- Analiza

- Novosti i instrumenti

- Vesti sa tržišta

Novosti i prognoe: devizno tržište od 28-08-2022

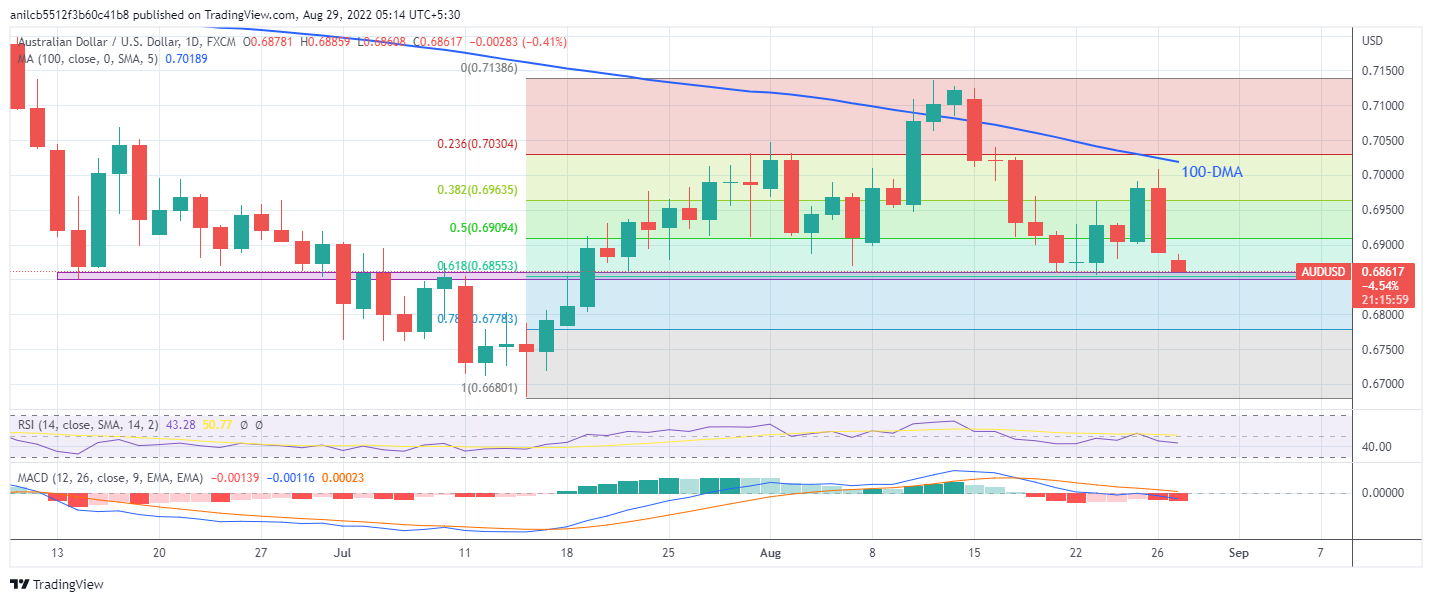

- AUD/USD takes offers to extend Friday’s pullback from one-week high.

- Downbeat oscillators, U-turn from 100-DMA keep sellers hopeful.

- 78.6% Fibonacci retracement may test bears before highlighting the yearly low.

AUD/USD remains on the back foot at 0.6861, extending Friday’s south-run while attacking a 2.5-month-old horizontal support area amid Monday’s Asian session. In doing so, the Aussie pair marks another attempt to conquer the key support zone, after failing the last week.

It’s worth noting that the oscillators like RSI (14) and the MACD appear more bearish during this time and can help the quote to conquer the aforementioned key support zone around 0.6855-50.

Following that, the 78.6% Fibonacci retracement level of July-August upside, near 0.6780, may act as an intermediate halt during the expected south-run targeting the yearly low surrounding 0.6680 marked in July.

On the contrary, the 50% Fibonacci retracement level near 0.6910 guards the quote’s immediate recovery ahead of the 100-DMA resistance close to 0.7020.

Should the quote crosses the 0.7020 hurdle, the early August high near 0.7050 may test the AUD/USD bulls before highlighting the monthly peak of 0.7136.

Overall, AUD/USD bears keep the reins but the quote’s further downside hinges on its ability to conquer the 0.6850 support.

AUD/USD: Daily chart

Trend: Further weakness expected

South Korea's Vice Finance Minister Yong-beom Kim said on Monday that they “will respond to herd-like behaviors in financial markets.”

He added that they “need to monitor the financial market.”

Yong-beom Kim said on Friday that “we are monitoring the fx market.”

His comments come as Yonhap news agency reports that the government may increase city gas rates due to rising costs and a weaker won.

Earlier on, South Korea's new central bank Governor Rhee Chang-yong said that “rising US interest rates will lead to higher inflation in Korea via won.”

Market reaction

USD/KRW was last seen trading at 1,342, flat on the day. The South Korean won (KRW) licks its wounds after falling sharply against the US dollar on Friday after Fed Chair Jerome Powell’s hawkish stance.

Liz Truss, the UK Foreign Minister and the leading contender in the Conservative Party’s leadership race, is likely to officially declare China as an ‘acute threat’, The Times reports, citing allies of Truss.

Key takeaways

She will reshape foreign policy if she becomes prime minister

Will reopen the integrated review, published last year, which set out British priorities in diplomacy and defence over the next decade.

China was described as a “systemic competitor” but the review argued that the UK should deepen its trading relationship with Beijing.

China would be elevated to a similar status as Russia, which is defined in the review as an “acute threat”.

Market reaction

Amidst risk-aversion, GBP/USD is extending losses below 1.1700, the lowest level since March 2020. The pound could be hurt further by the above comments.

The spot is losing 0.48% on the day to trade at 1.1688, as of writing.

- USD/JPY catches a fresh bid in Asia on renewed USD buying.

- Powell, Kuroda underscore Fed-BOJ monetary policy divergence.

- The triangle breakout on the 1D chart puts focus back on 139.39.

USD/JPY is rising for the second straight day on Monday, storming through the 138.00 hurdle for the first time in a week. The extension of the US dollar recovery amid broad risk-aversion and hawkish rhetoric from Fed Chair Jerome Powell is boding well for the currency pair.

However, the main catalyst behind the latest leg higher in the spot could be linked to the widening Fed-BOJ monetary policy divergence after Powell signaled a continuation of the Fed tightening cycle in coming months to tame inflation while BOJ Governor Haruhiko Kuroda said that the central bank will stick to its easing policy stance “until wages and prices rise in a stable and sustainable manner.”

Both central banks’ leaders delivered remarks on the economic and policy outlooks at the Kansas City Fed’s Jackson Hole Symposium held on August 25-27. Next of relevance for the major remains the US ISM business surveys and Nonfarm Payrolls due later this week, as Monday lacks top-tier economic events.

Meanwhile, markets will also pay close attention to the repricing of the Fed rate hike bets for September, in light of the incoming data. At the start of the week, markets are wagering a 64% probability of a 75 bps Fed rate hike next month, up from 61% seen on Friday.

From a short-term technical perspective, bulls are likely to flex their muscles going forward, especially after the pair validated an upside breakout from a triangle on the daily chart on Friday.

The bullish formation points to more upside in the near term, with buyers eyeing a test of the two-decade highs of 139.39.

Ahead of that, the 138.50 psychological level and the July 21 high of 138.87 will challenge the bearish commitments.

The 14-day Relative Strength Index (RSI) is trading listlessly above the midline, keeping bulls hopeful.

On the downside, the immediate cushion is seen at the triangle resistance now support at 137.43. Sellers will then seek a test of the mildly bullish 50-Daily Moving Average (DMA) support at 136.85.

USD/JPY: Daily chart

USD/JPY: Additional levels to consider

- WTI remains pressured amid mixed clues as the NFP week begins.

- Doubts about the US-Iran oil deal join recession woes to trouble traders.

- US jobs report, OPEC+ verdict will be crucial for near-term directions.

WTI crude oil struggles to extend the previous weekly gains, taking rounds to $92.50 during Monday’s Asian session, as traders witness mixed catalysts. Among them, concerns surrounding the US-Iran oil deal and recession gained major attention.

“The US and Iran remain at loggerheads over key details of an emerging deal to revive a landmark nuclear agreement and may need several weeks to resolve their differences, according to officials familiar with the talks,” reported Bloomberg on Saturday. The news also mentioned that even if Washington and Tehran agree to revive the accord, implementing it will be a challenge, according to the European official, implying that a full Iranian return to oil markets would take months.

Alternatively, multiple central bankers sounded hawkish, led by Fed Chair Jerome Powell, during the latest annual Jackson Hole Symposium event, paying little heed to the impending recession woes. With this, the economic slowdown fears join rate hikes and can underpin the US dollar, which in turn could exert downside pressure on the black gold.

On the same line could be the recent increase in the US-China tension, which in turn could raise worries over the oil demand. China's military said on Sunday, per Reuters, that it was monitoring US Navy vessels sailing through the Taiwan Strait, maintaining a high alert and ready to defeat any provocations.

Elsewhere, Reuters cites multiple sources to mention the likelihood of the output cut by OPEC and its allies when and if Iranian production returns depending on the revival of the nuclear deal. During the last week, Saudi Arabian Energy Minister Prince Abdulaziz bin Salman said that OPEC and its allies (OPEC+) may be compelled to reduce oil production.

To sum up, the likely delay in the US-Iran oil deal and OPEC+ output cut could join the looming economic fears to entertain WTI traders. However, the US dollar strength appears the key catalyst to watch, which in turn highlights Friday’s US jobs report for August as an important factor for near-term directions.

Technical analysis

Contrary to the fundamentals, Friday’s Doji candlestick above the 21-DMA, at $90.78 by the press time, could help WTI crude oil buyers again poke the 50-DMA hurdle surrounding $96.10.

Citing a story carried by Sueddeutsche Zeitung newspaper over the weekend, Reuters reports that Germany's ruling party Social Democrats (SPD) will propose further measures to help ease the impact of rising energy prices on citizens.

Key takeaways

“A third relief package would include a similar ticket but with a less heavily discounted price tag of 49 euros per month,” according to a party resolution paper.

“The paper also envisages direct payments for middle and low-income households, measures to protect tenants from evictions if they cannot pay their ancillary bills, and reforms to housing allowance to include heating costs.”

“The party will also propose a readjustment of the gas levy that will come into force in October so that energy companies making profits do not also benefit from it.”

Market reaction

The shared currency fails to find any comfort from the above headlines, as EUR/USD is challenging daily lows near 0.9950, down 0.13% so far.

- USD/CAD takes the bids to extend Friday’s run-up towards one-week high.

- 3.5-month-old horizontal resistance area appears a tough nut to crack for bulls.

- Rising wedge raise doubts about bull’s dominance despite firmer oscillators.

USD/CAD remains on the front foot around 1.3050, extending Friday’s heavy gains towards a one-week high, as buyers cheer the previous day’s bounce off the 50-DMA during Monday’s initial Asian session.

The Loonie pair marked the biggest daily gains in more than a week on Friday after taking a U-turn from the 50-DMA support. The recovery moves also took clues from the firmer RSI and bullish MACD signals.

However, a horizontal area comprising multiple tops marked since May 12, around 1.3075-85, could challenge the USD/CAD bulls.

If not, then the upper line of the aforementioned three-week-old rising wedge near 1.3105 and the mid-July peak of 1.3135 could appear as intermediate halts during the run-up towards the yearly high near 1.3225.

On the contrary, pullback moves remain elusive until staying beyond the wedge’s support line, at 1.2940 by the press time.

Even if the USD/CAD declines below the 1.2940 support, the bears need confirmation from the 50-DMA support of 1.2920 to retake control.

Following that, the monthly low near 1.2730 and an upward sloping trend line from May, around 1.2690 will be in focus.

USD/CAD: Daily chart

Trend: Limited upside expected

South Korea's new central bank Governor Rhee Chang-yong said on Monday, “rising US interest rates will lead to higher inflation in Korea via won.”

Additional quotes

If inflation rises, BOK should put pricing stability first.

Data must be used to inform policy decisions.

Housing market correction is inevitable.

Fed's Powell comments were in line with what we anticipated.

The time when China was the world's factory is coming to an end.

Market reaction

At the time of writing, USD/KRW is clinging on to Friday’s upside near 1,342, as investors get started on another eventful week ahead. Last Thursday, South Korea's central bank said that its Monetary Policy Board hiked the key rate to 2.50% from 2.25% as expected.

- GBP/USD is at two-year lows, with a break below 1.1700 inevitable.

- The US dollar cheers Powell’s comments-led risk-off sentiment.

- Bear flag confirmation on the 1D chart opens more downside for cable.

GBP/USD is closing in on 1.1700, extending Friday’s decline amid an extension of risk-off sentiment and the US dollar recovery. Asian traders react negatively to Fed Chair Jerome Powell’s Jackson Hole remarks, as reflective of the 0.80% drop in the US S&P 500 futures in opening trades.

Expectations of higher rates for longer have ramped up after Powell’s comments, stoking growth fears and boding ill for global stocks. Investors continue to seek refuge in the safe-haven US dollar at the expense of high-beta currencies such as the British pound.

Meanwhile, the UK currency battles a dire economic outlook amid surging energy costs, which accentuates the country’s cost-of-living crisis. Looking ahead, the moves in the major could be exaggerated amid low volumes and minimal volatility, as the British traders are away, observing the Summer Bank holiday on Monday.

Amidst a lack of top-tier US economic data, traders will await Fed official Lael Brainard’s speech for fresh trading impetus.

As observed on cable’s daily chart, the downside break below the rising trendline support at 1.1777 on Friday has confirmed a bearish flag.

The downtrend could now extend towards the 1.1650 psychological level. Ahead of that the 1.1705 demand area will challenge the bullish commitments. That zone is the confluence of the two-year lows and the falling (dashed) trendline.

Also read: GBP/USD Weekly Forecast: Braces for more pain in the NFP week ahead

The 14-day Relative Strength Index (RSI) inches lower while sitting just above the oversold region, suggesting that there is more room for a downside move. Adding credence to the bearish potential, the 21 and 50-Daily Moving Averages (DMA) bearish crossover confirmed earlier this week also remains in play.

Alternatively, bulls need a sustained move above the rising trendline resistance at 1.1879 to negate the near-term bearish bias. The next significant upside target is aligned at 1.1900 the round figure. The August 19 high at 1.1937 will be next on buyers' radars.

GBP/USD: Daily chart

-637973234282558442.png)

GBP/USD: Additional technical levels

- NZD/USD extends Friday’s losses towards refreshing a multi-day low.

- US dollar cheers Fed Chair Powell’s hawkish bias, doubts over central banks ability to tame recession.

- Escalating Sino-American tussles, RBNZ’s cautious mood appears to exert more downside pressure.

- No major data from New Zealand this week, US jobs report will be crucial for clear directions.

NZD/USD drops to the fresh low in six weeks, taking offers to 0.6125 during Monday’s Initial session, as risk-aversion underpins the US dollar’s safe-haven demand. Also exerting downside pressure on the Kiwi pair is the recent shift in the Reserve Bank of New Zealand’s (RBNZ) tone, despite favoring further rate hikes, as well as the US-China tension.

“Restoring price stability will take some time, require using central bank's tools 'forcefully',” said Fed Chairman Jerome Powell during his much-awaited Jackson Hole speech on Friday. The policymaker also stated that restoring price stability will likely require maintaining a restrictive policy stance for 'some time'.

RBNZ Governor Adrian Orr, on the other hand, spoke earlier at the Jackson Hole and mentioned that we think there will be at least another two rate hikes. The policymaker also said, “Our core view is we won't see a technical recession.” However, his comments like, “Central banks may need to push towards zero growth,” seemed to have weighed on the NZD/USD prices.

It’s worth noting that the concerns over the global central bankers’ ability to tame inflation, as well as increasing the odds of the recession, joined fears of more US-China tussles to also favor the US dollar’s demand.

US Senator Elizabeth Warren said on Sunday, per Reuters, that she was very worried that the Federal Reserve was going to tip the US economy into recession. On the same line was a study presented at the Jackson Hole Symposium stating that the central banks will fail to control inflation and could even push price growth higher unless governments start playing their part with more prudent budget policies. "If the monetary tightening is not supported by the expectation of appropriate fiscal adjustments, the deterioration of fiscal imbalances leads to even higher inflationary pressure," said Francesco Bianchi of Johns Hopkins University and Leonardo Melosi of the Chicago Fed.

Elsewhere, China's military said on Sunday, per Reuters, that it was monitoring US Navy vessels sailing through the Taiwan Strait, maintaining a high alert and ready to defeat any provocations.

It should be noted that the mixed US data couldn’t derail the NZD/USD downside. That said, US Core Personal Consumption Expenditures (PCE) Price Index, mostly known as the Fed’s preferred inflation gauge, edged lower to 4.6% in July from 4.8% prior and 4.7% market forecasts. Further, the University of Michigan Consumers Confidence Index was revised upwards in August, with the final print arriving at 58.2, versus the preliminary reading of 55.1 and 55.2 expected.

Against this backdrop, Wall Street benchmarks dropped more than 3.0% each while the US 10-year Treasury yields printed mild gains to end the week around 3.04%.

To sum up, NZD/USD bears are in control and can keep reins ahead of Friday’s US Nonfarm Payrolls (NFP).

Technical analysis

The NZD/USD pair’s sustained downside break of monthly horizontal support, now resistance around 0.6155-50, directs the pair sellers towards the 0.6100 threshold ahead of highlighting the yearly bottom surrounding 0.6020.

- EUR/USD remains on the back foot after calling in bears the previous day.

- Fed Chair Powell’s hawkish tone favored sellers, ECB policymakers’ signaled large rate hikes and challenged downside.

- Wall Street closed in the red, yields dropped amid risk-off mood.

- Fedspeak, US PMIs and EU/German inflation can entertain traders ahead of Friday’s US NFP.

EUR/USD begins the week on a negative note, after a two-week downtrend that refreshed the yearly low, taking offers to refresh intraday bottom around 0.9950 by the press time. In doing so, the currency major pair struggles to justify the recently hawkish comments from the European Central Bank (ECB) policymakers as markets still give high importance to Fed Chair Jerome Powell’s hawkish statements ahead of Friday’s monthly jobs report for the US.

The annual Jackson Hole Symposium appeared to have mostly marked the hawkish colors as policymakers gave high importance to taming inflation.

“Restoring price stability will take some time, require using central bank's tools 'forcefully',” said Fed Chairman Jerome Powell during his much-awaited Jackson Hole speech on Friday. The policymaker also stated that restoring price stability will likely require maintaining a restrictive policy stance for 'some time'.

On the other hand, ECB board member Isabel Schnabel, French Central Bank chief Francois Villeroy de Galhau and Latvian central bank Governor Martins Kazaks all argued for forceful or significant policy action, per Reuters.

Elsewhere, doubts over the global central bankers’ ability to tame inflation, as well as increasing the odds of the recession, also exert downside pressure on the EUR/USD prices. US Senator Elizabeth Warren said on Sunday, per Reuters, that she was very worried that the Federal Reserve was going to tip the US economy into recession. On the same line was a study presented at the Jackson Hole Symposium stating that the central banks will fail to control inflation and could even push price growth higher unless governments start playing their part with more prudent budget policies. "If the monetary tightening is not supported by the expectation of appropriate fiscal adjustments, the deterioration of fiscal imbalances leads to even higher inflationary pressure," said Francesco Bianchi of Johns Hopkins University and Leonardo Melosi of the Chicago Fed.

Talking about the data, US Core Personal Consumption Expenditures (PCE) Price Index, mostly known as the Fed’s preferred inflation gauge, edged lower to 4.6% in July from 4.8% prior and 4.7% market forecasts. Further, the University of Michigan Consumers Confidence Index was revised upwards in August, with the final print arriving at 58.2, versus the preliminary reading of 55.1 and 55.2 expected.

Amid these plays, Wall Street benchmarks dropped more than 3.0% each while the US 10-year Treasury yields printed mild gains to end the week around 3.04%.

Looking forward, EUR/USD traders will pay attention to the US/Eurozone PMIs, as well as initial readings of the EU/Germany inflation data for fresh impulse. However, major attention will be given to Friday’s US Nonfarm Payrolls (NFP) as Fed’s Powell sounded firmly hawkish.

Technical analysis

A clear U-turn from the 10-DMA, around 1.0005 by the press time, directs EUR/USD towards the recently flashed multi-year low surrounding 0.9900.

- Gold Price holds lower ground after Friday’s over 1% steep sell-off.

- Hawkish Fed’s Powell sparks US dollar upswing, as risk tone sours.

- XAU/USD challenges critical daily support line, more downside likely.

Gold Price is licking its wounds while keeping its range below $1,740, as a fresh week kicks off on a defensive note. Markets reprice September rate hike expectations in the lead-up to the US Nonfarm Payrolls week, especially after Fed Chair Jerome Powell’s hawkish remarks at Friday’s Jackson Hole appearance.

Powell maintained that the Fed will continue with its tightening path until inflation is brought down substantially from a four-decade high. The Fed Chief also added that the September rate hike decision will be data-dependent.

The US dollar bulls the hawkish comments in their stride and staged an impressive comeback in American trading on Friday while Wall Street indices suffered heavy losses, as Powell doused speculation of policy easing in the months ahead to tackle economic slowdown.

The extension of risk-aversion combined with the dollar gains in Asia so far this Monday is keeping gold traders on the back foot, as they gear up for another critical week. The US will publish the critical ISM Manufacturing and Services PMIs ahead of Friday’s payrolls. Each incoming data will be closely examined for signals on the size of the next Fed rate hike.

China’s economic data will also hog the limelight, as it will have a significant impact on the market’s perception of risk sentiment, eventually affecting the dollar’s valuation.

Also read: Gold Price Forecast: XAU/USD closes the week above 50 DMA, what’s next?

Technically, gold price tumbled to challenge the critical rising trendline support, now at $1,735. Daily closing below the latter is needed to extend Friday’s sell-off towards the previous week’s low of $1,728.

Bears will revive the bets for a test of the $1,700 threshold in the upcoming sessions.

The 14-day Relative Strength Index (RSI) is holding flat but below the midline, backing the ongoing weakness in the yellow metal.

On the upside, any recovery attempts will need to beat Friday’s high of $1,759, around where the bearish 50-Daily Moving Average (DMA) lurks.

Gold Price: Daily chart

Gold Price: Additional levels to consider

Over the weekend, we had several European Central Bank (ECB) policymakers speaking in interviews on the sidelines of the Kansas City Fed’s Jackson Hole Symposium, expressing their concerns over the depreciation of the euro while maintaining the case for further rate increases in the coming months.

ECB Governing Council member Francois Villeroy de Galhau noted that ECB needs another significant interest rate hike in September

On neutral rate and further rate hikes, he said "We could be there before the end of the year, after another significant step in September. Have no doubt that we at the ECB would if needed raise rates further beyond normalization: bringing inflation back to 2% is our responsibility; our will and our capacity to deliver on our mandate are unconditional.”

Olli Rehn voiced his concerns over the inflationary impact of the falling euro, saying, “Certainly we are monitoring the exchange rate. This indirect channel is important - we are monitoring it and are looking at it as one indicator. It’s already a significant consideration” in setting monetary policy.”

Commenting on the September rate hike outlook, Rehn said: “The reality is that we have excessively high inflation globally, also in Europe -- that’s why it’s action time. The next step will be a significant move in September, depending on the incoming data and the inflation outlook.”

“Monetary policy is now facing the dual dilemma of on the one hand maintaining inflation expectations anchored, and on the other hand avoiding that we would push the economy into a recession. We have a severe energy crisis in Europe. it's quite likely that the euro-zone economy is slowing down. It’s slowing down as we speak, Rehn said while speaking about the euro area economic outlook.

The central bank board member Isabel Schnabel said, "even if we enter a recession, we have little choice but to continue the normalization path."

"If there was a de-anchoring of inflation expectations, the effect on the economy would be even worse, Schnabel added.

She further said that rates need to stay high, cautioned against pausing on early signs of a potential turn in inflationary pressures, adding that central bank rate-setters should instead signal their "strong determination" to bring inflation back to target quickly.

Meanwhile, Martins Kazaks, another Governing Council member said that he’s “not happy where the exchange rate has moved because the lower rate further fuels inflationary pressures and the benefit of cheaper exports is diminished by supply chain disruption.”

On the September rate hike decision, he said that “the increase needs to be strong and significant, and at the current moment, I would say 50 or 75 basis points.”

“At least 50 basis points would be appropriate,” he said, adding that “the pace at which monetary support is removed must be orderly.”

FX implications

At the press time, EUR/USD is licking its wounds around 1.1960, almost unchanged on the day. The mixed remarks from the ECB officials fail to have any impact on the shared currency, as the US dollar price action and the prevailing risk tone are likely dominating fx currencies in Asia this Monday.

Speaking at the Kansas City Fed’s annual conference in Jackson Hole Symposium, Wyoming over the weekend, Bank of Japan (BOJ) Governor Haruhiko Kuroda said that the central bank will likely continue with its accommodative policy in Japan.

Key quotes

“Somewhat miraculously, now we have 2.4% inflation. But almost wholly caused by the international commodity price hike, energy and food.”

“So we expect that by the end of this year, may be inflation rate may approach 2 or 3%, but next year, inflation rate again decelerate toward 1.5%.”

“So, we have no choice other than continued monetary easing until wages and prices rise in a stable and sustainable manner.”

Market reaction

At the time of writing, USD/JPY is digesting the weekend’s remarks by policymakers in early Monday, keeping its range around 137.60, up 0.08% on the day.

- AUD/USD bears keep their defensive mode intact below 0.6900.

- USD holds the upper hand amid a risk-off mood, hawkish Powell.

- The aussie eyes Retail Sales data in the critical US NFP week ahead.

AUD/USD is trading below 0.7000, starting a brand new week on the back foot, as US dollar bulls keep the upper hand following Fed Chair Jerome Powell’s hawkish rhetoric during his appearance at the Jackson Hole Symposium on Friday.

Powell, in his prepared remarks on day 2 of the annual Fed event, said that “restoring price stability will likely require maintaining a restrictive policy stance for 'some time, adding that the Decision on the September rate hike will depend on the totality of data since July meeting.”

The US dollar staged a sharp V-shaped recovery on his comments, despite the retracement in the Treasury yields across the curve. The negative shift in the market’s perception of risk sentiment helped the uptick in the safe-haven greenback, as major Wall Street indices tumbled roughly 3.50% after Powell poured cold water on the idea of a Fed pivot that could jeopardize its war against inflation.

Heading into a new week, risk-off flows seem to extend into the Asian trading this Monday, reflective of the submissive tone in the higher-yielding aussie. Bulls also remain at bay, awaiting the Australian Retail Sales data for July due for release at 0130 GMT. The country’s consumer spending is seen rising by 0.3% in the reporting period vs. 0.2% booked previously.

Australian retail sales volumes rose 1.4% in the June quarter of 2022, hitting a new record level, for the third consecutive quarter, the Australian Bureau of Statistics (ABS) showed about a month ago.

The pair will also take cues from the broader market sentiment and the speech from Fed official Lael Brainard in the US Nonfarm Payrolls week ahead. China’s Manufacturing and Services PMIs will be also closely eyed for fresh hints on the health of Australia’s biggest trading partner, China.

AUD/USD: Technical levels to consider

© 2000-2026. Sva prava zaštićena.

Sajt je vlasništvo kompanije Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

Svi podaci koji se nalaze na sajtu ne predstavljaju osnovu za donošenje investicionih odluka, već su informativnog karaktera.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Izvršenje trgovinskih operacija sa finansijskim instrumentima upotrebom marginalne trgovine pruža velike mogućnosti i omogućava investitorima ostvarivanje visokih prihoda. Međutim, takav vid trgovine povezan je sa potencijalno visokim nivoom rizika od gubitka sredstava. Проведение торговых операций на финанcовых рынках c маржинальными финанcовыми инcтрументами открывает широкие возможноcти, и позволяет инвеcторам, готовым пойти на риcк, получать выcокую прибыль, но при этом неcет в cебе потенциально выcокий уровень риcка получения убытков. Iz tog razloga je pre započinjanja trgovine potrebno odlučiti o izboru odgovarajuće investicione strategije, uzimajući u obzir raspoložive resurse.

Upotreba informacija: U slučaju potpunog ili delimičnog preuzimanja i daljeg korišćenja materijala koji se nalazi na sajtu, potrebno je navesti link odgovarajuće stranice na sajtu kompanije TeleTrade-a kao izvora informacija. Upotreba materijala na internetu mora biti praćena hiper linkom do web stranice teletrade.org. Automatski uvoz materijala i informacija sa stranice je zabranjen.

Ako imate bilo kakvih pitanja, obratite nam se pr@teletrade.global.

транcфери