- Analiza

- Novosti i instrumenti

- Vesti sa tržišta

Forex-novosti i prognoze od 23-08-2022

Federal Reserve's Neel Kashkari is crossing the wires with his comments dripping through throughout early Asia.

His pivot on his outlook for rates impacted recently when he said the ''Fed is far, far, far away from declaring victory on inflation'' following the recent surprise fall in inflation data. This is when prices rose 8.5% on an annualized basis in July, a slower pace than the 9.1% rise reported in June and below analysts' consensus expectations for an 8.7% rise.

Key comments

Half to two-thirds of US high inflation is driven by supply-side shocks.

There is some evidence supply chains are beginning to normalize.

We need to get some help on the supply side to get inflation down.

The more help we get from the supply side, the less fed has to do and better able to avoid a hard landing.

We need to make sure the underlying inflation trend gets back down to 2%.

We need to tighten monetary policy.

Right now there is no tradeoff between employment and inflation mandates.

If inflation was at 4%, I would be more willing to say let's take our time, and avoid the risk of overdoing it.

With inflation at 8% or higher, we don't want to allow inflation expectations to unanchor.

We can only relax on rate hikes when we see compelling evidence inflation is heading toward 2%.

Fear in the back of the mind is that inflation is more embedded at a higher level than appreciation.

A lot of balance sheet tightening has already happened due to forward guidance.

The biggest fear is that we are misreading underlying inflation dynamics.

Market implications

Old news has failed to move the needle and the greenback remains pressured albeit within a bullish correction on the lower timeframes:

The overall picture is that the Fed has hiked rates from near zero in March to their current range of 2.25% to 2.50%, with more expected in the months ahead.

Kashkari has flipped more hawkish as of late as the Fed tries to tame inflation, which is running near a 40-year high.

However, while WIRP suggests a 50 bp hike is fully priced in for the September 20-21 FOMC meeting, the odds of a 75 bp hike could start to dwindle and weigh on the greenback, reviving the bull's hopes elsewhere.

Nevertheless, analysts at TD Securities argued that with regards to the Jackson Hole that is coming up later this week, the Fed's Chair, Jerome Powell's speech ''will likely aim to reinforce the message that multiple, sizable hikes are still in the pipeline, and easing should not be expected to be on the horizon anytime soon.''

US treasury auction

Meanwhile, we were seeing a bid back into the greenback and US yields following today's bullish 2-year Treasury auction.

- High yield 3.307%.

- Tail 1.4 bps vs a 6-month average of -0.3 bps.

- Bid to cover 2.49X vs 6-month avg of 2.59X.

- Dealers 23% vs a 6-month average of 17.4%.

- Directs 17.3 vs a 6-month average of 22.2%.

- Indirects 59.7% vs a 6-month average of 60.4%.

The demand from domestic and international buyers is far below a 6-month average which has seen the 2 and 10-year yields rally, supporting the US dollar and weighing on gold prices in the recent hours since the auction:

- EUR/JPY is expected to display more weakness on a downside move below 136.00.

- An energy supply halt for three days could dampen the already vulnerable German energy market.

- Japan’s dismal PMI numbers despite prolonged dovish BOJ is a big reason to worry.

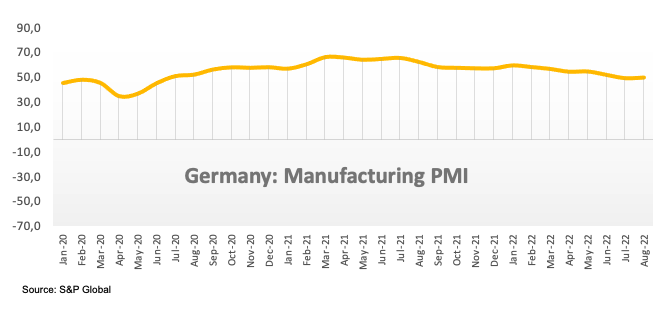

The EUR/JPY pair has displayed a short-lived pullback to near 136.40 after the shared currency bulls defended an establishment below 136.00. The asset defended further losses on mixed German Purchasing Managers Index (PMI) numbers, released on Tuesday.

The German Services PMI contracted to 48.2 against the forecast of 49 and the former release of 49.9. However, the Manufacturing PMI expanded to 49.8 from the expectations of 48.2 and the prior release of 49.3. It is worth noting that Germany is displaying a decline in the Manufacturing PMI consecutively for the past six months and the unavailability of downside exhaustion could have soared Germany’s recession fears.

Now, the entire focus of the market participants is on energy supply in Germany as Nord Stream 1 pipeline is going under unscheduled maintenance, and the winter season is coming in when demand for energy surges sharply.

Russia will halt natural gas supplies to Europe for the last three days of August to run the unscheduled maintenance under the Baltic Sea to Germany. The unexpected natural gas supply cut to Germany from Nord Stream 1 pipeline will accelerate the imbalance of the energy demand-supply mechanism. Investors should be aware of the fact that Germany is a core European Union (EU) member and an occurrence of an energy crisis in Germany could drag the shared currency.

On the yen front, investors have ignored the downbeat Japan PMI numbers despite the continuation of an ultra-loose monetary policy by the Bank of Japan (BOJ). Dismal PMI numbers by the Western leaders are the consequences of tight monetary policy by the Western central banks. However, the BOJ keeps on flushing liquidity in the economy and dismal PMI numbers at the same time are a big reason to worry.

- GBP/JPY marginally advances almost 0.05% on Wednesday’s Asian session.

- The GBP/JPY is seesawing in the 161.00-162.30 area, unable to break beyond the range.

The GBP/JPY is almost flat as the Asian session begins, still below the 20-day EMA for the third consecutive trading day, whilst price action continues to record successive series of lower highs and lows. At the time of writing, the GBP/JPY Is trading at 161.86.

Sentiment has improved, as shown by Asian equities set to open higher. GBP/JPY Tuesday’s price action illustrates the pair seesawing between 161.00-162-30, while all the hourly moving averages (HMAs) meandering around the exchange rate are almost flat.

GBP/JPY Price Analysis: Technical outlook

The GBP/JPY daily chart illustrates the pair as neutral biased. Helped by the GBP/USD recovery, the British pound edged higher, after recording a fresh five-daily low at 160.80, bounced off to close the session around 161.77. That said the GBP/JPY printed back-to-back doji’s, meaning indecision lurks in the pair.

In the near term, the GBP/JPY hourly chart illustrates the pair fulfilling the head-and-shoulders chart pattern target. Once the target was achieved, the GBP/JPY rallied sharply, testing a downslope trendline, drawn from the August 17 high around 163.56, which confluences with the 200-hour EMA at 161.96.

A breach of the latter will expose the 162.00 figure, followed by the August 22 high at 162.30, followed by the R1 pivot at 162.47. On the flip side, the GBP/JPY first support would be the daily pivot at 161.62. Break below will expose the figure at 161.00, immediately followed by the S1 pivot at 160.94.

GBP/JPY Key Technical Level

Reuters shared a research note from Goldman Sachs during early Wednesday in Asia. The report said, “Goldman economists said the message will be the same as laid out in his July news conference and in the minutes of the July Federal Open Market Committee meeting released last week.”

Key quotes

He is likely to balance that message by stressing that the FOMC remains committed to bringing inflation down and that upcoming policy decisions will depend on incoming data.

Policymakers saw the easing of financial conditions since July as unhelpful to keeping the economy on a below-potential growth trajectory.

Goldman expects the FOMC to hike rates by 50 basis points (bps) in September and by 25 bp in November and December, less aggressive than the 75 basis-point hikes at each of its last two meetings.

Also read: EUR/USD Forecast: A small respite for the shared currency

- USD/CHF retreats from monthly top as buyers struggle after six-day uptrend.

- 61.8% Fibonacci retracement triggered pullback amid overbought RSI, looming bear cross on MACD.

- 200-SMA, two-week-old ascending trend line restricts immediate downside.

USD/CHF keeps the previous day’s pullback from a one-month high as sellers flirt with the 50% Fibonacci retracement of the July-August downside during Wednesday’s Asian session. That said, the Swiss currency (CHF) pair remains pressured at around 0.9640 by the press time.

In doing so, the quote portrays a reversal from the 61.8% Fibonacci retracement, known as the golden ratio, amid the RSI retreat from the overbought territory and an impending bear cross of the MACD.

It’s worth noting, however, that the 200-SMA and an upward sloping support line from August 11, respectively around 0.9615 and 0.9590, challenge the USD/CHF bears.

Should the pair decline below 0.9590, the odds of witnessing a slump towards the 23.6% Fibonacci retracement level surrounding 0.9490 appear brighter. Following that, the monthly low of 0.9370 will be in focus.

Meanwhile, recovery moves remain elusive unless crossing the golden ratio, around 0.9690.

Even so, the July 13 swing low near 0.9750 precedes the previous monthly high surrounding 0.9885 could lure the USD/CHF bulls.

USD/CHF: Four-hour chart

Trend: Further downside expected

- EUR/USD is juggling in a 13-pip range as investors await US Durable Goods Orders data.

- The US Durable Goods Orders data is likely to trim to 0.5% vs. 2%.

- A mixed German PMI helped EUR/USD in bottoming out after hitting a multi-year low of 0.9900.

The EUR/USD pair is displaying back and forth moves in a narrow range of 0.9959-0.9972 in the early Tokyo session. The asset has turned sideways after a mild correction from 1.0012 and is expected to continue its lackluster performance as investors are awaiting the release of the US Durable Goods Orders data.

On Tuesday, the asset printed a multi-year low near 0.9900 as the US dollar index (DXY) got strengthened. However, the release of mixed German Purchasing Managers Index (PMI) data helped the asset in bottoming out quickly. The German Manufacturing PMI improved to 49.8 from the expectations of 48.2 and the prior release of 49.3. However, the Services PMI contracted to 48.2 against the forecast of 49 and the former release of 49.9.

The shared currency bulls attempted to regain the territory above the magical figure of 1.0000 after the US dollar index (DXY) tumbled on poor US PMI data. The Services PMI contracted vigorously to 44.1 against the forecast of 49.2 and the prior release of 47.3. Also, the Manufacturing PMI landed lower to 51.3 vs. estimates of 52 and the prior release of 52.2.

The Eurozone bulls still have a chance to establish above the 1.0000 figure if US Durable Goods Orders also get contracted. As per the market consensus, the economic data is expected to slip to 0.6% against the former figure of 2%. In times, when the US economy has already displayed an unchanged US core Consumer Price Index (CPI), a decline in the economic data is not lucrative for the US dollar index (DXY).

- NZD/USD fades bounce off monthly low amid fears of economic slowdown, Fed’s aggression.

- Tepid US data triggered DXY pullback ahead of Friday’s key Jackson Hole Speech form Fed’s Powell.

- Light calendar allows risk catalysts to keep driver’s seat, US data eyed for fresh impulse.

NZD/USD retreats towards 0.6200 during the initial Asian session on Wednesday, after bouncing off the monthly low, as the market’s fears of economic slowdown and the Fed’s aggression remain intact ahead of this week’s key data/events. Also challenging the quote could be looming concerns over China and a light calendar that allows traders to consolidate recent moves.

US Dollar Index (DXY) poked the yearly high during the initial Tuesday trading amid fears of recession and increasing hawkish Fed bets, as well as growing pessimism in China. However, downbeat US economics triggered the greenback’s much-needed correction ahead of today’s Durable Goods Orders for July, not to forget Friday’s speech from Fed Chairman Jerome Powell at the Kansas City Fed’s symposium in Jackson Hole.

That said, preliminary readings of the US S&P Global Manufacturing PMI for August eased to 51.3 versus 52.0 expected and 52.2 prior while the Services gauge plunged to 44.1 from 47.3, compared to 49.2 market forecasts. According to S&P Global, the US economy is also in trouble as the Composite PMI shrank to 45, its lowest in 27 months.

Furthermore, the US New Home Sales for July dropped to the lowest levels in six years, to 0.511M from 0.585M prior and 0.575M market forecasts. Furthermore, the US Richmond Fed Manufacturing Index for August dropped to -8.0 compared to the 0.0 previous reading.

While the downbeat data allowed the USD bulls to take a breather, the yields remained firmer and Wall Street also failed to hold initial gains by closing with mild losses.

It’s worth noting that the market’s bets on the 75 basis points (bps) of Fed rate hike in September increase gradually despite the latest downbeat US data, which in turn also keeps the US dollar buyers hopeful ahead of crucial catalysts.

Talking about recession woes, the European energy crisis is getting worse amid Nord Stream 1 maintenance and fears of more geopolitical tension between Russia and Ukraine. On the same line could be the fears that China will have to go through a recession despite all efforts. Bloomberg recently came out with an analysis portraying the domestic currency yuan’s fall as another worry for the dragon nation. “The Chinese yuan’s slump to its weakest against the dollar in almost two years adds to what is already a precarious balancing act for Beijing, which is seeking ways to prop up its struggling economy without stoking financial instability,” said the piece.

To sum up, NZD/USD bears remain hopeful despite the latest corrective bounce. However, today’s US Durable Goods Orders for July, expected 0.6% versus 2.0% prior, will be important to watch for clear directions, not to forget the risk catalysts.

Technical analysis

NZD/USD rebound failed to provide a daily closing beyond the 50-DMA, around 0.6235 by the press time, which in turn joins bearish MACD signals and downbeat RSI to direct the quote towards 61.8% Fibonacci retracement of July-August upside, near 0.6190.

- AUD/JPY extended its gains to four consecutive days,

- Worldwide weaker than expected S&P Global PMIs reignited recession fears, but the AUD held to gains.

- If the AUD/JPY breaks above 95.00, it will pave the way towards the YTD high at 96.88; otherwise, a re-test of 93.00 is on the cards.

The AUD/JPY marginally advances as the Asian session begins up by 0.01%, carrying on the momentum gathered on Tuesday, when the cross-currency pair finished the session with solid gains of 0.24%. At the time of writing, the AUD/JPY is trading at 94.69.

On Tuesday, the AUD/JPY price action witnessed the pair opening around the 94.50 area, followed by a dip towards its daily low at 94.10. However, despite a dismal sentiment in the financial markets, courtesy of dismal S&P Global PMIs readings across the globe, the AUD/JPY rallied towards its daily high at 94.85 before retreating toward current price levels.

AUD/JPY Price Analysis: Technical outlook

The AUD/JPY advance now totals four consecutive days of gains. Worth noting that on its way north, AUD/JPY buyers reclaimed the 20, 50, and 100-day EMAs. However, they had failed to clear a three-month-old downslope trendline drawn from June highs near the 94.80-95-00 area. A breach of the latter will clear the way towards the YTD high at 96.88, but buyers will need to reclaim the 96.00 mark.

In the near term, namely the 4-hour chart, the AUD/JPY is facing solid resistance around the abovementioned trendline, putting a lid to AUD/JPY’s higher prices. Additionally, the pair is trading below an upslope trendline drawn from August 16 lows, which, acting as resistance, has kept the cross-currency pair seesawing within the 94.10-80 range.

All that said, the AUD/JPY is trading sideways. Therefore, a break above 94.80 would pave the way towards the 95.00 figure, followed by 96.00 and the YTD high at 96.88. On the flip side, the AUD/JPY first support will be the confluence of the 20-EMA and the daily pivot at around 94.57, followed by the S2 pivot at 94.28, and the confluence of the 100 and 200-EMA at 94.22.

AUD/JPY Key Technical Levels

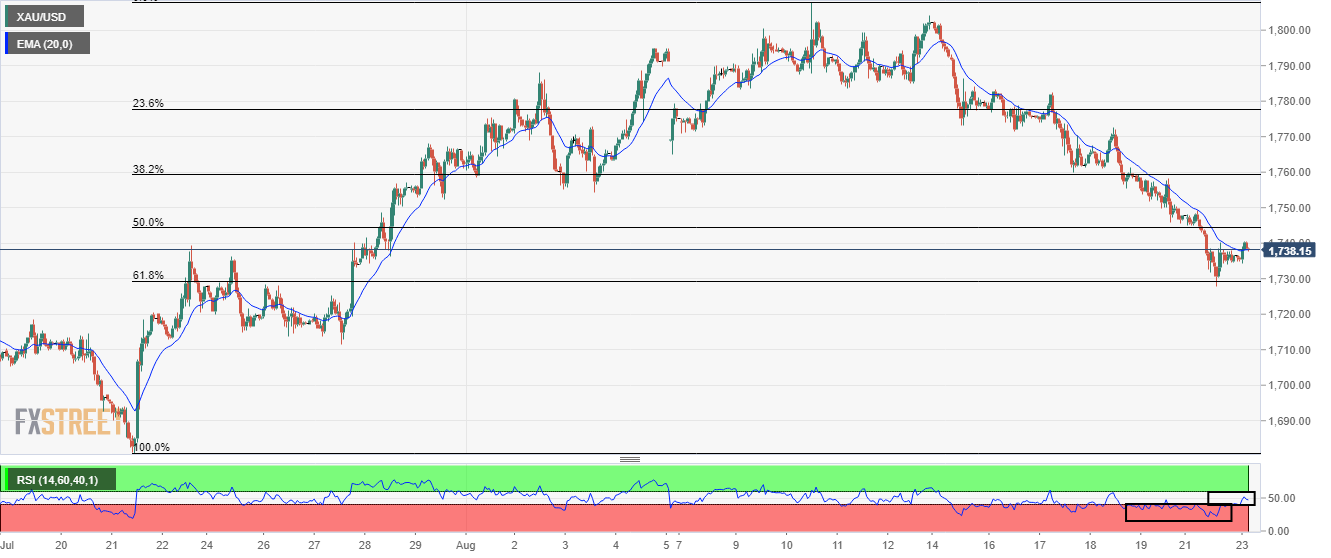

- Gold price is aiming to recapture the immediate hurdle of $1,750.00.

- Investors are focusing on the US Durable Goods Orders data for further cues.

- The downbeat US PMI is the consequence of hiking interest rates by the Fed vigorously.

Gold price (XAU/USD) has attempted a rebound after a mild correction to near $1,746.00. A rebound move is less-confident, at the press time, but is expected to gain momentum as investors are likely to discount poor consensus for the US Durable Goods Orders data.

Earlier, the gold prices displayed a sheer upside after a contraction in Purchasing Managers Index (PMI) numbers. The Manufacturing PMI contracted to 51.3 from the estimates of 52 and the prior release of 52.2. The Services PMI remained more vulnerable and contracted dramatically to 44.1 against the forecast of 49.2 and the prior release of 47.3.

This is a warning signal for the Federal Reserve (Fed) to slow down the pace of hiking interest rates as the unavailability of cheap money has restricted the private sector from exploiting entire production capacities.

Going forward, the US economy will see another consequence of price pressures in the form of a decline in the overall demand. Soaring price pressures have resulted in higher payouts for households. Due to the inevitable demand for necessity goods, households are surrendering demand for durable goods, which may weigh pressure on the US dollar index (DXY) further.

Gold technical analysis

On an hourly scale, gold prices are attempting to cross the 61.8% Fibonacci retracement (placed from July 27 low at $1,711.53 to August 10 high at $1,807.93) at $1,748.38 comfortably. The 20-and 50-period Exponential Moving Averages (EMAs) are on the verge of providing a bullish crossover at $1,744.38.

Meanwhile, the Relative Strength Index (RSI) (14) has shifted into the bullish range of 60.00-80.00, which indicates more upside ahead.

Gold hourly chart

- GBP/USD pares the week-start rebound from multi-month low.

- Bearish chart pattern, key SMAs challenge buyers even as RSI, MACD favor further recovery.

- The longer-term falling channel adds barriers to the trading filters.

GBP/USD rebound fails to gain acceptance inside a one-week-old descending trend channel. That said, the cable pair seesaws around the resistance line of the stated bearish chart pattern, close to 1.1835 during the initial Asian session on Wednesday.

In addition to the aforementioned channel’s top, near 1.1855, the 100-HMA and the 200-HMA could also challenge GBP/USD bulls around 1.1870 and 1.1990 in that order.

GBP/USD: Hourly chart

Trend: Further weakness expected

Following that, the 1.2000 psychological magnet and convergence of the 21-DMA and the 50-DMA on the daily chart will be crucial for the pair buyers to watch.

Above all, the upper line of the downward sloping trend channel from mid-May, close to 1.2200, appears the last defense of the GBP/USD sellers.

GBP/USD: Daily chart

Trend: Bearish

It’s worth noting that the MACD and RSI are both suggesting short-term recovery on the hourly chart.

Alternatively, the 1.1790 level acts as the immediate support ahead of the latest lows near 1.1720-15.

Following that, the weekly channel’s support line and the lower line of the longer-term trend channel, respectively near 1.1660 and 1.1615, will be crucial supports to watch during the GBP/USD pair’s further weakness.

- AUD/USD is concluding its correction and will advance to reclaim its three-day high at 0.6960.

- Dismal performance on the PMI front resulted in a steep decline in the DXY.

- Investors have now shifted their focus on US Durable Goods Orders for further guidance.

The AUD/USD pair displayed a correction to near 0.6920 after a stellar rebound from a low of 0.6860. The asset has comfortably established above the critical hurdle of 0.6900 and is likely to recapture its three-day high at 0.6960. The major has strengthened after the release of the dismal Purchasing Managers Index (PMI) data by the US.

A sharp contraction in the US PMI is indicating the consequences of squeezing liquidity from the market. The US Services PMI has contracted dramatically to 44.1 against the forecast of an expansion to 49.2 and the prior release of 47.3. Also, the Manufacturing PMI has contracted to 51.3 from the estimates of 52 and the prior release of 52.2.

Stick to the path of achieving price stability in the economy, the Federal Reserve (Fed) is hiking the borrowing rates with severe momentum. The Fed has elevated its interest rates to 2.25-2.50% from 0-0.25% in its last four monetary policy meetings. And, one can assume the velocity of squeezing liquidity from the market. The unavailability of cheap money for the corporate sector resulted in the selection of ultra-filtered investment projects only and therefore a decline in the PMI data.

Now, investors are focusing on the US Durable Goods Orders data, which are expected to contract to 0.6% from the prior release of 2%. This also indicates a decline in the overall demand and may result in more pressure on the US dollar index (DXY).

On the aussie front, investors have ignored the downbeat Australian PMI numbers and have punished the DXY. The S&P Global Manufacturing PMI slipped sharply to 54.5 vs. expectations of 57.3 and the prior release of 55.7. While the Services PMI data landed lower to 49.6 against the forecasts of 54 and the former figure of 50.9.

- The silver price climbed 0.70% amidst a downbeat market sentiment, which weighed on the greenback.

- Higher US Treasury yields put a lid on XAG/USD prices.

- Market players’ focus turns to Wednesday’s Durable Good Orders, alongside Fed speaking on Friday, led by Chair Powell.

Silver price erases Monday’s losses and is higher as Wall Street’s ended the day with minimal losses, amidst a dismal sentiment propelled by US economic data dropping to contractionary readings. Also, traders are preparing for an expected hawkish speech by Federal Reserve Chairman Jerome Powell in Jackson Hole, which bolstered silver’s appeal, to the detriment of the US dollar At the time of writing, XAG/USD is trading at $19.11 up by 0.70%.

US equities finished the day in the red. Earlier in the New York session, S&P Global reported US PMIs, for August, with the Services and Composite indices plunging to contractionary territory, each with readings at 44.1 and 47, respectively. Contrarily, the Manufacturing Index downtick to 51.3 but remained in expansionary territory, despite missing estimates.

In the US data release, the US dollar weakened across the board, with the US Dollar Index sliding from around 109.000 to 108.200. On the contrary, US T-bond yields rose, led by the 10-year US Treasury yield, up by four bps, sitting at 3.057%, a headwind for silver prices.

Additionally, US housing data portrayed that New Home Sales dipped to their slowest pace since 2016, dropping for the sixth consecutive month, as the market continues to deteriorate as the Federal Reserve tightens monetary policy. New Home Sales dropped by 0.51M vs. estimations of 0.575M.

What to watch

The US economic docket will feature Durable Good Orders for July, alongside Housing Data, illustrating that the US economy is slowing down on Wednesday.

Silver Key Technical Levels

- EUR/USD bulls tiring and the bears are moving in in the near term.

- Longer-term, there are prospects of a bullish continuation in this daily correction for the days ahead.

EUR/USD has rallied on the day and is now consolidating in a correction of the bullish im[pulse. The following illustrates the potential flight trajectory based upon multi-time frame price action and structure between the daily, 4 and 1-hour charts, down to the 15-minute chart.

EUR/USD daily chart

The M-formation is a reversion pattern on the daily chart that has seen the price pull into the 38.2% Fibonacci. It would be unusual for the price to continue lower from here without at least another bar or two of corrective activity that could see the price move higher in the days ahead before the next sell-off.

H4 chart

Meanwhile, with the price forming a W-formation on the 4-hour chart, there would appear to be some prospect of a deeper correction of the current bullish impulse.

EUR/USD H1 chart

The hourly chart sees the price formation an M-formation and should the neckline hold as resistance, then the price will likely follow the 4-hour bearish bias for the session ahead.

EUR/USD M15 chart

With that being said, there would appear to be the possibility of a break higher in the very short term considering the inverse head and shoulders on the 15-min chart.

What you need to take care of on Wednesday, August 24:

The greenback turned south after extending its rally throughout the first half of the day, ending the day down against most major rivals. The catalyst was dismal US data, as the US Services S&P Global PMI contracted to 44.1. At the same time, the manufacturing index expanded at a slower-than-anticipated pace, with the index down to 51.3 from 52.2 in July.

However, S&P Global PMIs for most major economies indicated slowing economic progress and even contraction, indicating it is a global issue. The greenback recovered some ground ahead of Wall Street’s close as risk-off flows continue. The dollar’s decline seems corrective amid extreme overbought conditions. Tepid US data helped investors book some profits, but there are no signs of a trend change.

ECB Executive Board member Fabio Panetta painted a gloomy picture. He said that the central bank might need to adjust the monetary policy further as the probability of a recession increases. Meanwhile, speculative interest is slowly but steadily increasing bets of a US Federal Reserve 75 bps rate hike in September.

GBP/USD hovers around 1.1830, while AUD/USD stands in the 0.6920 region. The USD/CAD pair fell sharply and finished the day at 1.2950.

Safe-haven currencies posted gains vs the greenback, with USD/CHF hovering at around 0.9640 and USD/JPY trading at 136.77.

Gold is currently trading at $1,7477 a troy ounce, up for the day, while crude oil prices extended their latest advance amid market talks suggesting OPEC+ may cut back production. WTI is now at $93.60 a barrel.

The macroeconomic calendar will remain empty in Asia, with the focus on US Durable Goods Orders on Wednesday.

Like this article? Help us with some feedback by answering this survey:

- USD/CHF records minimal gains of just 0.09% on Tuesday.

- Softer US housing and PMI data weakened the US dollar.

- UJSD/CHF Price Analysis: RSI’s aiming higher, coincided with the major beginning to shift upwards.

The USD/CHF marginally advances on Tuesday after hitting a daily high nearby the 0.9700 figure, but weaker than estimated US data weighed on the greenback, boosting the Swiss franc. Nevertheless, the USD/CHF keeps trading above its opening price, at 0.9646, at the time of writing.

USD/CHF Price Analysis: Technical outlook

The USD/CHF from a daily chart perspective is neutral-biased. During the day, the USD/CHF tested the July 22 high at 0.9704, but sellers stepped in, sending the price dipping below the 100-day EMA. If buyers would like to remain in charge, they would need a break above the 0.9700 figure, which would pave the way for parity’s retest.

Zooming to a 4-hour time frame, the USD/CHF illustrates the pair as upward biased, as the major crossed above the 200-EMA around 0.9618. However, due to broad US dollar strength since the middle of the last week, the Relative Strength Index (RSI) entered overbought conditions, spurring a drop from around weekly highs towards the daily pivot point at 0.9623.

Once the RSI exited overbought conditions, it rebounded around the 60 reading. In the last 10 days, RSI touched the previously mentioned area five times, which equals the USD/CHF dips. That said, RSI begins to aim higher, meaning that the USD/CHF uptrend is about to resume.

Therefore, the USD/CHF first resistance would be the R1 pivot at 0.9672. Break above will expose the R2 daily pivot at 0.9709, followed by the July 21 high at 0.9739.

USD/CHF Key Technica Levels

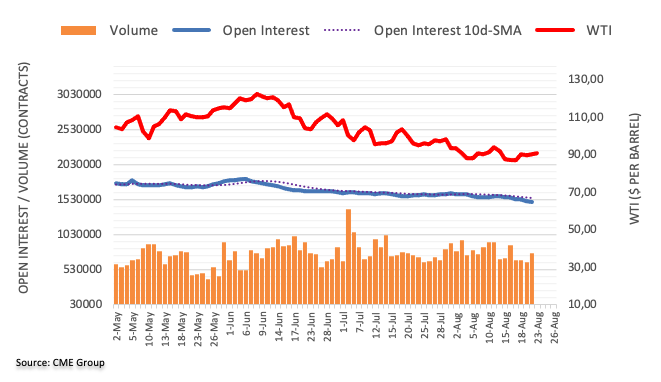

- Oil prices rallied on Tuesday while Saudi Arabia warning that OPEC+ could cut production.

- Iran remains the wild card in the energy sector.

When oil futures trade at lower levels than spot prices and near-term futures, that’s known as backwardation and it's been a theme in 2022 that has seen Saudi Arabia warning that OPEC+ could cut production to narrow a gap between high prices in the physical oil market and weaker futures prices. The comments have sent the spot price higher on the day. At the time of writing, WTI is trading at $93.60, up 3.32% but of the highs of $94.19.

Saudi oil minister Prince Abdulaziz bin Salman told Bloomberg News that OPEC+ could cut production when the group next meets to raise prices. However, the wild card in the oil market stays with Iran. ''When it comes to the potential Iran deal, no news has been good news,'' analysts at TD Securities explained.

''While fears of an imminent deal had seen a sharp slump in our gauge of energy supply risk, raising the alarm on the bull market in oil, energy traders have grown increasingly skeptical of the legal and political risks associated with a potential resolution. After all, the clock is ticking for a resolution that has the potential to drive a continued and substantial erosion of supply risk premia, but a potential resolution appears plagued with legal and political risks which blur the outlook,'' the analysts at TD Securities explained.

The analysts warned that failure to reach a deal would suggest that oil is still on a runaway train, as even slowing demand growth would still continue to sap the world's spare capacity.

On the other side, of the coin, "how a lower production volume is supposed to restore the balance between the futures market and the physical market remains unclear, though. Possibly Saudi Arabia wants to prepare for a scenario in which the US agrees to a renewal of the nuclear agreement with Iran, thereby allowing the latter to return to the oil market. The fact that Saudi Arabia appears to regard an oil price of around $90 as too low could be seen by speculators as an invitation," Commerzbank said in a note.

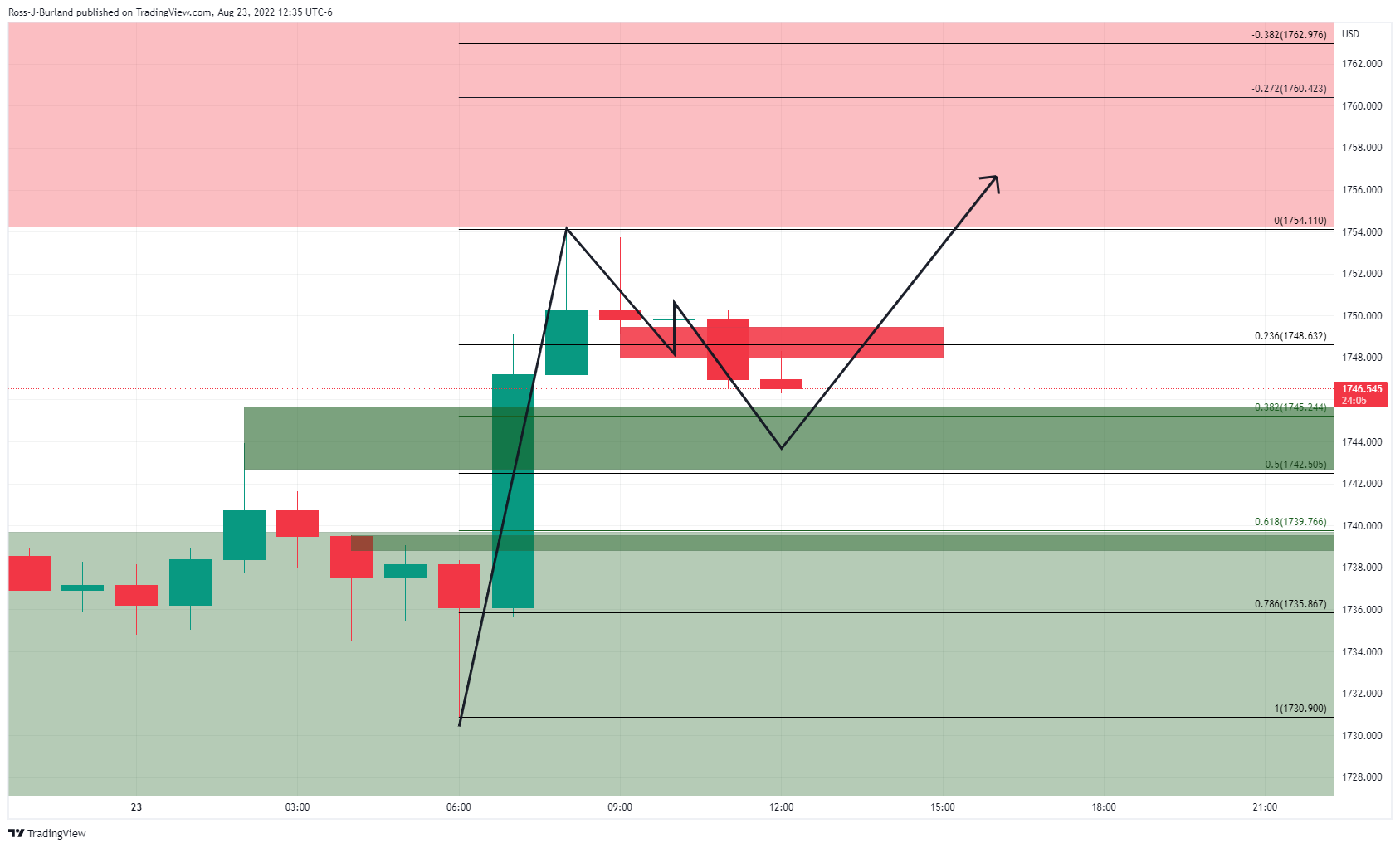

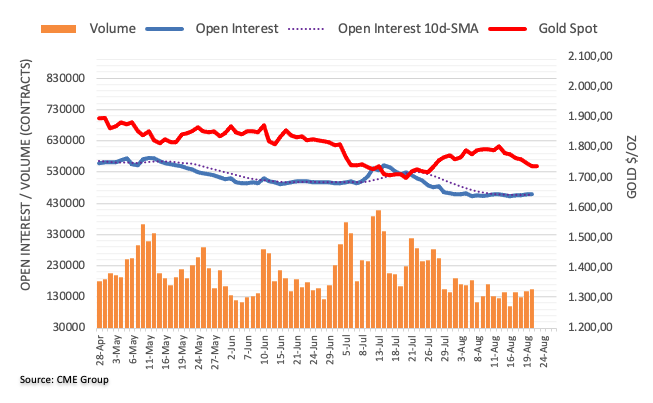

- Gold is on the verge of a downside correction following today's 2-year auction and recovery in yields.

- Gold bulls are eyeing a deeper correction on the daily chart.

- The Fed is the theme with US data taking the front seat in markets.

The gold price rallied on Tuesday following US data that proves the Federal Reserve's tactics could be going to plan in trying to rein in higher inflation in the US economy. At the time of writing, the yellow metal is trading at $1,747.50, 0.67% higher after rallying from a low of $1,730.90 to a high of $1,754.11.

The drop in the US dollar and yields helped the precious metal recover a lot of ground to the upside at the start of the New York day after a report showed US private sector activity contracted for a second-straight month in August. The data was the nail in the coffin for the greenback that had already started to flutter as investors started to trim long positions in anticipation of risk events that include the Jackson Hole as the showdown for the week.

Given a data-dependent Fed, markets will be cautious being too long of the greenback into such data as today's S&P Global flash composite purchasing managers index (PMI), tomorrow's Durable Goods Orders and Thursday's Gross Domestic Product, Initial Jobless Claims and Personal Consumption Expenditures. For instance, today's miss in the flash composite purchasing managers index (PMI) has raised the prospects the Federal Reserve will ease its rate hiking cycle. The data is showing exactly what the Fed is trying to achieve with its stiffest run of interest rate increases since the 1980s — a drop in demand which can help to tame the risks of rising inflation.

The S&P Global flash composite purchasing managers index (PMI) for August dropped to 45 this month, the lowest since February 2021, as demand for services and manufacturing weakened in the face of inflation and tighter financial conditions. A reading below 50 indicates a contraction in activity. If we see more of the same from the forthcoming data this week ahead of the Jackson Hole, then the US dollar may continue to struggle in the face of a cooling demand-side economy.

The Fed has hiked rates from near zero in March to their current range of 2.25% to 2.50%, with more expected in the months ahead, as it tries to tame inflation, which is running near a 40-year high. However, while WIRP suggests a 50 bp hike is fully priced in for the September 20-21 FOMC meeting, the odds of a 75 bp hike could start to dwindle and weigh on the greenback, reviving the bull's hopes for the higher gold prices.

Nevertheless, analysts at TD Securities argued that with regards to the Jackson Hole, the analysts suggest that the Fed's Chair, Jerome Powell's speech ''will likely aim to reinforce the message that multiple, sizable hikes are still in the pipeline, and easing should not be expected to be on the horizon anytime soon.''

''This fits with the recent easing in market expectations for rate cuts to immediately follow the rate hiking cycle, which we expect will be the focus of Fedspeak in the coming weeks. In this context, we are anticipating a capitulation event in gold driven by the unwind of a bloated position held by a few prop-shops and family offices.''

US treasury auction

Meanwhile, we are seeing a bid back into the greenback and US yields following today's bullish 2-year Treasury auction.

- High yield 3.307%.

- Tail 1.4 bps vs a 6-month average of -0.3 bps.

- Bid to cover 2.49X vs 6-month avg of 2.59X.

- Dealers 23% vs a 6-month average of 17.4%.

- Directs 17.3 vs a 6-month average of 22.2%.

- Indirects 59.7% vs a 6-month average of 60.4%.

The demand from domestic and international buyers is far below a 6-month average which has seen the 2 and 10-year yields rally, supporting the US dollar and weighing on gold prices in the recent hours since the auction.

The 2-year yield, as illustrated above, has recovered significantly following the auction, weighing on gold:

Gold technical analysis

As per the prior analysis, it was stated that the price of gold had left behind an M-formation on the daily chart, a reversion pattern that would be expected to see the price revert towards the neckline in due course. However, it also suggested that given the over-extension of the latest impulse, the correction will more probably only reach as far as the prior support near a 38.2% Fibonacci around $1,755.

As illustrated, the prior analysis anticipated the correction, above, and the bulls committed to the moves today, below:

Meanwhile, the price could be on the verge of a significant bearish correction as per the hourly chart:

The W-formation is compelling with the neckline meeting the 61.8% Fibo should the 38.2% and 50% ratios give out. On the other hand, should the 38.2% and 50% hold, given the M-formaiton, the bulls could be encouraged to move in for a deeper correction on the daily chart:

- USD/CAD erases its Monday gains and slides more than 0.60%.

- Weaker US housing and PMI data weighed on the greenback.

- TDS Analysts expect the BoC will hike 75 bps in September; estimates the first cut in Q3 2023.

The USD/CAD stumbles from weekly highs around 1.3063 and plunged on weaker than expected US economic data, which reignited US recession fears amidst a week where traders are bracing for Fed Chair Jerome Powell’s speech.

The USD/CAD is trading at 1.2069, below its opening price, after hitting a daily high at 1.3063, followed by a dip towards its daily low at 1.2933, before settling at current exchange rates.

USD/CAD tumbled on weak US housing/PMI data

Earlier in the North American session, S&P Global reported that the US Services PMI for August plunged to contractionary territory, with a reading of 44.1, while the Composite Index followed suit at 47. Contrarily, the Manufacturing PMI, although it slowed, persisted in an expansionary territory at 51.3, less than estimated.

Furthermore, US housing data showed that New Home Sales dived to its slowest pace since 2016, falling for the sixth consecutive month, as the market continues to deteriorate as the Federal Reserve tightens monetary policy. New Home Sales dropped by 0.51M vs. estimations of 0.575M.

Aside from this, the USD/CAD slid from around 1.3010s to 1.2975 on the release of US data. An absent Canadian docket let traders lean on the dynamics of the US dollar and oil prices. That said, WTI futures contracts rose 3.65%, exchanging hands at $93.89 per barrel.

TDS Analysts foresee a 75 bps increase by the BoC and expect the first cut in 2023

Elsewhere, TDS analysts estimate that the Bank of Canada will hike 75 bps in September. They wrote in a note, “We continue to look for the Bank of Canada to deliver a 75bp hike before a final 25bp hike for a 3.50% terminal rate by October.”

“While we look for a 3.50% terminal rate for the BoC’s tightening cycle, we also expect slowing growth will force the Bank to cut rates in starting in Q3 2023, before reaching a long-term neutral rate of 2.25% by mid-2024.”

What to watch

The US economic docket will feature Durable Good Orders for July, alongside Housing Data, illustrating that the US economy is slowing down on Wednesday.

USD/CAD Key Technical Levels

- US dollar tumbles after weak economic data.

- US PMI S&P Global shows the lowest reading in more than a year.

- AUD/USD finds resistance around 0.6960 and losses momentum.

The AUD/USD broke above 0.6900 after the release of US economic data and peaked at 0.6962, the highest level since Thursday. The pair lost momentum and pulled back under 0.6950.

The August preliminary US S&P Global PMI report came in below expectations, particularly the Service sector index that plunged to 44.1 against expectations of a recovery to 49.2. The numbers increased concerns about the health of the US economy.

The demand for Treasuries rose after the numbers, pushing US yield sharply to the downside and at the same time weakening the greenback. The DXY dropped from above 109.00 to 108.10, it is hovering around 108.45, down by 0.48%.

During the last hour, the dollar stabilized and trimmed losses. Still, it remains negative for the day, about to post the first decline in days. The main trend is still bullish for the dollar. Attention now turns to the Jackson Hole symposium that will start on Thursday. Fed Chair Jerome Powell will deliver a speech on Friday.

Earlier on Tuesday, the Australian PMI came also below expectations. The S&P Global Composite dropped below 50 for the first time since January.

Key support at 0.6850/55

The outlook for the aussie versus the dollar improved following the rebound. On the upside, the level to break for AUD/USD now is 0.6960. On the flip side a slide back under 0.6895 would expose again the crucial support area around 0.6850/55. A break under 0.6850 should weaken the pair considerably targeting initially the 0.6800 zone.

Technical levels

- USD/JPY sinks 100 pips and is losing more than 0.70% due to mixed US economic data.

- A bearish-engulfing candle pattern in the daily chart could pave the way for further losses.

- The USD/JPY is trading below the 100-hour EMA, with sellers keeping the fort afloat.

The USD/JPY plunges from weekly highs around 137.70 as US recession fears were fueled by mixed US economic data, dropping into contractionary territory, namely S&P Global Services and Composite PMIs, while the Manufacturing expanded. Nevertheless, traders took advantage of an overpriced US dollar and sent the major down. At the time of writing, the USD/JPY is trading at 136.39, below its opening price by 0.80%.

USD/JPY Price Analysis: Technical outlook

The daily chart shows that a bearish-engulfing candle pattern is emerging, which could pave the way for further losses. However, it’s worth noting that the pair tested the August 19 daily low at 135.71, but sellers could not hold buyers from reclaiming the 136.00 figure. Even though a bearish-engulfing candle pattern is bearish, sellers will face solid support at 135.71, followed by the 50-day EMA at 135.52.

The one-hour scale depicts that the USD/JPY broke below a confluence of the S1 daily pivot and a downslope trendline, exacerbating a fall towards the S3 pivot at 135.91, where USD buyers stepped in. Nevertheless, they’re facing resistance at the 100-hour EMA at 136,39, which, once cleared, could pave the way towards the 137.00 figure. Nonetheless, the most likely scenario is that the USD/JPY head downwards due to a confluence of the indicators tilting the pair as bearish,

Therefore, the USD/JPY first support will be the S3 pivot at 135-90. Break below will expose the August 7 high at 135.58, followed by the 200-hour EMA at 134.98.

USD/JPY Key Technical Levels

- GBP/USD jumps from YTD lows after US economic data reignited recession fears.

- US S&P Global PMIs were mixed, though reignited recession fears.

- The S&P Global Manufacturing PMI in the UK dropped to the contractionary territory.

- GBP/USD Price Analysis: If it clears 1.1900, a test of 1.1936 is on the cards.

The GBP/USD recovered some ground bouncing from weekly lows below the 1.1800 figure due to dismal US economic data, which increased fears of a US recession. Consequently, the greenback fell, alongside US T-bond yields, while most G8 currencies advanced. The GBP/USD is trading at 1.1860, after hitting a YTD low at 1..1716, so the major swang more than 100 pips as a reaction to the abovementioned data, while sentiment shifted positively, with US equities gaining.

The US and UK S&P Global PMIs came mixed; consequently, the greenback weakened

The US S&P Global PMI Composite for August showed that business activity in the US contracted for the second consecutive month. On the contrary, the Manufacturing PMI, although slowed, remained in expansionary territory, at 51.3, lower than expected.. The figures portray the Composite Index at 45, less than estimates of 47, while the Services PMI plunged to 44.1, below forecasts.

Meanwhile, during the European session, S&P Global revealed that August UK Manufacturing PMI plummeted into contractionary territory, falling to 46.0, shy of estimates of 51.1, driven by high energy prices across Europe, supply chain disruptions, and higher interest rates. Contrarily to the US, the UK’s Services PMI was unchanged at 52.5, while the Composite PMI downtick to 50.9.

What to watch

The US economic docket will feature Durable Good Orders for July, alongside Housing Data, illustrating that the US economy is slowing down on Wednesday. A light calendar will feature CBI Distributive Trades on the UK front on Thursday.

GBP/USD Price Analysis: Technical outlook

The GBP/USD is climbing as buyers eye a test of the August 19 daily high of 1.1935. Once the GBP/USD cleared the figure at 1.1800, followed by the August 22 daily high at 1.1836. The next resistance will be the 1.1900 figure on its way towards the August 19 daily high. Despite that the pound is staging a comeback, the Relative Strength Index (RSI), is still in negative territory, so caution is warranted.

- US dollar tumbles following the August preliminary US S&P Global PMI.

- Eurozone consumer confidence rises unexpectedly in August.

- EUR/USD is having the best day in two weeks.

A sharp decline of the US Dollar across the board boosted the EUR/USD pair following the release of US economic data. The pair climbed from under 0.9950 to 1.0018, printing a fresh daily high. It then pulled back, and as of writing, it is hovering around 1.0000.

US PMIs trigger alarms

The August preliminary S&P Global PMI showed numbers below expectations and activity at the lowest level in almost two years. The greenback tumbled across the board after the report. The DXY is falling by 0.70%, at 108.20, after testing multi-year highs.

US Treasuries rallied after the numbers. The US 10-year yield collapsed from 3.07% to 2.97% in a few minutes while the 30-year dropped from weekly highs at 3.28% to 3.20%. The moves in the bond market boosted the Japanese yen which become the best performer among majors.

Earlier on Tuesday, European PMI showed mixed numbers. More recently, during the American session, the European Commission announced that the Consumer Confidence Indicator for the Eurozone rose to -24.9 in August from July's record low of -27, against expectations of a decline to -28.

The euro is holding onto important daily gains versus the dollar, up for the first time after falling for three consecutive days. The main trend in EUR/USD is still bearish. The pair is up by almost 60 pips, the biggest daily gain in two weeks.

Technical levels

Citing nine OPEC sources familiar with the matter, Reuters reported on Tuesday that OPEC and its allies, the group known as OPEC+, may lean towards oil output cuts when and if Iranian production returns depending on the revival of the nuclear deal.

On Monday, Saudi Arabia's energy minister told Bloomberg that OPEC+ may be compelled to reduce oil production, as the physical and futures markets get increasingly strayed away from fundamentals.

Market reaction

Crude oil prices continued to push higher on this headline. As of writing, the barrel of West Texas Intermediate was trading at $93.75, where it was up 3.6% on a daily basis.

- Consumer confidence in the euro area improved modestly in early August.

- EUR/USD trades in positive territory near parity after the data.

The European Commission announced on Tuesday that the Consumer Confidence Indicator for the euro area rose to -24.9 (flash) in August from July's record low of -27. This reading came in better than the market expectation of -28.

For the EU, the Consumer Confidence Indicator rose to -26 from -27 in the same period.

Market reaction

The EUR/USD pair clings to daily recovery gains near parity after this data.

- USD/TRY extends the advance north of 18.00 on Tuesday.

- The rally in the US dollar sustains the upside in spot.

- Türkiye Consumer Confidence improved to 72.2 in August.

The persistent upside momentum in the greenback lifts USD/TRY to the area of 2022 highs past the 18.00 hurdle on Tuesday.

USD/TRY up on USD-buying, targets the all-time high

USD/TRY advances for yet another session on the back of the unabated uptrend in the greenback, which in turn appears bolstered by the Fed’s tightening expectations as well as another uptick in US yields.

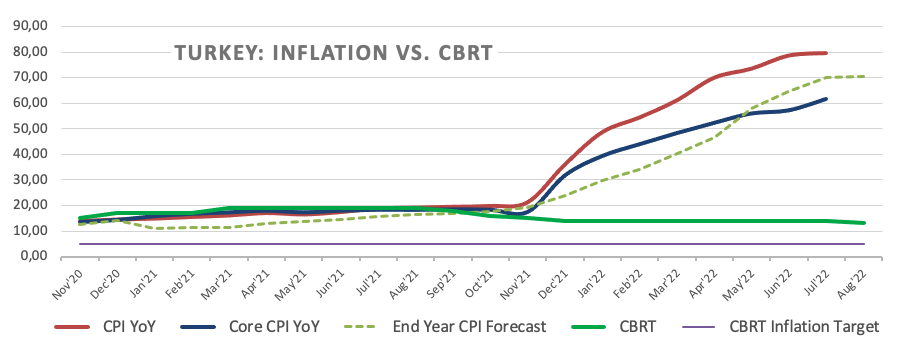

The lira, in the meantime, continues to depreciate, as investors keep evaluating last week’s interest rate cut by the Turkish central bank (CBRT) despite inflation ran at nearly 80% in the year to July, the highest level since 1998.

Adding downside pressure to TRY, President Erdogan reiterated once again his opposition to raising interest rates earlier on Tuesday, increasing the rhetoric that the country needs “an increase in investment, employment, production, exports and current account surplus”… (nothing else).

Further news on Tuesday saw finmin N.Nebati suggesting (hoping) that inflation would start a sharp downside correction around December following base effects and that this strong downtrend could extend into 2023.

Again: with inflation around 80% YoY in July, the central bank’s CPI forecast at 70% by year end, no signs of an end to the Russia-Ukraine war for the time being and the energy crunch expected to get worse before it gets better, Nebati’s promises look no less than unachievable.

Back to reality, and in the domestic calendar, Consumer Confidence in Türkiye improved to 72.2 in August (from 68.0).

What to look for around TRY

The upside bias in USD/TRY remains unchanged and now targets the all-time high around 18.25 following the unexpected interest rate cut by the CBRT.

In the meantime, the lira’s price action is expected to keep gyrating around the performance of energy and commodity prices - which are directly correlated to developments from the war in Ukraine - the broad risk appetite trends and the Fed’s rate path in the next months.

Extra risks facing the Turkish currency also come from the domestic backyard, as inflation gives no signs of abating (despite rising less than forecast in July), real interest rates remain entrenched in negative figures and the political pressure to keep the CBRT biased towards low interest rates remains omnipresent. In addition, there seems to be no Plan B to attract foreign currency in a context where the country’s FX reserves dwindle by the day.

Key events in Türkiye this week: Consumer Confidence (Tuesday) – Capacity Utilization, Manufacturing Confidence (Thursday).

Eminent issues on the back boiler: FX intervention by the CBRT. Progress (or lack of it) of the government’s new scheme oriented to support the lira via protected time deposits. Constant government pressure on the CBRT vs. bank’s credibility/independence. Bouts of geopolitical concerns. Structural reforms. Presidential/Parliamentary elections in June 23.

USD/TRY key levels

So far, the pair is gaining 0.48% at 18.1164 and faces the immediate target at 18.1338 (2022 high August 23) seconded by 18.2582 (all-time high December 20) and then 19.00 (round level). On the other hand, a breach of 17.7586 (monthly low August 9) would pave the way for 17.4711 (55-day SMA) and finally 17.1903 (weekly low July 15).

- New Home Sales in the US fell sharply in July.

- The US Dollar Index continues to push lower toward 108.00.

Sales of new single‐family houses declined by 12.6% in July to a seasonally adjusted annual rate of 511,000, the data published jointly by the US Census Bureau and the Department of Housing and Urban Development showed on Tuesday.

"The median sales price of new houses sold in July 2022 was $439,400," the publication further revealed. "The average sales price was $546,800."

Market reaction

The dollar stays under heavy selling pressure after this data and the US Dollar Index was last seen losing nearly 0.7% on the day at 108.20.

- S&P Global Composite PMI for the US continued to decline in August.

- US Dollar Index continues to push lower on weak PMI figures.

The data published by S&P Global showed on Tuesday that the business activity in the US private sector contracted at a stronger pace in early August than it did in July with the Composite PMI falling to 45 from 47.7. The Manufacturing PMI declined to 51.3 from 52.2 and the Services PMI plunged to 44.1 from 47.3. Both of these readings fell short of market expectations.

Commenting on the data, "August flash PMI data signalled further disconcerting signs for the health of the US private sector. Demand conditions were dampened again, sparked by the impact of interest rate hikes and strong inflationary pressures on customer spending, which weighed on activity," noted Siân Jones, Senior Economist at S&P Global Market Intelligence.

"One area of reprieve for firms came in the form of a further softening in inflationary pressures," Jones further noted. "Input prices and output charges rose at the slowest rates for a year-and-a-half amid reports that some key component costs had fallen."

Market reaction

The dollar came under heavy bearish pressure after the disappointing PMI surveys and the US Dollar Index was last seen losing 0.45% on the day at 108.46.

- Gold catches some bids on Tuesday and recovers further from a multi-week low.

- A softer risk tone, along with a modest USD pullback, offers support to the metal.

- Hawkish Fed expectations, elevated US bond yields should cap any further gains.

Gold reverses an intraday dip to the $1,730 area and climbs to a fresh daily high during the early North American session. The XAU/USD, for now, seems to have snapped a six-day losing streak to a nearly four-week low and is currently placed around the $1,745 region, though any meaningful upside still seems elusive.

Macroeconomic headwinds stemming from China’s COVID-zero policy - imposing snap lockdowns after just a handful of cases - continue to fuel recession fears. This, in turn, tempers investors' appetite for riskier assets, which is evident from a generally weaker tone around the equity markets and benefits the safe-haven metal. Apart from this, a modest US dollar pullback from a two-decade peak further seems to underpin the dollar-denominated gold.

The USD lost additional ground following the release of weaker-than-expected flash US PMI prints for August. That said, expectations for a more hawkish message from Fed Chair Jerome Powell at the Jackson Hole symposium on Friday favour the USD bulls. This, in turn, suggests that the path of least resistance for gold is to the downside. Even from a technical perspective, the emergence of fresh selling at higher levels validates the negative outlook.

Furthermore, firming expectations that the Fed would continue to tighten its monetary policy leads to an extended sell-off in the US fixed income market. This, in turn, lifts the yield on the benchmark 10-year US government bond to a nearly one-month high and exerts some downward pressure on the non-yielding yellow metal. That said, a combination of factors offers some support to gold and helps limit the downside, at least for the time being.

Hence, any subsequent move up might still be seen as a selling opportunity and runs the risk of fizzling out rather quickly near the $1,754-$1,755 horizontal support breakpoint. Gold seems poised to prolong its recent retracement slide from the $1,808 area, or over a one-month high touched earlier this August. The downward trajectory could drag spot prices towards the $1,710 intermediate support en route to the $1,700 round-figure mark.

Technical levels to watch

EUR/USD has tested the 0.99 area. A break below here could trigger a substantial drop towards the 0.9575/70 support.

Weak demand for the euro

“Short-term price action does reflect some positives for the EUR – bullish reversals on the one and six-hour charts – but the lack of follow through off the intraday low at 0.99 suggests only weak demand for the EUR here, with the figure area still drawing attention.”

“We spot intraday resistance at 0.9950.”

“Support below the figure is really limited to 50s and 00s until 0.9570/75.”

USD/CAD dips modestly on crude rebound. The loonie could enjoy some strength if the pair breaks below 1.3010, economists at Scotiabank report.

WTI may head back towards the $95 area in the near term

“We still think the 1.3075 zone should provide some resistance to the USD’s advance but it may be hard for the CAD to resist a more generalized USD strength.”

“Key support is 1.3010; weakness below here should see the CAD regain a little more positive momentum.”

“WTI may head back towards the $95 area in the near term which may provide a little support for the CAD but the broader USD tone and risk appetite are likely to remain more influential drivers of the CAD in the absence of any major domestic developments.”

Gold’s recent selloff continued as precious metals traders are front-running Chair Powell's speech at the Jackson Hole symposium, economists at TD Securities report.

Easing in market expectations for rate cuts to immediately follow the rate hiking cycle

“In line with our view that the Fed may use Jackson Hole to push back against the notable easing in financial conditions sparked by the Chair's last remarks, precious metals prices have started to ease. Further, this fits with the recent easing in market expectations for rate cuts to immediately follow the rate hiking cycle, which we expect will be the focus of Fedspeak in the coming weeks.”

“We are anticipating a capitulation event in gold driven by the unwind of a bloated position held by a few prop-shops and family offices.”

- USD/JPY attracts some dip-buying on Tuesday and moves back closer to a one-month high.

- The USD stands tall near a two-decade high and offers support amid elevated US bond yields.

- The Fed-BoJ policy divergence favours bullish traders and supports prospects for further gains.

The USD/JPY pair reverses an intraday dip to the 137.00 mark and climbs back closer to over a one-month high touched earlier this Tuesday. The pair is seen trading just above mid-137.00s during the early North American session and looking to build on its recent upward trajectory witnessed over the past two weeks or so.

The US dollar hits a two-decade high amid hawkish Fed expectations, which turns out to be a key factor acting as a tailwind for the USD/JPY pair. Bullish traders further took cues from elevated US Treasury bond yields, resulting in the widening of the US-Japan rate differential and undermining the Japanese yen. This, along with the divergent Fed-Bank of Japan policy stance, supports prospects for a further near-term appreciating move.

Despite signs of easing US inflation, the recent hawkish remarks by several Fed officials suggested that the US central bank will continue to tighten its monetary policy to tame inflation. In contrast, the BoJ has repeatedly said that it will stick to its ultra-easy policy settings and

remains committed to keeping the 10-year Japanese government bond yield around 0%. This, in turn, reaffirms the near-term positive outlook for the USD/JPY pair.

Traders, however, might refrain from placing aggressive bullish bets and prefer to wait for a more hawkish message from Fed Chair Jerome Powell at the Jackson Hole symposium on Friday. Traders will further take cues from this week's important US macro releases. The combination of factors will play a key role in influencing the near-term USD price dynamics and help determine the next leg of a directional move for the USD/JPY pair.

In the meantime, Tuesday's US economic docket - featuring the flash PMI prints, New Home Sales data and Richmond Manufacturing Index - will drive the USD demand. This, along with the US bond yields and the broader market risk sentiment, should provide some impetus to the USD/JPY pair and allow traders to grab short-term opportunities.

Technical levels to watch

UOB Group’s Economist Ho Woei Chen, CFA, evaluates the latest move by the PBoC.

Key Takeaways

“The People’s Bank of China (PBoC)’s benchmark 1Y Loan Prime Rate (LPR) was fixed lower by a smaller-than-expected 5 bps to 3.65% (Bloomberg and UOB est: 3.60%) compared with the 10 bps cut to the 1Y medium-term lending facility (MLF) earlier this month. This is the first cut since Jan when the 1Y LPR was set lower by 10 bps.”

“Comparatively, Chinese banks have set the 5Y LPR lower by a larger 15bps to 4.30% (Bloomberg est: 4.35%). This follows 15 bps cut in May and 5 bps cut in Jan this year. The larger cut to the 5Y rate which mortgages are benchmarked against, suggests that authorities are increasingly concerned over the real estate downturn and continued to guide banks to set LPRs lower, in particular for the longer-tenor.”

“With the less optimistic outlook for the Chinese economy and measured pace of monetary policy easing so far, the 1Y LPR could continue to move lower to 3.55% by end-4Q22, instead of our earlier expectation that the monetary easing would cease by end-3Q22. After 35 bps cut YTD, the 5Y rate is still poised to fall further as PBoC extends support to the property market. However, there is less room for aggressive monetary policy easing by cutting interest rates and the PBoC will likely focus on using targeted tools including the relending programmes and guiding banks to increase credit.”

- EUR/USD clocks new cycle lows in the sub-0.9900 zone.

- Further losses could test the December 2002 low near 0.9860.

EUR/USD accelerates the daily losses and briefly breaks below the 0.9900 level, or new cycle lows.

Further weakness remains in the pipeline for the time being. Against that, the breakdown of the 2022 low at 0.9899 (August 23) should leave the door open to a probable deeper retracement to the December 2002 low at 0.9859.

In the longer run, the pair’s bearish view is expected to prevail as long as it trades below the 200-day SMA at 1.0845.

EUR/USD daily chart

Bank Indonesia (BI) unexpectedly raised its policy rate by 25 bps today. In the view of economists at ING, the Indonesian rupiah (IDR) could strengthen in the near-term after the surprising rate hike.

BI likely not done for the year

“BI finally hiked after staying on hold for the whole of 2022, confident that policy tightening would not derail the economy's recovery. We expect at least two more rate hikes by the central bank this year.”

“The IDR could gain support from the surprise rate hike in the near-term and could strengthen further should Indonesia's trade surplus remain sizable.”

Both the euro (EUR) and the British pound (GBP) have lost over 12% vs. the US dollar (USD) in the year to date. Economists at Rabobank expect the EUR/GBP pair to hover around the 0.84 area in the near-term but a move towards 0.86 is on the horizon.

EUR/GBP to hold around 0.84 on a one-to-three-month view

“We retain our forecast that EUR/GBP will hold around 0.84 on a one-to-three-month view.”

“For choice, we are forecasting a move to 0.86 on a six-month view, but how the eurozone copes this winter will be a strong determinant of whether the EUR can pull back some ground vs. GBP in the months ahead.”

- USD/CHF gains traction for the seventh straight day and jumps to a one-month high.

- A recovery in the risk sentiment undermines the safe-haven CHF and offers support.

- Hawkish Fed expectations act as a tailwind for the USD and favour bullish traders.

The USD/CHF pair prolongs its bullish move for the seventh successive day on Tuesday and climbs to over a one-month high during the mid-European session. The pair is currently placed comfortably above the 0.9650 horizontal resistance and seems poised to appreciate further.

A modest recovery in the global risk sentiment - as depicted by a positive turnaround in the equity markets - seems to undermine the safe-haven Swiss franc. This, along with the underlying bullish tone surrounding the US dollar, favours bullish traders and supports prospects for an extension of the recent recovery from the 0.9370 area, or the monthly low.

Despite signs of easing US inflation, investors seem convinced that the Fed will stick to its policy tightening path and have been pricing in at least a 50 bps rate hike in September. The bets were reaffirmed by the recent hawkish comments by several Fed officials and the FOMC minutes, indicating that the US central bank would continue hiking rates to tame inflation.

That said, a downtick in the US Treasury bond yields seems to hold back the USD bulls from placing fresh bets, especially after the recent run-up to a two-decade high. This could keep a lid on any further gains for the USD/CHF pair. That said, a sustained break through the previous monthly high, around the 0.9650 area, suggests that the path of least resistance is to the upside.

Market participants now look forward to the US economic docket - featuring the flash PMI prints, New Home Sales data and Richmond Manufacturing Index. This, along with the US bond yields, might influence the USD price dynamics and provide some impetus to the USD/CHF pair. Traders will further take cues from the broader risk sentiment to grab short-term opportunities.

Technical levels to watch

EUR/USD has tested 0.9900. Economists at BBH expect the pair to head lower towards the September 2002 low near 0.9615.

Preliminary eurozone August PMI readings continue to weaken

“The euro remains heavy and traded at new lows for this move near 0.9900. The next near-term target is the September 2002 low near 0.9615.”

“Headline manufacturing came in at 49.7 vs. 49.0 expected and 49.8 in July, services came in at 50.2 vs. 50.5 expected and 51.2 in July, and the composite came in at 49.2 vs. 49.0 expected and 49.9 in July.”

The US Dollar Index (DXY) is up for the fifth straight day and is coming off of its best week since March 2020. Economists at BBH note that the DXY could rally towards the 121 level on a break past the July 14 high near 109.294.

The dollar continues to strengthen

“DXY is trading at the highest since July 15 and it is on track to test the July 14 high near 109.294. After that, there really aren't any major chart points until the January 2002 high near 120.51 and the July 2001 high near 121.”

“Can the dollar rally another 10% from current levels? Fundamentally, that seems hard to justify but stranger things have happened.”

Economist at UOB Group Enrico Tanuwidjaja reviews the recently published Current Account results in the Indonesian economy.

Key Takeaways

“Indonesia’s current account posted a wider surplus amounting to USD 3.9bn (1.1% of GDP) in 2Q22, up significantly from a surplus of USD 0.4bn (0.1% of GDP) in 1Q22.”

“Indonesia also posted a balance of payment (BOP) surplus of USD 2.4bn in 2Q22, supported by a significantly larger current account surplus and a narrower capital and financial account deficit.”

“For 2022, we forecast that current account will return to a deficit of 0.2% of GDP as imports demand is likely to hasten up, while exports revenue is expected to moderate significantly.”

European Central Bank (ECB) executive board member Fabio Panetta said on Tuesday that they may have to adjust the monetary policy further, as reported by Reuters.

Panetta acknowledged that the probability of a recession in the eurozone was increasing and added that a recession would mitigate inflation pressures.

Market reaction

These comments don't seem to be having a noticeable impact on the shared currency's performance against its major rivals. As of writing, EUR/USD was trading at 0.9922, where it was down 0.2% on a daily basis.

Bank Indonesia (BI) hiked its policy rate by 25 bps today. Economists at TD Securities expect another 25 bps hike, potentially as early as next month. The USD/IDR has dropped following the hawkish pivot and is set to remain below the 15,000 level.

BI delivers a surprise hike

“In a surprise policy U-turn, BI hiked its 7-day reverse repo rate by 25 bps. BI justified the hike today as a preemptive move to address inflation pressures.”

“While BI took a hawkish stance on inflation, it appeared more dovish on other policy settings. BI is now signalling its own form of 'Operation Twist', joining other central banks like the RBI. We don't expect BI to stop with a one-off 25b ps hike today and expect another 25 bps, potentially as early next month.”

“We think IDR should be relatively more resilient compared to other EM-Asia currencies despite renewed USD strength.”

“We think BI will continue to defend the USD/IDR 15,000 level, which will act as a strong line in the sand.”

- DXY remains bid and flirts with the 2022 top near 109.30.

- Further north of comes the September 2002 high around 109.80.

DXY keeps the rally well and sound and trades at shouting distance from the YTD highs near 109.30 on Tuesday.

The continuation of the upside momentum looks increasingly likely in the very near term. That said, beyond the 2022 high at 109.29 (July 14) the index could challenge the September 2002 peak at 109.77 prior to the round level at 110.00.

In the meantime, while above the 6-month support line near 105.10, the index is expected to keep the short-term positive stance.

Looking at the long-term scenario, the bullish view in the dollar remains in place while above the 200-day SMA at 100.49.

DXY daily chart

Senior Economist Julia Goh and Economist Loke Siew Ting at UOB Group assess the release of the trade balance figures in Malaysia.

Key Takeaways

“Both export and import growth fell short of expectations in Jul, moderating to 38.0% y/y (UOB est: +41.5% vs Bloomberg est: +39.0%, Jun: +38.7%) and 41.9% y/y (UOB est: +49.0% vs Bloomberg est: +46.9%, Jun: +49.2%) respectively. Trade surplus narrowed to MYR15.5bn last month (from +MYR21.9bn in Jun) as a result of faster import growth over that of exports in the month.”

“Jul’s export growth was primarily supported by resilient demand for manufactured goods (particularly electrical & electronics, refined petroleum and chemicals & chemical products) and mining goods as overseas sales of agriculture goods were weighed by lower crude palm oil (CPO) prices and Indonesia’s palm oil exports policy. Higher shipments to the ASEAN region, US, EU, China including Hong Kong and Japan were key export growth drivers last month, with the ASEAN region logging an all-time high export value for two straight months.”

“Despite strong double-digit gains over the past one year, export growth is set to taper in the greater part of 2H22 as favourable base effects wane, major commodity prices retreating lately, and as heightened global headwinds keep businesses and consumers in a more cautious mode. Locally, the ongoing shortages of foreign labour continue to constrain manufacturers’ production capacity, in addition to the shortages of raw materials, higher cost pressures and currency volatility. We keep our 2022 full-year export growth forecast of 18.0% (BNM est: +10.9%, 2021: +26.0%).”

- EUR/JPY adds to Monday’s pullback above the 136.00 barrier.

- Bullish attempts remain capped by the August high at 138.40.

EUR/JPY extends the bearish start of the week, although it manages to bounce off earlier lows in the 135.70 region.

If the cross manages to break above the ongoing consolidation, the so far August high at 138.39 (August 10) is expected to come into focus once again. Above the latter, EUR/JPY could attempt a move to the 55-day SMA, today at 139.26.

While above the 200-day SMA at 134.12, the prospects for the pair should remain constructive.

EUR/JPY daily chart

- AUD/USD consolidates in a range near a one-month low touched earlier this Tuesday.

- A modest recovery in the equity markets offers support to the risk-sensitive aussie.

- Hawkish Fed expectations act as a tailwind for the USD and continue to cap the upside.

The AUD/USD pair struggles to gain any meaningful traction and seesaws between tepid gains/minor losses through the first half of the European session. The pair is currently placed in neutral territory, around the 0.6875 region, just a few pips above a one-month low touched earlier this Tuesday.

The US dollar pulls back from a two-decade high amid a softer tone surrounding the US Treasury bond yields. Adding to this, a goodish recovery in the global risk sentiment - as depicted by a positive turnaround in the equity markets - further underpins the safe-haven greenback. This turns out to be a key factor offering some support to the AUD/USD pair, through the attempted recovery move lacks bullish conviction.

Growing worries about a global economic downturn keep a lid on any optimistic move in the markets and act as a headwind for the risk-sensitive aussie. Furthermore, firming expectations that the Fed would continue to tighten its monetary policy to tame inflation should help limit any deeper USD corrective slide. The aforementioned factors should contribute to capping gains for the AUD/USD pair, warranting caution for bulls.

Investors might also be reluctant to place aggressive bets and prefer to move on the sidelines ahead of Fed Chair Jerome Powell's speech at the Jackson Hole symposium later this week. Investors will look for clues about the possibility of a 75 bps rate hike at the September FOMC meeting. This, along with important US macro data, will drive the USD demand and help determine the near-term trajectory for the AUD/USD pair.

In the meantime, Tuesday's US economic docket, featuring the flash PMI prints, New Home Sales data and Richmond Manufacturing Index might provide some impetus later during the early North American session. Apart from this, the broader risk sentiment could influence the USD price dynamics and allow traders to grab short-term opportunities around the AUD/USD pair.

Technical levels to watch

- UK CBI Manufacturing Order Book Balance fell below 0 for the first time in over a year.

- GBP/USD continues to fluctuate in a tight range above 1.1750.

Results from the latest survey released on Tuesday by the Confederation of British Industry (CBI) of trends in British manufacturing showed that the Manufacturing Order Book Balance dropped to -7 in August from +8 in July. This reading missed Reuters' estimate of +3 and it was the first negative reading since April 2021.

Further detail of the publication revealed that the Manufacturing Export Orders Balance remained unchanged at -12 and the Price Balance for the next three months climbed to +57 from +48.

Market reaction

This report doesn't seem to be having a significant impact on the British pound's performance against the dollar. As of writing, GBP/USD was unchanged on the day at 1.1765.

UOB Group’s Senior Economist Julia Goh and Economist Loke Siew Ting comment on the recent rate hike by the BSP.

Key Takeaways

“As expected, Bangko Sentral ng Pilipinas (BSP) continued to normalise its monetary policy rates today (18 Aug) with an additional 50bps hike. This brings the overnight reverse repurchase (RRP) rate to 3.75%, overnight deposit rate to 3.25%, and lending rate to 4.25%. Today’s interest rate hike marked the fourth back-to-back rate increases with a cumulative 175bps since May.”

“The Monetary Board (MB) judged that further monetary policy action is necessary to anchor inflation expectations and prevent a further breach in the inflation target over the policy horizon. The strong domestic economic growth in 1H22 also gave the central bank the flexibility to act against inflation pressures. It expects the national headline inflation to jump further to 5.4% this year (from its Jun’s estimate of 5.0%, UOB est: 5.0%) before decelerating to 4.0% in 2023 (from Jun’s estimate of 4.2%, UOB est: 4.0%) and 3.2% in 2024 (from Jun’s estimate of 3.3%).”

“Overall, the monetary policy statement and BSP Governor’s comments at the press briefing today indicated that the MB continues to the leave the door open for additional rate hikes. That said, BSP has almost fully unwound its collective 200bps rate cuts in the pandemic year of 2020. Ongoing uncertainties particularly global recession risks into 2023 and a tentative retreat in global oil prices could also lead the central bank to pause its rate hikes soon. Thus, we stick to our call for BSP to hike its policy rates by another 25bps in Sep and thereafter keep the RRP rate at 4.00% through 4Q22 and 2023, unless both global and domestic environments move in unexpected directions.”

- Gold edges higher on Tuesday and snaps a six-day losing streak to a multi-week low.

- Softer US bond yields prompt some USD profit-taking and offer support to the metal.

- Hawkish Fed expectations should continue to underpin the greenback and cap gains.

Gold gains some positive traction on Tuesday and moves away from a four-week low touched the previous day. The XAU/USD, for now, seems to have snapped a six-day losing streak and sticks to its modest recovery gains, around the $1,740 area through the first half of the European session, though lacks follow-through.

A slight US dollar pullback from a two-decade high turns out to be a key factor offering some support to the dollar-denominated gold. Following the recent strong run-up, the USD bulls to take some profits off the table amid a softer tone surrounding the US Treasury bond yields. In fact, the yield on the benchmark 10-year US government bond dips back below the 3.0% threshold, which further benefits the non-yielding yellow metal.

That said, a goodish recovery in the equity markets, along with hawkish Fed expectations, should hold back traders from placing aggressive bullish bets around gold. Despite signs of easing US inflation, investors seem convinced that the Fed will stick to its policy tightening path. The bets were reaffirmed by the recent hawkish comments by several Fed officials, which should act as a tailwind for the US bond yields and the greenback.

Investors also anticipate a more hawkish message from Fed Chair Jerome Powell's speech at the Jackson Hole symposium later this week. Apart from this, this week's important US macro releases will play a key role in influencing the near-term USD price dynamics and provide a fresh directional impetus to gold. This further warrants some caution before confirming that the XAU/USD has formed a bottom and positioning for any further appreciating move.

In the meantime, traders on Tuesday will take cues from the flash US PMI prints, due for release later during the early North American session. This, along with the US bond yields, will drive the USD demand. Apart from this, the broader risk sentiment would allow traders to grab short-term opportunities around gold.

Technical levels to watch

- GBP/USD whipsaws after UK services PMI improves but manufacturing PMI contracts.

- The US dollar maintains the pullback amid cautious optimism, weaker Treasury yields.

- Bear cross remains in play, as GBP bears eye a daily close below critical 1.1760 support line.

GBP/USD is struggling once again to extend the recovery while holding below the 1.1800 level, as bears remain unconvinced by the mixed UK Preliminary Business PMI surveys.