- Analiza

- Novosti i instrumenti

- Vesti sa tržišta

Forex-novosti i prognoze od 04-08-2022

- NZD/USD struggles to extend the previous day’s run-up below two-month-old resistance line.

- RSI hints at limited upside room, two-week-old ascending trend line adds to the downside filters.

- Multiple supports below 0.6200 signal bumpy road for bears.

NZD/USD bulls take a breather, after snapping a two-day downtrend, as the quote seesaws around the 0.6300 threshold during Friday’s Asian session.

In doing so, the Kiwi pair fades bounce off 100-SMA and an 11-day-long support line. The pullback also takes place ahead of the resistance line stretched from June 2022.

It’s worth observing that the lower highs of the RSI (14) also invalidate the previous recovery and hence keeping NZD/USD sellers hopeful.

With this in mind, the intraday bears can aim for the 38.2% Fibonacci retracement of the June-July downside, near 0.6260.

However, the 100-SMA and the aforementioned support line, respectively around 0.6240 and 0.6215, could challenge the NZD/USD sellers afterward.

In a case where the quote drops below 0.6215, the 0.6200 and multiple supports beyond 0.6100 could challenge the further downside.

Alternatively, recovery moves may initially attack the 50% Fibonacci retracement level of 0.6320 before poking the downward sloping resistance line from June, close to 0.6335 by the press time.

In a case where the NZD/USD prices rally beyond 0.6335, the mid-June swing high near 0.6395 and the 0.6400 could lure the bulls.

NZD/USD: Four-hour chart

Trend: Pullback expected

- WTI crude oil holds lower ground near six-month bottom after declining for the last four days.

- Fears of economic slowdown, central bank aggression outweigh geopolitical woes linked to China, Russia.

- US jobs report for July, developments surrounding China will be important for fresh impulse.

WTI crude oil prices remain depressed at the lowest levels in six months as fears of economic slowdown supersede geopolitical crisis. That said, the black gold seesaws around $87.20-30, after refreshing the multi-day low with the $87.18 mark, as traders await the US employment data on Friday.

The energy benchmark dropped during the last four consecutive days to print the six-month bottom the previous day as mixed statistics from the major economies join aggressive monetary policy actions to highlight the recession fears.

It’s worth noting that the Bank of England’s (BOE) open acceptance of the economic slowdown in late 2022 amplified the fears. On the same line was Cleveland Fed President Loretta Mester who said that recession risks have increased in the US.

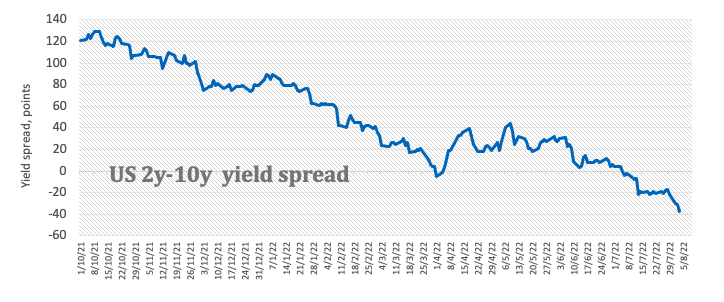

It’s worth noting that the US Treasury yields continued to portray the risk of recession as the difference between the 10-year and 2-year bond coupons remain the widest since 2000. That said, the US 10-year Treasury yields closed near 2.069% while the 2-year counterpart dropped to 3.049% at the latest.

Alternatively, a smaller output increase by the Organization of the Petroleum Exporting Countries (OPEC) and allies, collectively known as OPEC+, should have helped the oil buyers but did not. The reason could be linked to the weekly stockpile data from the US Energy Information Administration (EIA) marked a notable increase in inventories. “Crude inventories rose by 4.5 million barrels in the week to July 29 to 426.6 million barrels, the EIA said, compared with analysts' expectations in a Reuters poll for a 600,000-barrel drop,” stated the news.

Also likely to have challenged the oil prices are headlines surrounding China and Russia. Recently, the dragon nation’s heavy military drills near the Taiwan border gained major attention and challenges the global trade channel, which in turn should mark further strain on the supply chain and might create an imbalance in the oil supply-demand matrix. However, the same could also escalate the recession fears and may not be that effective. On the other hand, Russia’s sustained invasion of Ukraine has been old news and hence gained little attention from the markets.

Amid these plays, the oil bears keep reins ahead of the key US employment data for July that will be crucial for determining near-term market moves.

Also read: Nonfarm Payrolls Preview: High expectations set deal the dollar a blow, create buying opportunity

Technical analysis

A daily close below July’s low of $88.34 directs bears towards October 2021 peak near $85.00.

- AUD/NZD has shifted into a consolidation mode ahead of the RBA’s monetary policy statement.

- The RBA raised its OCR by 50 bps consecutively for the third time to 1.85%.

- A downbeat NZ employment data released this week may keep the kiwi bulls on the tenterhooks.

The AUD/NZD pair is witnessing topsy-turvy moves in a range of 1.1043-1.1075 from Thursday. The market participants are likely to remain on the sidelines as investors are awaiting the release of the monetary policy statement (MoPS) by the Reserve Bank of Australia (RBA).

The minutes from the RBA MoPS will provide a detailed view of Tuesday’s interest rate decision. The investing community should be aware of the fact that RBA Governor Philip Lowe announced a rate hike by 50 basis points (bps) and raised the Official Cash Rate (OCR) to 1.85%. This was the third consecutive 50 bps rate hike by the RBA.

In order to combat the soaring price pressures, the RBA needed to tighten its policy extremely and squeeze liquidity from the market. For the second quarter of CY2022, the inflation rate has landed at 6.1%, significantly higher than the prior release of 5.1%.

On the kiwi front, the ineffectiveness of the kiwi economy in generating job opportunities has created immense trouble for the Reserve Bank of New Zealand (RBNZ). Price pressures are soaring in the NZ economy and the RBNZ was expecting decent performance from the labor market to get strengthened for hiking the Official Cash Rate (OCR) unhesitatingly. Now, crippled RBNZ would resort to a less-hawkish stance on the policy rates.

Stats NZ reported that the Unemployment Rate increased to 3.3% from the estimates of 3.1% and the prior release of 3.2% in the second quarter. Also, the Employment Change for the second quarter has landed at 0%, significantly lower than the estimates of 0.4% and the prior print of 0.1%.

- The GBP/JPY prepares to finish the week with losses of almost 0.50%.

- The cross-currency daily and hourly charts suggest that a mean reversion move towards 162.83 could be on the cards.

The GBP/JPY plummeted on Thursday, failing to crack the 50-day EMA at 164.12, so the pair tumbled towards its daily low at 161.12 before recovering some ground and settling near current exchange rates. As the Asian Pacific session begins, the GBP/JPY is trading at 161.47, registering a minimal losses of 0.06%.

GBP/JPY Price Analysis: Technical outlook

Once the dust settled, after the Bank of England acknowledged that the UK might tap into a recession, the GBP/JPY daily chart shows sellers are in control, tuned in with the Relative Strength Index (RSI), in bearish territory, and below its 7-day RSI’s SMA. Despite some selling pressure lying in the cross, the move’s size suggests a possible mean reversion impulse before extending downwards.

Unless the GBP/JPY decisively breaks below the August 4 low at 161.12, a pullback towards the 100-day EMA at 162.83 is on the cards.

GBP/JPY Hourly chart

In the near term, the GBP/JPY is neutral-biased but slightly tilted downwards. Failure to conquer 164.00 leaves the pair exposed to selling pressure, so bears could be piling around the confluence of the 200-hour EMA and the 61.8% Fibonacci level, around the 162.84-162.93 area. However, if the cross-currency pair tumbles below 161.00, a re-test of the weekly low at 159.44 is on the cards.

GBP/JPY Key Technical Levels

- USD/CHF is oscillating in an 11-pip range as investors await US NFP data.

- A 200k consensus for the US NFP could drag the asset further.

- The DXY has failed to capitalize on hawkish commentary from the Fed policymaker.

The USD/CHF pair is displaying back and forth moves in a narrow range of 0.9543-0.9554 in the early Tokyo session. The asset has turned lackluster as investors are focusing on the release of the US Nonfarm Payrolls (NFP). On Thursday, the asset witnessed a steep fall after surrendering the crucial support of 0.9600 and printed a low of 0.9543.

Economists at JP Morgan predict the US Nonfarm Payrolls (NFP) to come in weaker at 200K in July’s labor market report. In the month of June, the US economy added 372k jobs in the labor market. Rising interest rates and their multiplier effects have trimmed the job opportunities in the market. Well, the Unemployment Rate is seen unchanged at 3.6%.

The corporate players have inculcated more filters in the selection of investment opportunities due to the unavailability of the cheap dollar. So lower investment planning by the firms is resulting in lower job creation. It is worth noting that various firms in their quarterly earnings commentary have hinted announced that they have halted their recruitment process for the rest of CY2022.

Meanwhile, the US dollar index (DXY) has surrendered the crucial support of 106.00. The asset is hinting at a subdued movement ahead despite the higher targets for interest rates by Federal Reserve (Fed) policymakers. Cleveland Fed President Loretta J. Mester is seeing interest rates above 4% as halting the policy tightening program without finding a slowdown in the inflation rate for months is not feasible.

On the Swiss franc front, the inflation rate has remained in line with the prior release of 3.5%. However, investors were expecting an improvement to 3.5%. Well, this doesn’t trim the odds of a rate hike by the Swiss National Bank (SNB) ahead, but hawkish guidance could get mild.

- AUD/JPY holds lower ground after reversing from weekly top.

- Convergence of 21-DMA, 50-DMA precedes previous support line from early May to restrict immediate upside.

- Bearish MACD signals also favor the decline towards 50% Fibonacci retracement.

AUD/JPY bears keep reins after retaking control from crucial resistances, despite recent dribbling of around 92.60 during Friday’s Asian session.

That said, the cross-currency pair refreshed a one-week high the previous day before reversing from a confluence of the 21-DMA and the 50-DMA, as well as reversing from the resistance-turned-support stretched from May 12.

The pullback moves join bearish MACD signals to keep sellers hopeful.

However, the 50% Fibonacci retracement level of May-June upside, around 92.10, quickly followed by the 92.00 threshold, could challenge the AUD/JPY sellers.

It’s worth noting that July’s bottom near 91.40 and the 61.8% Fibonacci retracement level of 90.95 will precede the latest swing low close to 90.50 to restrict the cross-currency pair’s downside past 92.00.

Alternatively, recovery moves may initially confront the aforementioned DMA convergence of 93.75 before poking the previous support line surrounding 93.85.

Even if the AUD/JPY prices cross the 93.85 hurdle, the bulls need validation from the 94.00 round figure before retaking control.

AUD/JPY: Daily chart

Trend: Further weakness expected

- USD/CAD bears could be on the verge of an attack.

- The bears can eye a break to 1.2780 for the day ahead.

As per the prior analysis, USD/CAD Price Analysis: Bears lurking and break below 1.2800 eyed, the price was going through a consolidative phase and price discovery. There was little bias to go on although there had been a lower high printed.

The price was holding up in the 1.2830s and a correction to mitigate the price imbalance between spot and 1.2865 was anticipated to result in further supply in order to break down the support of 1.2820. In doing so, this was going to leave the price imbalance between 1.2800 and 1.2780 exposed.

USD/CAD H1, prior analysis

USD/CAD H1 target reached

As illustrated, the price moved in on the targetted level. However, the bulls came up for air again as follows:

USD/CAD H1 live market

The level proved to be a strong support area from which the price has rallied. However, the bulls have failed to print a higher high so far and should the price respect the trendline resistance, this could be the makings of a breakout to the downside in line with the original bearish scenario and to target a break of 1.2780.

- EUR/JPY oscillates around 136.20 after buyers struggle at 137.00.

- In the near term, the EUR/JPY is range-bound within 136.00-136.80.

The EUR/JPY finished almost flat on Thursday after hitting a daily low at 135.63, followed by a rally towards its weekly high at 136.92. Nevertheless, buyers lost steam and booked profits, while the EUR/JPY dived towards the 136.10 area. At the time of writing, the EUR/JPY is trading at 136.21 up 0.09% as the Asian session begins.

EUR/JPY Price Analysis: Technical outlook

The EUR/JPY daily chart illustrates the formation of a doji, as Thursday’s price action, even though was large, neither buyers/sellers capitalized on each other weaknesses. Therefore, due to the uptrend preceding the chart pattern, the EUR/JPY might dip towards 136.00 due to its neutral-to-downward bias.

EUR/JPY Hourly chart

The EUR/JPY 1-hour chart depicts price action contracting, trapped between the 200 and the 50-hour EMA, meaning that prices could remain sideways or it’s going to break outside the range. On the upside, the EUR/JPY’s first resistance would be the confluence of the 200-hour EMA and the R1 pivot at 136.82. The break above will expose 137.00, followed by July 27 139.34.

On the flip side, the EUR/JPY first support will be the 50-hour EMA at 135.99. Once cleared, the next support would be the confluence of the 100-hour EMA and the S1 pivot at 135.51, followed by the S2 pivot at 135.00.

EUR/JPY Key Technical Levels

- EUR/USD grinds higher amid pre-NFP trading lull, seesaws after the biggest daily jump in a fortnight.

- Treasury yields drown US dollar amid recession risk, mixed data.

- Pre-NFP anxiety, China-linked fears add to the trading filters.

EUR/USD bulls take a breather after the heavy run, grinding higher around 1.0250 during the initial Asian session on Friday. In the doing so, the major currency pair portrays the typical cautious mood ahead of the key US Nonfarm Payrolls (NFP) release. That said, the quote rose the most in 13 days amid broad US dollar weakness and firmer German data on Thursday.

German Factory Orders dropped 0.4% MoM versus -0.8% expected and -0.2% downwardly revised prior. Also adding strength to the Euro were the hopes of economic recovery in the bloc, despite the energy crisis, mainly due to the European Central Bank’s (ECB) bond-buying, per the monthly ECB Economic Bulletin.

In a case of the US, the Initial Jobless Claims rose to 260K for the week ended on July 30 versus 254K prior and 259K expected. Further, the Goods and Services Trade Balance improved to $-79.6B versus $-80.1B market consensus and $-84.9B revised prior. Despite the mixed data, the market players remained hopeful of the Fed’s aggression but that couldn’t lift the US dollar amid fears of recession. On the same line could be an absence of major instances during US House Speaker Nancy Pelosi’s Taiwan visit, despite the verbal war.

The economic slowdown woes gained momentum after the Bank of England (BOE) formally accepted the fears of recession and further hardships while Cleveland Fed President Loretta Mester said that recession risks have increased in the US.

It should be noted that China’s military drills have sparked geopolitical fears as five test missiles landed in Japan’s exclusive economic zones. This adds to the US-China tension over Taiwan and could have challenged the US dollar bears.

Against this backdrop, Wall Street closed mixed but the yields were down for the second consecutive day to 2.69% at the latest, which in turn pressured the US dollar ahead of the key data.

Moving on, the EUR/USD traders should wait for the US Nonfarm Payrolls (NFP) for July, expected 250K versus 372K prior, for clear directions as recession fears jostle with the Fed’s aggression.

Technical analysis

EUR/USD justified Wednesday’s bullish Doji to portray notable run-up. However, failure to cross the two-month-old resistance line on daily closing, at 1.0245 by the press time, seemed to teased the sellers to revisit the 21-DMA support surrounding 1.0165.

- A responsive buying action near the rising channel lower portion indicates the strength of an asset.

- Pound bulls have successfully defended the 200-EMA near 1.2125.

- A golden cross formation by the 50-and 200-EMAs adds to the upside filters.

The GBP/USD pair has turned sideways around 1.2160 in the early Tokyo session after extending recovery above 1.2120 on Thursday. Earlier, the cable displayed a responsive buying action after plummeting below 1.2080 as the Bank of England (BOE) announced an interest rate decision. The BOE elevated the interest rates by 50 basis points (bps) to 1.75%.

On a four-hour scale, the cable found a cushion from the lower portion of the Rising Channel, which is placed from July 14 low at 1.1760. While the upper portion is placed from July 13 high at 1.1968. The availability of decent buying interest around the lower portion of the Rising Channel indicates a fresh bullish impulsive wave ahead.

The pound bulls have confidently defended the 200-period Exponential Moving Average (EMA) at 1.2125, which signals the strength of the asset. Also, a golden cross formation by the 50-and 200-EMAs has infused fresh blood in the cable.

Meanwhile, the Relative Strength Index (RSI) (14) is oscillating in the 40.00-60.00 range but is likely to fetch momentum if the asset oversteps 60.00 swiftly.

The cable may initiate a fresh bullish impulsive wave if the asset oversteps Thursday at 1.2212. This will drive the asset towards the round-level resistance of 1.2300, followed by a June 27 high at 1.2332.

On the flip side, a decisive slippage below Thursday's low at 1.2065 will drag the asset towards the psychological support at 1.2000. A downside move from 1.2000 will unleash the greenback bulls and will drag the asset towards July 12 high at 1.1967.

GBP/USD four-hour chart

-637952494617036227.png)

- AUD/USD bulls take a breather after two-day uptrend, eases of late.

- US dollar dropped despite recession fears, mixed data and geopolitical woes.

- Yields remained pressured for the second consecutive day.

- RBA MPS, US NFP will be important, risk catalysts should also be watched carefully for clear directions.

AUD/USD bulls take a breather after a two-day uptrend, recently easing to 0.6965 as the key NFP Friday begins. The pair’s latest moves could be linked to the cautious sentiment ahead of the key Monetary Policy Statement (MPS) from the Reserve Bank of Australia (RBA), as well as the US employment report for July. However, the buyers remain hopeful over the broad US dollar weakness.

That the RBA matched the market’s expectations of announcing 50 basis points (bps) rate hike, the fourth in 2022, while inflating the benchmark rate to 1.85%. However, the RBA Statement that says, “The central bank is not on the pre-set path in normalizing rates,” appeared to have lured the AUD/USD bears after the monetary policy decision, which in turn highlights today’s RBA MPS.

On the other hand, the US Initial Jobless Claims rose to 260K for the week ended on July 30 versus 254K prior and 259K expected. Further, job cuts eased and German Factory Orders improved while the US Goods and Services Trade Balance improved to $-79.6B versus $-80.1B market consensus and $-84.9B revised prior. Despite the mixed data, the market players remained hopeful of the Fed’s aggression but that couldn’t lift the US dollar amid fears of recession.

On Thursday, the Bank of England (BOE) formally accepted the fears of recession and further hardships while Cleveland Fed President Lorretta Mester said that recession risks have increased in the US.

Elsewhere, China’s military drills resulted in missiles landing on the Japanese economic zone and escalated geopolitical fears, adding to the US-China tension over Taiwan.

It should be noted that the firmer Aussie trade numbers and an absence of major instances during US House Speaker Nancy Pelosi’s Taiwan visit, despite the verbal war, also appeared to have underpinned the AUD/USD strength the previous day.

Amid these plays, Wall Street closed mixed but the yields were down for the second consecutive day to 2.69% at the latest, which in turn pressured the US dollar ahead of the key data.

Looking forward, the AUD/USD traders should wait for the RBA’s MPS for clear directions amid fears that the hawks are running out of steam. Following that, the US Nonfarm Payrolls (NFP) for July, expected 250K versus 372K prior, will be crucial for AUD/USD traders to watch for clear directions.

Also read: Nonfarm Payrolls Preview: High expectations set deal the dollar a blow, create buying opportunity

Technical analysis

AUD/USD pair’s successful rebound from a four-month-old previous support line, around 0.6875 by the press time, directs the quote towards a downward sloping resistance line from April 20 and 100-day EMA, close to 0.7025 and 0.7040 in that order.

- Silver price is still directionless amid the lack of tier 1 US economic data.

- Sentiment is fragile due to increased concerns of a recession, as the BoE concedes that the UK might tap into one.

- US Initial Jobless Claims could be a prelude to Friday’s NFP, estimated to add 250K jobs.

Silver price climbs for two straight days, registering gains of 0.51%, as US equities finished mixed, while Asian stock futures are fluctuating as recession fears reignited, courtesy of the Bank of England. That said, alongside a soft US dollar, underpinned by falling US Treasury yields, bolstered the white metal on Thursday. At the time of writing, XAGUSD is trading at $20.14.

Silver trades range-bound, waiting for a catalyst

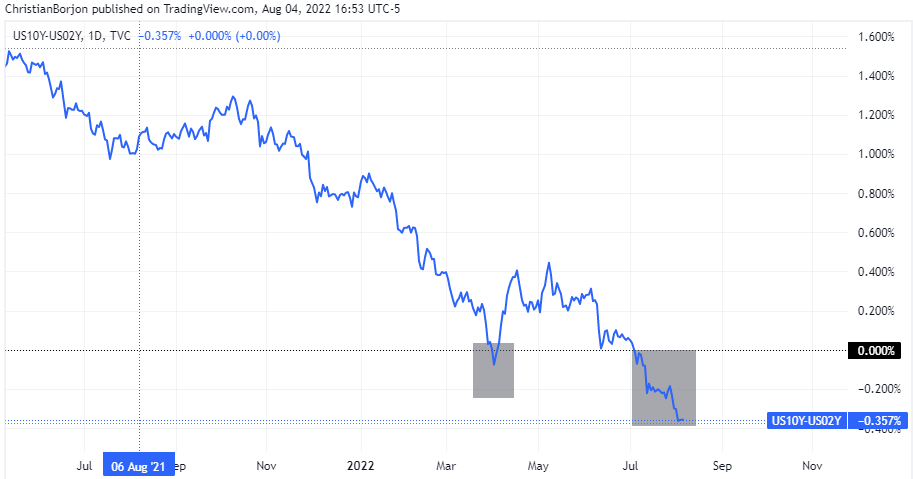

The story of the day is the BoE hiking rates by 50 bps but acknowledged that the UK might tap into a 15-month recession, beginning at the end of the 2022 Q4. Meanwhile, in the US, the 2s-10s yield curve inversion further deepened, sits at -0.357%, and extended to 23 days, while the US 10-year benchmark note rate retraced five bps to 2.694%.

US 2s-10s yield curve inversion

Data-wise, the US calendar featured Initial Jobless Claims for the week ending July 30, which increased by 260K, more than estimated, showing signs that the labor market is easing. At the same time, the US Trade Balance narrowed its deficit from -$80.1 B in May to -$79.6 B in June, propelled by Exports.

In the meantime, the US Dollar Index, a gauge of the buck’s value vs. a basket of peers, tumbled 0.58% at 105.700, accumulating losses from the YTD peak of 3.8%, a tailwind for the dollar-denominated XAGUSD.

Late in the day, Fed speaking, led by Cleveland’s Fed Loretta Mester, reiterated that there’s a path for a soft landing but recognized that recession fears have risen, adding some fuel to the uncertainty confirmed by the UK, recession lingering worldwide.

Shifting to geopolitical jitters, tensions between the US and China persist. In response to US House Speaker Nancy Pelosi’s trip to Taiwan, China fired missiles over Taiwan during military drills, while Japan complained that five of those missiles landed in Japan’s exclusive economic zone. The US National Security spokesman John Kirby said that “China has chosen to overreact,” while adding they’re using the visit to increase military activity around Taiwan.

Those plays, amongst market mood, will keep the silver price fluctuating. Nevertheless, it appears that buyers don’t have the strength to crack the XAGUSD’s 50-day EMA at $20.39.

What to watch

The US economic docket will feature July’s Nonfarm Payrolls estimated at 250K, less than June’s 372K. At the same time, the Unemployment Rate is foreseen to persist unchanged at 3.6%.

Silver (XAGUSD) Key Technical Levels

- Gold price is focused to recapture the psychological resistance of $1,800.00.

- Cleveland Fed President Loretta J. Mester sees interest rates above 4%.

- The downbeat consensus for the US NFP will keep gold bulls solid ahead.

Gold price (XAU/USD) has sensed minor selling pressure after hitting a high of $1,794.91. The precious metal is directed to recapture the psychological resistance of $1.800.00 as the US dollar index (DXY) is facing severe heat despite hawkish commentary from Federal Reserve (Fed) policymakers. Also, the lower consensus for the US Nonfarm Payrolls (NFP) is keeping the DXY on the back foot.

Cleveland Fed President Loretta J. Mester cited on Thursday that the policy tightening measures should not be halted by the Fed without recording downward signs in the price pressures for months. The Fed should raise interest rates to above 4% in order to bring inflation back down to the 2% target. Therefore, the interest should see the continuation of elevation this year and for the next half year. Despite, the hawkish commentary, the DXY bulls failed to capitalize on the same.

On the economic data front, the US NFP will remain the show-stopper event for today. As per the market estimates, the US economy has failed to outperform June’s job additions numbers and has added 250k jobs in the labor market in July. Also, the Unemployment Rate is seen flat at 3.6%. The commentary from big US corporate players indicated that the firms have halted their recruitment process for the remaining year, whose consequences will be displayed in the labor market data. This will keep the gold bulls in the driving seat.

Gold technical analysis

On a four-hour scale, the gold price is facing resistance around the upper portion of the Rising Channel formation. The upper portion of the above-mentioned chart pattern is plotted from July 22 high at $1,739.37 while the lower portion is placed from July 21 low at $1,681.87.

The precious metal is confidently established above the 50-and 200-period Exponential Moving Averages (EMAs) at $1,759.62 and $1,765.06 respectively, which adds to the upside filters.

Also, the Relative Strength Index (RSI) (14) has shifted into the bullish range of 60.00-80.00, which indicates more gains ahead.

Gold four-hour chart

- NZD/USD bears move in within a bullish trend.

- The Us dollar is giving back some ground ahead of NFP.

NZD/USD has started to bleed out although remains 0.45% higher on the day. The US dollar was lower vs. most major currencies on Thursday, down some 0.5% at the time of writing as per the DXY to 105.81. The positive impact of hawkish Federal Reserve comments faded this week while investors waited for more signs on the data front. Friday's Nonfarm Payrolls and next week's inflation data will be critical.

''The Kiwi is back above 0.63 this morning, having capitalised on the downward correction of the USD DXY on the back of lower interest rates. What this has meant is that the NZD has held fairly steady on key crosses like NZD/AUD (although for various other reasons, we have seen volatility on some other crosses, as below),'' analysts at ANZ Bank explained.

''There is no local data today, but the US gets monthly jobs data, and that’s the next key risk event (at 12.30am tonight). Markets aren’t expecting a big jobs print, or a change in the unemployment rate, or the monthly pace of wage growth, and in that regard, the hurdle to an upside surprise seems low. The fall in US bond yields does seem out of character with the tone of Fedspeak, but of course markets remain fearful of a US recession, so it’s all a bit mixed.''

Looking ahead, the Nonfarm Payrolls data likely continued to advance firmly in July but at a more moderate pace after four consecutive job gains at just below 400k in March-June, according to analysts at TD Securities. ''High-frequency data, including Homebase, still point to above-trend job creation. We also look for the UE rate to stay at 3.6% for a fifth straight month, and for wage growth to remain steady at 0.3% m/m (4.9% YoY).''

- EUR/GBP rallied more than 100 pips on Thursday after BoE’s dovish hike.

- Longs remain hopeful of cracking 0.8438, the 200-DMA.

- EUR/GBP Price Analysis: in the near term is upward biased; once buyers break resistance at 0.8438, a rally to 0.8500 is in the cards.

The shared currency benefitted from UK’s macroeconomic news, rising almost 100 pips on Thursday after the Bank of England hiked rates but warned that the country might tap into a 15-month recession. Bolstered by the previously mentioned, the EUR/GBP hit a daily high at the confluence of the 20 and 200-day EMAs around 0.8437-41 region. At the time of writing, the EUR/GBP is trading at 0.8426.

EUR/GBP Price Analysis: Technical outlook

The EUR/GBP daily chart depicts that the pair rallied towards the 0.8437-41 area but failed to crack it, meaning that sellers stepped in. As long as EUR/GBP longs keep the spot price above the July 27 high at 0.8426, buyers could remain hopeful of breaching that ceiling level towards the 100-day EMA at 0.8462. Otherwise, the cross would be vulnerable to sellers, which could send the pair towards 0.8400.

EUR/GBP Hourly chart

The EUR/GBP hour chart illustrates that once the pair hit a daily high at 0.8437, they retreated and is consolidating in the 0.8415-37 range. The RSI further confirms the previously mentioned, exiting from overbought conditions but stills in bullish territory, about to cross over the 7-hour RSI’s SMA. Therefore, the EUR/GBP might print a leg-up, but it would need to break above 0.8437.

Once that scenario plays out, the EUR/GBP’s first resistance will be the July 27 high at 0.8491. Break above will expose 0.8500, followed by the July 25 pivot high at 0.8525.

EUR/GBP Key Technical Levels

- EUR/USD has burst to life leaving an inverse H&S on the daily chart.

- The hourly 38.2% Fibonacci, 50% mean reversion and 61.8% ratio could be an area of support in the coming sessions.

As per the prior analysis, EUR/USD Price Analysis: Bulls eye a break of 1.0171 structure, the bulls have taken control and rallied all the way to 1.0253.

The prior analysis said the bullish correction could eventually result in an upside continuation leaving behind the outcome of an inverted head and shoulders.

EUR/USD daily chart, prior analysis

EUR/USD live market

The price has moved higher as anticipated and there are prospects of a move into the greyed area in the forthcoming days. The bulls will need to overcome the resistance, however between 1.0250 and 1.0300. At this juncture, a pull back on the houly time frame is probable:

The 38.2% Fibonacci, 50% mean reversion and 61.8% ratio could be an area of support in the coming sessions and in the countdown to the Nonfarm Payrolls event to end the week.

What you need to take care of on Friday, August 5:

The dollar fell against most of its major rivals, ending the day near its recent lows, usually a sign of further declines ahead in the near term.

Fears of a global recession returned after the Bank of England announced its latest decision on monetary policy. The central bank hiked rates by 50 bps to 1.75% as expected. But policymakers upwardly revised their inflation forecast while anticipating a recession in the next five quarters. Among other things, Governor Andrew Bailey said that while he understands that raising interest rates will cause financial pain to many, "the alternative is even worse."

Federal Reserve official Loretta Mester stated that recession risks have increased in the US, adding that supply issues are likely to persist for some time. Finally, she said that interest rates should continue to rise at least through this year and the first half of 2023.

The GBP/USD pair plunged to 1.2064 but recovered 100 pips ahead of the daily close. EUR/USD benefited from the broad dollar’s weakness and settled around 1.0250.

AUD/USD advanced and hovers around 0.6970, helped by gold, as the bright metal reached fresh one-month highs in the $1,790 price zone. The USD/CAD pair edged higher and settled at 1.2860, as the CAD was hammered by falling oil prices. The barrel of WTI currently trades at $88.40 a barrel.

Finally, USD/CHF is down to 0.9550, while USD/JPY declined to 132.80.

On Friday, the focus will be on US employment figures. The country will release the Nonfarm Payrolls report, expected to show the country added 250K new jobs in July. The unemployment rate is expected to remain steady at 3.6%.

Ethereum Price Prediction: Too soon to call it quits, too late to walk away

Like this article? Help us with some feedback by answering this survey:

- GBP/USD marches firmly, gaining some 0.17% on Thursday.

- The Bank of England (BoE) raised the Bank Rate to 1.75% in an 8-1 vote.

- Bailey and Co,, acknowledged that the UK would hit a recession, beginning late in 2022.

- US Initial Jobless Claims rose 260K more than expected as the labor market eases.

The British pound recovered some ground vs. the greenback after the Bank of England (BoE) hiked rates 50 bps, the highest increase in 27 years, while it warned that the UK economy would hit a recession during the second half of the year. That said, the GBP/USD seesawed in a volatile session, hitting a daily high at 1.2212 before plunging to 1.2065 daily lows. At the time of writing, the GBP/USD is trading at 1.2165, up by 0.16%.

GBP/USD pares its losses after a BoE’s dovish hike

On Thursday, the BoE raised the Bank Rate to 1.75% in an 8-1 vote, with Sylvana Tenreyro dissenting as she backed a 25 bps. The Bank of England foresees that the UK will tap into a 15-month recession later in the year, projecting GDP to tumble by 1.5% in 2023.

Regarding inflation, the BoE updated its forecast, which increased to 13% in 2022 Q4, more than the 9.4% estimated in June, and acknowledged it will remain elevated through the rest of 2022 and 2023, at the same time consumption further weakens. Additionally, the BoE announced that it would begin reducing its balance sheet by £10 billion a quarter from next month.

Later, after the BoE’s decision, US Initial Jobless Claims for the week ending on July 30 rose by 260K, higher than 259K estimated, a signal that the labor market is easing. Furthermore, the Balance of Trade in the US narrowed the US deficit to -$79.6 B from -$80.1 B estimations, while Exports jumped compared to imports.

All that said, the GBP/USD settled just below the 50-day EMA after a 150 pip volatile session. Although it stays under the daily moving averages (DMA), the Relative Strength Index (RSI) is aiming higher in bullish territory, keeping GBP/USD buyers hopeful of higher prices.

Upwards, the GBP/USD’s next resistance would be 1.2188, the 50-day EMA. On the downside, the first support would be 1.2100.

What to watch

The UK docket will unveil the Halifax House Price Index for July, alongside the BBA Mortgage Rate. On the Us front, the economic calendar will reveal July’s Nonfarm Payrolls figures foreseen at 250K, less than June’s 372K. The Unemployment Rate is expected to persist unchanged at 3.6%.

GBP/USD Key Technical Levels

- Gold bulls have taken charge in the build-up to the NFP showdown.

- Bulls are eyeing a deeper correction towards the golden 61.8% ratio.

The gold price surged on Thursday as the US bond yields fell and the Bank of England warned the United Kingdom's economy could be headed for a recession later this year with inflation rising as high as 13%. XAU/USD has pushed don within its weekly bullish correction to mark a high of $1,794.23. Gold for December delivery was printing above $1,800 per ounce.

Gold has been benefitting from softer US bond yields, bullish for gold since it offers no yield. The US 10-year note was last seen paying 2.699%, down 0.26% on the day. The US dollar was lower vs. most major currencies on Thursday, down some 0.5% at the time of writing as per the DXY to 105.81. The positive impact of hawkish Federal Reserve comments faded this week while investors waited for more signs on the data front. Friday's Nonfarm Payrolls and next week's inflation data will be critical.

The Fed hiked rates by 75 basis points at its meeting in June and July. For now, the money markets are pricing in a 50 basis point hike at the Fed's September meeting, and a roughly 44% chance of another massive 75 bps increase. Today, Loretta J. Mester, president of the Federal Reserve Bank of Cleveland said on Thursday that the Fed should raise interest rates to above 4% in order to bring inflation back down to target.

"I would pencil in going a bit above four as appropriate," Mester told reporters following an event held at the Economic Club of Pittsburgh, in reference to the central bank's policy rate. "It's not unreasonable I think to maintain that as where we're getting to and then we'll see."

- ''We will need to raise interest rates and then hold them there for a while.

- Then we'll bring them back down once inflation gets back closer to our 2% goal.''

Analysts at TD Securities explained that ''while Fedspeak has pushed back against the market's dovish interpretation of the FOMC, and yesterday's data surprised to the upside, seeing rates and pricing of the September hike increase, the gold market is thus far trading with a mind of its own.''

''CTA triggers for additional short covering are coming well within reach. Indeed, we estimate prices closing above $1789/oz would catalyze enough of a shift in momentum to see trend followers target a roughly flat net position,'' the analysts added. ''However, with nonfarm payrolls headlining the week tomorrow, our expectations of a stronger-than-anticipated report could quickly put a cap on the prevailing bullishness among gold bugs.''

The monthly US Nonfarm payrolls report will be closely watched on Friday after data early Thursday showed a tick up in jobless claims.

- Ready for trading the NFP?

''A strong payroll print should help drive a further rebound in the market's pricing in terminal rate pricing. This should pressure front-end rates higher, and continue to flatten the 2s10s curve. We remain short Jan 2023 Fed funds futures to position for Fed rate hikes,'' the analysts at TD Securities said.

Gold technical analysis

As per the prior analysis, Gold Price Forecast: XAU/USD bulls are back in play, it was explained that the price was running higher in a correction of the weekly M-formation:

The grey area was a price imbalance that has now been mitigated by a 50% mean reversion:

There are prospects for further upside with the 61.8% Fibonacci meeting prior structure around $1,800.

Loretta J. Mester, president of the Federal Reserve Bank of Cleveland said on Thursday that the Fed should raise interest rates to above 4% in order to bring inflation back down to target.

"I would pencil in going a bit above four as appropriate," Mester told reporters following an event held at the Economic Club of Pittsburgh, in reference to the central bank's policy rate. "It's not unreasonable I think to maintain that as where we're getting to and then we'll see."

Key quotes

- Business contacts tell me not looking for as many workers as before.

- But these are only nascent signs; labour market still quite strong.

- Fed's framework still stands up with respect to our dual goals.

- But there are lessons to be learned on not having such strict forward guidance again.

- Need to see several months of monthly changes moving down on inflation.

- We will need to raise interest rates and then hold them there for a while.

- Then we'll bring them back down once inflation gets back closer to our 2% goal.

- I would pencil in going a bit above 4% on interest rates.

- That's what I had in my Sep at the last meeting.

- Not unreasonable to think we might have to do a 75 in September; but it could very well be 50 and we'll be guided by the data.

- Interest rates should continue to rise this year and through the first half of next year; then we can maybe pause and start bringing them back down.

US dollar update

Meanwhile, the US dollar was lower vs. most major currencies on Thursday, down some 0.5% at the time of writing as per the DXY to 105.81. The positive impact of hawkish Federal Reserve comments faded this week while investors waited for more signs on the data front. Friday's Nonfarm Payrolls and next week's inflation data will be critical.

- The USD/CHF tumbling below the 100-day EMA could pave the way for a re-test of 0.9470.

- In the near term, the USD/CHF is neutral downwards, and once it clears 0.9550, it could open the door toward 0.9500.

The USD/CHF retraces under the 100-day EMA and shifts the pair’s bias to neutral-downwards as the exchange rate further separates from the previously mentioned moving average (MA) and closes to the August 3 daily low at 0.9542. At the time of writing, the USD/CHF is trading at 0.9655.

USD/CHF Price Analysis: Technical outlook

From a daily chart perspective, the USD/CHF is neutral-to-downward biased reinforced for several reasons. Firstly, the exchange rate is below the 20, 50, and 100-DMAs. Secondly, the Relative Strength Index (RSI) is in negative territory, made a U-turn, from aiming higher, now is headed downwards, narrowing the distance with its 7-day RSI’s MA. Once the RSI crosses under the latter, it confirms the bearish bias.

Therefore, the USD/HF path of least resistance is downwards. The major’s first support would be 0.9542. Once broken, it will expose the 0.9500, followed by the August 2 low at 0.9470.

USD/CHF Hourly chart

The USD/CHF hourly chart illustrates the pair as neutral-to-downward biased. However, the confluence of the S1 daily pivot and the 100-hour EMA around 0.9550 stopped the downtrend at the time of typing. Nevertheless, USD/CHF traders should notice that the Relative Strength Index (RSI) exited from oversold conditions, with its slope aiming higher, so a correction might be on the cards. Therefore, the USD/CHF might aim toward Fibonacci’s 50% retracement at 0.9588 before cracking 0.9550. Once cleared, the major’s next support will be the August 1 daily low at 0.9470.

USD/CHF Key Technical Levels

Following Bank of England’s 50 basis points rate hike, analysts at Dankse Bank still see the case for the EUR/GBP cross to move higher on the near-term. They target the cross at 0.86 in three months.

Key Quotes:

“We change our Bank of England call now expecting another 50bp rate hike in September and another 25bp in November, recognising that the Bank of England is probably not ready to fully stop hiking just yet despite rising recession risks. Further tightening is needed in order to cool extraordinarily high inflation pressure. We expect no rate hikes beyond the November meeting (although another 25bp rate hike in December seems like a close call at this point) and believe markets will start to focus even more on possible rate cuts in 2023 when the UK actually falls into recession.”

“We are slightly more dovish than markets, as the Bank of England has more emphasis on the economic outlook than what markets believe in. We still see a case for EUR/GBP to move slightly higher near-term on relative rates, targeting the cross at 0.86 in 3M. Further out, GBP usually appreciates vs EUR in an environment where USD performs and expect EUR/GBP to move back towards 0.84 in 12M.”

The AUD/USD climbs during the North American session off weekly lows around 0.6880s despite investors’ mixed mood due to increasing tensions post-US House Speaker Pelosi’s visit to Taiwan, with China’s military drills deploying missiles and more than 100 planes, as a response to the trip.

The AUD/USD is trading at 0.6972 after dipping to its daily low at 0.6934 early in the Asian Pacific session. Still, as North American traders got to their offices, the Aussie strengthened, and the major hit a daily high at 0.6989 before settling around current exchange rate levels.

AUD/USD ascends, despite positive US data

US equities wobble as sentiment remains fragile. Based on mixed US economic data, AUD/USD dived from daily highs towards 0.6945. Initial Jobless Claims for the week ending on July 30, uptick to 260K, higher than 259K estimated, illustrating that the labor market is loosening. At the same time, the Balance of Trade in the US witnessed a shrinking in the US deficit to -$79.6 B from -$80.1 B estimations, while Exports jumped in comparison with imports.

Even though US data keeps the traders hopeful of missing a recession, the AUD/USD bounced off once analysts digested data, but the major was unable to reach its daily high.

In the meantime, the US Dollar Index, a gauge of the buck’s value vs. a basket of peers, tumbles 0.50%, at 105.867, underpinned by falling US Treasury yields, led by the 10-year benchmark note coupon at 2.674%, down by three basis points.

On the Australian side, the Trade Balance hit a surplus of A$17.7 B in July, from A$12.3 B in June. Australia has benefitted from Iron ore, LNG gas, and coal exports. Nevertheless, its biggest trading partner, namely China, has been trying to limit its reliance on coal imports, and its steel output will weaken late this year.

Analysts at ANZ commented that “Given this and the fact that commodity prices appear to have peaked, we think the trade surplus will soon start to slide.”

What to watch

The Australian docket will feature the Reserve Bank of Australia (RBA) Statement of Monetary Policy alongside the AIG Services Index.

The US economic calendar will feature July’s Nonfarm Payrolls estimated at 250K, less than June’s 372K. The Unemployment Rate is expected to persist unchanged at 3.6%.

AUD/USD Key Technical Levels

The Central Bank of Brazil (BCB) raised its key interest rate by 50 basis points. Analysts at Wells Fargo believe policymakers will opt for a 25 bps rate hike in September and take the Selic rate to 14.00%. They forecast the USD/BRL exchange rate to reach 5.75 by the end of this year, and 5.95 by year-end 2023.

Key Quotes:

“While we have revised our Selic rate forecast higher, we still believe the outlook for the Brazilian real will be challenging going forward. We share the BCB's concerns of fiscal policy and believe Bolsonaro-led increased social spending will materialize and weigh on the currency ahead of the election. Right now, we would argue Brazil's debt trajectory is still unsustainable. Should Bolsonaro extend spending that is not fiscally prudent or evades the spending cap, market sentiment toward Brazil is likely to turn negative. This is our base case scenario for the Brazilian real, and in the short term, we believe the USD/BRL exchange rate can reach BRL5.75 by the end of 2022 on risks tied to the election.”

“We also believe that increased fiscal spending is likely to become more permanent going forward, regardless of the outcome of the election as both Bolsonaro and Lula have suggested their preference is to eliminate Brazil's fiscal spending cap altogether. We believe this capital flight scenario could pick up momentum over the longer term and the Brazilian real is likely to suffer the consequences.”

“With Brazil's economy already likely on the path toward recession by the end of this year, BCB policymakers are likely to be the first major emerging market central bank to unwind interest rate hikes. As fiscal risks persist well into 2023 and the BCB lowers its Selic rate, BRL depreciation is likely to continue. In that context, we believe the USD/BRL exchange rate can reach BRL5.95 by the end of 2023.”

The Bank of England raised its key interest rate by 50 basis points to 1.75%, as expected. According to analysts from Rabobank, considering the next UK PM is likely to be Liz Truss, they expect 100 basis points in rate hikes during 2022.

Key Quotes:

“Even though the forecast is based on market curves, which takes into account the high probability of Liz Truss receiving the keys of 10 Downing Street, the central bank currently assumes no changes in fiscal policy. This is not realistic. If she will be elected by the Tory membership –and we think she will– it won’t be long before we will see emergency fiscal action. It remains to be seen whether ‘at least £30 billion’, which amounts to nearly 1.5% of GDP, will be deployed, but we expect a combination of significant tax cuts and energy bill rebates to be put in place this autumn.”

“We now expect 100 bps extra rate increases this year: 50 in September, 25 in November and 25 in December. There is a high risk this tightening will be reversed from 2023 H2 onwards.”

“It remains astonishing to see a central bank stepping up its pace of interest rate hikes while forecasting a long recession with a historically weak recovery and a sharp rise in unemployment. It is hard to avoid the conclusion that it has decided a recession and a much softer labour market is necessary to return inflation back towards 2%, even as most of the inflation overshoot finds its origins in international markets.”

The weekly report showed Initial Jobless Claims rose to 260K in the week ended July 30 while Continuing Claims rose to 1.41 million, the highest level since March. The recent trend in jobless continuing claims adds weight to the argument that the US economy is not currently in recession, explained analysts at Wells Fargo. However, they warn that the recent uptick resembles the months that preceded prior recessions, suggesting that the start of a recession may not be far off.

Key Quotes:

“Initial jobless claims have been trending higher since early April in one of the clearest signs that labor market conditions have begun to deteriorate. While jobless claims have a successful track record foreshadowing recession, we find continuing claims to be a better check on whether the economy is already in one. The recent trend in continuing claims adds weight to the argument that the economy is not currently in recession. That said, the recent uptick bears some resemblance to the months that preceded prior recessions, suggesting that the start of a recession may not be far off.”

“While the potential for payrolls to be revised over the next few months or even year limit the conviction with which we can say whether the U.S. economy is in recession, continuing claims add weight to the argument that the recession clock has not started ticking. That said, continuing claims are starting to drift higher and, with the rise in initial claims, suggest the start of a recession might not be far off either.”

“Whether the U.S. economy may already be in a recession is likely to have minimal bearing on the course of Fed policy in the near term, however. With inflation still raging and FOMC members, including Chair Powell, acknowledging that an “over-tight” labor market is contributing to price pressures, we suspect the Fed will be undeterred by the recent slowing in activity both inside and outside the labor market, and it will push ahead with raising the fed funds rate to around 4% in the coming months.”

Data released on Thursday showed the Canadian trade surplus widened to CAD5.0B in June, in line with market expectations. Analysts at CIBC, explained the trade surplus was in somewhat of a holding pattern during June, but should narrow ahead with oil prices having fallen recently.

Key Quotes:

“Exports of goods increased by 2.0% on the month, with oil leading the way. The 3.7% increase in that area was a reflection of both higher volumes and prices, although given the decline in global oil prices seen recently the value of exports in this area has likely peaked for now. While energy remained a key driver to overall exports, non-energy exports were also up by a solid 1.4% compared with the prior month.”

“The trade deficit in services widened modestly from $1.1bn in May to $1.3bn in June, with imports rising faster than exports. While trade in travel services continues to improve on both the import and export side, the 5.6% increase in imports during June easily outpaced the 2.1% gain in exports and still has much further to go before reattaining prepandemic levels. The wider services deficit broadly offset the larger goods surplus in terms of the overall trade balance.”

“The Canadian trade surplus was in somewhat of a holding pattern during June, but should narrow ahead with oil prices having fallen recently. The revision to May leaves imports rising at a much stronger pace than exports during the second quarter as a whole. While that implies that net trade will be a fairly big negative for GDP growth in isolation, it could also signal a stronger rebuilding of inventories or growth in consumer spending as an offset.”

- US dollar losses momentum amid lower US yields.

- After US Jobless Claims attention turns to Friday’s Non-farm payrolls.

- USD/JPY fails again to break 134.50, and drops sharply.

The USD/JPY dropped further after the beginning of the American session and printed a fresh daily low at 133.02. A weaker US dollar weighed on the pair.

US data on focus

Economic data released in the US on Thursday showed an increase in Continuing Claims to the highest level since March; while Initial Claims rose to 260K. The trade deficit narrowed to $99.5B in June, the lowest in five months.

On Friday, the US official employment report is due. Market consensus is for an increase in payrolls by 250K. “Data surprises have been strongly correlated with broad USD variation. An above-consensus print should leave a slightly firmer tone but would expect price action to be somewhat contained. EURUSD bias leans lower but should be contained above 1.01. USDJPY faces more topside extension risk on a break of 134.80/00”, explained analysts at TD Securities.

The dollar is falling modestly across the board on Thursday. The US 10-year yield stands at 2.67% and the 30-year at 2.96%. In Wall Street, the Dow Jones is falling by 0.27% and the Nasdaq 0.37%.

The combination of lower US yields and negative risk sentiment is favoring the yen. The Japanese currency is among the top performs. The USD/JPY is near the 133.00 zone a break lower could open the doors to more losses, with the next support at 132.70 followed by 132.20. On the upside, above 134.50 the dollar should strengthen.

Technical levels

- USD/CAD advances during the day face resistance at the 50-day EMA at 1.2857.

- Falling oil prices and sentiment weighed on the Canadian dollar, a tailwind for the USD/CAD.

- USD/CAD Price Analysis: A break above the 50-day EMA might clear the way to 1.3000; otherwise, 1.2800 is eyed.

The USD/CAD climbs and trims some of Wednesday’s losses, as sentiment is mixed after US House Speaker Pelosi’s trip to Taiwan, increasing regional tensions. China’s military drills commenced as expected, with the country firing missiles in its biggest test in two decades.

After hitting a daily low at 1.2820 and rallying towards 1.2876, a daily high, the USD/CAD is trading at 1.2858, up by 0.18%.

USD/CAD rises on sentiment and on CAD weakness

Sentiment is fragile, as abovementioned. EU and US equities fluctuate, while the greenback is soft, trading at 106.200, down 0.30%, underpinned by falling US bond yields. US employment data, namely the Initial Jobless Claims for the week ending on July 30, rose 260K a thousand more than estimated, indicating that the labor market is easing. The trend will likely continue as the Federal Reserve extends its tightening cycle.

At the same time, the US Balance of Trade deficit narrowed from -$80.1 billion forecasts to -$79.6 billion in June. Exports increased to $260.8 billion, while imports rose to $340.4 billion as expected.

On the Canadian side, the country’s trade surplus widened to C$5.05 billion in June, more than the C$4.8 billion estimated, bolstered by energy products climbing 3.2%, reaching a record high.

In the meantime, falling crude oil prices left the Canadian dollar exposed to further selling pressure as investors sought safety.

What to watch

The Canadian economic docket will update employment conditions in the country, with analysts expecting an increase of 20K jobs added to the economy in July and the Unemployment Rate at 5%. The US economic calendar will feature July’s Nonfarm Payrolls estimated at 250K, less than June’s 372K. The Unemployment Rate is expected to persist unchanged at 3.6%.

USD/CAD Price Analysis: Technical outlook

The USD/CAD has been seesawing with the 50-day EMA in the last three days. Although buyers are in control, per the long-term daily EMAs residing below the spot price, they will face strong resistance at the confluence of the August 3 high and the 20-day EMA at 1.2907, which, if broken, could send the major to test the 1.3000 figure. Otherwise, a fall towards 1.2800 and further, eyeing the 100-day EMA at 1.2779, is in the cards.

- USD/TRY records decent gains just below the 18.00 mark.

- The pair is expected to remain cautious ahead of US NFP.

- The CBRT expects inflation to hit 90% before easing.

The Turkish lira gives away Wednesday’s gains and resumes the downside, lending upside pressure to USD/TRY to the 17.97 level on Thursday.

USD/TRY stays capped by the 18.00 region

USD/TRY extends the consolidative stance in the upper end of the current range just below the 18.00 yardstick on Thursday amidst unclear risk appetite trends and the usual cautiousness among investors in the pre-NFP trade.

In the meantime, the lira remains under scrutiny after inflation figures tracked by the CPI rose to the highest level since September 1998 at nearly 80.0% in July, boosted by high commodity, energy and food prices.

It is worth noting that the Turkish central bank (CBRT) recently revised up its forecast for inflation and now sees consumer prices rising 60.4% by year-end (from 42.8%). Furthermore, the CBRT expects inflation to rise 19.2% by the end of 2023 and 8.8% at some point towards the end of 2024.

The fact that the CPI rose less than expected in July seems to have sparked some optimism in the government after President Erdogan said that consumer prices are expected to slow down to more “appropriate” levels in early 2023, at a time when he stressed that “a price stabilization trend has already started”.

What to look for around TRY

The upside bias in USD/TRY remains unchanged and stays on course to revisit the key 18.00 zone.

In the meantime, the lira’s price action is expected to keep gyrating around the performance of energy and commodity prices - which are directly correlated to developments from the war in Ukraine - the broad risk appetite trends and the Fed’s rate path in the next months.

Extra risks facing the Turkish currency also come from the domestic backyard, as inflation gives no signs of abating (despite rising less than forecast in July), real interest rates remain entrenched in negative figures and the political pressure to keep the CBRT biased towards low interest rates remains omnipresent. In addition, there seems to be no Plan B to attract foreign currency in a context where the country’s FX reserves dwindle by the day.

Eminent issues on the back boiler: FX intervention by the CBRT. Progress (or lack of it) of the government’s new scheme oriented to support the lira via protected time deposits. Constant government pressure on the CBRT vs. bank’s credibility/independence. Bouts of geopolitical concerns. Structural reforms. Presidential/Parliamentary elections in June 23.

USD/TRY key levels

So far, the pair is gaining 0.11% at 17.9360 and faces the immediate target at 17.9694 (2022 high August 4) seconded by 18.2582 (all-time high December 20) and then 19.00 (round level). On the other hand, a breach of 17.1903 (weekly low July 15) would pave the way for 17.0851 (55-day SMA) and finally 16.0365 (monthly low June 27).

Economist at Commerzbank provide their afterthoughts on the latest Bank of England monetary policy decision, announced earlier this Thursday. The UK central bank announced the sixth rate hike in the current cycle and raised its key interest rate by 50 bps to 1.75%.

Key Quotes:

“The reason for the sharp hike is increasing inflationary pressure. According to the BoE, the labor market remains tight and domestic cost and price pressures are high. The central bank now forecasts inflation to peak at 13% in the fall. Inflation concerns obviously outweighed the economic slowdown – the BoE expects a recession in the UK from the fourth quarter.”

“The BoE would take the necessary decisions to bring inflation back to the 2% target, it said. In doing so, the Committee will be particularly alert to indications of more persistent inflationary pressures, and will if necessary act forcefully in response.”

“In our assessment, the interest rate hikes so far have not been sufficient to get inflation under control. At 1.75%, the bank rate has probably not even reached the "neutral level" at which the economy is neither boosted nor dampened. We therefore continue to expect further interest rate hikes to 2.75% by early 2023. However, following the most recent sharp tightening and against the backdrop of the weaker economy, we believe it is likely that the next meeting in September will see another smaller step of 25 basis points.”

Analysts at TD Securities (TDS) offered a brief preview of the Canadian monthly employment report, due for release on Friday. The data would influence the loonie and provide some meaningful impetus to the USD/CAD pair.

Key Quotes:

“We look for job growth of 38k in July, driven by a partial rebound for trade services and natural resources after their sharp decline in June. Full-time hiring should lead the increase, while stronger labour force participation should keep unemployment stable at 4.9%. We also expect to see wage growth firm to 6.0% y/y in July, although AHE (Average Hourly Earnings) should slow on a m/m basis.”

“The CAD is most correlated with US equities and broad USD variation, neither of which will be affected by this data release. 1.28/29 range should persist and dips in USDCAD are a fade.”

“Overall direction will depend on the Treasury market, but an upside surprise on jobs supports both wider Canada-US spreads and a flatter curve domestically.”

- Gold scales higher through the early North American session and refreshes one-month high.

- Geopolitical tensions, recession fears, softer US bond yields, weaker USD offer some support.

- Signs of stability in the financial markets act as a headwind ahead of the NFP report on Friday.

Gold eased a bit from a fresh one-month high touched during the early North American session and sliped back below the $1,780 level in the last hour. The XAU/USD, however, maintains its positive tone for the second straight day and is trading with gains of nearly 0.70% for the day.

Investors remain worried about a global economic downturn, which along with China's heightened military threats, continue to act as a tailwind for the safe-haven gold. China holds its largest-ever military exercises around Taiwan in retaliation to US House Speaker Nancy Pelosi's visit to the island. In the latest development, China on Thursday said that it conducted “precision missile strikes” in the Taiwan Strait as part of military exercises. The five missiles fired by China landed within Japan's exclusive economic zone and raises tensions in the region.

Apart from this, a modest US dollar weakness turns out to be another factor further underpinning the dollar-denominated gold. Despite more hawkish remarks by several Fed officials this week, investors have been pushing back against the idea of a larger rate hike at the September FOMC meeting. This is evident from a softer tone around the equity markets, which keeps the USD bulls on the defensive and lends some support to the non-yielding yellow metal. That said, signs of stability in the equity markets capped any further for the commodity, at least for the time being.

Investors also seem reluctant to place aggressive bets and prefer to wait for a fresh catalyst from the closely-watched US monthly jobs data. The popularly known NFP is scheduled for release on Friday and will play a key role in influencing the near-term USD price dynamics. Apart from this, geopolitics, along with the broader market risk sentiment, would assist traders to determine the next leg of a directional move for gold.

Technical levels to watch

- Initial Jobless Claims rose by 6,000 in the week ending July 30.

- US Dollar Index continues to fluctuate above 106.00 after the data.

There were 260,000 initial jobless claims in the week ending July 30, the weekly data published by the US Department of Labor (DOL) showed on Thursday. This print followed the previous week's print of 254,000 and came in slightly worse than the market expectation of 259,000.

Further details of the publication revealed that the advance seasonally adjusted insured unemployment rate was 1% and the 4-week moving average was 254,750, an increase of 6,000 from the previous week's revised average.

"The advance number for seasonally adjusted insured unemployment during the week ending July 23 was 1,416,000, an increase of 48,000 from the previous week's revised level," the publication further revealed.

Market reaction

The US Dollar Index showed no immediate reaction to these comments and was last seen posting small daily losses at 106.20.

- EUR/USD regains poise and approaches 1.0200 on Thursday.

- Price action remains stuck with the 1.0100-1.0300 range.

EUR/USD reverses part of the weekly pullback and manages to retest the vicinity of the 1.0200 region on Thursday.

In light of key releases in the US docket on Friday, the pair is expected to keep the current 1.0100-1.0300 range broadly in place for the time being. The loss of the lower bound of the range could see a potential visit to the parity level return to the radar.

In the longer run, the pair’s bearish view is expected to prevail as long as it trades below the 200-day SMA at 1.0934.

EUR/USD daily chart

Bank of England (BoE) Governor Andrew Bailey is delivering his remarks on the policy outlook and responding to questions from the press following the bank's decision to hike the policy rate by 50 basis points to 1.75%.

Key takeaways

"If there are very high wage rises, then we will get persistent inflation."

My concern isn't about any wage increase, but about high wage increases."

"We don't target the exchange rate, we factor in impact of exchange rate on future inflation."

"Larger Fed rate rises reflect different shocks faced by the UK and the US.

About Andrew Bailey (via bankofengland.co.uk)

"Andrew Bailey previously held the role of Deputy Governor, Prudential Regulation and CEO of the PRA from 1 April 2013. While retaining his role as Executive Director of the Bank, Andrew joined the Financial Services Authority in April 2011 as Deputy Head of the Prudential Business Unit and Director of UK Banks and Building Societies. In July 2012, Andrew became Managing Director of the Prudential Business Unit, with responsibility for the prudential supervision of banks, investment banks and insurance companies. Andrew was appointed as a voting member of the interim Financial Policy Committee at its June 2012 meeting."

- GBP/USD dives to a fresh weekly low after the BoE announced its policy decision.

- Ascending trend-channel breakdown supports prospects for a further downfall.

- Attempted recovery towards the 1.2100 mark could be seen as a selling opportunity.

The GBP/USD pair extends the post-Bank of England downfall and has now retreated around 140 pips from the daily high - levels just above the 1.2200 mark. The pair maintains its heavily offered tone through the early North American session and is currently trading near the weekly low, just above the mid-1.2000s.

The BoE warned that a UK recession will begin in the fourth quarter and last all the way through next year and said that the monetary policy is not on a pre-set path. This suggests that the UK central bank would adopt a more gradual approach to raising interest rates, which, in turn, weighs heavily on the British pound.

The GBP/USD pair loses ground for the third successive day and fails to gain any respite from subdued US dollar price action. This, along with a convincing break below a three-week-old ascending trend-channel support, near the 1.2140 area, and a subsequent fall below the 1.2100 mark supports prospects for additional losses.

The negative outlook is reinforced by the fact that technical indicators on the daily chart have just started drifting into bearish territory. Hence, some follow-through weakness towards testing intermediate support near the 1.2030-1.2025 area, en-route the 1.2000 psychological mark, now looks like a distinct possibility.

The downward trajectory could further get extended towards the 1.1945-1.1940 region before the GBP/USD pair eventually drops to sub-1.1900 levels.

On the flip side, the 1.2100 mark now becomes immediate strong resistance. Any further recovery could be seen as a selling opportunity and is likely to remain capped near the ascending channel support breakpoint, around the 1.2140 region. The latter should now act as a key pivotal point for short-term traders.

GBP/USD 4-hour chart

-637952127226044103.png)

Key levels to watch

Bank of England (BoE) Governor Andrew Bailey is delivering his remarks on the policy outlook and responding to questions from the press following the bank's decision to hike the policy rate by 50 basis points to 1.75%.

Key takeaways

"We would have had to raise interest rates in double digits last year to fully offset current inflation, causing far deeper recession than now forecast."

"Parts of UK economy are still going forward strongly, including in job market."

"Pass-through of BOE rate rises has been faster to borrowers than to savers so far."

"Important that savers receive the return they should."

About Andrew Bailey (via bankofengland.co.uk)

"Andrew Bailey previously held the role of Deputy Governor, Prudential Regulation and CEO of the PRA from 1 April 2013. While retaining his role as Executive Director of the Bank, Andrew joined the Financial Services Authority in April 2011 as Deputy Head of the Prudential Business Unit and Director of UK Banks and Building Societies. In July 2012, Andrew became Managing Director of the Prudential Business Unit, with responsibility for the prudential supervision of banks, investment banks and insurance companies. Andrew was appointed as a voting member of the interim Financial Policy Committee at its June 2012 meeting."

- GBP/JPY comes under intense selling pressure after the BoE warns of an economic downturn.

- The BoE now expects that a UK recession will begin in Q4 and last all the way through next year.

- Reviving demand for the safe-haven JPY also contributes to the intraday slide of nearly 250 pips.

The GBP/JPY cross witnesses a dramatic turnaround from the vicinity of the 164.00 mark, or a one-week high touched earlier this Thursday. Spot prices dive to the mid-161.00s. tumbling nearly 250 pips after the Bank of England announced its policy decision.

The British pound weakens across the board after the BoE warned that a UK recession will begin in the fourth quarter and last all the way through next year. Furthermore, the UK central bank said that the monetary policy is not on a pre-set path. This suggests that the BoE is more likely to slow down the pace of its tightening cycle, which, in turn, weighs heavily on sterling and prompts aggressive selling around the GBP/JPY cross.

The intraday selling pressure remains unabated during the post-meeting press conference, where BoE Governor Andrew Bailey noted that the uncertainty surrounding the outlook is exceptionally high. This overshadowed the BoE's historic move to hike benchmark interest rates by 75 bps - the most since 1995 - to 1.75%, or the highest level since late 2008. Meanwhile, reviving demand for the safe-haven Japanese yen exerted additional pressure on the GBP/JPY cross.

The latest leg down suggests that this week's recovery from over a two-month low has run out of steam and supports prospects for a further near-term depreciating move for the GBP/JPY cross. Hence, some follow-through downfall, back towards the 161.00 round-figure mark, now looks like a distinct possibility. Any attempted recovery move could now be seen as a selling opportunity and runs the risk of fizzling out rather quickly.

Technical levels to watch

Bank of England (BoE) Governor Andrew Bailey is delivering his remarks on the policy outlook and responding to questions from the press following the bank's decision to hike the policy rate by 50 basis points to 1.75%.

Key takeaways

"Inflation that is concentrated on essentials hits those on lowest incomes the hardest."

"If we don't bring inflation back to target, things will get worse for those who are least well-off."

"Alternatives to not raising interest rates are even worse, in terms of persistent inflation."

"We see upside risks to inflation over next year, risks are balanced after that."

"Very important that we have moved away from a framework of predictive forward guidance."

"Notwithstanding slowing demand, our agents tell us that businesses feel they can raise prices to meet higher costs."

"I don't think critics have a point when they say BOE is slamming on the brakes at the wrong time."

About Andrew Bailey (via bankofengland.co.uk)

"Andrew Bailey previously held the role of Deputy Governor, Prudential Regulation and CEO of the PRA from 1 April 2013. While retaining his role as Executive Director of the Bank, Andrew joined the Financial Services Authority in April 2011 as Deputy Head of the Prudential Business Unit and Director of UK Banks and Building Societies. In July 2012, Andrew became Managing Director of the Prudential Business Unit, with responsibility for the prudential supervision of banks, investment banks and insurance companies. Andrew was appointed as a voting member of the interim Financial Policy Committee at its June 2012 meeting."

Five missiles fired by China landed within Japan's exclusive economic one, Kyodo news agency reported on Thursday, citing a Japanese foreign ministry official.

"Japan lodged a stern protest against China," the official added and noted that this is the first time Chinese ballistic missiles have landed within Japan's exclusive economic zone.

Meanwhile, Taiwan urged China to be rational and restrain itself. "China's heightened military threats have unilaterally damaged the status quo and stability of the Indo-Pacific region," the island's presidential office said in a post on its official Facebook account.

Market reaction

US stock index futures showed no immediate reaction to this report and were last seen posting small daily gains.

Bank of England (BoE) Governor Andrew Bailey is delivering his remarks on the policy outlook and responding to questions from the press following the bank's decision to hike the policy rate by 50 basis points to 1.75%.

Key takeaways

"BOE will not comment on Conservative leadership candidates' plans."

"BOE has a very clear mandate of price stability."

"Consequences of Russia's actions in Ukraine have a serious economic impact."

"Political pressures have been very well managed since BOE independence."

"I have not abandoned the narrow path analogy for UK policy outlook."

"A number of central banks have a similar narrow path to tread."

About Andrew Bailey (via bankofengland.co.uk)

"Andrew Bailey previously held the role of Deputy Governor, Prudential Regulation and CEO of the PRA from 1 April 2013. While retaining his role as Executive Director of the Bank, Andrew joined the Financial Services Authority in April 2011 as Deputy Head of the Prudential Business Unit and Director of UK Banks and Building Societies. In July 2012, Andrew became Managing Director of the Prudential Business Unit, with responsibility for the prudential supervision of banks, investment banks and insurance companies. Andrew was appointed as a voting member of the interim Financial Policy Committee at its June 2012 meeting."

- DXY trades without a clear direction around 106.40.

- Occasional bullish attempts target the weekly high near 107.40.

DXY attempts a consolidative move in the 106.50 region on Thursday amidst a cautious tone prior to the release of July’s Nonfarm Payrolls on Friday.

In the meantime, occasional gains in the index should meet the initial resistance at the post-FOMC top at 107.42 (July 27), which is deemed as the last defense for an assault of the 2022 high at 109.29 (July 14).

Further near-term upside remains on the cards while above the 6-month support line, today at 104.15.

Furthermore, the broader bullish view in the dollar remains in place while above the 200-day SMA at 99.68.

DXY daily chart

Bank of England (BoE) Governor Andrew Bailey is delivering his remarks on the policy outlook and responding to questions from the press following the bank's decision to hike the policy rate by 50 basis points to 1.75%.

Key takeaways

"Faster policy tightening now reduces the risk of a more extended and costly tightening cycle later."

"50 bp rate rise today does not mean we are now moving to a pre-determined path of raising rates by 50 bp per meeting."

"All options are on the table for the September meeting and beyond."

About Andrew Bailey (via bankofengland.co.uk)