- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 25-05-2017

(raw materials / closing price /% change)

Oil 48.71 -0.39%

Gold 1,255.30 -0.09%

(index / closing price / change items /% change)

Nikkei +70.15 19813.13 +0.36%

TOPIX +3.31 1578.42 +0.21%

Hang Seng +202.28 25630.78 +0.80%

CSI 300 +61.49 3485.66 +1.80%

Euro Stoxx 50 -2.07 3584.55 -0.06%

FTSE 100 +2.81 7517.71 +0.04%

DAX -21.15 12621.72 -0.17%

CAC 40 -4.18 5337.16 -0.08%

DJIA +70.53 21082.95 +0.34%

S&P 500 +10.68 2415.07 +0.44%

NASDAQ +42.23 6205.26 +0.69%

S&P/TSX -8.76 15410.73 -0.06%

(pare/closed(GMT +2)/change, %)

EUR/USD $1,1207 -0,06%

GBP/USD $1,2936 -0,25%

USD/CHF Chf0,9727 -0,08%

USD/JPY Y111,81 +0,22%

EUR/JPY Y125,32 +0,18%

GBP/JPY Y144,63 -0,02%

AUD/USD $0,7453 -0,60%

NZD/USD $0,7015 -0,38%

USD/CAD C$1,3487 +0,60%

02:00 U.S. FOMC Member James Bullard Speaks

07:00 Eurozone ECB's Benoit Coeure Speaks

12:30 U.S. Durable Goods Orders April 0.9% Revised From 0.7% -1.2%

12:30 U.S. Durable Goods Orders ex Transportation April 0.0% Revised From -0.2% 0.5%

12:30 U.S. Durable goods orders ex defense April 0.1% 0.4%

12:30 U.S. PCE price index, q/q (Revised) Quarter I 2.3% 2.3%

12:30 U.S. PCE price index ex food, energy, q/q(Revised) Quarter I 1.3% 2%

12:30 U.S. GDP, q/q (Revised) Quarter I 2.1% 0.9%

14:00 U.S. Reuters/Michigan Consumer Sentiment Index (Finally) May 97 97.5

17:00 U.S. Baker Hughes Oil Rig Count May 720

The main US stock indexes showed a moderate increase, which was supported by strong reports of companies in the retail sector.

The sentiment of investors also gained momentum after the minutes of the last meeting of the Federal Reserve showed that politicians expect the economy to pick up momentum and raise interest rates sooner rather than later.

In addition, as it became known, the number of Americans applying for unemployment benefits last week grew less than expected, and the four-week moving average fell to a 44-year low, which suggests a further tightening of the labor market situation. Initial claims for unemployment benefits rose by 1,000 and, taking into account seasonal fluctuations, reached 234,000 for the week of May 20. This growth followed three weeks of decline.

At the same time, the deficit of international trade in April was 67.6 billion, which is 2.5 billion more than in March, when the deficit reached 65.1 billion. The export of goods for April amounted to 125.9 billion, which is 1.1 Billion less than in March. Imports of goods for April amounted to 193.4 billion, which is 1.4 billion more than in March.

Oil prices fell by about 5% on Thursday after OPEC approved the extension of the current agreement to reduce oil production for nine months, until March 2018, but refused to consider a possibility of a more significant decline in production.

Most components of the DOW index recorded a rise (22 out of 30). The leader of growth was shares UnitedHealth Group Incorporated (UNH, + 1.62%). The shares of E.I. du Pont de Nemours and Company fell more than others (DD, -1.25%).

Most sectors of the S & P index finished trading in positive territory. The leader of growth was the service sector (+ 1.0%). Most of all fell the sector of basic materials (-1.2%).

At closing:

DJIA + 0.33% 21,082.61 +70.19

Nasdaq + 0.69% 6.205.26 +42.24

S & P + 0.44% 2.415.04 +10.65

EURUSD: 1.1165-75 (EUR 672m) 1.1190-00 (485m)

USDJPY: 110.00 (USD 1.4bln)

GBPUSD: 1.3200 (GBP 558m)

U.S. stock-index futures rose as the minutes of the Fed's May meeting signaled that the U.S. central bank's officials had good confidence in the economic outlook and expected to raise interest rates soon.

Stocks:

Nikkei 19,813.13 +70.15 +0.36%

Hang Seng 25,630.78 +202.28 +0.80%

Shanghai 3,107.87 +43.80 +1.43%

S&P/ASX 5,789.63 +20.65 +0.36%

FTSE 7,509.25 -5.65 -0.08%

CAC 5,344.53 +3.19 +0.06%

DAX 12,628.69 -14.18 -0.11%

Crude $50.75 (-1.19%)

Gold $1,256.60 (-0.28%)

(company / ticker / price / change ($/%) / volume)

| ALTRIA GROUP INC. | MO | 73.58 | 0.73(1.00%) | 310 |

| Amazon.com Inc., NASDAQ | AMZN | 984.4 | 4.05(0.41%) | 34070 |

| Apple Inc. | AAPL | 153.86 | 0.52(0.34%) | 96223 |

| AT&T Inc | T | 38.25 | 0.10(0.26%) | 528 |

| Barrick Gold Corporation, NYSE | ABX | 16.59 | -0.12(-0.72%) | 18725 |

| Caterpillar Inc | CAT | 104.01 | 0.06(0.06%) | 1879 |

| Chevron Corp | CVX | 105.94 | -0.28(-0.26%) | 1280 |

| Cisco Systems Inc | CSCO | 31.54 | 0.05(0.16%) | 860 |

| Citigroup Inc., NYSE | C | 62.5 | 0.23(0.37%) | 4932 |

| Exxon Mobil Corp | XOM | 82.09 | -0.20(-0.24%) | 7283 |

| Facebook, Inc. | FB | 150.31 | 0.27(0.18%) | 55131 |

| Ford Motor Co. | F | 10.98 | 0.02(0.18%) | 4407 |

| Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 11.95 | 0.05(0.42%) | 785 |

| General Electric Co | GE | 27.84 | 0.01(0.04%) | 18512 |

| Goldman Sachs | GS | 224.55 | 0.72(0.32%) | 2649 |

| Google Inc. | GOOG | 958.65 | 3.69(0.39%) | 4664 |

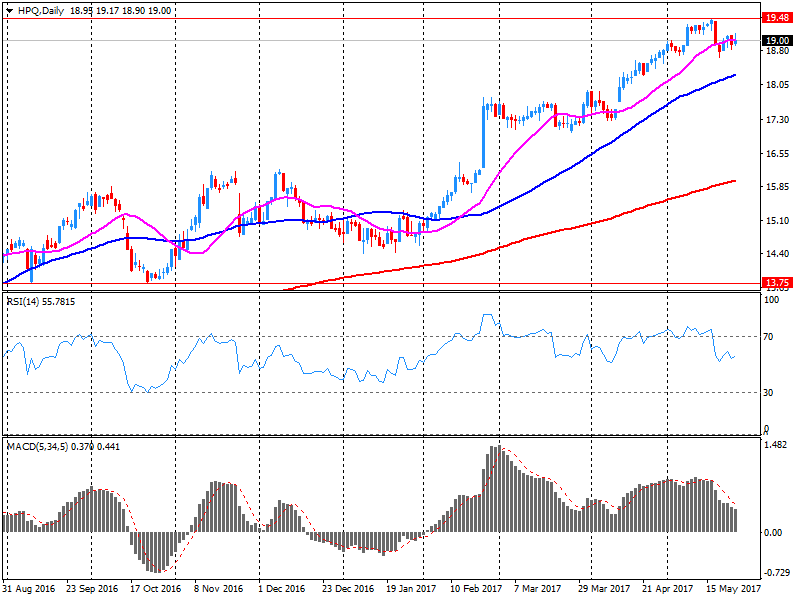

| Hewlett-Packard Co. | HPQ | 19.69 | 0.68(3.58%) | 19805 |

| Home Depot Inc | HD | 155.62 | 0.62(0.40%) | 2509 |

| Intel Corp | INTC | 36.18 | 0.06(0.17%) | 161520 |

| Johnson & Johnson | JNJ | 127.46 | 0.79(0.62%) | 218 |

| JPMorgan Chase and Co | JPM | 85.93 | 0.22(0.26%) | 8083 |

| Merck & Co Inc | MRK | 64.99 | 0.06(0.09%) | 131 |

| Microsoft Corp | MSFT | 69 | 0.23(0.33%) | 8534 |

| Nike | NKE | 52.2 | 0.19(0.37%) | 1126 |

| Procter & Gamble Co | PG | 86.74 | 0.24(0.28%) | 621 |

| Starbucks Corporation, NASDAQ | SBUX | 62.1 | 0.21(0.34%) | 2118 |

| Tesla Motors, Inc., NASDAQ | TSLA | 311.07 | 0.85(0.27%) | 21767 |

| The Coca-Cola Co | KO | 44.93 | -0.10(-0.22%) | 3076 |

| Twitter, Inc., NYSE | TWTR | 18.05 | 0.07(0.39%) | 25542 |

| Verizon Communications Inc | VZ | 45.1 | 0.06(0.13%) | 3058 |

| Visa | V | 95.3 | 0.49(0.52%) | 1401 |

| Walt Disney Co | DIS | 107.99 | 0.28(0.26%) | 359 |

| Yandex N.V., NASDAQ | YNDX | 28.7 | 0.23(0.81%) | 585 |

|

|

|

|

|

|

Altria (MO) initiated with an Overweight at Piper Jaffray

McDonald's (MCD) target raised to $170 from $160 at Bernstein

The international trade deficit was $67.6 billion in April, up $2.5 billion from $65.1 billion in March. Exports of goods for April were $125.9 billion, $1.1 billion less than March exports. Imports of goods for April were $193.4 billion, $1.4 billion more than March imports.

Wholesale inventories for April, adjusted for seasonal variations but not for price changes, were estimated at an end-of-month level of $592.0 billion, down 0.3 percent (±0.4 percent)* from March 2017, and were up 1.8 percent (±1.1 percent) from April 2016. The February 2017 to March 2017 percentage change was revised from up 0.2 percent (±0.4 percent)* to up 0.1 percent

In the week ending May 20, the advance figure for seasonally adjusted initial claims was 234,000, an increase of 1,000 from the previous week's revised level. The previous week's level was revised up by 1,000 from 232,000 to 233,000.

The 4-week moving average was 235,250, a decrease of 5,750 from the previous week's revised average. This is the lowest level for this average since April 14, 1973 when it was 232,750. The previous week's average was revised up by 250 from 240,750 to 241,000.

EUR/USD

Offers: 1.1260 1.1275-80 1.1300 1.1320 1.1350 1.1400

Bids: 1.1220 1.1200 1.1180 1.1165 1.1140-50 1.1120 1.1100

GBP/USD

Offers: 1.3000 1.3020 1.3030 1.3050 1.3080 1.3100

Bids: 1.2970 1.2950 1.2930 1.2920 1.29001.2875-80 1.2850

EUR/JPY

Offers: 125.80 126.00 126.50 126.80 127.00

Bids: 125.20 125.00 124.50 124.30 124.00

EUR/GBP

Offers: 0.8665 0.8680 0.8700 0.8720 0.8750

Bids: 0.8650 0.8630 0.8600 0.8585 0.8570 0.8550

USD/JPY

Offers: 112.00 112.30 112.50 112.80 113.00

Bids: 111.60 111.50 111.30 111.00 110.80-85 110.50

AUD/USD

Offers: 0.7500 0.7530 0.7550 0.7570 0.7600

Bids: 0.7465 0.7450 0.7430 0.7400 0.7385 0.7350

HP Inc. (HPQ) reported Q2 FY 2017 earnings of $0.40 per share (versus $0.41 in Q2 FY 2016), beating analysts' consensus estimate of $0.39.

The company's quarterly revenues amounted to $12.400 bln (+7% y/y), beating analysts' consensus estimate of $11.933 bln.

The company raised guidance for FY 2017, projecting EPS of $1.59-1.66 versus analysts' consensus estimate of $1.62.

HPQ rose to $19.60 (+3.10%) in pre-market trading.

-

Most important issue is to regulate and stabilise market, lower oil inventory levels to 5yr average

-

Says Chevron is welcome partner in his country

Gross fixed capital formation (GFCF), in volume terms, was estimated to have increased by 1.2% to £79.0 billion in Quarter 1 (Jan to Mar) 2017 from £78.1 billion in Quarter 4 (Oct to Dec) 2016.

Business investment was estimated to have increased by 0.6%, to £43.8 billion between Quarter 4 2016 and Quarter 1 2017.

Between Quarter 1 2016 and Quarter 1 2017, GFCF was estimated to have increased by 2.2%, from £77.3 billion and business investment was estimated to have increased by 0.8% from £43.4 billion.

The sectors contributing most to GFCF growth between Quarter 4 2016 and Quarter 1 2017 were public corporations and private sector dwellings, and business investment. Dwellings and other buildings and structures were the assets which contributed most to the increase in GFCF for the same period.

Services output increased by 0.2% between February and March 2017.

The largest contribution to the month-on-month growth came from transport, storage and communication, which contributed 0.23 percentage points of which motion pictures contributed 0.16 percentage points.

The Index of Services increased by 0.2% in Quarter 1 (Jan to Mar) 2017 compared with Quarter 4 (Oct to Dec) 2016; following growth of 0.8% between Quarter 3 (July to Sept) 2016 and Quarter 4 2016.

The slowdown in growth in Quarter 1 2017 mainly came from the distribution, hotels and restaurants sector with notable falls in some consumer-focused industries such as retail.

Growth between Quarter 4 2016 and Quarter 1 2017 has been revised down 0.1% from the previous estimate used in the gross domestic product preliminary estimate, published on 28 April 2017; this was primarily due to the receipt of late data for January and February.

UK gross domestic product (GDP) in volume terms was estimated to have increased by 0.2% between Quarter 4 (Oct to Dec) 2016 and Quarter 1 (Jan to Mar) 2017.

UK GDP growth in Quarter 1 2017 has been revised down by 0.1 percentage points from the preliminary estimate published on 28 April 2017; mainly due to broad-based downward revisions within the services sector.

UK GDP growth slowed to 0.2% in Quarter 1 2017 as consumer facing industries such as retail and accommodation fell and household spending slowed. This was partly due to rising prices. Construction and manufacturing also showed little growth, while business services & finance continued to grow strongly.

GDP in current prices increased by 0.7% between Quarter 4 2016 and Quarter 1 2017.

GDP per head in volume terms was flat between Quarter 4 2016 and Quarter 1 2017.

In March 2017 the seasonally adjusted turnover index increased by 0.5% compared to the previous month (+1.1% in domestic market and -0.9% in non-domestic market). The percentage change of the average of the last three months compared to the previous three months was +0.4% (+1.0% in domestic market and -0.8% in non-domestic market).

In March 2017 the seasonally adjusted industrial new orders index decreased by 4.2% compared with February 2017 (-0.8% in domestic market and -8.3% in non-domestic market). The percentage change of the average of the last three months compared to the previous three months was +1.5% (-1.7% in domestic market and +6.1% in non-domestic market).

With respect to the same month of the previous year the calendar adjusted industrial turnover index increased by +7.2% (calendar working days in March 2017 being 23 versus 22 days in March 2016).

EURUSD: 1.1165-75 (EUR 672m) 1.1190-00 (485m)

USDJPY: 110.00 (USD 1.4bln)

GBPUSD: 1.3200 (GBP 558m)

-

Will be advocating raising rates when he sees an opportunity to do so

-

He is not taking explicit account of new U.S policies as he makes his forecasts

-

Increased operating surpluses to be spent on new capital investments

-

New spending includes NZD7 bln over 4 yrs in public services, NZD11 bln on infrastructure

-

Medium term economic outlook positive

-

Don't need to take additional easing steps to achieve inflation target earlier than what is forecast in april outlook report

-

Must ensure boj communicates well with markets to alleviate any worries about future exit from stimulus programme

-

Believe it would be fine to maintain for now boj's pledge to increase its bond holdings by around 80 trln yen per year

-

It is true boj's recent bond buying pace somewhat slower compared with its 80-trln-yen pledge

-

Fiscal consolidation is an important long-term goal

EUR/USD

Resistance levels (open interest**, contracts)

$1.1378 (3017)

$1.1341 (5066)

$1.1282 (5628)

Price at time of writing this review: $1.1234

Support levels (open interest**, contracts):

$1.1171 (833)

$1.1130 (1157)

$1.1067 (2131)

Comments:

- Overall open interest on the CALL options with the expiration date June, 9 is 82063 contracts, with the maximum number of contracts with strike price $1,1000 (6104);

- Overall open interest on the PUT options with the expiration date June, 9 is 100131 contracts, with the maximum number of contracts with strike price $1,0700 (5492);

- The ratio of PUT/CALL was 1.22 versus 1.20 from the previous trading day according to data from May, 24

GBP/USD

Resistance levels (open interest**, contracts)

$1.3301 (1043)

$1.3202 (2706)

$1.3104 (3157)

Price at time of writing this review: $1.2986

Support levels (open interest**, contracts):

$1.2894 (1291)

$1.2797 (2220)

$1.2698 (1756)

Comments:

- Overall open interest on the CALL options with the expiration date June, 9 is 35692 contracts, with the maximum number of contracts with strike price $1,3000 (4169);

- Overall open interest on the PUT options with the expiration date June, 9 is 36220 contracts, with the maximum number of contracts with strike price $1,1500 (3061);

- The ratio of PUT/CALL was 1.01 versus 1.03 from the previous trading day according to data from May, 24

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

Most major European stock markets closed out a choppy session slightly lower, with investors staying on the sidelines ahead of the Federal Reserve minutes due later in the day. Dovish comments from European Central Bank President Mario Draghi did little to pull markets out of their narrow trading ranges.

The S&P 500 gained ground for a fifth consecutive session Wednesday to close at a record as minutes of the Federal Reserve's latest policy meeting showed broad agreement on plans to begin shrinking the central bank's balance sheet and also pointed to a likely rate increase next month, as widely expected.

Chinese stocks closed higher Wednesday, shaking off losses as initial concerns wore off from Moody's Investors Service's decision to lower the country's credit rating for the first time since 1989. Equities fell more than 1% in early trading in both Shanghai and Shenzhen, with the downgrade reminding investors of China's continued growth in outstanding borrowings-especially among companies.

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers