | July | 20.4 | 20.0 | |

| 06:00 | Germany | Trade Balance (non s.a.), bln | July | 15.6 | 19.2 | |

| 06:45 | France | Trade Balance, bln | July | -8.06 | -6.99 |

During today's Asian trading, the US dollar was trading steadily against the euro and the yen

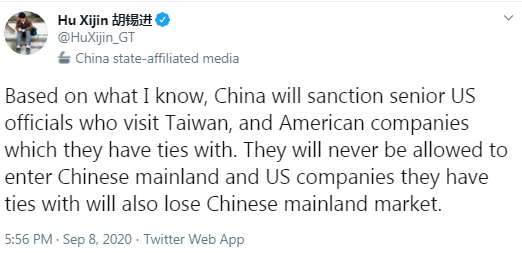

Traders are assessing the statements of US President Donald Trump regarding China, and are also waiting for the next meeting of the European Central Bank (ECB). Trump said on Monday that he intends to sever ties between the American economy and China if he is re-elected as President. In addition, Trump promised to punish companies that "want to leave America to create jobs in China and other countries."

Traders ' attention is focused on the upcoming ECB meeting, as its results may seriously affect the dynamics of the euro. Statements by chief economist Philip Lane last week triggered a fall in the euro from the highest level in more than two years at $1.2, and experts will closely monitor the Central Bank's rhetoric for its concern about the recent strengthening of the euro.

"The key question is whether ECB chief Christine Lagarde will try to prevent the resumption of bullish momentum for the euro against the dollar," Rabobank analysts said.

The pound fell against the dollar amid growing doubts that the UK will be able to negotiate with the EU in the near future. British Prime Minister Boris Johnson announced yesterday that a trade agreement with the EU must be concluded by October 15, otherwise it will not be. This week, investors expect another round of talks between London and Brussels.

The ICE index, which tracks the dynamics of the US dollar against six currencies (euro, swiss franc, yen, canadian dollar, pound sterling and swedish krona), rose by 0.38%.

FXStreet reports that EUR/JPY uptrend at 125.61 is being eroded and Karen Jones, Team Head FICC Technical Analysis Research at Commerzbank, is looking to the downside, specifically to the 124.34 mark.

“EUR/JPY is eroding trend line support at 125.61 but only just! It is also failing at the 2014-2020 resistance line at 127.38.”

“The recent high at 127.07 has been accompanied by a divergence of the daily RSI and our attention has reverted to the downside and we would allow for losses to the 124.34 10th August low.”

“Below 124.34 would target the January high at 122.88. The latter guards the July low at 120.28.”

Reuters reports that France's INSEE official statistics agency confirmed on Tuesday a forecast of a 9% drop in gross domestic product (GDP) in 2020 due to the coronavirus pandemic.

French economic activity should run at 95% of pre-epidemic levels in the third quarter and at 96% of pre-outbreak levels in the fourth, INSEE added.

Economic activity ran at 81% of pre-outbreak levels in Q2, data showed.

INSEE also said that employment fell by 0.9% in the second quarter after a -2% slump in Q1.

According to the report from Federal Statistical Office (Destatis), Germany exported goods to the value of 102.3 billion euros and imported goods to the value of 83.1 billion euros in July 2020. Destatis also reports that exports declined by 11.0% and imports by 11.3% in July 2020 year on year.

Compared with June 2020, exports were up 4.7% and imports 1.1% after calendar and seasonal adjustment. Compared with February 2020, the month before restrictions were imposed due to the corona pandemic, exports decreased by a calendar and seasonally adjusted 12.1%, and imports by 11.5%.

The foreign trade balance showed a surplus of 19.2 billion euros in July 2020. In July 2019, the surplus amounted to 21.3 billion euros. In calendar and seasonally adjusted terms, the foreign trade balance recorded a surplus of 18.0 billion euros in July 2020.

The German current account of the balance of payments showed a surplus of 20.0 billion euros in July 2020, which takes into account the balances of trade in goods (+18.8 billion euros), services (-2.4 billion euros), primary income (+7.1 billion euros) and secondary income (-3.6 billion euros). In July 2019, the German current account showed a surplus of 19.4 billion euros.

EUR/USD

Resistance levels (open interest**, contracts)

$1.1997 (3848)

$1.1949 (625)

$1.1917 (345)

Price at time of writing this review: $1.1806

Support levels (open interest**, contracts):

$1.1780 (902)

$1.1728 (2850)

$1.1660 (4415)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date September, 4 is 56688 contracts (according to data from September, 4) with the maximum number of contracts with strike price $1,1700 (4415);

GBP/USD

Resistance levels (open interest**, contracts)

$1.3502 (762)

$1.3446 (220)

$1.3401 (156)

Price at time of writing this review: $1.3145

Support levels (open interest**, contracts):

$1.3125 (397)

$1.3063 (2621)

$1.3029 (553)

Comments:

- Overall open interest on the CALL options with the expiration date September, 4 is 9387 contracts, with the maximum number of contracts with strike price $1,3500 (1164);

- Overall open interest on the PUT options with the expiration date September, 4 is 10812 contracts, with the maximum number of contracts with strike price $1,3000 (2621);

- The ratio of PUT/CALL was 1.15 versus 0.95 from the previous trading day according to data from September, 4

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

| Raw materials | Closed | Change, % |

|---|---|---|

| Brent | 41.74 | -0.38 |

| Silver | 26.81 | -0.07 |

| Gold | 1928.313 | -0.22 |

| Palladium | 2292.37 | -0.11 |

| Index | Change, points | Closed | Change, % |

|---|---|---|---|

| NIKKEI 225 | -115.48 | 23089.95 | -0.5 |

| Hang Seng | -105.8 | 24589.65 | -0.43 |

| KOSPI | 15.97 | 2384.22 | 0.67 |

| ASX 200 | 19.3 | 5944.8 | 0.33 |

| FTSE 100 | 138.32 | 5937.4 | 2.39 |

| DAX | 257.62 | 13100.28 | 2.01 |

| CAC 40 | 88.65 | 5053.72 | 1.79 |

| Time | Country | Event | Period | Previous value | Forecast |

|---|---|---|---|---|---|

| 01:30 | Australia | National Australia Bank's Business Confidence | August | -14 | |

| 05:00 | Japan | Eco Watchers Survey: Current | August | 41.1 | |

| 05:00 | Japan | Eco Watchers Survey: Outlook | August | 36 | |

| 05:30 | France | Non-Farm Payrolls | Quarter II | -2.0% | |

| 06:00 | Germany | Current Account | July | 22.4 | |

| 06:00 | Germany | Trade Balance (non s.a.), bln | July | 15.6 | |

| 06:45 | France | Trade Balance, bln | July | -8 | |

| 09:00 | Eurozone | Employment Change | Quarter II | -0.2% | |

| 09:00 | Eurozone | GDP (QoQ) | Quarter II | -3.6% | -12.1% |

| 09:00 | Eurozone | GDP (YoY) | Quarter II | -3.1% | -15% |

| 19:00 | U.S. | Consumer Credit | July | 8.95 | 13.75 |

| Pare | Closed | Change, % |

|---|---|---|

| AUDUSD | 0.72746 | -0.13 |

| EURJPY | 125.546 | -0.17 |

| EURUSD | 1.18134 | -0.21 |

| GBPJPY | 139.828 | -0.81 |

| GBPUSD | 1.31588 | -0.83 |

| NZDUSD | 0.66901 | -0.41 |

| USDCAD | 1.30947 | 0.28 |

| USDCHF | 0.91584 | 0.29 |

| USDJPY | 106.259 | 0.03 |

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers