- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 18-09-2012

The euro continues to decline in the dollar and yen, despite the figures exceeded expectations of confidence of investors and analysts to the German economy and the euro zone.

Index of investor and analyst expectations for the economy in Germany for the next six months (confidence index) calculated by research institute ZEW, rose in September for the first time in 5 months - to minus 18.2 points from minus 25.5 points in August. However, the value of the indicator remains negative, which is not inspired investors. Index of investors and analysts to the current situation in the German economy in September, down from 18.2 points to the lowest since June 2010, 12.6 points. Analysts on average forecast a rise of the first indicator to minus 20 points and the second reduction to 18 points. Overall, for the euro area index was -3.8 -16.3 points at the forecast.

Also today it was announced that Spanish borrowing costs fell at today's auction, the first once since the European Central Bank on September 6, announced plans to buy government debt in the region to contain borrowing costs.

The demand for the yen is still limited due to the forecasts, the Bank of Japan will take an intervention after a meeting on September 17-18. More active than an intervention, investors expect the Bank of Japan's new measures to support the economy after the Federal Reserve and the European Central Bank.

The Bank of Japan increased the size of the fund to buy assets such as government debt by 5 trillion yen to 45 trillion yen in July, and continued to hold the interest rate at around 0.1%, which was established in October 2010.

European stocks declined the most in two weeks as investors bet that the rally in the Stoxx Europe 600 Index to a 15-month high overshot the economic outlook and prospects for corporate earnings.

German investor confidence rose for the first time in five months in September, a report showed today.

The ZEW Center for European Economic Research in Mannheim said its index of investor and analyst expectations, which aims to predict economic developments six months in advance, climbed to minus 18.2 from minus 25.5 in August. Economists forecast a gain to minus 20.

National benchmark indexes fell in 15 of the 18 western European markets. Germany’s DAX slid 0.8 percent, while the U.K.’s FTSE 100 lost 0.4 percent. France’s CAC 40 dropped 1.2 percent.

Akzo Nobel dropped 5.5 percent to 46.16 euros, the biggest decline since September 2011. Buechner will take leave for one month to recuperate from fatigue on the advice of his doctor, Amsterdam-based Akzo said. He plans to return in the first half of October and Chief Financial Officer Keith Nichols will be the point-person in the interim period.

Aviva lost 4 percent to 344.9 pence. Deutsche Bank AG downgraded the stock to hold from buy and Bank of America Corp. cut its rating to underperform, the equivalent of sell, from neutral.

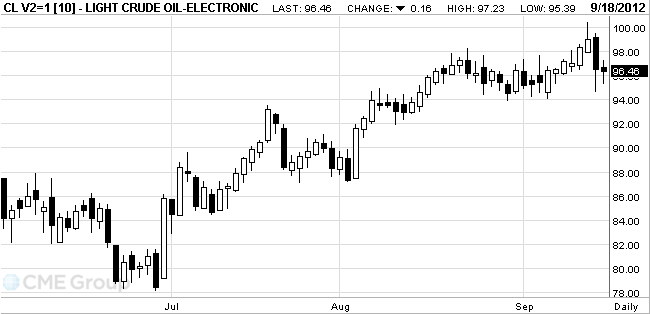

Oil declined for a second day in New York, extending its biggest drop in two months, on concern that a U.S. economic slowdown may curb demand in the world’s largest consumer of crude.

Futures fell as much as 1.3 percent, deepening yesterday’s 2.4 percent loss. Crude tumbled almost $4 in three minutes yesterday before the expiry of October options contracts. The Federal Reserve Bank of New York’s general economic index, known as the Empire State Index, fell to a three-year low. Saudi Arabia is taking action to reduce oil prices, a Persian Gulf official with knowledge of the matter said today.

Oil for October delivery fell as much as $1.23 to $95.39 a barrel in electronic trading on the New York Mercantile Exchange.

Brent crude for November settlement fell 30 cents to $113.49 on the London-based ICE Futures Europe exchange. It dropped 2.5 percent yesterday.

Gold cheaper together with shares, oil and the euro due to profit taking following the price increase to a maximum of 6.5 months last week.

Last week, the price rose by 2 percent a day after the U.S. Federal Reserve announced the start of the third stage of "quantitative easing" - buying mortgage-bonds to $ 40 billion a month.

In Europe, investors focused on concerns regarding the banking system in Spain and Greece's ability to make budget cuts necessary to obtain further financial support.

October futures price of gold on the COMEX is now 1766.4 dollars per ounce.

EUR/USD $1.3000, $1.3100, $1.3100, $1.3130-35, $1.3150, $1.3230

USD/JPY Y78.75, Y78.50, Y78.30, Y78.00, Y77.50, Y77.20

GBP/USD $1.6200, $1.6000

EUR/GBP stg0.8075

AUD/USD $1.0450, $1.0500, $1.0600

U.S. stock futures are mixed as investors watched European leaders’ efforts to resolve their debt crisis.

FedEx reduced its profit outlook for the year through May after quarterly earnings dropped for the first time in almost three years amid reduced demand for premium shipping services.

Global Stocks:

Nikkei 9,123.77 -35.62 -0.39%

Hang Seng 20,601.93 -56.18 -0.27%

Shanghai Composite 2,059.54 -18.96 -0.91%

FTSE 5,865.57 -27.95 -0.47%

CAC 3,531.81 -21.88 -0.62%

DAX 7,365.11 -38.58 -0.52%

Crude oil $96.12 -0,52%

Gold $1767.57 -0.18%

Intel (INTC) downgraded to Sector Perform from Outperform at RBC Capital

Alcoa (AA) downgraded to Hold from Buy at Jefferies

Data

01:30 Australia RBA Meeting's Minutes -

02:30 Australia RBA Assist Gov Debelle Speaks -

05:45 Switzerland SECO Economic Forecasts IV quarter

08:30 United Kingdom HICP, m/m August +0.1% +0.5% +0.5%

08:30 United Kingdom HICP, Y/Y August +2.6% +2.5% +2.5%

08:30 United Kingdom HICP ex EFAT, Y/Y August +2.3% +2.2% +2.1%

08:30 United Kingdom Retail Price Index, m/m August +0.1% +0.5% +0.4%

08:30 United Kingdom Retail prices, Y/Y August +3.2% +3.0% +2.9%

08:30 United Kingdom RPI-X, Y/Y August +3.2% +3.0% +2.9%

09:00 Germany ZEW Survey - Economic Sentiment September -25.5 -19.4 -18.2

09:00 Eurozone ZEW Economic Sentiment September -21.2 -16.3 -3.8%

09:30 United Kingdom BOE Inflation Letter September

The euro continued its decline from the four-month high against the dollar and the yen after a survey showed that German investor sentiment remained negative this month amid fading optimism in resolving the debt crisis.

The single currency weakened against all but two of its 16 major counterparts as European stocks fell on fears that there may be a delay in the provision of financial resources to Spain that it needs to solve its financial problems.

The Australian dollar continued its decline yesterday after the policy stated that the strong currency has the expense of economic growth. Also, there are rumors that soon the bank may seek to lower the interest rate.

Also today it was announced that Spanish borrowing costs fell at today's auction, the first once since the European Central Bank on September 6, announced plans to buy government debt in the region to contain borrowing costs.

The yen rose against all but one of the 16 major currencies, as the central bank of Japan began its two-day meeting. Some economists predict that the Bank will announce the introduction of further measures to mitigate the monetary policy.

The Bank of Japan increased the size of the fund to buy assets such as government debt by 5 trillion yen to 45 trillion yen in July, and continued to hold the interest rate at around 0.1%, which was established in October 2010.

The Swiss franc has appreciated even after the government's expert group has cut its growth forecast for this year and next year on the background of the fact that the debt crisis in the eurozone affects the slowdown in exports.

EUR / USD: during the European session, the pair has fallen by more than half the figure, and is now trading at $ 1.3055

GBP / USD: the pair is trading in a narrow range at maximum

USD / JPY: the pair is trading without a trend and is now at Y78.63

At 12:30 GMT the United States will report on the balance of the current account balance of payments for the 2nd quarter. At 13:00 GMT, the U.S. announced on net purchases of long-term U.S. securities by foreign investors and the total net purchases of U.S. securities by foreign investors in July. At 20:30 GMT the U.S. become aware of changes in the volume of crude oil, according to the API for September. At 22:45 GMT New Zealand, there are data on the balance of the current account balance of payments against the current account deficit to GDP and Gross Domestic Product for the second quarter.

Germany's export sector is expected to suffer from the decline in external demand

The deterioration of the economic situation will be rather moderate

Experts predict that the German economy will lose momentum in the next 6 months

The decision of the Constitutional Court of Germany did not affect the ZEW index

The debt crisis remains a risk to economic activity

The debt crisis is not resolved

EUR/USD

Offers $1.3170/75, $1.3130-35

Bids $1.3020/00, $1.2980, $1.2950, $1.2935/30, $1.2900, $1.2855/50

AUD/USD

Offers $1.0670, $1.0585/90, $1.0540/50

Bids $1.0405/00, $1.0350/40

GBP/USD

Offers $1.6330/35, $1.6300, $1.6280, $1.6273

Bids $1.6220-00, $1.6180/70, $1.6150/40, $1.6120, $1.6085/80

EUR/JPY

Offers Y103.80/4.00, Y103.40/60

Bids Y102.50/40, Y100.80/60, Y100.50

USD/JPY

Offers Y79.50, Y78.80-9.00

Bids Y78.48, Y78.00/7.90

EUR/GBP

Offers stg0.8200, stg0.8180, stg0.8150

Bids stg0.8020/00, stg0.7970, stg0.7945/40

European stock indexes began trading lower. At the end of this affected euphoria over the start QE3, slow pace of China to take measures to stimulate economic growth, unrest in China, which led to the suspension of the Japanese factories in the Chinese territory, the protests in Spain against the budget measures.

Currently already published data on the sentiment index in the business environment of the euro area institution ZEWza September. Figure was -3.8%, forecast -16.3 points. The value of the same index for Germany was -18.2 -19.4 points at the forecast.

Today, the focus of the market is the upcoming publication of data on the U.S. balance of payments for the II quarter, net purchases of U.S. securities by foreign investors in July, and the index of the state of the U.S. housing market by NAHB in September.

FTSE 100 5,842.53 -50.99 -0.87%

CAC 40 3,506.34 -47.35 -1.33%

DAX 7,322.37 -81.32 -1.10%

Shares of Akzo Nobel NV, fell to eight-month low after CEO Ton Beuchner went on sick leave. Paper Aviva Plc fell 4.5% after analysts downgraded the shares. Renault SA capitalization fell due to lower vehicle sales in August. Shares of Unilever and Diageo Plc rose 1% after analysts raised their rating on the stock.

EUR/USD $1.3000, $1.3100, $1.3100, $1.3130-35, $1.3150, $1.3230

USD/JPY Y78.75, Y78.50, Y78.30, Y78.00, Y77.50, Y77.20

GBP/USD $1.6200, $1.6000

EUR/GBP stg0.8075

AUD/USD $1.0450, $1.0500, $1.0600

Sold E4.576bln vs target E3.5-E4.5bln

E3.557bln 12-month Letra; bid-to-cover 2.03 (1.91)

E1.019ln 18-month Letra; bid-to-cover 3.56 (3.98)

Sold 12-month Letra at avg yield 2.835% vs 3.07% prev

Sold 18-month Letra at avg yield 3.072% vs 3.335% prev

Asian stocks fell as rising tensions between Japan and China pushed down shares of Tokyo- listed companies from Honda Motor Co. to Fast Retailing Co. amid signs of slowing growth in the U.S. and a worsening European debt crisis.

Nikkei 225 9,123.77 -35.62 -0.39%

S&P/ASX 200 4,394.7 -7.83 -0.18%

Shanghai Composite 2,059.54 -18.96 -0.91%

BHP Billiton Ltd., the world’s largest mining company, slid 0.6 percent in Sydney as metal prices dropped.

Fast Retailing, Asia’s biggest apparel chain, tumbled 7 percent, in Tokyo as it was forced to shut stores in China amid anti-Japanese protests.

Hokuriku Electric Power Co. surged 6.4 percent after a Japanese government minister signaled he has no plans to stop construction of nuclear reactors.

01:30 Australia RBA Meeting's Minutes -

02:30 Australia RBA Assist Gov Debelle Speaks

The euro weakened versus most of its major peers before a German report forecast to show investor confidence hovered near the lowest level this year. Germany’s ZEW Center for European Economic Research is forecast to say its index of investor and analyst expectations, which aims to predict economic developments six months in advance, was at minus 20 in September, according to a Bloomberg News survey of economists. The gauge slid to minus 25.5 last month, the lowest this year.

The euro’s 14-day relative strength index versus the dollar and the yen remained above 70 today, a level that some traders see as a sign that an asset price may be about to reverse course.

The yen was close to a one-week low against the dollar amid speculation the Bank of Japan will expand monetary stimulus to rein in currency strength that hurts exporters. In Japan, the central bank is set to begin a two-day policy meeting today. Five of 21 economists surveyed by Bloomberg predict policy makers will announce further easing tomorrow, with sixteen expecting a move by October.

The Australian dollar held onto a decline from yesterday after minutes of the Reserve Bank’s meeting this month showed officials saw the currency’s strength as a risk to the economy, signaling scope to cut interest rates.

EUR / USD: during the Asian session, the pair traded in the range of $1.3085-15.

GBP / USD: during the Asian session, the pair traded in the range of $1.6230-60.

USD / JPY: during the Asian session, the pair traded in the range of Y78.45-75.

At 0900GMT, Germany's Sep ZEW survey is released. At 0830GMT, UK Aug Consumer Prices numbers are released. Energy prices look likely to drive inflation higher in the near term than the Bank of England's Monetary Policy Committee had forecast in its August Inflation Report.

Yesterday the euro rose against the dollar to a maximum of the beginning of May, after the September manufacturing activity in the area of the Federal Reserve Bank of New York dropped more than expected by a decline in orders. General economic index of the New York Fed declined to -10.41 versus -5.85 in August, reaching the lowest level since April 2009 values. Economists had expected a drop to -2. Factories slow conveyors weakened exports, limited business investment and lower household spending. Unemployment rate is more than 8% over three years, and the weakening of the economy this year to explain what the Fed policymakers who decided to additional stimulus during a recent meeting.

Earlier, the euro weakened against the yen and the U.S. dollar for the first time in five days amid unrest in Spain, and after the Spanish Prime Minister Mariano Rajoy said that Spain may need financial assistance. As market participants expect the meeting, the Prime Minister of Spain with the Prime Minister of Italy, Mario Monti, to be held in Rome on 21 September. The next day, German Chancellor Angela Merkel will hold talks with French President François Hollande. The single currency fell against most of its 16 major counterparts after European leaders last week in Cyprus to discuss the terms of salvation and the role of the European Central Bank. Euro also declined following the demonstrations in Madrid, which took place two days and were directed against the additional austerity measures.

The dollar rose against the yen on expectations of intervention by the Japanese authorities.

British pound updated four month high against the dollar on optimism about the third round of quantitative easing from the Fed.

Most Asian stocks outside Japan and China rose, led by mining companies, amid speculation U.S. stimulus measures will boost global demand. Shares in Shanghai and Hong Kong retreated as Citigroup Inc. cut its 2013 growth outlook for China.

Nikkei 225 closed

S&P/ASX 200 4,402.5 +12.54 +0.29%

Shanghai Composite 2,085.17 -38.67 -1.82%

BHP Billiton Ltd. the world’s largest mining company, climbed 2.5 percent in Sydney as rising metals prices boosted raw-material companies.

Some Chinese car sellers dropped as anti-Japan protests turned violent over the weekend.

European stocks declined from a 15- month high as concern of a deepening economic slowdown in China overshadowed optimism resulting from the Federal Reserve’s third round of quantitative easing.

Citigroup Inc. cut its forecast for China’s 2013 growth to 7.6 percent from 8 percent on weakening external demand. Separately, the official Xinhua News Agency said China needs to be more cautious with its monetary policies as quantitative easing in the U.S. will create more pressure to control inflation.

National benchmark indexes fell in all of the 18 western European markets, except Belgium. Germany’s DAX slipped 0.1 percent, the U.K.’s FTSE 100 (UKX) declined 0.4 percent, while France’s CAC 40 dropped 0.8 percent.

SSAB (SSABA) tumbled 6.9 percent to 53.05 kronor, the biggest decline since February. The steelmaker said demand for strip products has been much weaker than expected in the third quarter and warned that falling iron ore prices are expected to hurt earnings in the first quarter of next year.

H&M (HMB) declined 1.6 percent to 243.20 kronor as Europe’s second-largest clothing retailer reported third-quarter sales that missed analysts’ estimates after an August heatwave in some parts of the region hurt business. Revenue excluding value-added tax rose to 28.8 billion kronor ($4.4 billion) through Aug. 31, the Stockholm-based company said, missing the 29.8 billion-kronor average estimate. Sales at stores open at least a year declined 4 percent in August.

Major U.S. stock indexes spent trading in negative territory in a small minus, consolidating after rising last week in the highs.

The pressure on the index was published index of activity in the manufacturing sector of the New York Fed, which in September unexpectedly fell to -10.4 vs. -5.85 in August and forecast -1.9.

However, the negative trend has more to do not with the weak data, and with a reduction in euphoria about to launch a new round of quantitative easing. Stock indexes are at multi-year highs - levels that are not very attractive to buy. Moreover, the recent increase in the indices was not caused by fundamental factors, and the actions of central banks of the U.S. and Europe. In the near future the focus of market participants will shift to the upcoming earnings season, which, given the further deterioration in the global economy, it may be weak. Against this background, markets may substantially adjusted to the levels achieved.

As a part of most of the components of the index DOW dropped in price. In the plus side there are only 9 components, among which more than other stocks rose Pfizer (PFE, +0.88%). More than the others fell in the share price Alcoa (AA, -2,54%) and Bank of America (BAC, -2.21%).

Most of the major economic sectors are reduced. The plus is just the health sector (+0.4%). More than the others fell in value conglomerates sector (-1.1%).

Iron ore miner Cliffs Natural Resources dipped 7.0% after analysts at JPMorgan downgraded the stock from "Outperform" to "neutral."

Shares of high-tech giant Apple gained 1.1% - orders for the new iPhone 5 has already exceeded 2 million.

Manufacturer of electric Tesla Motors rose by 7.0% on the news of increasing its stock investment rating analysts Morgan Stanley to "Underperform" to "Outperform."Change % Change Last

Oil $98.10 -0.21 -0.21%

Gold $1,767.00 -5.10 -0.29%Change % Change Last

Nikkei 225 closed

S&P/ASX 200 4,402.5 +12.54 +0.29%

Shanghai Composite 2,085.17 -38.67 -1.82%

FTSE 100 5,893.52 -22.03 -0.37%

CAC 40 3,553.69 -27.89 -0.78%

DAX 7,403.69 -8.44 -0.11%

Dow 13,553 -40 -0.30%

Nasdaq 3,179 -5 -0.16%

S&P 500 1,461 -5 -0.33%

(pare/closed(00:00 GMT +02:00)/change, %)

EUR/USD $1,3113 -0,12%

GBP/USD $1,6247 +0,19%

USD/CHF Chf0,9274 +0,08%

USD/JPY Y78,72 +0,43%

EUR/JPY Y103,23 +0,30%

GBP/JPY Y127,88 +0,63%

AUD/USD $1,0470 -0,74%

NZD/USD $0,8264 -0,28%

USD/CAD C$0,9746 +0,30%

01:30 Australia RBA Meeting's Minutes -

02:30 Australia RBA Assist Gov Debelle Speaks -

05:45 Switzerland SECO Economic Forecasts IV quarter

08:30 United Kingdom HICP, m/m August +0.1% +0.5%

08:30 United Kingdom HICP, Y/Y August +2.6% +2.5%

08:30 United Kingdom HICP ex EFAT, Y/Y August +2.3% +2.2%

08:30 United Kingdom Retail Price Index, m/m August +0.1% +0.5%

08:30 United Kingdom Retail prices, Y/Y August +3.2% +3.0%

08:30 United Kingdom RPI-X, Y/Y August +3.2% +3.0%

09:00 Germany ZEW Survey - Economic Sentiment September -25.5 -19.4

09:00 Eurozone ZEW Economic Sentiment September -21.2 -16.3

09:30 United Kingdom BOE Inflation Letter September

12:30 U.S. Current cccount, bln Quarter II -137 -126

13:00 U.S. Net Long-term TIC Flows July 9.3 45.3

13:00 U.S. Total Net TIC Flows July 16.7

14:00 U.S. NAHB Housing Market Index September 37 38

22:45 New Zealand Current Account Quarter II -1.31 -1.63

23:45 U.S. FOMC Member Laker Speaks -

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers