- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 29-01-2019

| Time | Country | Event | Period | Previous value | Forecast |

|---|---|---|---|---|---|

| 00:30 | Australia | Trimmed Mean CPI y/y | Quarter IV | 1.8% | 1.8% |

| 00:30 | Australia | CPI, y/y | Quarter IV | 1.9% | 1.7% |

| 00:30 | Australia | CPI, q/q | Quarter IV | 0.4% | 0.4% |

| 00:30 | Australia | Trimmed Mean CPI q/q | Quarter IV | 0.4% | 0.4% |

| 05:00 | Japan | Consumer Confidence | January | 42.7 | 42.5 |

| 06:30 | France | GDP, q/q | Quarter IV | 0.3% | 0.1% |

| 07:00 | Germany | Gfk Consumer Confidence Survey | February | 10.4 | 10.3 |

| 07:45 | France | Consumer spending | December | -0.3% | -0.2% |

| 08:00 | Switzerland | KOF Leading Indicator | January | 96.3 | 97 |

| 09:00 | Switzerland | Credit Suisse ZEW Survey (Expectations) | January | -22.2 | |

| 09:30 | United Kingdom | Net Lending to Individuals, bln | December | 4.4 | 4.3 |

| 09:30 | United Kingdom | Consumer credit, mln | December | 0.924 | 0.8 |

| 09:30 | United Kingdom | Mortgage Approvals | December | 63.73 | 63 |

| 10:00 | Eurozone | Economic sentiment index | January | 107.3 | 106.8 |

| 10:00 | Eurozone | Consumer Confidence | January | -8.3 | -7.9 |

| 10:00 | Eurozone | Industrial confidence | January | 1.1 | 0.5 |

| 10:00 | Eurozone | Business climate indicator | January | 0.82 | 0.75 |

| 13:00 | Germany | CPI, m/m | January | 0.1% | -0.9% |

| 13:00 | Germany | CPI, y/y | January | 1.7% | 1.6% |

| 13:15 | U.S. | ADP Employment Report | January | 271 | 178 |

| 15:00 | U.S. | Pending Home Sales (MoM) | December | -0.7% | 0.5% |

| 15:30 | U.S. | Crude Oil Inventories | January | 7.97 | |

| 19:00 | U.S. | Fed Interest Rate Decision | 2.5% | 2.5% | |

| 19:00 | U.S. | FOMC Statement | |||

| 23:50 | Japan | Industrial Production (MoM) | December | -1.0% | -0.4% |

| 23:50 | Japan | Industrial Production (YoY) | December | 1.5% |

Major US stock indices ended mixed: the S & P 500 fell slightly, the Dow rose slightly, and the high-tech Nasdaq fell by about 0.8%, as mixed income reports and concerns about the upcoming trade negotiations between the US and China gave little incentive to recover markets from falling the day before.

Investors also awaited the start of a two-day Fed meeting. This will be the first meeting of the American regulator this year. Investors expect the Fed to take a more cautious stance on monetary policy this year than in 2018, under pressure from the peak of US corporate income and the threat of slowing economic growth both domestically and globally.

A certain impact on the course of trading has data for the United States. The Consumer Confidence Index from the Conference Board deteriorated markedly in January after it recorded a decline in December. The index now stands at 120.2 (1985 = 100), compared with 126.6 in December (revised from 128.1). Analysts had expected the index to be 124.9. The current situation index, based on consumers ’assessment of the current business and labor market conditions, fell from 169.9 to 169.6, while the expectations index, based on short-term consumer forecasts for income, business and labor market conditions, fell from 97.7 in December to 87.3 in January.

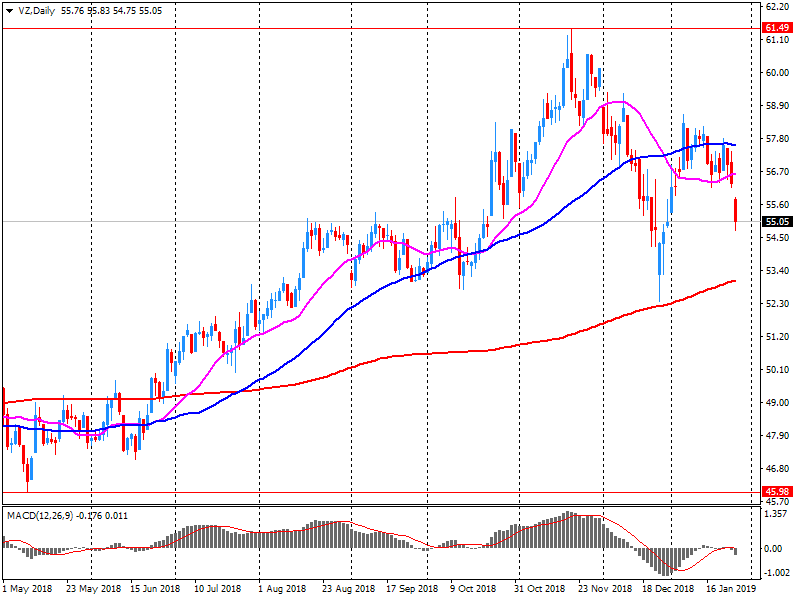

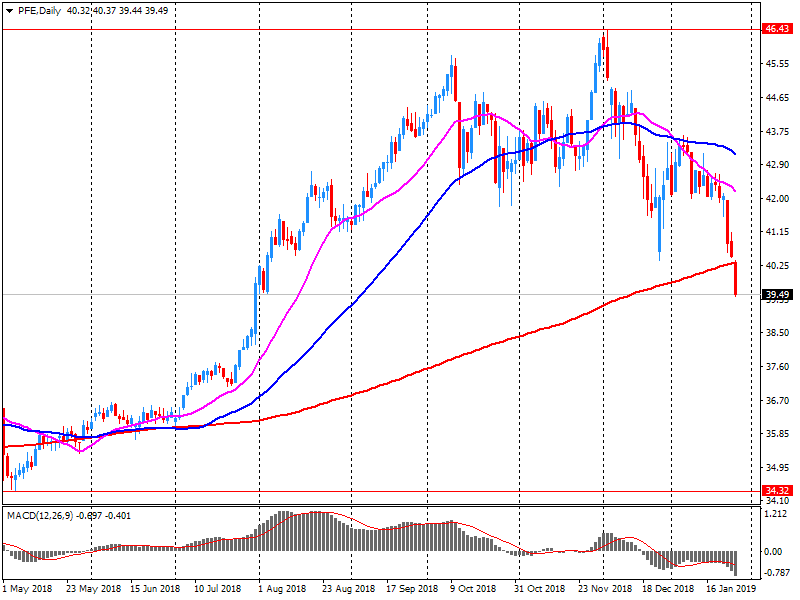

Most of the components of DOW finished trading in positive territory (16 of 30). The growth leader was Pfizer Inc. (PFE, + 3.14%). The outsider was Verizon Communications Inc. (VZ, -3.36%).

Most sectors of the S & P recorded an increase. The largest growth was shown by the industrial goods sector (+ 1.2%). The technological sector decreased more than others (-1.0%)

At the time of closing:

Dow 24,579.96 +51.74 +0.21%

S & P 500 2,640.00 -3.85 -0.15%

Nasdaq 100 7,028.29 -57.40 -0.81%

| Time | Country | Event | Period | Previous value | Forecast |

|---|---|---|---|---|---|

| 00:30 | Australia | Trimmed Mean CPI y/y | Quarter IV | 1.8% | 1.8% |

| 00:30 | Australia | CPI, y/y | Quarter IV | 1.9% | 1.7% |

| 00:30 | Australia | CPI, q/q | Quarter IV | 0.4% | 0.4% |

| 00:30 | Australia | Trimmed Mean CPI q/q | Quarter IV | 0.4% | 0.4% |

| 05:00 | Japan | Consumer Confidence | January | 42.7 | 42.5 |

| 06:30 | France | GDP, q/q | Quarter IV | 0.3% | 0.1% |

| 07:00 | Germany | Gfk Consumer Confidence Survey | February | 10.4 | 10.3 |

| 07:45 | France | Consumer spending | December | -0.3% | -0.2% |

| 08:00 | Switzerland | KOF Leading Indicator | January | 96.3 | 97 |

| 09:00 | Switzerland | Credit Suisse ZEW Survey (Expectations) | January | -22.2 | |

| 09:30 | United Kingdom | Net Lending to Individuals, bln | December | 4.4 | 4.3 |

| 09:30 | United Kingdom | Consumer credit, mln | December | 0.924 | 0.8 |

| 09:30 | United Kingdom | Mortgage Approvals | December | 63.73 | 63 |

| 10:00 | Eurozone | Economic sentiment index | January | 107.3 | 106.8 |

| 10:00 | Eurozone | Consumer Confidence | January | -8.3 | -7.9 |

| 10:00 | Eurozone | Industrial confidence | January | 1.1 | 0.5 |

| 10:00 | Eurozone | Business climate indicator | January | 0.82 | 0.75 |

| 13:00 | Germany | CPI, m/m | January | 0.1% | -0.9% |

| 13:00 | Germany | CPI, y/y | January | 1.7% | 1.6% |

| 13:15 | U.S. | ADP Employment Report | January | 271 | 178 |

| 15:00 | U.S. | Pending Home Sales (MoM) | December | -0.7% | 0.5% |

| 15:30 | U.S. | Crude Oil Inventories | January | 7.97 | |

| 19:00 | U.S. | Fed Interest Rate Decision | 2.5% | 2.5% | |

| 19:00 | U.S. | FOMC Statement | |||

| 23:50 | Japan | Industrial Production (MoM) | December | -1.0% | -0.4% |

| 23:50 | Japan | Industrial Production (YoY) | December | 1.5% |

Officials Will Make Sure U.S. Infrastructure Protect From Spying Risks

President Hasn't Made Any Decision on Whether to Drop All Tariffs

Treasury Will Make Recommendation on Tariffs After Agreement With China

No Question Chinese Economy Slowing Down, Affecting Global Growth

No Question President Wants to Do Fair Deal on Border Security, Funding

He Is Determined We Will Have Border Security

Declines to Say Whether President Would Shut Down Government Again

U.S. stock-index rose slightly on Tuesday, as stock market stabilized after a slide a day earlier driven by concerns that the fallout from the U.S.-China trade dispute could outweight corporate earnings season and weaken future profits.

Global Stocks:

Index/commodity | Last | Today's Change, points | Today's Change, % |

Nikkei | 20,664.64 | +15.64 | +0.08% |

Hang Seng | 27,531.68 | -45.28 | -0.16% |

Shanghai | 2,594.25 | -2.72 | -0.10% |

S&P/ASX | 5,874.20 | -31.40 | -0.53% |

FTSE | 6,842.11 | +95.01 | +1.41% |

CAC | 4,945.19 | +56.61 | +1.16% |

DAX | 11,242.09 | +31.78 | +0.28% |

Crude | $52.43 | +0.85% | |

Gold | $1,313.80 | +0.34% |

The S&P Home Price NSA Index, covering all nine U.S. census divisions, reported a 5.2% annual gain in November, down from 5.3% in the previous month. The 10- City Composite annual increase came in at 4.3%, down from 4.7% in the previous month. The 20-City Composite posted a 4.7% year-over-year gain, down from 5.0% in the previous month.

Las Vegas, Phoenix and Seattle reported the highest year-over-year gains among the 20 cities. In November, Las Vegas led the way with a 12.0% year-over-year price increase, followed by Phoenix with an 8.1% increase and Seattle with a 6.3% increase. Seven of the 20 cities reported greater price increases in the year ending November 2018 versus the year ending October 2018.

(company / ticker / price / change ($/%) / volume)

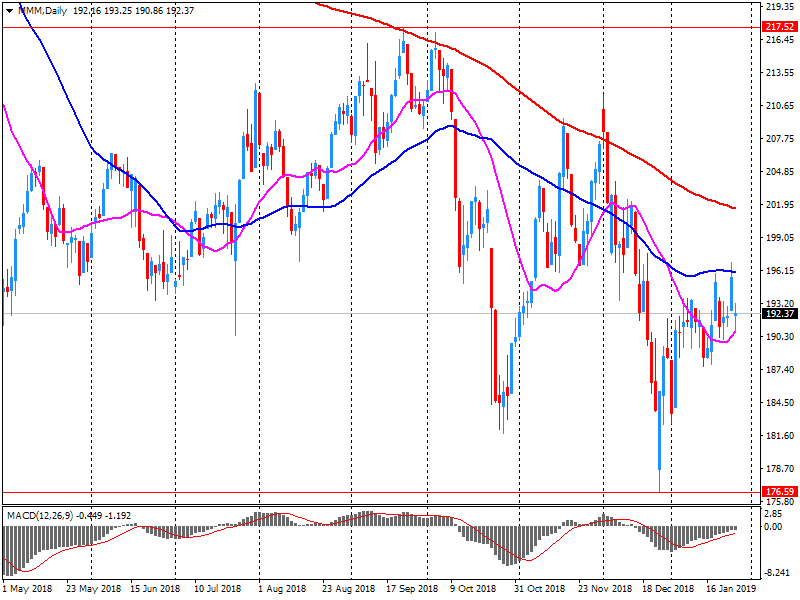

3M Co | MMM | 198.55 | 5.35(2.77%) | 88180 |

ALCOA INC. | AA | 28.15 | 0.17(0.61%) | 551 |

ALTRIA GROUP INC. | MO | 45.5 | 0.20(0.44%) | 14658 |

Amazon.com Inc., NASDAQ | AMZN | 1,636.50 | -1.39(-0.08%) | 40964 |

American Express Co | AXP | 100.8 | 0.42(0.42%) | 1011 |

Apple Inc. | AAPL | 156.6 | 0.30(0.19%) | 136299 |

AT&T Inc | T | 30.45 | -0.22(-0.72%) | 64879 |

Boeing Co | BA | 363.38 | 0.41(0.11%) | 9826 |

Caterpillar Inc | CAT | 125.65 | 1.28(1.03%) | 64451 |

Chevron Corp | CVX | 112.71 | 0.54(0.48%) | 6537 |

Cisco Systems Inc | CSCO | 45.72 | -0.03(-0.07%) | 5485 |

Citigroup Inc., NYSE | C | 64.04 | 0.19(0.30%) | 1052 |

Exxon Mobil Corp | XOM | 71.45 | 0.21(0.29%) | 3607 |

Facebook, Inc. | FB | 148.16 | 0.69(0.47%) | 45776 |

Ford Motor Co. | F | 8.7 | 0.04(0.46%) | 12857 |

Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 10.35 | 0.07(0.68%) | 68082 |

General Motors Company, NYSE | GM | 38.45 | -0.01(-0.03%) | 661 |

Goldman Sachs | GS | 199.65 | -0.07(-0.04%) | 1896 |

Hewlett-Packard Co. | HPQ | 21.99 | 0.01(0.05%) | 300 |

HONEYWELL INTERNATIONAL INC. | HON | 141 | 0.52(0.37%) | 1084 |

Intel Corp | INTC | 46.72 | 0.01(0.02%) | 25078 |

International Business Machines Co... | IBM | 134.2 | -0.07(-0.05%) | 670 |

Johnson & Johnson | JNJ | 129.22 | 0.23(0.18%) | 549 |

McDonald's Corp | MCD | 183 | -0.60(-0.33%) | 826 |

Merck & Co Inc | MRK | 72.85 | -0.07(-0.10%) | 956 |

Microsoft Corp | MSFT | 105.24 | 0.16(0.15%) | 112829 |

Pfizer Inc | PFE | 38.3 | -1.23(-3.11%) | 273228 |

Procter & Gamble Co | PG | 93.48 | -0.04(-0.04%) | 1457 |

Starbucks Corporation, NASDAQ | SBUX | 66.72 | -0.18(-0.27%) | 829 |

Tesla Motors, Inc., NASDAQ | TSLA | 295.6 | -0.78(-0.26%) | 37798 |

Twitter, Inc., NYSE | TWTR | 33.47 | 0.34(1.03%) | 60867 |

UnitedHealth Group Inc | UNH | 266.5 | -0.27(-0.10%) | 208 |

Verizon Communications Inc | VZ | 53.09 | -1.98(-3.60%) | 1096830 |

Visa | V | 137 | 1.01(0.74%) | 9685 |

Walt Disney Co | DIS | 110.77 | -0.04(-0.04%) | 896 |

Yandex N.V., NASDAQ | YNDX | 32.85 | -0.21(-0.64%) | 1483 |

American Express (AXP) upgraded to Overweight from Neutral at Atlantic Equities

We Feel Comfortable U.S. Economy Hit 3% GDP in 2018

Still Very Good Case for Hitting 3% GDP Growth in 2019

U.S. Making Significant Progress on Trade Issues

Verizon (VZ) reported Q4 FY 2018 earnings of $1.12 per share (versus $0.86 in Q4 FY 2017), beating analysts’ consensus estimate of $1.09.

The company’s quarterly revenues amounted to $34.281 bln (+1.0% y/y), generally in line with analysts’ consensus estimate of $34.446 bln.

The company also issued in-line guidance for FY 2019, projecting EPS to be similar to FY 2018’s EPS of $4.71 versus analysts’ consensus estimate of $4.73.

VZ fell to $53.37 (-3.09%) in pre-market trading.

Pfizer (PFE) reported Q4 FY 2018 earnings of $0.64 per share (versus $0.62 in Q4 FY 2017), beating analysts’ consensus estimate of $0.63.

The company’s quarterly revenues amounted to $13.976 bln (+2.0% y/y), generally in line with analysts’ consensus estimate of $13.920 bln.

The company also issued downside guidance for FY 2019, projecting EPS of $2.82-2.92 (versus analysts’ consensus estimate of $3.04) and revenues of $52-54 bln (versus analysts’ consensus estimate of $54.31 bln).

PFE fell to $38.50 (-2.61%) in pre-market trading.

3M (MMM) reported Q4 FY 2018 earnings of $2.31 per share (versus $2.10 in Q4 FY 2017), beating analysts’ consensus estimate of $2.28.

The company’s quarterly revenues amounted to $7.945 bln (-0.6% y/y), being generally in line with analysts’ consensus estimate of $7.873 bln.

The company also lowered guidance for FY 2019, projecting EPS of $10.45 to $10.90 versus analysts’ consensus estimate of $10.70.

MMM rose to $198.50 (+2.74%) in pre-market trading.

In December 2018 the total producer price index decreased by 0.5% compared with the previous month. The domestic producer price index decreased by 0.6% and the non-domestic market stayed unchanged.

The percentage change of the average of the last three months with respect to the previous three months was 1.1% (1.6% for the domestic market and stayed unchanged for the non-domestic market).

The total producer price index increased by 4.1% compared with December 2017 (5.2% on domestic market and 1.2% on foreign market).

The construction producer price index stayed unchanged in December 2018 and rose 2.1% on the same month of the previous year.

The average of the last three months with respect to the previous three months of the construction producer price stayed unchanged.

After having deteriorated significantly at the end of 2018, households’ confidence in the economic situation recovered in January 2019: the synthetic index has gained 5 points and returned to its last November level. Now standing at 91, it remains however below its long term average (100).

In January, the share of households considering it is a suitable time to make major purchases has risen sharply. The corresponding balance has gained 10 points,after experiencing a 15-point loss in December. However, it remains below its long term average.

Households’ opinion balance on their future personal situation has improved: it has gained 8 points but still remains below its long term average. Similarly, households’ opinion balance on their past financial situation has increased: it has gained 4 points but remains below its long term average.

Despite the global economic uncertainties, Swiss foreign trade set high standards in both directions of trade in 2018: exports grew at their strong-est rate (+5.7%) since 2010 in nominal terms and thus reached a new high. The same applies to imports, which even grew by 8.6% year on year and thereby exceeded the 200 billion franc mark. The trade balance showed a surplus of CHF 31.3 billion.

EUR/USD

Resistance levels (open interest**, contracts)

$1.1519 (3539)

$1.1502 (650)

$1.1484 (551)

Price at time of writing this review: $1.1436

Support levels (open interest**, contracts):

$1.1407 (2948)

$1.1374 (4184)

$1.1335 (4365)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date February, 8 is 70356 contracts (according to data from January, 28) with the maximum number of contracts with strike price $1,1700 (4525);

GBP/USD

Resistance levels (open interest**, contracts)

$1.3272 (1426)

$1.3241 (1945)

$1.3210 (1208)

Price at time of writing this review: $1.3156

Support levels (open interest**, contracts):

$1.3050 (397)

$1.2987 (368)

$1.2950 (604)

Comments:

- Overall open interest on the CALL options with the expiration date February, 8 is 23693 contracts, with the maximum number of contracts with strike price $1,3000 (1945);

- Overall open interest on the PUT options with the expiration date February, 8 is 27771 contracts, with the maximum number of contracts with strike price $1,2600 (2016);

- The ratio of PUT/CALL was 1.17 versus 1.14 from the previous trading day according to data from January, 28

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

1Q19 Earnings for Some Issuers Might Be Slightly Affected by Closure

Shutdown Could Affect U.S. GDP in First Quarter 2019

Working Assumption Is Fiscal Policy Continues to Provide Support to U.S. Domestic Demand Growth in 2019

CBO Estimates Shutdown Will Subtract About 0.2% From Real GDP in 1Q

Broad-Based Financial Implications from Shutdown for U.S. Corporations Didn't Materialize

Most Companies Continued to Monitor Closely

Goods exports fell $27 million (0.5 percent) in December 2018, with some contrasting movements across several commodity groups.

The leading contributor was exports of meat and edible offal, down $70 million (9.7 percent). Beef fell $42 million (13 percent) in value and 9.4 percent in quantity; Sheep meat fell $22 million (6.2 percent) in value and 8.5 percent in quantity.

Aluminium and aluminium articles was also down $70 million (41 percent). This movement was partly due to unusually high values and quantities of aluminium exports in December 2017. In December 2018, the value ($101 million) was close to the average monthly value over the last 24 months ($99 million).

Goods imports in December 2018 rose $323 million (6.6 percent) to $5.2 billion, with contrasting movements across several commodity groups.

Business conditions fell sharply in December, and while caution should be taken when interpreting data around the Christmas/New Year period, this outcome continues the downward trend in conditions over the second half of 2018. At face value, the fall over the past 6 months suggests a significant slowing in the momentum of activity in the business sector – especially from the highs seen earlier in the year.

The deterioration in conditions in the month was driven by declines across trading, profitability and employment and was relatively broad-based across states and industries. Conditions remain particularly weak in the retail industry which reports further ongoing deterioration. Capacity utilisation remains above average, though forward orders are below average (and falling) and alongside below average confidence suggests conditions are unlikely to rebound. Monitoring the future conditions and orders track will be critical regarding our outlook for the economy in 2019.

The 10-year Treasury note yield fell 0.9 basis point to 2.744%, after hitting an intraday high of 2.766%. The 2-year note yield inched lower by 0.6 basis point to 2.592%. The 30-year bond yield was virtually unchanged at 3.059%, according to Tradeweb data. Bond prices move in the opposite direction of yields

| Raw materials | Closed | Change, % |

|---|---|---|

| Brent | 59.8 | -2.48 |

| WTI | 52.11 | -2.45 |

| Silver | 15.72 | 0 |

| Gold | 1303.127 | 0.12 |

| Palladium | 1331.42 | -1.84 |

| Index | Change, points | Closed | Change, % |

|---|---|---|---|

| NIKKEI 225 | -124.56 | 20649 | -0.6 |

| Hang Seng | 7.77 | 27576.96 | 0.03 |

| KOSPI | -0.43 | 2177.3 | -0.02 |

| FTSE 100 | -62.12 | 6747.1 | -0.91 |

| DAX | -71.48 | 11210.31 | -0.63 |

| Dow Jones | -208.98 | 24528.22 | -0.84 |

| S&P 500 | -20.91 | 2643.85 | -0.78 |

| NASDAQ Composite | -79.18 | 7085.68 | -1.11 |

| Pare | Closed | Change, % |

|---|---|---|

| AUDUSD | 0.71637 | -0.17 |

| EURJPY | 124.909 | 0.02 |

| EURUSD | 1.1425 | 0.21 |

| GBPJPY | 143.822 | -0.44 |

| GBPUSD | 1.31551 | -0.24 |

| NZDUSD | 0.68289 | -0.01 |

| USDCAD | 1.32609 | 0.33 |

| USDCHF | 0.99187 | -0.11 |

| USDJPY | 109.325 | -0.19 |

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers