- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 26-10-2020

| Time | Country | Event | Period | Previous value | Forecast |

|---|---|---|---|---|---|

| 09:00 (GMT) | Eurozone | Private Loans, Y/Y | September | 3% | |

| 09:00 (GMT) | Eurozone | M3 money supply, adjusted y/y | September | 9.5% | 9.6% |

| 11:00 (GMT) | United Kingdom | CBI retail sales volume balance | October | 11 | |

| 12:30 (GMT) | U.S. | Durable goods orders ex defense | September | 0.7% | |

| 12:30 (GMT) | U.S. | Durable Goods Orders ex Transportation | September | 0.4% | 0.4% |

| 12:30 (GMT) | U.S. | Durable Goods Orders | September | 0.4% | 0.5% |

| 13:00 (GMT) | U.S. | Housing Price Index, m/m | August | 1% | |

| 13:00 (GMT) | U.S. | Housing Price Index, y/y | August | 6.5% | |

| 13:00 (GMT) | U.S. | S&P/Case-Shiller Home Price Indices, y/y | August | 3.9% | 4.2% |

| 14:00 (GMT) | U.S. | Richmond Fed Manufacturing Index | October | 21 | |

| 14:00 (GMT) | U.S. | Consumer confidence | October | 101.8 | 102.5 |

- Overvalued Swiss franc can pose problem for Swiss financial industry

- So far Swiss banks have withstood the effects of pandemic well

FXStreet notes that the S&P 500 Index has rebounded off September’s correction but has also pulled back from October’s highs around 3,550. Nathan Peterson from Charles Schwab expects the index to remain rangebound while the VIX is set to stay within a 25-30 range as well.

“The VIX has been in a trading range of roughly 25-30 over the past six weeks and it’s likely to stay within this range until after the elections.”

“If there is uncertainty around the outcome of the elections this could result in an uptick in the VIX, but it feels to me like the higher probability is that the VIX heads back down towards the low 20s by mid-November, and potentially even lower than that (18-20).”

“It feels to me that the most likely scenario between now and the elections is that the S&P 500 remains sandwiched within a range of roughly 3,400 (which coincides with the 50-day SMA) and that October high of 3,550, so my near-term outlook calls for choppy, sideways action.”

The Federal Reserve Bank of Dallas reported Monday its general business activity index for manufacturing in Texas rose to 19.8 in October from an unrevised 13.6 in September, pointing to expansion in Texas factory activity for the third straight month. This was the highest reading since October 2018 as well.

According to the report, the production index, a key

measure of state manufacturing conditions, came in at 25.5 in October, up 3.2

points from September, indicating a slight acceleration in output growth. The new orders index rose 5.2 points to 19.9, and the growth rate of orders

index increased 1.1 points to 14.3. The shipments index edged up 0.4 points to

21.9, while the capacity utilization index climbed 5.5 points to 23.0. Meanwhile,

the employment index fell 5.8 points to 8.7, suggesting less robust hiring.

The U.S.

Commerce Department announced on Monday that the sales of new single-family

homes fell 3.5 percent m-o-m to a seasonally adjusted annual rate of 959,000

units in September.

Economists had

forecast the sales pace of 1,025,000 last month.

August’s sales

pace was revised down to 994,000 units from the originally reported 1,011,000 units.

According to

the report, new home sales in the South, the largest area, fell 4.7 percent

m-o-m in September. Sales in the Northeast tumbled 28.9 percent m-o-m, while

sales in the Midwest decreased 4.1 percent m-o-m. Meanwhile, sales in the West increased

0.7 percent m-o-m.

FXStreet notes that NZD/USD closed above the top of its recent range at 0.6682 on Friday, which should trigger a short-term base to open up a move back to medium-term resistances at 0.6791/6806, according to the Credit Suisse analyst team.

“NZD/USD closed just above key short-term resistance at 0.6682/93 on Friday, although the market is struggling to so far follow through on this break this morning. Nevertheless, the break above here should trigger a small base, which should lead to an acceleration of upside momentum and open the door to 0.6737/52 next, then a key cluster of medium-term resistances at 0.6778/6806 – the recent and current year highs as well as the 78.6% retracement of the December 2018/March 2020 fall.

“A break above 0.6806 would complete a major medium-term base to open up significantly higher levels, with 0.6860 just the next initial resistance.”

- Says that time is very short

- Welcomes that they are now negotiating on basis of legal text

- Stimulus talks have slowed but not ended

- U.S. economy still needs targeted relief

U.S. stock-index futures plunged on Monday amid news that talks between the White House and House Democrats on a new fiscal stimulus package remained at a stalemate and the U.S. hit a new daily record for coronavirus cases.

Global Stocks:

Index/commodity | Last | Today's Change, points | Today's Change, % |

Nikkei | 23,494.34 | -22.25 | -0.09% |

Hang Seng | - | - | - |

Shanghai | 3,251.12 | -26.88 | -0.82% |

S&P/ASX | 6,155.60 | -11.40 | -0.18% |

FTSE | 5,834.01 | -26.27 | -0.45% |

CAC | 4,851.09 | -58.55 | -1.19% |

DAX | 12,285.04 | -360.71 | -2.85% |

Crude oil | $38.73 | -2.81% | |

Gold | $1,903.70 | -0.08% |

FXStreet notes that S&P 500 is seen finely balanced near term and needs to hold 3420/15 to maintain an upward bias with resistance seen at 3477. The VIX though has moved sharply higher this morning and the Credit Suisse analyst team watches resistance from the 31.18 late September high.

“The S&P 500 continues to hold the 38.2% retracement of its September/October rally at 3420, but is unable to make a decisive break higher and with the US election getting closer the immediate outlook stays finely balanced.”

“For now, we continue to look for 3420/15 to try and hold with resistance seen at 3477 initially, above which is needed to clear the way for a move back to 3516, then the potential downtrend from early September, today seen at 3536. Above 3550 remains needed to open the door to a challenge on the 3588 record high.”

“The VIX has moved sharply higher this morning and we watch resistance from the 31.18 late September high. Above here would mark a base to warn of a more concerted move higher, with resistance then seen next at 36.25.”

(company / ticker / price / change ($/%) / volume)

3M Co | MMM | 167.5 | -2.30(-1.35%) | 1206 |

ALCOA INC. | AA | 13.3 | -0.17(-1.26%) | 18567 |

ALTRIA GROUP INC. | MO | 38.9 | -0.18(-0.46%) | 3639 |

Amazon.com Inc., NASDAQ | AMZN | 3,187.90 | -16.50(-0.51%) | 41097 |

American Express Co | AXP | 99.73 | -1.25(-1.24%) | 11302 |

AMERICAN INTERNATIONAL GROUP | AIG | 31.82 | -0.56(-1.73%) | 6615 |

Apple Inc. | AAPL | 113.56 | -1.48(-1.29%) | 1280231 |

AT&T Inc | T | 27.56 | -0.26(-0.93%) | 2035560 |

Boeing Co | BA | 164.2 | -3.16(-1.89%) | 141792 |

Caterpillar Inc | CAT | 166.87 | -1.72(-1.02%) | 11298 |

Chevron Corp | CVX | 71.44 | -1.13(-1.56%) | 15930 |

Cisco Systems Inc | CSCO | 38.39 | -0.43(-1.11%) | 30421 |

Citigroup Inc., NYSE | C | 43.43 | -0.52(-1.18%) | 69068 |

Deere & Company, NYSE | DE | 237.55 | -1.98(-0.83%) | 547 |

E. I. du Pont de Nemours and Co | DD | 58.26 | -1.56(-2.61%) | 4092 |

Exxon Mobil Corp | XOM | 33.62 | -0.54(-1.58%) | 65108 |

Facebook, Inc. | FB | 283.13 | -1.66(-0.58%) | 175308 |

FedEx Corporation, NYSE | FDX | 279.5 | -4.06(-1.43%) | 4030 |

Ford Motor Co. | F | 8.04 | -0.12(-1.47%) | 340814 |

Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 17.9 | -0.46(-2.51%) | 59567 |

General Electric Co | GE | 7.48 | -0.15(-1.97%) | 669956 |

General Motors Company, NYSE | GM | 36.12 | -0.71(-1.93%) | 67214 |

Goldman Sachs | GS | 201.5 | -3.54(-1.73%) | 12351 |

Google Inc. | GOOG | 1,627.01 | -13.99(-0.85%) | 7364 |

Hewlett-Packard Co. | HPQ | 18.99 | -0.13(-0.68%) | 9834 |

Home Depot Inc | HD | 280.75 | -2.25(-0.80%) | 2443 |

HONEYWELL INTERNATIONAL INC. | HON | 172.5 | -3.04(-1.73%) | 2044 |

Intel Corp | INTC | 47.69 | -0.51(-1.06%) | 305214 |

International Business Machines Co... | IBM | 114.93 | -1.07(-0.92%) | 13522 |

International Paper Company | IP | 45.36 | -1.04(-2.24%) | 2094 |

Johnson & Johnson | JNJ | 145 | -0.24(-0.17%) | 7560 |

JPMorgan Chase and Co | JPM | 102.15 | -1.66(-1.60%) | 45021 |

McDonald's Corp | MCD | 226.54 | -2.17(-0.95%) | 4571 |

Merck & Co Inc | MRK | 79.99 | 0.16(0.20%) | 20135 |

Microsoft Corp | MSFT | 213.88 | -2.35(-1.09%) | 196569 |

Nike | NKE | 128 | -1.99(-1.53%) | 6571 |

Pfizer Inc | PFE | 37.94 | -0.24(-0.63%) | 110575 |

Procter & Gamble Co | PG | 141.3 | -1.08(-0.76%) | 4007 |

Starbucks Corporation, NASDAQ | SBUX | 89.75 | -1.05(-1.16%) | 52442 |

Tesla Motors, Inc., NASDAQ | TSLA | 413.06 | -7.57(-1.80%) | 446554 |

The Coca-Cola Co | KO | 50.24 | -0.28(-0.55%) | 39235 |

Twitter, Inc., NYSE | TWTR | 49.98 | -0.46(-0.91%) | 52964 |

UnitedHealth Group Inc | UNH | 326.72 | -3.88(-1.17%) | 932 |

Verizon Communications Inc | VZ | 57.55 | -0.41(-0.71%) | 11118 |

Visa | V | 195.3 | -2.71(-1.37%) | 16644 |

Wal-Mart Stores Inc | WMT | 143.19 | -0.66(-0.46%) | 14487 |

Walt Disney Co | DIS | 126.38 | -1.97(-1.53%) | 17280 |

Yandex N.V., NASDAQ | YNDX | 58.55 | -0.57(-0.96%) | 12249 |

Starbucks (SBUX) target raised to $97 from $89 at RBC Capital Mkts

Apple (AAPL) resumed with an Overweight at Atlantic Equities; target $150

The Chicago

Federal Reserve announced on Monday the Chicago Fed national activity index

(CFNAI), a weighted average of 85 different economic indicators, came in at 0.27

in September, down from an upwardly revised 1.11 in August (originally 0.79),

pointing to slower growth in economic activity than in the previous month but

still slightly above the average. That was the lowest reading since the sharp decline

in April.

Economists had

forecast the index to come in at 0.39 in September.

At the same

time, the index’s three-month moving average fell to +0.51 in September from

+0.71 in August.

According to

the report, three of the four broad categories of indicators used to construct

the index made positive contributions in September, but three of the four

categories declined from August.

Production-related

indicators made a negative contribution of -0.24 to the CFNAI in September,

down from +0.31 in August. Meanwhile, the contribution of the personal

consumption and housing category to the CFNAI improved to +0.09 in September

from a neutral value in August. Employment-related indicators contributed +0.35

to the CFNAI in September, down from +0.71 in August. The contribution of the

sales, orders, and inventories category to the CFNAI decreased to +0.07 in

September from +0.10 in August.

| Time | Country | Event | Period | Previous value | Forecast | Actual |

|---|---|---|---|---|---|---|

| 09:00 | Germany | IFO - Expectations | October | 97.7 | 95.0 | |

| 09:00 | Germany | IFO - Current Assessment | October | 89.2 | 90.3 | |

| 09:00 | Germany | IFO - Business Climate | October | 93.4 | 92.7 |

USD firmed against most of its major counterparts in the European session on Monday as U.S. stimulus hopes waned, while coronavirus worries intensified.

The U.S. Dollar Index (DXY), measuring the U.S. currency's value relative to a basket of foreign currencies, rose 0.22% to 92.97.

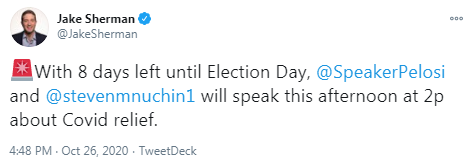

Talks between the White House and House Democrats on a new fiscal stimulus package didn't make much headway. The U.S. House Speaker Nancy Pelosi said on Sunday the House could pass a relief package this week but "that's up to [Senate Majority Leader] Mitch [McConnell] as to whether it would happen in the Senate and go to the president's desk, which is our hope and prayer." Pelosi also added that she sent the White House a list of remaining concerns she had on Friday and hopes to get answers on those issues on Monday. However, CNN reported, citing sources, that McConnell privately had urged the White House not to strike a stimulus deal before the election because there was no support among Senate Republicans to pass it.

Meanwhile, coronavirus cases in the U.S. hit a single-day record of 85,085 on Saturday. Overall, the number of COVID-19 infected people in the country has increased to 8,637,109, the most in the world, according to the latest data from Johns Hopkins University. The U.S. death toll from coronavirus has reached 225,239, also the most in the world.

The White House chief of staff Mark Meadows acknowledged on Sunday that the U.S. is not going to control the coronavirus pandemic. "We’re not going to control the pandemic,” he told CNN. “We are going to control the fact that we get vaccines, therapeutics and other mitigations.”

October 27

Before the Open:

3M (MMM). Consensus EPS $2.27, Consensus Revenues $8380.39 mln

Caterpillar (CAT). Consensus EPS $1.17, Consensus Revenues $9779.54 mln

Merck (MRK). Consensus EPS $1.43, Consensus Revenues $12213.18 mln

Pfizer (PFE). Consensus EPS $0.71, Consensus Revenues $12298.26 mln

Raytheon Technologies (RTX). Consensus EPS $0.50, Consensus Revenues $15157.09 mln

After the Close:

Advanced Micro (AMD). Consensus EPS $0.31, Consensus Revenues $2561.16 mln

Microsoft (MSFT). Consensus EPS $1.36, Consensus Revenues $35780.60 mln

October 28

Before the Open:

Boeing (BA). Consensus EPS -$2.20, Consensus Revenues $14201.02 mln

General Electric (GE). Consensus EPS -$0.03, Consensus Revenues $18943.65 mln

MasterCard (MA). Consensus EPS $1.66, Consensus Revenues $3955.33 mln

UPS (UPS). Consensus EPS $1.89, Consensus Revenues $20261.65 mln

Yandex N.V. (YNDX). Consensus EPS RUB21.83, Consensus Revenues RUB57894.62 mln

After the Close:

Amgen (AMGN). Consensus EPS $3.74, Consensus Revenues $6363.34 mln

eBay (EBAY). Consensus EPS $0.84, Consensus Revenues $2639.69 mln

Ford Motor (F). Consensus EPS $0.18, Consensus Revenues $32901.31 mln

Visa (V). Consensus EPS $1.10, Consensus Revenues $5029.26 mln

October 29

Before the Open:

DuPont (DD). Consensus EPS $0.75, Consensus Revenues $5033.92 mln

Int'l Paper (IP). Consensus EPS $0.48, Consensus Revenues $5144.90 mln

United Micro (UMC). Consensus EPS $0.43, Consensus Revenues $44336.58 mln

After the Close:

Alphabet (GOOG). Consensus EPS $11.14, Consensus Revenues $42813.83 mln

Amazon (AMZN). Consensus EPS $7.15, Consensus Revenues $92463.12 mln

Apple (AAPL). Consensus EPS $0.70, Consensus Revenues $63732.88 mln

Facebook (FB). Consensus EPS $1.91, Consensus Revenues $19764.36 mln

Starbucks (SBUX). Consensus EPS $0.31, Consensus Revenues $6067.36 mln

Twitter (TWTR). Consensus EPS $0.05, Consensus Revenues $768.12 mln

October 30

Before the Open:

Altria (MO). Consensus EPS $1.16, Consensus Revenues $5383.63 mln

Chevron (CVX). Consensus EPS -$0.24, Consensus Revenues $26338.93 mln

Exxon Mobil (XOM). Consensus EPS -$0.24, Consensus Revenues $48356.88 mln

Honeywell (HON). Consensus EPS $1.49, Consensus Revenues $7649.90 mln

FXStreet reports that analysts at Credit Suisse note that EUR/USD remains capped at the top of its short-term channel but with support at 1.1786/82 ideally holding to keep the broader risk skewed higher.

“EUR/USD extends its near-term consolidation following the rejection from the top of its short-term trend channel, today seen at 1.1900 but with daily MACD still positive and with our broader view still that weakness from the beginning of September is a corrective phase only, we maintain our view that the risks are skewed to the upside from here.”

“Immediate resistance is seen at 1.1867, above which should see a move back to 1.1880/81, then 1.1900/01, with the next key resistance seen at the 1.1918/30 corrective price high and 78.6% retracement of the September fall. This latter area remains seen as the barrier to a fresh challenge on the 1.2011 high.”

“Immediate support moves to 1.1825, with a move below 1.1786/82 needed to mark a near-term (minor) top for a fall back to the lower end of the short-term channel, today seen at 1.1727.”

- Expects German economic recovery to continue in Q4

- But at a "considerably slower" pace

- Hospitality in particular to get hit badly

- Recent, strong increase in infection numbers and the associated containment measures taken in some regions may hurt mostly the service sectors and the hotel and catering industries

- German economy has clawed back a little more than half of the output lost during the slump seen in H1 2020

- But output is still probably some 5% below the level recorded in Q4 last year

FXStreet reports that economist at UOB Group Lee Sue Ann assessed the latest inflation figures in New Zealand.

“Consumer prices in New Zealand rose 0.7% q/q in the third quarter, reversing a 0.5% q/q decline in the second quarter, but less than the 0.9% q/q forecast”

“The Reserve Bank of New Zealand (RBNZ) in August had projected inflation would slow to just 0.3% by the end of 2021, and has signalled it is prepared to provide more stimulus through negative interest rates if needed.”

Bloomberg reports that President Xi Jinping opened a meeting in Beijing this week to map out the next phase of economic development, just days before one of the most contentious U.S. elections in history will produce a president resistant to China’s ascent no matter who wins.

The country’s 14th five-year plan is expected to center around technological innovation, economic self reliance and a cleaner environment. Communist Party officials will also set goals for the next 15 years as Xi seeks to deliver on his vow for national rejuvenation by gaining the global lead in technology and other strategic industries. The meeting is closed to the press, and key decisions likely won’t be made clear before it wraps up on Thursday.

If China’s economy -- which is already recovering swiftly from the coronavirus shock -- can stick to the growth trajectory of recent years, it’ll surpass the U.S. within the next decade. The prospect of ever deeper frictions with the U.S. underpins Xi’s strategy to accelerate plans to shield China from swings in the world economy.

FXStreet reports that economists at Danske Bank forecast the USD/CNY pair at 6.60 on a twelve-month view but there are downside risks to their outlook.

“We think two factors explain the move. The outperformance of the Chinese economy amid better control over the coronavirus and higher interest rates than the US; and the increased likelihood of a Biden win, reducing the risks of an uncontrolled, damaging trade war that would ensue under a second term Trump presidency.”

“We see potential for more strength if indeed the US election turns out to provide a clear Biden win, creating downside risk to our twelve-month USD/CNY forecast of 6.60. Among upside risk for the cross is a surprise Trump win and/or a muddy election result as well as renewed rising tensions between US and China, but also between China and Taiwan where tensions have built lately.”

Reuters reports that polling firm YouGov and the Centre for Economics and Business Research said that a measure of consumer confidence among people in Britain fell for the first time in six months in October as worries mounted about new COVID-19 restrictions.

Concerns about household finances and property values pushed down the index to 101.3, down 1.1 points from September.

"The first fall in the Consumer Confidence Index in six months may prove to be a turning point in consumer sentiment as the reality of a second wave sets in," Kay Neufeld, head of macroeconomics at Cebr said.

FXStreet reports that FX Strategists at UOB Group do not expect USD/CNH to grind lower and test the 6.6030 region in the next weeks.

Next 1-3 weeks: “We have held a negative view in USD since last Friday, 16 Oct. In our latest narrative from Wednesday, we indicated that USD ‘is still weak but the next major support at 6.6030 may not come into the picture so soon’. USD subsequently dropped to a low of 6.6275 before rebounding. Downward momentum is beginning to slow and this coupled with rather oversold conditions suggests 6.6030 could be out of reach this time round. That said, only a break of 6.6980 (no change in ‘strong resistance’ level) would indicate the risk for further USD weakness has eased.”

According to the report from ifo Institute, German business climate Index came in at 92.7 in October, weaker than last month's 93.2. Economists had expected a decrease to 93.0.

Meanwhile, the current economic assessment arrived at 90.3 points as compared to last month's 89.2 and 89.8 anticipated.

On the other hand, the expectations index – indicating firms’ projections for the next six months, came in at 95.0 for October, up from the previous month’s 97.4. Economists had expected a decrease to 96.5.

Following the release , the Ifo institute’s Economist Klaus Wohlrabe said that the economy is growing more nervous amid rising coronavirus infections.

RTTNews reports that data from the statistical office INE showed that Spain's producer prices continued to fall in September.

Producer prices declined 3.3 percent year-on-year in September, slower than the 3.5 percent decrease seen in August.

On a monthly basis, producer prices grew 0.3 percent, reversing a 0.2 percent drop in the previous month.

Among sub-groups, energy prices showed the biggest annual fall of 10 percent in September. Prices of intermediate goods dropped 1.6 percent.

FXStreet reports that cable needs to break above 1.3120 to allow for the continuation of the upside pressure, suggested FX Strategists at UOB Group.

Next 1-3 weeks: “After GBP surged to a high of 1.3135, we indicated last Thursday that ‘there is room for further GBP strength towards 1.3250 but it is left to be seen if GBP can maintain a foothold above this level’. Since then, GBP has not been able to make much headway on the upside. Upward momentum is beginning to ease but only a break of 1.2990 (no change in ‘strong support’ level) would indicate that the current upside risk has dissipated. Meanwhile, in order to rejuvenate the current flagging momentum, GBP has to move and stay above 1.3120 within these 1 to 2 days or the odds for further GBP strength would diminish quickly.”

| Time | Country | Event | Period | Previous value | Forecast | Actual |

|---|---|---|---|---|---|---|

| 05:00 | Japan | Coincident Index | August | 78.3 | 79.4 | 79.2 |

| 05:00 | Japan | Leading Economic Index | August | 86.7 | 88.8 | 88.4 |

During today's Asian trading, the US dollar strengthened against most of the world's major currencies.

Demand for the dollar, as well as other "safe haven" assets, is rising due to the growing incidence of COVID-19 in the United States and Europe, with weak hopes for the adoption of a new stimulus package in the States before the November presidential election.

This week, the market is focused on the meetings of the European Central Bank (ECB) and the Bank of Japan, as well as data on the dynamics of US GDP for the third quarter.

House speaker Nancy Pelosi said Sunday that the House of representatives may pass a new stimulus package of about $2 trillion this week, but it is not known whether the Senate is ready to approve it. "We want the package to be adopted as quickly as possible, and therefore we are making concessions," Pelosi said.

Meanwhile, White house chief of staff Mike Meadows accused Pelosi of constantly " changing the rules of the game." "We continue to make one offer after another, and Nancy Pelosi continues to change the rules of the game," he said.

The ICE index, which tracks the dynamics of the US dollar against six currencies (Euro, Swiss franc, yen, canadian dollar, pound sterling and Swedish Krona), rose 0.17%.

FXStreet reports that FX Strategists at UOB Group noted that AUD/USD is expected to navigate between 0.7030 and 0.7185 in the next weeks.

Next 1-3 weeks: “There is not much to add to our latest narrative from last Thursday. As highlighted, the current movement in AUD is viewed as the early stages of a consolidation phase and AUD could trade between 0.7030 and 0.7185 for now. While AUD could test 0.7185 first, the current lackluster momentum suggests that a sustained advance above this level is unlikely.”

eFXdata reports that Danske Research discusses its expectations for ECB meeting.

"At the ECB policy meeting, we do not expect any new measures to be announced. However, with the COVID-19 spreading increasing, we expect the ECB to send its usual dovish signals, which could raise further market expectations for a December decision to increase/extend PEPP due to its open interpretation of the language. Our baseline is for the ECB to signal a readiness to act subject to incoming data in the coming 6 weeks and not a pre-commitment to expand already next week," Danske notes.

"We expect Lagarde to be questioned on the economic and inflation uncertainty and upcoming December staff projections, the content of the toolbox, effectiveness of the tools the divergence of views in the governing council," Danske adds.

RTTNews reports that final data from the Cabinet Office showed that Japan's leading index rose less than estimated in August.

The leading index, which measures the future economic activity, rose to 88.4 in August from 86.7 in July. In the initial estimate, the reading was 88.8.

The coincident index increased to 79.2 in August versus 79.4 in the initial estimate.

The lagging index fell to 91.4 in August from 92.3 in the prior month. In the initial estimate, the reading was 89.7.

EUR/USD

Resistance levels (open interest**, contracts)

$1.1939 (3333)

$1.1918 (4069)

$1.1902 (496)

Price at time of writing this review: $1.1833

Support levels (open interest**, contracts):

$1.1783 (1071)

$1.1754 (1033)

$1.1720 (1559)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date November, 6 is 57402 contracts (according to data from October, 23) with the maximum number of contracts with strike price $1,1800 (4069);

GBP/USD

Resistance levels (open interest**, contracts)

$1.3187 (2027)

$1.3137 (2629)

$1.3100 (265)

Price at time of writing this review: $1.3027

Support levels (open interest**, contracts):

$1.2988 (826)

$1.2952 (296)

$1.2929 (245)

Comments:

- Overall open interest on the CALL options with the expiration date November, 6 is 32722 contracts, with the maximum number of contracts with strike price $1,3950 (3784);

- Overall open interest on the PUT options with the expiration date November, 6 is 25715 contracts, with the maximum number of contracts with strike price $1,2050 (2391);

- The ratio of PUT/CALL was 0.79 versus 0.77 from the previous trading day according to data from October, 23

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

| Raw materials | Closed | Change, % |

|---|---|---|

| Brent | 41.57 | -1.8 |

| Silver | 24.57 | -0.45 |

| Gold | 1901.26 | -0.13 |

| Palladium | 2381.69 | -0.02 |

| Index | Change, points | Closed | Change, % |

|---|---|---|---|

| NIKKEI 225 | 42.32 | 23516.59 | 0.18 |

| Hang Seng | 132.65 | 24918.78 | 0.54 |

| KOSPI | 5.76 | 2360.81 | 0.24 |

| ASX 200 | -6.8 | 6167 | -0.11 |

| FTSE 100 | 74.63 | 5860.28 | 1.29 |

| DAX | 102.69 | 12645.75 | 0.82 |

| CAC 40 | 58.26 | 4909.64 | 1.2 |

| Dow Jones | -28.09 | 28335.57 | -0.1 |

| S&P 500 | 11.9 | 3465.39 | 0.34 |

| NASDAQ Composite | 42.28 | 11548.28 | 0.37 |

| Time | Country | Event | Period | Previous value | Forecast |

|---|---|---|---|---|---|

| 05:00 (GMT) | Japan | Coincident Index | August | 78.3 | 79.4 |

| 05:00 (GMT) | Japan | Leading Economic Index | August | 86.7 | 88.8 |

| 09:00 (GMT) | Germany | IFO - Expectations | October | 97.7 | |

| 09:00 (GMT) | Germany | IFO - Current Assessment | October | 89.2 | |

| 09:00 (GMT) | Germany | IFO - Business Climate | October | 93.4 | |

| 12:30 (GMT) | U.S. | Chicago Federal National Activity Index | September | 0.79 | 0.39 |

| 14:00 (GMT) | U.S. | New Home Sales | September | 1.011 | 1.025 |

| 15:30 (GMT) | Switzerland | SNB Chairman Jordan Speaks | |||

| 21:45 (GMT) | New Zealand | Trade Balance, mln | September | -353 |

| Pare | Closed | Change, % |

|---|---|---|

| AUDUSD | 0.71362 | 0.33 |

| EURJPY | 124.173 | 0.2 |

| EURUSD | 1.18591 | 0.34 |

| GBPJPY | 136.57 | -0.39 |

| GBPUSD | 1.30428 | -0.27 |

| NZDUSD | 0.66875 | 0.33 |

| USDCAD | 1.31237 | -0.06 |

| USDCHF | 0.90401 | -0.33 |

| USDJPY | 104.704 | -0.13 |

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers