- Analytics

- News and Tools

- Market News

Analytics, News, and Forecasts for CFD Markets: currency news — 03-04-2024.

- AUD/USD edges up, buoyed by Fed's rate talk and mixed US data.

- Fed's data-focused rate policy, strong US job market, and services data are headwinds for the US Dollar.

- Australia's services sector gains boost AUD amid global economic uncertainties.

The Aussie Dollar posted solid gains against the US Dollar on Wednesday, boosted by falling US Treasury yields and a soft US Dollar. Federal Reserve policymakers grabbed the headlines, while US economic data was mixed, with a strong ADP report but softer PMIs. The AUD/USD trades at 0.6565, posting minimal gains of 0.02% early during Thursday’s Asian session.

AUD/USD sees slight uptick as dovish Federal Reserve remarks and uneven US data fuel optimism in Forex markets.

On Wednesday, the market was attentive to the remarks of Fed Chair Jerome Powell, who reiterated the US central bank's readiness to cut rates, albeit with a data-dependent approach. Atlanta Fed President Raphael Bostic's statement, supporting a rate cut in the last quarter of 2024, also drew significant attention.

Lately, Adriana Kugler, one of the newest Fed Governors appointed to the board, stated that the disinflation process would continue, and that would warrant lowering rates at least three times toward the last quarter of 2024.

The Aussie Dollar also benefited from an upbeat market mood as Wall Street snapped two days of losses. US Treasury yields finished flat, a headwind for the American currency. The US Dollar Index (DXY) tumbles more than 0.50%, down to 104.22.

Elsewhere, the March ADP report revealed that private hiring increased by 184K, exceeding estimates and forecasts. In the meantime, the US S&P Global and the ISM Services PMIs, were a touch softer.

In the meantime, Aussie’s data revealed the Judo Bank Services PMI improved from 53.5 in February to 54.4 in March. The report highlighted “This is the fourth consecutive month of improvement, with the services output index increasing by 8.4 points, the largest gain in the series outside of recovery from lockdowns.”

AUD/USD Price Analysis: Technical outlook

From a technical perspective, the AUD/USD shifted to a neutral-upward bias. A ‘bullish harami’ candlestick chart pattern, followed by Wednesday’s large candle breaching the 200-day moving average (DMA) at 0.6543, could pave the way to challenge the 100-DMA at 0.6597, ahead of the 0.6600 mark. The momentum has shifted in favor of the bulls, as the Relative Strength Index (RSI) turned bullish and aims higher.

On the other hand, a drop below the 200-DMA could expose the 0.6500 figure.

Australian Dollar FAQs

One of the most significant factors for the Australian Dollar (AUD) is the level of interest rates set by the Reserve Bank of Australia (RBA). Because Australia is a resource-rich country another key driver is the price of its biggest export, Iron Ore. The health of the Chinese economy, its largest trading partner, is a factor, as well as inflation in Australia, its growth rate and Trade Balance. Market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – is also a factor, with risk-on positive for AUD.

The Reserve Bank of Australia (RBA) influences the Australian Dollar (AUD) by setting the level of interest rates that Australian banks can lend to each other. This influences the level of interest rates in the economy as a whole. The main goal of the RBA is to maintain a stable inflation rate of 2-3% by adjusting interest rates up or down. Relatively high interest rates compared to other major central banks support the AUD, and the opposite for relatively low. The RBA can also use quantitative easing and tightening to influence credit conditions, with the former AUD-negative and the latter AUD-positive.

China is Australia’s largest trading partner so the health of the Chinese economy is a major influence on the value of the Australian Dollar (AUD). When the Chinese economy is doing well it purchases more raw materials, goods and services from Australia, lifting demand for the AUD, and pushing up its value. The opposite is the case when the Chinese economy is not growing as fast as expected. Positive or negative surprises in Chinese growth data, therefore, often have a direct impact on the Australian Dollar and its pairs.

Iron Ore is Australia’s largest export, accounting for $118 billion a year according to data from 2021, with China as its primary destination. The price of Iron Ore, therefore, can be a driver of the Australian Dollar. Generally, if the price of Iron Ore rises, AUD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Iron Ore falls. Higher Iron Ore prices also tend to result in a greater likelihood of a positive Trade Balance for Australia, which is also positive of the AUD.

The Trade Balance, which is the difference between what a country earns from its exports versus what it pays for its imports, is another factor that can influence the value of the Australian Dollar. If Australia produces highly sought after exports, then its currency will gain in value purely from the surplus demand created from foreign buyers seeking to purchase its exports versus what it spends to purchase imports. Therefore, a positive net Trade Balance strengthens the AUD, with the opposite effect if the Trade Balance is negative.

Federal Reserve (Fed) Governor Adriana Kugler said on Wednesday that she believes inflation will continue to fall this year and pave the way for the central bank to cut interest rates, per Reuters

Key quotes

“My policy rate expectation is consistent with March FOMC meeting policymaker projections.”

“If disinflation and labor market conditions proceed as I am currently expecting, then some lowering of the policy rate this year would be appropriate.”

“Expect the disinflationary trend to continue.”

“Policy is currently restrictive, and my baseline expectation is that disinflation will continue without a broad economic slowdown.”

“Such an outcome is not assured.”

“Inflation progress has sometimes been bumpy.”

“Annual core PCE at 2.8% represents 'considerable progress' but is still 'meaningfully above' Fed's 2% target.”

“Data on new tenant rent agreements suggest that housing inflation broadly will continue to cool.”

“Continued disinflation will indeed require further progress in housing and non-housing services.”

“Labor market has moved into better balance.”

“Suspect strong population growth 'helps resolve the puzzle' of labor market growth and strong consumption even as inflation eases.”

“Important that wage growth be consistent with 2% inflation over time; US is moving back toward that kind of wage growth.”

“Anchored inflation expectations are evident in consumer and business surveys.”

“Expect consumption growth to slow some this year.”

“Consumer spending was soft in January and February, suggesting we are on track for lower consumption growth in q1 vs second half of 2023.”

“Expect GDP growth this year to be solid but slower than 2023 pace of 3.1%.”

“My baseline expectation is that further disinflation can be accomplished without a significant rise in unemployment.”

“Appears supply networks are adapting to port of Baltimore disruption.”

“New businesses are creating a lot of new jobs.”

“Around 150,000 jobs a month have come from new businesses.”

Market reaction

At the press time, the US Dollar Index (DXY) was down 0.01% on the day to trade at 104.23.

Fed FAQs

Monetary policy in the US is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability and foster full employment. Its primary tool to achieve these goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, it raises interest rates, increasing borrowing costs throughout the economy. This results in a stronger US Dollar (USD) as it makes the US a more attractive place for international investors to park their money. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates to encourage borrowing, which weighs on the Greenback.

The Federal Reserve (Fed) holds eight policy meetings a year, where the Federal Open Market Committee (FOMC) assesses economic conditions and makes monetary policy decisions. The FOMC is attended by twelve Fed officials – the seven members of the Board of Governors, the president of the Federal Reserve Bank of New York, and four of the remaining eleven regional Reserve Bank presidents, who serve one-year terms on a rotating basis.

In extreme situations, the Federal Reserve may resort to a policy named Quantitative Easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used during crises or when inflation is extremely low. It was the Fed’s weapon of choice during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy high grade bonds from financial institutions. QE usually weakens the US Dollar.

Quantitative tightening (QT) is the reverse process of QE, whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing, to purchase new bonds. It is usually positive for the value of the US Dollar.

The final reading of Australia's Judo Bank Services Purchasing Managers Index (PMI) improved to 54.4 in March from the previous reading of 53.5, the latest data published by Judo Bank and S&P Global showed on Thursday.

The Judo Bank Australian Composite PMI rose to 53.3 in March versus 52.4 in the previous reading.

Additional takeaways

“Output index rising to a new cyclical high of 54.4. This is the fourth consecutive month of improvement, with the services output index increasing by 8.4 points, the largest gain in the series outside of recovery from lockdowns.”

“Services output index is now above its long-run average level of 51.7.”

“March 2024 reading is the highest since April 2022, when the monetary policy tightening cycle commenced.”

“Outstanding Business Index rose to its highest level since the Reserve Bank of Australia started raising interest rates in May 2022.”

“Other activity indicators in the survey were down slightly in March, but remained well above the neutral 50 index level.”

“Cost pressures remain elevated, although there are some signs of a gradual easing over the past six months.”

“Input price index fell slightly to 61.5, the lowest since 2021, but not much lower than the average reading of 62.8 seen through the second half of 2023.”

“Prices Charged Index remained unchanged at 55.0 in March, a little higher than the average over the past quarter and broadly in line with index readings of the past year.”

Market reaction

At the press time, the AUD/USD pair was up 0.01% on the day to trade at 0.6565.

Australian Dollar FAQs

One of the most significant factors for the Australian Dollar (AUD) is the level of interest rates set by the Reserve Bank of Australia (RBA). Because Australia is a resource-rich country another key driver is the price of its biggest export, Iron Ore. The health of the Chinese economy, its largest trading partner, is a factor, as well as inflation in Australia, its growth rate and Trade Balance. Market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – is also a factor, with risk-on positive for AUD.

The Reserve Bank of Australia (RBA) influences the Australian Dollar (AUD) by setting the level of interest rates that Australian banks can lend to each other. This influences the level of interest rates in the economy as a whole. The main goal of the RBA is to maintain a stable inflation rate of 2-3% by adjusting interest rates up or down. Relatively high interest rates compared to other major central banks support the AUD, and the opposite for relatively low. The RBA can also use quantitative easing and tightening to influence credit conditions, with the former AUD-negative and the latter AUD-positive.

China is Australia’s largest trading partner so the health of the Chinese economy is a major influence on the value of the Australian Dollar (AUD). When the Chinese economy is doing well it purchases more raw materials, goods and services from Australia, lifting demand for the AUD, and pushing up its value. The opposite is the case when the Chinese economy is not growing as fast as expected. Positive or negative surprises in Chinese growth data, therefore, often have a direct impact on the Australian Dollar and its pairs.

Iron Ore is Australia’s largest export, accounting for $118 billion a year according to data from 2021, with China as its primary destination. The price of Iron Ore, therefore, can be a driver of the Australian Dollar. Generally, if the price of Iron Ore rises, AUD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Iron Ore falls. Higher Iron Ore prices also tend to result in a greater likelihood of a positive Trade Balance for Australia, which is also positive of the AUD.

The Trade Balance, which is the difference between what a country earns from its exports versus what it pays for its imports, is another factor that can influence the value of the Australian Dollar. If Australia produces highly sought after exports, then its currency will gain in value purely from the surplus demand created from foreign buyers seeking to purchase its exports versus what it spends to purchase imports. Therefore, a positive net Trade Balance strengthens the AUD, with the opposite effect if the Trade Balance is negative.

- The daily RSI recovered from near-oversold levels.

- The hourly chart indicators exhibited a sharp uptick with the RSI above 70.

- Buyers need to breach the key 20-day SMA for further ascents.

The NZD/USD was trading around the 0.6000 zone during Wednesday's session, reflecting an increase of 0.55%. The technical outlook indicates that sellers have had a more significant influence on the market. Nevertheless, buying momentum grew during the session as the Greenback was one of the weakest performers due to fundamental reasons.

On the daily chart, the Relative Strength Index (RSI) predominantly exists in negative territory, despite Wednesday’s recovery from oversold areas, and currently stands at 44. This indicates that stronger market influence is currently in the hands of sellers despite the slight recovery.

NZD/USD daily chart

Turning to the hourly chart, an upward trend in the RSI was observed, reaching a peak at 76 before falling slightly to 71 as investors took some profits. At the same time, the Moving Average Convergence Divergence (MACD) histogram exhibited flat green bars, hinting at a waning short-term momentum. Despite an active sellers' market on the daily chart, the hourly indicators suggest a more balanced market with potential opportunities for buyers.

NZD/USD hourly chart

Broadly speaking, the NZD/USD is currently performing under a bearish signal across all Simple Moving Averages (SMA) as it trades below its 20,100-day, and 200-day averages. The completed SMA crossover between the 20 and 200-day averages adds arguments for a negative outlook and could limit the pair's upside.

- GBP/USD climbs to 1.264, lifted by soft USD and dovish Fed cues, weak services data.

- Powell ties rate cuts to data; Bostic hints at delayed cuts to late 2024.

- Shifts in BoE and Fed rate cut expectations indicate evolving monetary policies.

The Pound Sterling posted solid gains against the Greenback on Wednesday after bouncing from a seven-week low of 1.2539 on Tuesday. Federal Reserve officials crossing the newswires and weaker-than-expected US services sector data are a headwind for the US Dollar, which tumbled for the second day in a row. The GBP/USD trades at 1.264, gains 0.56%.

GBP/USD rebounds from lows as Fed officials' comments and US services sector data influence currency dynamics

The Institute for Supply Management (ISM) revealed a softer-than-expected Services PMI, along with Fed Chair Jerome Powell, reaffirming that interest rates would be cut, but it would depend on upcoming data. On the contrary, Atlanta’s Fed President Raphael Bostic stood by his stance of just one rate cut, adding that it could happen in the last quarter of 2024.

In the meantime, US Treasury yields trimmed its earlier gains a headwind for the buck. The US Dollar Index (DXY) which tracks the performance of the American currency against other six, tumbles 0.46%, down at 104.26. This comes after the release of the ISM Manufacturing PMI sent the DXY rallying to the 105.00 mark.

Bank of England and Fed rate cut expectations

Money market futures traders see the Bank of England (BoE) cutting rates 25 basis points in June, with odds standing at 66%. Across the Atlantic, traders had fully priced in a 25-basis point cut by the Fed until July 31.

GBP/USD Price Analysis: Technical outlook

Given the fundamental backdrop, GBP/USD price action suggests the pair could test the 50-day moving average (DMA) after reclaiming the 200 and the 100-DMA, each at 1.2586 and 1.2656, respectively. If those levels are taken out of the way, expect further upside at around 1.2700. On the other hand, if sellers step in and push the exchange rate below the 200-DMA at 1.2586, that could spur a test of 1.2500.

Pound Sterling FAQs

The Pound Sterling (GBP) is the oldest currency in the world (886 AD) and the official currency of the United Kingdom. It is the fourth most traded unit for foreign exchange (FX) in the world, accounting for 12% of all transactions, averaging $630 billion a day, according to 2022 data. Its key trading pairs are GBP/USD, aka ‘Cable’, which accounts for 11% of FX, GBP/JPY, or the ‘Dragon’ as it is known by traders (3%), and EUR/GBP (2%). The Pound Sterling is issued by the Bank of England (BoE).

The single most important factor influencing the value of the Pound Sterling is monetary policy decided by the Bank of England. The BoE bases its decisions on whether it has achieved its primary goal of “price stability” – a steady inflation rate of around 2%. Its primary tool for achieving this is the adjustment of interest rates. When inflation is too high, the BoE will try to rein it in by raising interest rates, making it more expensive for people and businesses to access credit. This is generally positive for GBP, as higher interest rates make the UK a more attractive place for global investors to park their money. When inflation falls too low it is a sign economic growth is slowing. In this scenario, the BoE will consider lowering interest rates to cheapen credit so businesses will borrow more to invest in growth-generating projects.

Data releases gauge the health of the economy and can impact the value of the Pound Sterling. Indicators such as GDP, Manufacturing and Services PMIs, and employment can all influence the direction of the GBP. A strong economy is good for Sterling. Not only does it attract more foreign investment but it may encourage the BoE to put up interest rates, which will directly strengthen GBP. Otherwise, if economic data is weak, the Pound Sterling is likely to fall.

Another significant data release for the Pound Sterling is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period. If a country produces highly sought-after exports, its currency will benefit purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

- The daily chart presents a strong buying momentum with indicators deep in positive territory.

- On the hourly chart, the RSI resides in the overbought zone, suggesting a short-term consolidation of the recent gains.

In Wednesday's session, the AUD/JPY pair is trading at 99.58, following an increase of 0.82%. Buyers appear in control, but indicators are flashing signals of a short-term consolidation.

On the daily chart, the AUD/JPY pair reveals a bullish sentiment. The Relative Strength Index (RSI) resides deep in positive territory, with recent readings reaching as high as 61, indicating the domination of buyers in the market. Furthermore, the rising green bars on the Moving Average Convergence Divergence (MACD) histogram show a positive momentum, supporting the bullish outlook.

AUD/JPY daily chart

Upon inspecting the hourly chart, the RSI readings consistently hover in the overbought zone, with the latest entry at 78 but the index has started to edge downwards. A flat green histogram on the MACD also gives arguments for a short-term consolidation.

AUD/JPY hourly chart

Considering the broader outlook, the pair also stands above the 20,100 and 200-day Simple Moving Averages (SMAs). This setup suggests short-term and long-term trends are bullish, and traders may expect further upside.

In conclusion, both daily and hourly charts for the AUD/JPY pair highlight a bullish outlook. The RSI values and the MACD histograms across both timelines point to strong upward movement, with buyers currently holding market reins. However, indicators on the hourly chart point to further consolidation as they lie deep in the overbought zone.

- Gold price soars, supported by weakening US Dollar in face of high Treasury yields.

- XAU/USD was boosted by Fed Chair Powell hinting at rate cuts within the year, contingent on sustained inflation decline.

- Despite a strong job market as shown by ADP data, indications of a slowdown in services activity contribute to the precious metal's gains.

Gold price climbs steadily, eyeing Wednesday's $2,300 psychological figure amid high US Treasury bond yields and a soft US Dollar. Speeches from Federal Reserve officials, strong jobs data, and a dip in services business activity weighed on the American currency. Therefore, the XAU/USD spot price is at $2,295, refreshing all-time highs and gaining more than 0.60%.

Recently, Fed Chair Jerome Powell stated the US central bank has time to deliberate about rate cuts, given the strength of the economy and the inflation readings. He reiterated that if the economy evolves as expected, they will cut borrowing costs “at some point this year.”

Nevertheless, Powell emphasized that could happen once they “have greater confidence that inflation is moving sustainably down.”

Earlier, Atlanta Fed President Raphael Bostic acknowledged the robust momentum of the economy yet stressed the necessity for both growth and inflation to decelerate. He forecasts a rate cut in the final quarter of 2024 and envisions inflation aligning with the Fed's 2% target by 2026.

The US economic calendar highlighted employment figures and Services PMI. ADP reported higher-than-expected private sector job growth in March, indicating a robust labor market favorable to the US Dollar. However, signs of slowing business activity from recent S&P Global and ISM Services PMI reports have limited the US Dollar's recovery.

Daily digest movers: Gold price shrugs off hawkish Fed speakers amid mixed data

- The ADP Employment Change for March exceeded expectations, reporting 184,000 jobs added, outperforming the anticipated 148,000 and February's 155,000.

- In service sector activity, S&P Global noted a decrease in the Services PMI to 51.7 from 52.3, with the Composite Index also dipping from 52.5 to 52.1. The ISM's Non-Manufacturing PMI fell to 51.4, below the expected 52.7 and the previous 52.6, indicating a slowdown in service sector expansion.

- Cleveland Fed President Loretta Mester expressed that current data does not support a rate cut by the May meeting, but she anticipates three rate cuts in 2024, highlighting the Fed's task of balancing inflation and employment risks.

- Similarly, San Francisco Fed President Mary Daly emphasized the need to evaluate the duration for maintaining current interest rates. While Daly supports the possibility of three rate cuts, she clarified that this outlook should be seen as a projection rather than a guarantee.

- In terms of the Federal Reserve's future interest rate movements, the CME FedWatch Tool indicates that traders currently assign a 58% likelihood to the prospect of the US central bank reducing borrowing costs.

Technical analysis: Gold rally to extend as buyers target $2,300

The XAU/USD daily chart suggests the yellow metal is headed toward the $2,300 figure amid renewed buying pressures observed in the Relative Strength Index (RSI). On Monday, I mentioned that “The XAU/USD daily chart depicts Gold's last uptick to new all-time highs, achieved on lower momentum, as depicted by the Relative Strength Index (RSI).” However, as of writing, the RSI has punched above the 80.00 threshold, an indication that buyers are in charge.

With price action at uncharted territory, the next resistance level would be the $2,300 mark, followed by the $2,350 psychological figure. Up next would be $2,400.

On the other hand, if XAU/USD drops below $2,250, that could sponsor a correction. The first support would be the $2,200 figure, followed by the March 8 high turned support at $2,195, ahead of extending its losses to $2,150.

Gold FAQs

Gold has played a key role in human’s history as it has been widely used as a store of value and medium of exchange. Currently, apart from its shine and usage for jewelry, the precious metal is widely seen as a safe-haven asset, meaning that it is considered a good investment during turbulent times. Gold is also widely seen as a hedge against inflation and against depreciating currencies as it doesn’t rely on any specific issuer or government.

Central banks are the biggest Gold holders. In their aim to support their currencies in turbulent times, central banks tend to diversify their reserves and buy Gold to improve the perceived strength of the economy and the currency. High Gold reserves can be a source of trust for a country’s solvency. Central banks added 1,136 tonnes of Gold worth around $70 billion to their reserves in 2022, according to data from the World Gold Council. This is the highest yearly purchase since records began. Central banks from emerging economies such as China, India and Turkey are quickly increasing their Gold reserves.

Gold has an inverse correlation with the US Dollar and US Treasuries, which are both major reserve and safe-haven assets. When the Dollar depreciates, Gold tends to rise, enabling investors and central banks to diversify their assets in turbulent times. Gold is also inversely correlated with risk assets. A rally in the stock market tends to weaken Gold price, while sell-offs in riskier markets tend to favor the precious metal.

The price can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can quickly make Gold price escalate due to its safe-haven status. As a yield-less asset, Gold tends to rise with lower interest rates, while higher cost of money usually weighs down on the yellow metal. Still, most moves depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAU/USD). A strong Dollar tends to keep the price of Gold controlled, whereas a weaker Dollar is likely to push Gold prices up.

Further selling pressure prompted the Greenback to retreat further and put the USD Index (DXY) on track to challenge the 104.00 support after weaker-than-expected. On another front, further disinflationary pressures in the euro area bolstered an ECB rate cut in the summer.

Here is what you need to know on Thursday, April 4:

The Greenback faced extra downside pressure, putting the 104.00 zone to the test when tracked by the USD Index (DXY). On April 4, February’s Balance of Trade results are due seconded by weekly Initial Jobless Claims. In addition, the Fed's Barkin, Goolsbee, and Mester are all due to speak.

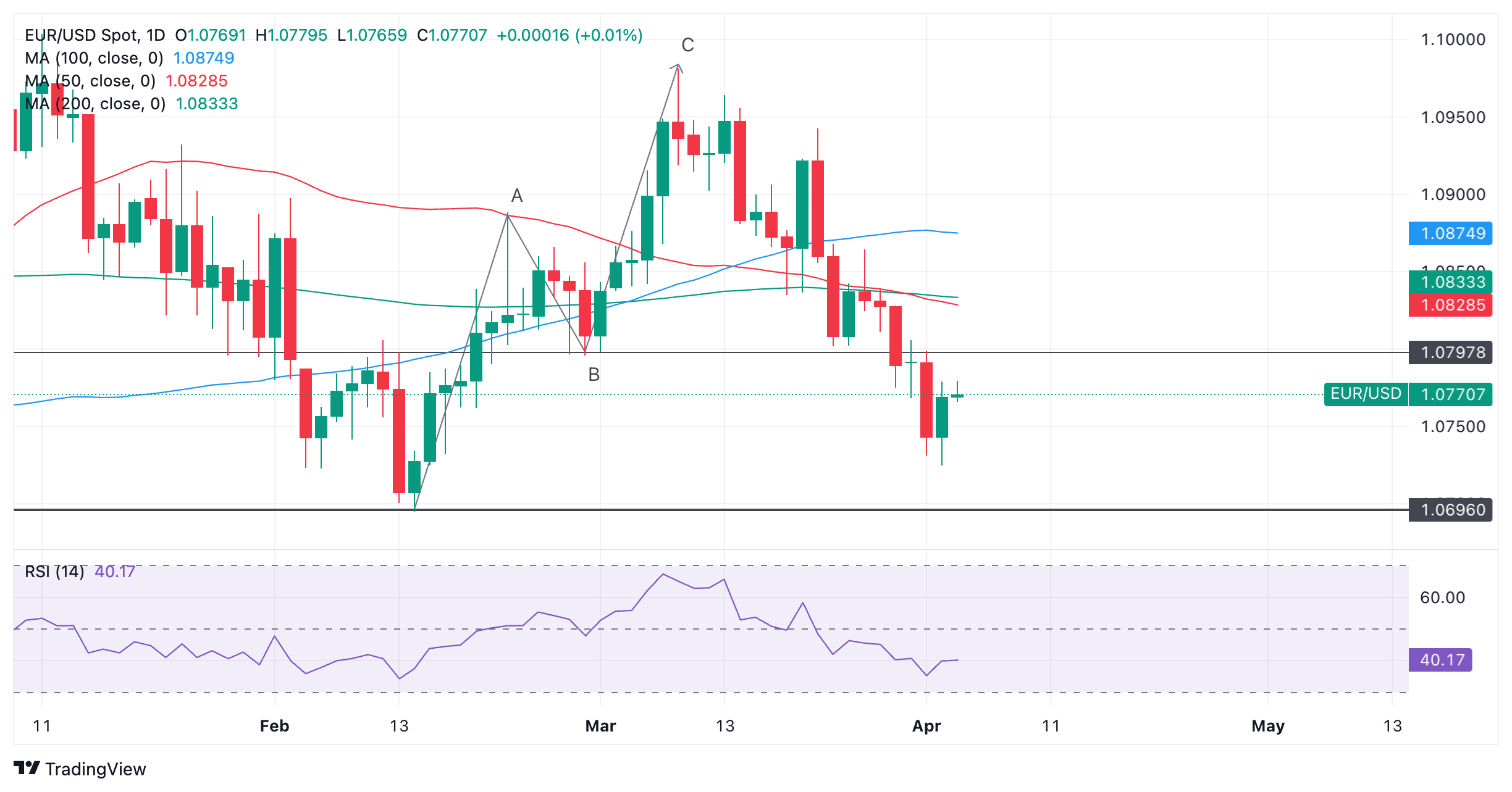

EUR/USD gathered extra upside traction and managed to confront the key 200-day SMA in the 1.0830 region. On April 4, the final HCOB Services PMIs in Germany and the euro area are expected along with the release of the ECB Accounts.

GBP/USD rose to multi-day highs well past the 1.2600 mark, an area coincident with the interim 100-day SMA. The final S&P Global Services PMI will take centre stage across the Channel on April 4.

USD/JPY kept its side-lined performance intact for yet another session, always below the 152.00 milestone. The usual weekly Foreign Bond Investment figures are scheduled for April 4 in the Japanese docket.

AUD/USD picked up further buying interest and left behind the critical 200-day SMA around 0.6545. On April 4, the final Judo Bank Services PMI is due.

Unabated geopolitical concerns lifted WTI prices to new 2024 peaks north of the $86.00 mark per barrel.

Persistent safe-haven demand and hopes of Fed rate cuts in June helped Gold prices reach a record peak near the $2,300 mark per troy ounce. In the same line, the rally in Silver remained unabated, hitting fresh highs just above the $27.00 level per ounce for the first time since June 2021.

- The daily RSI on the GBP/JPY reveals a strong bullish posture, while the MACD shows a shift towards a more balanced market.

- The hourly chart discloses the RSI regularly exceeding overbought thresholds.

In Wednesday's session, the GBP/JPY is trading at the 191.65 level, showing a 0.57% uptick. The market sentiment for GBP/JPY is majorly bullish, but there is a high likelihood that investors may start taking profits as the cross reached overbought conditions on the hourly chart.

On the daily chart, the Relative Strength Index (RSI) pointing north above 50 indicates that buyers currently have a slight advantage in the market. While there are no extreme levels, suggesting overbought conditions, the RSI reveals a generally strong bullish posture. On the contrary, the Moving Average Convergence Divergence (MACD) is generating decreasing red bars, hinting at the presence of negative momentum and pointing toward more balanced market conditions.

GBP/JPY daily Chart

The hourly chart presents a contrasting perspective with the RSI logging higher values, lying deep in overbought terrain. This tends to predict a downward correction as the upward momentum may be overextended. In addition, the green rising bars of the MACD histogram also demonstrate positive momentum, reinforcing the strong presence of buyers in the market.

GBP/JPY hourly Chart

In terms of the overall trend, the GBP/JPY is positioned above its 20-day, 100-day, and 200-day SMAs. This pattern signals an enduring bullish trend in both short-term and long-term periods. In summary, while both the daily and hourly charts appear mostly bullish, the indicators reveal a stronger upward momentum in the hourly market with the possibility of a downward correction in the short term. However, as the pair holds above the main SMAs, the downward movements could be considered a mere correction.

- The Euro jumps on Wednesday with the US Dollar dropping across the board.

- The unexpected decline of the US ISM Services PMI has eased concerns about a hawkish turn by the Fed.

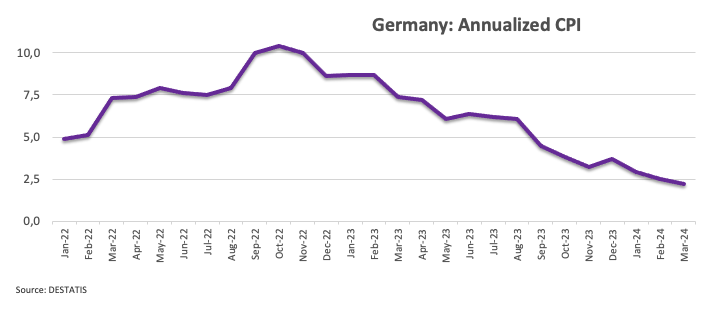

- Earlier on Wednesday Eurozone CPI reflected softer-than-expected price pressures in March.

The Euro is going through a sharp recovery in Wednesday’s US trading session. The pair has rallied about 60 pips following weaker-than-expected US services sector’s activity, which has eased fears of a hawkish steer by the Federal Reserve.

Data released by ISM Insitute revealed that business activity in the services sector slowed down to 51.4 in March from 52.6 in the previous month, against expectations of a slight acceleration to 52.7. Beyond that, the Prices Paid sub-index has dropped to 53.4 from 58.6 in February and 64 in January confirming the disinflationary trend in the sector.

The PMI figures have offset the impact of a strong ADP report, which suggests a resilient labour market ahead of Friday’s Nonfarm Payrolls report. later on Wednesday Atlanta Fed President Bostic and Fed Chair Powell have cooled hopes about imminent rate cuts, yet with no significant impact on the pair.

During the European Session, the Eurozone CPI figures confirmed the soft inflation readings seen in Germany on Tuesday. The Core Inflation has declined below the 3% yearly rate, with the headline CPI easing to 2.4%, well below the 2.6% foreseen by the market. These figures pave the path for the ECB to cut rates over the coming months, although the impact on the Euro has been marginal.

- EUR/JPY breaks above Tenkan-Sen, eyes 165.00 potential.

- Holding above 164.00 may lead to testing yearly highs.

- Bears aim below 164.00 for reversal; Tenkan-Sen, Kijun-Sen as supports.

The Euro posted solid gains against the Japanese Yen (JPY) on Wednesday, amid an improvement in risk appetite and the dovish stance adopted by the Bank of Japan (BoJ) despite rising interest rates. At the time of writing, the EUR/JPY trades at 164.25, up 0.67%.

EUR/JPY Price Analysis: Technical outlook

Euro bulls re-entered the market, lifting the EUR/JPY pair above the Tenkan-Sen a 163.71, which opened the door to reclaim the 164.00 mark. That suggests that buyers are gathering steam, which would open the door to challenge the 165.00 mark. A breach of the latter will expose the year-to-date (YTD) high of 165.34.

On the flip side, sellers must drag prices below 164.00 to challenge the new Tenkan-Sen level at 163.71, the next support level. Once surpassed, traders could test the Senkou Span Aat 163.25, followed by the Kijun-Sen level at 162.78.

EUR/JPY Price Action – Daily Chart

- ISM Services PMI figures from March were weaker than expected. ADP numbers were strong.

- The odds of an interest rate cut somewhat increased for the June Fed meeting.

- The focus is set on Friday’s Nonfarm Payroll report.

The US Dollar Index (DXY) is currently trading at 104.3, reflecting a daily decline. Despite the Federal Reserve's (Fed) cautious stance, consensus forecasts indicate that the beginning of the easing cycle will begin in June. That being said, mixed data from the US economy may make Fed officials think twice about rushing to start cutting.

The US labor market remains resilient as well as the overall economy, with little signs of a slowdown. In case the economy doesn’t show conclusive evidence of cooling down, the Fed might consider delaying the start of the easing cycle.

Daily digest market movers: DXY impacted by service sector slowdown, Fed remains cautious

- The Institute for Supply Management (ISM) released a report noting that business activity in the US service sector expanded in March, but growth was slower than the previous month. The ISM Services Purchasing Managers Index (PMI) decreased to 51.4 from February's 52.6.

- The reported YoY decrease in the Prices Paid Index from 58.6 to 53.4 suggests an overall declining trend in inflation.

- The Employment Index noted a slight yearly increase, up to 48.5 from an earlier 48.0, continuing to signify a decline in payrolls within the service sector.

- Data from Automatic Data Processing (ADP) showed private sector employment in the US increased in March with 184,000 new jobs, which was an improvement upon the revised February figures of 155,000 from 140,000.

- Cleveland Fed President Loretta Mester and San Francisco Fed President Mary Daly suggested three potential rate cuts in 2024 but underscored that it's too soon to act.

- On Tuesday, Jerome Powell commented that there was no rush to cut rates and that the bank remains data-dependent.

- June has not been ruled out for the initial cut, with current market odds still favoring a rate cut at 68%.

DXY technical analysis: DXY grapples with slight selling pressure, overall bullish sentiment remains

In the DXY technical landscape, the Relative Strength Index (RSI), although on a negative slope, is still situated in positive territory, implying a stalling upward momentum. However, the recent decrease in green bars on the Moving Average Convergence Divergence (MACD) histogram echoes a similar sentiment, suggesting a subtle shift in the dynamics from buying to selling pressure.

Still, on an encouraging note, the index continues to trade above the critical support levels dictated by its 20, 100, and 200-day Simple Moving Averages (SMAs). Despite a short-term negative outlook, this notably upbeat stance suggests that the bulls are still in control over the longer horizon.

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022. Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

- Dow Jones bounces up as soft US services data eases concerns about a “higher for longer” monetary policy outlook.

- US Services activity softened against expectations in March with the Prices Paid sub-index posting its lowest reading in years.

- Intel is leading losses in the Dow Jones after news of hefty losses in its foundry business.

The Dow Jones Industrial Average (DJIA) has moved into positive territory following a weak opening. The soft US services activity data has offered some relief to investors, increasingly concerned that a string of strong US macroeconomic releases would force the Fed to dial down their monetary easing plans.

The US ISM Services PMI eased to 51.4 in March from 52.6 in February against market expectations of a slight increase to 52.7. Beyond that, the Prices Paid sub-index retreated to 53.4 from 58.6 in the previous month. This is the lowest reading in years and suggests a disinflationary contribution to the economy.

All three main Wall Street Indexes have jumped after the data. The Dow Jones is lagging with a 1.2% advance, trading at 39,243, still well below the 40,000 high hit last week. The NASDAQ is leading gains with a 0.53% advance to 16,326, followed by the S&P 500, up 0.37% to 5,225.

Dow Jones news

The Energy sector is the best performer on Wednesday with a 0.65% advance followed by Industrials, up 0.61%. On the losing end, only three of the eleven sectors are in the red with Consumer Staples losing 0.99% followed by the Real State, down 0.25%.

Down to single stocks, the market is showing a more mixed picture. Intel (INTC) fell 7.2% to $40.88 following a report stating that its foundry business recorded an operating loss of $7 billion in 2023.

Next is Procter & Gamble (PG), down 2.54% to $156.52, and Johnson & Johnson (JNJ), losing 1.35% to $155.59.

On the positive side, Caterpillar (CAT) advances 1.7% to $372, followed by Apple (AAPL), which is 0.88% up at $170.37.

Dow Jones technical outlook

The technical picture is little changed from Tuesday, with the Dow Jones Index correcting lower, yet with the broader bullish trend still intact. Price Action remains contained between the 50% and the 61.8% Fibonacci retracement of the March rally, at 39,300, with bears in control after the rejection at the 40,000 psychological level last week.

The 39,000 support area is holding sellers for now and closing the path to the trendline support, now at 38,850. On the upside, the index is struggling to breach the mentioned 50% Fibonacci retracement at 39,195. Further up at 39,457 and the mentioned 40,000 would be the next targets.

Dow Jones 4-Hour Chart

Dow Jones FAQs

The Dow Jones Industrial Average, one of the oldest stock market indices in the world, is compiled of the 30 most traded stocks in the US. The index is price-weighted rather than weighted by capitalization. It is calculated by summing the prices of the constituent stocks and dividing them by a factor, currently 0.152. The index was founded by Charles Dow, who also founded the Wall Street Journal. In later years it has been criticized for not being broadly representative enough because it only tracks 30 conglomerates, unlike broader indices such as the S&P 500.

Many different factors drive the Dow Jones Industrial Average (DJIA). The aggregate performance of the component companies revealed in quarterly company earnings reports is the main one. US and global macroeconomic data also contributes as it impacts on investor sentiment. The level of interest rates, set by the Federal Reserve (Fed), also influences the DJIA as it affects the cost of credit, on which many corporations are heavily reliant. Therefore, inflation can be a major driver as well as other metrics which impact the Fed decisions.

Dow Theory is a method for identifying the primary trend of the stock market developed by Charles Dow. A key step is to compare the direction of the Dow Jones Industrial Average (DJIA) and the Dow Jones Transportation Average (DJTA) and only follow trends where both are moving in the same direction. Volume is a confirmatory criteria. The theory uses elements of peak and trough analysis. Dow’s theory posits three trend phases: accumulation, when smart money starts buying or selling; public participation, when the wider public joins in; and distribution, when the smart money exits.

There are a number of ways to trade the DJIA. One is to use ETFs which allow investors to trade the DJIA as a single security, rather than having to buy shares in all 30 constituent companies. A leading example is the SPDR Dow Jones Industrial Average ETF (DIA). DJIA futures contracts enable traders to speculate on the future value of the index and Options provide the right, but not the obligation, to buy or sell the index at a predetermined price in the future. Mutual funds enable investors to buy a share of a diversified portfolio of DJIA stocks thus providing exposure to the overall index.

In his remarks at the Stanford Graduate School of Business, Chair Jerome Powell reiterated once again that the policy rate is likely at its peak in the current cycle.

Additional key quotes

“If economy evolves as central bank expects, most federal open market committee participants see it as likely appropriate to begin cutting policy rate at some point this year.”

“Too soon to say whether recent inflation readings are more than just a bump”.

“Fed has time to let incoming data guide its policy decisions; central bank is making decisions meeting by meeting.”

“Recent readings on job gains and inflation higher than expected, but do not materially change overall picture.”

“Outlook still quite uncertain, fed faces risks on both sides of its mandate”.

“Fed continues to believe policy rate likely at peak for this cycle.”

Market Reaction

The Greenback mainatins its negative performance so far on Wednesday, prompting the USD Index (DXY) to drop to new lows near 104.30 amidst higher yields and a dominating risk-on sentiment among investors.

- Mexican Peso rises despite higher US Treasury yields, mixed data.

- Atlanta Fed President Bostic’s hawkish outlook sponsored traders repricing for a less dovish Fed.

- US jobs data was strong, while Services PMI suggests business activity decelerates.

The Mexican Peso posts gains against the US Dollar on Wednesday as US Treasury yields climbed, sponsored by Atlanta Federal Reserve President Raphael Bostic's hawkish comments. Economic data from the United States (US) was mixed, while goodish Gross Fixed Investment figures in Mexico capped the emerging market currency’s fall. The USD/MXN trades at 16.54, down 0.06%.

The Greenback is trading mixed during the session, depreciating against most G8 currencies but clocking gains against emerging market ones. Atlanta Fed President Raphael Bostic highlighted the economy's strong momentum but emphasized the need for growth and inflation to slow. He anticipates a rate cut in the last quarter of 2024 and projects inflation to reach the Fed's 2% target by 2026.

Data-wise, the US economic docket features employment data and Services Purchasing Managers Index (PMI) by S&P and the Institute for Supply Management (ISM). Automatic Data Processing (ADP) revealed that private hiring increased above estimates and the previous month’s reading in March, portraying a tight labor market, which is positive for the Greenback. However, recently released data suggesting that business activity is cooling down, as portrayed by S&P Global and ISM Services PMI, capped US Dollar recovery.

Daily digest market movers: Mexican Peso advances, shrugging off mixed US data

- Mexico’s Gross Fixed Investment figures in January came at 0.1% MoM, up from December’s 0%. In the twelve months to January, investment grew 15.3%, crushing December’s 13.4% increase.

- Last week, Banxico Governor Victoria Rodriguez Ceja remained dovish despite acknowledging that the battle against inflation hasn’t been won. She added, “When macroeconomic conditions and the inflationary outlook allow us to make additional adjustments to the reference rate to the one we already have, I consider that they would be gradual.”

- The ADP Employment Change in March was 184K, above the 148K foreseen by the consensus and February’s 155K.

- S&P Global revealed that the Services PMI came to 51.7, down from 52.3, while the Composite Index slowed from 52.5 to 52.1. The ISM revealed that Non-Manufacturing PMI was 51.4, down from 52.6 and lower than projections for a 52.7 expansion.

- On Tuesday, Cleveland Fed President Loretta Mester said that she doesn’t have enough information for a May meeting cut yet foresees three rate cuts in 2024. Mester added the Fed’s challenge would be balancing the risks between inflation and employment.

- San Francisco Fed President Mary Daly said the Fed needs to see how long to keep rates at current levels. She supports three rate cuts but added that it’s a projection, not a promise.

- Regarding future interest rate expectations of the Fed, the CME FedWatch Tool suggests that traders see a 57% chance of the US central bank cutting borrowing costs.

Technical analysis: Mexican Peso buyers in charge but could shift neutral with USD/MXN clearing 16.70

The USD/MXN remains bearish with sellers eyeing a re-test of the year-to-date (YTD) low of 16.51. Nevertheless, the pair could consolidate at 16.50 as the Relative Strength Index (RSI) remains in bearish territory. But sellers are losing momentum. However, a push below 16.50 would expose the October 2015 low of 16.32, ahead of the 16.00 mark.

On the flip side, If USD/MXN buyers enter, they must lift the exchange rate above the 16.70 area. Once cleared, the next stop would be the 50-day Simple Moving Average (SMA) at 16.94, with further upside seen at the 100-day SMA at 17.04, ahead of the 200-day SMA at 17.18.

Mexican Peso FAQs

The Mexican Peso (MXN) is the most traded currency among its Latin American peers. Its value is broadly determined by the performance of the Mexican economy, the country’s central bank’s policy, the amount of foreign investment in the country and even the levels of remittances sent by Mexicans who live abroad, particularly in the United States. Geopolitical trends can also move MXN: for example, the process of nearshoring – or the decision by some firms to relocate manufacturing capacity and supply chains closer to their home countries – is also seen as a catalyst for the Mexican currency as the country is considered a key manufacturing hub in the American continent. Another catalyst for MXN is Oil prices as Mexico is a key exporter of the commodity.

The main objective of Mexico’s central bank, also known as Banxico, is to maintain inflation at low and stable levels (at or close to its target of 3%, the midpoint in a tolerance band of between 2% and 4%). To this end, the bank sets an appropriate level of interest rates. When inflation is too high, Banxico will attempt to tame it by raising interest rates, making it more expensive for households and businesses to borrow money, thus cooling demand and the overall economy. Higher interest rates are generally positive for the Mexican Peso (MXN) as they lead to higher yields, making the country a more attractive place for investors. On the contrary, lower interest rates tend to weaken MXN.

Macroeconomic data releases are key to assess the state of the economy and can have an impact on the Mexican Peso (MXN) valuation. A strong Mexican economy, based on high economic growth, low unemployment and high confidence is good for MXN. Not only does it attract more foreign investment but it may encourage the Bank of Mexico (Banxico) to increase interest rates, particularly if this strength comes together with elevated inflation. However, if economic data is weak, MXN is likely to depreciate.

As an emerging-market currency, the Mexican Peso (MXN) tends to strive during risk-on periods, or when investors perceive that broader market risks are low and thus are eager to engage with investments that carry a higher risk. Conversely, MXN tends to weaken at times of market turbulence or economic uncertainty as investors tend to sell higher-risk assets and flee to the more-stable safe havens.

- Canadian Dollar bounces up with the US Dollar retreating on downbeat US data.

- US service sector activity decelerated against expectations with Prices Paid printing lowest level in years.

- Strong US ADP and hawkish comments from Fed’s Bostic have failed to support USD.

The Canadian Dollar (CAD) is trading higher on Wednesday, retracing the previous two days’ losses. The Loonie is favored by the US Dollar's knee-jerk reaction following downbeat US services activity data.

The US ISM Services PMI missed market expectations in March, with the Prices Paid sub-index showing a significant slowdown. This has eased investors' fears of a strong economy that would prompt the Federal Reserve (Fed) to dial down its monetary easing plans, which have pushed US Treasury yields and the US Dollar lower.

The downbeat services data has offset the larger-than-expected increase in the ADP Employment Report, which opens the doors for a bright Nonfarm Payrolls reading on Friday that might restore confidence in the US Dollar.

Beyond that, the increasing geopolitical tensions and growing concerns about tighter supply have pushed crude prices to a fresh year-to-date (YTD) high. This is providing additional support to the commodity-linked CAD.

Daily digest market movers: USD/CAD dives as services activity data disappoints

- Later on Wednesday, Fed Chair Jerome Powell will speak about the US economic outlook and might shed some light on the central bank’s monetary policy plans.

- Canadian Dollar regained lost ground on Wednesday with the USD under pressure ahead of Fed Powell’s speech.

- US ISM Services PMI dropped to 51.4 in March from 52.6 in February against market expectations of a slight increase to 52.7.

- The ISM Prices Paid sub-index has dropped to 53.4, its lowest level in years, from 58.6 in February and 64 in January. This signals a disinflationary contribution to the economy.

- Earlier on Wednesday, the US ADP Employment Report showed an increase of 184,000 new payrolls in March from 155,000 in February. The market had forecasted a decline to 148,000.

- Atlanta Fed President Raphael Bostic struck a hawkish note on Wednesday suggesting that rate cuts might not arrive after the Q4.

Canadian Dollar price today

The table below shows the percentage change of Canadian Dollar (CAD) against listed major currencies today. Canadian Dollar was the weakest against the .

| USD | EUR | GBP | CAD | AUD | JPY | NZD | CHF | |

| USD | -0.53% | -0.44% | -0.30% | -0.66% | 0.12% | -0.44% | -0.43% | |

| EUR | 0.53% | 0.08% | 0.23% | -0.13% | 0.64% | 0.07% | 0.09% | |

| GBP | 0.43% | -0.10% | 0.14% | -0.22% | 0.55% | -0.01% | 0.01% | |

| CAD | 0.30% | -0.23% | -0.13% | -0.35% | 0.42% | -0.14% | -0.15% | |

| AUD | 0.64% | 0.12% | 0.23% | 0.35% | 0.77% | 0.19% | 0.23% | |

| JPY | -0.11% | -0.65% | -0.57% | -0.41% | -0.76% | -0.56% | -0.57% | |

| NZD | 0.44% | -0.09% | 0.01% | 0.14% | -0.22% | 0.56% | 0.01% | |

| CHF | 0.43% | -0.09% | -0.01% | 0.12% | -0.22% | 0.55% | -0.01% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent EUR (base)/JPY (quote).

Technical analysis: The USD/CAD is under pressure with support levels at 1.3515 and 1.3475

The strong bearish reversal on the USD/CAD following the release of the ISM Services PMI has put bears back in control. They aim to breach support at 1.3515, which is under pressure at the moment.

The overall picture shows choppy and volatile trading with the pair still moving inside a slightly bullish channel. The mentioned 1.3515 level is guarding the base of the channel at 1.3475 and 1.3440. On the upside, resistances are at 1.3585 and 1.3615.

USD/CAD 4-Hour Chart

- USD/CHF faces selling pressure near 0.9100 as US Dollar drops on weak ISM Services PMI data.

- Fed’s hawkish guidance has dented Fed rate cut expectations for June.

- Swiss weak Retail Sales boost speculation for more rate cuts by the SNB.

The USD/CHF pair faces a sharp sell-off near the round-level resistance of 0.9100 as the United States Institute of Supply Management (ISM) has reported weak Services PMI data for March. The Services PMI, which represents the service sector that accounts for two-thirds of the US economy, falls to 51.4 from expectations of 52.7 and the prior reading of 52.6.

The US Dollar has faced significant selling pressure after weak US Services PMI data. The US Dollar Index (DXY), which tracks the Greenback’s value against six major currencies, drop to 104.40. The market sentiment improves as the S&P 500 has added significant gains after a subdued opening

Meanwhile, market expectations for the Federal Reserve (Fed) reducing interest rates from the June meeting have eased significantly. The CME FedWatch tool shows that traders are pricing in a 54% chance that the Fed will trim interest rates in June, down from 70% a week ago. 10-year US Treasury yields rise to 4.39%.

Market prospects for the Fed pivoting to rate cuts have eased due to hawkish guidance from Fed policymakers. Atlanta Fed Bank President Raphael Bostic told CNBC that he sees the central bank reducing interest rates only once this year as the economy is maintaining strong momentum.

This week, investors will keenly focus on the US Nonfarm Payrolls (NFP) data for March, which will be published on Friday.

On the Swiss Franc front, weak Real Retail Sales have boosted expectations of more rate cuts by the Swiss National Bank (SNB). The Retail Sales data, which represents consumer spending, surprisingly dropped by 0.2% while investors projected a growth of 0.4%. Deepening cost-of-living crisis would force SNB policymakers to consider more quantitative easing decisions.

- US ISM Services PMI declined in March but held above 50.

- US Dollar Index stays in negative territory near 104.50.

Business activity in the US service sector continued to expand in March, albeit at a more moderate pace than in February, with the ISM Services PMI edging lower to 51.4 from 52.6. This reading came in below the market expectation of 52.7.

Other details of the report showed that the Prices Paid Index, the inflation component, declined to 53.4 from 58.6, while the Employment Index recovered to 48.5 from 48.0, reflecting a continuing decrease in the sector's payrolls.

Assessing the survey's findings, "the decrease in the rate of growth in March and the decline in the composite index is a result of slower new orders growth, faster supplier deliveries and a contraction in employment," said Anthony Nieves, Chair of the Institute for Supply Management Services Business Survey Committee, and continued:

"The report continued to reflect growth month over month. Respondents indicated continuing improvement in logistics and the supply chain. Employment challenges remain a combination of difficulties in backfilling positions and/or controlling labor expenses."

Market reaction

The US Dollar came under selling pressure with the immediate reaction to the PMI data. At the time of press, the US Dollar Index was down 0.25% on the day at 104.49.

- USD/CAD is steadily channeling higher on US Dollar strength.

- Underneath price lie the three most important Moving Averages providing a safety net.

- Price is marginally biased to continue rising within the bullish channel.

USD/CAD is broadly channeling higher on the daily chart as the US Dollar (USD) steadily appreciates against the Canadian Dollar (CAD).

The range stretches from around the 1.3600s to the 1.3400s at the moment, although it is incrementally slanting higher.

US Dollar versus Canadian Dollar: Daily chart

USD/CAD is currently trading plum in the middle of the channel as it seesaws between tepid gains and losses.

Given the bullish slant to the channel there is a slight but not significant bias for more upside and the pair could rise to the top of the channel at roughly 1.3675.

Clustering just beneath price action around the 1.3500 level are the three most important Moving Averages – the 50, 100 and 200-day (Simple Moving Averages). These are key because they are not only followed by private investors but also institutional players.

Additionally, on the chart of USD/CAD it is notable how price action has respected the support cushion provided by these SMAs on several occasions during the formation of the channel.

A move down from the current level in the mid 1.3500s will find support at the first SMA, the 50-day, at 1.3512, and probably bounce. Even if it penetrates below it is likely to find support from the 200-day SMA at 1.3502.

If it gets through all three SMAs the bottom of the channel comes in with further support at roughly 1.3470.

- USD/JPY hovers near historic highs around 152.00 ahead of Fed Powell’s speech.

- The US ADP Employment report for March has indicated that private labor demand remains strong.

- Investors remain uncertain over Japan’s wage growth spiral.

The USD/JPY pair rebounds to historic highs of 152.00 in Wednesday’s early American session. The asset is expected to extend its upside by easing expectations that the Federal Reserve (Fed) will begin reducing interest rates from the June meeting.

Fed policymakers don’t see any urgency for rate cuts as labor market conditions are tight and the economic outlook is strong. On Tuesday, Cleveland Fed Bank President Loretta Mester said that the central bank sees more risk in cutting interest rates too early. Fed Mester added: “With labor markets and economic growth both being very solid, we do not need to take that risk”. At the same time, she sees three rate cuts as “reasonable” this year.

Meanwhile, the United States ADP reported upbeat employment data for March. The agency reported that private employers hired 184K new workers against expectations of 148K and the prior reading of 155K (revised up from 140K).

Going forward, investors will focus on Fed Chairman Jerome Powell's speech, which is expected at 16:10 GMT. Powell is expected to provide cues about when the central bank will pivot to rate cuts.

Meanwhile, the Japanese Yen is broadly weak as investors lack confidence that the Bank of Japan (BoJ) will tighten its policy sooner due to uncertainty over the wage growth spiral. Investors seem to have digested fears of Japan’s intervention in the FX domain to support the Japanese Yen.

- AUD/USD pauses its slide from the March 8 highs following the release of the RBA minutes.

- The minutes showed risks to the outlook as more balanced and notably did not mention discussing raising interest rates.

- US data showed a rise in payrolls commensurate with the US’s solid run of employment data.

The AUD/USD trades marginally higher in the 0.6510s midweek after pivoting and temporarily pausing its almost-month-long broad slide down from the early March 0.6660 highs.

The key event for the Australian Dollar was the release of the Reserve Bank of Australia (RBA) meeting minutes from the March policy meeting on Tuesday.

In the minutes, a shift in language was noted by the mention, for the first time, that the Board had not considered the option to raise interest rates.

On monetary policy, the central thrust appeared to be that the Board agreed “it was difficult to either rule in or out future changes in cash rate,” a statement repeated several times in the minutes.

The balance of risks to the outlook had changed and were “a little more even” than previously, it was noted.

The minutes showed a shift from a slightly hawkish view to a more “neutral stance,” according to analysts at Westpac.

In the US, data out on Wednesday showed ADP Employment Change private payrolls registered a rise of 184,000 new workers starting jobs in the month of March, beating analysts’ expectations of 148,000.

The prior month was revised up from 140,000 to 155,000. The data continued the theme of a robust US labor market, which is likely to support the US Dollar (USD) going forward.

Other data from Australia showed CoreLogic March house prices rose 0.6%, matching February’s monthly gain, while the Melbourne Institute inflation gauge eased to 3.8% YoY from 4.0% YoY.

Atlanta Federal Reserve Bank President Raphael Bostic told CNBC on Wednesday that he is forecasting the US central bank to lower the policy rate just one time this year.

Key quotes

"Economy is maintaining strong momentum it has had."

"If there is any weakening, it's at a very incremental level."

"Over longer arc, economy does need to slow to get to longer-run potential."

"I think you can still get growth and get inflation to continue to come down."

"But in that environment, inflation would come down much slower than expected."

"That's partly why I changed my forecast as fed would have to be more patient than expected."

"I am still forecasting one rate cut this year."

"We are going to have to watch and wait and see how things evolve."

"If economy evolves as I expect, I think appropriate to cut rates in Q4 this year."

"My outlook right now is inflation will drop incrementally through 2024."

"I think we won't be back to 2% inflation target until 2026."

"The road is going to be bumpy, over last several months inflation hasn't moved very much relative to 2023."

"I am not in a rush to disrupt economy's dynamic as long as inflation is moving toward our target rate."

"That said, if employment starts to degrade I would have to take that on board."

"My contacts are not giving me any concerns on employment though."

Market reaction

The US Dollar Index showed no immediate reaction to these comments and was last seen losing 0.04% on the day at 104.70.

- Gold price rises further to $2,290 as investors ignore higher bond yields.

- Fed policymakers see no urgency for rate cuts.

- Investors await the US ADP Employment Change, Services PMI, and Fed Powell’s speech.

Gold price (XAU/USD) falls after refreshing all-time highs near $2,290 in Wednesday’s European session on multiple tailwinds. The near-term demand for the precious metal is upbeat due to deepening geopolitical tensions in Eastern Europe and the Middle East regions. Escalating geopolitical tensions have increased demand for safe-haven assets, providing strength to bullions. This is offsetting the impact of higher bond yields and waning Federal Reserve (Fed) rate cut expectations for the June meeting.

10-year US Treasury yields rise to 4.37% as Fed policymakers see no need to hurry for rate cuts due to a strong economic outlook and tight labor market conditions. Cleveland Fed Bank President Loretta Mester, “I think the bigger risk would be to begin reducing the funds rate too early.” Fed’s pivot to rate cuts could tighten the labor market further, which will eventually increase wage growth and revamp inflation. Generally, higher bond yields dampen Gold’s appeal as they increase the opportunity cost of holding investment in the latter.

This week, the major event will be the United States Nonfarm Payrolls (NFP) data, which will be published on Friday. The labor market data will influence market expectations for Fed rate cuts in June.

Daily digest market movers: Gold price rises while US Dollar corrects

- Gold price keeps rising as geopolitical tensions strengthen the safe-haven bid and the US Dollar corrects from fresh four-month highs. Rising geopolitical tensions lead investors towards safe-haven assets such as Gold.

- In the eastern part of Europe, continuous drone attacks from Ukraine on Russian Oil refineries have resulted in a fresh escalation in the Moscow-Kyiv tensions. US President Joe Biden criticized the event of Ukraine targeting Russia’s Oil infrastructure as it could have drastic consequences for global Oil prices.

- In the Middle East, Iran vows to retaliate on the deaths of their high-ranking commanders in an attack at the Iranian embassy in Damascus by the Israeli army. This has deepened fears of Iran’s direct entry into Israel-Palestine tensions. Moreover, the killing of seven aid workers in Gaza on Tuesday after an Israeli attack has also raised tensions between Israel and some of its main allies in the West.

- Meanwhile, the US Dollar Index (DXY) corrects to 104.70 from a four-month high at 105.10 even though Federal Reserve policymakers seem to be leaning towards delaying interest-rate cuts until later than June.

- Cleveland Fed Bank President Loretta Mester and San Francisco Fed Bank President Mary Daly spoke on Tuesday. They both suggested that the Fed sees more risk in cutting interest rates too early. Fed Mester added: “With labor markets and economic growth both being very solid, we do not need to take that risk.” Both policymakers see three rate cuts as “reasonable” this year.

- In Wednesday’s session, investors will focus on Fed Chairman Jerome Powell’s speech and the economic data such as ADP Employment Change and the ISM Services PMI data for March. Powell is expected to provide cues about when the central bank will pivot to rate cuts.

- US private employers are anticipated to have hired 148K job-seekers, slightly higher from 140K payrolls in February. The ISM is expected to report that the Services PMI rose marginally to 52.7 from 52.6 in February.

Technical Analysis: Gold price prints fresh lifetime highs near $2,290

Gold price secures another milestone in Wednesday’s session. The precious metal prints a fresh all-time high near $2,290 after extending above Tuesday’s high of $2,275. However, the yellow metal struggles to continue its six-day winning spell as momentum oscillators have turned extremely overbought. The 14-period Relative Strength Index (RSI) tests 80.00.

The near-term demand is strong as the RSI has been oscillating in the bullish range of 60.00-80.00 for more than a month, making it a “buy on dips” contender.

All short-to-long term Exponential Moving Averages (EMAs) are sloping higher, suggesting strong near-term demand. On the downside, March 21 high at $2,223 will be a major support area for the Gold price bulls.

Gold FAQs

Gold has played a key role in human’s history as it has been widely used as a store of value and medium of exchange. Currently, apart from its shine and usage for jewelry, the precious metal is widely seen as a safe-haven asset, meaning that it is considered a good investment during turbulent times. Gold is also widely seen as a hedge against inflation and against depreciating currencies as it doesn’t rely on any specific issuer or government.

Central banks are the biggest Gold holders. In their aim to support their currencies in turbulent times, central banks tend to diversify their reserves and buy Gold to improve the perceived strength of the economy and the currency. High Gold reserves can be a source of trust for a country’s solvency. Central banks added 1,136 tonnes of Gold worth around $70 billion to their reserves in 2022, according to data from the World Gold Council. This is the highest yearly purchase since records began. Central banks from emerging economies such as China, India and Turkey are quickly increasing their Gold reserves.

Gold has an inverse correlation with the US Dollar and US Treasuries, which are both major reserve and safe-haven assets. When the Dollar depreciates, Gold tends to rise, enabling investors and central banks to diversify their assets in turbulent times. Gold is also inversely correlated with risk assets. A rally in the stock market tends to weaken Gold price, while sell-offs in riskier markets tend to favor the precious metal.

The price can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can quickly make Gold price escalate due to its safe-haven status. As a yield-less asset, Gold tends to rise with lower interest rates, while higher cost of money usually weighs down on the yellow metal. Still, most moves depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAU/USD). A strong Dollar tends to keep the price of Gold controlled, whereas a weaker Dollar is likely to push Gold prices up.

- Silver price drops slightly from fresh two-year of $26.30 ahead of key events.

- The near-term appeal is upbeat due to deepening geopolitical tensions.

- The US Dollar corrects ahead of Fed Powell speech.

Silver price (XAG/USD) faces nominal selling pressure after printing a fresh two-year high at $26.30 in the European session on Wednesday. The near-term demand for the white metal is upbeat due to deepening geopolitical tensions and a correction in the US Dollar.

Major agencies have accused Israel’s military for targeting charity staff who were advised to deliver necessities to civilians in Gaza. Non-yielding assets, such as Silver, expect higher investment in times of geopolitical uncertainty.

Meanwhile, a corrective move in the US Dollar has also boosted demand for silver. The US Dollar Index (DXY) drops to 104.73 despite upbeat United States Manufacturing PMI for March has improved the economic outlook.

In today’s session, investors will focus on the Federal Reserve (Fed) Chairman Jerome Powell’s speech, and the release of the ADP Employment Change and the Services PMI for March. Fed Powell’s speech could provide clues about when the central bank will start reducing interest rates. The ADP agency will report the number of jobseekers recruited by private employers.

Later this week, the release of the US Nonfarm Payrolls (NFP) data for March will be the major event. The official labor market data could influence market expectations for Fed rate cuts at the June meeting.

Silver technical analysis

Silver price prints a fresh two-year high at $25.30 after break above the crucial resistance of $26.22, plotted from 22 April 2022. The near-term demand is strong as the 20-week Exponential Moving Average (EMA) at $24.08 is sloping higher.

The 14-period Relative Strength Index (RSI) moves into the bullish range of 60.00-80.00, indicating that momentum towards the upside is strong.

- The New Zealand Dollar extends its downtrend in most pairs as broadly weak fundamentals exert pressure.

- RBNZ governor Orr says the bank is “laser-focused” on beating inflation.

- Technically, price could be about to correct higher within a persistent downtrend.

The New Zealand Dollar (NZD) edges lower in its most heavily-traded pairs on Wednesday following the trend of the previous weeks as bearish fundamentals, including an overall negative outlook for growth, continue to weigh.

Recent comments from the Reserve Bank of New Zealand (RBNZ) Governor Adrian Orr failed to give the Kiwi much support, despite the prospect of the RBNZ maintaining relatively high interest rates. Orr stressed the importance of battling too-high inflation in a speech on Tuesday.

Normally higher interest rates help a currency as they attract more foreign capital inflows but in the case of New Zealand this does not appear to be the case. It is possible this is because the high inflation is accompanied by weak growth after the economy fell into a technical recession in the fourth quarter of 2023.

New Zealand Dollar in downtrend as negative fundamentals weigh

The New Zealand Dollar is under pressure. The latest figures from Statistics New Zealand showed the New Zealand economy contracted by 0.1% in Q4 of 2023 following a 0.3% contraction in Q3.

At the same time, headline inflation remained relatively high at 4.7% during the same reporting period, although it showed a slowdown from the 5.6% recorded in Q3.

Normally weak growth would call for lower interest rates. However, the Reserve Bank of New Zealand (RBNZ) cannot cut interest rates because of too-high inflation. Elevated price growth is partly a result of structural issues such as a tight labor market, which in turn keeps wage inflation high.

In his speech on Tuesday, Governor Orr said the RBNZ remains “laser-focused on its job to control inflation.”

“We're now in a much happier space, where most central banks feel we're back on top of inflation, [but we are] not there yet,” he added.

Technical Analysis: New Zealand Dollar could undergo a correction

NZD/USD is falling in the final wave C of a bearish three-wave pattern, known as a Measured Move. This type of pattern is made up of three waves, usually labeled ABC.

The end of wave C can be calculated because it is often the same length or a 0.618 Fibonacci ratio of wave A. According to that method of forecasting, wave C still has a way to go before completing.

New Zealand Dollar versus US Dollar: Daily chart

Assuming the pattern unfolds as expected, NZD/USD is likely to fall to a target at roughly 0.5847, corresponding to the end of wave C. It has already met the conservative target measured using the 0.618 Fibonacci ratio of wave A, at 0.5988.

The bearish outlook is complicated by The Relative Strength Index (RSI) momentum indicator, however, which briefly dipped into oversold territory on Monday and then recovered on Tuesday. The entry and then exit from oversold levels is a buy signal. It recommends that short sellers should close their bets and open longs. It suggests the possibility of a correction evolving.

It is therefore quite possible NZD/USD could undergo some upside before eventually continuing lower in line with the dominant downtrend, towards the target generated by the Measured Move.

New Zealand Dollar FAQs

The New Zealand Dollar (NZD), also known as the Kiwi, is a well-known traded currency among investors. Its value is broadly determined by the health of the New Zealand economy and the country’s central bank policy. Still, there are some unique particularities that also can make NZD move. The performance of the Chinese economy tends to move the Kiwi because China is New Zealand’s biggest trading partner. Bad news for the Chinese economy likely means less New Zealand exports to the country, hitting the economy and thus its currency. Another factor moving NZD is dairy prices as the dairy industry is New Zealand’s main export. High dairy prices boost export income, contributing positively to the economy and thus to the NZD.