- Analytics

- News and Tools

- Market News

Analytics, News, and Forecasts for CFD Markets: currency news — 29-05-2022.

US inflation expectations, as per the 10-year breakeven inflation rate per the St. Louis Federal Reserve (FRED) data, rose for the third consecutive day by the end of Friday’s North American session.

That said, the inflation gauge rose from 2.62% to 2.63% at the latest as traders gained mixed signals from the Fed’s preferred inflation barometer, namely the US Core Personal Consumption Expenditure (PCE) Price Index for April.

That said, the US Personal Consumption Expenditure (PCE) data came in mixed for April, mostly downbeat, as the Core PCE Price Index matched 4.9% YoY forecasts versus 5.2% prior. Further, Personal Income rose less than expected but the Personal Spending improved.

Following the data release, The Times came out with the analysis suggesting inflation puts further pressure on the Fed to lift interest rates. The same could be linked to the latest US dollar consolidation from the monthly low during Monday’s Asian session.

Also read: US PCE prices ebb in April, a sign that inflation is slowing?

- USD/JPY may elevate to 124.00 as investors’ focus has shifted to Employment data.

- BOJ Kuroda demands a wage hike along with the price hike to keep inflationary pressures stable.

- The Unemployment Rate in the US and Japan will remain stable at 3.6% and 2.6% respectively.

The USD/JPY pair has displayed a sheer upside move in the early Asian session. A bullish open-drive session has pushed the asset to near Friday’s high at 127.34. The asset is scaling sharply higher right from the first needle of the trading session.

A wide divergence in the monetary policies is impacting the Japanese yen. The yen bulls are worried over the grounded inflation in its region. On Friday, the Statistics Bureau of Japan reported the Tokyo Consumer Price Index (CPI) at 2.4%, lower than the estimates of 2.7% and the prior print of 2.5%.

A statement from Japan’s Prime Minister Fumio Kishida, last week, that the Bank of Japan (BOJ) should make some efforts to achieve the targeted inflation rate of 2% has renewed growth concerns. In response to that BOJ Governor Harihuko Kuroda stated that the price rise should be accompanied by a wage hike if stable inflation is required at desired levels.

This week employment data from Japan and the US will keep investors busy. The Statistics Bureau of Japan is likely to display an improvement in the Jobs/Applicants Ratio at 1.23 against the prior print of 1.22. Also, the Unemployment Rate is expected to remain stable at 2.6%. On the US front, the US Nonfarm Payrolls are expected to land at 310k vs. 428k last recorded. The jobless rate may remain stable at 3.6%.

- AUD/JPY grinds higher around two-week top, sidelined after rising the most in two months.

- Risk appetite remains firmer amid hopes of further improvement in consumption, BOJ’s firm support for easy money.

- RBA vs. BOJ battle keeps buyers hopeful, qualitative catalysts are important for fresh impetus.

AUD/JPY extends the previous two-week upside to 91.10, refreshing a two-week high, as traders seek fresh clues during Monday’s initial Asian session. That said, the market’s risk-on mood joined the Bank of Japan’s (BOJ) firmer support for the easy money policies previously favored the pair buyers.

On Friday, risk appetite improved after the US inflation data matched easy expectations but the consumption improved in April. That said, the US Personal Consumption Expenditure (PCE) data came in mixed for April, mostly downbeat, as the Core PCE Price Index, the Fed’s preferred measure of inflation, matched 4.9% YoY forecasts versus 5.2% prior. Further, Personal Income rose less than expected but the Personal Spending improved.

Also likely to have favored the optimist was a headline suggesting a reduction in China’s covid hardships, as well as the dragon nation’s readiness for more stimulus.

It’s worth noting that the Reserve Bank of Australia’s (RBA) recently hawkish tone, backed by upbeat Aussie data, contrasts with the BOJ policymakers’ readiness to keep the easy money flowing despite the inflation fears also underpin the AUD/JPY prices. “BOJ will continue to work closely with government, strive to achieve 2% inflation target,” said Bank of Japan Governor Haruhiko Kuroda on Friday.

Against this backdrop, the Wall Street benchmarks posted another positive day but there was no major change in the US 10-year Treasury yields. That said, the S&P 500 Futures print 0.20% intraday gains at the latest.

Moving on, a lack of major data/events could restrict market moves, as well as challenge AUD/JPY traders, but risk catalysts will be important to watch for clear directions.

Technical analysis

AUD/JPY bulls need to cross a five-week-old descending trend line, around 91.35 by the press time, to keep the reins.

- USD/CAD is bracing a sheer downside move below 1.2718 ahead of hawkish BOC.

- Canada’s CPI at 6.9% is compelling a jumbo rate hike by the BOC this week.

- The DXY is likely to dance to the tunes of the US NFP.

The USD/CAD pair is oscillating in a narrow range of 1.2718-1.2728 in the early Asian session. The loonie bulls remained favored last week after the asset tumbled below the critical support of 1.2765 on Friday. A downside move below 1.2765 has opened doors for 1.2700 as technical downside will be accompanied by the interest rate decision from the Bank of Canada (BOC), which is due on Wednesday.

Citing the inflationary pressures in the loonie region, the BOC is expected to remain extremely hawkish in its monetary policy announcement. The April inflation rate landed at 6.9%, above the forecasts of 6.7% and more than a two-decade high. Mounting price pressures are impacting the real income of the households and eventually, the BOC is left with no other choice than to dictate a rate hike. As per the market consensus, the BOC is expected to elevate the interest rates by 50 basis points (bps). This may be a consecutive jumbo rate hike as the BOC also announced a half-a-percent rate hike in April.

On the oil front, boiling oil prices are supporting loonie. Mounting supply worries due to expectations of an embargo on Russian oil from Europe have kept the oil prices in the grip of bulls. Apart from that, the demand is expected to revive in China as the Chinese administration is expected to lift complete Covid-19 restrictions in Shanghai. The black gold is expected to remain established above $115.00 ad higher oil prices will fetch more funds into the loonie’s economy.

On the dollar front, the US dollar index (DXY) is consolidating below 101.70. The DXY will remain highly uncertain this week ahead of the release of the US Nonfarm Payrolls (NFP). The US economy may report an addition of 310k jobs in the labor market against the prior print of 428k.

- AUD/USD remains sidelined after printing the biggest weekly gains since mid-March.

- Firmer sentiment, hawkish RBASpeak and softer USD allowed bulls to keep reins.

- Market sentiment dwindles amid a lack of major catalysts, bank holiday in the US.

- Risk catalysts are important for intraday moves, Aussie Q1 GDP, US jobs report for April are crucial for the week.

AUD/USD takes rounds to mid-0.7100s as bulls take a breather following the biggest weekly jump in March. That said, a lack of major data/events restrict the Aussie pair’s moves around 0.7150 during Monday’s initial Asian session.

It’s worth noting that the week-start consolidation of recent gains, as well as caution ahead of this week’s key US employment numbers for April, namely the Nonfarm Payrolls (NFP) and the Unemployment Rate, seem to test the AUD/USD bulls.

On the same line are geopolitical headlines concerning Russia’s aggression in Donbas, as well as covid fears in China.

Additionally, the US dollar weakness could also be linked to the AUD/USD gains. The US Dollar Index (DXY) dropped for the second consecutive week to refresh the monthly low at the latest. That said, risk-on mood and mixed US data could be linked to the greenback’s recent weakness. Also weighing on the DXY are the repeated comments from the Fed policymakers suggesting 50 bps rate hikes and the latest FOMC minutes that raised concerns over a softer rate lift after September.

On Friday, the US Personal Consumption Expenditure (PCE) data came in mixed for April, mostly downbeat, as the Core PCE Price Index, the Fed’s preferred measure of inflation, matched 4.9% YoY forecasts versus 5.2% prior. Further, Personal Income rose less than expected but the Personal Spending improved.

Amid these plays, the Wall Street benchmarks posted another positive day but there was no major change in the US 10-year Treasury yields. That said, the S&P 500 Futures print 0.20% intraday gains at the latest.

Considering a light calendar and the US Bank holiday, AUD/USD traders should pay attention to the risk catalyst for fresh impulse.

Technical analysis

A two-week-old ascending trend line, around 0.7085 by the press time, directs AUD/USD buyers towards the 50-DMA and the monthly peak, respectively around 0.7260 and 0.7265.

- NZD/USD grinds higher after posting the biggest weekly gain since October 2021.

- Risk sentiment improved amid an increase in US consumption, softer inflation data, which in turn weighed on USD.

- Receding fears of inflation can help Kiwi but risks from China, Russia and growth concerns can probe bulls.

- China PMIs, US employment numbers for April appear the week’s key data.

NZD/USD dribbles above 0.6500 after posting the biggest weekly gains in 2022 as traders seek fresh clues to extend the latest run-up. That said, the Kiwi pair eases to 0.6530 during the initial Asian session on Monday.

Underlying the quote’s latest pullback could be the profit-booking moves amid a light calendar and an absence of major macros of late. Also likely to have probed the pair buyers is the caution ahead of this week’s key US employment numbers for April, namely the Nonfarm Payrolls (NFP) and the Unemployment Rate. Also, geopolitical headlines concerning Russia’s aggression in Donbas, as well as covid fears in China, exert additional downside pressure on the NZD/USD prices.

It’s worth noting that the broad US dollar weakness and the Reserve Bank of New Zealand’s (RBNZ) ahead-of-the-curve rate hikes keep the Kiwi pair on the front foot.

The US Dollar Index (DXY) dropped for the second consecutive week to refresh the monthly low at the latest. That said, risk-on mood and mixed US data could be linked to the greenback’s recent weakness. Also weighing on the DXY are the repeated comments from the Fed policymakers suggesting 50 bps rate hikes and the latest FOMC minutes that raised concerns over a softer rate lift after September.

On Friday, the US Personal Consumption Expenditure (PCE) data came in mixed for April, mostly downbeat, as the Core PCE Price Index, the Fed’s preferred measure of inflation, matched 4.9% YoY forecasts versus 5.2% prior. Further, Personal Income rose less than expected but the Personal Spending improved.

The upbeat sentiment could be well witnessed by Wall Street’s run-up, as well as no major change in the US 10-year Treasury yields.

Looking forward, a lack of major data/events may offer a dull start to the key week but macros and risk catalysts may entertain NZD/USD traders.

Technical analysis

NZD/USD buyers need to cross the 0.6570 hurdle comprising the monthly high to keep reins otherwise a pullback towards a fortnight-old rising trend line, around 0.6420 by the press time, appears more likely.

- EUR/USD is eyeing an imbalance move above 1.0765 as investors await EU Leaders Summit.

- An embargo on oil imports from Russia in Europe could be the highlight of the summit.

- Investors will remain busy ahead of the US NFP later this week.

The EUR/USD pair auctioned in a 1.0642-1.0765 range in the last week after establishing itself above the critical resistance of the May 5 high at 1.0645. The pair is expected to remain positive amid broader weakness in the US dollar index (DXY). An imbalance move above the last week’s high price at 1.0765 looks likely as investors are awaiting the European Union (EU) Leaders summit, which is due in the Asian session.

The EU leaders are expected to discuss various agendas however, a discussion over an embargo on oil imports from Russia will remain a major subject. The EU looks dedicated to punishing Russia for its inhuman activities in Ukraine. Despite getting opposition from various EU members, the EU is gauging ways to announce a complete prohibition on fossil fuels from Moscow. Following Germany’s approval of banning Russian oil, opposition came from Hungary and the EU is still convincing the latter to support the boycott.

Meanwhile, the US dollar index (DXY) is displaying some signs of exhaustion after printing a low of 101.43 last week. A minor rebound could take place as investors may prefer some short coverings. This week, the DXY is likely to be guided by the uncertainty over the US Nonfarm Payrolls (NFP). A preliminary estimate for the US NFP is 310k against the prior print of 428k.

- GBP/USD is steady in the open as markets open in a quiet start to the week.

- Eyes will be on the BoE this month and UK GDP.

GBP/USD is trading around flat for the start of the week as traders look ahead for what could be a busy month for the pair after the announcement of a £15bn support package for households across the UK, along with the central bank meetings and important economic data.

The Bank of England is expected to raise rates further at its June 16 meeting to combat the risk of self-perpetuating price rises.''Reconciling growth and inflation risks is a tough task for the BoE,'' analysts at Rabobank explained.

''That said, the Bank can be expected to want to urgently repair its inflation-fighting credibility. This is especially true in the wake of the criticism from Westminster which has triggered a defensive statement from BoE Governor Bailey, '' the analysts explained.

''He rejected the argument that the MPC “let demand get out of hand and stoked inflation” and made clear that the bank has not only raised rates four times so far in this cycle but is prepared to do so again based on the assessment at each of its meetings. Last week the MPC’s Pill made clear that the current challenges are an important reminder of the importance of price stability as an anchor for wider economic stability. This is evidence that his focus is firmly on inflation risks rather than growth.''

The current inflation focus of the BoE has been a focus of support for the pound. However, the economy will fall under the microscope this month as investors will look to the April Gross Domestic Product in the coming days, mid-June. Additionally, the pound is regarded as a risky currency and it is high beta to equities.

''Slowing growth in China and energy security risks in Europe could bolster safe-haven demand for the USD,'' analysts at Rabobank argued in this regard.

''In an environment in which the Fed and other central banks are removing liquidity, we expect higher levels of volatility in the FX market. We see risk that GBP/USD could again re-visit it recent lows in the coming months.''

The US dollar was mixed against its major trading partners around the final data of the week that included personal income and spending reports, the PCE price measures favoured by the Federal Reserve and the final reading of the May Michigan Sentiment index.

Reuters reported that ''Personal consumption expenditures rose by 0.9% in April after a 1.4% surge in March, lifted by gains in both goods and services spending. Core PCE prices rose by 0.3% for a third straight month, as expected, slowing the year-over-year rate to a still-brisk 4.9% from 5.2% in the previous month. Personal income was up 0.4% in April after larger gains in the previous two months, with transfer payments flat and wage and salary growth slower than in February and March.''

As for the Federal Reserve, comments from FOMC officials this week turned slightly dovish in terms of how fast rates should be lifted later in the year after an initial surge. In turn, the US dollar has been on the backfoot, despite expectations of an increase of 50 basis points for the June 14-15 meeting.

- Gold price looks to slip below $1,850.00 as the DXY may rebound ahead of jobless data.

- The US NFP is expected to print the job additions of 310k.

- A tight labor market may force the Fed to sound extremely hawkish in June monetary policy.

Gold price (XAU/USD) is expected to tumble below the crucial support of $1,850.00 on expectations of a rebound in the US dollar index (DXY) as a significant fall in an asset consecutively for two weeks is followed by a minor rebound. The precious metal remained stronger last week after a recovery move from the psychological support of $1,800.00. Investors put bets on the precious metal as the hangover of policy tightening got diluted.

This week investors will keep focusing on the US Employment Data. The labor market has remained stronger in the US economy unlike the other nations, which failed to generate sufficient job opportunities. The US Bureau of Labor Statistics will report the Nonfarm Payrolls (NFP) later this week. The US administration is expected to report the addition of 310k job opportunities this month against the prior print of 428k. While the Unemployment Rate is expected to remain stable at 3.6%. A higher-than-expected US NFP data may spurt a rally in the DXY as the occurrence will result in an extreme hawkish stance by the Federal Reserve (Fed).

Gold technical analysis

On a daily scale, gold bulls have attacked the 200-period Exponential Moving Average (EMA) at $1,856.60. Considering the action on the daily chart, a bear cross of 20- and 200-EMA near $1,855.00 looks likely. However, the Relative Strength Index (RSI) (14) is displaying an alternative action. The RSI (14) has shifted from the bearish range of 20.00-40.00 to the 40.00-60.00 range, which diminishes the downside bias. After interpreting the bear cross and neutral RSI (14), a future consolidation move looks likely.

Gold daily chart

-637894580457946484.png)

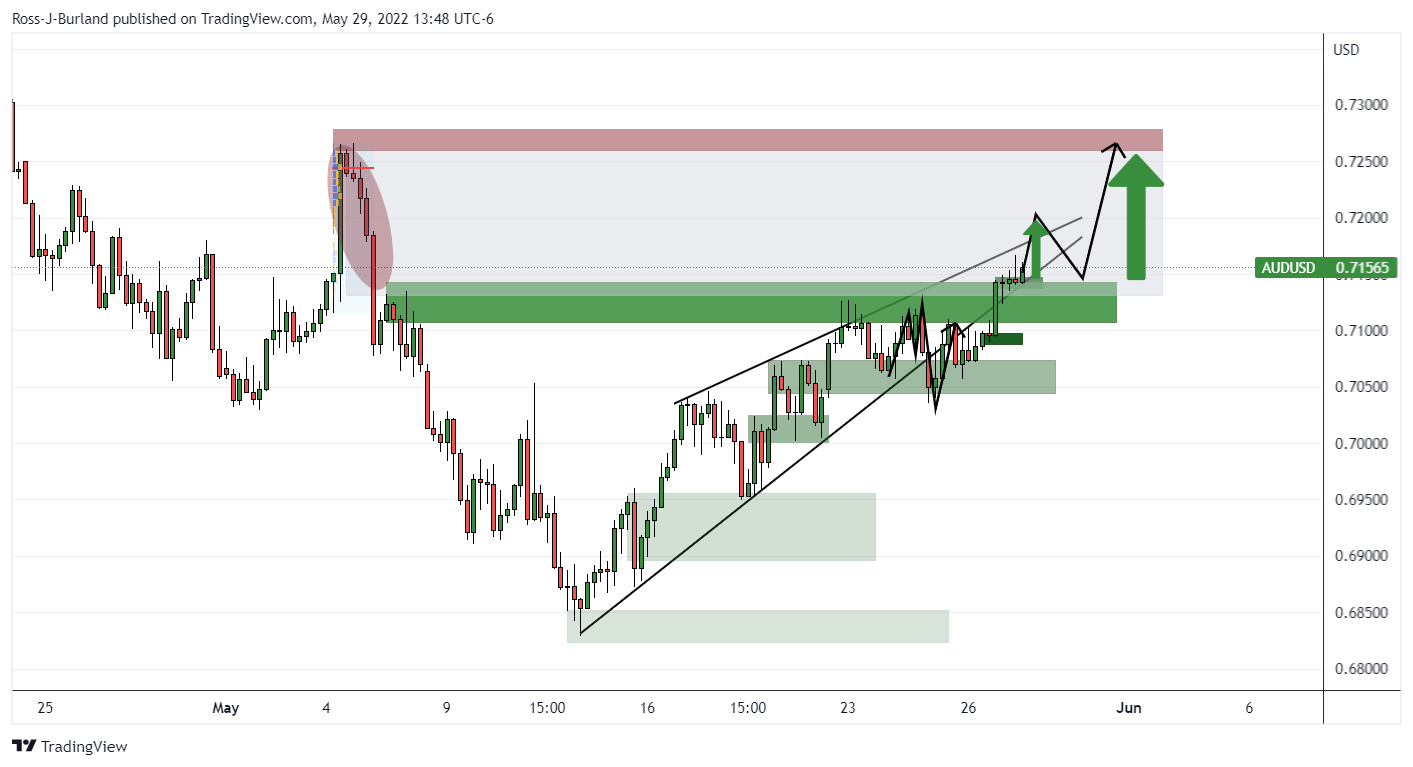

- AUD/USD bulls are poised for taking on a key area of imbalance on the H4 chart.

- Bulls can target the round 0.7250 for the opening sessions.

As per the prior analysis, AUD/USD Price Analysis: Bulls firming to test critical 0.71 the figure that guards a much stronger correction, the price has moved in on a key area on the charts that paths the way to a run towards 0.7250. The following illustrates the bullish bias for the opening sessions of the week.

AUD/USD prior analysis, H4 chart

It was stated last week that ''the bears tried to take control below the rising wedge, but the bulls firmed at horizontal support and have taken the bears back into the channel. The pull of the M-formation was too much for the bears and the bulls are testing the neckline near the current levels at 0.71 the figure. A break here will leave the bulls in good stead for a break of resistance around 0.7135 and a run of 0.7150 could open the way towards 0.7200 and then the 0.7260s and prior highs.''

AUD/USD live market

The price remains on course as illustrated, respecting the support structures in its pursuit of the price imbalance between recent highs and the May 4 highs at 0.7266. The price would be expected to mitigate this area of imbalance with relative ease.

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers