- Analytics

- News and Tools

- Market News

Analytics, News, and Forecasts for CFD Markets: currency news — 20-03-2024.

- AUD up 0.83% vs. USD after Fed holds policy steady.

- Wall Street up, praises US economy, labor strength post-Fed.

- US 10-year yield dips, Dollar Index down, hints AUD/USD rise.

- Mixed Australia PMI, strong job outlook may sway RBA policy.

The Australian Dollar soared 0.83% against the US Dollar on Wednesday as the Federal Reserve held rates steady while maintaining their monetary policy outlook from last year, with 75 basis points (bps) of rate cuts in 2024. As the Asian session begins, the pair trades at 0.6595, up 0.14%.

Aussie Dolar gains momentum amid the beginning of Asia session

Wall Street ended the session on a higher note following the Fed’s decision. The US central bank kept the Federal Funds rate (FFR) at 5.25%- 5.50% and stated that the economy and the jobs market are robust. The disinflation process had evolved, but the last two readings of the CPI and PPI justified the Fed’s rhetoric of being patient. Despite that, Fed officials stick to their three rate cuts in 2024.

Following the data, the US 10-year Treasury note yield fell one and a half basis points to 4.277%, while the Greenback got battered. The US Dollar Index (DXY), a gauge of the buck’s value against other currencies, tumbles 0.42% and sits at 103.38, aiming below the 200-day moving average (DMA), a key dynamic support level, that depicts a financial markets asset as bullish or bearish.

On the Aussies' front, the schedule featured the release of Judo Bank Flash PMI figures for March. The manufacturing PMI dipped from 47.8 to 46.8, while the Services PMI rose from 53.1 to 53.5. The Composite Index came at 52.4, up from 52.1.

AUD/USD traders’ eye further data from Australia, with the jobs market expected to add 40,000 people to the workforce. That would lower the unemployment rate, from 4.1% to 4%. A strong reading could suggest the Reserve Bank of Australia (RBA) should stick to its current stance and shrug off speculations of the first-rate cut in August.

AUD/USD Price Analysis: Technical outlook

From a technical perspective, the AUD/USD printed a leg-up, clearing key resistance levels and poised to breach the 0.6600 figure. The Relative Strength Index (RSI) confirms that statement, as it aims higher in bullish territory, with the pair closing at weekly highs, snapping four days of losses. The next supply zone would be the psychological 0.6650 mark, followed by the March 8 high at 0.6667. Once cleared, that would expose 0.6700.

Australia's Judo Bank Purchasing Managers Index (PMI) came in mixed in the early Thursday market session, with a lift in the Services component mixing with an easing in the Manufacturing PMI.

Judo Bank's March Manufacturing PMI ticked down to 46.8 after the previous month's 47.8, while the Services component rose to 53.5 from the previous 53.1. The Composite March Judo Bank PMI rose to 52.4 from 52.1.

According to Warren Hogan, Chief Economic Advisor at Judo Bank: "Over the survey's nine-year history, this is the largest four-month increase in the Composite Output index outside of the two recovery periods when the economy was locked down during the pandemic."

Warren added, "The underlying details of the survey highlight that the improvement in business performance in 2024 is not even across the economy. Manufacturing activity remains soft in early 2024, with the Australian Manufacturing PMI down to a new cyclical low point well below 50.0".

Warren also noted that underlying details about Australia's manufacturing sector may be irrelevant to the country's overall economic outlook, as manufacturing accounts for less than 10% of Australia's economy.

Market reaction

AUD/USD stepped into a fresh near-term high as markets head into the Thursday market session, with the pair approaching 0.6600 following a Fed-fueled rally from Wednesday's early lows near 0.6510.

AUD/USD 5-minute chart

About Australia's Judo Bank Composite PMI

The Composite Purchasing Managers Index (PMI), released on a monthly basis by Judo Bank and S&P Global, is a leading indicator gauging private-business activity in Australia for both the manufacturing and services sectors. The data is derived from surveys to senior executives. Each response is weighted according to the size of the company and its contribution to total manufacturing or services output accounted for by the sub-sector to which that company belongs. Survey responses reflect the change, if any, in the current month compared to the previous month and can anticipate changing trends in official data series such as Gross Domestic Product (GDP), industrial production, employment and inflation. The index varies between 0 and 100, with levels of 50.0 signaling no change over the previous month. A reading above 50 indicates that the Australian private economy is generally expanding, a bullish sign for the Australian Dollar (AUD). Meanwhile, a reading below 50 signals that activity is generally declining, which is seen as bearish for AUD.

- NZD/USD gains ground around 0.6090 on the weaker USD.

- New Zealand's GDP for Q4 came in at -0.1% QoQ vs. -0.3% prior, weaker than expected.

- The Fed held interest rates steady at its March meeting on Wednesday, as widely expected.

- The US S&P Global PMI for March will be due on Thursday.

The NZD/USD pair trades on a stronger note below the 0.6100 mark during the early Asian session on Thursday. The decline of the US Dollar (USD) after the Federal Reserve (Fed) left its interest rates unchanged and Fed Chair Jerome Powell delivered a dovish message to provide some support to the pair. NZD/USD currently trades around 0.6090, gaining 0.15% on the day.

The latest data from Statistics New Zealand on Thursday showed that the nation’s GDP growth number contracted 0.1% QoQ in the fourth quarter from the previous reading of 0.3% contraction. The Annualized GDP for Q4 shrank 0.3% YoY from the 0.6% contraction in the previous reading. Both figures came in worse than market expectations, which might cap the upside of the New Zealand Dollar (NZD).

On the other hand, the Fed held the rate steady at 5.25–5.50% at its March meeting on Wednesday, with the median dot plot for 2024 unchanged from the 75 basis points (bps) of cuts shown in the December projections. During the press conference, Fed Chair Jerome Powell stated that a strong labour market Data wouldn’t deter the central bank from cutting rates. Powell emphasized that the central bank will wait for more data that inflation is sustainably moderating toward its 2% target.

Furthermore, Fed’s Powell reiterated that policymakers still intend to cut rates before the end of this year, given economic growth continues. The dovish comments from Powell exert some selling pressure on the Greenback and create a tailwind for NZD/USD.

Looking ahead, traders will keep an eye on the preliminary US S&P Global Purchasing Managers Index (PMI) for March, the weekly Initial Jobless Claims and Existing Home Sales. On Friday, New Zealand’s Trade Balance will be released.

New Zealand's Gross Domestic Product (GDP) contracted another -0.1% in the fourth quarter, recovering from the previous quarter's -0.3% but missing the median market forecast of an increase of 0.1%.

Annualized YoY GDP in Q4 also missed the mark, coming in at -0.3%. Annualized quarterly GDP bounced from the previous print of -0.6%, but failed to hit the market's forecast 0.1%.

According to national accounts industry and production senior manager Ruvani Ratnayake, "Wholesale trade was the largest downwards driver this quarter, led by falls in grocery and liquor wholesaling; and machinery and equipment wholesaling."

Ruvani Ratnayake continued, "Increased activity associated with the NZ General Election contributed to growth in public administration, safety, and defence."

Market reaction

The NZD/USD pair saw a quick drop when the GDP print missed the mark, declining into 0.6055 in early Thursday trading. The pair initially rallied on Wednesday after the Fed held rates but tilted its head at future rate cuts, driving Kiwi to an intraday high of 0.6085.

About New Zealand's quarterly GDP

The Gross Domestic Product (GDP), released by Statistics New Zealand, highlights the overall economic performance on a quarterly basis. The gauge has a significant influence on the Reserve Bank of New Zealand’s (RBNZ) monetary policy decision, in turn affecting the New Zealand dollar. A rise in the GDP rate signifies improvement in the economic conditions, which calls for tighter monetary policy, while a drop suggests deterioration in the activity. An above-forecast GDP reading is seen as NZD bullish.

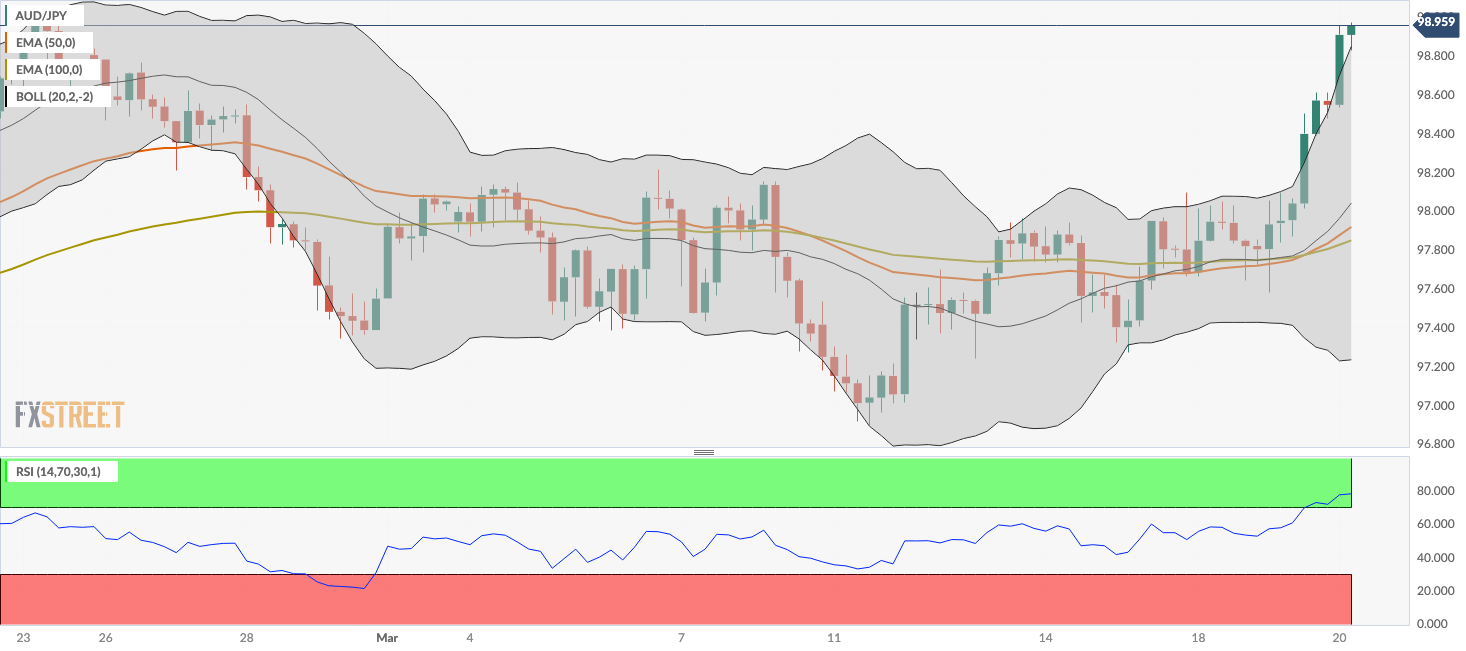

- The daily chart analysis reveals consistent bullish sentiment with RSI nearing overbought conditions, indicating possible pullbacks.

- The AUD/JPY hourly chart paints a similar picture, with the RSI deep in overbought terrain.

- Even with a potential short-term bearish correction, the AUD/JPY standing above SMA shows an overall bullish trend.

In Wednesday's session, AUD/JPY is experiencing an uptake, trading at 99.62, its highest level since 2014, and showing a gain of 1.15%. Although there are hints of a short-term consolidation incoming, any downward movements could be considered as a mere technical correction.

Based on the indicators of the daily chart for the AUD/JPY pair, a positive trend is seen, as indicated by the positive territory of the Relative Strength Index (RSI). The RSI is nearing the overbought territory, signaling that while the trend is bullish, an increasing risk of a pullback due to overbought conditions is also present. In agreement with this, the Moving Average Convergence Divergence (MACD) histogram also reveals a rising trend, indicated by green bars, corroborating the positive momentum.

AUD/JPY daily chart

Contrarily, on the hourly chart, the AUD/JPY pair shows a sharp move into the overbought territory, as indicated by the RSI of 78. This demonstrates that the pair might face a corrective pullback in the short term given these extreme over-extended conditions. The MACD histogram also confirms this, as it continues to print green bars.

AUD/JPY hourly chart

These observations generally point towards bullish conditions for the AUD/JPY pair in the short term but buyers might consider taking profits in the next sessions. On a broader perspective, buyers are also in command as the pair trades above the 20,100 and 200-day Simple Moving Averages (SMAs).

- The Australian Unemployment Rate is expected to have eased to 4% in February.

- Employment Change is foreseen to bounce after January's disappointing 0.5K increase.

- AUD/USD turned marginally bullish near-term following the Federal Reserve’s decision.

Australia is scheduled to release the February monthly employment report on Thursday, following the Reserve Bank of Australia (RBA) monetary policy decision on Tuesday. The Australian Bureau of Statistics (ABS) is expected to announce that the economy added 40K new job positions in February, while the seasonally adjusted Unemployment Rate is foreseen at 4%, easing from 4.1% in January. The Australian Dollar (AUD) heads into the event with a weak tone, trading against the US Dollar at around 0.6570.

Australian Employment Change is divided into full-time and part-time positions. Full-time jobs imply working 38 hours per week or more and usually include additional benefits, but they mostly represent consistent income. On the other hand, part-time employment generally means higher hourly rates but lacks consistency and benefits. That’s why the economy prefers full-time jobs.

In January, the economy shed 10,600 part-time roles and added 11,100 full-time, leaving a measly headline net gain of around 500 jobs for the month.

Meanwhile, the Reserve Bank of Australia (RBA) announced its monetary policy decision on Tuesday. As widely anticipated, the RBA kept the Cash Rate at 4.75% for the third consecutive meeting. Policymakers acknowledged inflation is moderating but added the economic outlook remains uncertain. The decision fell short of impressive and came out alongside the Bank of Japan's (BoJ) decision to drop its ultra-loose monetary policy, hiking rates for the first time in seventeen years. As a result, the US Dollar soared across the board, pushing AUD/USD to a two-week low of 0.6503.

Australian unemployment rate likely to have declined in February

As said, the Unemployment Rate is foreseen at 4% in February, easing from the previous 4.1%, although still higher than the 2023 low of 3.5%. RBA Governor Michele Bullock noted in the press conference following the monetary policy announcement that “The judgement at the moment is the labour market still is slightly on the tight side,” based on the fact that the Unemployment Rate is still lower than it was before the Coronovirus pandemic. Back then, the Unemployment Rate averaged 5% for nearly a decade.

It is worth remembering that the RBA mandate is “to contribute to the stability of the currency, full employment, and the economic prosperity and welfare of the Australian people,” according to the central bank’s own definition. Hence, a bounce in employment stands in the way of rate cuts.

The Australian economy has cooled more than enough with recent interest-rate hikes, and a recession is not out of the picture. In fact, economists believe the November hike accelerated the slowdown and may have been excessive. If unemployment continues to rise, the RBA would be forced into early rate cuts.

That said, a lower-than-anticipated Unemployment Rate will allow Australian policymakers to maintain rates higher for longer, which, conversely, will mean higher risks for an economic setback.

Wage growth in the country is reported separately. The Australian ABS releases the Wage Price Index quarterly, which “measures changes in the price of labour, unaffected by compositional shifts in the labour force, hours worked or employee characteristics.”

The latest report shows that the Wage Price Index rose 0.9% for the three months to December and 4.2% over the year. That was the first time in three years that wage growth outstripped inflation and the highest annual increase since early 2009. Wage increases pose a risk to inflation.

The RBA is on a narrow path, as former Governor Philip Lowe used to say, and may be forced into quick, unexpected monetary decisions in the months to come. A higher-than-anticipated Unemployment Rate may not bother Australian policymakers, but it could indeed take its toll on the Aussie.

When will the Australian employment report be released and how could it affect AUD/USD?

The ABS will publish the February employment report on Thursday at 00:30 GMT. As previously stated, Australia is expected to have created 40K new jobs in the month, while the Unemployment Rate is foreseen at 4%. The Participation Rate is foreseen unchanged at 66.8%.

Ahead of the release of Australian employment figures, the United States (US) Federal Reserve (Fed) announced that it left the benchmark rate unchanged at 5.25%-5.5%, as widely anticipated. As a result, the US Dollar entered a selling spiral that pushed AUD/USD higher.

The Fed also unveiled the Summary of Economic Projections (SEP) or dot plot, which showed that policymakers still aim to cut rates three times this year, more than the suspected two. Additionally, the central bank upwardly revised its growth and inflation forecast, while unemployment is foreseen to ease. Chairman Jerome Powell held a press conference and hinted that the central bank is in no rush to cut rates. The economy is growing, inflation is still high, and the labour market is tight.

From a technical perspective, Valeria Bednarik, Chief Analyst at FXStreet, notes: “The AUD/USD pair trimmed its weekly losses and moved further away from the 2024 low at 0.6442. Still, as seen in the weekly chart, the wider perspective indicates that the pair has room to break lower and test buyers’ determination at around 0.6400, particularly if the Aussie pair turns south with employment figures.”

Bednarik adds: “On a daily basis, AUD/USD is turning bullish. The pair develops between directionless moving averages, while the Relative Strength Index (RSI) indicator turns marginally higher but remains at negative levels. The Momentum indicator lacks directional strength, advancing modestly just above the 100 level, in line with recent price action, but still not enough to confirm a bullish continuation.”

Finally, she notes: “The pair has retreated sharply after reaching the 50% Fibonacci retracement of the 0.6871-0.6442 slide at 0.6656 but has recovered above the 23.6% retracement of the aforementioned slide at 0.6543. The pair can now extend its advance towards the 0.6600-0.6610 area, while once above the latter, the pair could reach the mentioned Fibonacci retracement at 0.6656.”

Australian Dollar FAQs

One of the most significant factors for the Australian Dollar (AUD) is the level of interest rates set by the Reserve Bank of Australia (RBA). Because Australia is a resource-rich country another key driver is the price of its biggest export, Iron Ore. The health of the Chinese economy, its largest trading partner, is a factor, as well as inflation in Australia, its growth rate and Trade Balance. Market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – is also a factor, with risk-on positive for AUD.

The Reserve Bank of Australia (RBA) influences the Australian Dollar (AUD) by setting the level of interest rates that Australian banks can lend to each other. This influences the level of interest rates in the economy as a whole. The main goal of the RBA is to maintain a stable inflation rate of 2-3% by adjusting interest rates up or down. Relatively high interest rates compared to other major central banks support the AUD, and the opposite for relatively low. The RBA can also use quantitative easing and tightening to influence credit conditions, with the former AUD-negative and the latter AUD-positive.

China is Australia’s largest trading partner so the health of the Chinese economy is a major influence on the value of the Australian Dollar (AUD). When the Chinese economy is doing well it purchases more raw materials, goods and services from Australia, lifting demand for the AUD, and pushing up its value. The opposite is the case when the Chinese economy is not growing as fast as expected. Positive or negative surprises in Chinese growth data, therefore, often have a direct impact on the Australian Dollar and its pairs.

Iron Ore is Australia’s largest export, accounting for $118 billion a year according to data from 2021, with China as its primary destination. The price of Iron Ore, therefore, can be a driver of the Australian Dollar. Generally, if the price of Iron Ore rises, AUD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Iron Ore falls. Higher Iron Ore prices also tend to result in a greater likelihood of a positive Trade Balance for Australia, which is also positive of the AUD.

The Trade Balance, which is the difference between what a country earns from its exports versus what it pays for its imports, is another factor that can influence the value of the Australian Dollar. If Australia produces highly sought after exports, then its currency will gain in value purely from the surplus demand created from foreign buyers seeking to purchase its exports versus what it spends to purchase imports. Therefore, a positive net Trade Balance strengthens the AUD, with the opposite effect if the Trade Balance is negative.

Economic Indicator

Australia Unemployment Rate s.a.

The Unemployment Rate, released by the Australian Bureau of Statistics, is the number of unemployed workers divided by the total civilian labor force, expressed as a percentage. If the rate increases, it indicates a lack of expansion within the Australian labor market and a weakness within the Australian economy. A decrease in the figure is seen as bullish for the Australian Dollar (AUD), while an increase is seen as bearish.

Read more.Why it matters to traders

The Australian Bureau of Statistics (ABS) publishes an overview of trends in the Australian labour market, with unemployment rate a closely watched indicator. It is released about 15 days after the month end and throws light on the overall economic conditions, as it is highly correlated to consumer spending and inflation. Despite the lagging nature of the indicator, it affects the Reserve Bank of Australia’s (RBA) interest rate decisions, in turn, moving the Australian dollar. Upbeat figure tends to be AUD positive.

The Greenback halted its ongoing recovery and retreated markedly after the Fed left its interest rates unchanged and Powell delivered a dovish message, all morphing into extra oxygen for the risk-linked galaxy.

Here is what you need to know on Thursday, March 21:

The USD Index (DXY) plummeted to the low-103.00s after advancing well north of the 104.00 barrier earlier in the session. A busy US calendar on March 21 shows the usual weekly Initial Jobless Claims along with the Philly Fed Manufacturing Index and advanced S&P Global Manufacturing and Services PMIs. In addition, the CB Leading Index is also due followed by Existing Home Sales and the speech by FOMC M. Barr.

EUR/USD managed to advance to multi-day peaks past 1.0900 the figure in response to the Dollar’s pullback. On March 21, flash HCOB Manufacturing and Services PMIs are due.

GBP/USD advanced further and traded at shouting distance from the key 1.2800 milestone, underpinned by the weaker Greenback. In the UK, the BoE meets along with the release of preliminary S&P Global Manufacturing and Services PMIs.

USD/JPY rose to levels last seen in mid-November around 151.80 as investors continued to assess the latest BoJ gathering. Data-wise, In Japan, the Reuters Tankan Index and Balance of Trade results are due on March 21.

AUD/USD picked up renewed traction and reversed four consecutive daily declines ahead of key releases on Thursday. In the Australian calendar, the advanced Judo Bank Manufacturing and Services PMIs are scheduled for March 21 along with the labour market report and the RBA’s Consumer Inflation Expectations.

WTI prices retreated from recent tops and broke below the $81.00 mark per barrel despite persevering supply concerns and the sell-off in the greenback.

Gold prices rose sharply and revisited the $2,180 region per troy ounce following lower US yields and the collapse in the Dollar. Silver advanced strongly and tested an area last seen in early December around $25.60 per ounce.

- Silver prices surge nearly 3%, buoyed by the Federal Reserve's decision to maintain current interest rates.

- US Dollar Index declines, supporting silver's upward momentum as investors digest the Fed's dovish stance.

- Technical indicators suggest potential for further gains, with XAG/USD traders targeting the $26.00 resistance level.

- Downside risks include a retracement towards the $25.00 support, and below.

Silver prices climbed on Wednesday after the US central bank, the Federal Reserve, held rates unchanged, delivering a “dovish” hold. Consequently, US Treasury yields edged down, and the Greenback remained pressured, as shown by the US Dollar Index (DXY), down 0.37% at 103.44. Therefore, XAG/USD trades at $25.61, up close to 3%.

XAG/USD Price Analysis: Technical outlook

Silver rallied sharply above the $25.50 rea, hitting a daily high at $25.63. A further upside is seen above that area, with grey metal traders eyeing $26.00 a troy ounce as the next key resistance level. Once those two levels are taken out, the next supply zone would be the April 18, 2022, high at $26.21, followed by the March 8, 2022, high at $26.94.

If sellers move in and drag prices below March 15’s high of $25.43, look for a drop toward $25.00. Once cleared, the next stop would be the December 22 high turned support at $24.60, followed by the $24.00 mark.

XAG/USD Price Action – Daily Chart

Federal Reserve Chairman Jerome Powell explains the decision to leave the policy rate, federal funds rate, unchanged at the range of 5.25-5.5% and responds to questions in the post-meeting press conference.

Key quotes

"We are looking at incoming inflation data most importantly."

"That's where we are looking for more confidence."

"We will also be looking at other data in the economy but most important thing will be the inflation data."

"Wage increases are gradually coming down to levels more sustainable over time."

"High inflation was not caused mostly by wages; that said we need to see more gradual movement downwards on wage inflation."

"We need to be careful on when we start to cut rates."

About Jerome Powell (via Federalreserve.gov)

"Jerome H. Powell first took office as Chair of the Board of Governors of the Federal Reserve System on February 5, 2018, for a four-year term. He was reappointed to the office and sworn in for a second four-year term on May 23, 2022. Mr. Powell also serves as Chairman of the Federal Open Market Committee, the System's principal monetary policymaking body. Mr. Powell has served as a member of the Board of Governors since taking office on May 25, 2012, to fill an unexpired term. He was reappointed to the Board and sworn in on June 16, 2014, for a term ending January 31, 2028."

Federal Reserve Chairman Jerome Powell explains the decision to leave the policy rate, federal funds rate, unchanged at the range of 5.25-5.5% and responds to questions in the post-meeting press conference.

Key quotes

"We are seeing a strong labor market, extreme imbalances mostly resolved."

"Wage growth is gradually moderating."

"Things are returning more to the pre-pandemic state."

"Labor market is in good shape."

"We are closely watching layoffs."

"Initial claims are very very low."

"Fed is discussing slowing pace of runoff."

"In terms of timing, no more specific than fairly soon."

"Liquidity is not evenly distributed."

"We might be able to get to a lower level of reserves this time."

"We are looking at what would be best pace and best structure."

"Our longer run goal is to return to balance sheet that is mostly treasuries."

"It is not urgent to make changes to that right now, though; that is an issue further down the line."

"We are going to pay a lot of attention to past mistakes on balance sheet runoff."

"we have a better sense now on indicators we need to look at."

"By going slower on balance sheet, we think we can get further."

"It will mean we run much less risk on liquidity issues."

"We will be monitoring money market conditions carefully to know when to stop on balance sheet runoff."

"There isn't a dollar of % of GDP amount that we have in mind; we will look at indicators to tell us when we are close."

"We want to have a buffer on reserves. We don't want to find ourselves in the 2019 situation again."

About Jerome Powell (via Federalreserve.gov)

"Jerome H. Powell first took office as Chair of the Board of Governors of the Federal Reserve System on February 5, 2018, for a four-year term. He was reappointed to the office and sworn in for a second four-year term on May 23, 2022. Mr. Powell also serves as Chairman of the Federal Open Market Committee, the System's principal monetary policymaking body. Mr. Powell has served as a member of the Board of Governors since taking office on May 25, 2012, to fill an unexpired term. He was reappointed to the Board and sworn in on June 16, 2014, for a term ending January 31, 2028."

Federal Reserve Chairman Jerome Powell explains the decision to leave the policy rate, federal funds rate, unchanged at the range of 5.25-5.5% and responds to questions in the post-meeting press conference.

Key quotes

"We tend to see a little bit stronger inflation in first half of the year."

"We don't know if this is a bump on inflation road or something more."

"Latest inflation data certainly hasn't improved anyone's confidence."

"Recent inflation data hasn't altered story of inflation coming down to 2% on a sometimes bumpy path."

"We need to take time to assess if recent inflation represents more than bumps in the road."

"It is very important that we do get inflation sustainably down."

"I don't see cracks in the labor market."

About Jerome Powell (via Federalreserve.gov)

"Jerome H. Powell first took office as Chair of the Board of Governors of the Federal Reserve System on February 5, 2018, for a four-year term. He was reappointed to the office and sworn in for a second four-year term on May 23, 2022. Mr. Powell also serves as Chairman of the Federal Open Market Committee, the System's principal monetary policymaking body. Mr. Powell has served as a member of the Board of Governors since taking office on May 25, 2012, to fill an unexpired term. He was reappointed to the Board and sworn in on June 16, 2014, for a term ending January 31, 2028."

Federal Reserve Chairman Jerome Powell explains the decision to leave the policy rate, federal funds rate, unchanged at the range of 5.25-5.5% and responds to questions in the post-meeting press conference.

Key quotes

"If we are getting a lot of supply and demand, you could potentially have a bigger economy where inflation pressures are not increasing."

"Strong hiring all by itself would not be a reason to hold off on rate cuts."

"Strong job growth is not a reason for us to be concerned about inflation."

"Ultimately, we do think financial conditions are weighing on economic activity."

About Jerome Powell (via Federalreserve.gov)

"Jerome H. Powell first took office as Chair of the Board of Governors of the Federal Reserve System on February 5, 2018, for a four-year term. He was reappointed to the office and sworn in for a second four-year term on May 23, 2022. Mr. Powell also serves as Chairman of the Federal Open Market Committee, the System's principal monetary policymaking body. Mr. Powell has served as a member of the Board of Governors since taking office on May 25, 2012, to fill an unexpired term. He was reappointed to the Board and sworn in on June 16, 2014, for a term ending January 31, 2028."

Federal Reserve Chairman Jerome Powell explains the decision to leave the policy rate, federal funds rate, unchanged at the range of 5.25-5.5% and responds to questions in the post-meeting press conference.

Key quotes

"We made no decisions about future meetings today; will depend on data."

"We want to see more data that gives us higher confidence on inflation moving down sustainably."

"If there were a significant weakening in labor market, that would be a reason to start rate cuts."

"I don't think we know if rates are going to be higher in the longer run."

"My instinct is rates won't go back down to very low levels we saw before."

"But there is tremendous uncertainty around that."

"It is still likely in most people's view that we will have rate cuts this year, but depends on data

About Jerome Powell (via Federalreserve.gov)

"Jerome H. Powell first took office as Chair of the Board of Governors of the Federal Reserve System on February 5, 2018, for a four-year term. He was reappointed to the office and sworn in for a second four-year term on May 23, 2022. Mr. Powell also serves as Chairman of the Federal Open Market Committee, the System's principal monetary policymaking body. Mr. Powell has served as a member of the Board of Governors since taking office on May 25, 2012, to fill an unexpired term. He was reappointed to the Board and sworn in on June 16, 2014, for a term ending January 31, 2028."

Federal Reserve Chairman Jerome Powell explains the decision to leave the policy rate, federal funds rate, unchanged at the range of 5.25-5.5% and responds to questions in the post-meeting press conference.

Key quotes

"Discussed balance sheet at this meeting."

"We discussed issues related to slowing pace of decline in holdings."

"Our general sense is we will start run off fairly soon."

"Slowing pace of runoff will ensure smooth transition, mitigating chance of money market stress."

"Will limit risk to money market volatility."

"Economy is performing well."

"Projections do not mean higher tolerance for inflation."

"Inflation data came in a little bit higher than expected. Nevertheless, we continue to make good progress on bringing inflation down."

"There's some confidence that lower market rent increases in housing will show up over time."

"I assume we will continue to see goods prices continue into a new equilibrium."

"The risks are really two-sided now."

"First rate cut is therefore consequential."

"We can approach that question carefully and let the data speak."

"January CPI and PCE numbers were quite high but could have been due to seasonal adjustments."

"January inflation numbers were quite high but reason to think there were seasonal affects there."

"February was also high, but not terribly."

"Taking January and February together have not changed the overall story."

"It will be a bumpy path."

"Those January and February inflation numbers did not add to our confidence."

"We are not going to overreact to these two months of data; nor ignore them."

About Jerome Powell (via Federalreserve.gov)

"Jerome H. Powell first took office as Chair of the Board of Governors of the Federal Reserve System on February 5, 2018, for a four-year term. He was reappointed to the office and sworn in for a second four-year term on May 23, 2022. Mr. Powell also serves as Chairman of the Federal Open Market Committee, the System's principal monetary policymaking body. Mr. Powell has served as a member of the Board of Governors since taking office on May 25, 2012, to fill an unexpired term. He was reappointed to the Board and sworn in on June 16, 2014, for a term ending January 31, 2028."

Federal Reserve Chairman Jerome Powell explains the decision to leave the policy rate, federal funds rate, unchanged at the range of 5.25-5.5% and responds to questions in the post-meeting press conference.

Key quotes

"Risks to goals coming into better balance."

"Our policy rate is likely at its peak."

Likely to cut rates at some point this year but outlook is uncertain and we remain attentive to risks."

"Prepared to keep rates high longer if needed."

"We will carefully assess incoming data to decide policy."

"Committed to both sides of dual mandate."

"We need greater confidence of inflation moving sustainably down before we cut rates."

"We will make decisions meeting by meeting."

"Unexpected weakness in labor market could warrant a response too."

"Our projections are not a plan, we will adjust based on conditions."

About Jerome Powell (via Federalreserve.gov)

"Jerome H. Powell first took office as Chair of the Board of Governors of the Federal Reserve System on February 5, 2018, for a four-year term. He was reappointed to the office and sworn in for a second four-year term on May 23, 2022. Mr. Powell also serves as Chairman of the Federal Open Market Committee, the System's principal monetary policymaking body. Mr. Powell has served as a member of the Board of Governors since taking office on May 25, 2012, to fill an unexpired term. He was reappointed to the Board and sworn in on June 16, 2014, for a term ending January 31, 2028."

Federal Reserve Chairman Jerome Powell explains the decision to leave the policy rate, federal funds rate, unchanged at the range of 5.25-5.5% and responds to questions in the post-meeting press conference.

Key quotes

"The economy has made considerable progress."

"Inflation has eased substantially."

"Ongoing progress is not assured, though."

"The path forward is uncertain."

"GDP has been bolstered by strong consumer demand as well as healing supply chains."

"High interest rates have weighed on business fixed income investment."

"Participants revised up GDP estimates."

"Labor market remains relatively tight but supply and demand coming into better balance."

"Nominal wage growth has been easing."

"Labor demand still exceeds labor supply."

"FOMC participants expect rebalancing in labor market to continue."

"Inflation remains above our goal."

"Longer-term inflation expectations remain well-anchored."

About Jerome Powell (via Federalreserve.gov)

"Jerome H. Powell first took office as Chair of the Board of Governors of the Federal Reserve System on February 5, 2018, for a four-year term. He was reappointed to the office and sworn in for a second four-year term on May 23, 2022. Mr. Powell also serves as Chairman of the Federal Open Market Committee, the System's principal monetary policymaking body. Mr. Powell has served as a member of the Board of Governors since taking office on May 25, 2012, to fill an unexpired term. He was reappointed to the Board and sworn in on June 16, 2014, for a term ending January 31, 2028."

- GBP/USD sees a significant uptick, navigating the 1.2700/1.2750 range following the Federal Reserve's rate decision.

- Fed holds interest rates steady, with an emphasis on the ongoing strength of the US economy and labor market.

- Despite high recent inflation, Fed's projections for 2024 remain stable; slight adjustment made for 2025 FFR outlook.

The GBP/USD climbed sharply after the Federal Reserve’s (Fed) decision to hold rates but kept their interest rate cut projections unchanged for 2024. Consequently, the Greenback tumbled, while US Treasury bond yields climbed. At the time of writing, the GBP/USD trades volatile in the 1.2700/1.2750 area ahead of Fed Chair Jerome Powell's press conference.

Summary of the Fed’s monetary policy statement

The US Federal Reserve has decided to keep interest rates steady at 5.25%-5.50% and continue reducing its balance sheet at an ongoing pace since May 2023. In their announcement, Federal Reserve officials highlighted the strength of the US economy and the robustness of the labor market. While progress on inflation has been acknowledged, they cautioned that the effort to stabilize prices is not yet finished. They noted an improved balance in the risks associated with achieving the Fed's dual mandate of maximum employment and stable prices, affirming their commitment to data-driven decision-making.

Following two consecutive months of unexpectedly high inflation data, the Federal Reserve adjusted its monetary policy outlook for 2025. Although the median forecast for 2024 remains unchanged at 4.6% from December's projection, the forecast for the Federal Funds Rate (FFR) for 2025 was revised upwards from 3.6% to 3.9%. Other economic indicators were also updated in their statement.

- The Gross Domestic Product (GDP) for 2024 was revised to 2.1%, up from 1.4% in December.

- The Unemployment Rate was revised downward, expected to fall to 4.0%, from 4.1%.

- The Personal Consumption Expenditure (PCE) Price Index target wasn’t changed, remaining at 2.4%, while core PCE is estimated to end 2024 at 2.6%, up from 2.4%.

Following the release of the data, the yield on the US 10-year Treasury note decreased by two basis points to 4.275%. Concurrently, the US Dollar is experiencing downward pressure.

GBP/USD Price Action – Hourly Chart

The GBP/USD surged towards a daily high of 1.2752, but since then, the pair has retreated towards the 100-moving average (SMA) at around 1.2725. As the Fed Chair Jerome Powell press conference looms, the major could re-test daily highs on dovish remarks, and that could expose the 1.2800 mark. A breach of the latter will expose the March 14 high of 1.2823, followed by the March 8 high at 1.2894. on the flip side, the pair could edge towards the 50-SMA at 1.2713, ahead of the 1.2700 mark. Further downside is seen at the March 19 low of 1.2667.

- USD/JPY took a quick plunge into 151.25 after Fed held rates.

- FOMC sees slightly higher rates in the future than previously expected.

- Markets shrug off higher growth forecast, price in additional easing.

USD/JPY took a quick dive into 151.25 after the Federal Reserve (Fed) held its main reference rate at 5.5% as markets had broadly predicted. Risk-hungry investors are shrugging off higher-than-previous growth expectations and interest rate forecasts from the Federal Open Market Committee (FOMC). According to the FOMC, US Gross Domestic Product (GDP) growth through 2024 is going to be slightly higher than forecast, and year-end interest rates are likely to be higher than previously expected.

Despite upside shifts to the Dot Plot, the Fed still expects three rate cuts through 2024 for around 75 basis points, and markets are keeping hopes of near-term rate trimming to begin closer to the middle of the year. Fed Chairman Jerome Powell is due at the bottom of the hour at 18:30 GMT.

Read more: Fed leaves interest rate unchanged at 5.25%-5.5% as forecast

USD/JPY 5-minute chart

- EUR/USD bumped towards 1.0900 after Fed held steady.

- Fed Dot Plot still sees 75 bps in 2024.

- Fed expects rates to be held higher by end of 2026.

EUR/USD jumped on reaction to the Federal Reserve’s (Fed) latest rate call, which held rates at 5.5% as markets had broadly predicted. Investor expectations are pricing in additional easing in 2024, despite the Federal Open Market Committee seeing stronger growth through 2024 and 2025 than initially expected. The FOMC’s Dot Plot of interest rate expectations also saw a rise in the long tail end of the curve, with end-2026 rates now forecast to land somewhere around 3.1% versus the previous 2.9%.

The Fed is now projecting a higher long-term policy rate through December, ticking up to 2.6% from 2.5%, but markets are shrugging off the Fed’s growth expectations to push down the US Dollar (USD), sending the Euro (EUR) higher. EUR/USD crossed 1.0890 following the market’s pre-baked reaction to the Fed’s rate call. Investors will now buckle down for the short wait to Fed Chairman Jerome Powell’s press conference slated for the bottom of the hour at 18:30 GMT.

Read more: Fed leaves interest rate unchanged at 5.25%-5.5% as forecast

EUR/USD 5-minute chart

- Gold is flatlined as investors await Federal Reserve's monetary policy announcement.

- US 10-year Treasury yield dip reflects market caution before Fed's interest rate decision and economic outlook.

- A potential upward adjustment in Fed's Dot Plot may hint at hawkish shift, a headwind for Gold’s price.

Gold price is virtually unchanged ahead of the US Federal Reserve’s monetary policy decision as traders remain on the sidelines. In addition to delivering the statement, Fed officials will update their economic projections, with investors eyeing a tweak to the Dot Plot, which could pave the way for a US Dollar comeback. The XAU/USD trades near $2,150.00, almost flat.

An hour before the Fed’s meeting, the US 10-year Treasury note yields 4.281%, down one basis point, as market participants remained uncertain. The US Dollar Index (DXY), a gauge of the buck’s value against a basket of six other currencies, rose 0.12% to 103.94, putting a lid on Bullion’s advance.

Financial market chatter suggests that if two Fed Dot Plot projections adjust to the upside in 2024, it would be perceived as a “hawkish tilt;” therefore, further XAU/USD downside is expected. On the other hand, there’s some speculation that policymakers could adjust their monetary policy expectations for 2025, suggesting the Federal Funds Rate (FFR) would be higher than December’s 3.6% estimate.

Daily digest market movers: Gold stays firm amid strong US Dollar

- The Federal Reserve’s Summary of Economic Projections in December showed that policymakers expected GDP in 2024 to be at 1.4% and the Unemployment Rate to be at 4.1%.

- Regarding inflation figures, the Core Personal Consumption Expenditure (PCE) Price Index, favored by Fed Chair Jerome Powell for tracking inflation, is predicted to fall to 2.4% in 2024, aligning with the general PCE forecast.

- December’s Dot Plot suggested that Fed officials were expecting the FFR to end at 4.6%, down from 5.1%. However, if the median moves to 4.8%, that would imply Powell and company are expecting two rate cuts for 2024.

- The latest US economic data witnessed mixed business activity readings, making it challenging to predict the pace of economic deceleration in the US. The labor market has shown signs of cooling, though the economy added more people to the workforce than expected, while fewer people applied for unemployment benefits.

- Recent inflation data in the US showed that inflation on the consumer and producer side surprised to the upside, suggesting that inflation is stickier than expected.

- Given the backdrop, Fed Chair Jerome Powell’s testimony at the US Congress earlier this month, suggesting the Fed would begin to cut borrowing costs, were justified. However, last week’s inflation figures and Retail Sales data triggered a repricing of Fed rate cut bets, aligning with the US central bank's view of 75 basis points of easing toward the end of 2024.

- According to the CME FedWatch Tool, expectations for a June rate cut stand at 64%, down from 72% a week ago.

Technical analysis: Gold traders remain on the sidelines as XAU/USD stays around $2,150

XAU/USD price hovers around $2,150 unmoved ahead of the FOMC decision. A dovish tilt could open the door for a rally that prompts a jump in Gold prices, opening the door to challenge the all-time high (ATH) at $2,195.15. A retest there would expose $2,200 next.

On the other hand, if Gold spot price tumbles below $2,150, look for a breach below December’s 3 high, exposing the March 6 low of $2,123.80, followed by $2,100.

Gold FAQs

Gold has played a key role in human’s history as it has been widely used as a store of value and medium of exchange. Currently, apart from its shine and usage for jewelry, the precious metal is widely seen as a safe-haven asset, meaning that it is considered a good investment during turbulent times. Gold is also widely seen as a hedge against inflation and against depreciating currencies as it doesn’t rely on any specific issuer or government.

Central banks are the biggest Gold holders. In their aim to support their currencies in turbulent times, central banks tend to diversify their reserves and buy Gold to improve the perceived strength of the economy and the currency. High Gold reserves can be a source of trust for a country’s solvency. Central banks added 1,136 tonnes of Gold worth around $70 billion to their reserves in 2022, according to data from the World Gold Council. This is the highest yearly purchase since records began. Central banks from emerging economies such as China, India and Turkey are quickly increasing their Gold reserves.

Gold has an inverse correlation with the US Dollar and US Treasuries, which are both major reserve and safe-haven assets. When the Dollar depreciates, Gold tends to rise, enabling investors and central banks to diversify their assets in turbulent times. Gold is also inversely correlated with risk assets. A rally in the stock market tends to weaken Gold price, while sell-offs in riskier markets tend to favor the precious metal.

The price can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can quickly make Gold price escalate due to its safe-haven status. As a yield-less asset, Gold tends to rise with lower interest rates, while higher cost of money usually weighs down on the yellow metal. Still, most moves depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAU/USD). A strong Dollar tends to keep the price of Gold controlled, whereas a weaker Dollar is likely to push Gold prices up.

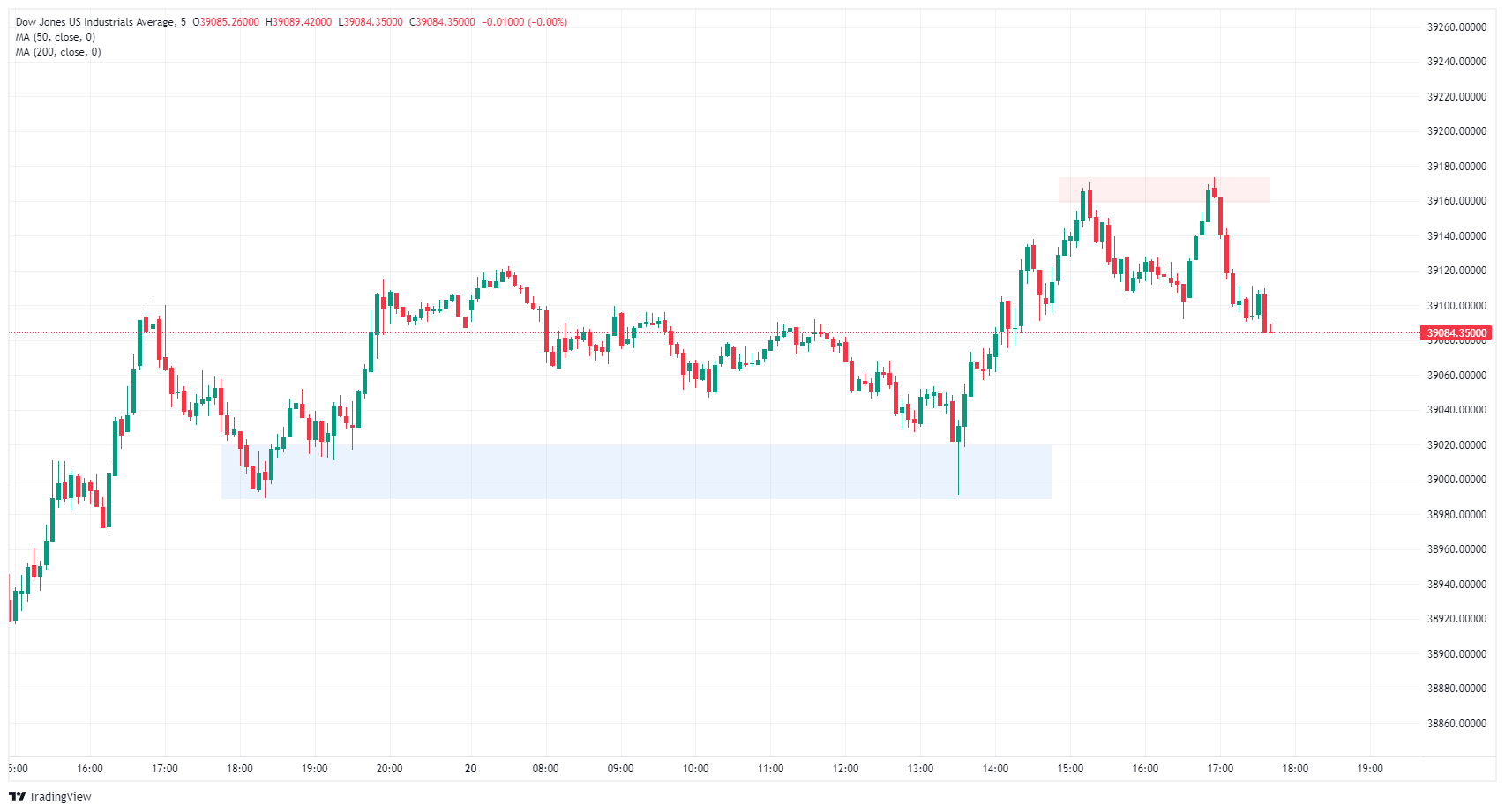

- Dow Jones goes flat as investors draw into the middle pre-Fed rate call.

- FOMC Interest Rate Projections also dropping on markets.

- Press conference from Fed Chairman Jerome Powell due after FOMC release.

The Dow Jones Industrial Average (DJIA) is churning at the day’s opening prices as investors brace for the latest Federal Reserve (Fed) rate call as well as a much-anticipated update to the Federal Open Market Committee’s (FOMC) Interest Rate Outlook. The FOMC’s rate call and rate forecast are due at the top of the hour at 18:00 GMT, with Fed Chairman Jerome Powell tabling a press conference 30 minutes later at 18:30 GMT.

Dow Jones news

The Dow Jones is mixed on Wednesday, with about half of the 30 listed securities trading into the low side. Boeing Co. (BA) is seeing a brief recovery from recent selling pressure, climbing around 2.3% to trade into $185.00 per share. On the bottom end, Chevron Corp. (CVX) is down nearly 1.5% in midweek trading, testing into $154.00 per share.

The Materials and Industrials Sectors are Wednesday’s early climbers, rising around 0.4% in midday pre-Fed trading. The Health and Energy Sectors are falling into the low side, falling 0.7% and 0.6%, respectively.

Dow Jones Industrial Average technical outlook

The Dow Jones drifted into an early low near 39,000.00 on Wednesday before recovering into 39,160.00. Bids have pulled back into the day’s opening prices near 39,100.00 as investors buckle down for a spark from the Fed.

The DJIA is trading into the top end of near-term consolidation as the index struggles to gain further ground above the 39,200.00 level. Swing lows have been etching in a higher lows pattern, and an intraday demand zone in priced in near 38,700.00.

Dow Jones Industrial Average 5-minute chart

Fed FAQs

Monetary policy in the US is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability and foster full employment. Its primary tool to achieve these goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, it raises interest rates, increasing borrowing costs throughout the economy. This results in a stronger US Dollar (USD) as it makes the US a more attractive place for international investors to park their money. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates to encourage borrowing, which weighs on the Greenback.

The Federal Reserve (Fed) holds eight policy meetings a year, where the Federal Open Market Committee (FOMC) assesses economic conditions and makes monetary policy decisions. The FOMC is attended by twelve Fed officials – the seven members of the Board of Governors, the president of the Federal Reserve Bank of New York, and four of the remaining eleven regional Reserve Bank presidents, who serve one-year terms on a rotating basis.

In extreme situations, the Federal Reserve may resort to a policy named Quantitative Easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used during crises or when inflation is extremely low. It was the Fed’s weapon of choice during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy high grade bonds from financial institutions. QE usually weakens the US Dollar.

Quantitative tightening (QT) is the reverse process of QE, whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing, to purchase new bonds. It is usually positive for the value of the US Dollar.

- The USD Dollar extended its gains on Wednesday.

- All eyes are set on the updated Dot Plot and Chair Powell’s tone.

- Any hawkish or dovish surprise from the Fed may trigger volatility in the USD.

The US Dollar Index (DXY) is currently trading near 104, demonstrating a gain not witnessed since March 1. The Greenback has been steadily ascending for the fifth day in a row, backed up by strong economic data and rising US Treasury yields in the last few sessions. However, the short-term trajectory will be dictated by the Federal Reserve’s (Fed) stance and projections.

The US economy remains resilient, with little evidence of inflation coming down and the labor market showing mixed signals. Investors will closely evaluate Chair Jerome Powell’s stance and how confident he is regarding cutting rates.

Daily digest market movers: DXY's rally persists as investors await FOMC decision and projections

- Markets are still expecting three rate cuts in 2024, starting in June, which matches the last projection from Fed officials.

- The focus will be on the Summary of Economic Projections (SEP) and how confident the bank is on the inflation progress.

- Any shifts seen in the Dot Plot may trigger a reaction in the Greenback.

DXY technical analysis: DXY's bullish momentum is under control, yet volatility is on the horizon

The technical indicators on the daily chart reflect strong buying momentum. The Relative Strength Index (RSI) registers a positive slope in bullish territory, underlining the dominating force of buyers. Simultaneously, the Moving Average Convergence Divergence (MACD) confirms this bullish sentiment by showing rising green bars, suggesting a sustained upward momentum for DXY.

The Simple Moving Averages (SMAs) provide further substantiation of this bullish market control. The index maintains a position above the critical 20, 100, and 200-day SMAs, highlighting a broader positive perspective.

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022. Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

- The Canadian Dollar is bound in the midrange as investors await FOMC.

- Bank of Canada to get drowned out by market’s Fed rate cut expectations.

- Fed expected to hold, investors hope for a June rate cut.

The Canadian Dollar (CAD) is mostly flat on the day as markets brace for the latest interest rate forecast and rate call from the Federal Reserve (Fed) at 18:00 GMT today, and the Bank of Canada (BoC) is unlikely to make waves as investors look for signs of a near-term Fed rate cut. Expectations of early and frequent rate trims from the Fed have been pushed down by reality for months, with the median forecast for a first rate slash currently set in June.

The Bank of Canada will release its latest Summary of Deliberations at 17:30 GMT, just ahead of the Fed’s latest Economic Projections. Canadian Consumer Price Index (CPI) inflation cooled this week, with February’s YoY CPI easing to 2.8% from the previous 2.9%, surprising markets that expected an increase to 3.1%. Canadian CPI inflation is easing enough that further rate hikes are unlikely, but not fast or hard enough to spark an immediate rate cut schedule.

Daily digest market movers: Canadian Dollar hung in midrange ahead of Fed

- The US Fed’s latest rate call and monetary policy statement will be released at 18:00 GMT today, alongside the Federal Open Market Committee’s (FOMC) Economic and Interest Rate Projections.

- Federal Reserve Chairman Jerome Powell will launch a press conference shortly after at 18:30 GMT.

- With the Fed broadly expected to hold rates steady at this week’s meeting, market focus will be pinned on the odds of a June rate call.

- According to the CME’s FedWatch Tool, money markets are pricing in a 65% chance of at least a 25 basis point rate trim at the June FOMC meeting.

- The Fed’s updated Dot Plot of interest rate projections will be closely watched today. The last iteration of the Fed’s internal rate outlook saw three rate cuts of 25 basis points each through the end of the year.

Canadian Dollar price today

The table below shows the percentage change of Canadian Dollar (CAD) against listed major currencies today. Canadian Dollar was the weakest against the Australian Dollar.

| USD | EUR | GBP | CAD | AUD | JPY | NZD | CHF | |

| USD | 0.06% | 0.04% | -0.09% | -0.08% | 0.36% | 0.18% | 0.25% | |

| EUR | -0.06% | -0.01% | -0.15% | -0.12% | 0.32% | 0.13% | 0.20% | |

| GBP | -0.02% | 0.01% | -0.14% | -0.10% | 0.32% | 0.16% | 0.20% | |

| CAD | 0.09% | 0.15% | 0.16% | 0.03% | 0.46% | 0.27% | 0.34% | |

| AUD | 0.06% | 0.12% | 0.11% | -0.02% | 0.43% | 0.24% | 0.32% | |

| JPY | -0.37% | -0.30% | -0.36% | -0.46% | -0.43% | -0.19% | -0.11% | |

| NZD | -0.19% | -0.13% | -0.14% | -0.28% | -0.26% | 0.18% | 0.06% | |

| CHF | -0.26% | -0.19% | -0.20% | -0.35% | -0.31% | 0.12% | -0.07% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent EUR (base)/JPY (quote).

Technical analysis: Canadian Dollar churns against Greenback after backsliding to 1.3600

The Canadian Dollar (CAD) kicked off Wednesday by stumbling back against the US Dollar (USD), pushing the USD/CAD pair into the 1.3600 handle. The CAD recovered into the day’s opening range, sticking close to 1.3560. Intraday action has a technical floor priced in at the 200-day Simple Moving Average (SMA) at 1.3515, and 1.3600 remains a key technical ceiling.

USD/CAD continues to churn in the same neighborhood as the 200-day SMA at 1.3480, and a rising higher lows pattern remains firmly printed into the charts, but momentum remains low. The pair is broadly stuck in a medium-term range, with bids cycling the midpoint between late December’s swing low into 1.3200 and last November’s peak bids near 1.3900.

USD/CAD hourly chart

USD/CAD daily chart

Canadian Dollar FAQs

The key factors driving the Canadian Dollar (CAD) are the level of interest rates set by the Bank of Canada (BoC), the price of Oil, Canada’s largest export, the health of its economy, inflation and the Trade Balance, which is the difference between the value of Canada’s exports versus its imports. Other factors include market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – with risk-on being CAD-positive. As its largest trading partner, the health of the US economy is also a key factor influencing the Canadian Dollar.

The Bank of Canada (BoC) has a significant influence on the Canadian Dollar by setting the level of interest rates that banks can lend to one another. This influences the level of interest rates for everyone. The main goal of the BoC is to maintain inflation at 1-3% by adjusting interest rates up or down. Relatively higher interest rates tend to be positive for the CAD. The Bank of Canada can also use quantitative easing and tightening to influence credit conditions, with the former CAD-negative and the latter CAD-positive.

The price of Oil is a key factor impacting the value of the Canadian Dollar. Petroleum is Canada’s biggest export, so Oil price tends to have an immediate impact on the CAD value. Generally, if Oil price rises CAD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Oil falls. Higher Oil prices also tend to result in a greater likelihood of a positive Trade Balance, which is also supportive of the CAD.

While inflation had always traditionally been thought of as a negative factor for a currency since it lowers the value of money, the opposite has actually been the case in modern times with the relaxation of cross-border capital controls. Higher inflation tends to lead central banks to put up interest rates which attracts more capital inflows from global investors seeking a lucrative place to keep their money. This increases demand for the local currency, which in Canada’s case is the Canadian Dollar.

Macroeconomic data releases gauge the health of the economy and can have an impact on the Canadian Dollar. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the CAD. A strong economy is good for the Canadian Dollar. Not only does it attract more foreign investment but it may encourage the Bank of Canada to put up interest rates, leading to a stronger currency. If economic data is weak, however, the CAD is likely to fall.

- Mexican Peso up vs. US Dollar, eyes on Fed and Banxico meetings.

- Banxico may ease policy, affecting USD/MXN as rates diverge in favor of Greenback.

- Mexico's inflation data on Thursday to hint at Peso's path.

- Fed's rate stance and hawkish cues might underpin USD/MXN with resistance levels the focus.

The Mexican Peso (MXN) recovers some territory on Wednesday against the US Dollar (USD) ahead of the US Federal Reserve’s (Fed) monetary policy decision at 18:00 GMT. During the first half of the week, the Mexican currency has been on the defensive amid speculation that on Thursday the Bank of Mexico – also known as Banxico – might begin its easing cycle. Consequently, the reduction of the interest rate spread between the US and Mexico could underpin the Greenback. At the time of writing, the USD/MXN trades at 16.78, down 0.14%.

Mexico’s economic calendar remains absent on Wednesday, but it will gather pace on Thursday. Besides Banxico’s decision, economic growth data and mid-month inflation figures in March, which are expected to remain virtually unchanged compared to previous readings, could impact the USD/MXN exchange rate.

The market anticipates the Fed maintaining interest rates at their current levels, but there is speculation of a hawkish tilt. This could potentially impact the USD/MXN exchange rate. Policymakers will update their economic and monetary policy projections – the so-called Dot Plot. If just two of the dots move up, that would indicate the Fed is considering two interest rate cuts instead of the three initially projected in the December meeting.

That could drive the USD/MXN higher toward the 17.00 figure, and buyers could threaten to break key resistance levels.

Daily digest market movers: Mexican Peso shrugs off Banxico’s imminent cut and rises

- Estimates that Banxico will lower the interest rate from 11.25% to 11% put “some” pressure on the Mexican currency, which could lift the USD/MXN toward the 17.00 mark.

- Mexico’s economic data released in the week:

- Aggregate Demand rose by 0.3% QoQ in Q4, up from 0%. On an annual basis, it decelerated from 2.7% to 2.6%.

- Private Spending on a quarterly basis slowed from 1.2% to 0.9%. On a yearly basis, it improved from 4.3% to 5.1%.

- On March 21, Banxico is expected to decrease interest rates, even though it could feature a 3-2 vote split. Recent speeches and media appearances show that Banxico’s Governing Council is divided, with Governor Victoria Rodriguez Ceja, Omar Mejia Castelazo and Galia Borja Gomez leaning dovish. On the hawkish front lie Jonathan Heath and Irene Espinosa Cantellano.

- The slowdown in Mexico’s economy is one of the main reasons that Banxico is eyeing the first cut. Mexico’s central bank expects the economy to grow 2.8% YoY in 2024, down from 3%, but maintained at 1.5% for 2025.

- The latest inflation figures in the United States prompted investors to price in a less dovish stance. Money market futures have adjusted their rate cut expectations to be more in line with the Fed's as they foresee the Federal Funds Rate (FFR) at 4.71% toward the end of the year. Analysts estimate the Fed will not change its Federal Funds Rates (FFR) level until June or later.

- US Treasury bond yields drop, but the US Dollar Index (DXY) advances 0.13%, up at 103.95, capping the USD/MXN fall.

Technical analysis: Mexican Peso counterattacks as USD/MXN slumps below 16.80

The USD/MXN is neutral to downwardly biased after buyers lifted the exchange rate to a weekly high of 16.94 before retreating beneath 16.80. If the pair extends its losses below 16.78, the January 8 swing low, that could exacerbate a test of last year’s low of 16.62 before diving to 16.32, the October 2015 low.

On the other hand, if buyers lift the pair above the current week’s high of 16.94, that would pave the way for testing 17.00. The next key resistance levels would be the 50-day Simple Moving Average (SMA) at 17.02, the 100-day SMA at 17.16, and the 200-day SMA at 17.21.

USD/MXN Price Action – Daily Chart

Mexican Peso FAQs

The Mexican Peso (MXN) is the most traded currency among its Latin American peers. Its value is broadly determined by the performance of the Mexican economy, the country’s central bank’s policy, the amount of foreign investment in the country and even the levels of remittances sent by Mexicans who live abroad, particularly in the United States. Geopolitical trends can also move MXN: for example, the process of nearshoring – or the decision by some firms to relocate manufacturing capacity and supply chains closer to their home countries – is also seen as a catalyst for the Mexican currency as the country is considered a key manufacturing hub in the American continent. Another catalyst for MXN is Oil prices as Mexico is a key exporter of the commodity.

The main objective of Mexico’s central bank, also known as Banxico, is to maintain inflation at low and stable levels (at or close to its target of 3%, the midpoint in a tolerance band of between 2% and 4%). To this end, the bank sets an appropriate level of interest rates. When inflation is too high, Banxico will attempt to tame it by raising interest rates, making it more expensive for households and businesses to borrow money, thus cooling demand and the overall economy. Higher interest rates are generally positive for the Mexican Peso (MXN) as they lead to higher yields, making the country a more attractive place for investors. On the contrary, lower interest rates tend to weaken MXN.

Macroeconomic data releases are key to assess the state of the economy and can have an impact on the Mexican Peso (MXN) valuation. A strong Mexican economy, based on high economic growth, low unemployment and high confidence is good for MXN. Not only does it attract more foreign investment but it may encourage the Bank of Mexico (Banxico) to increase interest rates, particularly if this strength comes together with elevated inflation. However, if economic data is weak, MXN is likely to depreciate.

As an emerging-market currency, the Mexican Peso (MXN) tends to strive during risk-on periods, or when investors perceive that broader market risks are low and thus are eager to engage with investments that carry a higher risk. Conversely, MXN tends to weaken at times of market turbulence or economic uncertainty as investors tend to sell higher-risk assets and flee to the more-stable safe havens.

- The daily chart reveals bullish sentiment, with RSI on an upward trajectory out of the negative zone and MACD depicting decreasing red bars.

- Indicators are consolidating overbought conditions on the hourly chart.

- Bulls must recover the 20-day SMA to confirm a recovery.

The NZD/JPY currency pair is trading at 91.54, showing gains in Wednesday's session. The broader technical landscape suggests the buyers. Despite recent bearish activity pushing the pair below the 20-day Simple Moving Averages (SMAs), the pair remains aloft of the 100 and 200-day SMAs, indicating an enduring bullish control.

On the daily chart, the NZD/JPY pair exhibits relatively bullish momentum. The Relative Strength Index (RSI) indicates a positive trend with an upward slope, moving above the negative territory. This, combined with the decreasing red bars from the Moving Average Convergence Divergence (MACD) which indicates declining negative momentum, suggests the buyers are gaining the upper hand over sellers.

NZD/JPY Daily Chart

Transitioning to the hourly chart for the NZD/JPY presents a slightly different scenario. Here, the RSI consistently indicates positive with minor fluctuations, hinting at strong buying momentum but consolidating after entering in the overbought area during the European session. Meanwhile, the MACD reveals flat red bars, signifying stagnant negative momentum suggesting that the buyers are gearing up for the next upward leg.

NZD/JPY Hourly Chart

After jumping out of the blocks at the start of the year, the US Dollar (USD) has run out of steam and is almost back to where it started 2024 against a basket of 26 currencies.

Monetary easing in the US to be less aggressive than in the rest of the world

The recent USD weakness probably reflects a sanguine view of a soft landing for the US economy, with very limited collateral damage to corporate earnings and limited job losses.

As we remain skeptical of this view and expect monetary easing in the US to be less aggressive than in the rest of the world, where negative growth is widespread, we expect the Dollar to rebound in the coming months.

- NZD/USD breaks to fresh lows after breaking out of the bottom of a multi-month range.

- The pair is now oversold and could correct back in the near-term.

- Eventually NZD/USD is likely to continue its descent towards bearish price targets.

NZD/USD has broken out of the bottom of a long-term range and despite reaching oversold extremes is tipped to go even lower.

The NZD/USD had been oscillating within a multi-month range stretching from a floor at about 0.6080 to a ceiling at roughly 0.6210. On Tuesday it decisively broke below the floor and took a step lower – a bearish sign for price.

New Zealand Dollar versus US Dollar: 4-hour chart

NZD/USD is currently trading at around 0.6035 and at oversold extremes according to the Relative Strength Index (RSI) momentum indicator. This indicates that there is a possibility the pair could pullback higher. The signal for a would come from the RSI existing oversold and rising again.Traders are advised not to add any more short-orders to their positions whilst the RSI is oversold and to close shorts when the indicator rises out of oversold.

Despite warning signs of a correction the longer-term outlook remains bearish. The pair is in an established short-term downtrend, with progressively lower peaks and troughs in the price action, and given the old adage that “the trend being your friend,” this suggests more downside as probable.

Further, NZD/USD has broken out of a long-term range and according to technical analysis theory the height of the range can be used as a guide to how much lower the pair could go. In the case of NZD/USD it suggests more downside is on the horizon.

The 0.618 Fibonacci ratio of the height of the range extrapolated from the breakout point lower provides an initial target at 0.5964. The 1.000 ratio provides a further target at 0.5892.

Economists at ING expect the EUR/USD pair to trend higher throughout the second half of 2024.

The Fed is the single most important driver of EUR/USD

The Fed is, and should remain, the single most important driver of EUR/USD: our call is they will cut more than markets expect and crucially around 50 bps more than the ECB.

Given that we also see both central banks starting to ease in June, we expect a bigger rally in EUR/USD in the second half of the year, when USD:EUR short-term rate convergence should accelerate. We target 1.1400 in 4Q24.

Rising geopolitical tensions, upward pressure on energy prices and a potential re-election of Donald Trump could all lead to a stronger Dollar.

- Core and headline inflation figures were softer than expected for February.

- Monetary policy divergences between the BoE and ECB continue favoring the GBP.

- The BoE meets on Thursday, a hold is priced in and the first cut is seen in August.

- The first cut from the ECB was seen in June.

The EUR/GBP is currently experiencing mild gains, trading at 0.8541 after peaking at a high of 0.8560. Markets are digesting British inflation data from February and gearing up for the Bank of England’s (BoE) decision on Thursday. In the meantime, monetary policy divergences between the BoE and the European Central Bank (ECB) give the GBP an advantage over the EUR/p>

The UK saw a softening in February CPI figures, with headline inflation at 3.4% YoY compared to January's 4.0%, and core inflation at 4.5% YoY down from 5.1%. Despite expectations, these numbers were slightly lower, marking the lowest since September 2021 but still above the 2% target. With the Bank of England's decision imminent, a policy hold is anticipated. However, given persistently high services inflation at 6.1% YoY, the BOE may take time to loosen policy. Market expectations of a 25 bp rate cut in August followed by two more by year-end are fully priced in. On the other hand, the ECB easing cycle is seen starting in June, followed by cuts in September and October. Investors see some chances of an additional cut in December as well.

EUR/GBP technical analysis

On the daily chart, the Relative Strength Index (RSI) for the EUR/GBP pair resides in negative territory, suggesting a slight bearish momentum. Despite brief transitions into positive territory, the RSI has reverted to negative levels in recent sessions, revealing that sellers maintain dominance. The green bars on the Moving Average Convergence Divergence (MACD) histogram reflect positive momentum, albeit flat, potentially indicating a weak presence of the bulls.

Regarding the overall trend, the pair is trading below its 20, 100, and 200-hour Simple Moving Averages, which gives arguments for a bearish outlook

EUR/GBP daily chart

The US Dollar (USD) is consolidating Tuesday’s gains. Economists at BBH analyze how the US Dollar (USD) could react to the Fed’s decision.

The risk is the Fed’s new funds rate projections imply less easing over 2024 and 2025

The two key points to scrutinize are: (i) The press release. A dovish risk is the press release is tweaked to signal greater confidence that inflation is moving sustainably towards 2%, in line with recent comments by Chair Powell. (ii) Summary of Economic Projections. Sticky underlying US inflation and an encouraging economic growth outlook suggest the risk is the Fed’s new funds rate projections (the so-called Dot Plot) imply less easing over 2024 and 2025.

If the Fed turns less dovish, the USD rally will get turbocharged as Fed funds rate expectations adjust higher. In contrast, if the Fed dismisses the latest high US inflation readings as noise and powers forward with a dovish outlook, USD will come under renewed downside pressure.

EUR/USD held steady below 1.0900. Economists at Commerzbank analyze how the Fed decision could impact the pair.

‘Dot plot’ is where the greatest potential for a decent Dollar movement lies

The new inflation and growth forecasts will be published, but above all the interest rate expectations of the FOMC members, the so-called ‘dot plots’. I think this is where the greatest potential for a decent Dollar movement lies, although the topic of balance sheet normalization (quantitative tightening) will certainly also take up quite some space.

The front end of the dots alone has to actually drift upwards to take into account the current, actual circumstances (that the Fed has become more cautious with regard to interest rate cuts since December). This alone could be interpreted by the market as a confirmation of its expectations and therefore positive for the Dollar, although it is only an overdue adjustment to reality.

If there are signs that the FOMC members are becoming more cautious about the timing and extent of future rate cuts, the Dollar may well gain further and EUR/USD may slip towards the 1.0800 mark.

- USD/JPY rallies up to multi-year highs in the 151.000s – a historical BoJ intervention zone.

- The move is backed by USD strength as interest rates are seen remaining high in the US.

- The BoJ raised interest rates but this did not defend the Yen as expected, since Japanese rates remain extremely low.