- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 11-07-2022

- EUR/USD remains pressured around 20-year low, sidelined of late.

- Impending gas shortage propels fears of recession in the bloc to favor the bears.

- Strong US inflation expectations, risk-aversion wave underpin USD’s safe-haven demand.

- ZEW Survey figures for July can entertain traders but risk catalysts are the key.

EUR/USD bears take a breather around 1.0050, after refreshing the 20-year low with the biggest daily slump in a week. That said, a lack of major catalysts and the market’s cautious mood ahead of the key data/events appear to challenge the pair traders during Tuesday’s Asian session.

With the chatters surrounding Russia’s closure of the Nordstorm 1 gas pipeline for maintenance fueling fears of economic slowdown in Europe, EUR/USD had a major downside to track the previous day. On the other hand, a jump in the US inflation expectations and comments from the US policymakers suggesting more pain ahead escalated the fears of economic slowdown, which in turn propelled the US dollar’s safe-haven demand.

German Economy Minister Robert Habeck said on Monday it was difficult to say whether Nord Stream 1 gas pipeline would come back online after the maintenance, as reported by Reuters. On the same line, a German Newspaper Handelsblatt quoted the Chief of the German trade union DGP as saying, “Millions of jobs could be threatened if Russian gas stop goes on for longer.” However, Vice President of the European Commission Valdis Dombrovskis mentioned, per Reuters, “Complete gas stop this month is a no base scenario.”

That said, one-year US inflation expectations jumped to the record high of 6.8% in June, versus 6.6% prior, per the NY Fed’s survey of one-year-ahead consumer inflation expectations. The inflation expectations followed strong US employment data, published Friday, to underpin hopes of an aggressive Fed rate hike and fuelled concerns over the health of the US economy, as well as the global ones. That said, the latest US jobs report mentioned that the US Nonfarm Payrolls (NFP) rose by 372K for June, versus expected 268K and downward revised 384K prior. Further, the Unemployment Rate matched market expectations of reprinting 3.6% level. Further details suggest that the annual wage inflation, as measured by the Average Hourly Earnings, edged lower to 5.1% from 5.3% in May and the Labor Force Participation declined to 62.2% from 62.3.

Elsewhere, White House Press Secretary Karine Jean-Pierre told reporters that she expects new Consumer Price Index (CPI) data to be highly elevated. Further, Atlanta Fed President Raphael Bostic said that recent inflation data has not been as encouraging as I would have liked, per Reuters.

Amid these plays, equities remained depressed and the US Treasury yields kept flashing recession fears. S&P 500 Futures, however, print mild gains by the press time.

Moving on, ZEW Survey for Economic Sentiment, for Eurozone and Germany, expected -32.8 and -38.0 respectively, appear important for the EUR/USD traders to watch amid fears of economic slowdown in the bloc. However, major attention will be given to fears of higher inflation ahead of the US Consumer Price Index (CPI) for June, up for publication on Wednesday.

Technical analysis

A clear downside break of the early 2017 low of 1.0340 keeps EUR/USD bears directed towards the August 2002 low near 0.9625. However, the 1.0000 psychological magnet may probe the short-term bears.

- USD/CHF is likely to display more gains above 0.9850 as a consensus for US CPI indicates higher print.

- The Fed is expected to maintain the status quo and will raise interest rates by 75 bps.

- Swiss’s light economic calendar compels US CPI to remain the major trigger for this week.

The USD/CHF pair is juggling in a narrow range of 0.9822-0.9834 in the Asian session as investors are shifting their focus on the release of the US Inflation on Wednesday. On a broader note, the asset has remained in the grip of bulls consecutively for the past seven trading sessions. It would be worth keeping an eye on Monday’s high of 0.9843 as a break of the same will strengthen the odds of the maintenance of the winning spree.

A preliminary estimate for the US Consumer Price Index (CPI) is 8.7%, modestly higher than the former release of 8.6%. The Federal Reserve (Fed) has already elevated its interest rates to 1.50-1.75% in its last three monetary policy meetings. Despite that, the price pressures have not shown any sign of exhaustion. Therefore, the odds of a consecutive 75 basis points (bps) interest rate hike by the Fed have bolstered.

Meanwhile, the US dollar index (DXY) is holding itself above 108.20 firmly amid an ongoing risk-off impulse. This has improved the appeal for the safe haven vigorously. On the lower timeframe, the DXY is displaying some exhaustion signals, therefore a minor correction cannot be ruled out.

On the Swiss franc front, the release of the flat jobless rate last week failed to support the Swiss franc bulls. The monthly data remained in line with the estimates and the prior release of 2.2%.

- WTI extends week-start pullback amid fears of slower demand, higher output.

- US President Biden is up for pushing Middle East producers for more oil production.

- 14 oil firms will benefit from the US Strategic Petroleum Reserve (SPR) action.

- US API inventories, risk catalysts will be important to watch for fresh impulse.

WTI crude oil takes offers to renew its intraday low near $100.25 during the initial Asian session on Tuesday. The black gold reversed from a one-week high the previous day while snapping a two-day uptrend as the market’s fears of recession joined chatters surrounding the likely increase in oil output.

Recently, White House National Security Adviser Jake Sullivan said, per Reuters, “US President Joe Biden will make the case for greater oil production from OPEC nations to bring down gasoline prices when he meets Gulf leaders in Saudi Arabia this week.”

The news joined another piece from Reuters suggesting an increase in the oil output saying, “The United States on Monday said 14 companies had been awarded contracts for the latest sale of oil from the Strategic Petroleum Reserve as part of the administration's efforts to ease disruption caused by the war in Ukraine.”

Elsewhere, a jump in the US inflation expectations and comments from the US policymakers suggesting more pain ahead escalated the fears of economic slowdown, which in turn weighed on the energy demand. That said, one-year US inflation expectations jumped to the record high of 6.8% in June, versus 6.6% prior, per the NY Fed’s survey of one-year-ahead consumer inflation expectations. The inflation expectations followed strong US employment data, published Friday, to underpin hopes of an aggressive Fed rate hike and fuelled concerns over the health of the US economy, as well as the global ones. That said, the latest US jobs report mentioned that the US Nonfarm Payrolls (NFP) rose by 372K for June, versus expected 268K and downward revised 384K prior.

Further, White House Press Secretary Karine Jean-Pierre told reporters that she expects new Consumer Price Index (CPI) data to be highly elevated. Further, Atlanta Fed President Raphael Bostic said that recent inflation data has not been as encouraging as I would have liked, per Reuters.

Additionally, Shanghai’s first coronavirus Omicron sub-variant BA-5 case escalated virus woes after the dragon nation failed to sustain the unlock activities. On the same line was firmer inflation data from the Asian major and doubts over Beijing’s GDP goal, as well as on the stimulus’ ability to renew optimism, which in turn challenges oil demand.

Moving on, weekly readings of the industrial player American Petroleum Institute (API), prior 3.825M, could entertain the oil traders. Though, major attention will be given to the chatters surrounding the recession.

Technical analysis

Although the 200-DMA challenges WTI bears around $93.00, any intermediate recovery appears elusive until the quote rises past $106.10-15 resistance confluence, including the 100-DMA and downward sloping trend line from June 14.

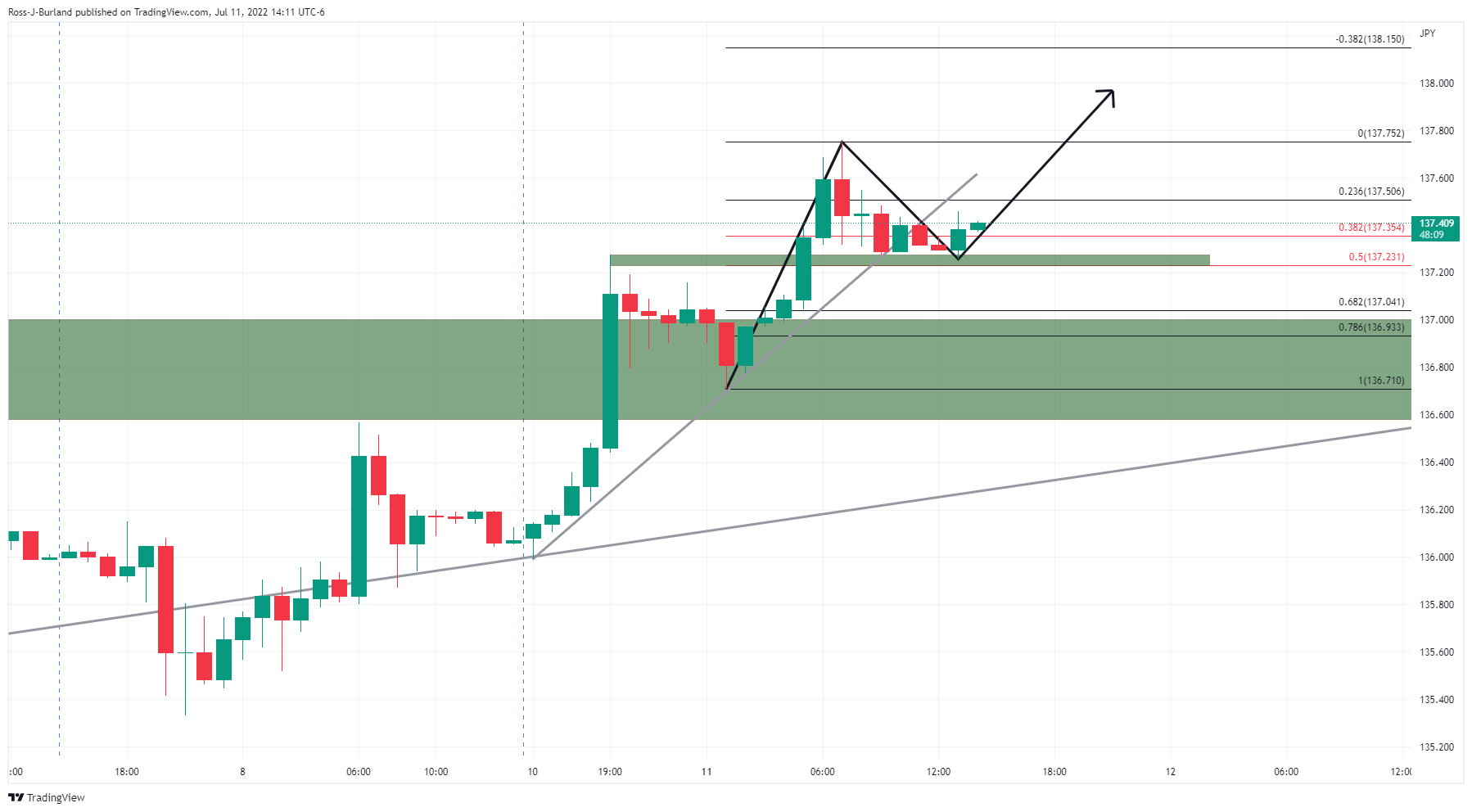

- The EUR/JPY remains heavy, extending its losses, also weighed by a falling EUR/USD, which is approaching parity.

- Sentiment is still negative; with Asian equities set to open lower, safe-haven flows will remain bid.

- EUR/JPY sellers stepped in around the 139.00 area and sent the pair sliding as they targeted a move towards the 100-day EMA around 136.00.

The EUR/JPY slumps below the 50-day EMA after last Friday’s buyers attempts to drag the pair above the 139.00 figure, though sellers regained control on Monday, courtesy of downbeat market sentiment sparked by the resurgence of covid-19 in China, as the US inflation data looms.

During Monday’s trading session, the EUR/JPY began trading around 138.50s, surging towards the daily high just above 139.15, tripping down afterward towards the daily low of the day at 137.88. At 137.90, the EUR/JPY stabilized as Tuesday’s Asian session began, almost flat.

EUR/JPY Daily chart

The EUR/JPY is upward biased, despite slipping through the 50-day EMA around 139.05. Nevertheless, oscillators residing in sellers’ territory, and pushing downwards, opens the door for a 100-day EMA test at 136.16. Regardless, the cross-currency might consolidate due to solid support around 137.20-60 and could form a bearish rectangle before aiming lower.

If that scenario plays out and the EUR/JPY breaks below, the first support would be 137.00. The break below would expose the 100-day EMA at 136.16. If that level is cleared, the next support would be the 200-day EMA at around 133.16.

EUR/JPY Key Technical Levels

- USD/CAD bulls take a breather after posting the biggest daily jump in a week.

- Oil prices remain pressured amid hopes of more output, recession fears.

- US dollar cheers market’s rush to risk-safety ahead of Wednesday’s key inflation data.

- BOC is up for a heavy rate hike in its fourth consecutive hawkish move.

USD/CAD seesaws around the 1.3000 psychological magnet after rising the most in a week as buyers struggle for fresh directions during Tuesday’s Asian session. The Loonie pair portrayed the broad risk-off mood, as well as softer oil prices, to begin the key week comprising the US inflation data, as well as the Bank of Canada (BOC) monetary policy meeting.

A jump in the US inflation expectations and comments from the US policymakers suggesting more pain ahead escalated the fears of economic slowdown, which in turn propelled the market’s rush towards risk safety. Also adding to the risk-off mood, as well as to the broad US dollar strength, were Friday’s upbeat US employment data and geopolitical/trade fears. It should be noted that the weakness in the oil prices, amid recession woes and expectations of higher output, offers extra support to the USD/CAD bulls, due to Canada’s reliance on crude oil export.

That said, one-year US inflation expectations jumped to the record high of 6.8% in June, versus 6.6% prior, per the NY Fed’s survey of one-year-ahead consumer inflation expectations. The inflation expectations followed strong US employment data, published Friday, to underpin hopes of an aggressive Fed rate hike and fuelled concerns over the health of the US economy, as well as the global ones. That said, the latest US jobs report mentioned that the US Nonfarm Payrolls (NFP) rose by 372K for June, versus expected 268K and downward revised 384K prior.

On a different page, White House Press Secretary Karine Jean-Pierre told reporters that she expects new Consumer Price Index (CPI) data to be highly elevated. Further, Atlanta Fed President Raphael Bostic said that recent inflation data has not been as encouraging as I would have liked, per Reuters.

Elsewhere, WTI crude oil keeps the week-start losses around $100.30, down 0.80% intraday, as fears of softer demand due to the global economic slowdown fears join the chatters that US President Joe Biden will push for greater oil output during his trip to the Middle East, starting from Tuesday.

Amid these plays, equities and were lower while the S&P 500 Futures remains directionless by the press time.

Moving on, risk catalysts could be of importance to the USD/CAD traders amid a light calendar at home. However, major attention will be given to Wednesday’s BOC meeting as the Canadian central bank is up for a heavy rate hike of 0.75% during its fourth attempt to tame inflation.

Technical analysis

USD/CAD struggles for clear directions between a two-month-old resistance line and an upward sloping support line from June 08, respectively around 1.3085 and 1.2925. That said, RSI (14) hints at a gradually rising bullish bias.

- The cable has given a downside break of the symmetrical triangle that signals more downside.

- Declining 20- and 50-period EMAs add to the downside filters.

- The RSI (14) has shifted into the bearish range of 20.00-40.00, which signals more pain ahead.

The GBP/USD pair is displaying topsy-turvy moves in a narrow range of 1.1882-1.1897 in the Asian session. The cable has shown a mild consolidation after a vertical downside move. The asset tumbled significantly on Monday after surrendering the psychological support of 1.2000. The asset is hovering around the fresh two-year low at 1.1866.

On the four-hour scale, the cable has given a downside break of the symmetrical triangle. The downward-sloping trendline of the above-mentioned pattern is plotted from July 4 high at 1.2161 while the upward-sloping trendline is placed from Wednesday’s low at 1.1876. Also, the horizontal resistance placed from June 14 at 1.1934 will remain a critical resistance for the cable.

Declining 20- and 50-period Exponential Moving Averages (EMAs) at 1.1970 and 1.2027 respectively signal that the downside is still far from over.

Also, the Relative Strength Index (RSI) (14) has shifted into the bearish range of 20.00-40.00, which adds to the downside filters.

The cable is expected to display more losses if the asset drops below Monday’s low at 1.1866. An occurrence of the same will drag the asset to the round-level support of 1.1800, followed by a 26 March 2020 low at 1.1777.

Alternatively, a decisive move above Friday’s high of 1.2056 will send the asset towards July 4 high at 1.2161. A breach of the latter will drive the cable towards June 28 high at 1.2292.

GBP/USD four-hour chart

-637931769434471212.png)

White House Press Secretary Karine Jean-Pierre told reporters that she expects new Consumer Price Index (CPI) data to be highly elevated.

Her comments escalate inflation woes ahead of Wednesday’s US CPI release for June, expected 8.8% YoY versus 8.6% prior.

It’s worth noting that the US inflation expectations jumped to the record high of 6.8% in June, versus 6.6% prior, per the NY Fed’s survey of one-year-ahead consumer inflation expectations.

On the same line, Atlanta Fed President Raphael Bostic said that recent inflation data has not been as encouraging as I would have liked, per Reuters.

FX implications

The inflation fears weigh on the market sentiment and fuel the US dollar due to its safe-haven appeal, also drowning the commodities and Antipodeans.

Also read: NZD/USD bears attack 0.6100 at two-year low amid inflation/recession fears, RBNZ eyed

“US President Joe Biden will make the case for greater oil production from OPEC nations to bring down gasoline prices when he meets Gulf leaders in Saudi Arabia this week, White House national security adviser Jake Sullivan said on Monday,” reported Reuters.

Key quotes

Biden leaves Tuesday night on his first visit to the Middle East as president, with stops in Israel, the occupied West Bank and Saudi Arabia on his agenda.

Sullivan said members of the Organization of the Petroleum Exporting Countries (OPEC) have the capacity to take ‘further steps’ to increase oil production despite suggestions from Saudi Arabia and the United Arab Emirates that they can barely increase oil production.

Experts say the White House understands Saudi Arabia is unlikely to move unilaterally and that Riyadh and other Gulf nations lack significant spare capacity.

In a commentary published in the Washington Post late on Saturday, Biden said his aim was to reorient and not rupture relations with a country that has been a U.S. strategic partner for 80 years.

Iran is expected to be discussed on the trip in a region nervous about Tehran's influence.

Sullivan said the United States believes Iran is preparing to provide Russia with up to several hundred drones, including some that are weapons capable, for use in its war against Ukraine.

FX implications

WTI crude oil remains pressured around $100.60, extending the week-start retreat, as recession fears join expectations of more output.

- NZD/USD stays depressed at the lowest levels since May 2020.

- Fears of higher inflation increase the odds of recession and underpin USD’s safe-haven demand.

- China’s covid woes, geopolitical/trade chatters also exert downside pressure on the pair.

- RBNZ is expected to lift interest rates by 0.50% on Wednesday, no major data/events appear interesting ahead of that.

NZD/USD struggles to defend the 0.6100 threshold, after refreshing the 26-month low as risk-aversion propelled the US dollar, amid early Tuesday morning in Asia. The Kiwi pair’s latest weakness could be linked to the market’s fears of recession and cautious mood ahead of Wednesday’s monetary policy decision of the Reserve Bank of New Zealand (RBNZ). It’s worth noting that hardships for China, the world’s biggest industrial player and New Zealand’s key customer, also drown the quote.

One-year US inflation expectations jumped to the record high of 6.8% in June, versus 6.6% prior, per the NY Fed’s survey of one-year-ahead consumer inflation expectations. The inflation expectations followed strong US employment data, published Friday, to underpin hopes of an aggressive Fed rate hike and fuelled concerns over the health of the US economy, as well as the global ones. That said, the latest US jobs report mentioned that the US Nonfarm Payrolls (NFP) rose by 372K for June, versus expected 268K and downward revised 384K prior. Further, the Unemployment Rate matched market expectations of reprinting 3.6% level. Further details suggest that the annual wage inflation, as measured by the Average Hourly Earnings, edged lower to 5.1% from 5.3% in May and the Labor Force Participation declined to 62.2% from 62.3.

It’s worth noting that Kansas City Federal Reserve President Esther George recently raised concerns over recession while saying, “Recession projections suggest to me that rapid rate hikes risk tightening faster than the economy and markets can adjust,” per Reuters.

Elsewhere, Shanghai’s first coronavirus Omicron sub-variant BA-5 case escalated virus woes after the dragon nation failed to sustain the unlock activities. It should be noted that firmer inflation data from the Asian major and doubts over Beijing’s GDP goal, as well as on the stimulus’ ability to renew optimism, exert additional downside pressure on the market sentiment.

Amid these plays, equities and US Treasury yields began the week on a back-foot while the yield curves kept signaling recession fears.

Considering these catalysts, analysts at the Australia and New Zealand Banking Group said, “We expect the RBNZ to be hawkish tomorrow (they can’t afford not to be), but in a world of dollar dominance that may not do a lot for the beleaguered Kiwi, especially amid NZ recession fears.”

Technical analysis

Oversold RSI (14) joins a one-month-old descending support line to restrict short-term NZD/USD declines around 0.6100. However, corrective pullback remains elusive unless crossing a downward sloping resistance line from June 16, close to 0.6215 by the press time.

- AUD/USD is hovering around monthly lows at 0.6715, downside remains warranted on risk-off impulse.

- Volatile energy and food products are still guiding the US CPI higher despite policy tightening measures.

- Aussie’s jobless rate may decline to 3.8% vs. 3.9% reported prior.

The AUD/USD pair has turned sideways after a sheer downside move to Monday’s low at 0.6715 on a risk-off impulse on the market. The asset is hovering around its fresh monthly low as the US dollar index (DXY) has printed a fresh 19-year high at 108.27.

The DXY extended its gains beyond the prior high of 107.79 on a higher consensus for US Inflation. A preliminary estimate for the plain-vanilla Consumer Price Index (CPI) is 8.7%, higher than the print of 8.6%. While the core CPI may settle lower to 5.7%.

The core CPI doesn’t include fossil fuels and food products and is seen lower, however, the annual CPI that includes the duo is seen higher. This indicates that the volatile energy bills and food items are still guiding the inflation rate significantly despite the deployment of policy restrictive measures by the Federal Reserve (Fed).

Apart from the US CPI, investors will also focus on the US Retail Sales this week. The economic data is seen meaningfully higher at 0.8% than the prior print of -0.3%.

On the aussie front, investors are keeping an eye on the employment data, which is due on Thursday. The Employment Change is expected to land at 25k, less-than-half than the prior release of 60.6K. However, the Unemployment Rate will slip to 3.8% vs. 3.9% reported previously.

- The AUD/JPY edges lower as the Asian session begins, almost flat during the day.

- Risk-aversion favors AUD/JPY downside, though support levels at around and below 92.00 might cap selling pressure.

- A break of a falling wedge might send the pair towards 97.00 before correcting towards 93.30s.

The AUD/JPY tumbles after recording two days of gains blamed on a gloomy market mood spurred by investors positioning ahead of the US inflation readings, China’s coronavirus reemergence, and broad safe-haven strength across the board.

At 92.55, the AUD/JPY lost almost 0.80% on Monday’s session, in which the pair began trading near the pivot point of the day, around 93.20. Then the cross rallied shy of 93.70, plunging afterward towards the daily lows around 92.30, finally settling down around current levels.

AUD/JPY Daily chart

The AUD/JPY depicts the formation of two different wedges, one rising and inside of it, another one falling. The former suggests that the AUD/JPY might be headed downwards, while the latter indicates that buying pressure remains, so the cross-currency pair still has another leg up.

The AUD/JPY price action is very close to the top trendline of the falling wedge, so that's the first scenario to discuss. If that plays out, the AUD/JY would break upwards, aiming toward its measured target profit right at the top-trendline of the rising wedge, around the 97.20-50 range.

Once that is achieved, the AUD/JPY might correct towards the bottom-trendline of the rising wedge and could probably break immediately, targeting 86.00, or print a subsequent leg-up at fresh YTD highs around 98.05 before plummeting towards the bottom-trendline of the wedge, followed by a break targeting 87.00.

AUD/JPY Key Technical Levels

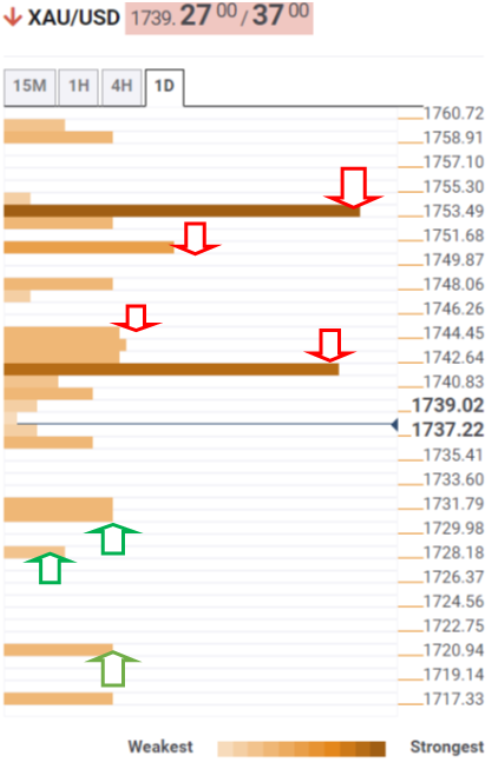

- Gold price is looking to come out of the woods by surrendering the critical support of $1,730.00.

- The DXY has printed a fresh 19-year high at 108.27 on expectations for higher US Inflation.

- Soaring expectations for lower earnings by the corporate have underpinned the risk-off market mood.

Gold price (XAU/USD) has established below $1,740.00 but is still inside the woods. The precious metal is witnessing back-and-forth moves in a range of $1,730.73-1,752.49 from the past three trading sessions. The bright metal is displaying subdued performance and the volatility prior to the release of the US Consumer Price Index (CPI) is expected to drag the asset below the critical support of $1,730.00.

As per the market consensus, the plain-vanilla CPI is seen minutely higher at 8.7% than the prior release of 8.6%. However, the core CPI that excludes food products and oil prices may drop to 5.7% vs. 6% reported earlier. This signifies that durable goods, automobiles, and other commodities are displaying the impact of policy restrictive measures, which have adopted by the Federal Reserve (Fed) earlier. However, the volatile food and fossil fuels are still not responding.

Meanwhile, the US dollar index (DXY) printed a fresh 19-year high at 108.27 on Monday amid a souring market mood. Escalating odds for one more bumper rate hike by the Fed are bolstering the case for lower earnings by the corporate. The unavailability of cheap money in the economy has forced the corporate sector to put an extra lens on investment opportunities.

Gold technical analysis

On an hourly scale, the gold prices are on the verge of giving a downside break of the consolidation formed in a $1,730.73-1,752.49 range. The 20- and 50-period Exponential Moving Averages (EMAs) at $1,737.04 and $1,740.86 respectively have started declining, which adds to the downside filters. Also, the Relative Strength Index (RSI) (14) is looking to surrender the cushion of 40.00 to add volatility to the counter.

Gold hourly chart

- EUR/USD moves closer to the parity level as bears commit.

- The US CPI will be a key catalyst this week that might either put 1.0100 back on the map or potentially result in a break of parity.

EUR/USD has come to its closest to parity in 20 years. At the turn of the roll-over and start of the Tuesday early Asian session, the pair had made a low for the week so far of 1.0037. Crucially, this is below the 1.0050 level and bears are going to be hunting down tepid pullbacks in a draw on liquidity for a move to challenge the bull's commitments below parity.

The US dollar has risen on safe-haven demand and the euro is under pressure due to concerns that an energy crisis will force the eurozone into a recession. Reuters reported that the biggest single pipeline carrying Russian gas to Germany, the Nord Stream 1 pipeline, began annual maintenance on Monday, with flows expected to stop for 10 days. ''Governments, markets and companies are worried the shutdown might be extended because of the war in Ukraine.''

Stocks were also under pressure as markets move out of risk ahead of the highly anticipated inflation reading from the US this week and the start of a key earnings season fuelling a bid in the greenback as for fears of a recession. ''Core prices likely stayed strong in June, with the series registering a 0.5% MoM gain,'' analysts at TD Securities said. ''Our MoM forecasts imply 8.9%/5.7% yoy for total/core prices.''

Meanwhile, net EUR speculators’ net short positions increased again last week as the market turned its attention to recession risks for the Eurozone, as analysts at Rabobank pointed out. ''This is linked to potential gas shortages during the winter and fears that industry may suffer rationing. This scenario is likely to focus the market on fragmentation risks.''

EUR/USD technical analysis

The pair is in a bearish channel and below 1.0050. This puts the emphasis on the downside. However, the M-formation is a bullish reversion pattern and a confluence with the bear-channel resistance, the 38.2% Fibonacci retracement level and the 50% mean reversion area is compelling above 1.0050.

If the bulls commit, there will be the case for a period of either accumulation that could result in a move back to 1.0100 and above, or, so long as the bears commit below this area of confluence, then a break of parity will be back on the cards for the days ahead.

- USD/JPY has been a head-turner at the start of the week.

- The pair has rallied to fresh bull cycle highs, but corrections are anticipated.

The US dollar soared to a 24-year high on the yen following Japan's ruling conservative coalition's strong election showing indicated no change to loose monetary policies. This has seen the pair move deeper into blue skies making analysis to the upside a tricky task. 109.77 is the Sep 2002 high in the DXY which leaves plenty of room for USD/JPY to move higher.

The dollar has already climbed to as high as 137.75, its firmest since late 1998. However, corrections are anticipated along the way and the following illustrates the potential trajectory for the pair on a multi-timeframe basis:

USD/JPY monthly chart

The pair is showing no signs of slowing and it is feasible for it to add to today's gains this week. But the question is how far can this run before pulling back?

USD/JPY daily chart

The bulls have taken out prior highs following a higher low. The old highs come as new support.

USD/JPY hourly chart

We have a classic impulse, correction and expected fresh impulse stacking up on the hourly chart with the price holding above prior highs and having made a deep 38.2% Fibonacci correction.

However, the downside cannot be ruled out given the break of the supporting trendline.

USD/JPY 15 min chart

If the downside were to play out, it could look something like the above with price imbalances, the grey boxes, being mitigated along the way as price targets.

- The USD/CAD buyers regain control and lift the pair above 1.3000, eyeing 1.30776.

- Decreased risk appetite and investors’ positioning ahead of the US CPI to keep the USD/CAD upward pressured.

- The Bank of Canada (BoC) is expected to hike rates by 75 bps, as shown by STIRs futures.

The USD/CAD snaps three days of consecutive losses and bounces off last week’s lows around 1.2930s due to a stronger greenback, bolstered by investors positioning ahead of a US inflation reading expected to remain hot and China’s coronavirus reemergence, particularly in Shanghai, threatening to derail the global economic growth.

After reaching a daily high at around 1.3030s, 100 pips up from the daily lows, the USD/CAD is trading at 1.3002, gaining some 0.51% during the North American session at the time of writing,

USD/CAD rises on risk-aversion and falling oil prices

Stocks slid while the greenback remains in the driver’s seat, as shown by the US Dollar Index, rallying more than 1%, printing a fresh YTD high at around 108.211, while US Treasury yields fell on safe-haven appetite. Those factors, alongside falling US crude oil prices with WTI trading at $103.68 BPR, are a headwind for the loonie, which trimmed last week’s losses since last Wednesday.

In the week, the Canadian economic calendar illustrated that the Bank of Canada (BoC) would have its monetary policy meeting, where the bank is expected to hike rates from 1.50% to 2.25%, a 75 bps. Money market futures STIRs, priced in a 99.8% chance of a 0.75% rate increase, while odds of a 1% upward move sit at 74.9%.

Analysts at TD Securities wrote in a note that the BoC Business and Consumer Surveys provided new evidence of rising inflation expectations, further cementing the case for a 75 bps rate hike. Additionally, “With the economy operating in excess demand and inflation running well above the target, we see little room for nuance at the upcoming meeting and look for a broadly hawkish tone.”

Furthermore added that “The policy statement should also repeat that rates need to rise further and that the Bank is prepared to act more forcefully if needed.”

On the US front, the US economic calendar is packed, reporting that US inflation readings for consumers and producers, with both numbers estimated at the top of the range. Late in the week, US Retail Sales are expected to be higher, and the University of Michigan Consumer Sentiment would be in the spotlight after June’s figures triggered a market shift and weighed on the Federal Reserve rate hike decision, according to some Fed speakers.

USD/CAD Key Technical Levels

What you need to take care of on Tuesday, July 12:

The American dollar reached fresh highs against most major rivals, as the week started in risk-off mode. News coming from China spurred the dismal mood, as inflation in the country surged by 2.5% YoY in June, above the market’s expectations. Furthermore, Shanghai officials reported the first case of the coronavirus Omicron sub-variant BA-5, spurring concerns of a new lockdown in the region just a few weeks after the end of a month-long isolation mandate.

The EUR/USD pair trades in the 1.0040 price zone, its lowest since December 2002. The shared currency is under additional pressure amid an energy crisis. As expected, Russia closed the Nord Stream 1 pipeline for maintenance, although Germany fears it would not reopen it.

The GBP/USD pair trades below 1.1900. The UK’s Conservative 1922 Committee announce that nominations to replace Boris Johnson as Prime Minister will open and close on Tuesday. They would have successive ballots until they reach the final two, which could happen early in the next week. Finally, the results will be announced on September 5.

Global equities fell ahead of earnings reports and US inflation figures.

The Australian dollar weakened against its American rival, with AUD/USD trading near a fresh 2-year low of 0.6713. The greenback advanced against the CAD, but USD/CAD remains within familiar levels and trades around 1.3000.

The USD/JPY pair surged to a fresh multi-year high of 137.74, holding nearby despite volatile action among government bonds. Nevertheless, and despite back and forth, the US yield curve remains inverted, hinting at an upcoming recession.

Gold weakened by the end of the day, now trading at around $1,731.00 a troy ounce. Crude oil prices remained stable, with the barrel of WTI now at $103.65.

Like this article? Help us with some feedback by answering this survey:

- GBP/USD bulls start to move in following a significant sell-off.

- The price is correcting into an M-formation's neckline on the 4-hour chart.

GBP/USD is pressured at around 1.1900, losing some 1% on the day following a move higher in the greenback that has sunk all ships. The US dollar gained 1% against a basket of six major currencies, reaching 108.191, the strongest since October 2002, DXY.

The expectation is that the Federal Reserve will continue to aggressively raise rates as it tackles soaring inflation which is supporting the currency ahead of this week's US Consumer Price Index data. The Fed is expected to lift rates by 75 basis points at its July 26-27 meeting. Fed funds futures traders are pricing for its benchmark rates to rise to 3.49% by March, from 1.58% now.

The inflation data that is due on Wednesday is this week’s major US economic focus and economists polled by Reuters expect the index to show that consumer prices rose by an annual rate of 8.8% in June. For the UK, growth data will be important. Analysts at TD Securities expect Gross Domestic Product to fall for the third consecutive month as the cost-of-living crisis continues to weigh on household spending. ''We look for a 0.2% decline in services (mkt: +0.1%) and a 0.3% m/m fall in manufacturing (mkt: 0.0%). This would confirm our view that the UK essentially is already in a recession—even though erratics might save it from one in a technical sense.''

Bank of England Governor Andrew Bailey said on Monday that he thought the BoE's most recent forecast for inflation, showing it was likely to fall sharply next year, remained valid.

"I always go into forecasts with an open mind, and that's critical, but I think the basic fundamentals of that profile remain in place today," the top central banker told lawmakers. ''Inflation was likely to be back at its 2% target in around two years' time, he added.

Meanwhile, net short GBP positions have increased moderately last week counter to the recent trend. ''More political scandal had begun to descend on UK PM Johnson at the start of last week which culminated in his resignation. Looking ahead, hopes of a more coherent government are likely to mingle with uncertainties about the policies of Johnson’s successor, suggesting that GBP may lack direction near term,'' analysts at Rabobank explained.

GBP/USD technical analysis

Friday's London session lows of 1.1920 are in sight for the immediate future:

The price has pierced the round 1.1900 level, but the tied is turning which leaves the buys stops above vulnerable with the 38.2% Fibonacci in confluence with the neckline of the M-formation, Friday's London sesison lows and a price imbalance in the hourly chart between the 1.1920/30s.

- The three major US equity indices plunge between 0.29% and almost 2%.

- Risk-aversion dominates Monday’s trading session, on China’s covid-19 fears and high inflation reducing corporate profits as the earnings session looms.

- Fed’s George worried that faster rates would be harmful to the economy.

- Fed’s Bullard commented that the US economy is solid and can withstand higher rates.

US stocks snapped five days of consecutive gains, trading lower on Monday, courtesy of risk aversion and fears that earnings would miss expectations due to the deteriorating economic outlook, spurring an appetite for safe-haven assets

At the time of writing, the S&P 500 sits at 3863.20, falling 0.93%, while the heavy-tech Nasdaq tumbles by 1.86% at 11,420.73. In the meantime, the Dow Jones Industrial slumps 0.29%, sitting at 31,246.41

Sector-wise, the leading sectors are Utilities, up by 0.37%, followed by Real Estate and Health, each recording gains of 0.20 % and 0.02%, respectively. As the appetite for riskier assets diminished, the biggest losers were Communication Services, Consumer Discretionary, and Technology, plummeting 2.59%, 2.31%, and 0.96% each.

Stocks fell due to renewed worries about China’s Covid-19 resurgence and tumbling commodity prices. Corporate America will begin earnings season late in the week, which could signal a high inflation impact on businesses. The US economic calendar will reveal inflation among consumers and producers, US Retail Sales, and the University of Michigan (UoM) Consumer sentiment.

In the meantime, Fed speakers crossed newswires, led by Kansas City Fed President Esther George, who said that “moving interest rates too fast raises the prospect of oversteering.” George said she agreed that hiking rates faster to dampen inflation, though she expressed concerns that it could harm the economy. Later, the St. Lous Fed President James Bullard reiterated that the US economy is solid and can handle higher rates while backing a 75 bps rate hike for the July meeting.

The US Dollar Index (DXY), a measurement of the greenback’s value against some currencies, rallies 1.04% to 108.003, while the 10-year US Treasury yield losses some ground dropping nine basis points, yielding 2.993%.

The US crude oil benchmark in the commodities complex, WTI drops 0.70%, exchanging hands at $104.05 BPD. Meanwhile, precious metals like gold (XAU/USD) drop 0.47%, trading at $1734.20 a troy ounce.

SP 500 Chart

Key Technical Levels

- The USD/CHF is upward biased, but the change of posture of the Swiss National Bank (SNB) from dovish to hawkish could cap USD/CHF rallies toward the YTD high.

- USD/CHF Price Analysis: The daily and 1-hour charts illustrate an upward bias in the pair, so any pullbacks are better opportunities for buyers to step in.

The USD/CHF advances firmly on Monday amidst traders’ risk-off sentiment, which bolstered the greenback. However, last month’s Swiss National Bank (SNB) sudden shift towards a hawkish posture put a lid on the USD/CHF climb, retreating from daily highs around 0.9840.

The USD/CHF is trading around the 0.9790s region and remains positive in the day, up by 0.33% amidst a risk-aversion trading day.

USD/CHF Daily chart

The USD/CHF is still in an uptrend, as depicted by the daily chart. However, some selling pressure emerged between the 0.9800-0.9900 range, dragging prices lower, below last Friday’s daily high at 0.9797. Oscillators remain in bullish territory, like the Relative Strength Index (RSI) at 60.67, with room to spare before reaching overbought conditions. Therefore, the USD/CHF path of least resistance will continue upwards.

That said, the USD/CHF first resistance will be 0.9800. A breach of the latter will send the major towards July 11 high at 0.9843, followed by May 23, 2020, daily high at 0.9901.

USD/CHF 1-Hour chart

The USD/CHF shows an upward trajectory, aligned with the USD/CHF higher time-frame (HT), being the daily chart. Nevertheless, the rally stalled around the R2 daily pivot, and subsequent pullbacks should be bought, as the major would continue to the upside. USD/CHF traders should be aware that the Relative Strenght Index (RSI) in this time frame, as the pair rallies and retraces, the RSI’s has been seesawing within the 50-70 boundaries without reaching overbought conditions, meaning the uptrend is solid.

Hence, the USD/CHF first resistance would be the R1 pivot point at 0.9800. The break above would expose the R2 daily pivot at 0.9835, followed by the daily high around 0.9843.

USD/CHF Key Technical Levels

- The gold bears have taken charge at the start of the week on a stronger US dollar ahead of more critical US events.

- The neckline of the H4 M-formation near $1,740 remains vulnerable to a test and break thereof.

- A move beyond $1,740 will open the risk of a run on the highs of Friday through $1,750 and then $1,759.60.

The gold price has been pressured by a resurgence in the greenback at the start of the trading week. The US dollar has torn through last week's highs and had denied the bears in the forex space that were in anticipation of corrections. At the time of writing, DXY, a measure of the US dollar vs. a basket of major currencies is up by over 1% and oscillates around 108 the figure.

Spot gold is moving in on the prior lows, July 8, of $1,729.98. It has made a low of $1,733.92 so far on the day and is currently down by 0.48% at $1,734.09. Sentiment had been brewing, supportive of gold, that the market may have over-estimated the extent to which the Federal Reserve will hike rates this cycle. However, a stronger than expected US June Nonfarm Payrolls report has reinforced expectations for another 75 bp Fed rate hike in July which is giving rise to demand in the greenback at the open before more critical US data this week.

Key US calendar events

The main event will be the publication of June’s consumer Price Index report. Analysts at the National Bank of Canada argue that ''the food component likely remained very strong given severe supply constraints globally, and this increase may have been compounded by sharply higher gasoline prices. As a result, headline prices could have increased 1.2% MoM, lifting the year-on-year rate to a 40-year high of 8.8%.''

US Retail Sales will also be important. A recovery in June is expected, following the series' first contraction this year in May. ''Spending was likely aided by another firm showing in gasoline station sales and a rebound in the auto segment,'' analysts at TD Securities said. ''We also look for another gain in the eating/drinking segment as consumers continue to transition away from goods. That said, control group sales likely fell again.''

Meanwhile, the analysts at TDS are highly bearish on the precious metal. Noting that ''gold bugs are falling like dominoes, with selling flow spreading across participants as CTA trend followers join into the vacuum'' they add that ''a major capitulation event may be unfolding in gold.''

''We see evidence that the steepest outflows from broad commodity funds since the Covid-19 crisis may be catalyzing a series of cascading liquidations from various speculative groups. This argues for substantial downside for gold in the coming sessions as participants are forced to sell in a vacuum.''

Gold technical analysis

The price action in gold has started to erode a pre-market-open corrective bias analysis on the 4-hour charts.

The spring was identified at around $1,730. However, the market is moving in on this level, so while it still remains valid until it is breached, the price behaviour at the start of this week is putting the bullish thesis in jeopardy. With that all being said, the M-formation is a bullish reversion pattern that could be the bulls get of jail free card:

The spring will still be intact if the bulls continue to correct into the neckline of the M-formation near $1,740. A move beyond there will open the risk of a run on the highs of Friday through $1,750. This will then expose the vulnerability of the price imbalance between there and $1,759.60. On the downside, a break of the lows opens the risk of another significant sell-off towards the monthly lows of $1,676.

- The white metal remains downward biased but appears to have found a base around $19.00.

- Safe-haven flows toward the greenback, and US Treasuries keep the precious metals complex under pressure.

- The US 2s-10s yield curve is still inverted, flagging recession fears.

Silver (XAGUSD) is subdued during the North American session, seesawing for the fourth consecutive day in a narrow $19.13-37 area. The white metal remains downward biased, pressured by a buoyant greenback, higher US Treasury yields, and risk aversion on investors’ uncertainty about the economic outlook.

The XAGUSD is trading at $19.19, near the daily pivot point around $19.26, down 0.61%, while the US Dollar Index, a measure of the greenback’s value against a basket of peers, sits at 107.949, up 0.98%. US Treasury yields are down, led by the 10-year benchmark note rate at 2.991%, dropping ten bps, while the US 2s-10s yield curve stays inverted for the fifth consecutive day, at -0.052%.

A risk-off impulse and US dollar flows drag precious metals down

Risk aversion dominates Monday’s session as global equities drop. China’s covid resurgence, the release of US inflation figures, and recession fears keep the king dollar intact. Shanghai reported a new coronavirus variant, while Macau shut off its business and casinos at least for one week.

In the meantime, the US economic calendar featured Fed speakers. The Kansas City Fed President Esther George said, “moving interest rates too fast raises the prospect of oversteering.”. George, a dissenter in the last meeting, who opposed a 75 bps, said that she agreed about hiking rates faster to dampen inflation, though expressed concerns that it could harm the economy.

Later the St. Lous Fed President James Bullard reiterated that the US economy is solid and can handle higher rates while backing a 75 bps rate hike for the July meeting.

What to watch

The week ahead, the US economic docket will feature the US Consumer Price Index, Retail Sales, PPI, and the University of Michigan Consumer Sentiment.

Silver (XAGUSD) Key Technical Levels

Emerging market currencies are under pressure on Monday; the USD/BRL is up by 1.85% at 5.35. Since June, the pair has been rising constantly. Analysts at Rabobank see the USD/BRL ending the year around 5.25.

Key Quotes:

“After the Fed released the latest FOMC meeting’s minutes, two Fed hawks said they would slow pace after July’s meeting decision while June’s payrolls surprise to the upside again. Domestically, June’s CPI inflation starts to show the temporary fuel-taxes cut impact of the recently approved PLP18 bill, but the key vote on the social benefits bill was postponed to next week. Over the week, the DXY dollar index appreciated 1.8%, the USDBRL ended up appreciating 1.5% (although it closed the week at 5.2559, the same level of 30 June), the Ibovespa rose 1.4%, while the local inverted yield curve steepened.”

“We still see a 50-bp hike at the August meeting, then likely staying put until yearend. Even though we expect a longer Selic hiking cycle than at the beginning of 2022, we believe the Fed’s recent display of hawkishness and the intensification of the traditional electoral cycle will end up weighing on the BRL and other local assets going forward. By year-end we expect the BRL to trade at 5.25.”

The EUR/USD hit new cycle lows on Monday at 1.0050 as it continues to approach parity. The next half of 2022 is unlikely to foster conditions for euro appreciation as the European economy could be in a technical recession, explained analysts at National Bank of Canada. They expect the euro to remain low in the near term and will require improvements for energy prices and supply to catch a bid.

Key Quotes:

“The first half of 2022 can only be described as eventful for the Eurozone. The common currency area has faced spiking energy prices, a war on its borders and surging inflation. The aforementioned factors have given no traction to the euro, the latter having slipped from 1.14 at the end of 2021 to nearly parity (1.01) as of this writing.”

“The next half of 2022 is unlikely to foster conditions for euro appreciation as the European economy could be in a technical recession. Some of the recent euro weakness can be retraced to the ECB emergency meeting on the 15th of June. The spread between an Italian and German 10y bond had reached 240 basis points, prompting serious discussions. The central bank promised an anti-fragmentation tool to help alleviate supposedly unjustified interest-rate spreads.”

“Altogether, the picture for the European economy is far from rosy and it may already be in the throes of a technical recession. As such, we expect euro to remain low in the near term and will require improvements for energy prices and supply in order to catch a bid.”

While testifying before the UK Treasury Select Committee on Monday, Bank of England (BOE) Governor Andrew Bailey argued that they should not pre-commit to the next policy move and said they have a range of options for the August meeting.

Key takeaways via Reuters

"UK is facing a very big real income shock."

"We need to assess how much real income shock will bring down inflation itself."

"We expect inflation to be back to target in around two years, other things being equal."

Market reaction

These comments failed to help the British pound find demand and the GBP/USD pair was last seen losing 1.1% on a daily basis at 1.1895.

- The Mexican peso resumes the decline versus the dollar.

- USD/MXN likely to rise further while above 20.70.

- USD/COP and USD/CLP hit record highs.

After a two-day correction, the USD/MXN resumed the upside and jumped to 20.78, matching the July high. A stronger US dollar across the board boosted the pair on Monday as risk aversion prevails.

In Wall Street, the Dow Jones is falling by 0.38% and the Nasdaq slides by 2.01%. US yields are sharply lower as the demand for Treasuries strengthens as investors look for safety.

Emerging markets under pressure

Stocks are also falling in Emerging Markets. Mexico’s IPC drops 0.51%, Brazil’s Bovespa tumbles 1.70%. Among currencies, the Chilean peso and the Colombian peso hit a new record low. USD/CLP traded above 1,000 and the USD/COP above 4,500 for the first time. The USD/BRL (Brazilian real) is up 1.78% at 5.34.

The negative global growth outlook and higher interest rates contribute to keep driving the dollar higher versus EM currencies, including the Mexican peso.

The USD/MXN is testing the July high and as long as it remains above 20.70 more gains seem likely. The next resistance is located at 20.90, the last defence to 21.00. On the flip side, a decline back below 20.45 would alleviate the bullish pressure.

Technical levels

- US Dollar rises across the board on risk aversion.

- DXY hits the highest level since October 2002.

- NZD/USD unable to regain 0.6200 and breaks the 0.6130 support.

The NZD/USD is falling on Monday and it printed a fresh two-year low at 0.6096, before trimming losses to 0.6130. The pair is under pressure amid risk aversion that continues to boost the US dollar.

The greenback, measured by the DXY, hit a fresh 19-year high above 108.00. The move took place even as US yields tumble. The US 10-year stands at 2.98%, down more than 3% while the 30-year is at 3.16%. In Wall Street, the Dow Jones falls by 0.32% and the Nasdaq by 1.85%.

Concerns about the economic outlook continue to weigh on market sentiment. New COVID-19 restrictions in China added to fears about global growth.

Regarding economic data, the focus is set on the June US CPI due on Wednesday. Earlier that day, the Reserve Bank of New Zealand will announce its decision on monetary policy. A 50 basis points rate hike to tame inflation is expected.

Breaking support

The NZD/USD dropped below the 0.6130 strong support area. If the pair consolidates below, more losses seem likely. A recovery back above could alleviate the pressure, favoring a return to the 0.6200/0.6130 range.

Technical levels

- On Monday, the AUD/USD nosedives mainly on risk-aversion spurred by China’s Covid-19 resurgence.

- US economic data and Fed speakers to remain in the driver’s seat throughout the week; US inflation and consumer sentiment watched.

- AUD/USD Price Analysis: Tilted to the downside, and a break below 0.6700, would expose May 2020 swing lows in the 0.6400-0.6600 area.

The AUD/USD is plunging in the North American session, in which the major reached a daily high of around 0.6854, diving to fresh two-year lows under 0.6730s, amidst China’s coronavirus reemergence, recession fears, and risk aversion.

The AUD/USD is trading at 0.6744, down almost 1.80%, slightly up from the daily lows at 0.6714, in the mid-0.6730-40s. in the meantime, the US Dollar Index, a gauge of the buck’s value vs. six currencies remains trading at 20-year highs around

AUD/USD tanks on safe-haven plays, falling commodity prices

The sentiment is downbeat as global equities fall. The AUD/USD stays on the defensive, adrift to investors’ mood, amidst the lack of economic data. In the week, the US economic calendar will be busy reporting that US inflation – consumer and producer based – is expected to rise. After that, US Retail Sales are expected to be higher, while the University of Michigan Consumer Sentiment could be in the spotlight after June’s figures triggered a market shift and weighed on the Federal Reserve rate hike decision. Meanwhile, money market futures odds of a Fed's 75 bps rate hikes are fully priced in at a 99% chance.

In the case of Australia, the Aussie remains heavy also on lower commodity prices. The Iron Ore price is down 1.22%, at 113.74 a ton, contrarily to the Bloomberg Commodity Index, up by a decent 0.22%. With the Reserve Bank of Australia (RBA) decision in the rearview mirror, the Australian economic docket will feature June’s Business and Consumer Confidence, alongside employment data.

Newswires reported that Kansas City Esther George crossed wires. She said that the speed of rates should be questioned, adding that raising rates too fast risks “oversteering.”

AUD/USD Price Analysis: Technical outlook

The AUD/USD daily chart depicts the pair as downward biased. Confirmation of the previously mentioned is the exchange rate below 0.7000, the daily moving averages (DMAs) above the spot price, and the Relative Strength Index (RSI) in bearish territory, crossing below the RSI’s 7-day SMA, a sell signal.

That said, the AUD/USD first support would be May 27, 2020, high at 0.6680. Break below will expose May 22, 2020, low at 0.6505, followed by May 15, 2020, daily low at 0.6402.

The Federal Reserve Bank of New York's monthly Survey of Consumer Expectations showed on Monday that the US Consumers' one-year inflation expectations rose to 6.8% in June from 6.6% in May. The three-year inflation expectations, however, declined to 3.6% from 3.9%.

Key takeaways as summarized by Reuters

"Consumers see home prices up 4.4% in the next year, down from 5.8% in May."

"Consumers' year-ahead earnings growth expectations were unchanged in June at 3%."

"Consumers' median 1-year household income growth expectation rises to 3.2% in June from 3.0% in May."

"Consumers on average see 40.4% probability of higher unemployment rate in a year, highest since April 2020."

"Consumers' median 1-year household spending growth expectation declines to 8.4% in June from 9.0% in May."

"A rising share of consumers say credit has been harder to get in the last year and will be in the year ahead."

"More than half of US consumers say their household financial situation deteriorated from a year ago and nearly half expect it to worsen in the year ahead, both up from May."

Market reaction

The US Dollar Index edged slightly lower from the multi-decade high it set above 108.00 earlier in the day and was last seen rising 0.9% on the day at 107.85.

Kansas City Fed President Esther George, who voted against the 75 basis points rate hike in June, argued on Monday that the pace of rate increases needs to be carefully balanced against the state of the economy, as reported by Reuters.

Key takeaways

"Speed at which interest rates should rise an open question, moving too fast risks oversteering."

Communicating the path for rates is far more consequential than the speed of policy change."

"Recession projections suggest to me that rapid rate hikes risk tightening faster than the economy and markets can adjust."

"Abrupt changes in rates could create strains in economy."

"Remarkable that there is growing discussion of recession risk just four months after Fed began raising rates."

"Transmission of policy to economy will be lagged and subject to considerable uncertainty, unclear how high rates will need to rise."

"Steady path of rate increases could improve market functioning and assist balance sheet runoff."

"GDP still 2.5% below pre-pandemic trend suggests pandemic did long-lasting damage to supply side, particularly service sector."

"Nature of inflation suggests tight economy rather than specific supply disruptions are driving prices."

"Raising short term rates faster than long-term rates adjust could invert yield curve, stress banks."

Market reaction

These comments don't seem to be having an impact on the greenback's valuation. As of writing, the US Dollar Index was up 1.05% on the day at 108.02.

- Gold Price witnessed some selling on Monday amid relentless USD buying interest.

- Bets for more aggressive rate hikes by the Fed pushed the USD to a fresh 20-year high.

- Recession fears weighed on investors’ sentiment and helped limit losses for the XAUUSD.

Gold Price edged lower through the early North American session and dropped to the $1,734 area in the last hour, back closer to its lowest level since September 2021 touched on Friday. The downtick was exclusively sponsored by the emergence of aggressive US dollar buying, which tends to undermine the dollar-denominated commodity.

In fact, the USD Index surged to a new 20-year high and continued drawing support from expectations that the Fed would retain its faster policy tightening path to curb soaring inflation. The bets were reaffirmed by last week's FOMC meeting minutes, which emphasized the need to fight inflation even if it results in an economic slowdown. Policymakers indicated that another 50 or 75 bps rate hike is likely at the upcoming FOMC meeting in July. Hence, the market focus now shifts to the latest US consumer inflation figures, due for release on Wednesday.

In the meantime, the prospects for rapidly rising interest rates and tightening financial conditions continued to fuel worries about the global growth outlook. This, in turn, tempered investors' appetite for perceived riskier assets, which was evident from a generally weaker tone around the equity markets and offered some support to the safe-haven gold. The flight to safety triggered a fresh leg down in the US Treasury bond yields and was seen as another factor that helped limit deeper losses for the non-yielding yellow metal, at least for the time being.

The mixed fundamental backdrop warrants some caution for bearish traders and before positioning for any further near-term depreciating move. Even from a technical perspective, the recent range-bound price action witnessed over the past three trading sessions points to indecision among traders over the next leg of a directional move. Hence, sustained weakness below the $1,733 region is needed to confirm a fresh breakdown, which would make gold price vulnerable to testing the $1,700 mark in the near term.

Technical levels to watch

- USD/JPY caught aggressive bids on Monday and rallied to a fresh 24-year high.

- The Fed-BoJ policy divergence weighed on the JPY and remained supportive.

- Technical buying above the 137.00 mark contributed to the strong move up.

The USD/JPY pair added to its strong intraday gains and rallied further beyond the mid-137.00s, to a fresh 24-year high during the early North American session. The pair was last seen trading around the 137.65 region, up over 1.15% for the day.

A strong showing by Japan’s ruling coalition in Sunday’s upper house election reinforced bets that the Bank of Japan would stick to its ultra-loose monetary policy stance. Adding to this, BoJ Governor Haruhiko Kuroda said on Monday that the central bank won’t hesitate to take additional monetary easing steps as necessary. This, in turn, weighed heavily on the Japanese yen, which, along with aggressive US dollar buying provided a goodish lift to the USD/JPY pair on the first day of a new week.

In fact, the USD Index surged to a fresh two-decade high amid growing acceptance that the Fed would retain a faster policy tightening path to curb soaring inflation. The June FOMC meeting minutes emphasized the need to fight inflation even if it results in an economic slowdown and indicated that another 50 or 75 bps rate hike is likely at the July meeting. Furthermore, Friday's upbeat US jobs report reaffirmed bets for more aggressive Fed rate hikes and continued underpinning the USD.

The USD/JPY pair's strong positive move on Monday could further be attributed to some technical buying on a sustained move beyond the previous YTD peak, around the 137.00 mark. The subsequent strength reaffirms a fresh bullish breakout and supports prospects for additional gains. That said, the prevalent risk-off environment could offer some support to the safe-haven JPY. This, along with extremely overbought conditions on hourly charts, could cap gains, at least for the time being.

Nevertheless, the divergent BoJ-Fed policy outlooks should continue to weigh on the JPY and supports prospects for a further appreciating move for the USD/JPY pair. The market focus now shifts to this week's release of the latest US consumer inflation figures, due on Wednesday. Apart from this, the US monthly Retail Sales data and Prelim Michigan Consumer Sentiment on Friday will influence the USD price dynamics. This, in turn, should provide a fresh impetus to the major.

Technical levels to watch

Gold Price sees a negative start to the week. The yellow metal sees more downside, in the view of strategists at TD Securities.

Cascading liquidations from various speculative groups

“We see evidence that the steepest outflows from broad commodity funds since the COVID-19 crisis may be catalyzing a series of cascading liquidations from various speculative groups. This is particularly concerning for gold prices given the extremely bloated length remaining in gold markets from proprietary traders.”

“The substantial size accumulated from proprietary traders during the pandemic appears complacent in the face of a steadfastly hawkish Fed. In a liquidation vacuum, these positions are now vulnerable, which suggests the yellow metal remains prone to further downside still.”

- EUR/USD tumbles further and clinches new YTD lows.

- Extra decline could test the parity zone soon-ish.

EUR/USD drops to new cycle lows around the 1.0050 region at the beginning of the week.

The pair’s bearish stance stays everything but abated for the time being. Against that, there are no support levels of note until the critical parity zone. Further south comes the December 2002 low at 0.9859.

As long as the pair navigates below the 5-month support line near 1.0580, further losses remain in store.

In the longer run, the pair’s bearish view is expected to prevail as long as it trades below the 200-day SMA at 1.1063.

EUR/USD daily chart

- GBP/USD witnessed a turnaround from the top end of a two-week-old descending channel.

- The USD climbed to a fresh two-decade high and was seen as a key factor exerting pressure.

- A sustained break below the YTD low would set the stage for a fall towards the 1.1800 mark.

The GBP/USD pair stalled last week's bounce from the 1.1875 region, or its lowest level since March 2020 and witnessed a turnaround from a two-week-old descending trend-channel resistance. The mentioned barrier, currently around the 1.2035-1.2040 region, nears the 50-period SMA on the 4-hour chart and should act as a pivotal point for short-term traders.

Against the backdrop of expectations for a more aggressive policy tightening by the Fed, the prevalent risk-off mood lifted the safe-haven US dollar to a fresh two-decade high. On the other hand, Brexit woes and speculations that the Bank of England would adopt a gradual approach toward raising interest rates continued weighing on the British pound. This, in turn, prompted fresh selling around the GBP/USD pair on the first day of a new week.

Market participants now look forward to BoE Governor Andrew Bailey's testimony before the Treasury Select Committee, which might influence sterling and provide some impetus to the GBP/USD pair. The market focus would then shift to the UK monthly GDP print and the latest US consumer inflation figures due for release on Wednesday.

In the meantime, some follow-through selling below the 1.1900 mark, leading to a subsequent break through the YTD low, around the 1.1875 region, would be seen as a fresh trigger for bearish traders. This, in turn, would set the stage for a slide towards the 1.1800 round-figure mark, or the lower end of the aforementioned channel.

On the flip side, the 1.1940-1.1950 region now seems to act as an immediate resistance ahead of the 1.200 psychological mark. Any further move up might continue to confront stiff resistance and remain capped near the ascending trend-channel barrier, which if cleared would suggest that the GBP/USD pair has formed a near-term bottom.

Some follow-through buying beyond the 50-period SMA on the 4-hour chart should allow the GBP/USD pair to aim back to reclaim the 1.2100 round figure. The momentum could further get extended and lift spot prices towards testing the next relevant resistance near the 1.2175-1.2185 supply zone en-route the 1.2200 mark.

GBP/USD 4-hour chart

-637931404636530662.png)

Key levels to watch

EUR/GBP has finally suffered an aggressive fall. In the view of analysts at Credit Suisse, a close below its 200-day moving average (DMA) at 0.8444 can reassert a broader sideways trend again.

Key support is seen at 0.8444/32 with resistance at 0.8516/40

“A close below the 200-DMA and late May reaction low at 0.8444/32 would be seen to reassert a broader sideways trend again with support seen next at the 61.8% retracement of the March/June rally and mid -May low at 0.8401/.8393.”

“Resistance is seen at 0.8479 initially, above which can ease the immediate downside bias for strength back to 0.8516/40 but with fresh sellers expected here.”

German Economy Minister Robert Habeck said on Monday it was difficult to say whether Nord Stream 1 gas pipeline would come back online after the maintenance, as reported by Reuters.

Additional takeaways

"Germany has become too dependent on Russia."

"Two floating terminals could be completed by the end of the year."

"Germany is aware gas needs to be distributed among others."

"We have to be prepared for various outcomes, including shipments not renewed after maintenance."

"We will help each other with gas supplies."

"People in Europe know that large savings in gas usage are possible."

"Winter will be critical and we need to prepare as well as possible."

Market reaction

EUR/USD pair showed no immediate reaction to these comments and was last seen losing 0.8% on a daily basis at 1.0100.

- DXY resumes the upside and advances to new cycle peaks.

- Next on the upside comes the round level at 108.00.

DXY fades the weakness seen in the last couple of sessions and prints new nearly 2-decade tops past 107.80 on Monday.

Further upside in the dollar remains in store in the short-term horizon. That said, the continuation of the uptrend initially targets the round level at 108.00 ahead of the October 2002 top at 108.74.

As long as the index trades above the 5-month line near 102.85, the near-term outlook for DXY should remain constructive.

In addition, the broader bullish view remains in place while above the 200-day SMA at 98.52.

Of note, however, is that the index trades in the overbought territory and it therefore could extend the corrective decline to, initially, the 105.80 region (high June 15).

DXY daily chart

USD/CAD has rejected the YTD high at 1.3078. Analysts at Credit Suisse look for a near-term consolidation below this level.

Drop below 1.2816/01 to signal a deeper move lower

“We stay biased for the market to remain capped below 1.3078/1.3123 to avoid a breakout higher and to see a near-term consolidation below this area, though a fall back below 1.2911 is needed reduce the immediate risk of a break higher.”

“Only a break below the recent low at 1.2816/01 would signal a mean-reversion back towards the bottom of the channel, with next support then seen at 1.2771/52 and then at 1.2680/71.”

“A sustained move above 1.3100/23 would make room for further upside to next resistance at 1.3172/77. Nonetheless, with the current volatile environment in mind, we would stay wary of a potential mean-reversion back upon reaching this level.”

GBP/USD closed the previous week above 1.20 but has reversed its course on Monday. The pair is expected to see a clear break below 1.1936, with Credit Suisse’s core technical objective at 1.15/1.14.

Next major support seen at 1.1500/1.1409

“With a top in place in trade-weighted terms and with short-term momentum reaccelerating, we look for a sustained break of the 1.1936 June low in due course. This should then clear the way for further weakness to next support at 1.1861/57 ahead of 1.1775 and eventually 1.1500/1.1409, the bottom of the six-year range and potential long-term trend support stretching back to 1985. Our bias remains to then look for a more important floor to be found here.”

“Near-term resistance is seen at 1.2003, then 1.2039/49, with the recent reaction high and 13-day exponential average at 1.2057/89 ideally capping on a closing basis.”

- A combination of factors assisted USD/CAD to regain strong positive traction on Monday.

- Sliding oil prices undermined the loonie and extended support amid resurgent USD demand.

- Bulls might wait for a sustained move beyond the 1.3080-85 area before placing fresh bets.

The USD/CAD pair caught aggressive bids on Monday and reversed a major part of its losses recorded over the past two trading sessions. The momentum lifted spot prices back above the 1.3000 psychological mark during the first half of the European session and was sponsored by a combination of factors.

Investors remain concerned that a possible global recession, along with the latest COVID-19 outbreak in China, would hurt fuel demand. This, in turn, exerted some downward pressure on crude oil prices, which undermined the commodity-linked loonie. Apart from this, the emergence of fresh US dollar buying provided a goodish lift to the USD/CAD pair.

From a technical perspective, the recent pullback from the 1.3080-1.3085 strong horizontal hurdle, or the YTD peal touched last week, stalled near the 100-period SMA on the 4-hour chart. The said support, currently around the 1.2940 region, should now act as a pivotal point for short-term traders ahead of this week's key event/data risks.

The latest US consumer inflation figures are due for release on Wednesday and will be followed by the Bank of Canada monetary policy decision. Apart from this, traders will take cues from the US monthly Retail Sales data and Prelim Michigan Consumer Sentiment on Friday, which would influence the USD and provide a fresh impetus to the USD/CAD pair.

In the meantime, any subsequent move up is likely to confront resistance near the 1.3065 region. Bulls, however, might wait for a sustained break through the 1.3080-1.3085 strong barrier before positioning for any further gains. Some follow-through buying beyond the 1.3100 round figure would mark a fresh bullish breakout and pave the way for additional gains.

The USD/CAD pair would then aim to surpass an intermediate barrier near the 1.3155-1.3160 region and reclaim the 1.3200 mark. The momentum could further get extended and eventually lift spot prices to the next relevant resistance near the 1.3270 zone.

On the flip side, the 1.2950-1.2945 region might continue to protect the immediate downside. A convincing break below could prompt some technical selling and drag the USD/CAD pair towards the 1.2900 mark. The latter should act as a strong base, which if broken would negate any near-term positive outlook and shift the bias in favour of bearish traders.

USD/CAD 4-hour chart

-637931379547294888.png)

Key levels to watch

EUR/USD has fallen sharply after its break below key price support from the YTD and 2017 lows at 1.0350/41. Analysts at Credit Suisse look for this to clear the way for a fall to parity/0.99, where another phase of consolidation is expected.

The 1.0341/66 price barrier ideally caps further strength

“We stay directly negative with support below 1.0073 seen next at 1.0060/50 ahead of parity/0.99, which we look to ideally be achieved within a 2-4 week time horizon. Thereafter, our bias would be for another consolidation/recovery phase to emerge, similar to the one we saw in May/June.”

“Immediate resistance is seen moving to 1.0185/92, above which can ease the immediate downside bias for a recovery back to resistance next at 1.027/77, with the 1.0341/66 price barrier ideally capping further strength.”

The S&P 500 recovery has extended towards the top of its downtrend channel from April at 3946/50. Analysts at Credit Suisse look for a fresh downturn from here.

Break above 3950 to improve the short-term technical outlook

“The spotlight now turns to the top of the trend channel from April and recent reaction high at 3946/50. Our bias remains for a fresh cap to be seen here and for fresh weakness to emerge over the next 2-4 weeks.”

“Support is seen at 3859 initially, with a break below gap support at 3838 needed to ease the immediate upside bias for weakness back to the short-term uptrend at 3785. Beneath 3742/39 though stays seen needed to open up a retest of the 3637 YTD low.”

“A break above 3950 would improve the short-term technical outlook with the next resistance seen at 3974 ahead of the top of the price gap from early in June at 4017/19. With the 63-day average seen not far above at 4059, we would look for a fresh cap here.”

USD/JPY is still struggling to clear the 137.21 high of September 1998. But as long as the pair trades above 135.35, it can keep the immediate risk higher, according to economists at Credit Suisse.

Support at 135.35 holding can still keep the immediate risk higher

“USD/JPY is still struggling to stage a clear break of the 137.21 high of September 1998. While support at 135.35 holds, the immediate risk is seen higher for now and with a multi-year ‘secular’ base completed earlier this year in April, we continue to look for an eventual sustained break higher. We would then see resistance next at 138.26, from which a fresh pause will be looked for.”

“Big picture, we look for a move to 139.00/10 next and eventually into the 147.62/153.01 zone.”

“Near-term support moves to 136.56, then 135.93. Below 135.35 can ease the immediate upside bias for a pullback to 134.79/79, potentially 134.27.”

- EUR/JPY navigates within an inconclusive range on Monday.

- The 139.85 region caps the upside for the time being.

EUR/JPY alternates gains with losses in the mid-138.00s at the beginning of the trading week.

In the meantime, the cross remains under pressure amidst the ongoing rebound from July lows in the 136.80 region (July 8). As long as the cross keeps trading below the 4-month resistance line near 139.85, extra losses should remain in the pipelie.

That said, further downtrend could revisit the 100-day SMA at 136.09 prior to the minor support at 133.92 (low May 19).

In the longer run, the constructive stance in the cross remains well propped up by the 200-day SMA at 133.12.

EUR/JPY daily chart

- A combination of factors failed to assist GBP/JPY to capitalize on its modest intraday gains.

- Brexit woes, less hawkish BoE expectations continued acting as a headwind for sterling.

- The risk-off environment benefitted the safe-haven JPY and capped the upside for the cross.

The GBP/JPY cross attracted some selling in the vicinity of mid-164.00s on Monday and for now, seems to have stalled last week's goodish rebound from the very important 200-day SMA support. Spot prices surrendered a major part of the modest intraday gains and retreated to the 163.70-163.75 area during the first half of the European session.

A strong election showing by Japan's ruling conservative coalition suggests no change to the ultra-loose monetary policy stance adopted by the Bank of Japan. In fact, BoJ Governor Haruhiko Kuroda reiterated on Monday that the central bank remains ready to take additional monetary easing steps as necessary. This, in turn, was seen as a key factor that undermined the Japanese yen and provided a goodish lift to the GBP/JPY cross on the first day of a new week.