- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 02-08-2022

- Gold remains in bullish territory but it has lost some of its shine to the greenback.

- The US dollar is picking up both a safe haven and Fed monetary policy bid.

The gold price is pressured in Asia, falling 0.2% to a low of $1,756.19 from a high of $1,762.07 in the session so far. US bond yields had been waning in the wake of a less hawkish narrative surrounding the Federal Reserve which has been beneficial for the gold price.

However, US yields have rallied recently weighing on the gold price. The yield on the US 10-year note was last seen trading at 2.748 % after recovering from the lowest since early April and at the bottom of a daily broadening formation's daily range. Meanwhile, the US dollar rose off the lowest in nearly a month early on Tuesday, with the DXY index last seen up 0.10% to 106.445. Markets are trading cautiously around simmering US-China tensions over Taiwan as well as the ongoing concerns about a cooling global economy.

''Fed Chair Powell catalyzed a short covering rally by tying another "unusually large" 75bp hike to data, which places a high bar for another jumbo-sized hike given the slowing trend in data. At the same time, the prevailing risk off tone in the market tied to US-China relations has further supported the yellow metal via modest haven flows,'' analysts at TD Securities said.

''Nonetheless, for further significant short covering from CTA trend followers to take place, gold prices would need to close north of $1820/oz to spark a change in trend signals. However, on the other hand, we see risks that Fed speakers can push back against market expectations for an early Fed pivot.''

US/Sino relations a concern

The greenback is in favour due to the concerns that a visit by U.S. House of Representatives Speaker Nancy Pelosi to Taiwan would further harm relations between China and the United States. China has threatened repercussions if Pelosi visited the self-ruled island, which Beijing claims as its territory.

The US said on Monday it would not be intimidated by China. Consequently, US long-term Treasury yields dropped to a four-month low while the US dollar gained against a basket of currencies. Gold also picked up a bid, but that is being demolished with the sudden corrective spike in US yields.

''Nonetheless, for further significant short covering from CTA trend followers to take place, gold prices would need to close north of $1820/oz to spark a change in trend signals,'' analysts at TD Securities argued.

''However, on the other hand, we see risks that Fed speakers can push back against market expectations for an early Fed pivot. In this sense, gold markets are faced with a massive amount of complacent length held by prop traders, which still hold the title as the dominant speculative force in gold.''

''We have yet to see capitulation in gold, suggesting the pain trade is still to the downside and we expect the recent rally will ultimately fade, facing a wall of offers.''

Gold technical analysis

As per the prior analysis, Gold Price Forecast: XAU/USD bulls are back in play, it was explained that the price was running higher in a correction of the weekly M-formation:

The rebound in yields is a weight on the yellow metal. Meanwhile, the US dollar rose off the lowest in nearly a month early on Tuesday, with the DXY index last seen up 0.72% to 106.166.

US/Sino relations are the wild card for gold

To add insult to injury, the US dollar is attracting a safe haven bid on worries a visit by US House of Representatives Speaker Nancy Pelosi to Taiwan would further harm relations between China and the United States. China has threatened repercussions if Pelosi visited the self-ruled island, which Beijing claims as its territory.

The US said on Monday it would not be intimidated by China. Consequently, US long-term Treasury yields dropped to a four-month low while the US dollar gained against a basket of currencies. Gold also picked up a bid, but that is being demolished with the sudden corrective spike in US yields.

Gold technical analysis

As per the prior analysis, Gold Price Forecast: XAU/USD bulls are back in play, it was explained that the price was running higher in a correction of the weekly M-formation:

The grey area was a price imbalance that has now been mitigated by a 50% mean reversion:

There are prospects for further upside with the 68.2% Fibonacci meeting prior structure around $1,800.

- USD/CAD takes the bids to refresh intraday high during three-day uptrend.

- Bullish MACD signals, successful break of two-week-old bearish channel’s resistance favors buyers.

- 200-SMA acts as an additional upside filter while sellers have a bumpy road to return.

USD/CAD extends the previous upside momentum while ejecting the short-term bearish chart pattern during Wednesday’s Asian session. In doing so, the Loonie pair refreshes intraday high around 1.2890 during the three-day uptrend.

In addition to the clear upside break of the two-week-old descending trend channel, the bullish MACD signals also keep USD/CAD buyers hopeful.

However, the 200-SMA hurdle surrounding 1.2930 probes the upside momentum before highlighting the 1.3000 threshold for the bulls.

In a case where the USD/CAD prices remain firm past 1.3000, the previous monthly peak near 1.3225 will be in focus.

Alternatively, sellers need to wait for a sustained pullback below the resistance-turned-support line, near 1.2875 at the latest.

It’s worth noting, however, that the USD/CAD weakness past 1.2875 appears bumpy as multiple support levels around 1.2800 could challenge the bears before the stated channel’s lower line, close to 1.2750 at the latest.

During the quote’s weakness past 1.2750, the odds of witnessing a south-run towards June’s low near 1.2515 can’t be ruled out.

USD/CAD: Four-hour chart

Trend: Further upside expected

- EUR/USD takes offers to refresh weekly low, extends the previous day’s pullback from monthly top.

- Fed policymakers appear hawkish, Bullard reiterated central bank’s commitment to inflation target.

- China resents US House Speaker Nancy Pelosi’s Taiwan visit.

- EU/US PMIs for July, Eurozone Retail Sales and US Factory Orders will decorate the calendar.

EUR/USD holds lower ground near 1.0150, refreshes weekly low, as bears cheer the market’s risk-off mood, as well as hawkish comments from the Fed policymakers during Wednesday’s Asian session. That said, the major currency pair dropped the most in more than a week, after taking a U-turn from the monthly high, the previous day.

Geopolitical tensions between the US and China, recently over Taiwan, exert more downside pressure on the market sentiment, as well as on the EUR/USD prices, especially at a time when the global economy is fragile. Also, the Federal Reserve (Fed) policymakers aren’t following Chairman Jerome Powell’s tunes and show no major signs of retreat from the rate-hike trajectory.

China showed irritation over US House Speaker Nancy Pelosi’s visit to Taiwan and raised fears that the tussles among the world’s top-two economies will have more negative consequences for the world amid recession fears. “US House of Representatives Speaker Nancy Pelosi arrived in Taiwan late on Tuesday on a trip she said shows an unwavering American commitment to the Chinese-claimed self-ruled island, but China condemned the highest-level U.S. visit in 25 years as a threat to peace and stability in the Taiwan Strait,” said Reuters.

Other than the Taiwan issue, talks of likely US restrictions on the chip-making machinery’s exports to China also magnified the Sino-American tussles. It’s worth noting that Beijing’s policymakers also showed a lack of confidence in this year’s Gross Domestic Product (GDP) and weighed on the EUR/USD prices, mainly due to the US dollar’s safe-haven demand.

Elsewhere, St. Louis Federal Reserve President James Bullard’s support for the hawkish Fed moves appeared to recently weigh on the EUR/USD prices. “Federal Reserve and the European Central Bank may both be able to execute a "relatively soft landing" that avoids a harsh recession for their respective economies as they raise interest rates to rein in inflation,” the policymaker said.

On Tuesday, San Francisco Fed President Mary Daly said that she is looking for incoming data to decide if they can downshift the rate hikes or continues at the current pace, as reported by Reuters. However, Chicago Fed President Charles Evans showed support for a 50 basis points (bps) rate hike for the September policy meeting if inflation does not improve, as reported by Reuters. Furthermore, Cleveland Fed President Loretta Mester, on the other hand, said she does not think the country is suffering a recession, adding that the labor market is in great shape. On inflation, however, she noted that it has not decreased "at all."

Amid these plays, Wall Street closed in the red and the US Treasury yields bounced off a four-month low.

Moving on, July month activity numbers from the Eurozone and the US will join German trade data and the Retail Sales from the bloc to entertain EUR/USD traders ahead of the US session. Following that, the US Factory Orders and ISM Services PMI will be crucial to watch for fresh directions.

Technical Analysis

EUR/USD confirms a rising wedge bearish chart pattern on breaking a three-week-old support line, now resistance around 1.0180, which in turn signals the pair’s further declines towards refreshing the yearly low surrounding 0.9950.

- Safe-haven flows bolstered the greenback, a tailwind for the USD/JPY.

- US House Rep. Pelosi’s trip to Taiwan escalates China-US tensions.

- USD/JPY traders should be aware of Japan and US Services and Composite PMIs.

The USD/JPY begins Wednesday’s Asian session on the right foot, amidst a risk-off impulse spurred by geopolitical tensions between China and the US, triggered by the trip of US House Speaker Pelosi to Taiwan, alongside a hawkish push by Fed policymakers.

Therefore, the USD/JPY is trading at 133.48, after hitting a weekly low on August 2 at 130.39, with buyers stepping in around the 100-day EMA at 130.37, lifting the major to current price levels.

USD/JPY got bolstered by safe-haven flows

During the US session, Fed speakers pushed back against a so-called “dovish” tilt, according to the market’s reaction to the US central bank’s 75 bps rate hike. Nevertheless, the San Francisco Fed President, Mary Daly, said that work in inflation is nowhere near almost done, and there is still a long way to go. In the same tone, Cleveland’s Fed President Mary Daly said that she hadn’t seen anything suggesting that inflation is leveling off and foresees prices would not come down quickly.

In the meantime, Chicago’s Fed President Charles Evans said a 50 bps is reasonable in September, but he didn’t discount a 75 bps if inflation remains stubbornly sticky.

The US bond market reacted to Fed policymakers and sent US 2-year bond yields above the 3% threshold. In comparison, the US 10-year benchmark note rate stayed around 2.74%, further deepening the yield curve inversion as traders discount a US recession.

Late in the North American session, US President Joe Biden signed the US chip production bill, aimed to compete with China.

What to watch

The Japanese economic docket will feature the Jibun Bank Services and Composite PMIs for July on its final readings. Expectations lie at 51.2 and 50.6, respectively.

The US calendar will feature July’s ISM Non-Manufacturing Business Activity is expected to decelerate to 52.5, alongside Factory Orders and Fed speakers, led by Philadelphia’s Fed Patrick Harker.

USD/JPY Key Technical Levels

- AUD/JPY is attempting to extend its gains above 92.00 on higher-than-expected Australian PMI data.

- Aussie’s S&P Global Services PMI has improved to 50.9 vs. 50.4 the prior release.

- The rate hike announcement by the RBA has escalated RBA-BOJ policy divergence.

The AUD/JPY pair is attempting a rebound after a corrective move below 92.00 in the early Tokyo session. The risk barometer is upbeat on a broader note, therefore, the upside will remain favored. The asset is expected to catch bids as the IHS Markit has reported higher-than-expected S&P Global Services and Composite PMI data.

The Services PMI has landed at 50.9, higher than the estimates and the prior release of 50.4. While the Composite PMI has improved to 51.1 from the former figure of 50.6. In times, when the odds of a recession and demand worries in China are accelerating, an improvement in Services PMI numbers will support the aussie bulls.

On Tuesday, the asset rebounded firmly after the Reserve Bank of Australia (RBA) announced a rate hike by 50 basis points (bps). RBA Governor Philip Lowe accelerated the Official Cash Rate (OCR) to 1.85% as their prime responsibility is to bring price stability to the economy. A third consecutive 50 bps rate hike by the RBA has escalated RBA-Bank of Japan (BOJ) policy divergence.

Meanwhile, the yen bulls are likely to return to the bears’ pool as the BOJ will continue with its ultra-loose policy stance on interest rates. The Japanese economy is struggling to push the inflation rate higher without the support of volatile oil and food product prices. To keep the inflation rate above 2%, a higher move in the Labor Cost Index is critical.

- NZD/JPY dropped 45 pips on New Zealand’s downbeat employment numbers.

- NZ Q2 Unemployment Rate, Employment Change marked softer than expected and prior releases.

- Ascending support line from late January defends buyers, 81.25 is a tough nut to crack for bears.

NZD/JPY holds lower ground near a 10-week low as sellers attack 82.80 support during the initial Asian session on Wednesday. That said, the cross-currency pair’s latest weakness could be linked to the downbeat New Zealand (NZ) employment data. However, an upward sloping support line from January 28, 2022 seems to challenge the pair sellers of late.

New Zealand employment numbers for the second quarter (Q2) raised concerns over the Reserve Bank of New Zealand’s (RBNZ) hawkish mood and drowned the New Zealand Dollar (NZD) on release. That said, NZ Unemployment Rate surprisingly grew to 3.3% versus 3.1% expected and 3.2% prior while the Employment Change dropped to 0.0% versus 0.4% market forecasts and 0.1% previous readings.

It should be noted that the bearish MACD signals and the pair’s sustained downside break of the 50-DMA keep sellers hopeful of breaking the nearby support line, at 82.80 by the press time.

In a case where the NZD/JPY prices drop below 82.80, a convergence of the 200-DMA and 50% Fibonacci retracement of January-April upside, near 81.25 will be a crucial support to watch for forecasting the next moves of the pair.

Alternatively, recovery remains elusive until the quote stays below the 100-DMA level of 84.33.

Following that, a downward sloping resistance line from April 20, near 86.15, will be important for the NZD/JPY bulls to watch before dominating further.

NZD/JPY: Daily chart

Trend: Further weakness expected

Federal Reserve and the European Central Bank may both be able to execute a "relatively soft landing" that avoids a harsh recession for their respective economies as they raise interest rates to rein in inflation, St. Louis Federal Reserve President James Bullard said on Tuesday.

"Since modern central banks have more credibility than their counterparts in the 1970s, it appears that both the Fed and the ECB may be able to disinflate in an orderly manner and achieve a relatively soft landing," Bullard said in slides prepared for the presentation.

- The Federal Reserve is committed to inflation target.

- Soft landing feasible if regime shift executed well.

US dollar catches a safe haven bid

Meanwhile, US stocks struggled for gains and the dollar and gold rallied on Tuesday in a flight for safety, Markets are trading cautiously around simmering US-China tensions over Taiwan as well as the ongoing concerns about a cooling global economy. DXY is 0.63% higher at 106.07 the high for the day so far.

- AUD/NZD takes the bids to extend the previous day’s rebound from one-week low.

- New Zealand’s Unemployment Rate, Employment Change surprised markets.

- Risk-aversion wave tames the pair’s upside momentum amid sluggish day-start.

- US-China headlines, China’s Caixin Services PMI will be important for fresh impulse.

AUD/NZD justifies downbeat New Zealand (NZ) employment data while picking up bids to refresh daily tops near 1.1110 during early Wednesday morning in Asia. Even so, risk-off mood and a lack of major trading participation appeared to have tamed the cross-currency pair’s latest moves.

New Zealand employment numbers for the second quarter (Q2) raised concerns over the Reserve Bank of New Zealand’s (RBNZ) hawkish mood and drowned the New Zealand Dollar (NZD) on release. That said, NZ Unemployment Rate surprisingly grew to 3.3% versus 3.1% expected and 3.2% prior while the Employment Change dropped to 0.0% versus 0.4% market forecasts and 0.1% previous readings.

Elsewhere, the escalated geopolitical tension between the US and China, as well as hawkish comments from the Fed policymakers, also weighed on the AUD/NZD prices. It’s worth noting, however, that the the Reserve Bank of Australia’s (RBA) failure to lure the bulls, despite the fourth rate hike, challenge the pair buyers.

US House Speaker Nancy Pelosi’s visit to Taiwan, despite China’s multiple warnings, raised fears that the tussles among the world’s top-two economies will have more negative consequences for the world amid recession fears. “US House of Representatives Speaker Nancy Pelosi arrived in Taiwan late on Tuesday on a trip she said shows an unwavering American commitment to the Chinese-claimed self-ruled island, but China condemned the highest-level U.S. visit in 25 years as a threat to peace and stability in the Taiwan Strait,” said Reuters.

Other than Taiwan, talks of likely US restrictions on the chip-making machinery’s exports to China also magnified the Sino-American tussles. It’s worth noting that Beijing’s policymakers also showed a lack of confidence in this year’s Gross Domestic Product (GDP) and weighed on the AUD/USD prices, due to the strong China-Australia trade ties.

The RBA matched the market’s expectations of announcing 50 basis points (bps) rate hike, the fourth in 2022, while inflating the benchmark rate to 1.85%. However, the RBA Statement that says, “The central bank is not on the pre-set path in normalizing rates,” appeared to have lured the AUD/NZD bears the previous day.

Technical analysis

A daily closing below an ascending trend line from November 2021, around 1.1040 by the press time, becomes necessary for the AUD/NZD bears to take entry. Until then, the quote is expected to mark another attempt in challenging the 1.1200 threshold.

- NZD/USD has slipped swiftly to 0.6225 as Stats NZ has reported downbeat labor market data.

- The NZ jobless rate has increased to 3.3% while Employment Change has landed at 0%.

- A lower consensus for the US ISM Services PMI could fade the DXY’s rally.

The NZD/USD pair has witnessed a steep fall as Stats NZ has reported vulnerable NZ employment data. The Unemployment Rate has increased to 3.3% from the estimates of 3.1% and the prior release of 3.2%. Also, the Employment Change for the second quarter has landed at 0%, significantly lower than the estimates of 0.4% and the prior print of 0.1%.

Kiwi economy’s failure in creating employment opportunities is going to create more troubles for the Reserve Bank of New Zealand (RBNZ). This will force RBNZ Governor Adrian Orr to go light on policy tightening due to the unavailability of fundamental support from the labor market. However, the Labor Cost Index has improved significantly to 1.3%, much higher than the expectations of 1.1% and the former print of 0.7% on a quarterly basis.

Meanwhile, the US dollar index (DXY) has recovered some of its losses after a juggernaut rebound on Tuesday. The asset picked bids after printing a fresh three-week low at 105.05 as investors underpinned the risk-aversion theme on escalating US-China tensions over Taiwan. US House Speaker Nancy Pelosi supported the Taiwanese local government despite the death threats from China on her personal visit to Taiwan.

Going forward, the US Institute of Supply Management (ISM) will release the Services PMI data. As per the market consensus, the Services PMI will land at 53.5, significantly lower than the prior release of 55.3. Apart from that, the US ISM Services New Orders Index data holds key importance as US big tech companies have lowered their guidance for the rest of the year. Also, they have ditched their recruitment process.

The New Zealand Unemployment Rate released by the Statistics New Zealand has been released as follows:

- New Zealand Q2 s/adj Unemployment rate 3.3% (Reuters poll 3.1%).

- NZQ2 s/adj Employment growth 0.0% (Reuters poll +0.4%).

- NZ Q2 Participation Rate 70.8% (Reuters poll 71.0%).

- NZ Q2 lci private sector wages (ex-o'time) +1.3% on pvs qtr (Reuters poll +1.1%).

''Finding workers remains the #1 constraint facing Kiwi businesses and this situation is expected to worsen as Kiwis are attracted across the Tasman'', analysts at ANZ Bank said.

''Australia’s labour market is experiencing similar challenges to the New Zealand market but the higher wages on offer in certain sectors are expected to attract New Zealanders into some of these positions.''

Meanwhile, NZD/USD has been under pressure. The greenback has picked up a safe haven bid relating to tensions surrounding Taiwan between the US and China. The miss in the Unemployment Rate is weighing on the bird, down 0.23% on the day so far.

About NZ Employment

Statistics New Zealand releases employment data on a quarterly basis. The statistics shed a light on New Zealand’s labor market, including unemployment and employment rates, demand for labor and changes in wages and salaries. These employment indicators tend to have an impact on the country’s inflation and Reserve Bank of New Zealand’s (RBNZ) interest rate decision, eventually affecting the NZD. A better-than-expected print could turn out to be NZD bullish.

- AUD/USD holds lower ground as bears take a breather following the heavy downside move.

- Sino-American jitters over Taiwan join hawkish comments from Fed policymakers to weigh on the quote.

- RBA’s 0.50% rate hike couldn’t please bulls as shift in language in Rate Statement gained bear’s attention.

- China’s Caixin Services PMI, US ISM Services PMI may entertain traders but risk catalysts are more important.

AUD/USD remains pressured around 0.6920, after posting the biggest daily slump in a month, as traders seek fresh clues during Wednesday’s initial Asian session.

That said, the Aussie pair’s latest fall could be linked to the escalated geopolitical tension between the US and China, as well as hawkish comments from the Fed policymakers. Further, the Reserve Bank of Australia’s (RBA) failure to lure the bulls, despite the fourth rate hike, also contributed to the AUD/USD pair’s weakness.

US House Speaker Nancy Pelosi’s visit to Taiwan, despite China’s multiple warnings, raised fears that the tussles among the world’s top-two economies will have more negative consequences for the world amid recession fears. “US House of Representatives Speaker Nancy Pelosi arrived in Taiwan late on Tuesday on a trip she said shows an unwavering American commitment to the Chinese-claimed self-ruled island, but China condemned the highest-level U.S. visit in 25 years as a threat to peace and stability in the Taiwan Strait,” said Reuters.

Other than Taiwan, talks of likely US restrictions on the chip-making machinery’s exports to China also magnified the Sino-American tussles. It’s worth noting that Beijing’s policymakers also showed a lack of confidence in this year’s Gross Domestic Product (GDP) and weighed on the AUD/USD prices, due to the strong China-Australia trade ties.

At home, the RBA matched the market’s expectations of announcing 50 basis points (bps) rate hike, the fourth in 2022, while inflating the benchmark rate to 1.85%. However, the RBA Statement that says, “The central bank is not on the pre-set path in normalizing rates,” appeared to have lured the AUD/USD bears.

Elsewhere, San Francisco Fed President Mary Daly said on Tuesday that she is looking for incoming data to decide if they can downshift the rate hikes or continues at the current pace, as reported by Reuters. However, Chicago Fed President Charles Evans showed support for a 50 basis points (bps) rate hike for the September policy meeting if inflation does not improve, as reported by Reuters. Furthermore, Cleveland Fed President Loretta Mester, on the other hand, said she does not think the country is suffering a recession, adding that the labor market is in great shape. On inflation, however, she noted that it has not decreased "at all."

In addition to the aforementioned catalysts, the risk-off mood and firmer US Treasury yields also underpinned the US Dollar Index's rebound from the monthly low and drowned the AUD/USD prices. To portray the mood, the Wall Street benchmarks posted losses while the US 10-year Treasury yields rose to 2.75% at the latest.

Moving on, AUD/USD traders should pay attention to China’s Caixin Services PMI and US ISM Services PMI for July for fresh impulse. However, major attention will be given to the risk catalysts, mainly concerning China and recession, for fresh impulse.

Technical analysis

A successful downside break of the three-week-old ascending trend line support, now resistance around 0.6975, directs AUD/USD prices towards the 21-DMA surrounding 0.6880 by the press time.

- The EUR/JPY rallied more than 150 pips and gained 0.25% on Tuesday.

- A hammer in the EUR/JPY daily chart could open the door for further gains.

- The cross faces solid resistance around 136.00-30 in the near term.

The EUR/JPY plunges to the 200-day EMA at 133.71, forms a hammer, and rallies above the August 1 daily close at 134.99, finishing the trading session at 135.37, as buyers regained control in a volatile session. As the Asian session begins, the EUR/JPY is trading at 135.20, almost flat.

EUR/JPY Price Analysis: Technical outlook

The EUR/JPY daily chart illustrates a hammer formed in the daily chart, right on the 200-day EMA. Nevertheless, the cross-currency closing below half of the August 1 price action exposes the pair to selling pressure. With the RSI sitting at negative territory, below the 7-day RSI’s SMA, and far from reaching the mid-line, it could keep the pair subject to market sentiment. If the EUR/JPY tumbles below 135.00, a re-test of the 200-day EMA could be possible due to the volatile price action in the last few days. On the other hand, the EUR/JPY upward moves could be capped at around 136.00.

EUR/JPY 1-hour chart

In the near term, the EUR/JPY bias is neutral to downwards, though the cross-currency pair is trading above the 20 and 50-hour EMAs. However, the pair struggled to crack 135.50, with significant resistance above it, at the confluence of the R1 daily pivot and the 100-hour EMA at 136.06. Any rallies could be capped at the previously mentioned area, alongside the weekly high at 136.34. On the flip side, the EUR/JPY first support would be 135.00-05 area, followed by the daily pivot at 134.72.

EUR/JPY Key Technical Levels

- AUD/NZD is juggling in a 17-pips range as investors await NZ labor market data.

- The NZ employment data is likely to remain upbeat amid decent employment generation in July.

- The RBA announced a third consecutive 50 bps rate hike to contain price pressures.

The AUD/NZD pair is displaying back and forth moves in a narrow range of 1.1051-1.1068 in the early Tokyo session. The asset has turned sideways as investors are awaiting the release of the employment data by Stats NZ.

According to the preliminary estimates, the employment data is expected to remain upbeat as the Employment Change will improve significantly to 0.4% from the prior print of 0.1%. Also, the Unemployment Rate is likely to trim to 3.1% vs. 3.2% in the previous figure.

One thing is worth considering that the Labor Cost Index is expecting an improvement to 1.1% from 0.7% on a quarterly basis. The inflation rate is sky-rocketing in the kiwi zone and households need higher paychecks to offset the higher payouts to address personal expenditure. This will strengthen the Reserve Bank of New Zealand (RBNZ) to sound hawkish further unhesitatingly.

On the Aussie front, the antipodean is still digesting the third consecutive 50 basis points (bps) by the Reserve Bank of Australia (RBA). RBA Governor Philip Lowe has hiked the Official Cash Rate (OCR) to 1.85%. To contain price pressures in the Australian economy, the RBA is needed to tighten its policy continuously. Investors should be aware of the fact that the inflation rate has climbed to 6.1% in the second quarter of CY2022 vs. the prior release of 5.1%.

New Zealand quarterly employment report overview

Early Wednesday in Asia, at 22:45 GMT Tuesday the world over, the global market sees the second quarter (Q2) 2022 employment data from Statistics New Zealand.

With the Reserve Bank of Australia’s (RBA) consecutive fourth rate lift, as well as robust inflation and hopes of tighter monetary policy from other major central banks, today’s jobs report becomes crucial for the NZD/USD traders, mainly due to the wage prices index data.

Market consensus suggests a slight reduction in the headline Unemployment Rate to 3.1% from 3.2% while the Employment Change figure is likely to increase to 0.4% from 0.1%. Further, the Participation Rate may also improve to 71.0% from 70.9% but the Labour Cost Index could rise to 3.3% QoQ from 3.1% prior.

Ahead of the data, ANZ said,

We anticipate the unemployment rate will hit a fresh record low of 2.8% in Q2 (down from 3.2% in Q1). Finding workers remains the #1 constraint facing Kiwi businesses and this situation is expected to worsen as Kiwis are attracted across the Tasman. Australia’s labor market is experiencing similar challenges to the New Zealand market but the higher wages on offer in certain sectors is expected to attract New Zealanders into some of these positions.

How could it affect the NZD/USD?

NZD/USD edges lower around 0.6250, extending the previous day’s downbeat performance led by the hawkish Fedspeak and the US-China tussles.

That said, the Kiwi pair is likely to mark a kneejerk positive reaction in case the New Zealand job numbers arrive strong, which more is likely considering the tight labor market in Auckland and higher demand from Australia. However, the NZD/USD prices may not remain firmer for long unless the data is extremely positive, mainly due to the current risk-off mood. Furthermore, the recent shift in the RBA’s language also raises doubts about the hawkish mood of the Reserve Bank of New Zealand (RBNZ) and could please sellers in case the data disappoints.

Technically, a clear downside break of the three-week-old ascending trend line, at 0.6270 by the press time, directs NZD/USD prices towards the 21-DMA support level near 0.6210 at the latest.

Key Notes

NZD/USD under pressure as US dollar resurges

New Zealand: Unemployment rate seen higher at 3.3% in Q2 2022 – TDS

About New Zealand unemployment rate and employment change

The quarterly report on New Zealand's unemployment rate and employment change is being released by Statistics New Zealand.

The unemployment rate is the number of unemployed workers divided by the total civilian labor force. If the rate is up, it indicates a lack of expansion within the New Zealand labor market. As a result, a rise leads to weaken the New Zealand economy. A decrease of the figure is seen as positive (or bullish) for the NZD, while an increase is seen as negative (or bearish).

On the other hand, employment change is a measure of the change in the number of employed people in New Zealand. Generally speaking, a rise in this indicator has positive implications for consumer spending which stimulates economic growth. A high reading is seen as positive (or bullish) for the NZ dollar, while a low reading is seen as negative (or bearish).

- The GBP/JPY rallied after hitting a three-month fresh low at 159.44.

- A risk-off impulse exacerbated GBP/JPY fall towards the double-top target.

- The GBP/JPY is neutral biased, but a break above 162.00 puts the 163.00 targets in place; otherwise, a drop to 161.00 is on the cards.

The GBP/JPY rallied after touching the double-top target and the daily low at around 159.44, then hitting a daily high at 162.00 before retracing to current price levels. At the time of writing, the GBP/JPY is trading at 161.99 as the Asian session begins.

Investor’s sentiment shifted sour as tensions arose between China and the US. The visit of US House Rep. Nancy Pelosi was promptly condemned by China, saying it “has a severe impact on the political foundation of China-US relations, and seriously infringes upon China’s sovereignty and territorial integrity.” Besides that, traders reconsidered the so-called Fed “dovish” pivot, with policymakers like Daly, Evans, and Mester reiterating Fed’s commitment to tackle inflation.

Also read: GBP/JPY Price Analysis: Double-top about to reach its target

GBP/JPY Price Analysis: Technical outlook

The GBP/JPY daily chart illustrates the pair as neutral biased once the double-top target was achieved when the pair hit 159.50. After that, the cross-currency rallied sharply, 250 pips, towards the daily highs, but short of August 1, open at 162.27, forming a hammer with bullish implications.

Therefore, the GBP/JPY first resistance would be 162.00. Break above will expose the August 1 high at 162.49, followed by the 100-day EMA at 162.73, and then the 163.00 mark.

GBP/JPY Key Technical Levels

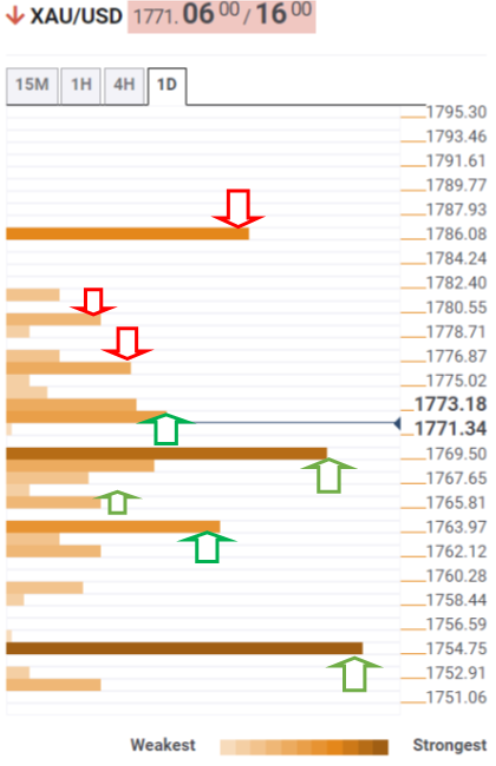

- Gold price has slipped swiftly to near $1,760.00 as market mood sours on US-China tensions.

- Fed policymakers have renewed inflation fears but have trimmed the odds of a recession.

- The US ISM Services PMI is likely to remain downbeat ahead.

Gold price (XAU/USD) has shifted into a correction phase after a juggernaut rally from yearly lows near $1,680.00 on Tuesday. The precious metal has plunged to near $1,760.00 as investors preferred the US dollar index (DXY) a better investment option after the market sentiment turned sour. The visit of US House Speaker Nancy Pelosi to Taiwan to support their local government despite the threat attempts of China spurred the risk-aversion theme.

The underpinned risk-aversion theme sent the risk-perceived currencies into the negative trajectory and improved the DXY’s appeal. The DXY displayed a sheer responsive buying action and reclaimed the crucial hurdle of 106.00. The asset extended its recovery and printed a high of 106.35 after commentary from Federal Reserve (Fed) policymakers.

Chicago Fed President Charles Evans dictated that the inflationary pressures are broadening out and favored a 50 basis point (bps) interest rate hike in September. While Cleveland Fed President Loretta Mester trimmed recession fears citing that the labor market is rock solid, however, price pressures have not decreased at all.

In today’s session, the entire focus will remain on the US ISM Services PMI data. A preliminary estimate for the economic data is 53.5, significantly lower than the prior release of 55.3. The US ISM Services New Orders Index data will be worth watching as US techs have lowered their guidance for the rest of the year.

Gold technical analysis

A rising channel formation by the gold prices on a four-hour scale advocates the continuation of an upside move on a broader bias. The upper portion of the above-mentioned chart pattern is placed from July 22 high at $1,739.37 while the lower portion is plotted from July 21 low at $1,681.87. The corrective wave in the chart pattern is likely to drag the gold prices below the 200-period Exponential Moving Average (EMA) at $1,748.57.

The precious metal has slipped below the crucial 50-EMA at $1,764.24, which signals more weakness ahead.

Also, the Relative Strength Index (RSI) (14) has slipped into the 40.00-60.00 range, which indicates that gold prices are not carrying bullish momentum for a while.

Gold four-hour chart

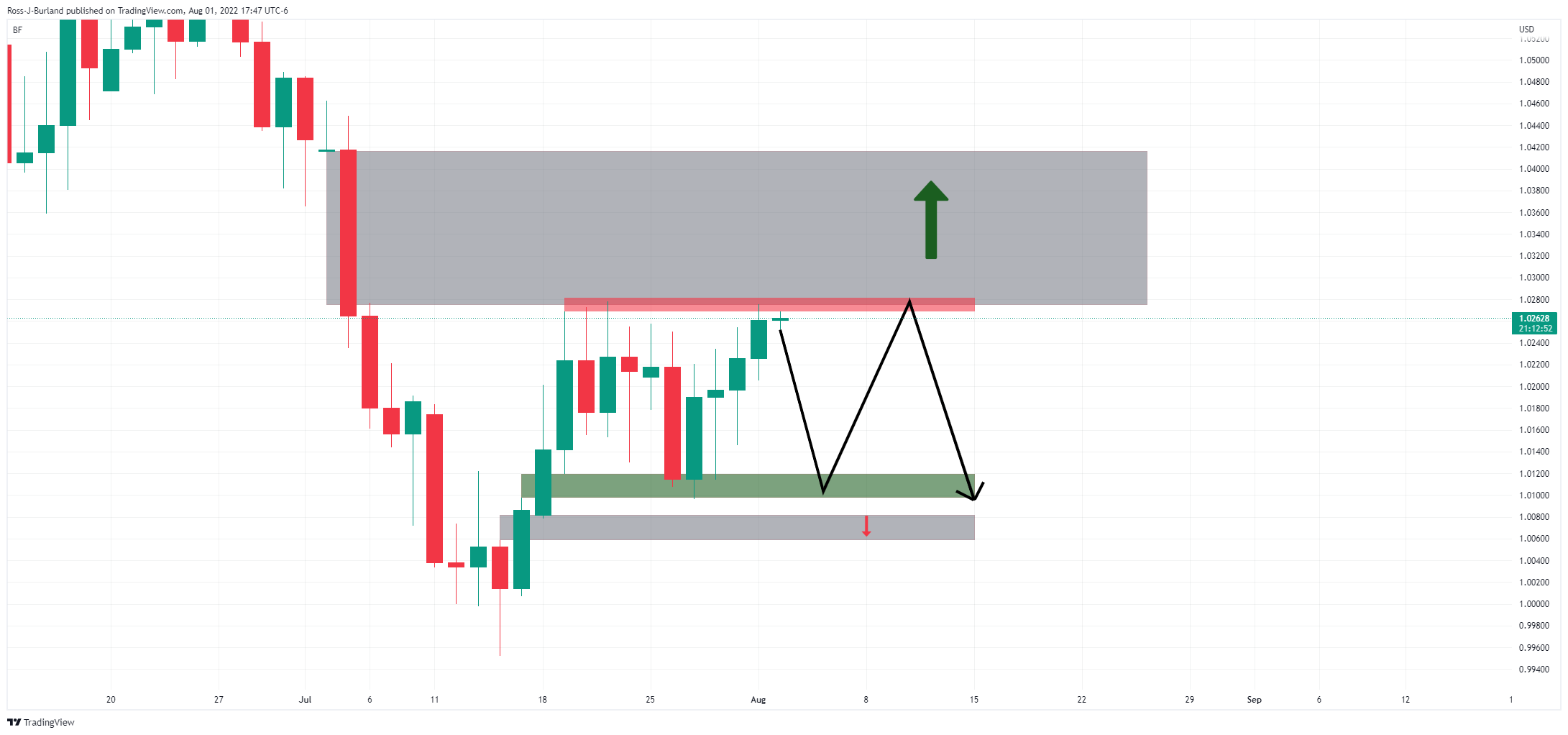

- EUR/USD is carving out an inverse H&S.

- The bulls are eyeing the price imbalance on the daily chart to the upside.

EUR/USD has been offered while the dollar rallied as risk appetite was dampened by economic uncertainties and escalating US-China tensions. However, from a technical perspective, there could be some gas left in the bulls yet and the following illustrates a bullish scenario for the days ahead.

EUR/USD daily chart

The euro is under pressure but could be on the verge of carving out an inverse head and shoulders. This is a bullish pattern that could lead to the price running higher into the area of price imbalance between 1.0293 and 1.0416.

- NZD/USD is under pressure as the US dollar bounces back.

- Unemployment data will be an important feature on the NZ calendar.

NZD/USD is down o the day by some 1.17% with the price falling from a high of 0.6343 to a low of 0.6253. The greenback has picked up a safe haven bid relating to tensions surrounding Taiwan between the US and China.

''The Kiwi is lower this morning, having been sideswiped by a resurgence in the USD amid a stiff rise in US interest rates that was, in turn, fuelled by a plethora of hawkish comments by Fed officials, the essence of which was: inflation is still too high, it may not have turned, and the Fed’s job is far from done,'' analysts at ANZ Bank said.

''Whether that vibe is enough to bring about another more sustained bout of USD strength remains to be seen, but markets have certainly been very “glass half full” on both the US economy and the inflation/Fed hikes threat, and that wiped a few percent off the USD DXY last month.''

Looking ahead of the day, domestically, New Zealand's labour market will be important. The analysts at ANZ bank, who are calling for a 2.8% unemployment rate, say the ''data can be volatile, but if they beat expectations, that could see the NZD beat peers amid USD strength.''

- Silver price drops on high yields as Fed policymakers push back against a dovish tilt.

- US House Speaker Pelosi’s visit to Taiwan turned sentiment sour.

- Silver Price Forecast (XAGUSD): Despite rallying $2 in the last five days, the bias is negative.

Silver price slides due to US Treasury yields rising as Fed officials pushed back markets’ expectations of a US central bank “dovish” pivot, which traders misread. At the same time, geopolitical jitters fueled flows towards safe-haven assets, which boosted the greenback. At the time of writing, XAGUSD is trading at $19.96.

Risk aversion originated from the visit of US House Speaker Nancy Pelosi, which rattled the financial markets. US equities are down, and the greenback is firm, as shown by the US Dollar Index at 106.183, up almost 0.80%. Meanwhile, US Treasury yields soared on Fed speaking, 16 basis points, yielding 2.743%, a headwind for precious metals prices.

XAGUSD drops on high yields and Fed speaking

Unleashed Fed officials have begun to cross wires led by San Francisco Fed President Mary Daly, saying that the Fed is “nowhere near” done in fighting inflation and added that “it would be premature to unwind all of that (Fed tightening) and say the job is done.”

Late in the morning, the Chicago Fed President Charles Evans said that going 50 bps “is a reasonable assessment, but 75 bps could also be okay.”

Loretta Mester, Cleveland’s Fed President, said that she has not seen inflation cool at all and is committed to bringing it under control. She added that she wants to see compelling evidence that inflation is moving down on a sustainable basis.

Data wise, US labor market data, namely JOLTs Job Openings for June, rose to 10.7 million, less than 11 million estimated by the streets. That suggests the labor market is easing amid growing economic pressures.

Silver Price Forecast (XAGUSD): Technical outlook

The XAGUSD illustrates the white metal as neutral-to-downward biased, as the $2 rally losses steam at $20.47, the 50-day EMA, further reinforced by the RSI, which turned down and aims towards the 50-midline. However, XAGUSD bears need a daily close below the $20.00 figure to extend the fall further, leaving silver exposed to selling pressure. If that scenario plays out, silver’s next support would be the 20-day EMA at $19.11. Otherwise, XAGUSD bulls could lick its wound before challenging the 50-day EMA for another time.

- GBP/USD is under pressure at the start of the week.

- The US dollar picks up a safe haven bid over US/Sino tensions.

GBP/USD is down on the day falling some 0.6% from a high of 1.2279 meeting a low of 1.2166 the low. The US dollar has been stronger against its major trading partners early Tuesday, apart from a further decline against the yen, in the midst of renewed Sino-US tensions over Taiwan.

Federal Reserve officials are also emerging from the pre-Fed meeting blackout period with traders on the lookout for clues about the Fed's plans after a second straight 75 basis point rate increase last week. Evans, Mester, and Bullard spoke today. Harker, Barkin, and Kashkari will speak tomorrow.

''Short-term we are focused on upcoming Fed speak and payrolls on Friday,'' analysts at TD Securities said. ''We see hawkish risks to the both which could help stabilize the USD. Tensions between US and China are likely to intensify given Pelosi's intended visit to Taiwan and the risk of an accident are likely underappreciated by markets, so we would tread cautiously on higher beta and equity-linked currencies.''

Meanwhile, the greenback has attracted a safe haven bid on worries a visit by US House of Representatives Speaker Nancy Pelosi to Taiwan would further harm relations between China and the United States. China has threatened repercussions if Pelosi visited the self-ruled island, which Beijing claims as its territory. The US said on Monday it would not be intimidated by China. Consequently, US long-term Treasury yields dropped to a four-month low while the US dollar gained against a basket of currencies.

Domestically, doused in political and economic woes, the pound has been one of the laggards this year despite the Bank of England being out of the traps with policy tightening relatively early.

Additionally, net short GBP positions edged lower for a second week with the market expecting more rate rises in the offing if Truss becomes the next UK PM in view of her tax-cutting agenda.

The latest YouGov / Times Tory members poll shows a 34 point lead for Truss:

- 60% Truss

- 26% Sunak

Nevertheless, the poor outlook for growth in the UK remains a significant concern for speculators.

''GBP has been trading under a cloud of negative sentiment for large swaths of this year,'' analysts at Rabobank noted. ''It was notable in May that the BoE’s (as expected) rate hike failed to stop the pound from falling as the market latched on to the Bank’s downside growth revision.''

''Around this time the OECD forecast that the UK would see no growth in 2023, a little worse than our house forecast of 0.2%. The BoE, like most other central banks, is committed to reigning in inflation, even at the cost of growth. However, the absence of the latter has provided a strong headwind for the pound.''

What you need to take care of on Wednesday, August 3:

Risk-aversion returned and benefited the greenback. Tensions arose on news of US House Speaker Nancy Pelosi's visit to Taiwan. Pelosi supports the local government against China's will, spurring geopolitical tensions between the two major economies.

Demand for the greenback temporarily eased early in the American session but resumed following comments from US Federal Reserve officials. Chicago Fed Charles Evans noted that inflationary pressures may be broadening out and that the jobless rate could increase to around 4.25%, but considered reasonable a 50 bps rate hike in September. Loretta Mester, on the other hand, said she does not think the country is suffering a recession, adding that the labour market is in great shape. On inflation, however, she noted that it has not decreased "at all."

The EUR/USD pair fell to 1.0170, settling some pips above the latter. The GBP/USD pair also settled in the red after a failed attempt to regain the 1.2200 threshold.

The dollar also appreciated against safe-haven rivals. USD/CHF trades around 0.9560 while USD/JPY is currently at around 132.80. Gold surged to an almost one-month high of $1,787.99, ending the day with modest losses at around $1,768.

Crude oil prices, on the other hand, recovered some ground and the barrel of WTI currently stands at $94.30.

US Treasury yields ticked higher. The yield on the 10-year Treasury note currently stands at 2.573%, while that on the 2-year note jumped to 3.07%. The yield curve is now the most inverted since 2000.

Finally, commodity-linked currencies weakened against the dollar in the American session amid the sour tone of Wall Street. AUD/USD trades near a relevant low of 0.6911, while USD/CAD stands at around 1.2850.

Top 3 Price Prediction Bitcoin, Ethereum, Ripple: WallStreet'ss bait and switch

Like this article? Help us with some feedback by answering this survey:

- The EUR/GBP remains on the defensive as sellers eye a break below 0.8346.

- The RSI in the EUR/GBP daily chart confirms the downward bias.

- A tweezers-top in the hourly chart sent the EUR/GBP sliding 60 pips.

The EUR/GBP extended its losses in the week, falling for two days in a row and challenging the 0.8345 July 28 low, which, once broken, would open the door for further losses. A risk-off impulse keeps safe-haven peers rising, as geopolitical US-China frays keep traders jittery. At the time of writing, the EUR/GBP is trading at 0.8350.

EUR/GBP Price Analysis: Technical outlook

The EUR/GBP is downward biased once the exchange rate tumbled below the daily EMAs, particularly the 200-day EMA on July 26. Since then, the cross remains range-bound in the 0.8330-0.8400 area, unable to crack any of the up/down boundaries, despite that the Relative Strength Index (RSI) is headed downwards, which might open the door for lower prices.

EUR/GBP 1-hour chart

The EUR/GBP hourly chart further confirms the higher time-frame bias. Additionally, after hitting a daily high at 0.8399, a tweezers-top candlestick chart pattern emerged, sending the pair tumbling to its daily low at 0.8339. Although the cross jumped at the lows and breached the S1 daily pivot on top, EUR/GBP buyers need to achieve a daily close above 0.8353. Failure to do so, sellers remain in charge.

Therefore, the EUR/GBP first support would be the S1 daily pivot at 0.8351. Once cleared, the next support would be the S2 pivot point at 0.8329, followed by the 0.83000 figure.

EUR/GBP Key Technical Levels

- Gold is back under pressure as US yields spike, but bulls are not far away.

- There is room for further upside with the 68.2% Fibonacci meeting prior weekly structure around $1,800.

- Markets are cautious over US/Sino tensions over Taiwan.

The gold price is dipping below $1,770 in the midday US session from $1,788.12 the high that was scored in the New York open. XAU/USD is down some 0.18% on the day currently as it moves in on the lows of the day at $1,767.76.

The price has been driven by US bond yields that have been waning in the wake of a less hawkish narrative surrounding the Federal Reserve. This has lifted gold futures and for December delivery, the precious metals climbed back above $1,800 per ounce on Tuesday.

The yield on the US 10-year note was last seen up 2.732 % after recovering from the lowest since early April and at the bottom of the broadening formation's daily range:

The rebound in yields is a weight on the yellow metal. Meanwhile, the US dollar rose off the lowest in nearly a month early on Tuesday, with the DXY index last seen up 0.72% to 106.166.

US/Sino relations are the wild card for gold

To add insult to injury, the US dollar is attracting a safe haven bid on worries a visit by U.S. House of Representatives Speaker Nancy Pelosi to Taiwan would further harm relations between China and the United States. China has threatened repercussions if Pelosi visited the self-ruled island, which Beijing claims as its territory.

said on Monday it would not be intimidated by China. Consequently, US long-term Treasury yields dropped to a four-month low while the US dollar gained against a basket of currencies. Gold also picked up a bid, but that is being demolished with the sudden corrective spike in US yields.

''Nonetheless, for further significant short covering from CTA trend followers to take place, gold prices would need to close north of $1820/oz to spark a change in trend signals,'' analysts at TD Securities argued.

''However, on the other hand, we see risks that Fed speakers can push back against market expectations for an early Fed pivot. In this sense, gold markets are faced with a massive amount of complacent length held by prop traders, which still hold the title as the dominant speculative force in gold.''

''We have yet to see capitulation in gold, suggesting the pain trade is still to the downside and we expect the recent rally will ultimately fade, facing a wall of offers.''

Gold technical analysis

As per the prior analysis, Gold Price Forecast: XAU/USD bulls are back in play, it was explained that the price was running higher in a correction of the weekly M-formation:

The grey area was a price imbalance that has now been mitigated by a 50% mean reversion:

There is room for further upside with the 68.2% Fibonacci meeting prior structure around $1,800.

- The USD/CHF stages recovery after hitting a four-month low at 0.9470.

- Sentiment remains negative, bolstering appetite for the greenback.

- In the long-term, the USD/CHF is neutral biased, but short-term is tilted upwards, opening the door for a test of the 0.9600 mark.

The USD/CHF rebounded from under the June 29 swing low at 0.9495 and climbed to the daily high at 0.9559s, amidst a sour market mood, on US-China tussles, while also Fed speakers continued to push back against the market’s reaction to the FOMC 75 bps rate hike. At the time of writing, the USD/CHF is trading at 0.9551, up 0.67%.

USD/CHF Price Analysis: Technical outlook

The USD/CHF is neutral biased on sellers’ failure to hold the exchange rate below 0.9495, which would have paved the way towards the 200-day EMA at 0.9412. Instead, the USD/CHF edged higher, forming a bullish-engulfing chart pattern, a reversal pattern indicating buyers outweigh sellers, keeping risks skewed to the upside. Besides, the Relative Strength Index (RSI) is about to cross over its 7-day RSI’s SMA, which would open the door for higher prices.

Therefore, the USD/CHF first ceiling level would be the 100-day EMA at 0.9614. Break above will expose the major for further upside. Otherwise, a breach under 0.9500 could send the pair towards 0.9412, the 200-day EMA.

USD/CHF 1-hour chart

The USD/CHF is neutral-upward biased but faced solid resistance at a fifteen-day-old downslope trendline, which capped the rally at 0.9559. However, with the spot price above the 20, 50, and 100-hour EMAs, alongside the Relative Strength Index (RSI) aiming higher. That could open the door for a USD/CHF re-test of 95.60, which would lift the major towards the 200-hour EMA at 0.9592.

USD/CHF Key Technical Levels

Loretta J. Mester, president of the Federal Reserve Bank of Cleveland, joins Washington Post global economics correspondent David J. Lynch to discuss the Fed’s plan to tamp down on inflation and the concerns that it could induce a recession.

Key quotes

We'll be growing below trend this year.

We are not in a recession.

Haven't seen inflation cool ‘at all,’ reiterates commitment to bringing inflation under control.

Have to take Fed's models with ‘some caution’.

No slowdown in US labour markets, looking very healthy right now.

US dollar catches a safe haven bid

Meanwhile, US stocks struggled for gains and the dollar and gold rallied on Tuesday in a flight for safety, Markets are trading cautiously around simmering US-China tensions over Taiwan as well as the ongoing concerns about a cooling global economy. DXY is 0.63% higher at 106.07 the high for the day so far.

- The shared currency struggled near 1.0300 and tumbled below 1.0200 before regaining the price level.

- Risk aversion keeps traders’ flows into safe-haven peers, like the greenback.

- EUR/USD Price Analysis: Failure to hold above 1.0200, the EUR/USD could dive towards 1.0100; otherwise, a rally to 1.0300 is on the cards.

The common currency remains heavy and falls on Tuesday, as risk-aversion dominates traders’ mood. Geopolitical tensions are arising from the visit of US House’s Nancy Pelosi to Taiwan, as news flows emerging from China condemned the visit. Besides that, Fed speaking commentary, saying that the US central bank is “nowhere near” to be done fighting inflation, keeps investors uneasy.

The EUR/USD is trading at 1.0200, after hitting a daily high at 1.0293, but flows to safety, augmented demand for the greenback.

EUR/USD creeps lower on haven flows

Newswires from China signaling increasing military drills around Taiwan would likely keep the sentiment sour. Aside from this, US labor market data, namely JOLTs Job Openings for June, rose to 10.7 million, less than 11 million estimated by the streets. That suggests the labor market is easing amid growing economic pressures.

Fed speakers have begun to cross wires led by San Francisco Fed President Mary Daly, saying that the Fed is “nowhere near” done in fighting inflation and added that “it would be premature to unwind all of that (Fed tightening) and say the job is done.”

Late, the Chicago Fed President Charles Evans said that going 50 bps “is a reasonable assessment, but 75 bps could also be okay.”

Whereas in the Eurozone, Spain reported data, with the July Consumer Confidence slowing to 55.5, less than estimates at 60.1, and lower than June’s 65.8. Though data was mainly ignored, the euro is feeling the pain from falling German bunds yields, with the 10-year bund rate down from 0.885% to 0.820%, higher than its daily low at 0.678%.

The US Dollar Index, a gauge of the greenback’s value vs. a basket of peers, rises 0.05% and sits at 105.882, underpinned by haven flows, as geopolitical tensions uprise, weighing on the Loonie.

What to watch

The EU economic docket will feature Germany’s Trade Balance and a tranche of S&P Global Services and Composite PMIs from Eurozone countries and the bloc. That, alongside EU, France, and Italy’s Retail Sales, would be some data to digest for EUR/USD traders.

On the US front, further Fed speakers will shed light on the future of further Fed tightening. On Wednesday, the docket will unveil S&P Global PMIs, ISM Non-Mfg. PMIs, and Factory Orders for June.

EUR/USD Price Analysis: Technical outlook

The EUR/USD is downward biased, even though it bounced off YTD lows, reached on July 14. Nevertheless, EUR/USD buyers could not crack above the 1.0300 mark, exposing the pair to selling pressure. Therefore, the EUR/USD first support would be the 20-day EMA at 1.0157. Once cleared, it would open the door for a dive towards 1.0100. Otherwise, if the EUR/USD breaks above 1.0300, it could send the pair towards the 50-day EMA at 1.0405.

The USD/ZAR is rising 1% on Tuesday at 16.650, amid a strong US dollar versus emerging market currencies. Analysts at MUFG Bank see that the recovery seen during the last week of the South African rand so far is just a “temporary reflief”. They forecast USD/ZAR at 17.250 by the end of the third quarter and at 16.500 by the end of the first quarter of 2023.

Key Quotes:

“The combination of tighter Fed policy and lower commodity prices is an unfavourable combination for the rand. In recent weeks there has been some temporary relief for the rand as global equity markets have staged a modest rebound and US yields have corrected lower. However, we are not yet convinced that the worst is over for the rand. It is premature to expect the Fed stage a dovish pivot in the near-term even as evidence continues to build that the US economy is slowing.”

“The SARB (South African central bank) has recently sped up the pace of rate hikes that is helping to provide more support for the rand. USD/ZAR broke back below the 17.000-level after the SARB delivered a larger 75bps hike on 21st July. It follows a further pick-up in the headline rate of inflation to 7.4% in June. On the other hand, the SARB has become more pessimistic over the outlook for growth next year (+1.3%). Tighter monetary policy and rolling energy blackouts, with outages hitting record levels so far this year, are increasing downside risks to the growth outlook.”

- Australian dollar recovers after falling sharply following the RBA meeting.

- US dollar posts mixed results, and receives support from higher US yields.

- AUD/USD finds support again around 0.6910.

The AUD/USD extended the recovery after the RBA slide and climbed to 0.6965. It is hovering around 0.6950/55, down 60 pips for the day, the worst performance since July 11.

From the RBA to higher US yields

The Reserve Bank of Australia raised the key interest rate by 50 basis points. The guidance offered by the central bank was seen as “dovish” and pushed the aussie to the downside. The AUD/USD dropped to 0.6910. After reaching a fresh daily high at 0.6909, it started to recover.

Since the beginning of the American session it recovered more than fifty pips. At the same time, the AUD/NZD that bottomed at 1.1007, the lowest in two weeks, rebounded and as of writing, it trades at 1.1055/60.

The move to the upside took place as equity prices in Wall Street turned positive and as the greenback lost momentum versus commodity currencies, even amid higher US yields.

The AUD/USD chart shows the pair still moving sideways around 0.6970. The 0.6910 zone has become a critical support that if broken should clear the way to more losses, targeting first the 20-day Simple Moving Average at 0.6878.

Analysts at Rabobank, see scope for another bout of broad-based USD strength to push AUD/USD lower on a 1 to 3 month view but then they see a recovery. “We expect AUD/USD to rise to the 0.74 area on a 12 month view.”

Technical levels

Chicago Fed President Charles Evans said on Tuesday that a 50 basis points rate hike would be a reasonable assessment for the September policy meeting if inflation does not improve, as reported by Reuters.

Additional takeaways

"75 bps increase is also okay; I doubt a 100 bps hike is called for."

"I am still hopeful we can do 50 bps hike in September and then continue with 25 bps rate hikes until the beginning of the second quarter of 2023."

"There’s still a reasonable expectation that monetary tightening into next year will lead to a restrictive setting but allow for a reasonably strong labor market."

"I see policy rate between 3.75 and 4% by end of next year."

"I see path to unemployment rate remaining below 4.5% with economic growth near trend."

"If we don’t see improvement in inflation over next few months, we may have to rethink rate path a little higher."

"It is possible we get a soft landing, but there are a lot of risks."

"A recession is unhealthy; so is such high inflation."

"Important to keep eye on where monetary policy has to go over medium term."

"Wouldn’t be surprising for unemployment rate to rise to region of 4.25%."

"I think unemployment rate will stay below 4% this year."

"I have downgraded my economic growth predictions somewhat for this year, probably looking at 1% or lower."

"We need to start getting less ugly inflation reports soon."

"We have to be mindful that inflationary pressures may be broadening out."

"A gentler incline once we have got slightly restrictive level would be a good path, but depends on the data."

Market reaction

The US Dollar Index showed no immediate reaction to these comments and was last seen rising 0.45% on the day at 105.88.

- USD/JPY finds support before 130.00 and breaks a negative streak.

- US dollar gains momentum as US yields rebound.

The USD/JPY rose more than a hundred pips during the last hours, recovering sharply from the lowest level in almost two months. The pair bottomed at 130.36 and recently printed a fresh daily high slightly above 132.00.

The dollar is rising across the board for the first time after falling for four consecutive days boosted by higher US yields. The 10-year rose from month lows at 2.54% to 2.67%, and the 30-year from 2.87% to 2.95%.

Equity prices are falling on Wall Street but off lows. The S&P 500 trimmed losses and is down by just 0.06%, the Dow Jones drops 0.47% and the Nasdaq is up by 0.21%.

The improvement in risk sentiment added pressure on the yen. The Japanese currency is the worst performer of the American session while the DXY is holding onto gain, rising for the first time out of the last five days.

Yen’s rally: is it over?

The reversal in USD/JPY on Tuesday could point to the end of the rally of the yen. Still, with many critical reports ahead, including July payroll on Friday, it appears too early to consider the pair is ready to resume the upside.

From a technical perspective, USD/JPY rose back above the 131.00 area (a critical support) and also rebounded at the 20-week Simple Moving average.

Technical levels

- USD/CAD jumped on risk-off impulse, spurred by geopolitical jitters between the US and China.

- In the FX space, safe-haven peers like the USD, the JPY, and the CHF appreciate.

- Fed Daly: Fed needs to keep committed to bringing inflation down.

The USD/CAD climbs above the 50-day EMA, due to several factors, including the visit of US House Speaker Nancy Pelosi to Taiwan and increasing tensions between the US and China. That alongside expectations of the Federal Reserve pushing back against a perceived “dovish” tilt when Chair Powell acknowledged that spending and production softened.

The USD/CAD is trading at 1.2857 after hitting a daily low of 1.2835, then bouncing off the daily lows and climbing to its daily high at 1.2887.

USD/CAD advanced on risk aversion

Global equities remain under pressure. Albeit a hiccup upwards, as reports that the plane of House speaker Pelosi landed, the dust begins to settle down, and equities are back in the red. Earlier, US data showed signs of constraints in the labor market, as the US JOLTS Openings reported that vacancies fell to 10.7 million, its lowest since September 2021.

In the meantime, the US Dollar Index, a gauge of the greenback’s value vs. a basket of peers, rises 0.05% and sits at 105.882, underpinned by haven flows, as geopolitical tensions uprise, weighing on the Loonie.

Fed officials have begun to cross wires. The San Francisco Fed President, Mary Daly, said so far, is “pleased” with the Fed decisions, but the Fed is “nowhere near” being almost done in fighting inflation. She added that the Fed needs to “keep committed until we actually see it in the data.”

On the Canadian side, the S&P Global Manufacturing PMI remains in the expansionary territory around 52.5, much lower than the forecasted, and trailed June’s 54 figure.

Elsewhere, crude oil prices begin to rise, putting a lid, on the rise of the USD/CAD, due to the CAD’s positive correlation with oil. WTI is trading at $94.00 PB, slightly up 0.25%.

What to watch

Additional Fed speakers will cross wires through the day, led by Charles Evans, Loretta Mester and James Bullard.

USD/CAD Key Technical Levels

In response to US House of Representatives Speaker Nancy Pelosi's arrival in Taiwan, China's Foreign Ministry said that Pelosi's visit seriously violated China's sovereignty and territorial integrity, as reported by Reuters.

Market reaction

These comments don't seem to be having a significant impact on risk perception. As of writing, the S&P 500 Index was down 0.05% on a daily basis at 4,116.

Additional takeaways

"Pelosi's visit to Taiwan severely impacts political foundation of Sino-US relations."

"Pelosi's visit to Taiwan seriously damages peace, stability in Taiwan Strait."

"Those who play with fire will perish by it."

"Urging US to stop interfering with c-China's internal affairs, not to continue in the wrong and dangerous path."

"China will definitely take all necessary measures to resolutely safeguard sovereignty, territorial integrity in response to Pelosi's visit."

"All consequences are to be borne by US side, Taiwan pro-independence forces."

- US JOLTS Job Openings declined sharply in June.

- US Dollar Index extends its recovery toward 106.00.

The number of job openings decreased to 10.7 million on the last business day of June, the US Bureau of Labor Statistics reported in its Job Openings and Labor Turnover Summary (JOLTS) on Tuesday. This print came in slightly lower than the market expectation of 11 million and followed May's reading of 11.3 million.

"Hires and total separations were little changed at 6.4 million and 5.9 million, respectively," the publication further read. "Within separations, quits (4.2 million) and layoffs and discharges (1.3 million) were little changed."

Market reaction

The US Dollar Index continues to push higher and was last seen rising 0.55% on the day at 105.98.

San Francisco Fed President Mary Daly said on Tuesday that she is looking for incoming data to decide if they can downshift the rate hikes or continues at the current pace, as reported by Reuters.

Additional takeaways

"Work on inflation is nowhere near almost done."

"We are still resolute and completely united on achieving price stability."

"We have a long way to go on that task."

"Gas price drop is going to provide some relief, housing market slowing is also a good sign."

"Getting too confident that we've already solved the problem would be a mistake."

"My modal outlook is we raise interest rates and hold them there for a while."

Market reaction

The US Dollar Index extended its rebound and was last seen gaining 0.35% on the day at 105.78.

Analysts at TD Securities (TDS) offered a brief preview of the final version of the monthly retail sales figures from Australia, scheduled for release during the Asian session on Wednesday. The data might influence the aussie and provide some impetus to the AUD/USD pair.

Key Quotes:

“Nominal Q2 retail sales was strong, up 3.2% q/q, albeit boosted by higher prices of goods and services. Nonetheless, we expect real Q2 retail sales to still increase by a still-robust pace of 2.0% q/q (cons: 1.2%, Q1: 1.2%) which should give a boost to Q2 GDP. “

“If real retail sales surprise strongly to the upside, this gives RBA room to continue its aggressive pace of rate hikes given the underlying strength in consumer spending. We expect the RBA to hike by another 50bps at the September meeting.”

- USD/TRY resumes the upside and approaches 18.00.

- Renewed buying interest in the dollar lifts the pair.

- Investors’ attention shifts to the release of July CPI on Wednesday.

The Turkish lira resumes its depreciation and lifts USD/TRY to new 2022 highs closer to the 18.00 hurdle on Tuesday.

USD/TRY now looks to CPI results

After two consecutive daily pullbacks, USD/TRY regains upside traction and trades closer to the key 18.00 hurdle, or new YTD tops, on Tuesday.

The re-emergence of the risk aversion on US-China jitters props up the better tone in the greenback and the safe haven universe, putting in consequence the EM FX space back under extra pressure.

In addition, investors are expected to remain wary in the next hours ahead of the release of inflation figures in Türkiye for the month of July on Wednesday, with consensus expecting the CPI to surpass the 80.0% mark over the last twelve months.

What to look for around TRY

The upside bias in USD/TRY remains unchanged and stays on course to revisit the key 18.00 zone.

In the meantime, the lira’s price action is expected to keep gyrating around the performance of energy prices, which appear directly correlated to developments from the war in Ukraine, the broad risk appetite trends and the Fed’s rate path in the next months.

Extra risks facing the Turkish currency also come from the domestic backyard, as inflation gives no signs of abating, real interest rates remain entrenched in negative figures and the political pressure to keep the CBRT biased towards low interest rates remain omnipresent. In addition, there seems to be no Plan B to attract foreign currency in a context where the country’s FX reserves dwindle by the day.

Key events in Türkiye this week: Inflation Rate, Producer Prices (Wednesday).

Eminent issues on the back boiler: FX intervention by the CBRT. Progress (or lack of it) of the government’s new scheme oriented to support the lira via protected time deposits. Constant government pressure on the CBRT vs. bank’s credibility/independence. Bouts of geopolitical concerns. Structural reforms. Presidential/Parliamentary elections in June 23.

USD/TRY key levels

So far, the pair is gaining 0.50% at 17.9491 and faces the immediate target at 17.9545 (2022 high August 2) seconded by 18.2582 (all-time high December 20) and then 19.00 (round level). On the other hand, a breach of 17.1903 (weekly low July 15) would pave the way for 17.0110 (55-day SMA) and finally 16.0365 (monthly low June 27).

- Canada S&P Global Manufacturing PMI declined in July.

- USD/CAD clings to small daily gains above 1.2850.

The business activity in Canada's manufacturing sector expanded at a softer pace in July than in June with the S&P Global Manufacturing PMI dropping to 52.5 from 54.6. This print came in weaker than the market expectation of 55.7.

Commenting on the data, "latest PMI data revealed another slowdown in operating conditions in Canada's manufacturing sector with the PMI at its lowest point for just over two years," said Shreeya Patel, Economist at S&P Global Market Intelligence. "Behind the latest moderation were contractions in both output and new orders which fell for the first time since the pandemic began in the first half of 2020."

Market reaction

The USD/CAD pair edged slightly higher with the initial reaction and was last seen rising 0.12% on the day at 1.2860.

- Gold gains traction for the fifth straight day and climbs to a four-week high on Tuesday.

- Declining US bond yields and the risk-off mood continue to offer support to the XAU/USD.

- A goodish USD bounce from a multi-week low is acting as a headwind for the commodity.

Gold builds on last week's bullish breakout momentum through the $1,745-$1,750 resistance zone and gains traction for the fifth successive day on Tuesday. The momentum remains uninterrupted through the early North American session and lifts spot prices to a four-week high, around the $1,788 region.

The ongoing decline in the US Treasury bond yields continues to offer some support to the non-yielding gold. In fact, the yield on the benchmark 10-year US government bond drops to a four-month low amid reduced bets for larger interest rate hikes by the Federal Reserve. It is worth recalling that the Fed last week hinted that it could slow the pace of the current rate hike cycle at some point. Furthermore, the Advance US GDP report released last Thursday confirmed a technical recession and forced investors to scale back expectations for a more aggressive policy tightening by the Fed.

Apart from this, the prevalent risk-off mood further benefits the safe-haven precious metal. The market sentiment remains fragile amid growing worries about a global economic downturn. Furthermore, mounting diplomatic tensions over US House Speaker Nancy Pelosi's Taiwan visit temper investors' appetite for perceived riskier assets. In fact, Wang Yi, senior Chinese diplomat and the Foreign Minister, warned on Tuesday that the US politicians are openly playing with fire with the Taiwan issue. This, in turn, is driving flows towards traditional safe-haven assets, including the XAU/USD.

That said, a goodish US dollar bounce from a four-week trough touched earlier this Tuesday is acting as a headwind for the dollar-denominated gold. That said, the aforementioned factors should continue to lend some support to the XAU/USD ahead of the next key data point from the US, the monthly jobs report (NFP) on Friday. This makes it prudent to wait for strong follow-through selling before confirming that the recent recovery from a 15-month low, around the $1,680 region touched in July, has run out of steam. In the absence of any major market-moving economic releases, the US bond yields, the broader risk sentiment and the USD price dynamics would continue to influence spot prices.

Technical levels to watch

- EUR/USD comes under pressure after faltering ahead of 1.0300.

- Further upside is seen once 1.0300 is cleared.

EUR/USD advanced to levels just shy of 1.0300 the figure and sparked a corrective downside soon afterwards.

Ideally, the pair should clear the area of recent peaks to allow for the continuation of the rebound in the near term. That said, above the 1.0300 zone the pair should meet the next up barrier at the 55-day SMA, today at 1.0423.

Beyond the latter emerges the 6-month support line around 1.0440, above which the downside pressure is predicted to mitigate.

In the longer run, the pair’s bearish view is expected to prevail as long as it trades below the 200-day SMA at 1.0949.

EUR/USD daily chart

Citing two OPEC+ delegates, Reuters reported on Tuesday that the OPEC+ Joint Technical Committee (JTC) lowered its oil market surplus forecast for 2022 by 200,000 barrels per day (bpd) to 800,000 bpd.

According to sources, the JTC did not discuss the output policy ahead of the ministerial meeting of OPEC+ on Wednesday.

Market reaction

Crude oil prices continue to edge lower following this report. As of writing, the barrel of West Texas Intermediate was trading at $93.35, where it was down 0.73% on a daily basis.

- GBP/USD edges lower on Tuesday and erodes a part of the overnight gains to a one-month high.

- Jitters ahead of Pelosi's Taiwan visit boost the safe-haven USD and exert downward pressure.

- The formation of an ascending channel supports prospects for the emergence of some dip-buying.

The GBP/USD pair witnesses some selling on Tuesday and extends the overnight modest pullback from the vicinity of the 1.2300 mark, or over a one-month high. Spot prices, however, show some resilience below the 1.2200 mark and have now managed to rebound a few pips from the daily low.

The US dollar draws some haven flows amid mounting diplomatic tensions over US House Speaker Nancy Pelosi's Taiwan visit and stages a goodish bounce from a fresh multi-week low. This turns out to be a key factor that exerted some downward pressure on the GBP/USD pair through the first half of the European session.

The anti-risk flow, along with expectations that the Fed would not increase rates as aggressively as previously estimated, continues to drag the US Treasury bond yields lower. This is acting as a headwind for the buck. Apart from this, rising bets for a 50 bps rate hike by the Bank of England have helped limit losses for the GBP/USD pair.

Looking at the broader picture, the recent recovery from the lowest level since March 2020 witnessed over the past two-and-half weeks or so has been along an upward sloping trend channel. This points to a well-established short-term bullish trend and supports prospects for the emergence of some dip-buying at lower levels.

Hence, any subsequent decline below the daily swing low, around the 1.2185 region, is likely to stall near the lower end of the ascending channel. The said support is currently pegged near the 1.2100 mark and is closely followed by the 200-period SMA on the 4-hour chart, around the 1.2080 region, which should act as a pivotal point.

On the flip side, the 1.2245 area could provide a hurdle ahead of the 1.2280 supply zone. Sustained strength beyond should allow the GBP/USD pair to surpass the 1.2300 mark and test the ascending channel resistance, currently around the 1.2315 region. Some follow-through buying would be seen as a fresh trigger for bulls.

GBP/USD 4-hour chart

-637950420544688635.png)

Key levels to watch

According to Win Thin, Global Head of Currency Strategy at BBH, the US dollar draws some support from haven flows on Tuesday amid mounting diplomatic tensions in the wake of the planned Taiwan visit by US House Speaker Nancy Pelosi. He further sticks to his medium-term USD bullish outlook ahead of Fed speakers and important US macro data this week.

Key Quotes:

“The dollar is getting some limited traction as risk off sentiment takes hold. DXY is up for the first time after four straight down days and trading near 105.541 as House Speaker Pelosi’s Taiwan visit has led to tensions with China. We maintain our strong dollar call and believe that markets are misreading the Fed’s commitment to lowering inflation. However, the greenback is unlikely to get much traction in the absence of strong economic data. This week’s U.S. data will be key for the medium-term dollar outlook.”