- Analiza

- Novosti i instrumenti

- Vesti sa tržišta

Forex-novosti i prognoze od 23-04-2023

- AUD/USD is expected to extend its downside journey amid hawkish Fed bets.

- The USD Index is trying to defend its immediate support of 101.63 ahead of US Durable Goods Orders.

- A consensus of further decline in Australian inflation will allow the RBA to keep rates steady.

The AUD/USD pair has shifted its suction below the round level support of 0.6700 in the Asian session. After defending the immediate support of 0.6680, an absence of recovery in the Aussie asset is making it vulnerable. The downside bias for the Aussie asset is also solid due to rising bets for one more consecutive 25 basis points (bps) rate hike from the Federal Reserve (Fed).

S&P500 futures are holding losses generated in the early Asian session, showing caution as more United States companies are going to report their quarterly earnings ahead. The US Dollar Index (DXY) is attempting to defend the four-day support of 101.63. The USD Index has been displaying topsy-turvy moves for the past four trading sessions in a 101.63-102.23 range amid an absence of a potential trigger.

A power-pack action is expected from the USD Index this week amid the release of the Durable Goods Orders data, which provides a glimpse of forward demand. For March, Durable Goods Orders data is seen expanding by 0.8% vs. a contraction of 1.0%. An upbeat economic data would be supportive of more rate hikes from the Federal Reserve (Fed).

This week, the Australian Dollar will remain in action amid the release of the Inflation data. As per the expectations, inflation data for the first quarter of CY2023 has decelerated to 1.3% from the prior release of 1.9%. Annual inflation has softened to 6.9% vs. the prior release of 7.8%. The monthly Consumer Price Index (CPI) indicator (March) is expected to show further softening to 6.5% against the former release of 6.8%. An occurrence of the same would allow the Reserve Bank of Australia (RBA) to keep the interest rate policy steady ahead.

- USD/CAD is building a base for a decisive break above 1.3550 despite downside bias for the US Dollar Index.

- Higher interest rates by the BoC have heavily impacted on Canada’s retail demand.

- The further downside in the oil price looks solid as global central banks are preparing for a fresh rate hike cycle.

The USD/CAD pair has turned sideways after a stellar north-side move around 1.3550 in the early Asian session. The Loonie asset is expected to extend its recovery sharply above the immediate resistance of 1.3550. The strength in the Loonie asset looks enormous despite a subdued performance by the US Dollar Index (DXY).

S&P500 futures are showing some losses in Asia as investors are worried about forthcoming quarterly results from the United States corporate, portraying a decline in the risk appetite of the market participants. The US Dollar Index (DXY) has dropped below 101.70 and is declining towards the four-day support of 101.63, showing strength in the downside momentum. The demand for US government bonds is getting sluggish as one more rate hike from the Federal Reserve (Fed) is widely expected. The 10-year US Treasury yields have scaled to near 3.57%.

The USD index has failed to capitalize on the upbeat preliminary United States S&P PMI data, released on Friday. S&P Manufacturing data jumped to 50.4 from the consensus of 49.0 and the former release of 49.2. The figure landed above 50.0 for the first time in the past six months, indicating economic recovery amid pessimist circumstances of higher interest rates from the Fed and tight conditions by US banks for consumers and business-type loans.

The Canadian Dollar has faced immense pressure due to Canada’s weak retail demand. February’s Retail Sales report showed that monthly Retail Sales contracted by 0.2% vs. an expectation of 0.6% contraction. Retail Sales ex-auto data contracted by 0.7% against a contraction of 0.1% as expected by the market participants. This shows a sheer impact on retail demand due to higher interest rates by the Bank of Canada (BoC). BoC Governor Tiff Macklem is expected to keep rates steady at elevated levels to bring down stubborn inflation.

On the oil front, oil prices are showing a sideways auction above $77.00. Further downside looks solid as global central banks are preparing for a fresh rate hike cycle, which would heavily impact oil demand. It is worth noting that Canada is the leading exporter of oil to the United States and lower oil prices will impact the Canadian Dollar.

- GBP/USD has stretched its recovery above 1.2440 as USD Index is struggling to defend its four-day support.

- BoE Ramsden warned that the central bank must stop the risk of high inflation becoming embedded in the economy.

- Consecutive Doji formations by GBP/USD indicate a sheer contraction in volatility.

The GBP/USD pair has rebounded sharply above 1.2440 in the early Tokyo session. The Cable is looking to extend its recovery ahead as investors are very much confident of further rate hikes from the Bank of England (BoE).

BoE Deputy Governor Dave Ramsden said in an interview with The Times that the central bank must stop the risk of high inflation becoming embedded in the economy. He added there were still signs of stubbornly high inflation. However, the United Kingdom Retail Sales data landed on Friday contracted more than expected. Monthly (March) Retail Sales data contracted by 0.9% while the street was anticipating a contraction of 0.5%. UK’s stubborn inflation has heavily impacted households’ retail demand.

Meanwhile, S&P500 futures are showing some losses in the early Asian session after a choppy Friday. Investors are witnessing a stock-specific action amid the quarterly earnings season, keeping investors risk-averse. The US Dollar Index (DXY) is struggling to defend the crucial support of 101.70.

Consecutive Doji candlesticks formation on the daily scale by GBP/USD indicates a sheer contraction in volatility. The Cable is struggling to find decisive movements amid an absence of a potential trigger. The 20-period Exponential Moving Average (EMA) at 1.2395 is providing cushion to the Pound Sterling.

Meanwhile, the Relative Strength Index (RSI) (14) has shown a loss in the upside momentum and has shifted into the 40.00-60.00 range.

Further stretch in recovery above April 13 high at 1.2537 will drive the asset towards a fresh 10-month high at 1.2597, which is 08 June 2022 high. A breach of the latter will expose the asset to May 27 high at 1.2667.

On the flip side, a slippage below April 10 low at 1.2345 will expose the asset to March 30 low at 1.2294 followed by March 27 low at 1.2219.

GBP/USD daily chart

- Gold price has stretched its recovery above $1,980.00 despite bets supportive of more rate hikes from the Fed.

- The US Preliminary Manufacturing PMI figure landed above 50.0 for the first time in the past six months.

- Gold price is struggling to defend the cushion from the lower portion of a Rising Channel chart pattern.

Gold price (XAU/USD) showed a recovery move from near the crucial support of $1,970.00 and has stretched its recovery above $1,980.00 in the early Asian session. The precious metal has rebounded after a sheer sell-off despite solid preliminary United States S&P PMI data released on Friday.

S&P500 ended mild positive on Friday as significant movements remained stock-specific due to the quarterly result season, portraying a quiet market mood. The US Dollar Index (DXY) has remained topsy-turvy, ranging in a tight boundary of 101.63-102.14 for the past four trading sessions. Meanwhile, the demand for US government bonds trimmed further as bets for one more rate hike remain solid. This has led to a further jump in US Treasury yields. The yields offered on 10-year US bonds jumped to near 3.57%.

On Friday, the preliminary S&P Manufacturing data jumped to 50.4 from the consensus of 49.0 and the former release of 49.2. The figure landed above 50.0 for the first time in the past six months. A recovery in manufacturing activities in spite of higher interest rates from the Federal Reserve (Fed) and tight credit conditions from US commercial banks supports further policy tightening. This also hints that demand for labor will remain extremely tight.

In addition, preliminary Services PMI jumped to 53.7 from the estimates of 51.5 and the former release of 52.6. An all-around strength in the US economic activities is backing the need for more rate hikes from the Fed.

Gold technical analysis

Gold price is struggling to defend the cushion from the lower portion of a Rising Channel chart pattern formed on a two-hour scale. The precious metal has shifted below the 200-period Exponential Moving Average (EMA) at $1,991.20, which indicates that the long-term trend has turned bearish. A slippage below the immediate support plotted from April 19 low at $1,969.26 will expose the asset to a fresh downside.

The Relative Strength Index (RSI) (14) has shifted its oscillation range into the 20.00-60.00 range indicating a bearish range shift.

Gold two-hour chart

- NZD/USD is correcting into bearish resistance between 0.6150 and the 0.6170s.

- Bears eye a move lower while front side of the bearish trendline.

NZD/USD is flat in the early Asian session and start of the week. The pair is around 0.6135 within a bearish trend and near a fresh low for the month as the US Dollar leads the pack.

´´That was likely a hangover from soft CPI numbers earlier in the week, with markets likely taking the view that soft NZ Consumer Price Index, CPI, might be a harbinger of things to come in AU this week, with neither the Kiwi or Aussie following other correlated currencies like EUR and GBP higher,´´ analysts at ANZ Bank said.

As for the US data, ´´preliminary PMI data indicated a firming in economic activity this month as composite indices recovered to their highest levels in 12 months,´´ the analysts said in a note on Monday morning.

´´ The FOMC is now beginning its blackout period and the ECB will start its quiet period late next week. The market is currently over 90% priced for a 25bp rate rise from the FOMC.´´

On the domestic front, after the surprise from the Reserve Bank of New Zealand, there was little public communication from Bank's officials on the rationale behind the decision, analysts at TD Securities explained. ´´Chief Economist Conway will speak at the universities with comments on monetary policy. Markets will watch Conway's comments on inflation and the Board's reaction function for the May policy decision, especially after the first quarter CPI downside miss.´´

NZD/USD daily charts

As per the prior analysis, NZD/USD Price Analysis: Bears about to reengage for another push to fresh lows, NZD/USD has indeed pushed lower.

(Prior analysis above, update below)

NZD/USD H4 charts

We have seen a firm move lower and the lower time frames can offer clues as to whether this has momentum.

NZD/USD is on the front side of the micro-bear trend and a pullback into the Fibonacci scale aligns with a test of the bearish resistance between 0.6150 and the 0.6170s.

- EUR/USD is on the verge of a breakout.

- EUR/USD bears on the backside of the bullish trend.

EUR/USD has moved to the backside of the bullish trend and below 1.0990 which is now acting as a resistance structure.

EUR/USD weekly chart

The weekly chart shows that the price is pausing at a longer-term resistance area:

The following is a daily and lower timeframe analysis that illustrates the prospects of a move to test 1.0909 and the 1.0830s for the week ahead.

EUR/USD daily chart

If the bears stay committed to the move below 1.1000 and to the back side of the bullish trend, then a break of 1.0910 opens the risk for lower levels:

The 4-hour chart shows that the bulls are attempting to take back control and a break of 1.1090 and 1.1030 will possibly see further demand for higher to come.

The EU is said to get ready a ban on many goods passing through Russia.

Meanwhile, it is reported that Russian troops are concentrating their efforts on conducting offensives toward Bakhmut, Avdiivka, and Marinka in Donetsk Oblast. Ukrainian troops repelled 58 Russian attacks in those directions on April 22, according to the military.

The Sankei newspaper reported Sunday that the Bank of Japan is planning to review and inspect policies taken over the past decades, kicking off discussions at a two-day meeting scheduled for April 27 and 28 under newly-appointed Governor Kazuo Ueda.

Sankei reported that the BOJ will examine the reasons undergirding Japan’s stagnant economy so the central bank can come up with effective policies under Ueda.

Earlier this month, Ueda said he was open to the idea of a longer-term policy review.

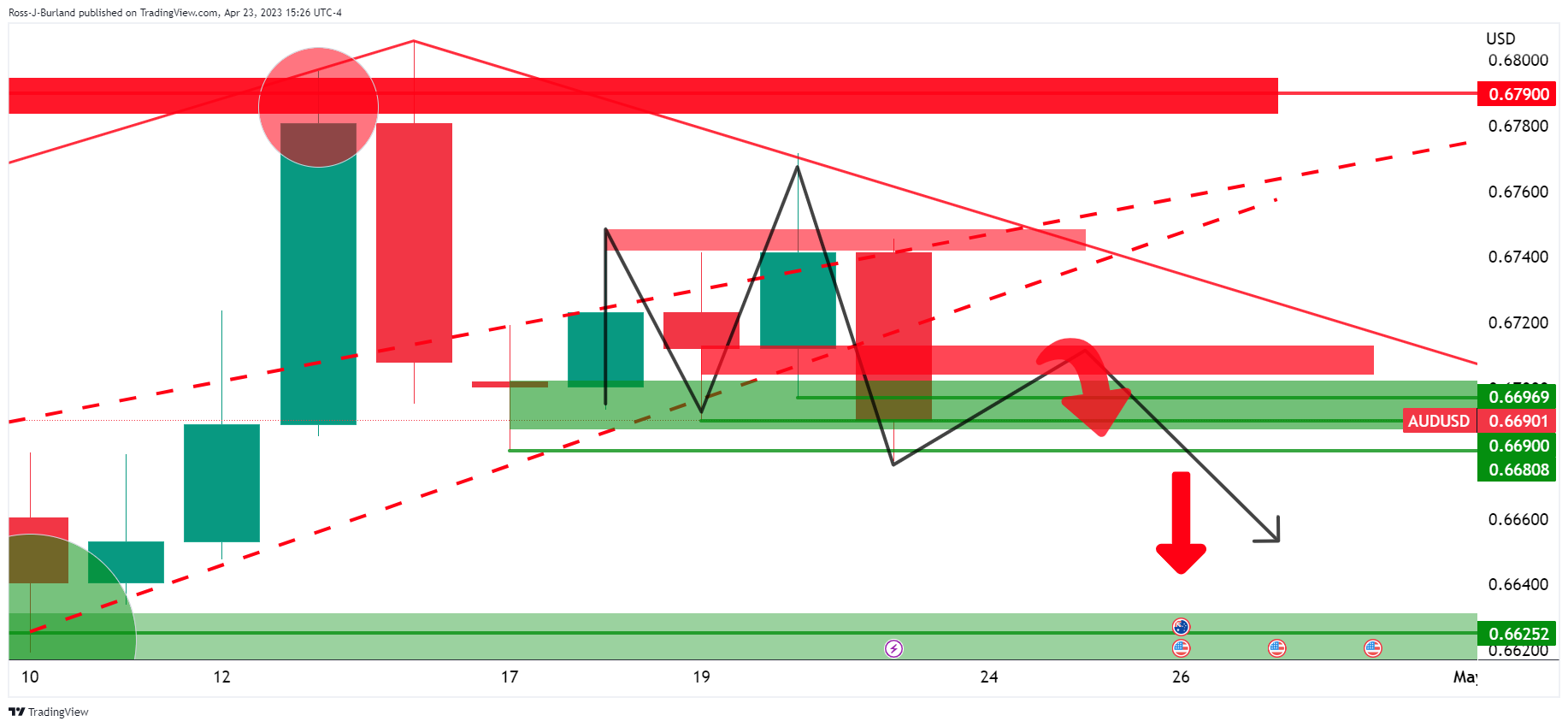

- AUD/USD bears are in the market and price is offered below 0.6710.

- Bears seeking a break in support structure.

AUD/USD has been under pressure over the course of the past few days, despite a strong Australian labour market report for March and the resultant boost in expectations that the RBA may hike rates again as soon as early May. The US Dollar has been firmer, however, as this is seeing to an offer in the pair as the following illustrates:

AUD/USD weekly chart

The weekly chart has the price coiling in the correction with the possibility of a downside continuation while stuck below 0.6790.

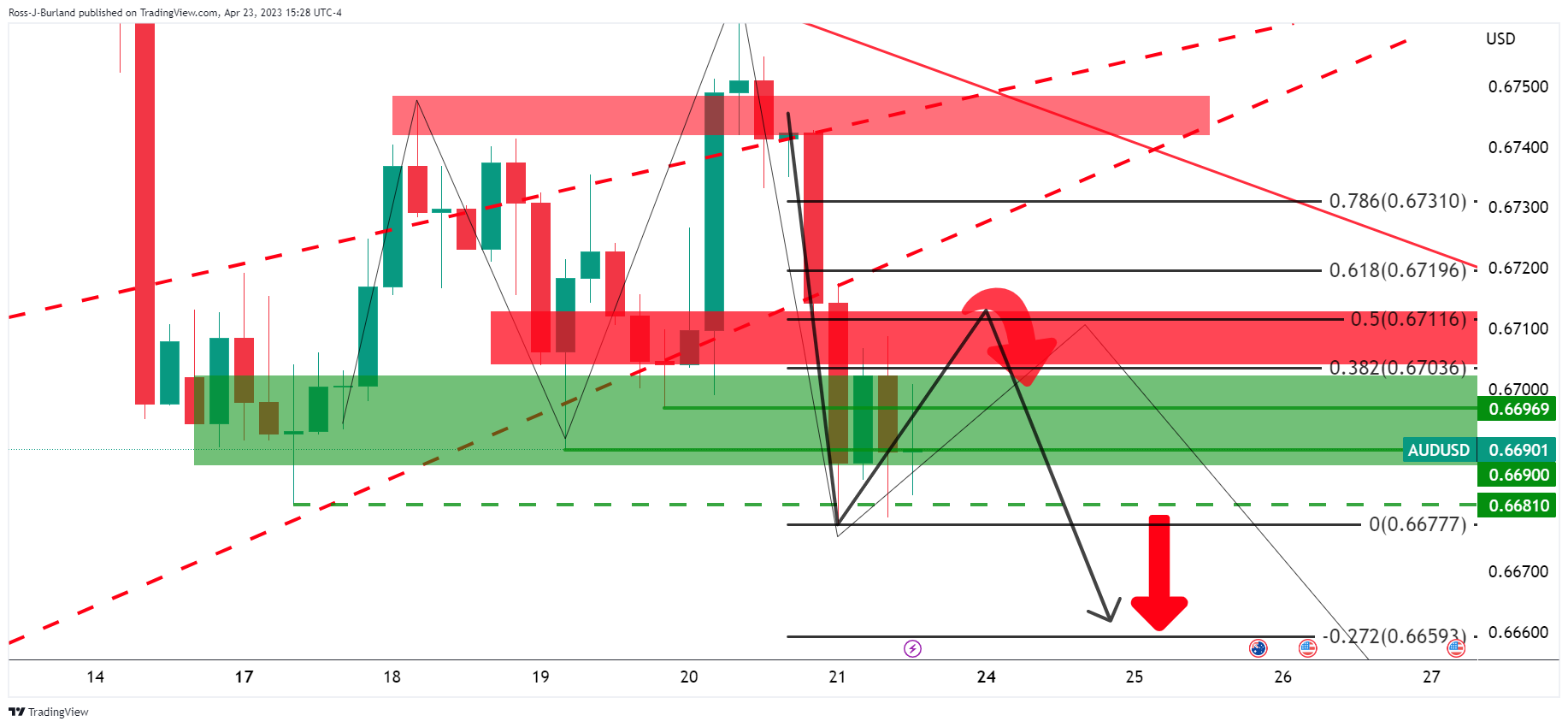

AUD/USD daily charts

The M-formation on the daily chart may act as the peak formation in the correction and lead to a move lower to break the structure on the downside.

AUD/USD H4 chart

The four-hour chart´s 50% mean reversion level near 0.6710 aligns with the neckline of the pattern that could continue to act as resistance.

© 2000-2026. Sva prava zaštićena.

Sajt je vlasništvo kompanije Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

Svi podaci koji se nalaze na sajtu ne predstavljaju osnovu za donošenje investicionih odluka, već su informativnog karaktera.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Izvršenje trgovinskih operacija sa finansijskim instrumentima upotrebom marginalne trgovine pruža velike mogućnosti i omogućava investitorima ostvarivanje visokih prihoda. Međutim, takav vid trgovine povezan je sa potencijalno visokim nivoom rizika od gubitka sredstava. Проведение торговых операций на финанcовых рынках c маржинальными финанcовыми инcтрументами открывает широкие возможноcти, и позволяет инвеcторам, готовым пойти на риcк, получать выcокую прибыль, но при этом неcет в cебе потенциально выcокий уровень риcка получения убытков. Iz tog razloga je pre započinjanja trgovine potrebno odlučiti o izboru odgovarajuće investicione strategije, uzimajući u obzir raspoložive resurse.

Upotreba informacija: U slučaju potpunog ili delimičnog preuzimanja i daljeg korišćenja materijala koji se nalazi na sajtu, potrebno je navesti link odgovarajuće stranice na sajtu kompanije TeleTrade-a kao izvora informacija. Upotreba materijala na internetu mora biti praćena hiper linkom do web stranice teletrade.org. Automatski uvoz materijala i informacija sa stranice je zabranjen.

Ako imate bilo kakvih pitanja, obratite nam se pr@teletrade.global.

транcфери