- Analiza

- Novosti i instrumenti

- Vesti sa tržišta

Forex-novosti i prognoze od 31-01-2018

(index / closing price / change items /% change)

Nikkei -193.68 23098.29 -0.83%

TOPIX -21.42 1836.71 -1.15%

Hang Seng +279.98 32887.27 +0.86%

CSI 300 +19.80 4275.90 +0.47%

Euro Stoxx 50 +2.54 3609.29 +0.07%

FTSE 100 -54.43 7533.55 -0.72%

DAX -8.23 13189.48 -0.06%

CAC 40 +8.15 5481.93 +0.15%

DJIA +72.50 26149.39 +0.28%

S&P 500 +1.38 2823.81 +0.05%

NASDAQ +9.00 7411.48 +0.12%

S&P/TSX -3.84 15951.67 -0.02%

(pare/closed(GMT +2)/change, %)

EUR/USD $1,2413 +0,09%

GBP/USD $1,4192 +0,31%

USD/CHF Chf0,93115 -0,30%

USD/JPY Y109,17 +0,37%

EUR/JPY Y135,53 +0,46%

GBP/JPY Y154,948 +0,68%

AUD/USD $0,8056 -0,35%

NZD/USD $0,7364 +0,46%

USD/CAD C$1,23134 -0,20%

00:30 Australia Export Price Index, q/q Quarter IV -3.0% -8%

00:30 Australia Import Price Index, q/q Quarter IV -1.6% -0.8%

00:30 Australia Building Permits, m/m December 11.7% -1.7%

00:30 Japan Manufacturing PMI (Finally) January 54.0 54.4

01:45 China Markit/Caixin Manufacturing PMI January 51.5 51.3

06:45 Switzerland SECO Consumer Climate Quarter I -2

07:00 United Kingdom Nationwide house price index January 0.6% 0.2%

07:00 United Kingdom Nationwide house price index, y/y January 2.6% 2.5%

08:15 Switzerland Retail Sales (MoM) December 1.3%

08:15 Switzerland Retail Sales Y/Y December -0.2%

08:30 Switzerland Manufacturing PMI January 65.2 64.0

08:50 France Manufacturing PMI (Finally) January 58.8 58.1

08:55 Germany Manufacturing PMI (Finally) January 63.3 61.2

09:00 Eurozone Manufacturing PMI (Finally) January 60.6 59.6

09:30 United Kingdom Purchasing Manager Index Manufacturing January 56.3 56.5

11:15 Eurozone ECB's Peter Praet Speaks

13:30 U.S. Continuing Jobless Claims January 1937 1916

13:30 U.S. Initial Jobless Claims January 233 238

13:30 U.S. Unit Labor Costs, q/q (Preliminary) Quarter IV -0.2% 0.8%

13:30 U.S. Nonfarm Productivity, q/q(Preliminary) Quarter IV 3.0% 1%

14:45 U.S. Manufacturing PMI (Finally) January 55.1 55.5

15:00 U.S. Construction Spending, m/m December 0.8% 0.4%

15:00 U.S. ISM Manufacturing January 59.7 58.8

20:00 U.S. Total Vehicle Sales, mln January 17.85 17.2

21:45 New Zealand Visitor Arrivals December 8.00%

21:45 New Zealand Building Permits, m/m December 10.8%

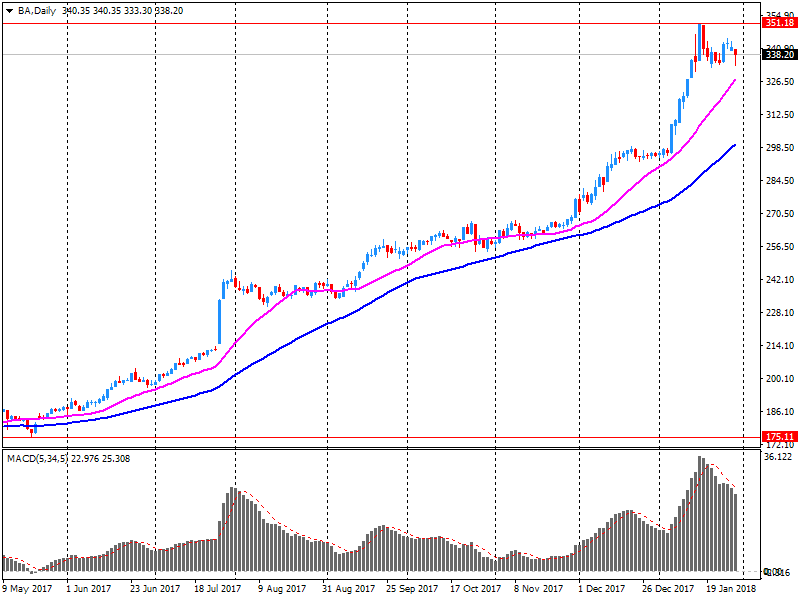

The main US stock indices grew moderately, helped by the Boeing rally after the publication of the quarterly report, as well as positive data on the US, and the results of the Fed meeting.

The ADP report showed that employment growth in the US private sector slowed in January, but was stronger than projected. According to the report, in January the number of employed increased by 234 thousand people compared with the figure for December at 242 thousand. It was expected that the number of employed will increase by 185 thousand.

In addition, Chicago Purchasing Managers Index fell 2.1 points to 65.7 in January from a revised 67.8 points in December. Despite the fact that in January it lost momentum, the index continued to move in the same direction as in the second half of 2017, which contributes to an encouraging new year. The index has grown by 28.3% since January last year and at the level of 65.7 exceeds the average of the second half of 2017, equal to 63.7.

Contracts for the purchase of previously owned homes in the United States rose for the third consecutive month in December, helped by a healthy labor market. The National Association of Realtors said that its index of unfinished transactions for the sale of housing rose to 110.1 points last month, which is 0.5% more than in November. Economists predicted that the index will increase by 0.4%, following an increase of 0.3% in the previous month (revised from + 0.2%).

As for the Fed meeting, it was decided to leave interest rates unchanged. At the same time, the Fed indicated that it intends to continue the gradual tightening of monetary policy in order to stimulate economic growth. In general, the rhetoric of the statement remained largely unchanged compared to December, indicating a still positive assessment of the prospects for the US economy. It should be noted that this meeting was the last for Fed Chairman Yellen, whose powers expire on Saturday. The new head of the Federal Reserve will be Powell

Most components of the DOW index finished trading in positive territory (17 out of 30). The leader of growth was the shares of The Boeing Company (BA, + 5.31%). Outsider were shares of Johnson & Johnson (JNJ, -2.43%).

Almost all sectors of the S & P index recorded an increase. The utilities sector grew most (+ 0.9%). Decrease showed only the health sector (-1.1%).

At closing:

DJIA + 0.28% 26.150.80 +73.91

Nasdaq + 0.12% 7,411.48 +9.00

S & P + 0.05% 2,823.93 +1.50

At 418.4 million barrels, U.S. crude oil inventories are in the middle of the average range for this time of year.

Total motor gasoline inventories decreased by 2.0 million barrels last week, and are near the top of the average range. Both blending components and finished gasoline inventories decreased last week.

Distillate fuel inventories decreased by 1.9 million barrels last week and are in the middle of the average range for this time of year. Propane/propylene inventories decreased by 0.9 million barrels last week, but are in the middle of the average range. Total commercial petroleum inventories increased by 2.1 million barrels last week.

The Pending Home Sales Index, a forward-looking indicator based on contract signings, moved higher 0.5 percent to 110.1 in December from an upwardly revised 109.6 in November. With last month's modest increase, the index is now 0.5 percent above a year ago.

Lawrence Yun, NAR chief economist, says pending sales edged up in December and reached their highest level since last March (111.3). "Another month of modest increases in contract activity is evidence that the housing market has a small trace of momentum at the start of 2018," he said. "Jobs are plentiful, wages are finally climbing and the prospect of higher mortgage rates are perhaps encouraging more aspiring buyers to begin their search now."

U.S. stock-index futures rose on Wednesday, after two days of sharp declines, boosted by a controversy-free State of Union speech by the U.S. President Donald Trump, with investors turning their focus back to the Fed's monetary policy and corporate segment's quarterly results.

Global Stocks:

Nikkei 23,098.29 -193.68 -0.83%

Hang Seng 32,887.27 +279.98 +0.86%

Shanghai 3,481.51 -6.50 -0.19%

S&P/ASX 6,037.70 +14.90 +0.25%

FTSE 7,580.65 -7.33 -0.10%

CAC 5,494.16 +20.38 +0.37%

DAX 13,228.74 +31.03 +0.24%

Crude $64.19 (-0.48%)

Gold $1,343.60 (+0.61%)

Real gross domestic product (GDP) increased 0.4% in November, with widespread growth across industries as 17 of 20 industrial sectors increased.

Goods-producing industries rose 0.8% after declining 0.5% in October. November's gain was mainly due to increases in the manufacturing and mining, quarrying and oil and gas extraction sectors, partly as a result of restoration in production capacity. Meanwhile, services-producing industries rose 0.3%, led by the real estate and rental and leasing, wholesale, and retail trade sectors.

The manufacturing sector was up 1.8% in November, the largest monthly increase since February 2014 as the majority of subsectors grew. Non-durable manufacturing rose 1.1%, while durable manufacturing jumped 2.5%.

Private sector employment increased by 234,000 jobs from December to January according to the January ADP National Employment Report.

"We've kicked off the year with another month of unyielding job gains," said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute. "Service providers were firing on all cylinders, posting their strongest gain in more than a year. We also saw robust hiring from midsize and large companies, while job growth in smaller firms slowed slightly."

(company / ticker / price / change ($/%) / volume)

| 3M Co | MMM | 253.6 | 2.06(0.82%) | 1445 |

| Amazon.com Inc., NASDAQ | AMZN | 1,451.78 | 13.96(0.97%) | 93961 |

| American Express Co | AXP | 99.08 | 0.37(0.37%) | 937 |

| Apple Inc. | AAPL | 166.49 | -0.48(-0.29%) | 501779 |

| AT&T Inc | T | 37.5 | 0.06(0.16%) | 18186 |

| Barrick Gold Corporation, NYSE | ABX | 14.42 | 0.11(0.77%) | 5468 |

| Boeing Co | BA | 356.3 | 18.59(5.50%) | 496388 |

| Caterpillar Inc | CAT | 165.02 | 1.26(0.77%) | 27210 |

| Chevron Corp | CVX | 125.75 | 0.52(0.42%) | 4127 |

| Cisco Systems Inc | CSCO | 42.01 | -0.24(-0.57%) | 36652 |

| Citigroup Inc., NYSE | C | 78.91 | 0.29(0.37%) | 50908 |

| Exxon Mobil Corp | XOM | 87.06 | 0.28(0.32%) | 6352 |

| Facebook, Inc. | FB | 188.6 | 1.48(0.79%) | 302124 |

| FedEx Corporation, NYSE | FDX | 264 | 2.54(0.97%) | 1434 |

| Ford Motor Co. | F | 11.13 | 0.07(0.63%) | 34194 |

| Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 19.42 | 0.29(1.52%) | 16894 |

| General Electric Co | GE | 16.07 | 0.12(0.75%) | 176932 |

| General Motors Company, NYSE | GM | 43 | 0.30(0.70%) | 5876 |

| Goldman Sachs | GS | 269.96 | 1.02(0.38%) | 10217 |

| Google Inc. | GOOG | 1,173.37 | 9.68(0.83%) | 12718 |

| Hewlett-Packard Co. | HPQ | 23.93 | 0.49(2.09%) | 780 |

| Home Depot Inc | HD | 203.5 | 1.69(0.84%) | 3240 |

| HONEYWELL INTERNATIONAL INC. | HON | 161 | 2.03(1.28%) | 1302 |

| Intel Corp | INTC | 49.13 | 0.34(0.70%) | 44367 |

| International Business Machines Co... | IBM | 164.62 | 1.00(0.61%) | 13281 |

| Johnson & Johnson | JNJ | 142.65 | 0.22(0.15%) | 4090 |

| JPMorgan Chase and Co | JPM | 115.79 | 0.68(0.59%) | 36570 |

| McDonald's Corp | MCD | 173.75 | 1.27(0.74%) | 16564 |

| Merck & Co Inc | MRK | 60.7 | 0.05(0.08%) | 8116 |

| Microsoft Corp | MSFT | 93.62 | 0.88(0.95%) | 240160 |

| Nike | NKE | 67.6 | 0.27(0.40%) | 3933 |

| Pfizer Inc | PFE | 37.94 | 0.14(0.37%) | 26547 |

| Procter & Gamble Co | PG | 86.94 | -0.01(-0.01%) | 7647 |

| Starbucks Corporation, NASDAQ | SBUX | 57.35 | 0.16(0.28%) | 9581 |

| Tesla Motors, Inc., NASDAQ | TSLA | 348.5 | 2.68(0.78%) | 18714 |

| The Coca-Cola Co | KO | 47.44 | 0.03(0.06%) | 1144 |

| Twitter, Inc., NYSE | TWTR | 25.7 | 0.08(0.31%) | 143380 |

| United Technologies Corp | UTX | 137.12 | 0.62(0.45%) | 740 |

| UnitedHealth Group Inc | UNH | 240.24 | 3.59(1.52%) | 9911 |

| Verizon Communications Inc | VZ | 54 | 0.10(0.19%) | 1069 |

| Visa | V | 124.6 | 1.05(0.85%) | 14679 |

| Wal-Mart Stores Inc | WMT | 108.6 | 0.87(0.81%) | 2842 |

| Walt Disney Co | DIS | 111.03 | 0.92(0.84%) | 1635 |

| Yandex N.V., NASDAQ | YNDX | 38.4 | 0.30(0.79%) | 200 |

McDonald's (MCD) target raised to $190 from $180 at Telsey Advisory Group

Apple (AAPL) downgraded to Market Perform from Outperform at BMO Capital

Boeing (BA) reported Q4 FY 2017 earnings of $3.04 per share (versus $2.47 in Q4 FY 2016), beating analysts' consensus estimate of $2.88.

The company's quarterly revenues amounted to $25.368 bln (+8.9% y/y), beating analysts' consensus estimate of $24.780 bln.

The company also issued upside guidance for FY 2018, projecting EPS of $13.80-14.00 (versus analysts' consensus estimate of $11.90) at revenues of $96-98 bln (versus analysts' consensus estimate of $93.6 bln).

BA rose to $355.00 (+5.12%) in pre-market trading.

The euro area (EA19) seasonally-adjusted unemployment rate was 8.7% in December 2017, stable compared to November 2017 and down from 9.7% in December 2016. This remains the lowest rate recorded in the euro area since January 2009.

The EU28 unemployment rate was 7.3% in December 2017, stable compared to November 2017 and down from 8.2% in December 2016. This remains the lowest rate recorded in the EU28 since October 2008.

Euro area annual inflation is expected to be 1.3% in January 2018, down from 1.4% in December 2017, according to a flash estimate from Eurostat, the statistical office of the European Union.

Looking at the main components of euro area inflation, energy is expected to have the highest annual rate in January (2.1%, compared with 2.9% in December), followed by food, alcohol & tobacco (1.9%, compared with 2.1% in December), services (1.2%, stable compared with December) and non-energy industrial goods (0.6%, compared with 0.5% in December).

In December 2017, 23.067 million persons were employed, -0.3% over November 2017. Unemployed were 2.791 million, -1.7% over the previous month.

Employment rate was 58.0%, -0.2 percentage points over the previous month, unemployment rate was 10.8% -0.1 percentage points over November 2017 and inactivity rate was 34.8%, +0.3 percentage points in a month.

Youth unemployment rate (aged 15-24) was 32.2%, -0.2 percentage points over the previous month and youth unemployment ratio in the same age group was 8.2%, -0.2 percentage points over November 2017.

Over a year, the Consumer Price Index (CPI) should rise by 1.4% in January 2018 after +1.2% in the previous month, according to the provisional estimate made at the end of January 2018. This increase in the year-on-year inflation should come from an acceleration in services prices and in energy prices and a slight rebound in "manufactured product" prices whereas food and tobacco should slow down.

Over one month, consumer prices should edge down by 0.1% after +0.3% in December. Energy prices should sharply accelerate because of the increase in Brent crude and in taxation. Food prices should rise slightly. On the other hand, "manufactured product" prices should fell back significantly, due to the beginning of winter sales. Tobacco prices shoud edge down. Lastly, services prices should slow down.

Year on year, the Harmonised Index of Consumer Prices should increase faster than in the previous month (+1.5% after +1.2% in December). Over one month, it should edge down: −0.1% after +0.4%.

EUR/USD

Resistance levels (open interest**, contracts)

$1.2553 (2636)

$1.2525 (1086)

$1.2501 (2264)

Price at time of writing this review: $1.2451

Support levels (open interest**, contracts):

$1.2366 (784)

$1.2340 (671)

$1.2308 (1538)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date February, 9 is 133118 contracts (according to data from January, 30) with the maximum number of contracts with strike price $1,1850 (7037);

GBP/USD

Resistance levels (open interest**, contracts)

$1.4304 (1187)

$1.4279 (739)

$1.4240 (561)

Price at time of writing this review: $1.4204

Support levels (open interest**, contracts):

$1.4094 (149)

$1.4048 (94)

$1.3987 (143)

Comments:

- Overall open interest on the CALL options with the expiration date February, 9 is 44652 contracts, with the maximum number of contracts with strike price $1,3600 (3462);

- Overall open interest on the PUT options with the expiration date February, 9 is 41923 contracts, with the maximum number of contracts with strike price $1,3400 (3038);

- The ratio of PUT/CALL was 0.94 versus 0.92 from the previous trading day according to data from January, 30

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

According to provisional data turnover in retail trade in December 2017 was in real terms 1.9% and in nominal terms 0.2% smaller than in November 2016. The number of days open for sale was 24 in December 2017 and 26 in December 2016.

Compared with the previous year, turnover in retail trade was in the whole year 2017 in real terms 2.3% and in nominal terms 4.2% larger than in 2016.

When adjusted for calendar and seasonal variations (Census-X-12-ARIMA), the December 2017 turnover was in real terms 1.9% and in nominal terms 1.5% lower than in November 2017.

-

Only need to look at "depraved character" of North Korean leadership to understand nature of nuclear threat to U.S. and its allies

-

U.S. will not repeat "mistakes of past administrations that got us into this very dangerous position" with North Korea

-

Careful consideration is needed for central banks to issue cryptocurrency given impacts on financial intermediation

-

Don't see problem with financial intermediation now

-

2 pct inflation is very far so current yield curve is appropriate

-

There is misunderstanding in market BoJ will exit easy policy soon

-

No need to raise yield targets now, see no change for some time

-

Important for BoJ to be ready to change yield targets if economy, price, financial conditions change

The manufacturing sector in China continued to expand in January, albeit at a slower pace, the National Bureau of Statistics, cited by rttnews, with a Manufacturing PMI score of 51.3.

That missed expectations for 51.5 and was down from 51.6 in December.

It also remained above the boom-or-bust line of 50 that separates expansion from contraction.

The bureau also noted that the non-manufacturing PMI came in with a score of 55.3 - beating forecasts for 54.9 and up from 55.0 in the previous month.

The all groups CPI

-

Rose 0.6% this quarter, compared with a rise of 0.6% in the september quarter 2017.

-

Rose 1.9% over the twelve months to the december quarter 2017, compared with a rise of 1.8% over the twelve months to the september quarter 2017.

Overview of CPI movements

-

The most significant price rises this quarter are automotive fuel (+10.4%), tobacco (+8.5%), domestic holiday travel and accommodation (+6.3%) and fruit (+9.3%).

-

The most significant offsetting price falls this quarter are international holiday travel and accommodation (-1.7%), audio visual and computing equipment (-3.5%), and telecommunication equipment and services (-1.4%).

Asia-Pacific shares broadly turned around early declines as President Donald Trump struck a mostly conciliatory tone in his first State of the Union address. After some of the biggest declines in several months Tuesday, indexes in Australia XJO, +0.34% , Hong Kong and South Korea SEU, +0.94% turned higher, gaining as much as much as 0.5%.

European stocks fell Tuesday, tracking losses across global markets, as investors grew increasingly concerned about a sharp rise in U.S. bond yields and its impact on the cost of borrowing. Heavily-weighted oil companies led the decliners, as crude-oil prices came under pressure.

U.S. stocks sold off for a second straight session on Tuesday, with the Dow suffering its biggest one-day drop in eight months, as heavy losses in health-care and energy shares weighed on the main indexes. The Dow Jones Industrial Average was down as much as 400 points after Amazon, Berkshire Hathaway and JPMorgan Chase announced they would partner in an effort to cut health-care costs and improve services for U.S. employees.

© 2000-2026. Sva prava zaštićena.

Sajt je vlasništvo kompanije Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

Svi podaci koji se nalaze na sajtu ne predstavljaju osnovu za donošenje investicionih odluka, već su informativnog karaktera.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Izvršenje trgovinskih operacija sa finansijskim instrumentima upotrebom marginalne trgovine pruža velike mogućnosti i omogućava investitorima ostvarivanje visokih prihoda. Međutim, takav vid trgovine povezan je sa potencijalno visokim nivoom rizika od gubitka sredstava. Проведение торговых операций на финанcовых рынках c маржинальными финанcовыми инcтрументами открывает широкие возможноcти, и позволяет инвеcторам, готовым пойти на риcк, получать выcокую прибыль, но при этом неcет в cебе потенциально выcокий уровень риcка получения убытков. Iz tog razloga je pre započinjanja trgovine potrebno odlučiti o izboru odgovarajuće investicione strategije, uzimajući u obzir raspoložive resurse.

Upotreba informacija: U slučaju potpunog ili delimičnog preuzimanja i daljeg korišćenja materijala koji se nalazi na sajtu, potrebno je navesti link odgovarajuće stranice na sajtu kompanije TeleTrade-a kao izvora informacija. Upotreba materijala na internetu mora biti praćena hiper linkom do web stranice teletrade.org. Automatski uvoz materijala i informacija sa stranice je zabranjen.

Ako imate bilo kakvih pitanja, obratite nam se pr@teletrade.global.

транcфери