- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 10-11-2011

The euro advanced from a one-month low versus the dollar after Standard & Poor’s clarified that France’s credit rating remains AAA, easing concern that a crisis was imminent in the region’s second-largest economy.

The 17-nation currency advanced earlier versus most major peers after Italy drew double the bids for the amount on offer at a bill sale, damping bets the nation will face a challenge funding itself. Greece chose an interim prime minister. Europe’s shared currency rallied from little-changed as S&P said a message was erroneously sent today to some of its subscribers suggesting France’s top-notch credit rating had been lowered. It affirmed the country’s AAA rating.

The euro gained earlier as Italy sold 5 billion euros ($6.8 billion) of bills to yield 6.087 percent, compared with 3.57 percent the last time it auctioned 12-month securities on Oct. 11, and European Central Bank was said to have bought Italy’s government bonds. Demand at the auction was 1.99 times the amount on offer.

Lucas Papademos, a former vice president of the ECB, was chosen to lead a new Greek unity government, paving the way for a coalition charged with securing additional financing to avert the country’s economic collapse. Papademos, 64, steered the country into the euro region as central bank governor more than a decade ago. He has never held elective office.

The Dollar Index declined 0.5 percent to 77.543 on reduced demand for a refuge after a report showed the number of Americans filing applications for unemployment benefits fell to the lowest level in seven months.

European stocks dropped, erasing earlier gains, as a surge in French borrowing costs added to concern the region’s debt crisis is spreading.

Stocks tumbled yesterday after Italian borrowing costs surged to euro-era records. Italy’s 10-year bond yield yesterday closed at 7.25 percent, near levels that prompted Greece, Ireland and Portugal to seek bailouts.

French 10-year bonds extended their declines today, sending the yield 20 basis points higher to 3.40 percent. Sean Egan, president and founding principal of Egan-Jones Ratings Co., told Bloomberg Radio the nation’s sovereign-debt rating is “probably headed south.”

The difference in yield with similar-maturity benchmark German bunds increased 18 basis points to 166 basis points, the most since the euro was introduced in 1999.

National benchmark indexes declined in 15 of the 18 western European markets today. France’s CAC 40 and the U.K.’s FTSE 100 both slid 0.3 percent, while Germany’s DAX rose 0.7 percent.

Credit Agricole SA slid 2.3 percent after France’s third- largest bank reported a drop in profit. The bank reported a 65 percent drop in third-quarter profit to 258 million euros as writedowns on Greek debt crimped earnings.

Vedanta Resources Plc led a retreat in mining companies, falling 9.5 percent after the largest copper producer in India reported a 92 percent drop in first-half profit to $27.8 million on foreign-exchange losses. The shares also fell as copper tumbled in London.

Air France-KLM lost 5 percent to 4.62 euros after Europe’s biggest airline reported a 31 percent drop in quarterly profit and said it expects to post a full-year loss as fuel costs surge and a sluggish economy weighs on ticket prices.

European Aeronautic Defence and Space Co. paced advancing shares, climbing 5 percent to 20.97 euros after third-quarter profit surged to 312 million euros from 13 million euros and the German government agreed to buy a 7.5 percent stake in the company from Daimler AG. The maker of Mercedes-Benz cars lost 1.2 percent to 33.16 euros.

Fed's doing what it can to get econ on track; econ is still far from where we want it.

U.S. stocks rose, following the biggest decrease in the Standard & Poor’s 500 Index since August, as concern about Europe eased as S&P said it did not downgrade France’s debt and American jobless claims fell. Earlier today, stocks trimmed gains amid investors’ concern that France’s rating would be lowered.

Equities tumbled yesterday on concern that European leaders may be unable to keep the euro zone intact as Italian yields surged to a record. The decline erased the month-to-date advance in the S&P 500. The measure had the biggest monthly gain in 20 years in October on speculation Europe would contain its crisis.

Former vice president of the European Central Bank Lucas Papademos will head a national unity government for Greece, according to the country’s presidency. The ECB bought Italian government bonds today, according to three people familiar with the transactions, who declined to be identified. Italy sold 5 billion euros ($6.8 billion) of one-year bills, the maximum for the auction, and demand rose as the Treasury lured investors with the highest yield in 14 years.

Stocks also rose as data showed the number of Americans filing applications for unemployment benefits fell to the lowest level in seven months, a sign the recovery may be encouraging companies to limit cuts in headcount. The U.S. trade deficit unexpectedly narrowed in September to the lowest level this year as exports surged to a record high, another report showed.

Dow 11,889.74 +108.80 +0.92%, Nasdaq 2,625.69 +4.04 +0.15%, S&P 500 1,238.52 +9.42 +0.77%

Cisco Systems Inc. (CSCO), a maker of networking equipment, climbed 6.3 percent as profit and sales beat estimates. Merck & Co. (MRK) jumped 3 percent after raising its dividend. Apple Inc. slumped 2.4 percent.

Gold futures fell the most in six weeks as demand for a haven eased after Italian bond yields dropped and a new Greek leader was named, reducing concerns that Europe’s sovereign-debt crisis will escalate. Italy sold 5 billion euros ($6.8 billion) of one-year bills, the maximum for the Treasury auction. Lucas Papademos, a former vice president of the European Central Bank, became the head of a national unity government in Greece. Gold jumped to a record $1,923.70 an ounce on Sept. 6 on demand for an alternative to equities and some currencies.

Gold futures for December delivery fell to $1,736.60 on the Comex in New York. A close at the price would mark the biggest gain for a most-active contract since Sept. 23. Before today, the metal climbed 26 percent in the past year.

Oil rose to the highest level in more than three months after a government report showed U.S. jobless claims unexpectedly declined, spurring optimism that a recovering economy will boost fuel demand.

Oil advanced as much as 2.3 percent after the Labor Department said the number of Americans filing applications for unemployment benefits fell by 10,000 to a seven-month low of 390,000 in the week ended Nov. 5. Prices also increased as Italian bond yields retreated from records, tempering concern that Europe’s debt crisis would spiral out of control.

Crude for December delivery climbed to $97.90, the highest intraday level since Aug. 1, on the New York Mercantile Exchange. Prices have risen 6 percent this year.

Brent oil for December settlement gained 41 cents, or 0.4 percent, to $112.72 a barrel on the London-based ICE Futures Europe exchange.

Techs support at $1.5846/49, the 55-day moving average and High 17 Oct.

Shares of Cisco Systems (CSCO) rose 6.25%. CSCO' FQ1 EPS of $0.43 beats by $0.04. Revenue of $11.26B (+5% Y/Y) beats by $240M.

USD/JPY Y77.25, Y77.50, Y77.70

EUR/PY Y106.55

GBP/USD $1.5890, $1.5900, $1.5965, $1.5995

EUR/GBP stg0.8500

USD/CHF Chf0.9100, Chf0.9035, Chf0.8980

EUR/CHF Chf1.2365, Chf1,2380, Chf1.2400 * Chf1.2300 digital,large

AUD/USD $0.9910, $0.9985, $1.0000, $1.0200, $1.0250

EUR/USD A$1.3450

NZD/USD $0.7535

AUD/NZD NZ$1.3000

USD/CAD C$1.0200-10, C$1.0250

NZD/CAD C$0.8150

Former vice president of the European Central Bank Papademos will head a national unity government for Greece, according to the country’s presidency.

The ECB bought Italian government bonds today, according to three people familiar with the transactions, who declined to be identified.

Stock futures extended gains as data showed the number of Americans filing applications for unemployment benefits fell to the lowest level in seven months, a sign the recovery may be encouraging companies to limit cuts in headcount. Jobless claims fell by 10,000 to 390,000 in the week ended Nov. 5, Labor Department figures showed. The median forecast of economists was 400,000 new claims.

World markets: Nikkei -2.91%, Hang Seng -5.25%, Shanghai Composite -1.80%, FTSE +0.37%, CAC +0.62%, DAX +1.25%.

Crude oil: $97.31 (+1,6%).

Gold: $1773,00 (-1,0%).

Data:

06:30 France CPI (October) unadjusted 0.2%

06:30 France CPI (October) unadjusted Y/Y 2.3%

06:30 France HICP (October) Y/Y 2.5%

07:00 Germany CPI (October) final 0.0%

07:00 Germany CPI (October) final Y/Y 2.5%

07:00 Germany HICP (October) final Y/Y 2.9%

07:00 Germany Wholesale prices (October) -1.0%

07:00 Germany Wholesale prices (October) Y/Y 5.0%

07:45 France Industrial production (September) -1.7%

07:45 France Industrial production (September) Y/Y 3.4%

09:00 Italy Industrial production (September) adjusted -4.8%

09:00 Italy Industrial production (September) Y/Y adjusted -2.7%

12:00 UK BoE meeting announcement 0.50%

The euro rose after Italy drew double the bids for the amount on offer at a bill sale, easing concern the nation is struggling to fund itself.

The euro advanced from a one-month low as the European Central Bank was said to buy Italy’s government bonds.

The country’s 10-year yields climbed yesterday above the 7 percent level that spurred Greece, Ireland and Portugal to request bailouts. The euro remained higher versus the greenback as U.S. initial unemployment claims dropped.

Italy sold 5 billion euros ($6.8 billion) of bills today, with investors bidding for nearly double the amount of securities on offer. The bills were sold to yield 6.087 percent today, compared with 3.57 percent the last time it auctioned 12-month securities on Oct. 11.

The Senate in Italy will vote tomorrow on debt-reduction measures that may lead to the resignation of Prime Minister Silvio Berlusconi within days. The pace of the euro’s decline also encouraged some investors to buy.

EUR/USD: the pair grown above $1.3600.

GBP/USD: the pair fell below $1.5900.

USD/JPY: the pair holds in Y77,55-Y77,90.

EUR/USD:

Offers $1.3720/25, $1.3680/700, $1.3660, $1.3650

Bids $1.3600, $1.3585/80, $1.3555/45, $1.3525/20

New government to be sworn in Friday Nov 11 1200GMT.

Committed to fully implement Oct 27 agreements.

Resistance 3: Y78.40 (Nov 2 high)

Resistance 2: Y78.00 (resistance line from Nov 2)

Resistance 1: Y77.90 (session high)

Current price: Y77.62

Support 1:Y77.55 (Nov 9 low, 50.0 % FIBO Y75,55-Y79,55)

Support 2:Y77.10 (61.8 % FIBO Y75,55-Y79,55)

Support 3:Y76.30 (area of Oct 25-26 highs)

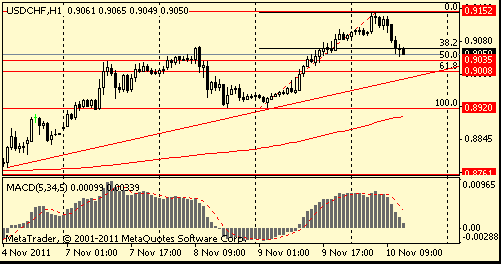

Resistance 3: Chf0.9360 (area of high of March)

Resistance 2: Chf0.9310 (area of high of October)

Resistance 1: Chf0.9150 (session high)

Current price: Chf0.9050

Support 1: Chf0.9030 (50.0 % FIBO Chf0,8920-Chf0,9150, session low)

Support 2: Chf0.9010 (61,8 % FIBO Chf0,8920-Chf0,9150, support line from Nov 3)

Support 3: Chf0.8920 (Nov 8-9 low)

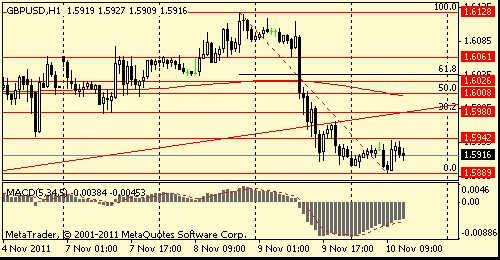

Resistance 3: $ 1.6000/10 (50,0 % FIBO $1,6130-$ 1,5890)

Resistance 2: $ 1.5980 (38,2 % FIBO $1,6130-$ 1,5890, support line from Oct 12)

Resistance 1: $ 1.5940 (area of Nov 4 low and session high)

Current price: $1.5916

Support 1 : $1.5890 (session low)

Support 2 : $1.5875 (Nov 7 low)

Support 3 : $1.5820 (38,2 % FIBO $1,5270-$ 1,6130)

Resistance 3: $ 1.3720 (area of 61,8 % FIBO $1,3850-$ 1,3485, Nov 8 low)

Resistance 2: $ 1.3675 (50,0 % FIBO $1,3850-$ 1,3485)

Resistance 1: $ 1.3630 (38,2 % FIBO $1,3850-$ 1,3485, session high)

Current price: $1.3584

Support 1 : $1.3485 (session low)

Support 2 : $1.3370 (Oct 10 low)

Support 3 : $1.3240 (Oct 6 low)

USD/JPY Y77.25, Y77.50, Y77.70

EUR/PY Y106.55

GBP/USD $1.5890, $1.5900, $1.5965, $1.5995

EUR/GBP stg0.8500

USD/CHF Chf0.9100, Chf0.9035, Chf0.8980

EUR/CHF Chf1.2365, Chf1,2380, Chf1.2400 * Chf1.2300 digital,large

AUD/USD $0.9910, $0.9985, $1.0000, $1.0200, $1.0250

EUR/USD A$1.3450

NZD/USD $0.7535

AUD/NZD NZ$1.3000

USD/CAD C$1.0200-10, C$1.0250

NZD/CAD C$0.8150

- Forecasters See GDP Up 0.8% In 2012 Vs 1.6% In Aug Forecast

- Forecasters See GDP Up 1.6% In 2013 Vs 1.8% In Aug Forecast

- ECB Forecasters Sharply Lower 2012 GDP Growth Forecast

- CPI To Stay Above 2% In Coming Months, Fall Thereafter

- Econ Outlook Subject To High Uncertainty, Intensified Downside Risks

- Some Risks To Econ Outlook Have Been Materializing

- Significant Downward Revision To 2012 GDP Forecast "Very Likely"

- All Euro Area Govts Must Honor Sovereign Signatures

- Forecasters See HICP Up 2.6% In 2011, Same As Aug Forecast

- Forecasters See HICP Up 1.8% In 2012 Vs 2.0% In Aug Forecast

- Forecasters See HICP Up 1.8% In 2013 Vs 1.9% In Aug Forecast

Nikkei 225 8,501 -254.64 -2.91%

Hang Seng 18,964 -1,050.54 -5.25%

S&P/ASX 4,244 -101.95 -2.35%

Shanghai Composite 2,480 -45.38 -1.80%

00:30 Australia Changing the number of employed October 10.1K

00:30 Australia Unemployment rate October 5.2%

02:00 China Trade Balance, bln October 17.0

05:00 Japan Consumer Confidence October 38.6

05:00 Japan Consumer Confidence Households October 38.6

06:00 Japan Prelim Machine Tool Orders, y/y October +25.9%

Canada’s dollar dropped to the lowest level in almost three weeks as concern Italy may become the latest European nation in need of a financial bailout drove investors to the safety of the U.S. currrency.

The Canadian currency dropped 1.6 percent, the most this week, extending its losses in the second half of the year to 5.9 percent.

The euro touched the lowest level in a month before Italy sells 5 billion euros ($6.8 billion) of one-year bills today, testing investor appetite after borrowing costs surged to euro-era records.

The 17-nation currency reached a two-week low against the yen after Italian yields yesterday climbed above the 7 percent level that spurred Greece, Ireland and Portugal to seek bailouts. Italy will sell five-year debt on Nov. 14.

EUR/USD: on Asian session the pair fell.

GBP/USD: on Asian session the pair decreased.

USD/JPY: on Asian session the pair fell.

On Wednesday UK data at 0930GMT includes the Trade Balance and also BOE Quoted Rates data. Despite turbulence in the euro zone, the UK's largest export market by far, the August trade data were surprisingly robust, with the global goods, and EU trade, deficits narrowing. US data starts at 1100GMT with the weekly MBA Mortgage Application Index. At 1430GMT, Fed Chairman Ben Bernanke gives welcoming remarks at the Fed's Small Business and Entrepreneurship conference in Washington. US data continues at 1500GMT with Wholesale Inventories and then at 1530GMT with the weekly EIA Crude Oil Stocks data. At 1715GMT, Fed Governor Daniel Tarullo delivers a speech on financial regulation at a Clearing House conference in New York.

Asian stocks rose for the first time in three days as Italian Prime Minister Silvio Berlusconi’s offer to resign bolstered optimism Europe may find a way to contain its debt crisis, and China’s inflation rate eased. The sovereign-debt crisis has stirred political dramas across the region, with Berlusconi offering to resign just days after Greek Prime Minister George Papandreou agreed to step aside. Financial stocks were the biggest contributors to the MSCI Asia Pacific Index’s advance today as Chinese lenders in Hong Kong rallied after China reported inflation at the slowest pace in five months.

Japan’s Nikkei 225 (NKY) Stock Average rose 1.2 percent. South Korea’s Kospi Index added 0.2 percent. Australia’s S&P/ASX 200 advanced 1.2 percent. Hong Kong’s Hang Seng Index climbed 1.7 percent, while China’s Shanghai Composite Index gained 0.8 percent.

Industrial & Commercial Bank of China Ltd. led a rally among Chinese lenders in Hong Kong as the nation’s inflation rate moderated to 5.5 percent last month. China Construction Bank Corp., the second- largest, advanced 1.6 percent to HK$5.71. Agricultural Bank of China Ltd. rose 1.9 percent to HK$3.67.

Australian banks advanced after the nation’s home-loan approvals rose more than economists forecast in September, the sixth straight monthly gain, as more first-time buyers entered the market Westpac Banking Corp., Australia’s second-largest lender by market value, gained 1.3 percent. Australia and New Zealand Banking Group Ltd., the nation’s third-biggest lender, increased 0.8 percent to A$21.76. National Australia Bank Ltd. added 1.3 percent to A$25.76.

A gauge of energy companies led the advance among the 10 industry groups in the regional benchmark index crude oil traded near a three-month high. Copper futures rose for the first time in four days in London. BHP Billiton Ltd., the world’s biggest mining company, rose 1.5 percent, Cnooc Ltd., China’s biggest offshore oil producer, jumped 4 percent to HK$15.66 in Hong Kong. Glencore International Plc, the world’s largest commodities trader, increased 3.1 percent to HK$55.75.

European stocks dropped for the third day in four as Italian bond yields surged to their highest since the introduction of the euro and Italy’s credit-default swaps jumped to a record.

Italian bonds tumbled, pushing two-, five-, 10- and 30-year yields to euro-era records. The 10-year note yield climbed to 7.25 percent.

Berlusconi last night said he will step down as soon as parliament passes austerity measures. He had pledged to cut spending in a bid to convince investors that Italy can manage the euro area’s second-largest debt. The government has yet to write the austerity bill, said Mario Baldassarri, head of the Senate Finance Committee.

In Greece, Prime Minister George Papandreou’s talks on forming an interim government to avert the economy’s collapse dragged into a third day as a near-agreement with the biggest opposition party stalled on European Union demands for written commitments. The makeup of Greece’s new government is to be announced today, the Associated Press reported, citing a government official who it did not name.

China’s inflation slowed by the most in almost three years, giving officials more room to support growth as industrial production cools, a report today showed. Consumer prices rose 5.5 percent in October from a year earlier, the statistics bureau said. The measure declined 0.6 percentage points from September, its biggest slide since February 2009.

National benchmark indexes fell in all of the 18 western European markets. France’s CAC 40 Index and Germany’s DAX Index retreated 2.2 percent. The U.K.’s FTSE 100 Index lost 1.9 percent.

HSBC Holdings Plc, Europe’s largest bank, retreated 5.8. The bank said pretax profit at its investment bank led by Samir Assaf fell to about $1 billion in the third quarter from a year-earlier. Bad-loan provisions increased to $3.89 billion from $3.15 billion, mainly related to its U.S. unit, the bank said.

Bank shares fell 3.7 percent, among the biggest drops of the 19 industry groups in the Stoxx 600, as Greek and Italian lenders slid. Piraeus Bank SA retreated 6.3 percent to 25.3 euro cents. Alpha Bank AE sank 9 percent to 1.11 euros.

Dexia SA, the lender being broken up after running out of short-term funding, plunged 11 percent to 37.2 euro cents. The bank said shareholder equity shrank 84 percent after the nationalization of its Belgian bank unit and declines in the value of government bond holdings.

Mediaset SpA, the broadcaster controlled by Berlusconi, tumbled 12 percent to 2.21 euros after the premier offered to resign once parliament approves stability measures.

Admiral Group sank 26 percent to 887.5 pence for the biggest decline on the Stoxx 600 and the shares’ largest retreat since 2004. The U.K. car insurer that owns the confused.com website said full-year pretax profit will be toward the lower end of analysts’ estimates.

Deutsche Post, Europe’s biggest postal service, rallied 3.8 percent to 11.10 euros. The company lifted its full-year forecast as increasing express shipments in Asia and parcel volume from Internet retailing boosted third-quarter earnings. Earnings before interest and taxes in 2011 will exceed 2.4 billion euros, the company said. That compared with an earlier prediction for Ebit at the upper end of a 2.2 billion-euro to 2.4 billion-euro range.

U.S. stocks slumped, driving the Standard & Poor’s 500 Index to its biggest decline since August, amid concern that European leaders may be unable to keep the euro zone intact as Italian yields surged to a record. Investors propelled Italy’s 10-year bond yield to close at a euro-era high of 7.25 percent after the promised exit of Prime Minister Silvio Berlusconi failed to convince them that his country can slash Europe’s second-largest debt burden.

Dow 11,780.94 -389.24 -3.20%, Nasdaq 2,621.65 -105.84 -3.88%, S&P 500 1,229.10 -46.82 -3.67%

Morgan Stanley and Goldman Sachs Group Inc. dropped at least 8.2 percent, following losses in European lenders, after LCH Clearnet SA raised the extra charge it levies on clients for trading Italian government bonds and index-linked securities.

General Motors Co. tumbled 11 percent after abandoning its target for European results. The automaker, which hasn’t turned an annual profit in Europe in more than a decade, fell after rescinding its target for break- even results in the region. Europe operations lost $292 million before interest and taxes in the quarter. GM said it no longer expects to break even on an EBIT basis before restructuring costs in Europe, citing “deteriorating economic conditions.”

Adobe Systems Inc. sank 7.7 percent on plans to cut jobs as it lessens its focus on older products. The company plans to cut 750 jobs as it lessens its focus on older products. The reduction, mostly in North America and Europe, will cost $87 million to $94 million before taxes, the company said. After the costs, net income will be 30 cents to 38 cents a share, compared with a previous forecast of 41 cents to 50 cents.

Energy and raw material producers retreated as the dollar rose, reducing the appeal of commodities. Alcoa Inc. (AA), the largest U.S. aluminum producer, slid 5.4 percent to $10.20. Chevron Corp. fell 4.2 percent to $104.28.

One stock in the S&P 500 rose today, the lowest number since June 2010. Best Buy Co., the world’s largest consumer- electronics, advanced 1.4 percent to $27.22, gaining 2.9 percent in two days.

The euro slid to a four-week low versus the dollar as Italian bond yields climbed to euro-era records after a firm raised the deposits it demands for clearing the nation’s securities, intensifying Europe’s debt crisis. The shared currency fell to a two-week low versus the yen on concern Italy will join Greece in struggling to form a new regime strong enough to implement austerity measures. LCH Clearnet SA announced the changes to its margin requirements on Italian government-debt on its website.

The 17-nation currency remained lower versus the dollar as Greek Prime Minister George Papandreou said in Athens his country’s two biggest political parties reached agreement on the creation of a national unity government after three days of talks. Papandreou will step down. He didn’t disclose the name of the new prime minister.

The dollar rose as U.S. 10-year note yields declined the most in a week as demand for refuge surged. The Dollar Index, which IntercontinentalExchange Inc. uses to track the greenback against the currencies of six major U.S. trading partners climbed 1.3 percent to 77.630.

The yen strengthened against most of its major peers as traders sought a haven. The Japanese currency and yen- denominated bonds were the most-sought assets, according to Bank of New York Mellon Corp. The yen tends to gain because Japan’s export-reliant economy doesn’t need foreign capital to balance current accounts the broadest measure of trade while the greenback tends to strengthen during periods of financial stress due to its status as the world’s reserve currency.

EUR/USD: the pair fell and has lost three figures.

GBP/USD: the pair has fallen having lost two figures.

USD/JPY: the pair holds near by Y78.70.

A heavy calendar Thursday starts at 0630GMT, with the release of French October inflation data. German HICP data and the October wholesale price data are due for release at 0700GMT. French industrial output data is released at 0745GMT, with Italian output data expected at 0900GMT. At 1215GMT, ECB Executive Board member Juergen Stark speaks on challenges for Germany and Europe, in Berlin. He speaks again at 1330GMT and again at 1800GMT. US data starts at 1330GMT, with the US Sep Intl Trade Balance data. Also at 1330GMT, the November jobless rate is released, along with import/export prices. Initial jobless claims are expected to rise 3,000 to 400,000 in the November 5 week after falling below 400,000 in the previous week. At 1900GMT, the US Oct Treasury Statement is released. The Treasury is expected to post a $104.5 billion budget gap to start the new 2012 fiscal year. October 1 was a Saturday in 2011, shifting transfer payments into September, so outlays for the current month should be smaller than in the previous year.

Resistance 3: Y78.45 (Nov 1 high)

Resistance 2: Y78.10 (Nov 8 high)

Resistance 1: Y77.90 (session high)

The current price: Y77.71

Support 1:Y77.55 (50.0% FIBO Y75.55-Y79.55)

Support 2: Y77.10 (61.8% FIBO Y75.55-Y79.55)

Support 3: Y76.65 (76.4% FIBO Y75.55-Y79.55)

Comments: the pair is on downtrend.

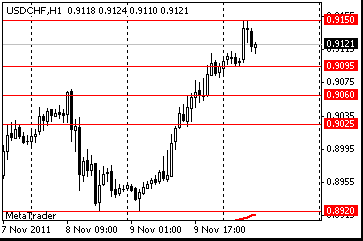

Resistance 3: Chf0.9215 (Oct 3 high)

Resistance 2: Chf0.9180 (Sep 22 high)

Resistance 1: Chf0.9150 (session high)

The current price: Chf0.9121

Support 1: Chf0.9095 (session low)

Support 2: Chf0.9060 (38.2% FIBO Chf0.9150-Chf0.8920)

Support 3: Chf0.9025 (low of the American session on Nov 9)

Comments: the pair is on uptrend. In focus resistance Chf0.9150.

Resistance 3: $1.6015 (50.0% FIBO $1.5900-$1.6130)

Resistance 2: $1.5985 (38.2% FIBO $1.5900-$1.6130)

Resistance 1: $1.5950 (23.6% FIBO $1.5900-$1.6130)

The current price: $1.5919

Support 1 : $1.5900 (session low)

Support 2 : $1.5875 (Nov 3 low)

Support 3 : $1.5840 (Sep 9 low)

Comments: the pair is on downtrend. In focus support $1.5900.

Resistance 3: $1.3685 (50.0% FIBO $1.3515-$1.3860)

Resistance 2: $1.3610 (high of the American session on Nov 9)

Resistance 1: $1.3560 (session high)

The current price: $1.3547

Support 1 : $1.3515 (session low)

Support 2 : $1.3485 (low of the European session on Sep 30)

Support 3 : $1.3415 (low of the American session on Sep 30)

Comments: the pair is on downtrend. In focus support $1.3515.

Change % Change Last

Nikkei 225 8,755 +99.93 +1.15%

Hang Seng 20,014 +335.96 +1.71%

S&P/ASX 200 4,346 +52.22 +1.22%

Shanghai Composite 2,525 +21.08 +0.84%

FTSE 100 5,460 -106.96 -1.92%

CAC 40 3,075 -68.14 -2.17%

DAX 5,830 -131.90 -2.21%

Dow 11,780.94 -389.24 -3.20%

Nasdaq 2,621.65 -105.84 -3.88%

S&P 500 1,229.10 -46.82 -3.67%

10 Year Yield 1.96% -0.11 --

Oil $95.91 +0.17 +0.18%

Gold $1,770.90 -20.70 -1.16%

00:30 Australia Changing the number of employed October 20.4K 10.3K

00:30 Australia Unemployment rate October 5.2% 5.3%

02:00 China Trade Balance, bln October 14.5 26.3

05:00 Japan Consumer Confidence October 38.6 39.3

05:00 Japan Consumer Confidence Households October 38.5

06:00 Japan Prelim Machine Tool Orders, y/y October +20.1%

06:30 France CPI, m/m October -0.1% +0.1%

06:30 France CPI, y/y October +2.2% +2.3%

07:00 Germany CPI (final), m/m September 0.0% 0.0%

07:00 Germany CPI (final), y/y September +2.5% +2.5%

07:45 France Industrial Production, m/m September +0.5% -0.6%

07:45 France Industrial Production, y/y September +4.4% +3.9%

09:00 Eurozone ECB Monthly Report

12:00 United Kingdom BoE Interest Rate Decision 0.50% 0.50%

12:15 Eurozone ECB’s Juergen Stark Speaks

13:30 Canada Trade balance, billions September -0.6 -0.5

13:30 U.S. International trade, bln September -45.6 -46.1

13:30 U.S. Initial Jobless Claims 397 402

15:40 U.S. FOMC Member Charles Evans Speaks

16:45 U.S. Fed Chairman Bernanke Speaks

19:00 U.S. Federal budget October -64.6 -110.3

23:50 Japan Tertiary Industry Index September -0.2% -0.4%

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers