- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 24-01-2019

| Time | Country | Event | Period | Previous value | Forecast |

|---|---|---|---|---|---|

| 09:00 | Germany | IFO - Current Assessment | January | 104.7 | 104.2 |

| 09:00 | Germany | IFO - Expectations | January | 97.3 | 97.0 |

| 09:00 | Germany | IFO - Business Climate | January | 101 | 100.6 |

| 09:30 | United Kingdom | BBA Mortgage Approvals | December | 39.403 | 39.0 |

| 11:00 | United Kingdom | CBI retail sales volume balance | January | -13 | 2 |

| 14:00 | Belgium | Business Climate | January | -0.9 | -1.5 |

| 18:00 | U.S. | Baker Hughes Oil Rig Count | January | 852 |

Major US stock indices closed mixed: Nasdaq rose moderately against the backdrop of rising prices for chip manufacturers and airlines, while the Dow Industrials and S & P 500 were under pressure due to concerns about the Sino-US trade dispute and the longest US government closing.

In addition, investors analyzed data for the United States. The Department of Labor said that the number of Americans applying for unemployment benefits fell to a more than 49-year low, but this decline probably overestimates the state of the labor market, as expected, in several states, including California. The initial volume of claims for unemployment benefits fell from 212,000 to 199,000 seasonally adjusted for the week ending January 19. This is the lowest level since mid-November 1969, when 197,000 applications were registered. Economists have predicted that the number of applications will be 220,000. The number of federal workers who have applied for unemployment benefits rose by 14,965 to 25,419 in the week to 12 January. Re-applications for benefits decreased by 24,000 to 1.71 million in the week to January 12. The 4-week follow-up moving average increased by 1,250 to 1.73 million.

Meanwhile, the Conference Board data showed that in December, the leading indicators index (LEI) for the USA decreased by 0.1 percent, to 111.7 (2016 = 100), after increasing by 0.2 percent in November and falling by 0, 3 percent in October. The leading economic index now significantly exceeds the previous peak at 102.4, set in March 2006. "The leading index declined slightly in December, and the recent LEI moderation suggests that US economic growth may slow this year. Although the effects of government closures are not yet reflected, LEI suggests that the economy may slow to 2 percent by the end of 2019 growth, ”said Ataman Ozildirim, director and chairman of the global research council of the Conference.

Most of the DOW components recorded a decline (17 of 30). The growth leader was shares of Intel Corporation (INTC, + 3.80%). The outsider was Merck & Co., Inc. (MRK, -3.01%).

Most sectors of the S & P ended in a plus. The largest growth was shown by the technology sector (+ 0.8%), the largest decrease was by the health sector (-0.8%).

At the time of closing:

Dow 24,553.24 -22.38 -0.09%

S&P 500 2,642.33 +3.63 +0.14%

Nasdaq 100 7,073.46 +47.70 +0.68%

| Time | Country | Event | Period | Previous value | Forecast |

|---|---|---|---|---|---|

| 09:00 | Germany | IFO - Current Assessment | January | 104.7 | 104.2 |

| 09:00 | Germany | IFO - Expectations | January | 97.3 | 97.0 |

| 09:00 | Germany | IFO - Business Climate | January | 101 | 100.6 |

| 09:30 | United Kingdom | BBA Mortgage Approvals | December | 39.403 | 39.0 |

| 11:00 | United Kingdom | CBI retail sales volume balance | January | -13 | 2 |

| 14:00 | Belgium | Business Climate | January | -0.9 | -1.5 |

| 18:00 | U.S. | Baker Hughes Oil Rig Count | January | 852 |

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) increased by 8.0 million barrels from the previous week. At 445.0 million barrels, U.S. crude oil inventories are about 9% above the five year average for this time of year.

Total motor gasoline inventories increased by 4.1 million barrels last week and are about 6% above the five year average for this time of year. Finished gasoline and blending components inventories both increased last week.

Distillate fuel inventories decreased by 0.6 million barrels last week and are about 2% below the five year average for this time of year. Propane/propylene inventories decreased by 3.7 million barrels last week and are about 2% above the five year average for this time of year. Total commercial petroleum inventories increased last week by 6.7 million barrels last week.

At 54.5 in January, up fractionally from 54.4 in December, the seasonally adjusted IHS Markit Flash U.S. Composite PMI Output Index was well above the 50.0 no-change value. The latest reading was close to the average seen over the final quarter of 2018 (54.7) and signalled robust expansion of private sector output at the beginning of 2019. The composite index is based on original survey data from the IHS Markit U.S. Services PMI and the IHS Markit U.S. Manufacturing PMI

Commenting on the flash PMI data, Chris Williamson, Chief Business Economist at IHS Markit said: “US businesses reported a solid start to 2019, with the rate of expansion running only slightly weaker than the average seen in the second half of last year. “The resilience of the survey data suggest little impact from the government shutdown on the private sector, with very few companies reporting any material detrimental impact on their output or order books. “Historical comparisons suggest January’s survey data are indicative of the economy growing at an annualised rate close to 2.5%. However, as the survey does not include the government sector, the impact of the shutdown may not be fully captured”.

Before the bell: S&P futures -0.03%, NASDAQ futures +0.30%

U.S. stock-index were mixed on Thursday, as investors digested the comments by the U.S. Commerce Secretary Wilbur Ross that the United States and China were “miles and miles” from resolving their trade dispute.

Global Stocks:

Index/commodity | Last | Today's Change, points | Today's Change, % |

Nikkei | 20,574.63 | -19.09 | -0.09% |

Hang Seng | 27,120.98 | +112.78 | +0.42% |

Shanghai | 2,591.69 | +10.69 | +0.41% |

S&P/ASX | 5,865.70 | +22.00 | +0.38% |

FTSE | 6,810.62 | -32.26 | -0.47% |

CAC | 4,856.48 | +16.10 | +0.33% |

DAX | 11,076.33 | +4.79 | +0.04% |

Crude | $52.48 | -0.27% | |

Gold | $1,285.00 | -0.40% |

If risks persists, momentum will be weak for longer

Cites slowdown in China,m waning US fiscal stimulus

Likelihood of recession is very low

The ECB has given itself more time to assess risks

(company / ticker / price / change ($/%) / volume)

ALCOA INC. | AA | 28.19 | -0.11(-0.39%) | 1250 |

ALTRIA GROUP INC. | MO | 44.6 | -0.10(-0.22%) | 6599 |

Amazon.com Inc., NASDAQ | AMZN | 1,638.52 | -1.50(-0.09%) | 35962 |

Apple Inc. | AAPL | 153.8 | -0.12(-0.08%) | 118907 |

AT&T Inc | T | 30.98 | 0.09(0.29%) | 12691 |

Boeing Co | BA | 357 | -1.61(-0.45%) | 4567 |

Caterpillar Inc | CAT | 131.87 | 0.05(0.04%) | 8343 |

Cisco Systems Inc | CSCO | 45.68 | 0.22(0.48%) | 18582 |

Citigroup Inc., NYSE | C | 61.85 | -0.28(-0.45%) | 13265 |

Deere & Company, NYSE | DE | 157.65 | 0.04(0.03%) | 900 |

Exxon Mobil Corp | XOM | 71.34 | 0.04(0.06%) | 6592 |

Facebook, Inc. | FB | 144.5 | 0.20(0.14%) | 43730 |

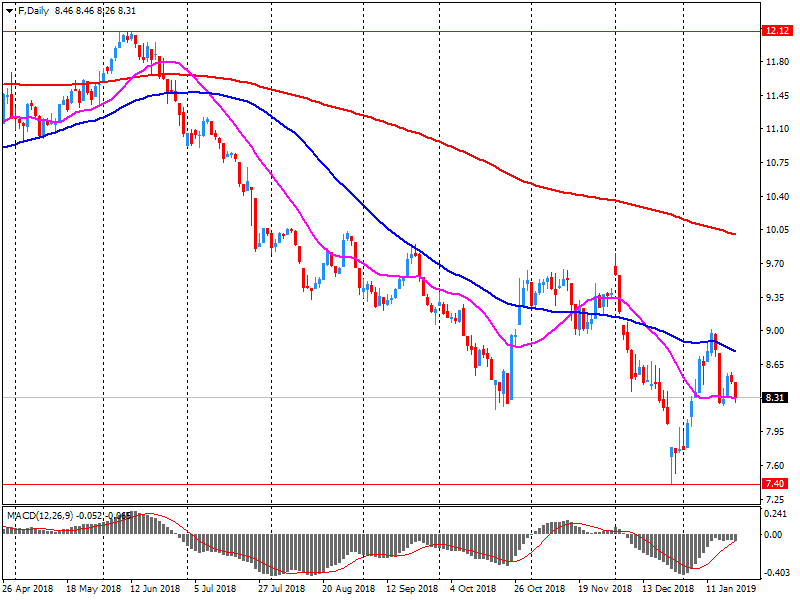

Ford Motor Co. | F | 8.36 | 0.02(0.24%) | 47908 |

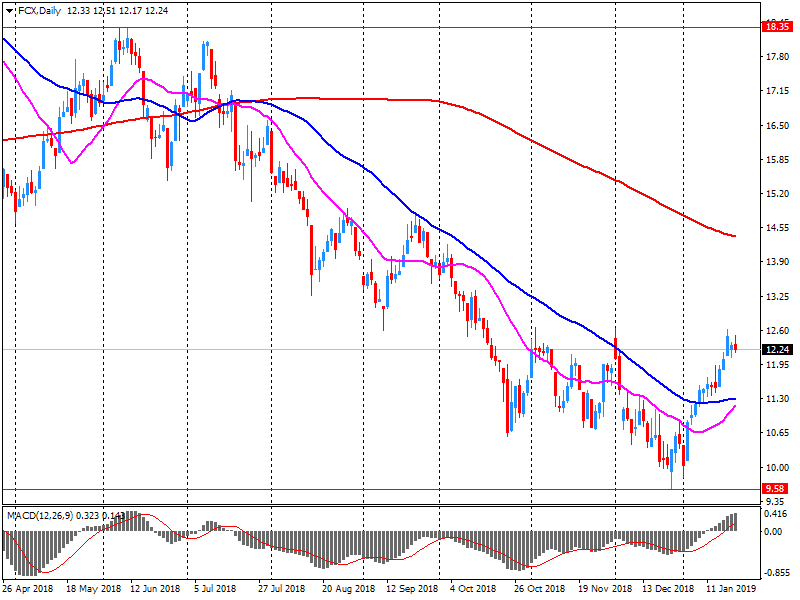

Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 11.65 | -0.66(-5.36%) | 148986 |

General Electric Co | GE | 8.7 | -0.03(-0.34%) | 83794 |

General Motors Company, NYSE | GM | 37.75 | 0.08(0.21%) | 1029 |

Goldman Sachs | GS | 196.56 | -0.34(-0.17%) | 2630 |

Google Inc. | GOOG | 1,077.20 | 1.63(0.15%) | 2787 |

Home Depot Inc | HD | 177 | 0.11(0.06%) | 564 |

Intel Corp | INTC | 48.6 | 0.66(1.38%) | 99206 |

International Business Machines Co... | IBM | 132.6 | -0.29(-0.22%) | 12271 |

International Paper Company | IP | 45.85 | 0.02(0.04%) | 201 |

Johnson & Johnson | JNJ | 128.85 | 0.05(0.04%) | 2089 |

JPMorgan Chase and Co | JPM | 102.26 | -0.42(-0.41%) | 1710 |

McDonald's Corp | MCD | 187 | 0.91(0.49%) | 1385 |

Microsoft Corp | MSFT | 106.8 | 0.09(0.08%) | 58075 |

Nike | NKE | 80.43 | -0.07(-0.09%) | 5552 |

Procter & Gamble Co | PG | 94.51 | -0.33(-0.35%) | 10072 |

Starbucks Corporation, NASDAQ | SBUX | 66.45 | 0.02(0.03%) | 13050 |

Tesla Motors, Inc., NASDAQ | TSLA | 282.35 | -5.24(-1.82%) | 77076 |

Twitter, Inc., NYSE | TWTR | 31 | 0.03(0.10%) | 11947 |

United Technologies Corp | UTX | 117.24 | 0.20(0.17%) | 3014 |

Verizon Communications Inc | VZ | 57.83 | 0.07(0.12%) | 563 |

Visa | V | 137.63 | 0.62(0.45%) | 2074 |

Wal-Mart Stores Inc | WMT | 98.67 | -0.04(-0.04%) | 2358 |

Walt Disney Co | DIS | 110.91 | -0.21(-0.19%) | 1027 |

Underlying inflation is expected to increase over the medium term, supported by our monetary policy measures

Slowdown is due to fall in external demand as well as some country-specific reasons

Risks around the eurozone outlook have moved to the downside

Governing Council stands ready to adjust all of its instruments

In the week ending January 19, the advance figure for seasonally adjusted initial claims was 199,000, a decrease of 13,000 from the previous week's revised level. This is the lowest level for initial claims since November 15, 1969 when it was 197,000. The previous week's level was revised down by 1,000 from 213,000 to 212,000. The 4-week moving average was 215,000, a decrease of 5,500 from the previous week's revised average. The previous week's average was revised down by 250 from 220,750 to 220,500.

Freeport-McMoRan (FCX) reported Q4 FY 2018 earnings of $0.11 per share (versus $0.51 in Q4 FY 2017), missing analysts’ consensus estimate of $0.19.

The company’s quarterly revenues amounted to $3.684 bln (-26.9% y/y), missing analysts’ consensus estimate of $3.858 bln.

FCX fell to $11.75 (-4.55%) in pre-market trading.

“At today’s meeting the Governing Council of the European Central Bank (ECB) decided that the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.40% respectively. The Governing Council expects the key ECB interest rates to remain at their present levels at least through the summer of 2019, and in any case for as long as necessary to ensure the continued sustained convergence of inflation to levels that are below, but close to, 2% over the medium term.

Regarding non-standard monetary policy measures, the Governing Council intends to continue reinvesting, in full, the principal payments from maturing securities purchased under the asset purchase programme for an extended period of time past the date when it starts raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:30 CET today”.

Ford Motor (F) reported Q4 FY 2018 earnings of $0.30 per share (versus $0.39 in Q4 FY 2017), being in line with analysts’ consensus estimate.

The company’s quarterly revenues amounted to $38.700 bln (+0.5% y/y), beating analysts’ consensus estimate of $36.834 bln.

F rose to $8.37 (+0.36%) in pre-market trading

Biggest Concern Are ‘Political Mistakes’

SNB Still has Some Room To Manoeuvre On Interest Rates

Uncertainties Around Global Economy Have Increased

Markets Still Fragile

The euro area economy edged closer to stagnation at the start of 2019, with businesses reporting the weakest rise in output for five-and-a-half years and the first fall in demand for over four years.

The IHS Markit Eurozone Composite PMI fell to 50.7 in January from 51.1 in December, its lowest since July 2013, according to the preliminary ‘flash’ reading. The flash estimate is typically based on approximately 85% of the final number of replies received each month. The latest reading indicated only marginal growth of business output, contrasting markedly with the strong rates of expansion seen this time last year.

At 47.9 in January, the IHS Markit Flash France Composite Output Index fell from 48.7 in December, and pointed to the quickest contraction in French private sector output for over four years. At the sector level, the latest decline was driven by service providers, as firms reported a moderate fall in activity. Moreover, the pace of contraction accelerated compared to December to reach its fastest for nearly five years. In contrast to the recent trend, manufacturers outperformed their service providing counterparts. Goods producers recorded broadly-unchanged output in the first month of 2019, stabilising after the contraction in December

Business activity growth across Germany’s private sector recovered slightly in January, though was still among the weakest seen over the past four years, according to the latest PMI data from IHS Markit. Meanwhile, the survey’s measures of new orders and job creation worsened, with inflows of new business shown to have declined for the first time in over four years and employment growth easing to the slowest since December 2016.

On the price front, latest data showed a further softening of underlying cost pressures, with input price inflation pulling back to a 17-month low. Having slumped to a 66-month low of 51.6 in December, the IHS Markit Flash Germany Composite Output Index recovered slightly in January to register a reading of 52.1.

NAB Says Rate Rise Due To Sustained Increase In Funding Costs

The unemployment rate fell to a lower-than-expected 5.0% in December from 5.1% in November. Economists expected an unemployment rate of 5.1% for the month.

The number of people employed rose by 21,600, compared with an expected 18,000 rise, the Australian Bureau of Statistics said Thursday.

The number of people in full-time work fell by 3,000 in December, while those in part-time work rose by 24,600.

Participation in the workforce fell to 65.6% in December from 65.7% in November and against a consensus expectation of 65.7%.

The ABS measures of underemployment and labor-market underutilization both fell in December.

Says One Cannot Give Any Concessions To Britain On Eu Basic Freedoms For Internal Market

EUR/USD

Resistance levels (open interest**, contracts)

$1.1508 (2637)

$1.1485 (497)

$1.1456 (548)

Price at time of writing this review: $1.1378

Support levels (open interest**, contracts):

$1.1350 (3908)

$1.1317 (4656)

$1.1279 (2554)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date February, 8 is 69977 contracts (according to data from January, 23) with the maximum number of contracts with strike price $1,1350 (4656);

GBP/USD

Resistance levels (open interest**, contracts)

$1.3184 (1968)

$1.3154 (632)

$1.3134 (1244)

Price at time of writing this review: $1.3065

Support levels (open interest**, contracts):

$1.2999 (396)

$1.2948 (370)

$1.2917 (592)

Comments:

- Overall open interest on the CALL options with the expiration date February, 8 is 23178 contracts, with the maximum number of contracts with strike price $1,3000 (1968);

- Overall open interest on the PUT options with the expiration date February, 8 is 26217 contracts, with the maximum number of contracts with strike price $1,2600 (1930);

- The ratio of PUT/CALL was 1.13 versus 1.12 from the previous trading day according to data from January, 23

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

| Raw materials | Closed | Change, % |

|---|---|---|

| Brent | 60.76 | -0.88 |

| WTI | 52.37 | -1.06 |

| Silver | 15.33 | 0.13 |

| Gold | 1282.384 | -0.2 |

| Palladium | 1346.94 | 0.06 |

| Index | Change, points | Closed | Change, % |

|---|---|---|---|

| NIKKEI 225 | -29.19 | 20593.72 | -0.14 |

| Hang Seng | 2.75 | 27008.2 | 0.01 |

| KOSPI | 10.01 | 2127.78 | 0.47 |

| ASX 200 | -15.1 | 5843.7 | -0.26 |

| FTSE 100 | -58.51 | 6842.88 | -0.85 |

| DAX | -18.57 | 11071.54 | -0.17 |

| Dow Jones | 171.14 | 24575.62 | 0.7 |

| S&P 500 | 5.8 | 2638.7 | 0.22 |

| NASDAQ Composite | 5.41 | 7025.77 | 0.08 |

| Pare | Closed | Change, % |

|---|---|---|

| AUDUSD | 0.71398 | 0.27 |

| EURJPY | 124.73 | 0.4 |

| EURUSD | 1.13795 | 0.18 |

| GBPJPY | 143.232 | 1.09 |

| GBPUSD | 1.30674 | 0.86 |

| NZDUSD | 0.67876 | 0.59 |

| USDCAD | 1.33436 | -0.07 |

| USDCHF | 0.99479 | -0.24 |

| USDJPY | 109.605 | 0.22 |

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers