- Analiza

- Novosti i instrumenti

- Vesti sa tržišta

- USD Index loses the grip and revisits 109.50

USD Index loses the grip and revisits 109.50

- The index comes under pressure and slips back to 109.50.

- The Federal Reserve starts its 2-day meeting later on Tuesday.

- Housing Starts, Building Permits next of note in the US calendar.

The USD Index (DXY), which gauges the greenback vs. a bundle of its main rivals, extends the gradual decline and hovers around the 109.50 region on turnaround Tuesday.

USD Index looks prudent ahead of FOMC

The index so far clinches its third consecutive daily pullback and extends the corrective downside from last week’s peaks past the 110.00 hurdle amidst the lack of a clear direction in the global markets and swelling cautiousness ahead of the FOMC event on Wednesday.

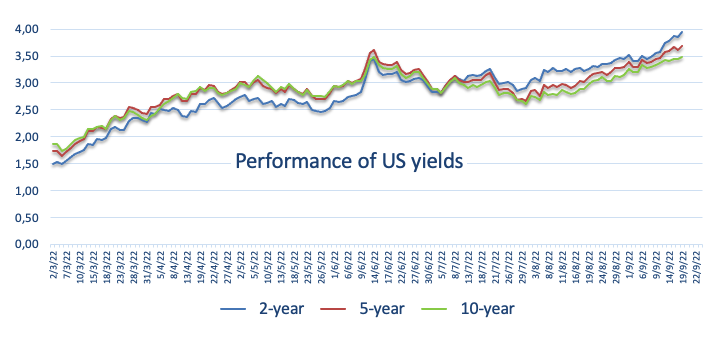

Some loss of momentum in US yields also accompany the slow decline in the dollar on Tuesday, as market participants seem to have already fully priced in a ¾ point interest rate raise by the Fed on Wednesday. Despite a 100 bps rate hike still remains on the table, its probability has dwindled to around 16% according to CME Group’s FedWatch Tool.

In the US data space, the housing sector will take centre stage in light of the publication of Building Permits and Housing Starts for the month of August.

What to look for around USD

The dollar grinds lower after climbing as high as the area above the 110.00 barrier in past days.

Bolstering the dollar’s underlying positive stance appears the firmer conviction of the Federal Reserve to keep hiking rates until inflation looks well under control regardless of a likely slowdown in the economic activity and some loss of momentum in the labour market.

Looking at the more macro scenario, the greenback appears propped up by the Fed’s divergence vs. most of its G10 peers in combination with bouts of geopolitical effervescence and occasional re-emergence of risk aversion.

Key events in the US this week: Building Permits, Housing Starts (Tuesday) – MBA Mortgage Applications, Existing Home Sales, FOMC Interest Rate decision, Powell press conference (Wednesday) – Initial Claims, CB Leading Index (Thursday) – Flash Manufacturing/Services PMIs, Powell speech (Friday).

Eminent issues on the back boiler: Hard/soft/softish? landing of the US economy. Prospects for further rate hikes by the Federal Reserve vs. speculation over a recession in the next months. Geopolitical effervescence vs. Russia and China. US-China persistent trade conflict.

USD Index relevant levels

Now, the index is retreating 0.04% at 109.54 and faces the next contention at 107.68 (monthly low September 13) followed by 107.58 (weekly low August 26) and finally 105.88 (100-day SMA). On the upside, a breakout of 110.26 (weekly high September 16) would expose 110.78 (2022 high September 7) and then 111.90 (weekly high September 6 2002).

© 2000-2026. Sva prava zaštićena.

Sajt je vlasništvo kompanije Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

Svi podaci koji se nalaze na sajtu ne predstavljaju osnovu za donošenje investicionih odluka, već su informativnog karaktera.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Izvršenje trgovinskih operacija sa finansijskim instrumentima upotrebom marginalne trgovine pruža velike mogućnosti i omogućava investitorima ostvarivanje visokih prihoda. Međutim, takav vid trgovine povezan je sa potencijalno visokim nivoom rizika od gubitka sredstava. Проведение торговых операций на финанcовых рынках c маржинальными финанcовыми инcтрументами открывает широкие возможноcти, и позволяет инвеcторам, готовым пойти на риcк, получать выcокую прибыль, но при этом неcет в cебе потенциально выcокий уровень риcка получения убытков. Iz tog razloga je pre započinjanja trgovine potrebno odlučiti o izboru odgovarajuće investicione strategije, uzimajući u obzir raspoložive resurse.

Upotreba informacija: U slučaju potpunog ili delimičnog preuzimanja i daljeg korišćenja materijala koji se nalazi na sajtu, potrebno je navesti link odgovarajuće stranice na sajtu kompanije TeleTrade-a kao izvora informacija. Upotreba materijala na internetu mora biti praćena hiper linkom do web stranice teletrade.org. Automatski uvoz materijala i informacija sa stranice je zabranjen.

Ako imate bilo kakvih pitanja, obratite nam se pr@teletrade.global.

транcфери