- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 04-09-2012

The euro fell versus the dollar and the yen amid speculation European Central Bank President Mario Draghi will announce measures as soon as this week to ease the region’s debt crisis.

Draghi said yesterday the bank’s primary mandate compels it to intervene in bond markets to wrest back control of interest rates and ensure the euro’s survival. The ECB announces its next policy decision on Sept. 6.

The 17-nation currency traded at almost the strongest in two months versus the dollar as European leaders stepped up shuttle diplomacy before erasing gains as global stocks declined.

European Union President Herman Van Rompuy traveled to Berlin for talks with German Chancellor Angela Merkel today as Italian Prime Minister Mario Monti hosts French President Francois Hollande in Rome.

Australia’s dollar climbed from a six-week low against the greenback after the Reserve Bank of Australia refrained from cutting the developed world’s highest benchmark rate.

The dollar briefly pared gains against major counterparts after a report showed manufacturing in the U.S. contracted for a third month.

European stocks retreated, paring yesterday’s biggest rally in a month, as investors awaited a report that may show U.S. manufacturing teetered between expansion and contraction in August.

The Institute for Supply Management’s factory index was little changed at 50 in August compared with 49.8 in July, according to the median estimate of 70 economists. A reading of 50 is the dividing line between contraction and expansion. Spending on construction projects probably rose in July, another release may show.

Euro-area countries will this week ask investors to stake more than 20 billion euros ($25 billion) on second-guessing the ECB, selling the most debt in more than three months before the central bank’s president, Mario Draghi, speaks on Sept. 6.

Spain, France, Austria and Belgium return to the market after a month-long pause, with Germany also selling debt. The auctions take place before the ECB’s meeting in Frankfurt, where Draghi may reveal details of a new bond-buying program.

The leaders of the single currency’s biggest economies hold further meetings this week as they brace for their central banker’s plan to defend the euro from bond-market turmoil. Draghi told the European Parliament yesterday he would be comfortable buying three-year government debt to bring down borrowing costs for nations in financial distress.

Vodafone slid 1.3 percent to 180.9 pence for the biggest contribution to the Stoxx 600’s retreat. Bernstein lowered the telecommunications company to market perform from outperform, meaning that investors should not buy more of the shares.

Ahold climbed 3 percent to 10.14 euros after the Dutch owner of the U.S. Stop & Shop grocery chain said it will take 6 to 12 months to review options for its stake in ICA. Ahold will probably return at least part of the proceeds from a sale to shareholders in the form of a buyback or special dividend, analysts at SNS Securities said in a note. They value the stake at 2.1 billion euros to 2.4 billion euros.

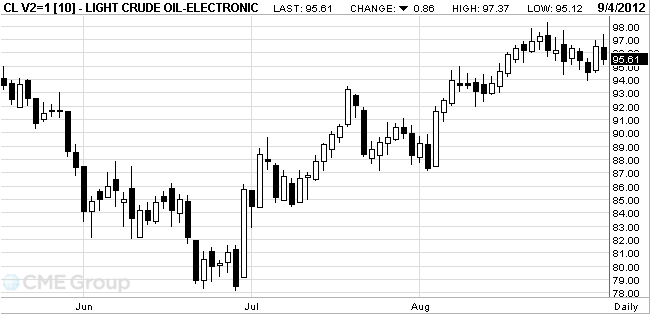

Oil fell as U.S. and euro-area manufacturing contracted in August, raising concern that slower economic growth will reduce oil demand.

Prices fell as much as 1.4 percent after the Institute for Supply Management’s U.S. factory index declined more than analysts forecast. In the euro area, manufacturing contracted more than initially estimated in August, London-based Markit Economics reported yesterday.

Moody’s Investors Service yesterday lowered the outlook on the European Union’s Aaa long-term bond rating to negative from stable yesterday, reflecting the risks to Germany, France, the U.K. and the Netherlands that account for about 45 percent of the group’s budget revenue, according to a company statement.

Oil for October delivery slipped to $95.12 a barrel on the New York Mercantile Exchange after rising to $97.37. Prices are down 3.3 percent this year.

There was no floor trading yesterday because of the U.S. Labor Day holiday, and transactions since the Aug. 31 close will be booked with today’s trades for settlement.

Brent oil for October settlement fell 85 cents, or 0.7 percent, to $114.93 a barrel on the London-based ICE Futures Europe exchange.

Gold prices close to the maximum level in six months due to long term liquidity injections by the central bank U.S.

Fed Chairman Ben Bernanke last week signaled that the central bank may take extraordinary measures to keep interest rates low, which caused a rise of commodity and stock markets. Experts believe that the rise in prices is holding back the possibility of disappointment the Fed or the European Central Bank.

In September, gold is usually more expensive - an average of over 44 years at 2.1 percent. In the near future direction of the market will determine the ECB and the Fed, central banks will have monthly meetings.

From the beginning, gold rose more than 8 percent.

September futures price of gold on the COMEX is now 1692.10 an ounce.

- For direct bank recapitalization ESM to create a single banking supervisory authority

- ECB may oversee banks only if the mandate to ensure price stability remains intact

- Lowering of interest rates in July, in some cases, no effect on the economy

- The euro may be stable only if its existence is not in doubt

EUR/USD $1.2500, $1.2540, $1.2550, $1.2600, $1.2700

USD/JPY Y78.00, Y78.45, Y79.00

EUR/JPY Y96.00

AUD/USD $1.0325

EUR/GBP stg0.8005

USD/CHF Chf0.9750, Chf0.9540

U.S. stock futures were little changed before a report on American manufacturing and as European leaders prepared for talks to address the debt crisis.

Global Stocks:

Nikkei 8,775.51 -8.38 -0.10%

Hang Seng 19,429.91 -129.30 -0.66%

Shanghai Composite 2,043.65 -15.50 -0.75%

FTSE 5,708.26 -50.15 -0.87%

CAC 3,430.71 -23.00 -0.67%

DAX 6,989.84 -24.99 -0.36%

Crude oil $96.68 +0,22%

Gold $1693.40 +0.34%

IBM upgraded to Overweight from Equal Weight at Barclays; tgt raised to $240 from $208.

Data

01:30 Japan Labor Cash Earnings, YoY July -0.6% -0.3% -1.2%

01:30 Australia Current Account, bln Quarter II -14.9 -12.3 -11.8

04:30 Australia Announcement of the RBA decision on the discount rate September 3.50% 3.50% 3.50%

04:30 Australia RBA Rate Statement -

05:45 Switzerland Gross Domestic Product (QoQ) Quarter II +0.7% +0.2% -0.1%

05:45 Switzerland Gross Domestic Product (YoY) Quarter II +2.0% +1.6% +0.5%

08:30 United Kingdom PMI Construction August 50.9 50.1 49.0

09:00 Eurozone Producer Price Index, MoM July -0.5% +0.3% +0.4%

09:00 Eurozone Producer Price Index (YoY) July +1.8% +1.6% +1.8%

During the session, the euro close to two-week high against the yen on speculation the European Central Bank President Mario Draghi announced a plan to buy bonds in the region, which will increase confidence in the currency.

The single currency rose for a third day against the dollar after a member of the European Parliament, Jean-Paul said yesterday that Draghi told lawmakers that he will buy bonds with maturities of up to three years.

The Australian dollar rose after the Reserve Bank at its meeting again refrained from cutting interest rates, which are the highest among the developed countries of the world at a political rally.

The pound fell against the dollar after the data has registered a decline in business activity index in the construction sector below 50, indicating contraction.

The dollar index (DXY), which is used to track the value of the dollar against six major currencies, was down by 0.1% to 81.165.

Sterling fell against the single currency on speculation that the European Central Bank President Mario Draghi will announce the details of the purchase of bonds in the political council this week to help in overcoming the debt crisis in the region. Also reported the decline in yield on 10-year UK government bonds.

The Swiss franc weakened against the dollar after it became known that the level of the Swiss GDP for the second quarter decreased by 0.1%, which was the first time in three quarters.

EUR / USD: during the European session the pair reached a high of $ 1.2626, and then fell to session lows

GBP / USD: the pair grown, updating the yesterday's high, but I could not hold out and fell to a session low below

USD / JPY: pair almost came close to the lowest level on Monday, and then grew up and is now trading at Y78.35

In the U.S. at 13:00 GMT will index of business activity in the manufacturing sector, 14:00 GMT - ISM manufacturing index for August and 20:30 GMT - the change in volume of crude oil, according to API. Finish the day at 23:30 GMT Australia data on the index of activity in the service sector of the AiG in August.

EUR/USD

Offers $1.2700, $1.2680, $1.2650, $1.2625/30

Bids $1.2585/80, $1.2555/50, $1.2520/15

AUD/USD

Offers $1.0380/90, $1.0350, $1.0325, $1.0300

Bids $1.0200, $1.0170, $1.0150

GBP/USD

Offers $1.6000, $1.5980, $1.5950, $1.5930/35

Bids $1.5855/50, $1.5830, $1.5820, $1.5800, $1.5765

EUR/JPY

Offers Y100.00, Y99.80, Y99.45/50

Bids Y98.55/50, Y98.00, Y97.85/80

USD/JPY

Offers Y78.90, Y78.80, Y78.60, Y78.50

Bids Y77.80, Y77.50

EUR/GBP

Offers stg0.8000, stg0.7980, stg0.7950

Bids stg0.7890

European stocks retreated after yesterday's rally most of the past month, as investors await data on the manufacturing index of the Institute for Supply Management U.S. in August. Also waiting for data on construction spending in the U.S..

International rating agency Moody's Investors Service affirmed the long-term rating of the European Union at the level of Aaa by changing the rating outlook from "stable" to "negative." In addition to "negative" outlook changed program-term bonds with a preliminary estimate of AAA. Such information is contained in the relevant report of the agency.

To date:

FTSE 100 5,715.07 -43.34 -0.75%

CAC 40 3,440.61 -13.10 -0.38%

DAX 7,004.87 -9.96 -0.14%

Vodafone Group Plc shares were down 1.3%, after Sanford C. Bernstein & Co. downgraded the operator. Royal Ahold NV gained 3% on rumors that it may sell its 60 percent stake in Scandinavian ICA, perhaps through an initial public offering.

May require action by the ECB to show irreversibility euro

ECB aid - not a substitute for fiscal reforms

There is no doubt that the ESM will be operational in the coming months

In the following weeks the situation should become clearer

- We need to know the conditions of assistance, before asking for it

EUR/USD $1.2500, $1.2540, $1.2550, $1.2600, $1.2700

USD/JPY Y78.00, Y78.45, Y79.00

EUR/JPY Y96.00

AUD/USD $1.0325

EUR/GBP stg0.8005

USD/CHF Chf0.9750, Chf0.9540

Asian stocks fell, with the regional benchmark index poised for its longest losing streak in six weeks, as the European Union’s outlook was cut by Moody’s Investors Service ahead of policy makers’ meetings. Australian shares declined as the central bank left the key rate unchanged.

Nikkei 225 8,775.51 -8.38 -0.10%

S&P/ASX 200 4,303.5 -26.17 -0.60%

Shanghai Composite 2,040.09 -19.05 -0.93%

Hutchison Whampoa Ltd., an operator of retail chains that gets 55 percent of its revenue in Europe, fell 0.2 percent in Hong Kong.

Westpac Banking Corp., Australia’s second-biggest lender by market value, slid 2.3 percent.

Agile Property Holdings Ltd. declined 5.7 percent in Hong Kong as its rating was cut at DBS Vickers after its chairman was arrested.

01:30 Japan Labor Cash Earnings, YoY July -0.6% -0.3% -1.2%

01:30 Australia Current Account, bln Quarter II -14.9 -12.3 -11.8

04:30 Australia Announcement of the RBA decision on the discount rate September 3.50% 3.50% 3.50%

04:30 Australia RBA Rate Statement

The euro gained against the yen on speculation European Central Bank President Mario Draghi’s plan to buy bonds of debt-saddled nations in the region will bolster confidence in the single currency.

The 17-nation euro rose versus most of its major peers and approached a two-month high against the dollar before European Union President Herman Van Rompuy meets with German Chancellor Angela Merkel today in Berlin for talks and Italian Prime Minister Mario Monti welcomes French President Francois Hollande to Rome.

The EU’s rating outlook was cut to negative by Moody’s Investors Service yesterday, reflecting the risks to Germany, France, the U.K. and the Netherlands that account for about 45 percent of the group’s budget revenue.

Australia’s dollar halted a decline from yesterday after the nation’s Reserve Bank left its benchmark interest rate unchanged at a developed-world high today.

EUR/USD: during the Asian session, the pair rose above $1.2600.

GBP/USD: during the Asian session, the pair rose to a yesterday's high to $1.5900 .

USD/JPY: during the Asian session, the pair rose to Y78.40.

Scheduled European data starts at 0700GMT with unemployment data from Spain. Core-European data continues at 0900GMT with industrial PPI for July. Later, at 1300GMT, ECB Executive Board member Joerg Asmussen is due to speak on regulatory challenges and the debt crisis, in Frankfurt. In the UK, at 0830GMT, Markit/CIPS Construction PMI data is due. US data includes domestic-made light vehicle sales, which are expected to rise to an 11.2 million annual rate in August after slowing modestly in July. Markit final US PMI data for August is due at 1258GMT, while at 1330GMT the weekly MNI Capital Goods Index is due. US data at 1400GMT includes the August ISM Manufacturing Index and July Construction Spending data.

Yesterday the euro traded in a narrow range against the U.S. dollar in relation to the output in the U.S. and Canada. Against this background, the market activity is quite low.

The yen rose against higher-yielding currencies such as the Australian and New Zealand dollar as signs of a global economic downturn caused demand for safe assets.Japan's currency strengthened against 13 of its 16 major counterparts after a report showed the euro zone, that index of business activity in the manufacturing sector declined in August. Revealed a reduction in the activity index non-manufacturing sector of China.

The Australian dollar fell to a five-week low against the U.S. dollar after retail sales declined. Federal Reserve Chairman Ben Bernanke said last week that we should not exclude stimulate growth.

The pound rose against the euro and the dollar after data showed that the level of production in the UK fell less than economists forecast.

Asian stocks outside Japan rose as economic reports across the region fueled speculation that central banks will boost stimulus measures. Japanese stocks fell as the yen rose against most of its major counterparts, weighing on the earnings outlook for exporters.

Nikkei 225 8,783.89 -56.02 -0.63%

S&P/ASX 200 4,329.7 +13.59 +0.31%

Shanghai Composite 2,057.68 +10.16 +0.50%

James Hardie Industries SE, a building-materials supplier that gets 67 percent of sales from the U.S., rose 1.2 percent in Sydney.

Canon Inc., a camera maker that gets 31 percent of its revenue in Europe, lost 1.7 percent.

Shimao Property Holdings Ltd. paced gains among Chinese developers on a report the nation should do more to help economic growth.

Samsung Card Co. soared 15 percent in Seoul after the credit-card issuer said it will buy back shares.

European stocks rose for a second day and copper advanced on speculation central banks will take more steps to boost growth as reports signaled the economic slowdown is deepening. Spain’s bonds gained and emerging-market shares climbed the most in a week.

Euro-area manufacturing contracted more than initially estimated in August and China’s factory output unexpectedly shrank for the first time in nine months, according to reports from London-based Markit Economics today and a government survey in Beijing Sept. 1. Federal Reserve Chairman Ben S. Bernanke said Aug. 31 that he wouldn’t rule out more stimulus. European Central Bank President Mario Draghi may unveil details of his bond-purchase program after a policy meeting Sept. 6.

The Stoxx 600 rebounded from two weeks of losses, the first back-to-back declines since May. BHP Billiton Ltd. and Rio Tinto Group led a rally in mining companies.

U.S. financial markets closed on Monday in observance of Labor Day

Change % Change Last

Nikkei 225 8,783.89 -56.02 -0.63%

S&P/ASX 200 4,329.7 +13.59 +0.31%

Shanghai Composite 2,057.68 +10.16 +0.50%

FTSE 100 5,753.98 +42.50 +0.74%CAC 40 3,448.7 +35.63 +1.04%

DAX 7,008.67 +37.88 +0.54%

Dow closed

Nasdaq closed

S&P 500 closed

(pare/closed(00:00 GMT +02:00)/change, %)

EUR/USD $1,2587 +0,10%

GBP/USD $1,5882 +0,11%

USD/CHF Chf0,9539 -0,09%

USD/JPY Y78,29 -0,08%

EUR/JPY Y98,54 -0,02%

GBP/JPY Y124,33 -0,01%

AUD/USD $1,0243 -0,78%

NZD/USD $0,7975 -0,71%

USD/CAD C$0,9858 -0,03%01:30 Japan Labor Cash Earnings, YoY July -0.6% -0.3%

01:30 Australia Current Account, bln Quarter II -14.9 -12.3 -11.8

04:30 Australia Announcement of the RBA decision on the discount rate September 3.50% 3.50%

04:30 Australia RBA Rate Statement -

05:45 Switzerland Gross Domestic Product (QoQ) Quarter II +0.7% +0.2%

05:45 Switzerland Gross Domestic Product (YoY) Quarter II +2.0% +1.6%

07:00 United Kingdom Halifax house price index August -0.6% +0.3%

07:00 United Kingdom Halifax house price index 3m Y/Y August -0.6% -0.8%

08:30 United Kingdom PMI Construction August 50.9 50.1

09:00 Eurozone Producer Price Index, MoM July -0.5% +0.3%

09:00 Eurozone Producer Price Index (YoY) July +1.8% +1.6%

14:00 U.S. ISM Manufacturing August 49.8 50.1

14:00 U.S. Construction Spending, m/m July +0.4% +0.4%

23:30 Australia AIG Services Index August 46.5

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers