- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 28-11-2022

Reuters has reported that Richmond Federal Reserve Bank President Thomas Barkin on Monday said he supports smaller interest-rate hikes ahead as the central bank moves to bring down too-high inflation.

"I'm very supportive of the path that is slower, probably longer and potentially higher," Barkin said in an interview with Bloomberg TV, though he declined to say how high he believes rates will need to go.

The Fed "will do what we need to do" to get inflation under control, he said.

Key quotes

Our foot is off the gas.

I'm supportive of a path that is slower, longer and potentially higher for rates.

Inflation has been stubborner than would like.

If inflation stays elevated, Fed needs to do more.

It's helpful to be somewhat more cautious.

Moving a little slower is better risk management.

Inflation expectations seem to have stayed stable.

If inflation stays high, will keep moving rates up.

Fed will do what we need to do.

I'm focused on bringing down inflation.

Don't want to do damage you don't have to do.

US Dollar update

The US Dollar is higher on the back foot amid a global risk-off start to the week. Major market averages opened trading at the start of this week lower due to the protests in China over COVID lockdowns bringing some selling pressure to global equities. DXY is up 0.57% to 106.66.

- AUD/JPY is declining towards 92.00 as China’s unrest-inspired volatility will stay for longer.

- Stable Japan’s employment numbers may weigh on the cross ahead.

- This week, the Caixin Manufacturing PMI data will be of utmost importance.

The AUD/JPY pair is expected to extend its downside journey towards the crucial support of 92.00 as the Statistics Bureau of Japan has reported stable employment data. The Unemployment Rate has landed at 2.6% higher than the expectations of 2.5% but in line with the prior release of 2.6%. While, the Jobs/Applicants ratio has been recorded similarly to the projections at 1.35, higher than the former figure of 1.34.

The risk barometer is going through a rough phase as enlarging unrest in China against the rollback of Covid-19 lockdown measures by the Chinese authorities has crippled the Aussie dollar. After meeting the headlines of public protest against curbs, economists didn’t waste a single second in providing weak economic projections for the Chinese economy.

No one could deny the fact that the impact of weaker projections for China won’t restrict to the dragon economy only. Its trading partners like Australia and New Zealand are also facing the heat. China’s protest-inspired risk aversion theme has dragged the AUD/JPY pair to near the critical hurdle of 92.00.

It is worth noting that individuals’ demand for democracy in the place of dictatorship could bring political instability to the Chinese economy. This could weaken investors’ risk appetite further.

Going forward, investors will focus on the Caixin Manufacturing PMI data, which will release on Thursday. The economic data is seen lower at 48.6 vs. the prior release of 49.2. A weaker-than-projected Caixin Manufacturing data could escalate volatility in the cross ahead.

- US Dollar Index struggles to extend the upside momentum after rising the most in a week.

- Clear break of three-week-old descending resistance line, bullish MACD signals favor buyers.

- Double bottoms around 105.30 appear as the key support.

US Dollar Index (DXY) remains sidelined around 106.60 amid early Tuesday, following the biggest daily jump in a week, as bulls seek more clues to extend the latest rebound. Also challenging the upside momentum is the 21-Day Moving Average (DMA).

However, a daily closing beyond the previous resistance line from November 03 joins the bullish MACD signals to suggest further upside of the Greenback’s gauge versus the major six currencies.

It’s worth noting, however, that the 21-DMA hurdle surrounding 106.85 isn’t the ultimate key to the DXY’s rally as a horizontal area established since September 12, near 108.00, could challenge the US Dollar bulls afterward.

Following that, the 61.8% Fibonacci retracement level of the DXY’s August-September upside, near 108.55, could act as the last defense of the bears.

Alternatively, pullback moves may initially aim for the resistance-turned-support line, close to 105.95 by the press time, before revisiting the latest double bottoms marked near 105.30.

In a case where the US Dollar Index remains bearish past 105.30, the odds of witnessing a south-run challenging August month low of 104.63 can’t be ruled out.

US Dollar Index: Daily chart

Trend: Further upside expected

- AUD/USD fell at the start of the week as China's covid spread, lockdowns and protests drive investors into safe havens.

- Iron Ore prices remain robust and have shrugged off China's covid woes.

- The Federal Reserve speakers on Monday fanned the flames of risks of higher for longer.

- US Dollar bulls move in for the kill and eye a break of 107.00, DXY.

AUD/USD is flat as we approach Tokyo but is at risk of updates relating to China's coronavirus spread, subsequent lockdowns and protests thereof. The risk-off mood has been supporting a move into the US Dollar while a Federal Reserve, (Fed), speaker at the start of the week made hawkish comments, pouring cold water on the brewing sentiment of a Fed pivot.

China covid woes

Global stocks closed ended lower on Monday as social unrest from China’s prolonged Covid restrictions weighed on investor sentiment. Local governments tightened Covid controls as cases surged, even though earlier this month Beijing adjusted some policies that suggested the world’s second-biggest economy was on its way to reopening. In spite of the readministered stringent measures, China's case numbers last week hit all-time records since the pandemic began.

The risk-off sentiment that sent global stocks lower was driven by demonstrations that broke out in mainland China as frustrations with Beijing’s zero-Covid policy flooded major cities. In the cities of Shanghai, Wuhan, Guangzhou and Beijing protesters were heard chanting ''down with XI''.

On Wall Street, supporting a bid in the US Dollar and weighing on the high beta currencies, such as AUD, the Dow Jones Industrial Average lost 497.57 points, or 1.45%, to end at 33,849.46. The S&P 500 fell 1.54% to end at 3,963.94. The Nasdaq Composite finished down 1.58% to close at 11,049.50.

US Dollar bounces back to life, weighing on AUD

The US Dollar, as measured by the DXY index, clawed back earlier losses on Monday. At 106.74 the high, the index was on the way to testing the bear's commitments near 107 the figure as a hawkish Federal Reserve official laid out the case for further rate hikes. James "Bullard, president and CEO of the Federal Reserve Bank of St. Louis said that rates need to go higher to bring inflation down. ''We've got a ways to go to get restrictive on policy,'' he said hawkishly.

Looking ahead, comments from Fed Chair Jerome Powell on Wednesday will be scrutinised closely by investors looking for fresh signals on further tightening. This will come ahead of the end of the week's potential showdown even in the key US Nonfarm Payrolls data. Bullard also said today that a ''tight labour market'' gives the Fed a ''license to pursue a disinflationary strategy.'' At this stage, the Fed is expected to hike rates by an additional 50 basis points when it meets on Dec. 13-14.

Australian macro is thrown a lifeline by Iron Ore

Despite the bleak outlook for the Chinese economy, Iron Ore, one of Australia's major exports, rose at the start of the week. ''Sentiment remains buoyed by recent measures to support the country’s beleaguered real estate sector,'' analysts at ANZ Bank explained.

''The People’s Bank of China cut the reserve ratio requirement by 25bp on Friday, following the State Council’s suggestion that monetary tools will be used to maintain liquidity. China also removed restrictions on fundraising used by developers in the past,'' the analysts added. ''They will now be able to raise capital via equity markets that can then be used for debt repayments and acquisitions. This follows earlier this month the release of a 16-point plan which it hopes will boost the real estate market.''

China economic data will be key

On November 20, China will release the NBS PMIs (for the month of November), in the Manufacturing and Non-Manufacturing sector. Analysts at TD Securities said that the PMIs are likely to fall further due to the rising Covid cases and tightening Covid restrictions that likely weighed heavily.

''Additionally, property woes continue to pressure construction. High-frequency indicators have slowed. Meanwhile, both exports and imports continue to weaken. Separately, increasing Covid cases in high-risk areas will continue to weigh on service sector activity.''

AUD/USD technical analysis

Now on the backside of the trendline, in the 4-hour time frame, the price is carving out the downside in a series of bearish impulses:

Zoomed in on the same time frame, we can see that the price is correcting at support having broken 0.6650. Should resistance hold, at old support, then there will be prospects of yet another bearish impulse for the sessions ahead. The 0.6580s guard 0.6550 and then 0.6500.

- GBP/JPY remains sidelined after falling the most since early November.

- Risk-aversion, fears surrounding labor strikes in UK weighed on the prices.

- Japan data, BOE Governor Bailey’s speech will direct intraday moves, bears may keep the reins amid sour sentiment.

GBP/JPY stays defensive around 166.00 during early Tuesday, after posting the biggest daily loss in three weeks the previous day. In doing so, the cross-currency pair portrays the market’s inaction, or a search for more clues, following a negative start to the key week.

Looming fears of public servants’ nationwide strike in the UK joined British Prime Minister (PM) Rishi Sunak’s readiness to jostle with China and the Covid woes emanating from the dragon nation to weigh on the GBP/JPY prices the previous day. On the same line could be the downbeat prints of the Confederation of British Industry's (CBI) latest Distributive Trades Survey for November.

As per the latest readings, published on Monday, the CBI Retail Sales for November printed -19 figures versus +18 prior while the gauge showing the Expected Retail Sales for December slumped to the lowest since March 2021, to -21 versus -9 previous readings.

UK PM Rishi Sunak’s indirect attack on Chinese policies joined British Foreign Secretary James Cleverly’s statements pushing Beijing to take note of the lockdown protests to highlight the recently sour terms between Britain and China. On the other hand, “Hundreds of demonstrators and police clashed in Shanghai on Sunday night as protests over the restrictions flared for the third day and spread to several cities, with police on Monday stopping and searching people at the sites of weekend protests in Shanghai and Beijing,” reported Reuters. The news joins the all-time high of daily virus infections from the dragon nation to weigh on the sentiment.

Against this backdrop, Wall Street closed in the red and the US Treasury yields improved after an initial slump.

Looking forward, Japan’s Retail Trade and employment numbers for October can offer immediate directions to the GBP/JPY pair traders ahead of a speech from the Bank of England (BOE) Governor Andrew Bailey.

That said, the risk-off mood could gain additional support from BOE’s Bailey and may drown the pair further toward the south amid the recent wave of speculations supporting easy rate hikes.

Technical analysis

A daily closing below the 21-DMA, around 166.90 by the press time, directs GBP/JPY bears towards a seven-week-long ascending support line, near 164.80 at the latest.

- Risk aversion weighed on risk-perceived currencies, bolstering the safe-haven Japanese Yen.

- Hawkish commentary by Federal Reserve officials kept the New Zealand Dollar pressured.

- NZD/JPY Price Analysis: Double top in the daily chart, targets a fall to 80.50.

The New Zealand Dollar (NZD) dropped on Monday, courtesy of US central bankers reassessing further rate hikes for the next year, alongside dented risk appetite by the Covid-19 crisis in China, triggering riots in the country. Therefore, the risk-perceived NZD/JPY weakened and tumbled by 1.55%. As the Asian session begins, the NZD/JPY is trading at 85.62.

NZD/JPY Price Analysis: Technical outlook

The NZD/JPY daily chart dropped from around 86.70 to 85.60s, exacerbated by the formation of a “double top” chart pattern and the fall below last week’s low of around 86.01. Oscillators led by the Relative Strength Index (RSI) turned bearish, which would open the door for the NZD/JPY to test the 100-day Exponential Moving Average (EMA) at 84.86, followed by the 50-day EMA at 84.52. If the NZD/JPY extends its losses, it will probe the confluence of the November 11 swing low and the 200-day EMA around 83.84/84.00. A breach of the latter would confirm the “double top” and will target a fall.

The NZD/JPY first ceiling level would be the 86.00 mark as an alternate scenario. A breach of the latter will expose the 87.00 mark, followed by the two-month high at 87.45. Once cleared, it will invalidate the double top and pave the way toward the YTD high at 87.86.

NZD/JPY Key Technical Levels

- The formation of the Double Bottom chart pattern supports a bullish reversal.

- The asset is on the verge of shifting its business comfortably above the 20-period EMA.

- A range shift by the RSI (14) into 40.00-60.00 indicates a loss in the downside momentum.

The USD/CHF pair is oscillating in a narrow range below the psychological resistance of 0.9500 in the early Tokyo session. The asset witnessed a juggernaut rally on Monday after sensing strength around 0.9410. The US Dollar received significant attention for parking funds by the market participants amid the risk-aversion theme.

The US Dollar Index (DXY) is having a sigh after a vertical rally and is also preparing to extend its rally amid a significant decline in investors’ risk appetite.

On a four-hour scale, the asset has rebounded after forming a ‘Double Bottom’ chart pattern. The formation of the above-mentioned chart pattern indicates a bullish reversal as the asset tested previous lows on November 24 around 0.9388 with less selling pressure.

The major is attempting to cross the 20-period Exponential Moving Average (EMA) at 0.9482, which will turn the short-term trend towards the upside.

Meanwhile, the Relative Strength Index (RSI) (14) has shifted into the 40.00-60.00 range from the bearish range of 20.00-40.00, which signals a loss in the downside momentum.

Going forward, a decisive move above the psychological resistance of 0.9500 will drive the pair towards the 50-EMA at 0.9572, followed by November 21 high around 0.9600.

Alternatively, a drop below November 24 low at 0.9388 will drag the asset towards November 15 low at 0.9356. A slippage below the latter will expose the asset for more downside towards February 10 high around 0.9300.

USD/CHF hourly chart

-638052736309396139.png)

- USD/CAD seesaws around the highest levels in two weeks after a heavy upside move.

- Oil prices struggle to defend the corrective bounce off the yearly low.

- Hawkish Fedspeak, fears emanating from China keep buyers hopeful.

- Canada’s Q3 GDP, US CB Consumer Confidence will be important for fresh impulse.

USD/CAD bulls take a breather around a fortnight top, making rounds to 1.3500 during Tuesday’s Asian session, after posting the biggest daily jump in 1.5 months the previous day.

The Loonie pair’s rally on Monday could be linked to the US Dollar’s broad run-up on hawkish comments from the Federal Reserve (Fed) officials, as well as Covid woes from China. It should be noted that with the improvement in prices of WTI crude oil, Canada’s key exports failed to weigh on the USD/CAD prices.

“Hundreds of demonstrators and police clashed in Shanghai on Sunday night as protests over the restrictions flared for the third day and spread to several cities, with police on Monday stopping and searching people at the sites of weekend protests in Shanghai and Beijing,” reported Reuters. The news joins the all-time high of daily virus infections from the dragon nation to weigh on the sentiment.

Elsewhere, Federal Reserve Bank of Cleveland President Loretta Mester marked the need to see several more good inflation reports and more signs of moderation to back the pause in rate hikes. On the same line, St. Louis Fed President James "Jim" Bullard stated that the situation calls for much higher interest rates than what we've been used to. Further, New York Federal Reserve Bank President John Williams said that he believes the Fed will need to raise rates to a level sufficiently restrictive to push down on inflation and keep them there for all of next year. Recently, Fed Vice Chair Lael Brainard advocated for tighter monetary policy while citing risk-management reasons.

Amid these plays, Wall Street closed in the red and the US Treasury yields improved after an initial slump. Further, WTI crude oil refreshed the yearly low before closing on the positive side, retreating to $76.60 as of late.

Looking forward, Canada’s third quarter (Q3) Gross Domestic Product (GDP) Annualized, expected to improve from 3.3% to 3.5%, will be important for the USD/CAD pair traders to watch for clear directions. Also crucial will be the monthly US Confederation Board’s (CB) Consumer Confidence for November and the aforementioned risk catalysts. Above all, Friday’s employment numbers from the US and Canada should be awaited before making any major trade decision.

Technical analysis

A daily closing beyond the convergence of the 21 and 50 Exponential Moving Averages (EMAs), around 1.3440 by the press time, favors USD/CAD buyers to aim for the six-week-old resistance line, around 1.3600 at the latest.

- Unable to crack the 200-day EMA, the GBP/USD fell beneath the psychological 1.2000 figure.

- Short-term, the GBP/USD is downward biased, and once reclaiming 1.1900, it might fall to 1.1820s.

The GBP/USD moved downward on Monday, spurred by tensions arising in China due to Covid-19 zero-tolerance restrictions. US central bankers foresee a 2023 year of high-interest rates as they commit to higher for longer bolstered the US Dollar (USD). At the time of writing, the GBP/USD is trading at 1.1957, below its opening price by 0.07%, as the Asian session begins.

GBP/USD Price Analysis: Technical outlook

On Monday, the GBP/USD dived below the 1.2000 figure, exacerbated by Pound Sterling (GBP) buyers unable to crack the 200-day Exponential Moving Average (EMA) around 1.2170. Therefore, the GBP/USD dropped below the 1.2000 figure, eyeing a re-test of an upslope trendline drawn from September lows that pass around 1.1640/60. For that scenario to play out, the GBP/USD needs to drop below the November 23 daily low of 1.1872, which, once cleared, could pave the way for the previously mentioned upslope trendline.

Short term, the GBP/USD is testing the 50-Exponential Moving Average (EMA) in the 4-hour chart at 1.1953. The Relative Strength Index (RSI) sliding below the 50-midline suggests sellers outweigh buyers. Hence, the GBP/USD path of least resistance is downward biased.

The GBP/USD first support would be 1.1953. A decisive break will expose the 1.1900 figure, followed by the S1 daily pivot at 1.1890, ahead of the S2 daily pivot at 1.1828. On the flip side, the GBP/USD first resistance would be 1.2000, followed by the daily pivot point at 1.2010, followed by the R1 daily pivot at 1.2070.

GBP/USD Key Technical Levels

- Gold price has shifted into an inventory adjustment after a sheer decline amid a downbeat market mood.

- The USD Index is aiming to smash the 107.00 hurdle amid an improvement in safe-haven’s appeal.

- Fed’s Mester needs more good inflation reports for supporting the rate hike pause scenario.

Gold price (XAU/USD) has turned sideways in the early Asian session after a perpendicular downfall above the key resistance of $1,760.00. The precious metal is building a cushion of around $1,740.00, at the time of writing. Later, it will be discovered whether the inventory adjustment is an accumulation or a distribution.

The risk profile is still negative, therefore, the odds are favoring the inventory adjustment as a distribution one. The US Dollar Index (DXY) is displaying back-and-forth moves around 106.70 and is aiming to kiss the critical resistance of 107.00 ahead. Meanwhile, the 10-year US Treasury yields are still auctioning below 3.70% despite hawkish commentaries from Federal Reserve (Fed) policymakers.

New York Fed Bank President John Williams is favoring pushing the interest rates to a restrictive level solid enough to propel inflation down and holding them till CY2024. Also, Cleveland Fed Bank President Loretta Mester believes that the Fed is not near to a pause in a rate hike, as reported by Financial Times. She added that more good inflation reports and more signs of moderation are required before building an action plan of pausing rate hikes.

Gold technical analysis

On an hourly scale, gold price is struggling to hold itself above the 23.6% Fibonacci retracement (plotted from November 3 low at $1,616.69 to November 15 high at $1,758.88) at $1,746.50. The precious metal has surrendered the critical support of the 200-period Exponential Moving Average (EMA) at $1,748.10, which was acting as major support earlier.

Meanwhile, the Relative Strength Index (RSI) (14) has shifted into the bearish range of 20.00-40.00, which indicates more weakness ahead.

Gold hourly chart

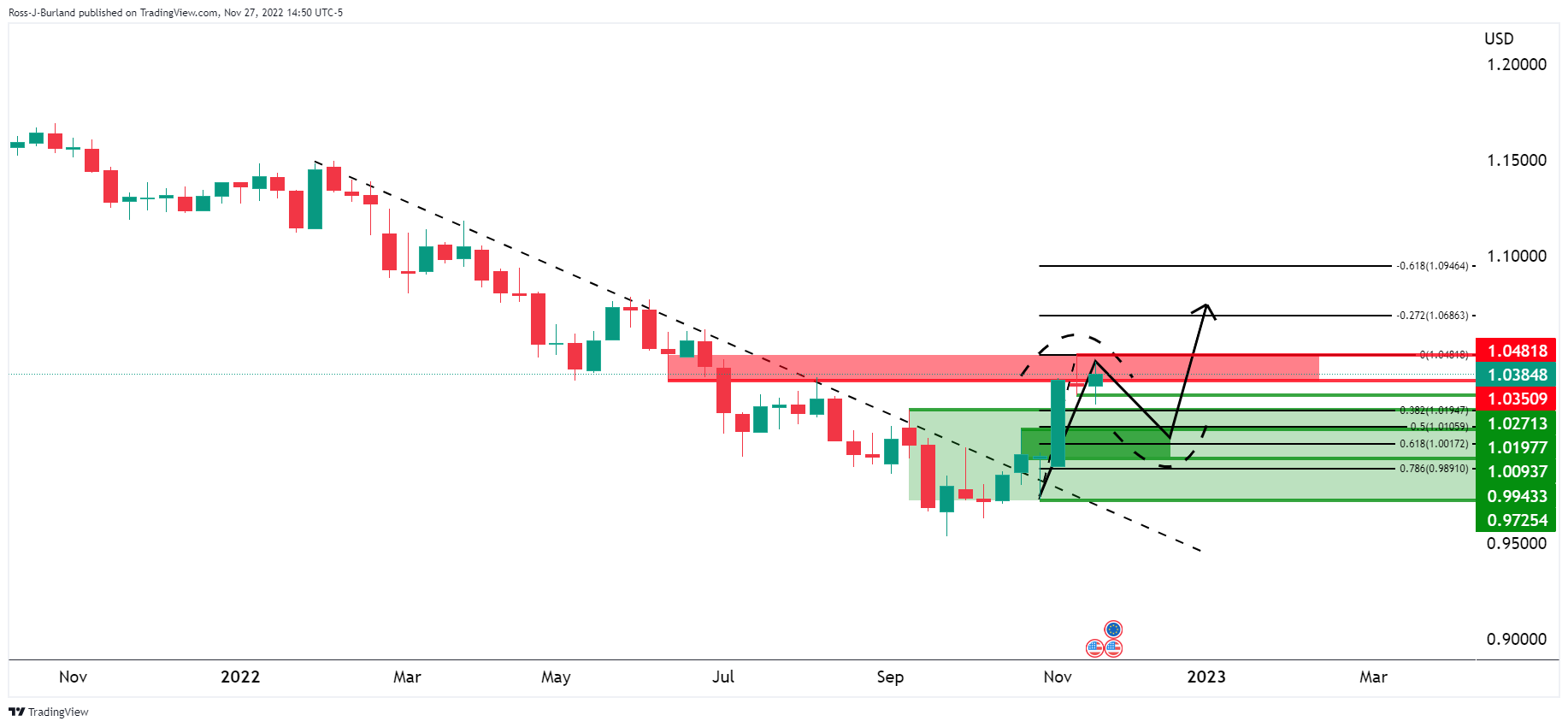

- EUR/USD holds lower ground after breaking a three-week-old ascending trend line.

- Impending bear cross on MACD, U-turn from five-month-long resistance line adds strength to bearish bias.

- 61.8% Fibonacci retracement level lures sellers, bulls need validation from monthly top.

EUR/USD remains depressed around 1.0340, following the biggest daily fall in a week. In doing so, the major currency pair also justifies the previous day’s downside break of a three-week-old support line.

Not only the trend-line break but the looming bear cross on the MACD and the EUR/USD pair’s U-turn from the downward-sloping resistance line from late June, around 1.0475, also keeps the bears hopeful.

That said, the pair’s latest weakness aims at the 61.8% Fibonacci retracement level of May-September downside, near 1.0310.

Following that, the previous weekly low and tops marked in September, respectively around 1.0225 and 1.0200, could lure the EUR/USD sellers.

Alternatively, recovery needs to stay beyond the support-turned-resistance, around 1.0410, to lure the short-term EUR/USD buyers. Even so, the multi-day-old descending resistance line, around 1.0475, could stop the quote’s further advances.

Even if the quote stays firmer past 1.0475, the monthly high near 1.0500 appears the last defense of the EUR/USD bears.

Overall, EUR/USD remains on the bear’s radar even if the downside room appears limited.

EUR/USD: Daily chart

-29112022-638052713940368691.png)

Trend: Further downside expected

The Democratic leader of the U.S. Senate urged lawmakers on Monday to back his proposal to bar the US government from doing business with companies that use semiconductors made by producers the Pentagon considers Chinese military contractors, reported Reuters late Monday.

The news quotes Senator Chuck Schumer as he speaks on the Senate restart after the Thanksgiving holiday recess.

“If American business wants the federal government to buy their products or services, they shouldn't be using the kind of Chinese-made chips that, because of Chinese government involvement, put our national security at risk," said Senator Schumer.

"We need our government and our economy to rely on chips made right here in America,” the diplomat adds.

Key quotes

Schumer and Republican Senator John Cornyn introduced their proposal as an amendment to the National Defense Authorization Act, or NDAA, an annual bill setting policy for the Department of Defense expected to pass the Senate and House of Representatives in December.

As one of the only major pieces of legislation Congress passes every year, the NDAA is closely watched by a broad swath of industry and other interests because it determines everything from purchases of ships and aircraft to pay increases for the troops and how to address geopolitical threats.

Lawmakers also use the bill as a vehicle for a wide range of policy measures. The proposal from Schumer and Cornyn would broaden an existing ban on government use of Chinese chips.

Risk-aversion gets more to watch

The news adds strength to the market’s risk-off mood but gets no major immediate response amid the early hours of the Asian session.

Also read: Forex Today: Safe havens in demand on China COVID woes

“The successive shocks to global supply chains from the pandemic and the war in Ukraine could ‘herald a shift’ to an era of more volatile inflation and force central banks to guard against it with tighter monetary policy,” Fed vice chair Lael Brainard said in remarks released on Monday by the U.S. central bank, reported Reuters.

Additional comments

The experience with the pandemic and the war highlights the challenges for monetary policy in responding to a protracted series of adverse supply shocks.

If supply continues to prove slow to respond ‘due to challenges such as demographics, deglobalization, and climate change, it could herald a shift to an environment characterized by more volatile inflation compared with the preceding few decades.’

A protracted series of adverse supply shocks could persistently weigh on potential output or could risk pushing inflation expectations above target in ways that call for monetary policy to tighten for risk-management reasons.

Monetary policy often recommends officials ‘look through’ supply shocks that are expected to be temporary, an approach that the Fed used initially when U.S. inflation rose for what were expected to be one-off ‘transitory’ reasons.

But the sequence of such shocks faced in the last two years, with one handing the baton to the other, ‘blurred the lines about what constitutes a temporary shock as opposed to a persistent shock to potential output.’

Even when each individual supply shock fades over time and behaves like a temporary shock on its own, a drawn-out sequence of adverse supply shocks that has the cumulative effect of constraining potential output for an extended period is likely to call for monetary policy tightening to restore balance between demand and supply.

EUR/USD stays pressured

Hawkish Fedspeak has recently helped the EUR/USD bears and so did the comments from Fed’s Brainard. That said, the major currency pair remains pressured near 1.0340 by the press time.

- NZD/USD has witnessed an attempt of recovery after dropping to near 0.6160.

- More downside in the kiwi asset is still favored as the risk-off impulse is still solid.

- This week, Fed Powell’s speech and US ADP Employment data will be of utmost importance.

The NZD/USD pair has sensed some bids after a vertical drop to near 0.6160 in the late New York session. The kiwi asset witnessed intense selling pressure on Monday after surrendering the round-level support of 0.6200. An attempt of a recovery near 0.6160 should not be considered a reversal yet as the market mood is still cautious and a cushion is yet to be finalized.

The US Dollar Index (DXY) has extended its gains to near 106.67 after a V-shape recovery from a low of 105.40. Rising protests against the Covid-19 lockdown in China have posed a significant impact on commodity-linked currencies, being their major trading partners. Therefore, the decline in antipodeans is higher in comparison with gains recorded in the USD Index.

S&P500 has experienced significant losses, portraying a sour market mood. Meanwhile, the returns on US Treasury bonds are still subdued ahead of a speech from Federal Reserve (Fed) chair Jerome Powell. The 10-year US Treasury yields are still below 3.70% after a mild recovery. It seems that anxiety ahead of Fed Powell’s speech has sidelined them.

Apart from Fed Powell’s speech, investors are keeping an eye on the United States Automatic Data Processing (ADP) Employment data. As per the estimates, the US economy has created additional 200k jobs in November vs. the prior release of 239k. The job creation numbers are declining in the past few months as higher interest rates and weaker economic projections have forced firms to use their current manpower in the best manner and postponement of the recruitment process.

It was a volatile start to the week and the US sessions stayed with the theme. The US Dollar edged up to 106.74 on Monday, slightly recovering from a 3-1/2-month low of 105.32 with investors concerned about a global slowing economy and the spread of coronavirus in China.

Federal Reserve policymakers also spoke on Monday and bucking the sentiment that it will be soon time to slow the pace of interest rate hikes for the central bank to assess the economic landscape. Instead, due to a tight labour market James "Jim" Bullard, president and CEO of the Federal Reserve Bank of St. Louis said that this gives the Fed a license to pursue a disinflationary strategy now.

New York Federal Reserve Bank President John Williams on Monday said that he believes the Fed will need to raise rates to a level sufficiently restrictive to push down on inflation, and keep them there for all of next year:

"I do think we're going to need to keep the restrictive policy in place for some time; I would expect that to continue through at least next year," Williams said at a virtual event held by the Economic Club of New York, adding that he does not expect a recession.

Earlier this month, the Fed delivered its fourth straight 75 basis point rate increase and pushed borrowing costs to the highest since 2008 to tame stubbornly high inflation. Money markets are now pricing in a 70% chance that the central bank would deliver a smaller 50-bps rate hike in December.

Meanwhile, risk-off markets weighed on high beta currencies such as the pound, AUD and euro. ''The lockdowns may make it challenging for China to achieve its forecast economic growth which will also have implications for global economic growth,'' analysts at ANZ Bank said in a note at the start of Tuesday's trade in Asia.

In late afternoon trading, the S&P 500 was down 1.59%. The Nasdaq Composite declined 1.5% while Dow Jones Industrial Average was down 1.44%.

EUR/USD was down some 0.44% falling to a low of 1.0333 from a higher of 1.0496. GBP/USD dropped to 1.1940 from 1.2117. AUD/USD sank to 0.6642 from 0.6727. The yield on the US 10-year note was up 3bp to 3.71%. Oil prices dropped to their lowest level in nearly a year, but then rebounded as the lower prices ignited demand. WTI was up 0.5% to $76.93. Gold fell 0.7% to $1,741.02/oz. BTC/USD was down 1.2% and near the low of the day at 16,004.

- US Dollar got bolstered by Federal Reserve policymaker’s hawkish commentary.

- New York Fed John Williams expects rate cuts by 2024.

- Weaker Retail Sales in Australia and protests in China weighed on the Australian Dollar.

- AUD/USD Price Analysis: Short-term downward biased, eyeing 0.6600.

The Australian Dollar (AUD) plunges as the week begins due to Federal Reserve (Fed) officials’ hawkish commentary, risk aversion spurred by China’s Covid-19 riots, and a weaker-than-expected retail sales report from Australia. Therefore, the US Dollar (USD) is appreciating, as shown by the US Dollar Index (DXY). At the time of writing, the AUD/USD is trading at 0.6650, below its opening price by 1.50%.

Federal Reserve officials to keep hiking rates, eyeing cuts in 2024

Investors’ sentiment remains negative. Federal Reserve officials said that additional rate hikes are needed. St. Louis Fed President James Bullard said the Fed needs to keep increasing rates until 2023. He commented that rates must reach the low end of the 5%-7% rate range, adding that a recession is not inevitable. Echoing some of his comments was the New York Fed President John Williams commenting that he expects inflation to fall to 5.0%-5.5% by the end of 2022 and 3.0%-3.5% by late 2023 and noted that the baseline forecast does not predict a recession for the US. However, traders should know that Williams said the Fed could reduce rates in 2024.

Traders should remember that the Federal Reserve Open Market Committee (FOMC) minutes for the last meeting indicated that “A substantial majority of participants judged that a slowing in the pace of increase would likely soon be appropriate,” cementing the Fed’s moderating interest rates.

China’s Covid-19 riots and weak Australian retail sales weighed on the AUD

Aside from this, protests in China related to Covid-19 lockdowns and mass testing, and fears that if it escalates might derail the global economy, weighed on investors’ mood. According to Bloomberg, “the protests are shaping up one of the biggest threats to the Communist Party since the 1989 Tiananmen crackdown,” keeping investors on their toes.

During the Asian session, Australia’s Retail Sales for October fell by 0.2% MoM vs. estimates of a 0.5% expansion, portraying a more “cautious consumer spending mood after 9 straight months of increase,” according to TD Securities analysts.

“However, sales are still robust on an annual basis at 12.5% y/y. Given the rapid rise in interest rate, household budgets are under pressure, and this is starting to be reflected in the slowdown in consumer spending,” TD analysts wrote.

What to watch

An absent Australian economic calendar will leave traders adrift to US Dollar dynamics. On the US side, the S&P/Case-Shiller Home Prices for September and the Conference Board (CB) Consumer Confidence for November will offer a fresh catalyst to AUD/USD traders.

AUD/USD Price Analysis: Short term

The AUD/USD 4-hour chart suggests that sellers are gathering momentum, pushing prices toward the 38.2% Fibonacci retracement at 0.6643. Additionally, the Relative Strength Index (RSI) dropped to bearish territory, exacerbated by weak Aussie economic data and the AUD/USD exchange rate falling beneath 0.6700. Therefore, the AUD/USD path of least resistance is downwards.

Therefore, the AUD/USD first support would be the 100-Exponential Moving Average (EMA) at 0.6631. Break below will expose the 50% Fibonacci retracement at 0.6594, followed by the 61.8 Fibonacci level at 0.6546. on the flip side, the AUD/USD first resistance would be 0.6700. A breach of the latter will expose the 0.6720 S1 daily pivot-turned-resistance, followed by the daily pivot at 0.6750.

- EUR/USD dropped into key support on risk-off themes.

- An inverse head & shoulders could be in the making.

At the time of writing, EUR/USD is down some 0.29% falling to a low of 1.0354 from a higher of 1.0496. Risk currencies, such as the Euro are under pressure as protests against COVID restrictions in China weighed on market sentiment.

The violent protests in major Chinese cities over the weekend against the country's strict zero-COVID curbs have knocked growth expectations in the world's second-largest economy. This is creating a flight to safety in support of the yen, US Dollar and CHF.

Meanwhile, the economic challenges facing the euro area are not the same as in the US which is a weight on the euro. ''Supply-side shocks set the scene for an extended period of high inflation coupled with lacklustre growth. A recession seems difficult to avoid and we expect Gross Domestic Product to decline by 0.9% in 2023, followed by stagnation in 2024,'' analysts at Danske Bank argued.

Key points:

''Elevated inflation pressures coupled with the risk of de-anchoring inflation expectations will keep the ECB firmly in tightening mode. Rate cuts could be on the cards in 2024, but uncertainty remains high.''

''Europe's biggest fragility stems from the (geo)political front, as well as a renewed flaring up of the energy crisis or new Covid-19 outbreaks next winter. Upside risks to the growth outlook arise from pandemic-related private savings buffers, fiscal measures and accelerated investment spending.''

'Stagflation' does not have to be the new normal, but structural reforms to address low productivity and adverse demographic trends as well as securing a leading position in the green transition race remain key.

Fed speakers in play

Federal Reserve speakers will be important this week. On Monday, New York Federal Reserve Bank President John Williams said that he believes the Fed will need to raise rates to a level sufficiently restrictive to push down on inflation, and keep them there for all of next year:

"I do think we're going to need to keep the restrictive policy in place for some time; I would expect that to continue through at least next year," Williams said at a virtual event held by the Economic Club of New York, adding that he does not expect a recession.

James "Jim" Bullard, president and CEO of the Federal Reserve Bank of St. Louis, has said that rates need to go higher to bring inflation down. ''We've got a ways to go to get restrictive on policy.'' He also said the Fed ''will have to keep rates at a sufficiently high level all through 2023 and into 2024.''

Bullard also said that a ''tight labour market gives us a license to pursue disinflationary strategy now.''

In this regard, for the week, investors will keep a close watch on Nonfarm Payrolls for November, as well as the second estimate for third-quarter gross domestic product and consumer confidence this month.

EUR/USD technical analysis

Despite the risks of a downside continuation, an inverse head & shoulders could be in the making at this juncture. Bullish commitments around 1.0300/50 would be forming the right-hand shoulder of the bullish pattern.

- Silver price falls below the psychological $21.00 after failing to hurdle the 200-day EMA.

- The break of an upslope trendline exacerbated a fall from daily highs around $21.60s.

- XAG/USD Price Analysis: Break below $20.89 to pave the way to $20.00.

Silver price tumbles below $21.00 late in the North American session amidst risk aversion and the recovery of the US Dollar (USD), as shown by the US Dollar Index (DXY) gaining 0.40% in the day. At the time of writing, the XAG/USD is trading at $20.95, below its opening price by almost 2%.

Silver Price Analysis (XAG/USD): Technical outlook

After XAG/USD failed to crack the 200-day Exponential Moving Average (EMA) at $21.34, the white metal is extending its losses below the $21.00 figure. It should be noted that Silver broke below a 20-day-old upslope trendline, exacerbating Silver’s drop. The Relative Strength Index (RSI), aiming towards the 50-midline, is accelerating, suggesting that sellers are gathering momentum.

Short term, the XAG/USD 4-hour chart portrays sellers’ strength. Notably, XAG/USD hit a daily high of around $21.61 before tumbling and reclaiming the 50 and 100-EMAs. Therefore, the XAG/USD path of least resistance is tilted to the downside. That said, the XAG/USD first support would be November 23, swing low at $20.89. Once cleared, the next support would be the November 21 pivot low at $20.56, followed by the 200-Exponential Moving Average (EMA) at $20.15.

As an alternate scenario, XAG/USD first resistance would be the confluence of the S1 pivot and the 40-EMA at $21.16, followed by the daily pivot point at $21.36, ahead of the R1 pivot at $21.55.

Silver Key Technical Levels

- Markets are risk-off and that is sending GBP below 1.2000.

- GBP/USD is breaking out of a coil which is significant.

- A 100% measured move of the range will target the prior structure at 1.1900.

At the time of writing, GBP/USD is down some 0.9% falling to a low of 1.1976 from a high of 1.2111. Risk currencies, such as the British pound, are under pressure as protests against COVID restrictions in China knocked market sentiment.

GBP/USD is falling below the psychological 1.2000 level and meeting short-term dynamic support. Additionally, fears of a lengthy UK recession were seen weighing on sentiment. Investors await to see what the Bank of England's (BoE) next move will be. There will be several BoE members due to speak this week, including BoE governor Andrew Bailey on Tuesday and chief economist Huw Pill on Wednesday.

The Old Lady has been trying to combat soaring inflation without damaging the economy too much in the process. ''Inflation pressures will remain elevated during 2023, forcing the Bank of England to deliver further hikes,'' analysts at Danske Bank explained. ''We do however see the peak rate well below market pricing and we expect the first cut to be delivered during 2024.''

Ears out for Fed speakers

Meanwhile, Federal Reserve speakers will be key this week. On Monday, New York Federal Reserve Bank President John Williams said that he believes the Fed will need to raise rates to a level sufficiently restrictive to push down on inflation, and keep them there for all of next year:

"I do think we're going to need to keep the restrictive policy in place for some time; I would expect that to continue through at least next year," Williams said at a virtual event held by the Economic Club of New York, adding that he does not expect a recession.

James "Jim" Bullard, president and CEO of the Federal Reserve Bank of St. Louis, has said that rates need to go higher to bring inflation down. ''We've got a ways to go to get restrictive on policy.'' He also said the Fed ''will have to keep rates at a sufficiently high level all through 2023 and into 2024.''

GBP/USD technical analysis

The bears are moving on the trendline support. However, a correction could be on the cards first as illustrated on the hourly chart above. Nevertheless, the price is breaking out of a coil and a 100% measured move of the range will target the prior structure at 1.1900 and then a 200% measure move aligns with 1.1800.

- AUD/USD bears breaking 4-hour supporting trendline.

- 0.6650 and then 0.6580 will be key milestones to leave the bears fully in control with 0.6550 and 0.6500 eyed.

Protests against China's strict zero-COVID policy and restrictions on freedoms in the nation have led to a risk-off start to the week, weighing head8ily on the Aussie as the following technical analysis will show. AUD/USD is currently down some 1.13% having lost its footing from a high of 0.6727 to a low of 0.6665 on the day so far.

AUD/USD daily chart

The price is testing a meanwhile trendline support on the daily chart, with resistance in a double top at the daily structure, as shown on the chart above. The bias is on the downside as follows:

AUD/USD H4 chart

The 4-hour time frame sees the price testing below the trendline and after a correction into the Fibonacci scale, the bears have moved back in. This puts the focus on the recent lows of 0.6665. However, it will not be until the price break below 0.6650 and then 0.6580 that the bears will be in fully control with 0.6550 and 0.6500 eyed.

- The Canadian dollar extended its losses amid a risk-off mood.

- New York Fed President Williams said the Fed could hike in 2024.

- Canada printed a deficit on its current account, a headwind for the Loonie.

The Loonie (CAD) extended its losses to two straight days, though it trimmed some of its losses after the USD/CAD hit a daily high of 1.3473 but retreated toward the current spot price. Factors like China’s riot due to Covid-19 zero-tolerance policies and Federal Reserve (Fed) officials laying the ground for slower borrowing cost increases capped the USD/CAD rally. At the time of writing, the USD/CAD is trading at 1.3442, above its opening price.

Fed’s Williams shifted dovish, eyeing the first-rate cut

Risk aversion is the name of the game on Monday. Protests in China related to Covid-19 lockdowns and mass testing, and fears that if it escalates might derail the global economy, weighed on investors’ mood. Federal Reserve officials crossing newswires, led by the New York Fed President John Williams, said that the Fed could reduce rates in 2024, a dovish statement that caused a fall in the USD/CAD from 1.3452 to 1.3420s.

Earlier, Williams said he expects inflation to fall to 5.0%-5.5% by the end of 2022 and 3.0%-3.5% by late 2023 and noted that the baseline forecast does not predict a recession for the US. In the meantime, the St. Louis Fed President James Bullard said the Fed needs to keep increasing rates until 2023. He commented that rates must reach the low end of the 5%-7% rate range, adding that a recession is not inevitable.

Traders should remember that the Federal Reserve Open Market Committee (FOMC) minutes for the last meeting indicated that “A substantial majority of participants judged that a slowing in the pace of increase would likely soon be appropriate,” cementing the Fed’s moderating interest rates.

Of late, the Cleveland Federal Reserve President Loretta Mester stated that she does not believe that the Fed is close to a pause on tightening, reiterating its hawkish stance. Traders should know that Mester expects the FFR to end at around 5%.

Canada posted a current account deficit of C$11.1-billion ($8.3-billion) in the third quarter after surpluses in the first two quarters of 2022, data from Statistics Canada showed.

USD/CAD Key Technical Levels

Reuters reported that the New York Federal Reserve Bank President John Williams on Monday said that he believes the Fed will need to raise rates to a level sufficiently restrictive to push down on inflation, and keep them there for all of next year:

"I do think we're going to need to keep restrictive policy in place for some time; I would expect that to continue through at least next year," Williams said at a virtual event held by the Economic Club of New York, adding that he does not expect a recession.

"I do see a point, probably in 2024," when the Fed will start reducing interest rates, he said.

US Dollar update

The US Dollar is higher in the North American trade with US stocks on the backfoot amid a global risk-off start to the week. Major market averages opened trading on Monday lower as protests in China over COVID lockdowns brought some selling pressure to global equities.

Early on the Dow dipped 0.4%, the S&P 500 slid 0.5%, and the Nasdaq lost 0.4%. DXY is up 0.18% to 106.25, but the downside is open while below 106.60:

James "Jim" Bullard, president and CEO of the Federal Reserve Bank of St. Louis has said that rates need to go higher to bring inflation down.

Key comments

Estimates are all over the map on how many basis points qt is worth.

We've got a ways to go to get restrictive on policy.

On pace of hikes, I defer to chair Powell, doesn't matter that much in macro terms how quickly we get to right level.

Most important thing is we get to sufficiently restrictive level and that it is well understood by financial markets.

.

All will go better if we get to restrictive level sooner to make 2023 a year of disinflation

Situation calls for much higher interest rates that what we've been used to.

Will have to keep rates at sufficiently high level all through 2023 and into 2024.

Labor markets continue to be extremely strong.

Feedback from labor market to inflation is not as strong as many people portray.

Tight labor market gives us license to pursue disinflationary strategy now.

Still think we'll have below trend growth in 2023.

Recession is not inevitable.

- USD/JPY tumbled to a fresh three-month-low but rebounded towards 138.70s.

- A double bottom in the USD/JPY daily chart targets a rise to 145.00.

- USD/JPY Price Analysis: Break above 139.00 will exacerbate a rally to 140.00.

The USD/JPY is falling in the North American session, comfortable below the 139.00 figure after hitting a daily low of 137.49, reaching a fresh three-month low on a soft US Dollar (USD). At the time of writing, the USD/JPY is trading at 138.80, below its opening price by 0.25%.

USD/JPY Price Analysis: Technical outlook

After testing during the last month, the 137.00 mark, the USD/JPY rebounded strongly, reclaiming the 138.00 figure, signaling that buyers stepped in. A possible formation of a “double bottom” chart pattern around 137.50/60 could open the door for a recovery, which could target the 50-day Exponential Moving Average (EMA) at 144.67, as the initial target, on its way to 147.00. Notably, the Relative Strength Index (RSI) remained unchanged as the USD/JPY price action dived toward a multi-month low. Hence, a positive divergence between RSI and price action could pave the way for further USD/JPY upside.

If that scenario continues, the USD/JPY first resistance would be the 140.00 mark. The break above will expose the 100-day EMA at 141.17, followed by the 142.00 figure, and the 50-day EMA at 144.67. In an alternate scenario, the USD/JPY first support would be 138.00. Once cleared, the next support would be the multi-month low around 137.49, ahead of an upslope trendline around 137.00.

USD/JPY Key Technical Levels

Economists at Deutsche Bank see the S&P 500 at 4500 in the first half of next year while EUR/USD is likely to hit 1.15 by late 2023.

2023 should be a more positive year for Treasuries

“When it comes to financial markets, our baseline view is that the current bear market equity rally will continue for now, taking the S&P 500 up to 4500 in the first half of 2023. However, as the recession takes hold from mid-year, we are likely to see the index slumping back.”

“With the end of the Fed’s tightening cycle, and then a recession, it should be a more positive year for Treasuries, with the 10-year yield ending 2023 around its current levels at 3.65%, but bunds will underperform, in our view, with 10-year yields moving to 2.60%.”

“Finally in FX, we see a reversal in the Dollar’s upswing, with EUR/USD strongly moving back above 1.10, likely reaching 1.15 by late 2023.”

- Gold price tumbles below $1750 on traders’ negative sentiment, spurred by geopolitical reasons.

- China’s Covid-19 riots across the country keep Gold on the defensive.

- Soft US Dollar, courtesy of the Fed’s moderating rate hikes, stalled the XAU/USD downfall.

- US Dollar to get direction on a busy economic calendar in the United States.

- Gold Price Analysis: Neutral-upwards, but capped around the $1725-$1770 range.

Gold price edges lower as trading in the United States (US) begins after hitting a daily high of $1763.75. China’s protests about its Covid-19 zero-tolerance policy and its economic consequences weigh on sentiment even though Federal Reserve (Fed) officials laid the ground for moderated rate hikes. A busy economic calendar in the United States might cap last week’s losses in the US Dollar (USD) after the Fed’s dovish November minutes. At the time of writing, the XAU/USD is trading at $1747.11, below its opening price by 0.40%.

Negative sentiment spurred by China's crisis keeps Gold defensive

Global equities are trading in the red, spurred by China’s civil unrest, as protesters take the streets sparked by the Covid-19 zero-tolerance policy and mass testing. According to Bloomberg, “the protests are shaping up one of the biggest threats to the Communist Party since the 1989 Tiananmen crackdown,” keeping investors on their toes. However, Gold’s safe-haven status kept the yellow metal from falling further while also benefitting from a soft US Dollar.

Federal Reserve ready to moderate borrowing costs increases

Since the last couple of weeks, Federal Reserve policymakers opened the door to some moderation in the pace of interest-rate increases. However, they emphasized that inflation is too high and that the Federal Funds rate (FFR) peak would be higher than September’s projections. It should be noted that the Federal Reserve Open Market Committee (FOMC) minutes for the last meeting indicated that “A substantial majority of participants judged that a slowing in the pace of increase would likely soon be appropriate,” further confirming the aforementioned.

Of late, the Cleveland Federal Reserve President Loretta Mester stated that she does not believe that the Fed is close to a pause on tightening, reiterating its hawkish stance. Traders should know that Mester expects the FFR to end at around 5%.

Busy economic calendar in the United States

In the meantime, the US docket will be busy. On the labor market side, the release of November’s ADP Employment Change report, October’s JOLTs Job Openings, Initial Jobless Claims for the last week, and the Nonfarm Payrolls for November would update the employment situation. Regarding the PMIs, the ISM Manufacturing PMIs would be released alongside the Chicago PMI and the S&P Global PMI.

On the Fed speaking side, ahead of the blackout period, for the December meeting, Williams, Bullard, Cook, Bowman, Logan, Barr, Evans, and Powell will speak during the week.

Gold Price Analysis (XAU/USD): Technical outlook

XAU/USD remains neutral-upward biased, as shown by the daily chart. However, it should be noted that in the last week, Gold’s failure to crack the $1770 resistance exacerbated a fall towards $1725.71 the previous week’s low, but a “packed” economic calendar could impact the yellow metal price in the second half of the week.

Upwards, the XAU/USD first resistance would be $1750, followed by the daily high of $1761.18. As an alternate scenario, XAU/USD first support would be $1725.71, followed by the 100-day Exponential Moving Average (EMA) at $1711.74, followed by $1700.

Gold Price closed the choppy week virtually unchanged. The focus shifts to the highly-anticipated November jobs report from the US and coronavirus headlines from China, FXStreet’s Eren Sengezer reports.

China Covid jitters, US NFP to drive XAU/USD's action

“There won’t be any high-impact data releases on Monday and investors should stay focused on coronavirus headlines from China.”

“On Thursday, the ISM will release the Manufacturing PMI data for November. The market reaction to S&P Global’s PMI surveys suggests that the US Dollar might come under selling pressure if the ISM’s PMI report shows that price pressures continued to ease in November while the activity contracted. In that scenario, Gold could push higher with the initial reaction.”

“The US Bureau of Labor Statistics will publish labor market data for November on Friday. Nonfarm Payrolls (NFP) are projected to decline by 30K following October’s growth of 261K. A negative print is likely to weigh heavily on the US Dollar and open the door for a bullish XAU/USD action ahead of the weekend. On the other hand, a positive NFP surprise should have the opposite effect on financial markets and force Gold price to decline.”

- Euro rises on Monday on the back of hawkish comments.

- EUR/GBP finds support again at the 0.8570 zone.

The EUR/GBP is rising sharply on Monday, boosted by a stronger Euro across the board. The cross peaked at 0.8675, hitting the highest level since Wednesday. It is hovering around 0.8560, up more than 50 pips for the day so far.

Key support at 0.8570

Last week and also during October, the 0.8570 area capped the downside. The mentioned area continues to be a critical support that if broken would open the doors to more losses, targeting the 0.8500 area.

As long as the cross remains above 0.8570, losses seem limited. On the upside, the crucial resistance is seen at 0.8690/0.8700, the convergence of horizontal levels and the 20-day Simple Moving Average. A break above would strengthen the outlook for the euro.

Hawkish comments from ECB officials

European Central Bank President Christine Lagarde testified before the Committee on Economic and Monetary Affairs (ECON) of the European Parliament. She reiterated that interest rates will remain their main tool for fighting inflation. Earlier on Monday, ECB Governing Council member Klaas Knot pointed out that more tightening was necessary.

The comments boosted the euro across the board. EUR/USD hit a fresh multi-month high before pulling bank modestly while EUR/CHF peaked at 0.9888, a one-week high.

Technical levels

Federal Reserve Bank of Cleveland President Loretta Mester told the Financial Times that she didn't think that the Federal Reserve was near a pause in interest rate rises. Mester noted that she would need to see several more good inflation reports and more signs of moderation.

"It’s very easy to be caught out by the good news, but we don’t want wishful thinking to take the place of really compelling evidence", Mester explained and added that costs of stopping too early would be too high.

Market reaction

The US Dollar Index, which dropped to a multi-month low of 105.32, has gone into a recovery phase in the early American session and was last seen losing 0.12% on the day at 105.94.

Brent Crude Oil has broken below the key support level of $83.00. Strategists at Société Générale note that the next targets are located at $79.20/$77.50, then $73.00.

Resistance aligns at $86.80

“Breakdown below the low of September affirms persistence in decline. Next potential objectives are at $79.20/$77.50, the 50% retracement of the whole uptrend since 2020 and projections of $73.00.”

“Recent pivot high near $86.80 is near-term resistance.”

See: WTI renews yearly low as Coronavirus woes join fears of higher supplies, Oil price cap

- EUR/USD trims part of the earlier advance to the 1.0500 zone.

- The dollar attempts a rebound from initial multi-month lows.

- Lagarde notes high inflation is dampening spending and production.

The still soft note in the dollar motivates EUR/USD to keep the upside bias well and sound above the 1.0400 barrier.

EUR/USD firm on USD-selling

EUR/USD trims part of its earlier advance to the boundaries of 1.0500 the figure at the beginning of the week on the back of the so far lacklustre recovery in the dollar, while yields keep the inconclusive performance on both sides of the Atlantic so far on Monday.

Nothing scheduled in the euro docket leaves all the attention to the speech by Chair Lagarde before the European Parliament. In fact, Lagarde notes that interest rates remain the exclusive tool for fighting inflation and that fiscal policy must be considerate and not add to inflationary pressures. Lagarde also said that inflation risks remain on the upside, at the time when she declined to comment on whether inflation has peaked.

In the US docket, the Dallas Fed Manufacturing Index is due next ahead of the speech by New York Fed J.Williams.

What to look for around EUR

EUR/USD remains firm and manages to surpass once again the 1.0400 hurdle on the back of some renewed weakness in the dollar amidst alternating risk appetite trends.

In the meantime, the European currency is expected to closely follow dollar dynamics, the impact of the energy crisis on the region and the Fed-ECB divergence. In addition, markets repricing of a potential pivot in the Fed’s policy remains the exclusive driver of the pair’s price action for the time being.

Back to the euro area, the increasing speculation of a potential recession in the bloc emerges as an important domestic headwind facing the euro in the short-term horizon.

Key events in the euro area this week: ECB Lagarde (Monday) - EMU Final Consumer Confidence, Economic Sentiment, Germany Flash Inflation Rate (Tuesday) - Germany Unemployment Rate, Unemployment Change, EMU Flash Inflation Rate (Wednesday) - Germany Retail Sales, ECB General Council Meeting, Germany/EMU Final Manufacturing PMI, EMU Unemployment Rate (Thursday) - ECB Lagarde, Germany Balance of Trade (Friday).

Eminent issues on the back boiler: Continuation of the ECB hiking cycle vs. increasing recession risks. Impact of the war in Ukraine and the persistent energy crunch on the region’s growth prospects and inflation outlook. Risks of inflation becoming entrenched.

EUR/USD levels to watch

So far, the pair is gaining 0.48% at 1.0434 and faces the next up barrier at 1.0496 (monthly high November 15) ahead of 1.0500 (round level) and finally 1.0614 (weekly high June 27). On the flip side, a breach of 1.0222 (weekly low November 21) would target 1.0032 (100-day SMA) en route to 0.9935 (low November 10).

While Gold is not a strategic asset class, there are tactical reasons to consider adding it. See three ways to go about it, according to strategists at Morgan Stanley.

Physical Gold

“Investors can buy Gold bars and coins. Investors may pay a premium over the spot price of Gold. Storage fees usually apply. Investors can also take delivery of physical Gold if they want to store it themselves. In such cases, delivery fees would apply.”

Gold funds that own the metal

“Some mutual funds and exchange-traded funds offer investors exposure to Gold. For funds that offer the most direct exposure, their value tracks the price of Gold. The fund shoulders the cost of holding physical supply and passes it along to the investors in the expense ratio. There are some drawbacks: Some Gold funds are taxed as collectibles, so they don’t benefit from the lower long-term capital-gains rates for which stocks may qualify. Plus, they don’t produce any income, so the expense ratio can eat into principal every year.”

Mining companies

“Investors can get exposure through equity in companies that mine for Gold, including the purchase of individual stocks or as part of a fund.”

- EUR/USD climbs to multi-month highs near 1.0500.

- Extra gains look likely beyond the 1.0500 hurdle.

EUR/USD picks up extra upside traction and pokes with the key barrier at 1.0500 the figure on Monday.

Once 1.0500 is cleared, the pair is expected to refocus on the weekly peak at 1.0614 (June 27) ahead of the June top at 1.0773 (June 9) and the May high at 1.0786 (May 30).

Above the 200-day SMA (1.0382), the pair’s outlook should remain constructive.

EUR/USD daily chart

The GBP/USD spotlight turns to its 200-Day Moving Average (DMA), currently seen at 1.2176. Economists at Credit Suisse expect Cable to struggle to surpass this hurdle.

Support at 1.2025 needs to hold to keep the immediate risk higher

“We look for the 200 DMA, now at 1.2176, to cap at first on a closing basis for some fresh consolidation. However, our bias would be to view a pause again as temporary, ahead of a close above the 200 DMA in due course for a test of the 50% retracement of the 2021-2022 fall and August highs at 1.2278/98. Our bias remains to look for this to then cap to define the top of a broader range. Should strength directly extend, we see resistance next at 1.2668.”

“Support at 1.2025 needs to hold to keep the immediate risk higher. Below can see a setback to 1.1958/52, then the 13 DMA and price support at 1.1910/00 but with fresh buyers expected to show here.”

While testifying before the Committee on Economic and Monetary Affairs (ECON) of the European Parliament in Brussels, European Central Bank (ECB) President Christine Lagarde reiterated that interest rates will remain their main tool for fighting inflation.

Additional takeaways

"In December, we will also lay out the key principles for reducing the bond holdings in our asset purchase programme portfolio."

"It is appropriate that the balance sheet is normalised over time in a measured and predictable way."

"How much further rates need to go, and how fast, will be based on our updated outlook, the persistence of the shocks, the reaction of wages and inflation expectations, and on our assessment of transmission."

"Strong labour markets are likely to support higher wages."

"Fiscal policy needs to be considerate to not add to inflationary pressures."

"Incoming data suggest that wages are picking up, and we will continue to assess their implications."

"Rate adjustments will take some time to be felt in the economy."

"Growth is expected to continue weakening for the remainder of this year and the beginning of next year."

Market reaction

EUR/USD retreated from the multi-month high it touched near 1.0500 earlier in the day and it was last seen trading at 1.0445, where it was up 0.5% on the day.

- The index resumes the downtrend and revisits the 105.30 region.

- The loss of the 200-day SMA opens the door to extra losses.

The US Dollar Index (DXY) comes under extra selling pressure and extends the breakdown of the key 106.00 barrier at the beginning of the week.

The selling pressure motivates the index to flirt with the always relevant 200-day Simple Moving Average (SMA), today at 105.36. A drop below the latter is expected to allow for losses to accelerate and target the August low at 104.63 (August 10).

South of the 200-day SMA, the outlook for the index should shift to bearish.

DXY daily chart

- GBP/USD reverses an intraday dip amid the emergence of heavy selling around the USD.

- Spot prices lack bullish conviction and remain below a technically significant 200-day SMA.

- The said hurdle coincides with ascending channel resistance and should act as a pivot point.

The GBP/USD pair attracts some buying near the 1.2025 region on Monday, albeit struggles to capitalize on the modest intraday uptick. The pair seesaws between tepid gains/minor losses through the early North American session and now seems to have stabilized in neutral territory, around the 1.2060 area.

The US Dollar comes under heavy selling pressure amid rising bets for a relatively smaller Fed rate hike in December and turns out to be a key factor offering support to the GBP/USD pair. That said, the risk-off mood helps limit the downside for the safe-haven buck. Apart from this, a bleak outlook for the UK economy contributes to capping any meaningful gains for the major.

From a technical perspective, spot prices have been trending higher along an upward-sloping channel over the past two months or so. The top boundary of the said channel, currently around the 1.2170-1.2175 zone, coincides with the very important 200-day SMA. This should now act as a pivotal point, which if cleared decisively will be seen as a fresh trigger for bullish traders.

Meanwhile, oscillators on the daily chart are holding in the positive territory and are still far from being in the overbought zone, favouring bullish traders. That said, it will still be prudent to wait for a convincing breakout through the aforementioned confluence hurdle before positioning for any further appreciating move towards the 1.2270-1.2275 resistance zone.

On the flip side, the daily swing low, around the 1.2025 area, could protect the immediate downside ahead of the 1.2000 psychological mark. Any further decline is more likely to attract fresh buyers and remain limited near the 1.1965 horizontal support. Failure to defend the said support levels will make the GBP/USD pair vulnerable to weakening further below the 1.1900 mark.

The corrective decline could drag spot prices towards the next relevant support near the 1.1845-1.1840 region en route to the 1.1800 mark. Some follow-through selling will expose the 1.1730 intermediate support, the 1.1700 round figure and the 100-day SMA, currently around the 1.1650-1.1640 area.

GBP/USD daily chart

Key levels to watch

NZD/USD’s gains late last week have been halted at the 200-Day Moving Average (DMA) at 0.6296. This barrier is likely to remain a cap for now in the near term, in the opinion of analysts at Credit Suisse.

Kiwi has rejected the 200DMA at 0.6296

“NZD/USD has seen a tentative rejection of major resistance at the 200DMA and the trendline from June at 0.6296/6304. With this rejection in place and daily RSI now again hovering close to overbought levels, we think another pause is likely to unfold. That said, should a break above .here be seen and a break below the 200DMA in the DXY also take place, this would be seen to signal further medium-term strength, with next key resistance seen at the August highs at 0.6456/68.”

“Near-term support is seen at 0.6162/58 and then at the 13-Day Exponential Average at 0.6135, though only below the recent lows at 0.6062/60 would bring more near-term stability.”

- AUD/USD edges lower for the second successive day, though lacks follow-through selling.

- China’s COVID-19 weigh on investors’ sentiment and undermines the risk-sensitive Aussie.

- The USD remains depressed amid bets for less aggressive Fed rate hikes and offer support.

The AUD/USD pair opens with a modest bearish gap on the first day of a new week and remains depressed through the early North American session. The pair, however, rebounds a few pips from a three-day low and now seems to have stabilized around the 0.6700 round-figure mark.

The global risk sentiment takes a hit amid the worsening COVID-19 situation in China and drives flows away from the perceived riskier Australian Dollar. In fact, China reported a record-high number of daily infections on Saturday. Moreover, the public discontent and widespread protests over the Chinese government's zero-COVID policy raise concerns about a further slowdown in economic activity. This, in turn, triggers a fresh wave of the risk-aversion trade, though the emergence of heavy US Dollar selling helps limit the downside for the AUD/USD pair.

The November FOMC meeting minutes released last week cemented market bets for a relatively smaller 50 bps rate hike by the US central bank in December. This, along with the flight to safety, contributes to the ongoing downfall in the US Treasury bond yields and drags the USD back closer to the monthly low. The fundamental backdrop makes it prudent to wait for strong follow-through selling before confirming that the AUD/USD pair has topped out. Moreover, absent relevant market-moving economic releases further warrant some caution for aggressive bearish traders.

Market participants now look for speeches by influential FOMC members - St. Louis Fed President James Bullard and New York Fed President John Williams. This, along with the US bond yields and the broader risk sentiment, will drive the USD demand and provide some impetus to the AUD/USD pair. The focus, however, will remain on this week's important US macro data, including the closely-watched monthly jobs report (NFP) and fresh developments in China.

Technical levels to watch

GBP/USD trades slightly below the 1.21 level. The pair needs to clear the 1.2080/90 region to open up room for further gains, economists at Scotiabank report.

Key support aligns at 1.2000/10

“Cable is trying to break out of last week’s bull flag consolidation (ceiling resistance at 1.2082). A clear move through the 80/90 zone should see the pair pick up a little more momentum – and perhaps allow the GBP to play catch up with the EUR to some extent – towards 1.2150/55.”

“Key support is 1.2000/10.”

USD/JPY is falling sharply again. Economists at Credit Suisse stay bearish for an eventual test of the 200-Day Moving Average (DMA), now at 134.09.

Initial resistance seen at 139.00

“We maintain our core bearish outlook and we look for an eventual sustained break lower for a test of the 200DMA, now at 134.09. We would not rule out an overshoot to the 38.2% retracement of the 2021/2022 uptrend not far below at 133.09, but we continue to look for a floor in this 134/133.09 zone.”

“Resistance is seen at 139.00 initially, with a break above 139.46/60 needed to ease the immediate downside bias for a recovery back to the 13DMA at 140.63, but with fresh sellers expected here.”

EUR/USD has reached its highest since the summer. Economists at Scotiabank believe that the pair could hit the 1.06 region.

Test of the low 1.05 area is beckoning

“A test of the low 1.05 area (50% retracement of the 2022 decline) is beckoning.”

“Broader trends are bullish, with the EUR trading above its 200-day MA and finding additional support from bullishly aligned DMI (trend strength) oscillators.”

“Further gains to the low 1.06 region are possible.”

See: EUR/USD could trade back up to the 1.0480/1.0500 area again – ING

- USD/JPY dives to a fresh three-month low on Monday and is pressured by a combination of factors.

- Bets for less aggressive Fed rate hikes and sliding US bond yields continue to weigh on the USD.

- The risk-off mood benefits the safe-haven JPY and also contributes to the sharp intraday decline.

The USD/JPY pair kicks off the new week on a downbeat note and dives to a fresh three-month low during the mid-European session. Spot prices, however, rebound a few pips from the 137.50 area and climb back above the 138.00 mark in the last hour.

The US Dollar fails to capitalize on its modest intraday uptick and comes under heavy selling pressure amid the prospects for a less aggressive policy tightening by the Fed. In fact, the USD Index, which measures the greenback's performance against a basket of currencies, dives back closer to the monthly low and turns out to be a key factor exerting pressure on the USD/JPY pair.

The November FOMC meeting minutes released last week cemented bets for a relatively smaller 50 bps rate hike by the US central bank in December. This is reinforced by the ongoing downfall in the US Treasury bond yields, narrowing the US-Japan rate differential. Apart from this, the risk-off mood benefits the safe-haven Japanese Yen and contributes to the USD/JPY pair's intraday decline.

Investors remain worried about a new COVID-19 outbreak in China and the imposition of strict lockdown measures in several cities. Furthermore, a wave of protests in China over the government’s zero-COVID policy takes its toll on the risk sentiment. Apart from this, technical selling below last week's swing low, around the 138.00 mark, aggravates the bearish pressure surrounding the USD/JPY pair.

That said, the Fed-BoJ policy divergence helps limit deeper losses and assists spot prices to find decent support near the mid-137.00s, at least for the time being. In the absence of any relevant economic data from the US, traders on Monday will take cues from speeches by influential FOMC members - St. Louis Fed President James Bullard and New York Fed President John Williams.

This, along with the US bond yields, will drive the USD demand and provide some impetus to the USD/JPY pair. Adding to this, the broader risk sentiment should allow traders to grab short-term opportunities ahead of the Japanese Unemployment Rate and Retail Sales figures, due for release during the Asian session on Tuesday.

Technical levels to watch

- EUR/JPY adds to Friday’s uptick and approaches 145.00.

- Next on the upside comes the minor hurdle at 146.13.

EUR/JPY extends the recent rebound to the vicinity of the 145.00 neighbourhood at the beginning of the week.

The cross manages to leave behind the earlier pullback to the 143.00 region and now targets the 145.00 zone. The continuation of the bounce exposes a potential test of the weekly high at 146.13 (November 23) in the short term.

In the longer run, while above the key 200-day SMA at 138.83, the positive outlook is expected to remain unchanged.

EUR/JPY daily chart

Recently, the British Pound has rallied largely alongside risk appetite. As the external backdrop is set to improve, economists at HSBC expect the GBP to strengthen against the USD in 2023.

GBP outperformance, despite challenging UK outlook

“The prospect of a fiscal deficit of around 5% of GDP next year is likely to keep structural concerns about the GBP to the fore, but at least the situation is not set to get worse. This may be enough to support a currency that has weakened so much already, especially as there are early signs that the trade balance has begun to improve.”

“The domestic situation is likely to remain challenging, but external sentiment has been the dominant factor for the GBP in recent years. In an environment where global growth bottoms out, rate volatility peaks, and risk sentiment picks up, the GBP is likely to benefit in 2023.”

The Indian Rupee is set to remain within the 80-83 range against the US Dollar as the Reserve Bank of India (RBI) will be involved in FX intervention, economists at Deutsche Bank report.

RBI to be proactively involved in FX intervention

“We expect the RBI to be proactively involved in FX intervention, to keep Rupee broadly within the 80-83 range, though we don't rule out intermittent overshoot and undershoot from time to time.”

“We expect USD/INR to be around 82.50 levels by end-Dec'23.”

As far as the need for replenishing FX reserves are considered, one potential positive could be if DXY continues to weaken meaningfully through 2023. This can then add to valuation gains for INR and push up FX reserves (in contrast to the large valuation losses that have led to the depletion in India’s FX reserves in 2022).”

USD/JPY pushes lower and trades below 138.00 for the first time in two weeks. A break under 137.68/137.00 would open up projections of 135.40 and the 200-Day Moving Average near 134.00, economists at Société Générale report.

Initial resistance seen at 139.60

“Daily MACD is in deep negative territory denoting an overstretched move however signals of a meaningful up-move are not yet visible.”

“The pair is close to the low formed earlier this month near 137.68/137.00. Failure to defend this can extend the decline towards projections of 135.40 and 200DMA near 134.00.”

“First resistance is at 139.60.”

- Gold price climbs to a one-week high on Monday and draws support from a combination of factors.

- Bets for less aggressive rate hikes by the Federal Reserve weigh on the US Dollar and offer support.

- China’s COVID-19 woes weigh on investors’ sentiment and further benefit the safe-haven XAU/USD.