- Analytics

- News and Tools

- Market News

Analytics, News, and Forecasts for CFD Markets: stock news — 26-07-2016.

(index / closing price / change items /% change)

Nikkei 225 16,383.04 -1.43%

Shanghai Composite 3,050.18 +1.14%

S&P/ASX 200 5,537.47 +0.07%

Xetra DAX 10,247.76 +0.49%

FTSE 100 6,724.03 +0.21%

CAC 40 4,394.77 +0.15%

S&P 500 2,169.18 +0.03%

Dow Jones 18,473.75 -0.10%

S&P/TSX Composite 14,550 +0.36%

Earnings from McDonald's Corp. to Caterpillar Inc. tugged U.S. stocks in opposite directions, leaving benchmark indexes little changed as investors turned attention to Wednesday's Federal Reserve policy decision.

Housing data that showed the biggest gain in new-home sales in eight years bolstered optimism in the economy and raised the specter that the Fed may strike a more hawkish tone on rates after its two-day meeting. Apple Inc. is slated to report results after the close of trading.

The rally that pushed the S&P 500 up for four straight weeks has faltered as the Fed kicks off a two-day meeting, with economists estimating the central bank will keep borrowing costs unchanged at its conclusion on Wednesday. Traders will also focus on earnings, with 45 companies in the S&P 500 scheduled to report results on Tuesday, including Apple Inc.

Traders are pricing in less than even odds of a rate increase until at least March 2017. While recent economic data have beaten forecasts, Chair Janet Yellen and her colleagues have emphasized a gradual pace of tightening. On Tuesday, data showed consumer confidence fell by less than forecast, while new-home sales rose in June to the highest level in more than eight years. Home prices in 20 U.S. cities rose less than projected in May from a year earlier.

Major U.S. stock-indexes demonstrated mixed dynamics as a number of companies (including McDonald's (MCD)), provided disappointing quarterly results. McDonald's reported Q2 earnings of $1.45 per share, beating analysts' consensus estimate of $1.39. At the same time, the company's quarterly revenues reduced by 3.6% y/y to $6.265 bln, strictly in-line with analysts' consensus estimate. Market participants are waiting for earnings reports from Apple (AAPL) and Twitter (TWTR), which are set to be published after the market's close. In addition, investors remain cautious ahead of the U.S.Federal Reserve meeting this week.

Dow stocks mixed (15 in positive area, 15 in negative). Top looser - McDonald's Corp. (MCD, -4.18%). Top gainer - Caterpillar Inc. (CAT, +4.03%).

Almost all S&P sectors in positive area. Top gainer - Conglomerates (+1.2%). Top looser - Utilities (-0.4%).

At the moment:

Dow 18388.00 -32.00 -0.17%

S&P 500 2162.50 +0.25 +0.01%

Nasdaq 100 4661.75 +8.00 +0.17%

Crude Oil 42.83 -0.30 -0.70%

Gold 1319.30 -0.20 -0.02%

U.S. 10yr 1.57 0.00

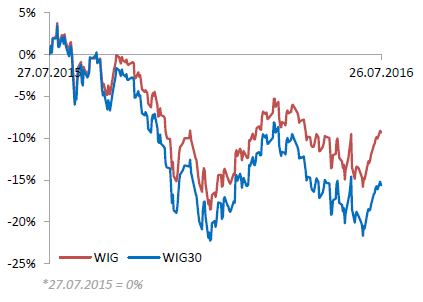

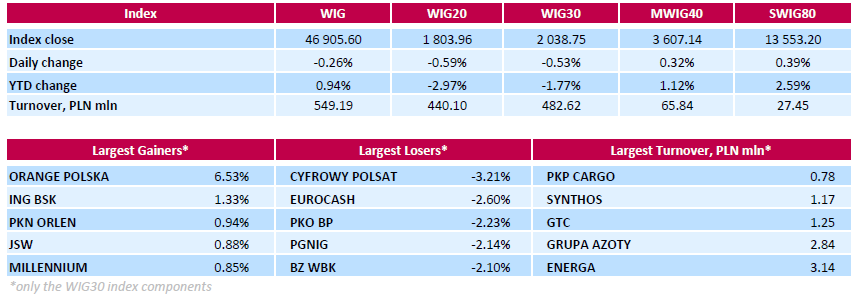

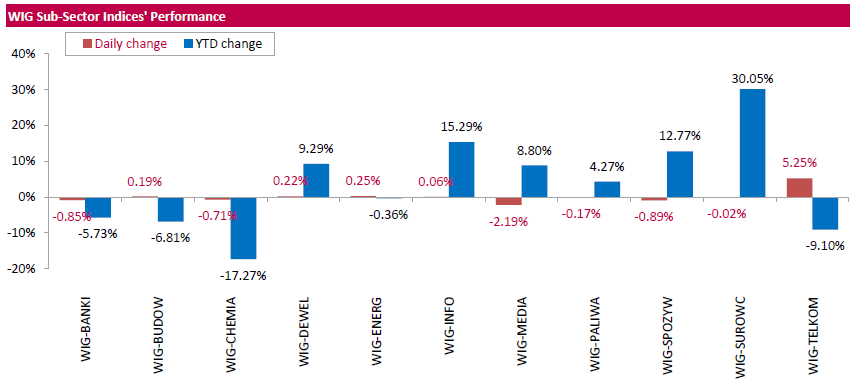

Polish equity market closed lower on Tuesday. The broad market benchmark, the WIG Index, fell by 0.26%. Sector performance within the WIG Index was mixed. Media stocks (-2.19%) tumbled the most, while telecoms (+5.25%) fared the best.

The large-cap stocks dropped by 0.53%, as measured by the WIG30 Index. In the index basket, media group CYFROWY POLSAT (WSE: CPS) recorded the biggest drop, down 3.21%. It was followed by FMCG-wholesaler EUROCASH (WSE: EUR), oil and gas producer PGNIG (WSE: PGN) and two banks PKO BP (WSE: PKO) and BZ WBK (WSE:BZW), declining by 2.1%-2.6%. At the same time, telecommunication services provider ORANGE POLSKA (WSE: OPL) was the strongest performer, climbing by 6.53%.

The market in the US started from moderate pros that looks comfortable in the ongoing from several days consolidation. A series of lower shadow indicates that strong demand is still present. Nevertheless contracts set new session highs what improves sentiment in Europe. Today begins a two-day meeting of the FOMC and tomorrow's message will be the first one, which may have influence on the market.

Since yesterday, almost completely nothing happening on the market of the zloty, which pairs USD / PLN and EUR / PLN entered into apathy. These fluctuations are a response to changes in the eurodollar. It also shows that foreign capital does not perform at the moment major movements in our market. This is evident also on the Warsaw Stock Exchange, especially after today turnover (only PLN 300 mln on the WIG20).

U.S. index futures were little changed as investors awaited a Federal Reserve update for clues on the trajectory of interest-rate increases and weighed earnings reports.

Global Stocks:

Nikkei 16,383.04 -237.25 -1.43%

Hang Seng 22,129.73 +136.29 +0.62%

Shanghai 3,050.18 +34.35 +1.14%

FTSE 6,728.57 +18.44 +0.27%

CAC 4,390.81 +2.81 +0.06%

DAX 10,234.19 +35.95 +0.35%

Crude $42.50 (-1.46%)

Gold $1320.00 (+0.04%)

(company / ticker / price / change ($/%) / volume)

| ALCOA INC. | AA | 10.4 | -0.09(-0.858%) | 10750 |

| 3M Co | MMM | 177.56 | -2.07(-1.1524%) | 4453 |

| ALTRIA GROUP INC. | MO | 68.79 | -0.01(-0.0145%) | 400 |

| Amazon.com Inc., NASDAQ | AMZN | 741.17 | 1.56(0.2109%) | 9021 |

| Apple Inc. | AAPL | 97.25 | -0.09(-0.0925%) | 103371 |

| AT&T Inc | T | 42.78 | -0.16(-0.3726%) | 2355 |

| Barrick Gold Corporation, NYSE | ABX | 20.12 | 0.29(1.4624%) | 98845 |

| Caterpillar Inc | CAT | 78 | -0.69(-0.8769%) | 103360 |

| Chevron Corp | CVX | 102.42 | -0.65(-0.6306%) | 4250 |

| Cisco Systems Inc | CSCO | 30.9 | 0.11(0.3573%) | 2385 |

| Citigroup Inc., NYSE | C | 43.98 | -0.06(-0.1362%) | 12545 |

| Deere & Company, NYSE | DE | 78.3 | 0.38(0.4877%) | 10000 |

| E. I. du Pont de Nemours and Co | DD | 69.79 | 0.91(1.3211%) | 4700 |

| Exxon Mobil Corp | XOM | 91.5 | -0.70(-0.7592%) | 10722 |

| Facebook, Inc. | FB | 121.9 | 0.27(0.222%) | 93498 |

| Ford Motor Co. | F | 13.74 | 0.06(0.4386%) | 69070 |

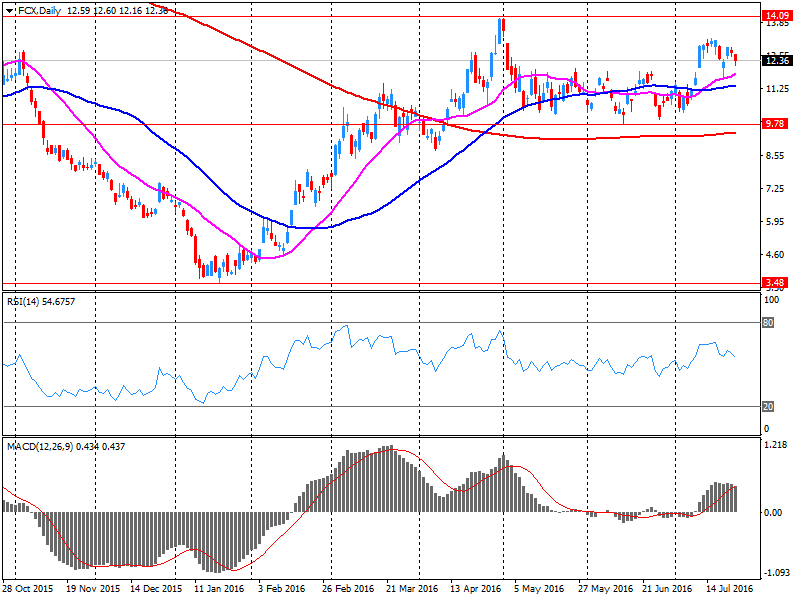

| Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 11.65 | -0.73(-5.8966%) | 1142584 |

| General Electric Co | GE | 31.6 | -0.04(-0.1264%) | 4342 |

| General Motors Company, NYSE | GM | 32.26 | 0.20(0.6238%) | 2523 |

| Google Inc. | GOOG | 740 | 0.23(0.0311%) | 1683 |

| HONEYWELL INTERNATIONAL INC. | HON | 115.65 | 0.16(0.1385%) | 150 |

| Intel Corp | INTC | 34.68 | -0.01(-0.0288%) | 7863 |

| International Business Machines Co... | IBM | 162.55 | -0.10(-0.0615%) | 402 |

| Johnson & Johnson | JNJ | 125 | 0.11(0.0881%) | 568 |

| JPMorgan Chase and Co | JPM | 63.71 | -0.16(-0.2505%) | 325 |

| McDonald's Corp | MCD | 124.2 | -3.20(-2.5118%) | 490671 |

| Microsoft Corp | MSFT | 56.63 | -0.10(-0.1763%) | 10122 |

| Nike | NKE | 57 | -0.14(-0.245%) | 6240 |

| Pfizer Inc | PFE | 36.84 | 0.06(0.1631%) | 525 |

| Procter & Gamble Co | PG | 85.8 | 0.00(0.00%) | 100 |

| Starbucks Corporation, NASDAQ | SBUX | 58.72 | 0.77(1.3287%) | 55815 |

| Tesla Motors, Inc., NASDAQ | TSLA | 227.03 | -2.98(-1.2956%) | 57508 |

| The Coca-Cola Co | KO | 45.55 | -0.02(-0.0439%) | 3429 |

| Twitter, Inc., NYSE | TWTR | 18.58 | -0.07(-0.3753%) | 96758 |

| United Technologies Corp | UTX | 106.5 | 1.85(1.7678%) | 32981 |

| Verizon Communications Inc | VZ | 55.7 | -0.17(-0.3043%) | 40042 |

| Visa | V | 79.11 | 0.17(0.2154%) | 1185 |

| Wal-Mart Stores Inc | WMT | 73.74 | -0.01(-0.0136%) | 1435 |

| Walt Disney Co | DIS | 96.95 | -0.44(-0.4518%) | 9290 |

| Yahoo! Inc., NASDAQ | YHOO | 38.11 | -0.21(-0.548%) | 27441 |

| Yandex N.V., NASDAQ | YNDX | 20.72 | -0.30(-1.4272%) | 7300 |

Upgrades:

Downgrades:

Walt Disney (DIS) downgraded to Market Perform from Outperform at FBR Capital; target lowered to $108 from $111

Yahoo! (YHOO) downgraded to Equal-Weight from Overweight at Morgan Stanley

Other:

Starbucks (SBUX) added to Conviction Buy List at Goldman

McDonald's reported Q2 FY 2016 earnings of $1.45 per share (versus $1.26 in Q2 FY 2015), beating analysts' consensus estimate of $1.39.

The company's quarterly revenues amounted to $6.265 bln (-3.6% y/y), strictly in-line with analysts' consensus estimate.

MCD fell to $123.00 (-3.45%) in pre-market trading.

Freeport-McMoRan reported Q2 FY 2016 loss of $0.02 per share (versus income of $0.14 in Q2 FY 2015), missing analysts' consensus estimate of a loss of $0.01.

The company's quarterly revenues amounted to $3.334 bln (-15.3% y/y), missing analysts' consensus estimate of $3.684 bln.

FCX fell to $11.61 (-6.22%) in pre-market trading.

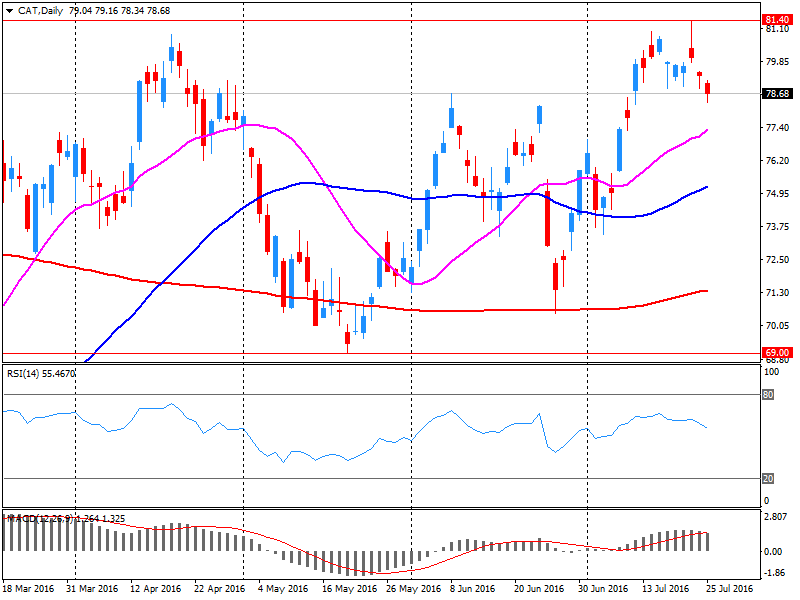

Caterpillar reported Q2 FY 2016 earnings of $1.09 per share (versus $1.27 in Q2 FY 2015), beating analysts' consensus estimate of $0.96.

The company's quarterly revenues amounted to $10.342 bln (-16% y/y), beating analysts' consensus estimate of $10.131 bln.

CAT fell to $77.97 (-0.91%) in pre-market trading.

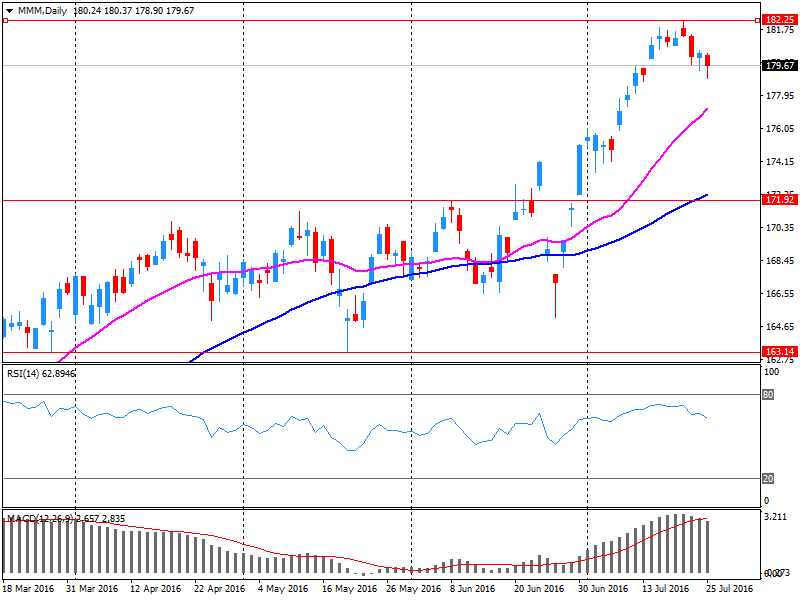

3M Company reported Q2 FY 2016 earnings of $2.08 per share (versus $2.02 in Q2 FY 2015), beating analysts' consensus estimate of $2.07.

The company's quarterly revenues amounted to $7.662 bln (-0.3% y/y), slightly missing analysts' consensus estimate of $7.711 bln.

MMM fell to $176.91 (-1.51%) in pre-market trading.

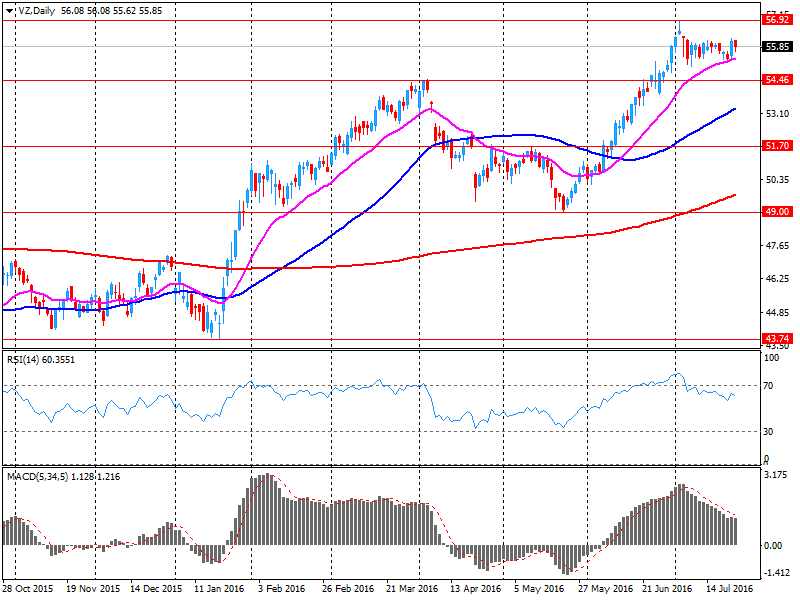

Verizon reported Q2 FY 2016 earnings of $0.94 per share (versus $1.04 in Q2 FY 2015), beating analysts' consensus estimate of $0.93.

The company's quarterly revenues amounted to $30.532 bln (-5.3% y/y), slightly missing analysts' consensus estimate of $30.968 bln.

VZ closed Monday's trading session at $55.87 (-0.41%).

United Tech reported Q2 FY 2016 earnings of $1.82 per share (versus $1.81 in Q2 FY 2015), beating analysts' consensus estimate of $1.68.

The company's quarterly revenues amounted to $14.874 bln (+1.3% y/y), beating analysts' consensus estimate of $14.693 bln.

UTX closed Monday's trading session at $104.65 (-0.46%).

First half of trading on the Warsaw Stock Exchange was marked by the return of most of yesterday's approach and return to the level of 1,800 points in the case of the WIG20 index. Weaker are banks, which may result from the inferior attitude of banks in Europe, where Commerzbank results were bad adopted. The German DAX after declines returned on the green side of the market, and discount of the CAC40 dwindled to 0.2%. We may see that investors are looking for a balance, and the DAX maintains a slight upward trend of recent days.

At the halfway point of the session the WIG20 index reached the level of 1, 801 points (-0,73%).

DuPont reported Q2 FY 2016 earnings of $1.24 per share (versus $1.18 in Q2 FY 2015), beating analysts' consensus estimate of $1.10.

The company's quarterly revenues amounted to $7.061 bln (-0.8% y/y), beating analysts' consensus estimate of $6.980 bln.

DD closed Monday's trading session at $68.88 (+0.66%).

WIG20 index opened at 1812.16 points (-0.14%)

WIG 46997.25 -0.06%

WIG30 2046.45 -0.16%

mWIG40 3600.50 0.14%

*/ - change to previous close

The futures market started the session from a fall of 0.11% to 1,811 points. The cash market (WIG20 index) opened with a drop of 0.14% to 1,812 points. In Euroland the opening of the session and the first bars run neutrally. Locally company results are accepted peacefully and share prices both of Millennium (WSE: MIL) and Orange (WSE: OPL) does not differ much from yesterday's close. The same morning does not bring greater changes and the session begins roughly where yesterday was over.

Yesterday's session in the US ended with a decline of 0.3%, and in the morning the American contracts are traded on neutral levels. This means that there has not been a larger correction, and the side trend close to maxima continues. This is a good news for the Warsaw market, which ended yesterday's session high and today may have relative easy start. The moods in Asia are balanced and on most parquets there are no major changes. In plus stands out Hong Kong with an increase of more than 1% and in minus falls Tokyo with a loss of approx. 1,2% as a result of the strengthening yen.

Investors on the Warsaw Stock Exchange must remember that at the end of the week in the Parliament is to appear presidential draft of law on foreign currency loans. This means that this week will be important from the point of view of local banks.

In today's macro calendar's most important publication will be consumer confidence index Conference Board, but like yesterday's Ifo, it should not permanently affect moods, as these will depend on the upcoming decision of major central banks, that is what tomorrow will announce the Fed and the BoJ on Friday.

European stocks ended a volatile session with small gains as optimism over upbeat earnings and deal-related news outweighed a slump in oil prices.

The Stoxx Europe 600 SXXP, +0.18% rose 0.2% to settle at 340.93, posting its first rise in three sessions.

U.S. stocks retreated from record levels to close lower Monday, as investors turned cautious ahead of a busy week of earnings and central bank meetings.

Stocks pared early losses, but the S&P 500 SPX, -0.30% closed down 6.55 points, or 0.3%, at 2,168.48, with all sectors finishing lower except consumer discretionary, which logged a fractional gain.

The Dow Jones Industrial Average DJIA, -0.42% finished down 77.79 points, or 0.4%, at 18,493.06, trimming what had been a 118-point deficit.

Meanwhile the Nasdaq Composite Index COMP, -0.05% shed 2.53 points, or 0.1%, to close at 5,097.63. Earlier in the session, the index had been down nearly 18 points.

The Federal Reserve kicks off its monetary policy meeting on Tuesday and will announce its decision on Wednesday at 2 p.m. Eastern time. The central bank is widely expected to hold interest rates steady and stop short of signaling a possible rate increase in September because of continued uncertainty about the economic outlook.

Caution gripped Asian markets on Tuesday, sending the safe-haven yen scampering higher ahead of central bank meetings in the United States and Japan, while a fresh skid in oil dampened energy stocks.

Japan's Nikkei .N225 shed 1.5 percent, with investors seemingly unimpressed by a Nikkei report the government planned a direct fiscal stimulus of around 6 trillion yen ($56 billion) over the next few years.

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers