- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 29-10-2018

| Time | Country | Event | Period | Previous value | Forecast |

|---|---|---|---|---|---|

| 00:30 | Australia | Building Permits, m/m | September | -9.4% | 3% |

| 06:30 | France | GDP, q/q | Quarter III | 0.2% | 0.5% |

| 07:00 | United Kingdom | Nationwide house price index, y/y | October | 2% | |

| 07:00 | United Kingdom | Nationwide house price index | October | 0.3% | |

| 07:45 | France | Consumer spending | September | 0.8% | -0.6% |

| 08:00 | Switzerland | KOF Leading Indicator | October | 102.2 | 100.6 |

| 08:55 | Germany | Unemployment Rate s.a. | October | 5.1% | 5.1% |

| 08:55 | Germany | Unemployment Change | October | -23 | -12 |

| 10:00 | Eurozone | Business climate indicator | October | 1.21 | 1.14 |

| 10:00 | Eurozone | Industrial confidence | October | 4.7 | 3.8 |

| 10:00 | Eurozone | Economic sentiment index | October | 110.9 | 110.0 |

| 10:00 | Eurozone | Consumer Confidence | October | -2.9 | -2.7 |

| 10:00 | Eurozone | GDP (YoY) | Quarter III | 2.1% | 1.9% |

| 10:00 | Eurozone | GDP (QoQ) | Quarter III | 0.4% | 0.4% |

| 11:00 | United Kingdom | CBI retail sales volume balance | October | 23 | |

| 13:00 | Germany | CPI, m/m | October | 0.4% | 0.1% |

| 13:00 | Germany | CPI, y/y | October | 2.3% | 2.4% |

| 13:00 | U.S. | S&P/Case-Shiller Home Price Indices, y/y | August | 5.9% | 6% |

| 14:00 | U.S. | Consumer confidence | October | 138.4 | 135.8 |

| 19:30 | Canada | BOC Gov Stephen Poloz Speaks | |||

| 21:45 | New Zealand | Building Permits, m/m | September | 7.8% | |

| 23:50 | Japan | Industrial Production (MoM) | September | 0.2% | -0.2% |

| 23:50 | Japan | Industrial Production (YoY) | September | 0.2% |

Major US stock indexes have fallen markedly against the backdrop of the collapse of technology sector stocks and concerns about the escalation of the tariff war between the United States and China.

The agency Bloomberg, referring to three sources, reported that the US is preparing to announce tariffs for all remaining Chinese imports by early December if negotiations between Trump and C fail. A new list of tariffs will be compiled for the remaining $ 257 billion of goods not yet covered by tariffs, and after the 60-day public comment period they will take effect in early February, when China celebrates the New Year according to the lunar calendar. "US officials are preparing for such a scenario if the Trump-C meeting planned for the end of November in Buenos Aires does not work," Bloomberg said.

Market participants also analyzed data on personal income and consumer spending. The Commerce Department reported that US consumer spending rose for the seventh consecutive month in September, but revenues recorded the smallest increase over the past year amid moderate wage growth, suggesting that the current spending rate is unlikely to be sustainable. According to the report, consumer spending rose by 0.4 percent, as households bought more cars and spent more on health care. Economists had expected consumer spending to rise 0.4 percent in September. Adjusted for inflation, consumer spending rose by 0.3 percent. Meanwhile, personal income rose by 0.2 percent in September, which is the smallest increase since June 2017, after they increased by 0.4 percent in August.

Most of the components of DOW finished trading in the red (18 out of 30). The outsider was The Boeing Company (BA, -7.36%). The growth leader was Verizon Communications Inc. (VZ, + 1.57%).

Almost all sectors of the S & P recorded a decline. The largest decline was shown by the industrial goods sector (-2.5%). The utility sector grew the most (+ 0.5%).

At the time of closing:

Dow 24,442.92 -245.39 -0.99%

S&P 500 2,641.25 -17.44 0.66%

Nasdaq 100 7,050.29 -116.92 -1.63%

| Time | Country | Event | Period | Previous value | Forecast |

|---|---|---|---|---|---|

| 00:30 | Australia | Building Permits, m/m | September | -9.4% | 3% |

| 06:30 | France | GDP, q/q | Quarter III | 0.2% | 0.5% |

| 07:00 | United Kingdom | Nationwide house price index, y/y | October | 2% | |

| 07:00 | United Kingdom | Nationwide house price index | October | 0.3% | |

| 07:45 | France | Consumer spending | September | 0.8% | -0.6% |

| 08:00 | Switzerland | KOF Leading Indicator | October | 102.2 | 100.6 |

| 08:55 | Germany | Unemployment Rate s.a. | October | 5.1% | 5.1% |

| 08:55 | Germany | Unemployment Change | October | -23 | -12 |

| 10:00 | Eurozone | Business climate indicator | October | 1.21 | 1.14 |

| 10:00 | Eurozone | Industrial confidence | October | 4.7 | 3.8 |

| 10:00 | Eurozone | Economic sentiment index | October | 110.9 | 110.0 |

| 10:00 | Eurozone | Consumer Confidence | October | -2.9 | -2.7 |

| 10:00 | Eurozone | GDP (YoY) | Quarter III | 2.1% | 1.9% |

| 10:00 | Eurozone | GDP (QoQ) | Quarter III | 0.4% | 0.4% |

| 11:00 | United Kingdom | CBI retail sales volume balance | October | 23 | |

| 13:00 | Germany | CPI, m/m | October | 0.4% | 0.1% |

| 13:00 | Germany | CPI, y/y | October | 2.3% | 2.4% |

| 13:00 | U.S. | S&P/Case-Shiller Home Price Indices, y/y | August | 5.9% | 6% |

| 14:00 | U.S. | Consumer confidence | October | 138.4 | 135.8 |

| 19:30 | Canada | BOC Gov Stephen Poloz Speaks | |||

| 21:45 | New Zealand | Building Permits, m/m | September | 7.8% | |

| 23:50 | Japan | Industrial Production (MoM) | September | 0.2% | -0.2% |

| 23:50 | Japan | Industrial Production (YoY) | September | 0.2% |

Texas factory activity continued to expand in October, albeit at a slower pace, according to business executives responding to the Texas Manufacturing Outlook Survey. The production index, a key measure of state manufacturing conditions, was positive but declined another six points to 17.6, indicating output growth continued to abate.

Some other indexes of manufacturing activity also suggested slower expansion in October. The capacity utilization index retreated six points to 15.4, while the shipments index fell four points to 16.6. Meanwhile, the new orders index rose-pushing up four points to 18.9-and the growth rate of orders index held steady at 11.0.

U.S. stock-index futures rose on Monday, pointing to a solidly higher start after steep losses last week.

Global Stocks:

| Index/commodity | Last | Today's Change, points | Today's Change, % |

| Nikkei | 21,149.80 | -34.80 | -0.16% |

| Hang Seng | 24,812.04 | +94.41 | +0.38% |

| Shanghai | 2,542.10 | -56.74 | -2.18% |

| S&P/ASX | 5,728.20 | +63.00 | +1.11% |

| FTSE | 7,073.53 | +133.97 | +1.93% |

| CAC | 5,019.92 | +52.55 | +1.06% |

| DAX | 11,426.04 | +225.42 | +2.01% |

| Crude | $67.32 | | -0.40% |

| Gold | $1,233.30 | | -0.20% |

(company / ticker / price / change ($/%) / volume)

| ALTRIA GROUP INC. | MO | 63.24 | 0.15(0.24%) | 662 |

| Amazon.com Inc., NASDAQ | AMZN | 1,666.00 | 23.19(1.41%) | 68587 |

| Apple Inc. | AAPL | 219.51 | 3.21(1.48%) | 322987 |

| AT&T Inc | T | 29.48 | 0.39(1.34%) | 93118 |

| Barrick Gold Corporation, NYSE | ABX | 12.77 | -0.08(-0.62%) | 56719 |

| Boeing Co | BA | 361.6 | 2.33(0.65%) | 11940 |

| Caterpillar Inc | CAT | 116.7 | 1.65(1.43%) | 6253 |

| Chevron Corp | CVX | 112.8 | 1.27(1.14%) | 671 |

| Cisco Systems Inc | CSCO | 44.97 | 0.72(1.63%) | 26177 |

| Citigroup Inc., NYSE | C | 65.15 | 0.94(1.46%) | 16023 |

| Deere & Company, NYSE | DE | 135.06 | 2.06(1.55%) | 4271 |

| Exxon Mobil Corp | XOM | 78.4 | 0.87(1.12%) | 9386 |

| Facebook, Inc. | FB | 148.55 | 3.18(2.19%) | 166919 |

| FedEx Corporation, NYSE | FDX | 213.5 | 2.97(1.41%) | 194 |

| Ford Motor Co. | F | 9.3 | 0.32(3.56%) | 891415 |

| Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 11.73 | 0.23(2.00%) | 10761 |

| General Electric Co | GE | 11.43 | 0.13(1.15%) | 130636 |

| General Motors Company, NYSE | GM | 34.16 | 1.51(4.62%) | 176681 |

| Google Inc. | GOOG | 1,085.39 | 13.92(1.30%) | 15346 |

| Hewlett-Packard Co. | HPQ | 23.4 | 0.27(1.17%) | 1000 |

| Home Depot Inc | HD | 173.5 | 1.27(0.74%) | 4280 |

| HONEYWELL INTERNATIONAL INC. | HON | 145 | 3.60(2.55%) | 1134 |

| Intel Corp | INTC | 46.47 | 0.78(1.71%) | 95366 |

| International Business Machines Co... | IBM | 120.09 | -4.71(-3.77%) | 544848 |

| International Paper Company | IP | 45.65 | 0.80(1.78%) | 1400 |

| Johnson & Johnson | JNJ | 137.58 | 0.61(0.45%) | 1044 |

| JPMorgan Chase and Co | JPM | 104.66 | 1.24(1.20%) | 9758 |

| McDonald's Corp | MCD | 174.25 | 0.91(0.53%) | 359 |

| Merck & Co Inc | MRK | 71 | 0.60(0.85%) | 865 |

| Microsoft Corp | MSFT | 108.54 | 1.58(1.48%) | 93573 |

| Nike | NKE | 72.96 | 0.89(1.23%) | 3903 |

| Pfizer Inc | PFE | 42.95 | 0.35(0.82%) | 1727 |

| Procter & Gamble Co | PG | 88.14 | 0.28(0.32%) | 1225 |

| Starbucks Corporation, NASDAQ | SBUX | 58.71 | 0.64(1.10%) | 1823 |

| Tesla Motors, Inc., NASDAQ | TSLA | 342 | 11.10(3.35%) | 285383 |

| The Coca-Cola Co | KO | 46.1 | 0.18(0.39%) | 879 |

| Twitter, Inc., NYSE | TWTR | 32.9 | 0.54(1.67%) | 166376 |

| UnitedHealth Group Inc | UNH | 260.81 | 2.63(1.02%) | 1376 |

| Verizon Communications Inc | VZ | 55.99 | 0.48(0.86%) | 1841 |

| Visa | V | 140.25 | 2.51(1.82%) | 9397 |

| Wal-Mart Stores Inc | WMT | 99.45 | 0.51(0.52%) | 1313 |

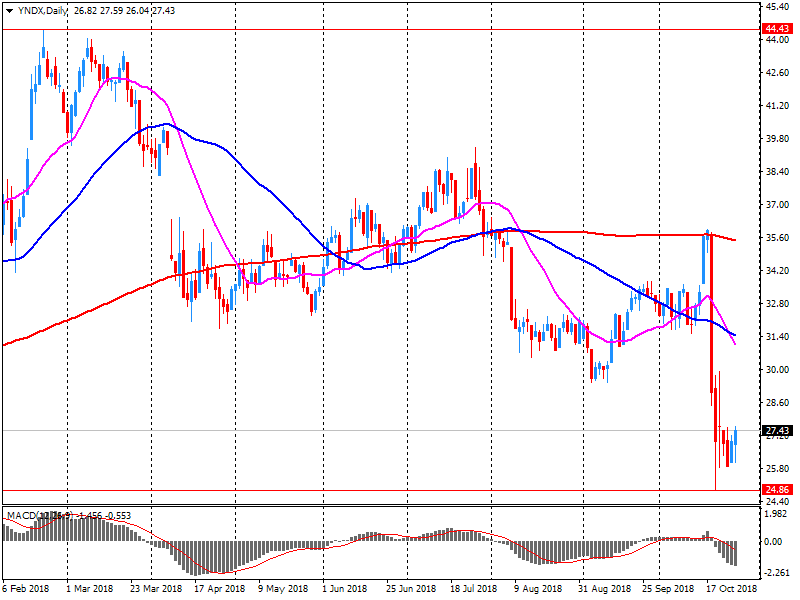

| Yandex N.V., NASDAQ | YNDX | 29.15 | 1.90(6.97%) | 232680 |

Apple (AAPL) initiated with a Buy at Jefferies; target $265

Starbucks (SBUX) target raised to $62 from $58 at Telsey Advisory Group

Verizon (VZ) target raised to $58 from $56 at Morgan Stanley

Amazon (AMZN) target lowered to $2050 from $2075 at JMP Securities

The 10-year Treasury note yield rose 2.2 basis points to 3.098%, while the 2-year note yield ticked higher by 1.6 basis points to 2.826%. The 30-year bond yield added 1.3 basis points to 3.328%. Bond prices move in the opposite direction of yields.

Personal income increased $35.7 billion (0.2 percent) in September according to estimates released today by the Bureau of Economic Analysis. Disposable personal income (DPI) increased $29.1 billion (0.2 percent) and personal consumption expenditures (PCE) increased $53.0 billion (0.4 percent).

Real DPI increased 0.1 percent in September and Real PCE increased 0.3 percent. The PCE price index

increased 0.1 percent. Excluding food and energy, the PCE price index increased 0.2 percent.

The increase in personal income in September primarily reflected increases in wages and salaries, government social benefits to persons, and rental income of persons that were partially offset by a decrease in proprietors' income.

The $33.2 billion increase in real PCE in September reflected an increase of $33.5 billion in spending for goods and a $3.5 billion increase in spending for services. Within goods, motor vehicles and parts was the leading contributor to the increase, with strong contribution from recreational goods and vehicles. Within services, the largest contributor to the increase was spending for health care that was more than offset by a decrease in spending for food services and accommodations. Detailed information on monthly real PCE spending can be found in Table 2.3.6U.

Personal outlays increased $57.9 billion in September. Personal saving was $975.7 billion in September, and the personal saving rate, personal saving as a percentage of disposable personal income, was 6.2 percent

Yandex N.V. (YNDX) reported Q3 FY 2018 earnings of RUB18.80 per share (versus RUB7.16 in Q3 FY 2017), beating analysts' consensus estimate of RUB17.66.

The company's quarterly revenues amounted to RUB32.570 bln (+39.0% y/y), beating analysts' consensus estimate of RUB30.884 bln.

YNDX rose to $28.97 (+6.31%) in pre-market trading.

October 29

Before the Open:

Yandex N.V. (YNDX). Consensus EPS RUB17.66, Consensus Revenues RUB30883.53 mln.

October 30

Before the Open:

Arconic (ARNC). Consensus EPS $0.30, Consensus Revenues $3484.09 mln.

Coca-Cola (KO). Consensus EPS $0.55, Consensus Revenues $8196.01 mln.

General Electric (GE). Consensus EPS $0.20, Consensus Revenues $29936.13 mln.

MasterCard (MA). Consensus EPS $1.68, Consensus Revenues $3862.59 mln.

Pfizer (PFE). Consensus EPS $0.75, Consensus Revenues $13532.96 mln.

After the Close:

Baidu.com (BIDU). Consensus EPS $2.56, Consensus Revenues $4051.94 mln.

eBay (EBAY). Consensus EPS $0.54, Consensus Revenues $2651.83 mln.

Facebook (FB). Consensus EPS $1.44, Consensus Revenues $13819.55 mln.

October 31

Before the Open:

General Motors (GM). Consensus EPS $1.25, Consensus Revenues $34848.26 mln.

After the Close:

American Inl (AIG). Consensus EPS $0.17, Consensus Revenues $12443.53 mln.

November 1

Before the Open:

DowDuPont (DWDP). Consensus EPS $0.72, Consensus Revenues $20222.24 mln.

After the Close:

Apple (AAPL). Consensus EPS $2.78, Consensus Revenues $61603.68 mln.

Starbucks (SBUX). Consensus EPS $0.60, Consensus Revenues $6274.76 mln.

November 2

Before the Open:

Alibaba (BABA). Consensus EPS $1.12, Consensus Revenues $12565.72 mln.

Chevron (CVX). Consensus EPS $2.09, Consensus Revenues $47171.48 mln.

Exxon Mobil (XOM). Consensus EPS $1.21, Consensus Revenues $72908.61 mln.

Consumer credit increased by £0.8bn in September. This was less than in August, as new borrowing for car finance fell sharply.

The flow of mortgage lending increased to £3.9 billion in September, following two relatively weak months.

Net finance raised by private non-financial corporations (PNFCs) was negative in September. Within this, negative movements in bank lending, and equity and commercial paper issuance were partially offset by net positive bond issuance.

The net amount of new consumer borrowing, excluding mortgages, fell to £0.8 billion in September, down from £1.2 billion in August. The fall on the month was due to weaker net borrowing for other loans and advances, which fell from £0.7 billion to £0.3 billion. Within this, new borrowing for car finance fell sharply, consistent with very weak car registration numbers in September,1 while other borrowing, such as personal loans and overdrafts, was robust. Net credit card borrowing was £0.5 billion in September, unchanged on the month and broadly in line with the average of the previous 6 months.

The annual growth rate of consumer credit slowed further in September, to 7.7%, reflecting these weaker monthly lending flows. The annual growth rate was the lowest since June 2015, and well below the peak of 10.9% in November 2016.

In September 2018 the total producer price index rose by 0.4% compared with the previous month. Domestic and non-domestic producer price indexes increased by 0.4% and 0.1%, respectively.

The percentage change of the average of the last three months with respect to the previous three months was 2.1% (2.8% for the domestic market and 0.3% for the non-domestic market).

The total producer price index increased by 4.7% compared with September 2017 (5.6% on domestic market and 2.0% on foreign market).

The construction producer price index was down 0.1% in September 2018 wih respect to the previous month, and rose by 1.6% on the same month of the previous year.

The average of the last three months with respect to the previous three months of the construction producer increased by 0.8%.

A positive start of tradin expected, after most Asian stock indices again suffered losses, although less significant than last week. Futures on U.S stock indexes are in the fla area, and their rebound from Friday's lows can be expected to continue.

Standard & Poor's rating agency maintained Italy's credit ratings, but lowered its outlook to negative from stable.

The agency left the debt rating at BBB, two points above the garbage status.

"The parameters of the economic and fiscal policies of the Italian government affect the prospects for economic growth in the country, which is a critical driver of the trajectory of public debt to GDP," the report says.

The negative outlook reflects the risk associated with the government's decision to further increase government borrowing, which will weigh on the country's growth prospects.

"In our opinion, the government's planned economic and fiscal policy parameters have undermined investor confidence, as evidenced by the growth in government debt yields," Standard & Poor's warned.

Japan's retail sales dropped for the first time in four months in September, the Ministry of Economy, according to rttnews.

Retail sales fell 0.2 percent month-on-month, in line with expectations but reversed a 0.9 percent rise in August.

The drop in retail sales in September suggests that consumer spending fell yet again in the third quarter, said Marcel Thieliant, an economist at Capital Economics. That is one reason to expect GDP to contract in third quarter.

On a yearly basis, retail sales growth eased to 2.1 percent in September from 2.7 percent in August. The annual rate also matched economists' expectations.

On Friday, the IMF Executive Board completed its first review of the Argentine 3-year Stand-By Arrangement (SBA). As a result, the revised SBA was upsized to $56.3 billion (SDR40.71BN), up from $50bn under the original program of which $15bn were disbursed in June.

-

IBM to Buy Red Hat for $190 Per Share

-

Deal for Red Hat has Total Enterprise Value of $34 Billion

-

Red Hat to Operate as a Distinct Unit Within IBM's Hybrid Cloud Team

Despite the monthly pause, the overall trend of decline in sales remains in train. Sales in the September quarter were 4.7 per cent lower than in the previous quarter and 8.0 per cent lower than in the September 2017 quarter. The monthly increase in sales was geographically widespread, with all but one of the mainland states posting monthly increases. Queensland was the outlier, experiencing a steep fall of 10.8 per cent during the month.

EUR/USD

Resistance levels (open interest**, contracts)

$1.1523 (614)

$1.1503 (707)

$1.1476 (91)

Price at time of writing this review: $1.1393

Support levels (open interest**, contracts):

$1.1352 (3587)

$1.1317 (3227)

$1.1273 (2740)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date November, 19 is 86997 contracts (according to data from October, 26) with the maximum number of contracts with strike price $1,1450 (5920);

GBP/USD

Resistance levels (open interest**, contracts)

$1.2971 (897)

$1.2946 (318)

$1.2909 (621)

Price at time of writing this review: $1.2833

Support levels (open interest**, contracts):

$1.2763 (1869)

$1.2733 (1429)

$1.2700 (1094)

Comments:

- Overall open interest on the CALL options with the expiration date November, 19 is 24943 contracts, with the maximum number of contracts with strike price $1,3500 (3217);

- Overall open interest on the PUT options with the expiration date November, 19 is 31890 contracts, with the maximum number of contracts with strike price $1,3000 (3117);

- The ratio of PUT/CALL was 1.28 versus 1.24 from the previous trading day according to data from October, 26

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

| Raw materials | Closing price | % change |

| Oil | $67.74 | +0.22% |

| Gold | $1,235.40 | -0.03% |

| Index | Change items | Closing price | % change |

| Nikkei | -84.13 | 21184.60 | -0.40% |

| SHANGHAI | -4.95 | 2598.85 | -0.19% |

| ASX 200 | +1.10 | 5665.20 | +0.02% |

| KOSPI | -36.15 | 2027.15 | -1.75% |

| FTSE 100 | -64.54 | 6939.56 | -0.92% |

| DAX | -106.50 | 11200.62 | -0.94% |

| CAC 40 | -64.93 | 4967.37 | -1.29% |

| DJIA | -296.24 | 24688.31 | -1.19% |

| S&P 500 | -151.12 | 7167.21 | -2.07% |

| NASDAQ | -46.88 | 2658.69 | -1.73% |

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers