- Analiza

- Novosti i instrumenti

- Vesti sa tržišta

Forex-novosti i prognoze od 02-04-2023

- US Dollar Index picks up bids to extend Friday’s recovery, pares three-week downtrend.

- OPEC+ supply cuts join mixed US data and Fed’s hesitance in letting doves in put a floor under DXY prices.

- Sino-American tension, pre-NFP anxiety also allow US Dollar Index to pare recent losses.

US Dollar Index (DXY) kick-starts the NFP week on a firmer footing, after a three-week losing streak, as it marches to 102.83 during the early hours of Monday’s Asian trading session. In doing so, the greenback’s gauge versus the six major currencies cheers the market’s risk aversion, as well as cautious mood ahead of the key US activity data and jobs report for March.

DXY dropped in the last three consecutive weeks amid receding fears of witnessing a bank crisis and the downbeat US data. Also weighing on the US Dollar Index could be the Federal Reserve (Fed) policymakers’ inability to convince markets of their hawkish capacity. However, the weekend news of the oil supply cut from the Organization of the Petroleum Exporting Countries (OPEC) and allies led by Russia, known as OPEC+, renew inflation fears and propel the concerns of higher rates, which in turn underpinned the US Dollar’s haven demand.

Talking about the key data, Friday’s US Core Personal Consumption Expenditures (PCE) Price Index, the Fed’s preferred gauge of inflation, declined to 4.6% YoY in February from 4.7% expected and prior. On a monthly basis, Core PCE inflation rose 0.3% while easing below the market expectation of 0.4% and a downwardly revised 0.5% previous reading. It should be noted that the final readings of the US fourth quarter (Q4) Gross Domestic Product (GDP), also known as the Real GDP, marked an easy Annualized growth number of 2.6% versus 2.7% previous forecasts.

Even so, Fed Chairman Jerome Powell pushed for one more rate hike while Federal Reserve Bank of Boston President Susan Collins highlighted the importance of higher rates to tame inflation during her latest speeches. On the same line, Federal Reserve Bank of New York President John C. Williams said that he expects inflation to decline to around 3-1/4 percent this year, before moving closer to our longer-run goal in the next two years.

On the other hand, bank shares recover after upbeat banking sector performance and mixed US data, not to forget the firmer closing of Wall Street, as well as recovery in the US Treasury bond yields.

Moving on, US ISM Manufacturing PMI and S&P Global Manufacturing PMI for March can direct intraday moves of the US Dollar Index. However, major attention should be paid to the risk catalysts for clear directions. Among them, Friday’s US jobs report and headlines suggesting inflation woes will be in the spotlight.

Technical analysis

A 13-day-old descending trend line joins the 10-day Exponential Moving Average (EMA) to highlight 102.85 as a short-term key hurdle to watch for the US Dollar Index buyers.

- NZD/USD bears are in the market testing dynamic support.

- Risk-off tones due to higher oil prices are dominating ahead of RBNZ.

NZD/USD is lower on the day by some 0.3% after falling from a high of 0.6255 to a low of 0.6232 so far. Risk-off markets are kicking in on the back of the weekend news regarding the oil production cut and soaring oil prices.

Saudi Arabia and other OPEC+ oil producers have announced further oil output cuts of around 1.16 million barrels per day. In a statement, the Saudi energy ministry said that the kingdom’s voluntary cut was a precautionary measure aimed at supporting the stability of the oil market. Consequently, WTI crude oil opened for the week with a significant price gap to print $81.51 during the early hours of Monday’s Asian session.

Meanwhile, domestically, this week the focus shifts to the Reserve Bank of New Zealand. ´´While they’re likely to acknowledge risks around financial instability, NZ is remote from all that, and we think the inflation risks relating to the cyclone recovery in an already capacity-constrained economy are a bigger story,´´ analysts at ANZ Bank said, adding, ´´that could help the NZD this week.´´

Meanwhile, analysts at TD Securities noted that the February Monetary Policy Statement noted the Bank thinks further hikes are needed. ´´Aside from Gross Domestic Product, other data suggest the Bank will continue hiking. The Bank may acknowledge the turmoil in US and EU financials but conclude NZ banks are in good shape,´´ the analysts said. ´´To the extent, offshore lending standards tighten and our Fed terminal rate is now lower, this implies downside risk to our 5.50% terminal rate forecast,´´ the analysts concluded.

NZD/USD technical analysis

The price is testing the dynamic support line on the daily chart and the M-formation is in play. If the bulls commit, a retest of the neckline and prior support might be expected to result in a downside continuation to break the dynamic trendline support.

- AUD/JPY has failed to sustain above 89.00 as investors turn anxious ahead of Caixin Manufacturing PMI data.

- RBA would continue its policy-tightening spell despite softening of Australian inflation.

- The Japanese Yen faced immense pressure led by a sharp jump in the oil price.

The AUD/JPY pair is struggling to keep itself above 89.00 after a decent opening in the early Asian session. The risk barometer witnessed a decent response from buyers as soaring oil prices weighed heavily on the Japanese Yen.

Investors discounted the surprise announcement of the oil production cut by OPEC+, made on weekend. Japan, being one of the leading importers of oil, witnessed intense selling pressure.

However, the Australian Dollar is getting volatile ahead of the release of the Caixin Manufacturing PMI data. The street is estimating a marginal rise in the economic data to 51.7 from the former release of 51.6. On Friday, official China’s Manufacturing PMI landed at 51.9, higher than the consensus of 51.5 but lower than the former release of 52.6.

It is worth noting that Australia is a leading trading partner of China and a higher Chinese Manufacturing PMI would also strengthen the Australian Dollar.

Going forward, volatility in the Australian Dollar is expected to remain high ahead of the interest rate decision by the Reserve Bank of Australia (RBA), which will be announced on Tuesday. Australian monthly inflation indicator has softened to 6.8% in the past two months from its peak of 8.4% recorded in December. Despite that, RBA Governor Philip Lowe is expected to hike rates further by 25 basis points (bps) to 3.80%.

There is no denying the fact that Australian inflation has softened firmly, however, the inflation rate is highly skewed from the desired inflation rate, which would force RBA policymakers to continue their tight monetary policy approach.

- USD/CHF extends Friday’s recovery from three-week low on DXY’s rebounds.

- Market sentiment sours on OPEC+ surprise output cut, cautious mood ahead of top tier data/events.

- Swiss CPI, US NFP will be the key, PMIs are also important to watch for clear directions.

USD/CHF picks up bids to renew intraday high around 0.9170 as it extends the previous day’s upside while consolidating the two-week downtrend during early Monday. In doing so, the Swiss Franc (CHF) pair justifies the market’s risk-off mood ahead of the key data/events amid fears of an additional toll on the global growth, mainly after the oil output cut from the Organization of the Petroleum Exporting Countries (OPEC) and allies led by Russia, known as OPEC+.

After multiple days of optimism, market sentiment sours during early Monday as an output cut from the global oil producers propels the odds of higher inflation and an additional burden on the economy, suggesting more chances of witnessing a recession. It’s worth noting that the cautious mood ahead of the Swiss Consumer Price Index (CPI) for March and the US Nonfarm Payrolls (NFP) for the said month also weigh on the risk appetite and fuel the USD/CHF prices.

It’s worth noting, however, that the receding hawkish bets on the Federal Reserve (Fed), especially after the previous week’s downbeat data, join the easing fears of the banking crisis to challenge the US Dollar bulls ahead of the key US jobs report.

As per the latest data, the US Core Personal Consumption Expenditures (PCE) Price Index, the Fed’s preferred gauge of inflation, for February declined to 4.6% YoY from 4.7% expected and prior. On a monthly basis, Core PCE inflation rose 0.3% while easing below the market expectation of 0.4% and a downwardly revised 0.5% previous reading. Further, the Chicago PMI reading for March came in stronger than expected at 43.8 while the final readings of the University of Michigan's (UoM) Consumer Confidence Index dropped to 62.0 in March, versus 63.4 flash estimations and 63.2 market forecasts. Additionally, Current Economic Conditions fell from 70.7 in February to 66.3 and the Index of Consumer Expectations declined from 64.7 to 59.2.

Amid these plays, S&P 500 Futures print mild losses despite the firmer closing of Wall Street while the US Treasury bond yields pause the three-day downtrend.

Moving on, the Swiss CPI and SVME Purchasing Managers’ Index for March will precede the US ISM Manufacturing PMI for the said month to direct intraday moves of the USD/CHF pair. However, major attention should be given to the risk catalysts and Friday’s US jobs report for a clear guide.

Technical analysis

A one-month-old descending resistance line, around 0.9180 by the press time, challenges USD/CHF bulls even if MACD and RSI suggest that the bears are running out of steam.

- GBP/USD bears are back in town after three-week uptrend as Cable news intraday low.

- Another failure to cross 1.2445-50 resistance zone, downside break of 13-day-old ascending support line lures sellers.

- Convergence of 50-DMA, 100-DMA appears the key support for bears to watch.

- Oscillators also suggest that buyers are running out of steam.

GBP/USD begins the week’s trading on a back foot after witnessing three consecutive weekly gains in the last, down 0.25% around 1.2310 by the press time.

In doing so, the Cable pair justifies the downside break of a two-week-old ascending support line, now resistance around 1.2365. Adding strength to the quote’s bearish bias is one more reversal from the 1.2445-50 resistance zone which has been restricting the quote’s upside since early December 2022.

Additionally, a looming bear cross on the MACD and a steady RSI (14) line also suggest that the GBP/USD pair could consolidate the latest weekly gains.

However, a convergence of the 50-DMA and 100-DMA, near 1.2140-45, appears a tough nut to crack for the Cable pair bears.

Following that, an upward-sloping support line from November, close to 1.1940 by the press time, can challenge the GBP/USD pair sellers.

Meanwhile, recovery moves not only need validation from the support-turned-resistance line of around 1.2365 but also need to provide a successful upside break of the 1.2445-50 area to convince the GBP/USD buyers.

Should the Cable pair manage to remain firmer past 1.2450, a run-up toward the May 2022 high of around 1.2665 can’t be ruled out.

GBP/USD: Daily chart

Trend: Further downside expected

- USD/CAD has failed to get accepted above 1.3500 as the higher oil price has strengthened the Canadian Dollar.

- The USD Index has scaled above 102.80 as higher oil prices would fuel persistent United States inflation.

- Canada’s upbeat January GDP data has trimmed the chances of reporting an overall quarterly contraction ahead.

The USD/CAD has retreated from 1.3520 after a rebound attempt followed by a gap-down opening from 1.3488 in the early Tokyo session. The Loonie asset has continued its downside journey as the oil price has soared dramatically after the announcement of a surprise cut in oil production by OPEC+. The oil cartel has decided to cut the oil production further by 1.16 million barrels each day, which has pushed the overall pledge of oil cut to 3.66 million bpd.

It is worth noting that Canada is the leading exporter of oil to the United States and significantly higher oil prices have infused fresh blood into the Canadian Dollar.

The Canadian Dollar remained in action on Friday after the release of upbeat monthly Gross Domestic Product (GDP) (Jan) data. The economic data landed at 0.5%, higher than the estimates of 0.3%. The GDP data was contracted by 0.1% in December and an optimist start of 2023 has trimmed chances of reporting an overall contraction ahead.

Meanwhile, S&P500 futures have recovered some of their losses posted in Asia, portraying recovery in the risk appetite of the market participants. It looks like investors have started digesting the consequences of higher oil prices. The US Dollar Index (DXY) has scaled above 102.80 as higher oil prices would fuel persistent United States inflation.

Going forward, the US ISM Manufacturing PMI data will be keenly watched. According to the consensus, the Manufacturing PMI is expected to decline marginally to 47.5 from the former release of 47.7. Investors should be aware that the US Manufacturing PMI has remained below 50.0 consecutively in the past four months.

From the US Manufacturing PMI gamut, New Orders Index would hog the limelight as it provides cues about the manufacturing outlook. The forward demand for the manufacturing sector is expected to contract significantly to 44.6 vs. the prior release of 47.00.

- AUD/USD begins the key week on a softer footing as market’s risk-on mood fades.

- Weekend announcements of surprise OPEC+ Oil output cut, anticipated dovish hike from RBA weigh on Aussie price.

- Firmer sentiment, downbeat US data pushed US Dollar down for the third consecutive week.

- US jobs report will be crucial amid fresh talks of Fed’s policy pivot.

AUD/USD struggles to extend the previous weekly gains as it prints minor losses around 0.6680 during early Monday morning in the Asia-Pacific region.

Markets brace for a dovish hike from the Reserve Bank of Australia (RBA) after downbeat inflation and Retail Sales data. However, the RBA policymakers defended their hawkish moves and hence the Aussie pair traders are more cautious. Also challenging the risk-barometer pair is the downbeat mood and the presence of the US jobs report for March, up for publishing on Friday.

The last week’s downbeat Aussie Consumer Price Index (CPI) and Retail Sales data raised concerns about the RBA’s last rate hike and flag the fears of the AUD/USD bear’s return. However, the softer US data and receding hawkish concerns from the Federal Reserve (Fed), not to forget the presence of the US Nonfarm Payrolls (NFP) release keeps the Aussie pair traders on their toes.

On Friday, the US Core Personal Consumption Expenditures (PCE) Price Index, the Fed’s preferred gauge of inflation, for February declined to 4.6% YoY from 4.7% expected and prior. On a monthly basis, Core PCE inflation rose 0.3% while easing below the market expectation of 0.4% and a downwardly revised 0.5% previous reading. Further, the Chicago PMI reading for March came in stronger than expected at 43.8 while the final readings of the University of Michigan's (UoM) Consumer Confidence Index dropped to 62.0 in March, versus 63.4 flash estimations and 63.2 market forecasts. Current Economic Conditions fell from 70.7 in February to 66.3 and the Index of Consumer Expectations declined from 64.7 to 59.2.

It should be noted that the global central bankers and policymakers appear successfully routed the markets off the banking crisis as the bank shares have recently recovered after witnessing a bloodbath during mid-March, led by the Silicon Valley Bank’s (SVB) fallout.

Alternatively, a surprise output cut from the Organization of the Petroleum Exporting Countries (OPEC) and allies led by Russia, known collectively as OPEC+, joins fresh fears of the US-China tension weighing on the AUD/USD prices. On Friday, China's top diplomat Wang Yi said that the US and China relations are facing challenges and difficulties. “I urge the US to stop suppression, decoupling is wrong,” Wang added.

Amid these plays, Wall Street closed on the positive side but the yields are down, despite marking weekly gains.

Looking forward, AUD/USD traders may pay attention to US ISM Manufacturing PMI for March for intraday directions. However, Tuesday’s RBA and Friday’s US jobs report are the key events to watch for this week.

Technical analysis

An upward-sloping support line from March 10, around 0.6670 by the press time, restricts the short-term downside of the AUD/USD price.

- Gold price has dropped sharply to near $1,960.00 as a surprise production cut by the OPEC+ would propel US Inflation.

- The Fed could keep rates higher for a longer period to bring down fresh persistent inflation.

- A power-pack action in the USD Index would continue ahead of the release of the US ISM Manufacturing PMI data.

Gold price (XAU/USD) is facing immense pressure in early Asia as United States inflationary pressures have propelled after the announcement of a surprise production cut by the OPEC+ on weekend. The precious metal has dropped firmly to near $1,960.00 on hopes that the Federal Reserve (Fed) would keep rates higher for a longer period. Expectations of a fresh impulse in US inflation led by higher oil prices after a sudden production cut are going to phase out odds of a steady monetary policy by the Fed in May.

According to Reuters, the oil cartel will cut the overall oil production by around 1.16 million barrels/day (bpd), which will lead to the overall pledge of production cut to 3.66 million bpd.

The US Dollar Index (DXY) has extended its upside momentum above 102.70 on expectations of the continuation of the 25 basis points (bps) rate hike spell by the Federal Reserve (Fed). This would push interest rates to 5.00-5.25%. S&P500 futures have dropped heavily in early Asia after a decent winning spree, portraying a caution in the overall risk-appetite theme.

A power-pack action in the USD Index would continue ahead of the release of the US ISM Manufacturing PMI data. As per the estimates, the Manufacturing PMI is expected to decline marginally to 47.5 from the former release of 47.7. This could be the fifth consecutive figure below 50.0, which itself is considered a contraction in manufacturing activities.

Apart from that, the Manufacturing New Orders Index will be keenly watched. The economic data provide cues about forward demand for goods, which is likely to contract firmly to 44.6 vs. the prior release of 47.00. Subdued consensus for the US Manufacturing PMI could be the outcome of higher interest rates by the Fed for bringing down persistent inflation.

Gold technical analysis

Gold price is hovering near the edge of the upward-sloping trendline of the Symmetrical Triangle chart pattern formed on an hourly scale. The upward-sloping trendline of the chart pattern is plotted from March 22 low at $1,934.34 while the downward-sloping trendline is placed from March 20 high at $2,009.88.

The Gold price has dropped below the 20-period Exponential Moving Average (EMA) at $1,974.10, which indicates that the short-term trend has turned bearish.

Meanwhile, the Relative Strength Index (RSI) (14) has slipped into the bearish range of 20.00-40.00, which indicates more weakness ahead.

Gold hourly chart

“Shadow Board members recommend a smaller hike in the Official Cash Rate (OCR) in the Reserve Bank’s upcoming April Monetary Policy Review,” said the latest New Zealand Institute of Economic Research (NZIER) report.

“The majority view was an OCR increase of 25 basis points, given inflation pressures are still high in the economy and inflation expectations remain above the Reserve Bank’s 1–3 percent inflation target band,” also mentions the NZIER report.

Key comments

However, two Shadow Board members recommended the Reserve Bank keep the OCR unchanged at 4.75 percent.

One of these members considered the OCR should have already peaked, while the other highlighted the increased risk of a recession looming.

Regarding where the OCR should be in a year, the Shadow Board’s core view ranged from 4.25 percent to 5.50 percent.

Some members recommend the Reserve Bank pause with OCR increases after April but keep it elevated for some time to bring inflation down.

There was one Shadow Board member in the business community who viewed the OCR should be lower in a year, given business profitability and finances are already hard hit by the interest rate increases to date.

NZD/USD drops

The news weighs on the NZD/USD prices, together with the sour sentiment, as the Kiwi pair drops to 0.6235, down 0.35% intraday at the latest by the press time.

- USD/NOK has delivered a gap-down open near 10.40 after a surprise oil production cut by OPEC+.

- Fresh pledge of cutting overall oil production by 1.16 million bpd has led to an overall cut of 3.66 million bpd.

- The odds for a further 25bp rate hike by the Fed remain solid despite softening of the US PCE Price Index.

The USD/NOK pair has witnessed an intense sell-off in the Asian session as investors discount the impact of the surprise drop in oil production announced by Saudi Arabia and other OPEC+ members. The oil cartel will cut the overall oil production by around 1.16 million barrels/day, which has strengthened the Norwegian Krone. Fresh pledge of cutting overall oil production by 1.16 million bpd has led to an overall cut of 3.66 million bpd.

The surprise move by OPEC+ in an attempt to support the oil price has strengthened the currencies of oil-exporting countries, which will receive more funds on exporting oil. Bloomberg reported that the surprise move by OPEC+ would increase the risk of higher inflationary pressures globally and might force central banks to keep policy rates higher for longer.

Meanwhile, S&P500 continued its winning spree on Friday in hopes of no further casualties to the United States banking sector, portraying a risk-on mood. However, fresh oil production cuts could spoil the market mood ahead, therefore, a cautionary approach would be advisable.

The US Dollar Index (DXY) recovered firmly on late Friday to near 102.60 despite more-than anticipated softening of US core Personal Consumption Expenditure (PCE) Price Index data. On a monthly basis, the US PCE Price Index accelerated by 0.3%, lower than the consensus of 0.4% and the former release of 0.5%. Also, the annual US PCE Inflation figure soften to 4.6% from the consensus and prior release of 4.7%. However, the move has not eased expectations of further 25 basis points (bps) rate hike by the Federal Reserve.

As per the CME Fedwatch tool, the odds for a 25bp rate hike to 5.00-5.25% for May monetary policy meeting stand more than 53%.

- WTI Crude oil marks a stellar run-up as OPEC+ shocks markets with surprise output cut.

- OPEC+ members announced voluntary production cut led by Saudi Arabia.

- Risk-on mood, softer US Dollar also propel WTI crude oil prices.

WTI crude oil begins the week with a huge price gap towards the north, jumping to $81.00 during the early hours of Monday’s Asian session. The black gold’s latest rally could be linked to the weekend announcements from the Organization of the Petroleum Exporting Countries (OPEC) and allies led by Russia, known collectively as OPEC+.

Also read: OPEC producers announce voluntary oil output cuts

The Oil cartel, led by Saudi Arabia, announced a total of around 1.16 million barrels a day of output cut during the weekend in a surprise move. Following the announcements, the US National Security Council said. “We don’t think cuts are advisable at this moment given market uncertainty - and we’ve made that clear."

Apart from the OPEC+ output cut, the US Dollar weakness and broad risk-on mood also allowed the WTI crude oil price to remain firmer. That said, the US Dollar Index (DXY) marked a three-week downtrend in the last whereas the receding fears of the banking crisis and the latest toll on the hawkish Fed bets allow the riskier assets to remain firmer.

Moving on, the US Nonfarm Payrolls (NFP) for March and the ISM PMIs for the stated month will be important to watch. Also, the US reaction to OPEC+ isn’t welcomed and hence more Strategic Petroleum Reserve (SPR) releases are likely on the way, suggesting a pullback in the Oil price.

Technical analysis

A clear upside break of the five-month-old descending resistance line, now support around $78.30, directs WTI crude oil buyers towards confronting the 200-DMA hurdle surrounding $83.35.

It’s worth noting that January’s high of around $82.70 can offer an immediate upside hurdle to the black gold.

Alternatively, the previous monthly high of nearly $81.00 and an ascending support line from March 20, close to $75.40, are extra filters towards the south.

WTI crude oil: Daily chart

Trend: Further upside expected

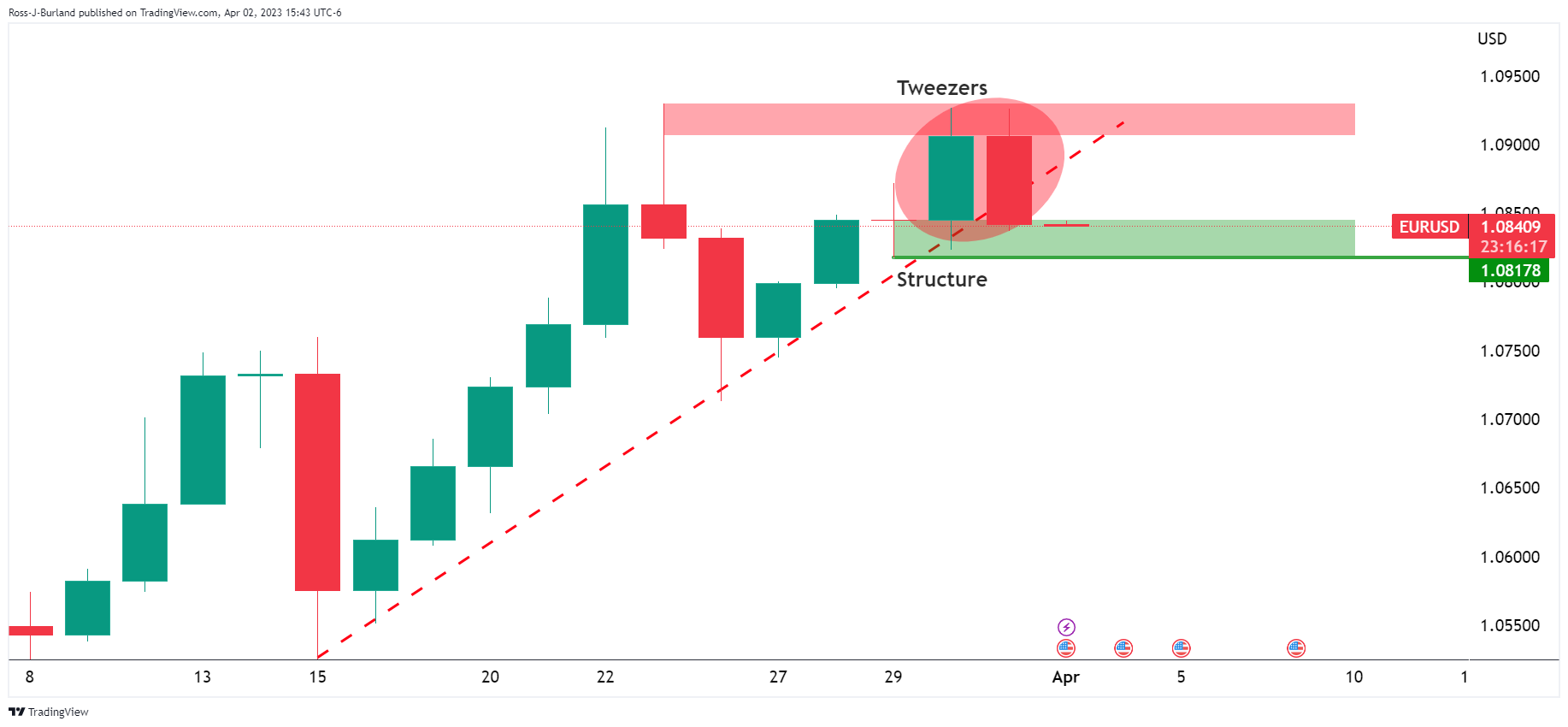

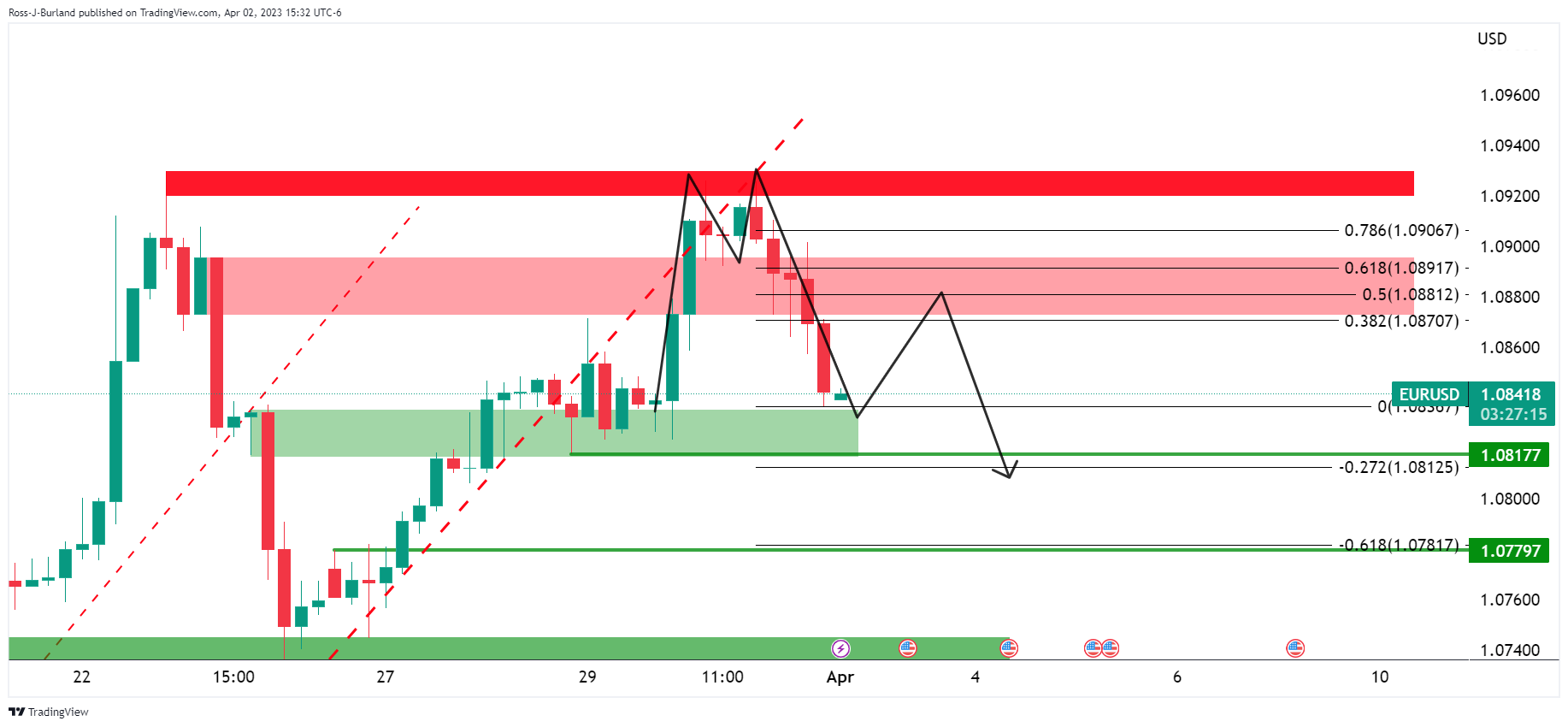

- EUR/USD bears are moving in and testing structure.

- The daily trendline support has been broken.

EUR/USD is flat in the open following a negative day on Friday as the following technical analysis will illustrate. The bears are in the market and structures are being tested.

EUR/USD daily chart

EUR/USD´s daily chart shows a tweezer top, a bearish formation that would be expected to be followed by lower highs and lower closes for the week ahead, especially givent he bears are on on the backside of teh bullish trend.

EUR/USD H4 charts

The 4-hour chart shows the price reaching out of the falling wedge, but the advance has been capped:

The M-formation is a topping pattern and a retest of the neckline could be on the cards prior to the next significant downside continuation for the days ahead.

- USD/CAD bears lurking for the open on OPEC news.

- OPEC producers announce voluntary oil output cuts.

USD/CAD ended Friday near flat but the Canadian Dollar edged lower against its US counterpart although it held near its strongest level in more than five weeks. The pair fell from a high of 1.3564 to a low of 1.3507 while the Canadian Dollar was supported by domestic data that pointed to stronger economic growth in the first quarter than the Bank of Canada has projected.

The Canadian economy expanded 0.5% in January, eclipsing the 0.3% increase economists had expected, while preliminary data for February showed Gross Domestic Product advancing by a further 0.3%. Meanwhile, slower US consumer spending growth boosted hopes the Federal Reserve would be less aggressive in hiking interest rates. The latest Personal Consumption Expenditure price index (PCE) also showed inflation is starting to slow in the US. The core price index lifted just 0.3% in February from 0.6% in January. Core inflation is now at 4.6% YoY and the headline level at 5.0% YoY. Personal income increased by 0.3% (from 0.6% in January) while personal spending dropped to 0.2% (from 2.0%).

Meanwhile, the price of oil, one of Canada's major exports, rose to the highest in three weeks on Friday touching $75.68 as a high in the spot market. The weekend news, OPEC producers announce voluntary oil output cuts, is anticipated to lift the price of oil which would be expected to be supportive of CAD.

Saudi Arabia and other OPEC+ oil producers have announced further oil output cuts of around 1.16 million barrels per day.

Riyadh, Saudi Arabia’s capital and main financial hub, said it would cut output by 500,000 barrels per day, or bdp, from May until the end of 2023, state media reported. Russia’s deputy prime minister also said Moscow would extend a voluntary cut of 500,000 barrels a day until the end of 2023. The United Arab Emirates, Kuwait, Iraq, Oman and Algeria said they would voluntarily cut output over the same time period. The UAE said it would cut production by 144,000 bpd, Kuwait announced a cut of 128,000 bpd while Iraq said it would cut output by 211,000 bpd and Oman announced a cut of 40,000 bpd. Algeria said it would cut its output by 48,000 bpd.

In a statement, the Saudi energy ministry said that the kingdom’s voluntary cut was a precautionary measure aimed at supporting the stability of the oil market.

This is expected to cause an immediate rise in prices for the open. West Texas Intermediate, WTI, crude oil rose to the highest in three weeks on Friday touching $75.68 as a high in the spot market.

- AUD/USD´s bearish engulfment on the last 4-hour candle is eyed.

- Bears eye a break of 0.6661 with 0.6625 seen below there guarding the 0.6550s.

The Australian dollar traded around 30 pips on either side of around 0.67 the figure vs. the greenback on Friday and ended the month little changed, in a period marked by constantly shifting outlooks for interest rates and the banking sector globally.

Meanwhile, easing domestic inflationary pressures leave a question mark over the Reserve Bank of Australia´s interest rate meeting this week. The RBA stated in its latest minutes it would reconsider the case for a pause at the April fixing to reassess the economic outlook.

Looking at the technicals, there is also a downside bias as follows:

AUD/USD weekly chart

The bearish pennant is a compelling feature across the weekly and daily time frames.

AUD/USD daily chart

Failures below 0.6720 keep the bearish bias in place.

AUD/USD H4 chart

The bearish engulfment, BE, on the last 4-hour candle could be the catalyst for a firm break of structure for the opening sessions near 0.6661 with 0.6625 eyed below there guarding the 0.6550s.

© 2000-2026. Sva prava zaštićena.

Sajt je vlasništvo kompanije Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

Svi podaci koji se nalaze na sajtu ne predstavljaju osnovu za donošenje investicionih odluka, već su informativnog karaktera.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Izvršenje trgovinskih operacija sa finansijskim instrumentima upotrebom marginalne trgovine pruža velike mogućnosti i omogućava investitorima ostvarivanje visokih prihoda. Međutim, takav vid trgovine povezan je sa potencijalno visokim nivoom rizika od gubitka sredstava. Проведение торговых операций на финанcовых рынках c маржинальными финанcовыми инcтрументами открывает широкие возможноcти, и позволяет инвеcторам, готовым пойти на риcк, получать выcокую прибыль, но при этом неcет в cебе потенциально выcокий уровень риcка получения убытков. Iz tog razloga je pre započinjanja trgovine potrebno odlučiti o izboru odgovarajuće investicione strategije, uzimajući u obzir raspoložive resurse.

Upotreba informacija: U slučaju potpunog ili delimičnog preuzimanja i daljeg korišćenja materijala koji se nalazi na sajtu, potrebno je navesti link odgovarajuće stranice na sajtu kompanije TeleTrade-a kao izvora informacija. Upotreba materijala na internetu mora biti praćena hiper linkom do web stranice teletrade.org. Automatski uvoz materijala i informacija sa stranice je zabranjen.

Ako imate bilo kakvih pitanja, obratite nam se pr@teletrade.global.

транcфери