- Analytics

- News and Tools

- Market News

Analytics, News, and Forecasts for CFD Markets: currency news — 08-02-2021.

| Time | Country | Event | Period | Previous value | Forecast |

|---|---|---|---|---|---|

| 00:30 (GMT) | Australia | National Australia Bank's Business Confidence | January | 4 | |

| 02:00 (GMT) | New Zealand | Expected Annual Inflation 2y from now | Quarter I | 1.6% | |

| 06:00 (GMT) | Japan | Prelim Machine Tool Orders, y/y | January | 8.7% | |

| 07:00 (GMT) | Germany | Current Account | December | 21.3 | |

| 07:00 (GMT) | Germany | Trade Balance (non s.a.), bln | December | 17.2 | |

| 15:00 (GMT) | U.S. | JOLTs Job Openings | December | 6.527 | |

| 17:00 (GMT) | U.S. | FOMC Member James Bullard Speaks | |||

| 23:30 (GMT) | Australia | Westpac Consumer Confidence | February | 107 |

FXStreet notes that returns on ten-year Treasuries are nearing 1.20% but economists at Capital Economics still would not expect Treasury yields to rise very sharply from here. They suspect that if they do increase over the next couple of years, it is likely to be driven by higher inflation compensation rather than higher real yields.

“We doubt that the nominal yield of 10-year conventional Treasuries will continue to rise significantly this year. Admittedly, we wouldn’t be surprised if inflation compensation increased further as the economic recovery gained traction. But we don’t think that this would lead to tighter monetary policy, and by extension, rising real yields.”

“We think the Fed would be comfortable with higher inflation compensation. By its own estimates, long-term inflation expectations are probably still below the level consistent with its policy goals. And in any case, the Fed has emphasised that it wants to see realised inflation sustainably above target before it considers any material tightening in monetary policy.”

- Recent events have shown we need to look at its application on ground

- There are a number of issues where we believe we need refinement about how it operates

- We can resolve company trade issues pragmatically

- European Commission probably owes its member states fuller explanation for its actions

- Progress is being made but we are far from resolving all issues

ING's economists note that a new divergence has characterised the economic performance of the eurozone since the summer.

"Since the summer, the manufacturing sector has decoupled from services, which have continued to suffer from ongoing social distancing and new lockdowns. However, this decoupling at the eurozone level has masked significant differences across individual countries. From the summer months onwards, the manufacturing sectors of Germany and Italy were able to expand, while in Spain and France, the sector flirted with contraction."

"And the start of the year didn’t change this dynamic. The Italian PMI for the manufacturing sector increased to 55.1 compared to 52.8 in December, while the index for Germany remained firmly above the 55 level. This is in contrast to the developments in France and Spain. "

"The severity of the pandemic and the strictness of the lockdown measures can only do so much to explain the depth of the trough in April. The number of new infections (per million inhabitants) did start to increase during the summer months in France and Spain, which was not the case in Germany and Italy."

"A more important driver of the divergence is the structure of the manufacturing sectors. Countries that produce a lot of products that can be exported to countries that are currently doing well economically, such as China, have shown a stronger and more stable performance."

"Add to this the fact that the share of the manufacturing sector in total added value for the entire economy is much larger in Germany (19%) and Italy (15%) than it is in Spain (11%) and France (10%), and it seems likely that we'll see not only continued divergence in manufacturing sectors but in total economic performance, too."

"Once the number of infections has come down, in particular in Spain, and more and more Europeans are vaccinated, we expect that manufacturing activity in Spain and France will also be able recover."

- We will continue with interest rate reform

- Will fend off systematic financial risks

- Will continue prudent and stable monetary policy

- Will make prudent monetary policy flexible, targeted, appropriate, with no sudden shift on monetary

- Will look to enhance flexibility of what you want exchange rates

FXStreet notes that the S&P 500 rally has finally extended to 3900 and with further layers of resistance seen here and stretching up to 3930, economists at Credit Suisse expect the 3900/3930 area to cap at first and for a temporary consolidation phase to emerge.

“Base case remains for a cap in the 3900/3930 zone and for a potentially lengthier consolidation/correction phase to then unfold. Indeed, this latest move higher has been seen on lower volume, RSI momentum holds a bearish divergence on a daily and weekly basis, which is seen adding weight to this risk.”

“Support is seen at 3875/71 initially, below which can ease the immediate upside bias for a retreat back to 3860, then 3847/37.”

| Time | Country | Event | Period | Previous value | Forecast | Actual |

|---|---|---|---|---|---|---|

| 06:45 | Switzerland | Unemployment Rate (non s.a.) | January | 3.5% | 3.7% | |

| 07:00 | Germany | Industrial Production s.a. (MoM) | December | 1.5% | 0.3% | 0% |

| 09:30 | Eurozone | Sentix Investor Confidence | February | 1.3 | -0.2 |

USD strengthened against its major rivals in the European session on Monday as the U.S. Treasury yields rose after a disappointing U.S. jobs report increased expectations for additional fiscal stimulus. The 10-year yield is currently up almost two basis points to 1.19% compared to 0.92% at the beginning of the year.

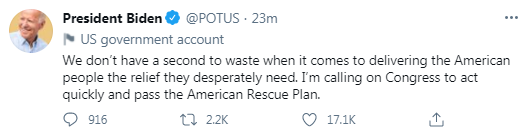

The House of Representatives approved a budget resolution on Friday, setting the stage for passage of the president Joe Biden's $1.9 trillion COVID-19 relief package.

On Sunday, the U.S. Treasury Secretary Janet Yellen endorsed a massive stimulus package, which should include checks to American workers who earn $60,000 per year. She also suggested that the full employment could return next year if Biden's proposed $1.9 trillion coronavirus relief bill was approved by Congress. Otherwise, she added, unemployment would linger for years.

Prospects of more stimulus raised fears of inflation rising, leading to a selloff in the U.S. Treasuries. However, Yellen noted that "we have good tools to deal with that risk if it materializes".

- All three vaccines approved in EU are effective, they help avoid serious cases

- We can't give people choice of vaccine currently due to limited doses

FXStreet reports that analysts at Credit Suisse note that the USD/CHF pair did unwind the overbought condition on Friday, but maintains a small “head and shoulders” base with key resistance seen at 0.9079/95.

“USD/CHF reverted lower on Friday as the market unwound the oversold condition, coming to a halt ahead of the crucial back of the broken downtrend at 0.8971. The pair has subsequently shifted into a very near-term consolidation range, however with daily MACD momentum still pointing higher, we look for strength to resume as a small ‘head and shoulders’ base is still in place.”

“Resistance is seen initially at 0.9007, then 0.9046, removal of which would expose the 61.8% retracement of the September 2020/January 2021 fall, our ‘measured base objective’ and the downtrend from early 2020 at 0.9079/95.”

After seven consecutive months of strong increases, Germany's industrial production took a break in December, remaining unchanged from an upwardly revised 1.5% month-on-month rate in November, noted Carsten Brzeski the Global Head of Macro for ING Research.

"On the year, industrial production was still down by 1%. While the production of consumer goods and intermediate goods increased, the production of capital goods slightly dropped. Likely driven by the Christmas break, activity in the construction sector dropped by 3.2% MoM."

"Since the summer, industrial activity has decoupled from the service sector and other lockdown-hit activities. The nature of the ‘smart lockdowns’ is clearly one important driver of this divergence. While many parts of the German manufacturing sector voluntarily closed down during the first lockdown, also driven by severe supply chain disruptions, factories have remained open during the second lockdown. Also, don’t forget that the German manufacturing sector seems to have benefited a lot from the strong and continuing recovery of the Chinese economy."

"Looking ahead, it currently looks unlikely that the manufacturing sector will save the German economy from contraction once again. Production expectations have recovered somewhat since November but are still below their summer levels. At the same time, the inventory reduction of the second half of 2020 seems to have come to an end at the turn of the year."

FXStreet reports that EUR/USD has posted a bullish “reversal day” from the 23.6% retracement of the entire 2020/2021 rally at 1.1945/14 and economists at Credit Suisse continue to look for a near-term recovery from here.

“Resistance moves to 1.2051/55 initially, then the near-term downtrend and price resistance at 1.2088, with the 38.2% retracement of the January/February fall seen at 1.2104. We would look for this 1.2088/1.2104 zone to then ideally cap for a fresh move lower.”

“Support is seen at 1.2001, then 1.1981. Below 1.1914 would warn of a more significant correction lower with support seen next at 1.1800 and more importantly at 1.1695 – the 38.2% retracement of the 2020/2021 uptrend and the 200-day average.”

FXStreet reports that economist at UOB Group Lee Sue Ann assesses the latest BoE event.

“At its first meeting for the year, the Bank of England (BOE)’s monetary policy committee (MPC) judged that the existing stance of monetary policy remains appropriate.”

“The BOE, on Thursday, also updated its forecasts, adding that the UK economy did not suffer as badly at the end of 2020 as previously expected, but there would be a downturn in the first quarter of 2021 because of the long lockdown while vaccinations were rolled out... But the economy is still predicted to return to its pre-pandemic size in early 2022, with consumers expected to spend heavily once the pandemic restrictions were lifted.”

“There is certainly somewhat less pressure for the BOE to offer furtther stimulus given the rapid vaccine rollout and the corresponding likelihood of a recovery beyond Spring. That said, the outlook for the UK remains incredibly uncertain with downside risks. At this juncture, we are not ruling out an acceleration in the pace of bond purchases, or changes to the Term Funding Scheme. As for negative interest rates, we are not expecting any further cuts for now, though policymakers will be careful not to shut the door to this option.”

FXStreet notes that EUR/USD holds long-term Fibonacci support at 1.1945. Nonetheless, analysts at Commerzbank expect that after a brief recovery towards 1.2085, the pair is to fall to 1.1750.

“EUR/USD has sold off to support at 1.1945, which is the 23.6% retracement of the move up since March 2020. While this has held the initial test, rallies from here are expected to struggle on moves to the six-week downtrend at 1.2085. This resistance is reinforced by the 55-day ma at 1.2129.”

“A close below 1.1945 is needed to imply a deeper sell-off to 1.1750 and possibly the 1.1695/02 support, this is the 38.2% retracement and the September and November lows.”

Bloomberg reports that yields on the longest-dated U.S. benchmark bond have topped 2% for the first time in close to a year, fueled by advancing talks on U.S. fiscal stimulus and rising expectations for inflation.

The selloff in Treasuries pushed the yield on the 30-year bond up by as much as three basis points to 2.00%, the highest since Feb. 2020. The level is psychologically important, in part because 2% is the pace of inflation that the Federal Reserve looks to maintain for consumer prices.

The move on Monday follows a series of comments from policy makers on both sides of the Atlantic at the weekend.

FXStreet reports that analysts at Mizuho Bank discuss USD/CAD prospects.

“Some observers say the vaccine roll-out has been delayed, but if a structure is put in place soon and vaccines are steadily implemented, then domestic economic growth could recover to pre-pandemic levels by the end of 2021. With the markets swinging between risk aversion and risk appetite on the covid situation, it seems WTI prices will continue trading around $40-50/barrel. Various countries will undergo economic recoveries in the medium-term, so WTI prices are unlikely to collapse, with the USD/CAD pair also set to continue trading below 1.30. The Bank of Canada will probably maintain its current pace of quantitative easing. This is another reason why the USD/CAD pair will broadly move between 1.26-1.29.”

CNBC reports that according to one market observer, China announced new anti-monopoly rules over the weekend, but that’s not likely to have much impact on the market for now.

“The new regulation is still, you know, slightly sketchy in details,” Hao Hong, managing director and head of research at Bank of Communications International, told CNBC.

China’s State Administration for Market Regulation (SAMR) has tightened restrictions on China’s internet giants such as Alibaba and Meituan, and introduced new guidelines on Sunday to curb monopolistic behavior. The new rules formalize a draft that was released months earlier.

Hong said the market needs time to digest the details of the latest anti-monopoly guidelines, adding that China’s internet giants have been operating for years and already have “very solid” market positions.

“The regulation, you know, is starting with a very good intention,” Hong said. “The actual fact is that ... the market position ... of these big internet platforms are very difficult to encroach for now.”

FXStreet reports that economists at the National Bank of Canada see the EUR/USD pair trading in a range of 1.23-1.25 in the second half of the year.

“The latest report on 12-month headline inflation in the Eurozone showed it at 0.9%, up significantly from the -0.3% of December. Although likely to be transitory, this spike could alleviate concern about deflationary pressure coming from the exchange rate. The euro is likely to be weaker in the first quarter of the year given weakening of the global economy (broad-based USD increase) and statements made by central bankers.”

“All in all, we see the euro trading in a range of 1.23-1.25 in the second half of the year. This forecast assumes no further ECB rate cuts.”

According to the report from the Sentix, the overall economic index for Euroland falls by -1.5 points in February to an index level of -0.2 points. The lockdowns in many European countries are leaving their mark. For Euroland, the assessment of the current situation falls by 1.0 points, while the expectations component drops by 2.0 points. A similar trend can be observed for the assessment of the German economy. In the international context, the euro zone is thus lagging well behind the global growth trend. Most recently, the recovery relied heavily on a successful vaccination campaign. The EU order debacle and the resulting slower pace of vaccination are weighing on the mind and exposing the bureaucratic deficits in Euroland. As a result, the EU economy is losing touch with the other regions of the world, which are continuing their recovery course in the month of February.

Economic expectations for the euro zone have been strongly advanced for many months. It is therefore important that the development of the real economy (assessment of the current situation) does not disappoint these hopes and delivers them in the foreseeable future. The "time" factor is thus crucial and cannot be stretched at will. A permanent prolongation of the lockdown could become a problem because the difference between expectation and the current situation (the so-called expectation gap) is extremely high! There is a potential for a temporary disillusionment here. Fatal would be in any case a repeated demolition of the expectation component. The consequence would be a renewed recession.

RTTNews reports that the statistical office INE said that Spain's industrial production declined at a slower pace in December.

Industrial production declined by adjusted 0.6 percent on year, following a 3.7 percent drop seen in November. Production has dropped over the last twelve months.

On an unadjusted basis, industrial output grew 2.9 percent annually, reversing a 2.1 percent fall in the previous month.

Month-on-month, industrial production advanced 1.1 percent in December, offsetting a 0.9 percent drop seen in November.

In the whole year of 2020, industrial production was down by adjusted 9.4 percent from the previous year.

FXStreet reports that economists at the National Bank of Canada discuss USD/CAD prospects.

“CAD weakness is likely to be transient. GDP might disappoint in the coming months as a result of recent government-ordered shutdowns and short-term disruption of vaccine availability. However, it is important to note that the Canadian economy has not been hit harder than other economies by the pandemic and that programs to encourage people to stay in the workforce have so far worked reasonably well. We find it hard to justify the Bank’s current pace of quantitative easing. The BoC’s QE program is much more aggressive as a share of GDP than that of the Federal Reserve. Concern for financial stability would argue for QE tapering in the coming months (April or May), provided of course that the global economy continues to recover. Such a move would provide some support for an appreciation of the CAD.”

Reuters reports that a Cabinet Office survey showed that Japan's service sector sentiment index worsened for a third straight month in January, hitting its lowest since last May after a state of emergency was reimposed in Tokyo areas and some other prefectures.

The survey of workers such as taxi drivers, hotel workers and restaurant staff showed their confidence about current economic conditions declined 3.1 points from December to 31.2.

It was the lowest level since the index hit 17.0 in May 2020, when the economy was reeling from the first wave of the pandemic and suffered its worst post-war slump.

Re-assessing the economy based on the survey's findings, the government said the economy was now weakening, downgrading its view for a third straight month.

The service sector sentiment outlook index, which indicates the level of confidence in future conditions, rose 3.8 points to 39.9 in January, up for a second straight month.

| Time | Country | Event | Period | Previous value | Forecast | Actual |

|---|---|---|---|---|---|---|

| 05:00 | Japan | Eco Watchers Survey: Current | January | 34.3 | 31.2 | |

| 05:00 | Japan | Eco Watchers Survey: Outlook | January | 36.1 | 39.9 | |

| 06:45 | Switzerland | Unemployment Rate (non s.a.) | January | 3.5% | 3.7% | |

| 07:00 | Germany | Industrial Production s.a. (MoM) | December | 1.5% | 0.3% | 0% |

During today's Asian trading, the US dollar consolidated against global currencies, despite the rise in US bond yields.

US Treasury Secretary Janet Yellen said on Sunday that the US economy could return to full employment by the end of 2022 if the stimulus package proposed by President Joe Biden is adopted. "There is absolutely no reason why the economic recovery should be long and slow," Yellen said.

The yield on ten-year US Treasury bonds rose to 1.188% per annum, compared with 1.169% at the market close on Friday. An increase in interest rates on US Treasury bonds traditionally supports the dollar - the higher the rates, the more attractive the US currency is for buyers.

The focus of traders this week is on US inflation data for January, which will be released by the Labor Department on Wednesday. Inflation in the country is expected to have increased to 1.5% year-on-year from 1.4% in December.

The ICE Dollar index, which shows the value of the US dollar against the six major world currencies, fell 0.02% to 91.02

FXStreet reports that economists at Rabobank stick to their forecast of 0.76-0.77 on AUD/USD in the coming months

“We maintain our view that RBA policy combined with concerns about trade tensions with China will keep a lid on AUD/USD. We retain our forecast that a 0.76-0.77 trade range may contain most activity in the coming months.”

“The policy measures taken by the RBA this month may have wrong-footed AUD bulls. However, the outlook for AUD/USD will also be determined by other factors. These include China/Australia trade tension, which we expect will weigh moderately on the AUD this year and on the relative pace of reflation in the US and Australia economies.”

“The RBA is forecasting that the economy should regain its end-2019 size by the middle of this year with 2021 and 2022 GDP growth projections both at a buoyant 3.5%. This outlook suggests scope for the RBA to pull back from its extraordinary policy measures ahead of the Fed, a move which could push AUD/USD higher. However, there are various caveats to this view.”

“The RBA has made it clear that it will not increase the cash rate until actual inflation is ‘sustainably within the 2 to 3 percent target range’ and it specifies that this will require wage inflation to push ‘materially higher’. The implication is that rates in Australia are set to remain low for a long time.”

RTTNews reports that Fitch Ratings maintained the sovereign ratings of Japan with a 'negative' outlook.

The ratings were retained at 'A' citing the strengths of an advanced and wealthy economy, with correspondingly robust governance standards and public institutions.

Fitch affirmed a 'negative' outlook on Japan's ratings, given continued downside risks to the macroeconomic and fiscal outlook from the coronavirus shock.

After a 5.3 percent fall in 2020, Fitch forecast the economy to rebound by 3.5 percent in 2021 and 1.5 percent in 2022, supported by continued overseas demand for Japanese exports, which have recovered over recent months.

Fitch estimated government debt to have jumped to 254.8 percent of GDP in 2020 from 231.2 percent in 2019, the highest pre-pandemic debt ratio among Fitch-rated sovereigns. The debt is forecast to peak at 258.6 percent in 2023.

According to the report from the Federal Statistical Office (Destatis), in December 2020, production in industry remained unchanged on the previous month on a price, seasonally and calendar adjusted basis. Economists had expected a 0.3% increase. Compared with December 2019, the decrease in calendar adjusted production in industry amounted to 1.0%.

Compared with February 2020, the month before restrictions were imposed due to the coronavirus pandemic in Germany, production in December 2020 was 3.6% lower in seasonally and calendar adjusted terms. In 2020, production in industry was 8.5% lower in calendar adjusted terms than in the previous year.

In December 2020, production in industry excluding energy and construction was up by 0.9%. Within industry, the production of intermediate goods showed an increase of 2.0% and the production of consumer goods of 2.6%. The production of capital goods decreased by 0.5%. Outside industry, energy production was down by 2.9% in December 2020, while production in construction was up by 3.2%.

In November 2020, the corrected figure on the production in industry showed an increase of 1.5% (provisional: +0.9%) on October 2020.

EUR/USD

Resistance levels (open interest**, contracts)

$1.2224 (2530)

$1.2153 (5242)

$1.2104 (818)

Price at time of writing this review: $1.2039

Support levels (open interest**, contracts):

$1.1999 (2173)

$1.1949 (3839)

$1.1877 (2948)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date March, 5 is 78860 contracts (according to data from February, 5) with the maximum number of contracts with strike price $1,2100 (5242);

GBP/USD

Resistance levels (open interest**, contracts)

$1.3841 (991)

$1.3817 (534)

$1.3782 (476)

Price at time of writing this review: $1.3730

Support levels (open interest**, contracts):

$1.3582 (920)

$1.3548 (351)

$1.3510 (957)

Comments:

- Overall open interest on the CALL options with the expiration date March, 5 is 16082 contracts, with the maximum number of contracts with strike price $1,4200 (3191);

- Overall open interest on the PUT options with the expiration date March, 5 is 12494 contracts, with the maximum number of contracts with strike price $1,3100 (1224);

- The ratio of PUT/CALL was 0.78 versus 1.95 from the previous trading day according to data from February, 5

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

| Time | Country | Event | Period | Previous value | Forecast |

|---|---|---|---|---|---|

| 05:00 (GMT) | Japan | Eco Watchers Survey: Current | January | 35.5 | |

| 05:00 (GMT) | Japan | Eco Watchers Survey: Outlook | January | 37.1 | |

| 06:45 (GMT) | Switzerland | Unemployment Rate (non s.a.) | January | 3.5% | |

| 07:00 (GMT) | Germany | Industrial Production s.a. (MoM) | December | 0.9% | |

| 09:30 (GMT) | Eurozone | Sentix Investor Confidence | February | 1.3 | |

| 16:15 (GMT) | Eurozone | ECB President Lagarde Speaks | |||

| 23:30 (GMT) | Japan | Labor Cash Earnings, YoY | December | -2.2% |

| Pare | Closed | Change, % |

|---|---|---|

| AUDUSD | 0.76704 | 0.95 |

| EURJPY | 126.944 | 0.59 |

| EURUSD | 1.20452 | 0.69 |

| GBPJPY | 144.733 | 0.41 |

| GBPUSD | 1.37335 | 0.53 |

| NZDUSD | 0.7203 | 0.71 |

| USDCAD | 1.27641 | -0.43 |

| USDCHF | 0.89917 | -0.54 |

| USDJPY | 105.385 | -0.09 |

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers