- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 20-02-2013

European stocks retreated from a three-week high as commodity producers declined and companies from Deutsche Lufthansa AG to RSA Insurance Group Plc cut their payouts to shareholders.

Negative data was caused by volume of construction in the EU, as well as data on car sales, which were published yesterday. Sales of passenger cars in the European Union in January 2013 fell to a record low. European automakers association ACEA said on Tuesday, February 18, that the first month of sales decreased by 8.7 percent compared to the same period last year to 885,159 new cars. January is the lowest figure since 1990, when the ACEA began keeping such records.

Positive news came from Greece, where the current account deficit of the balance of payments for 2012. declined by 73% year on year and reached the lowest level since the country's accession to the eurozone. Influence it reduce imports and reduced rates on sovereign debt.

Germany's DAX was down on the record CPI and HICP Germany, which rose by 1.7% y / y (vs. 1.9% previously), in line with the forecast. PPI rose 1.5% to 1.7% falling to 1.2%, and on a monthly basis rose by 0.8% (+0.3% expected).

France's CAC 40 fell, despite the restoration of the French business climate index. French business climate index unexpectedly rose from 87 (revised from 86) to 90 in February, and the HICP fell 0.6% m / m and up 1.4% y / y (vs. 1.5%), not short of projections.

Britain's FTSE 100 rose protocol IFA. Bank of England voted to King expansion QE, but was in a minority (6-3).

National benchmark indexes gained in 10 of the 18 western- European markets. Germany’s DAX declined 0.3 percent, while France’s CAC 40 slid 0.7 percent. The U.K.’s FTSE 100 climbed 0.3 percent.

BHP Billiton slipped 2.4 percent to 2,183.5 pence after the world’s biggest mining company reported a 58 percent decline in first-half profit and appointed Andrew Mackenzie as its new chief executive officer. Mackenzie, who takes over on May 10, was head of its copper unit.

Lufthansa dropped 6.2 percent to 15 euros after Europe’s biggest airline by sales canceled its dividend for 2012. The company made a payout of 25 euro cents a share for 2011.

Lafarge jumped 5.5 percent to 49.27 euros. The world’s biggest cement maker said fourth-quarter earnings before interest, taxes, depreciation and amortization rose to 856 million euros ($1.1 billion), beating the average analyst estimate of 821.6 million euros.

Credit Agricole SA rose 3.9 percent to 7.61 euros after saying it plans to reduce costs by 650 million euros by 2016. France’s third-largest bank said in a web presentation it expects to cut costs by 650 million euros by 2016 through information-technology resources, real estate and procurement.

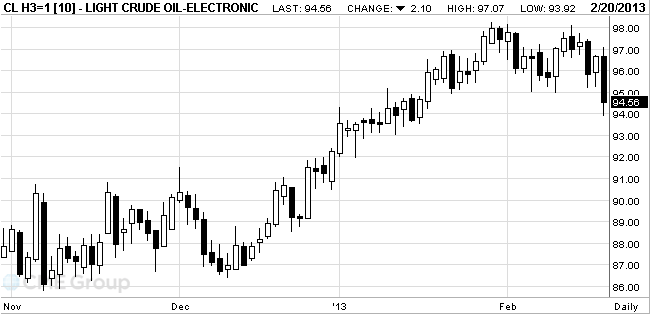

West Texas

Intermediate tumbled more than $2 a barrel following declines in metals on

speculation that a commodity fund is selling positions. Oil also decreased

after gasoline futures slid for a second day from the highest level since

September.

The Energy

Information Administration, the Energy Department’s statistical arm, is

scheduled to release its weekly report at

WTI for March delivery, which expires today, dropped to $93.92 a barrel on the New York Mercantile Exchange.

Brent for

April settlement dropped $1.60, or 1.4 percent, to $115.92 a barrel on the

London-based ICE Futures Europe exchange.

Today, gold prices confirmed break below the level of $ 1,600 an ounce for the first time since mid-August. In anticipation of the FOMC minutes precious metal is trading lower, although in the case declared the monthly purchases of bonds worth $ 85 billion may put pressure on prices. Investors are waiting for the publication of minutes of the last meeting of the U.S. Federal Reserve, to assess the attitude of the central bank to its policy, which helped gold to rise in recent years.

Gold cheaper in recent days due to better economic performance in Europe and the U.S. and rising stock markets.

Stocks of the largest gold-exchange-traded fund (ETF) SPDR Gold Trust on Tuesday fell more than 3 tons to 1.319,964 tons - the minimum level in nearly five months.

April futures price of gold on COMEX today dropped to 1577.50 dollars per ounce.

U.S. stock futures were little changed after government data showed builders broke ground on the most single-family homes in more than four years.:

Hang Seng 23,307.41 +163.50 +0.71%

Shanghai Composite 2,397.18 +14.26 +0.60%

FTSE 6,407.47 +28.40 +0.45%

CAC 3,729.02 -6.80 -0.18%

DAX 7,766.9 +14.45 +0.19%

Crude oil $96.52 -0.14%

Gold $1591.90 -0.77%

EUR/USD $1.3310, $1.3350, $1.3475, $1.3500

USD/JPY Y92.00, Y92.50, Y94.50

EUR/JPY Y125.00

GBP/USD $1.5500

AUD/USD $1.0350, $1.0400Data

00:30 Australia Wage Price Index, q/q Quarter IV +0.7% +0.8% +0.8%

00:30 Australia Wage Price Index, y/y Quarter IV +3.7% +3.4% +3.4%

02:30 New Zealand RBNZ Governor Graeme Wheeler Speaks February

04:30 Japan All Industry Activity Index, m/m December -0.4% +1.6% +1.8%

07:00 Germany Producer Price Index (MoM) January -0.3% +0.4% +0.8%

07:00 Germany Producer Price Index (YoY) January +1.5% +1.2% +1.7%

07:00 Germany CPI, m/m (Finally) January -0.5% -0.5% -0.5%

07:00 Germany CPI, y/y (Finally) January +1.7% +1.7% +1.7%

07:45 France CPI, m/m January +0.3% -0.2% -0.6%

07:45 France CPI, y/y January +1.3% +1.4% +1.4%

09:30 United Kingdom Average earnings ex bonuses, 3 m/y December +1.4% +1.4% +1.3%

09:30 United Kingdom Bank of England Minutes February

09:30 United Kingdom ILO Unemployment Rate December 7.7% 7.7% 7.8%

09:30 United Kingdom Average Earnings, 3m/y December +1.5% +1.4% +1.4%

09:30 United Kingdom Claimant count January -12.1 -5.3 -12.5

09:30 United Kingdom Claimant Count Rate January 4.8% 4.8% 4.7%

10:00 Switzerland Credit Suisse ZEW Survey (Expectations) February -6.9 10

The dollar rose against the euro, while restoring lost during the Asian session, the position, as many market participants are awaiting publication of U.S. data on the housing market, the index of producer prices, and no less important event - exit protocols meeting FOMC. Note also that some support euro was published data for Germany, which revealed that in January, the price pressure selling prices in Germany were stronger than expected due to the high cost of electricity, screening is widely expected slowdown in the German consumer price inflation. According to the report, producer prices rose in January by 0.8% in monthly terms, and rose by 1.7% per year, compared with forecasts at 0.4% and 1.2%, respectively.

The pound fell to a 15-month low against the euro after the Bank of England minutes showed that some officials voted to expand the program to buy assets at a meeting this month. Sterling fell to its lowest level since June against the dollar after reports showed that the policy is also considered cutting interest rates. Note that Mervyn King, Paul Fisher and David Miles in a vote called for increased bond purchase program by 25 billion pounds ($ 38.3 billion) to 400 billion pounds, while the remaining six members of the Monetary Policy Committee were against the increase. Also exerted pressure on the currency presented data that showed that, according to estimates of the International Labour Organization, the number of unemployed for three months (December) increased by 10,000, reaching with 2.5 million people, amid the unemployment rate rose to mark of 7.8%, compared to 7.7% three months earlier (before November). At the same time, the Office for National Statistics reported that the number of unemployed in the same period decreased by 14 thousand. The ONS also said that the number of employed people increased by 154,000 (in the three months to December), while still achieving the level of 29.730 million, which is the highest figure since the introduction of registration in 1971. In addition, the Office for National Statistics said the number of applications for unemployment benefits fell in January by 12,500 to 1.54 million,

The New Zealand dollar fell against 16 major peers after the governor of the Reserve Bank of New Zealand Wheeler said the bank is ready to intervene in the foreign exchange market if necessary. Meanwhile, he added that the official interest rate will also be used if necessary. In addition, it was announced that the central bank is also considering the possibility of macro tools that can support monetary policy. At the same time, Graham Wheeler acknowledged that the New Zealand dollar was "significantly overvalued" in terms of the economic base, a negative effect on some of the production sectors.

EUR / USD: during the European session, the pair decreased by setting the minimum at $ 1.3365

GBP / USD: during the European session the pair fell to the low of $ 1.5278

USD / JPY: during the European session, the pair has grown, and is now trading at Y93.55

At 13:30 GMT the U.S. will report the volume of building permits issued and the number of new foundations of bookmarks in January. Also at this time, will the producer price index and producer price index excluding prices for food and energy in January. At 15:00 GMT Eurozone present indicator of consumer confidence for February. At 19:00 GMT will be publication of the minutes of the Fed meeting.

EUR/USD

Offers $1.3550, $1.3520, $1.3480, $1.3450/60, $1.3440

Bids $1.3380, $1.3355/50, $1.3320, $1.3300, $1.3290, $1.3280/70

GBP/USD

Offers $1.5600/10, $1.5580/85, $1.5550, $1.5520, $1.5505/10, $1.5460-80

Bids $1.5270, $1.5235

AUD/USD

Offers $1.0450, $1.0415/20, $1.0405/10, $1.0400, $1.0380/85

Bidsу $1.0330, $1.0305/00, $1.0275/70, $1.0250, $1.0240/35

EUR/GBP

Offers stg0.8850, stg0.8800, stg0.8780

Bids stg0.8700, stg0.8665/60, stg0.8650, stg0.8640

EUR/JPY

Offers Y126.50, Y126.30, Y126.00, Y125.60/80

Bids Y124.80, Y124.55/50, Y124.40/35, Y124.05/00, Y123.55/50

USD/JPY

Offers Y94.40, Y94.20/30, Y93.95/00, Y93.70/80

Bids Y93.15/10, Y93.00, Y92.90, Y92.80/75, Y92.65/60, Y92.50

Negativity comes from macroeconomic data on the volume of construction in the EU, as well as data on car sales, which were published yesterday. Sales of passenger cars in the European Union in January 2013 fell to a record low. European automakers association ACEA said on Tuesday, February 18, that the first month of sales decreased by 8.7 percent compared to the same period last year to 885,159 new cars. January is the lowest figure since 1990, when the ACEA began keeping such records.

Positive news coming out of Greece, where the current account deficit of the balance of payments for 2012. declined by 73% year on year and reached the lowest level since the country's accession to the eurozone.

Influence it reduce imports and reduced rates on sovereign debt.

The course of today's trading may also affect stat data on real estate market in the U.S., which will be published at 15:30 Moscow time.

FTSE 100 6,403.31 +24.24 +0.38%

DAX 7,770.67 +18.22 +0.24%

CAC 3,730.45 -5.32 -0.14%

Capitalization of Lafarge SA, the world's leading cement producer, rose by 4.8%. EBITDA of the company for October-December rose to 856 million euros from 798 million euros, while the market expected figure at 821.6 million euros. In 2012 Lafarge has sold assets for 900 million euros, not one billion euros, as the company originally planned. Receivable decreased in the fourth quarter by 5% - to 11.3 million euros. The head of Lafarge Bruno Lafont intends to reduce debt below the level of 10 billion euros.

Shares of Credit Agricole SA rose 1.7% despite the fact that the French bank reported a record loss in the fourth quarter due to write-offs of goodwill in the Italian divisions. In the past quarter net loss of 3.98 billion euros, an increase of 30% compared to the same period of 2011.

Capitalization of Deutsche Lufthansa fell 3.9% on the information that the airline refuses to pay dividends in 2013 for the first time since 2010.

EUR/USD $1.3310, $1.3350, $1.3475, $1.3500

USD/JPY Y92.00, Y92.50, Y94.50

EUR/JPY Y125.00

GBP/USD $1.5500

AUD/USD $1.0350, $1.0400Asian stocks rose for a third day, with the regional benchmark index extending an 18-month high, amid signs the global economy is recovering.

Nikkei 225 11,468.28 +95.94 +0.84%

Hang Seng 23,307.41 +163.50 +0.71%

S&P/ASX 200 5,098.71 +16.82 +0.33%

Shanghai Composite 2,397.18 +14.26 +0.60%

South Korea’s Kospi Index led benchmark gauges higher after Bank of Korea Governor Kim Choong Soo said the world economic outlook is improving.

Tokyo Electric Power Co. led Japanese utilities higher.

BHP Billiton Ltd., the world’s largest mining company, fell 0.9 percent in Sydney after reporting a 58 percent drop in first-half profit.

Woodside Petroleum Ltd., Australia’s second-biggest oil and gas producer, added 3.1 percent after full-year profit almost doubled.The euro rose against the dollar on positive results of the February survey ZEW. Economic sentiment in Germany (from 31.5 to 48.2) and the euro area (from 31.2 to 42.4) improved in February, exceeding forecasts of 35.0 and 35.5 respectively. Assessment of the current situation fell from 7.1 to 5.2 vs. 9.0 (in Germany). We also learned that in December, production in the construction sector eurozone fell by 1.7% m / m vs. 0.4% a month earlier. In the annual comparison index fell by 4.8% compared to -4.7% in November. Current account deficit narrowed in December, Greece from € -0.850 billion to € -0.534 billion

The Australian dollar rose Tuesday against most major currencies after the Reserve Bank of Australia does not rule out the possibility of further lowering the interest rate in case of a fall in economic growth in the region. RBA said that he was satisfied that the series has lasted more than lower rates help stimulate the economy. According to published protocols Tuesday meeting of the central bank, which was held on February 5, the rate of inflation the central bank of Australia provides room for further lowering rates. As a result of this meeting, it was left unchanged at 3.0%.

The Canadian dollar has increased the loss and fell to a new 7-month low after weak economic data in Canada. Wholesale Canada in December fell by 0.9%. The rate of decline is more than two times higher than economists' expectations. Foreign investors reduced their holding are in Canadian shares for 6.68 billion Canadian dollars (6.59 billion U.S. dollars) in December, which was the most significant decline since November 2007. The reason for this was the activities of companies in mergers and acquisitions, said the agency Statistics Canada. Foreign investors in the year invested a total of 83.19 billion Canadian dollars in securities of Canada, with most of this capital was invested in debt securities.

The yen rose against the dollar on comments by Japanese authorities as well as the lack of a common position in the government as to the approach to monetary policy has an impact on the behavior of the Japanese yen. Finance Minister Aso spoke against purchases of foreign bonds, as opposed to Prime Minister Abe. The focus of investors is Abe met with U.S. President Barack Obama. If Obama will support policy measures taken by Abe, the weakening of the yen will continue, experts say.

The British pound fell to the lowest level since July 1.5415 dollar. On the British currency negatively affects fears that tighter fiscal policy will continue to put pressure on the economy, concerns possible downgrade the credit rating of the United Kingdom and the assumption that the next head of the Bank of England will announce the implementation Carney milder policy than that which supports the current Managing King. UK authorities may welcome drop pounds if it will strengthen the competitiveness of British exports. Last week, King said that the weakening of the pound is necessary to reduce the deficit of foreign trade in the UK.

Asian stocks rose, with the regional benchmark index trading near its highest close in 18 months, as Bridgestone Corp. surged by the most in four years on better- than-expected profit.

Nikkei 225 11,372.34 -35.53 -0.31%

Hang Seng 23,143.91 -238.03 -1.02%

S&P/ASX 200 5,081.9 +18.48 +0.36%

Bridgestone, the world’s biggest tiremaker, soared 10 percent in Tokyo, to the highest close since 2006.

Gree Inc., a Japanese social-network website operator, rose 2.7 percent on a share-buyback plan.

Nissan Motor Co., a Japanese carmaker that gets 79 percent of its revenue abroad, fell 1.1 percent as the yen strengthened after Finance Minister Taro Aso ruled out foreign bond buying.

Sands China Ltd. paced declines among casino operators in Hong Kong on a report Macau gaming revenue missed estimates.

European stocks rose to the highest level in three weeks as German economic sentiment improved more than forecast and Danone SA rallied after reporting earnings.

German investor confidence increased to the highest level in almost three years in February. The index of investor and analyst expectations climbed to 48.2 from 31.5 in January, the ZEW Center for European Economic Research said. That exceeded the median estimate of economists in a survey calling for an increase to 35.

National benchmark indexes advanced in all 18 western European markets, except Iceland. Germany’s DAX jumped 1.6 percent and France’s CAC 40 surged 1.9 percent. The U.K.’s FTSE 100 climbed 1 percent to a five-year high.

Danone jumped 5.9 percent to 53.15 euros as the company said it plans to cut 900 jobs in Europe after 2012 profitability declined on weak consumption in southern Europe. Fourth-quarter net income from continuing operations rose to 1.82 billion euros, in line with the 1.81 billion-euro average analyst estimate in a survey.

Bayer rose 2.50 euros to 71.79 euros after saying it began a Phase-3 trial of the Eylea injection, along with Regeneron Pharmaceuticals Inc. The trial aims to evaluate the efficacy and safety of the drug in treating Diabetic Macular Edema in Russia, China and other Asian countries, the companies said.

Vodafone dropped 2 percent to 163.5 pence after Bernstein lowered its recommendation on the shares to underperform, the equivalent of sell, from market perform. The European assets of the world’s second-largest wireless carrier will shrink by 23 percent in the next three years as the company faces “structural decline,” analysts led by Robin Bienenstock wrote in a report.

Nobel Biocare Holding AG fell 3.2 percent to 9.61 Swiss francs after Chief Executive Officer Richard Laube said markets will remain difficult in the short term. The world’s second- biggest maker of dental implants reported fourth-quarter net income of 11.2 million euros, exceeding the average analyst estimate of 9.55 million euros.

Major U.S. stock indexes spent trading in positive territory, with the DOW index and S & P 500 and the updated five-year highs.

Positive background of U.S. indices provided optimism from Europe, where the published data found a significant improvement in sentiment in the business environment in Germany, whose economy is the largest in the region. As shown by the results of recent studies that have been presented today by the Institute of ZEW, the level of confidence among German investors resumed their growth in February, registering with the third monthly increase in a row, on expectations that the debt crisis in the region is on the decline, as the measures taken European officials have helped to restore confidence in the region's largest economy. According to the data, the index of sentiment in the business environment in February rose to the level of 48.2, compared with 31.5 in the previous month, as well as expectations at 35.0.

Positively on the index also reflected reports that companies Office Depot Inc. and OfficeMax Inc. are in talks about a merger of the transaction may announce this week.

At the same time, the growth index was somewhat restrained sprouted data on the state of the housing market index from the NAHB, which in February dropped to 46 points in January against the value of 47 points. Expected growth rate of up to 48 points. However, the impact of the publication on the index was rather limited, because tomorrow will be presented to more important data on the U.S. housing market.

Most of the components of the index DOW finished trading in positive territory (22 of 30). More than the others fell in the share price Alcoa, Inc. (AA, -2.79%). Leader shares were Cisco Systems, Inc. (CSCO, +2.24%).

All sectors of the S & P showed an increase. Topped the rating of the consumer goods sector (+1.0%).

U.S. office products retailer Office Depot jumped 9.4% on news of the talks with one of his rivals OfficeMax on the possible merger. As expected, the announcement of the deal could be done this week. Shares of OfficeMax, in turn, have soared by 21%.

The world's largest consumer electronics retailer Best Buy boosted 2.7% after analysts at Barclays upgraded the stock from "market level" to "Outperform."

At the close:

S & P 500 1,530.11 +10.32 +0.68%

NASDAQ 3,213.59 +21.56 +0.68%

Dow 14,035.67 +53.91 +0.39%00:30 Australia Wage Price Index, q/q Quarter IV +0.7% +0.8% +0.8%

00:30 Australia Wage Price Index, y/y Quarter IV +3.7% +3.4% +3.4%

02:30 New Zealand RBNZ Governor Graeme Wheeler Speaks February

04:30 Japan All Industry Activity Index, m/m December -0.3% +1.6% +1.8%

The euro rose for a second day before data today that economists said will show consumer confidence in the currency bloc improved. The European Commission will probably say today that its index of consumer confidence improved to minus 23.2 this month from minus 23.9 in January, according the median estimate of economists surveyed by Bloomberg News. That would follow data from yesterday showing investor confidence in Germany, the region’s biggest economy, jumped to a three-year high.

The yen reversed an earlier slide as investors speculated the Bank of Japan’s policy board will refrain from adding to monetary stimulus until new leadership takes over. The currency fell earlier after Japan posted a record trade deficit. Japan posted a trade deficit of 1.63 trillion yen ($17.4 billion) in January, the Ministry of Finance said in Tokyo today, the biggest shortfall on record dating back to 1947.

New Zealand’s dollar plunged after the central bank said it’s prepared to intervene to weaken its currency. In New Zealand, central bank Governor Graeme Wheeler said the monetary authority is prepared to step in to curb gains in the nation’s currency. “When the New Zealand dollar is coming under upward pressure, we want investors to know that the kiwi is not a one- way bet,” Wheeler said in a speech to manufacturers and exporters in Auckland today.

EUR / USD: during the Asian session, the pair rose to $1.3435.

GBP / USD: during the Asian session, the pair rebounded to $1.5450.

USD / JPY: during the Asian session the pair fell to a week's low.

German PPI and CPI data due up at 0700GMT to provide the early interest, US PPI at 1330GMT into the afternoon, with Eurozone consumer confidence at 1500GMT gaining some interest. ECB Noyer in a WSJ interview was seen countering calls for a cut in the refi rate, preferring to narrow spreads. ECB Asmussen suggested market could be cautiously optimistic on Q1 growth following a weak Q4. Fed FOMC Minutes due for release at 1900GMT.

Change % Change Last

Oil $95.34 -1.27 -1.30%

Gold 1,608.00 -1.50 -0.09%

Change % Change Last

Nikkei 225 11,372.34 -35.53 -0.31%

Hang Seng 23,143.91 -238.03 -1.02%

S&P/ASX 200 5,081.9 +18.48 +0.36%

FTSE 100 6,379.07 +60.88 +0.96%CAC 40 3,735.82 +68.78 +1.88%

DAX 7,752.45 +123.72 +1.62%

Dow Closed

Nasdaq Closed

S&P Closed

(pare/closed(00:00 GMT +02:00)/change, %)

EUR/USD $1,3387 +0,28%

GBP/USD $1,5424 -0,25%

USD/CHF Chf0,9224 -0,09%

USD/JPY Y93,56 -0,41%

EUR/JPY Y125,26 -0,13%

GBP/JPY Y144,30 -0,67%

AUD/USD $1,0355 +0,48%

NZD/USD $0,8467 +0,20%

USD/CAD C$1,0112 +0,07%

00:30 Australia Wage Price Index, q/q Quarter IV +0.7% +0.8%

00:30 Australia Wage Price Index, y/y Quarter IV +3.7% +3.4%

02:30 New Zealand RBNZ Governor Graeme Wheeler Speaks February

04:30 Japan All Industry Activity Index, m/m December -0.3% +1.6%

07:00 Germany Producer Price Index (MoM) January -0.3% +0.4%

07:00 Germany Producer Price Index (YoY) January +1.5% +1.2%

07:00 Germany CPI, m/m (Finally) January -0.5% -0.5%

07:00 Germany CPI, y/y (Finally) January +1.7% +1.7%

07:45 France CPI, m/m January +0.3% -0.2%

07:45 France CPI, y/y January +1.3% +1.4%

09:30 United Kingdom Average earnings ex bonuses, 3 m/y December +1.4% +1.4%

09:30 United Kingdom Bank of England Minutes February

09:30 United Kingdom ILO Unemployment Rate December 7.7% 7.7%

09:30 United Kingdom Average Earnings, 3m/y December +1.5% +1.4%

09:30 United Kingdom Claimant count January -12.1 -5.3

09:30 United Kingdom Claimant Count Rate January 4.8% 4.8%

10:00 Switzerland Credit Suisse ZEW Survey (Expectations) February -6.9

13:30 U.S. Building Permits, mln January 0.903 0.920

13:30 U.S. Housing Starts, mln January 0.954 0.925

13:30 U.S. PPI, m/m January -0.2% +0.3%

13:30 U.S. PPI, y/y January +1.3% +1.6%

13:30 U.S. PPI excluding food and energy, m/m January +0.1% +0.2%

13:30 U.S. PPI excluding food and energy, Y/Y January +2.0% +1.6%

15:00 U.S. Mortgage Delinquencies Quarter IV 7.4%

15:00 Eurozone Consumer Confidence February -23.9 -23.1

19:00 U.S. FOMC meeting minutes January

21:00 New Zealand ANZ Job Advertisements (MoM) January +0.4%

21:30 U.S. API Crude Oil Inventories February -2.3

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers