- Analiza

- Novosti i instrumenti

- Vesti sa tržišta

Forex-novosti i prognoze od 26-05-2023

Reuters reported that the US Treasury Secretary Janet Yellen spoke on Friday and extended the deadline for raising the federal debt limit, saying the government could default on its debt as early as June 5 without increasing the country's $31.4 trillion debt ceiling.

Yellen had previously put that date as in early June, or potentially as early as June 1.

Meanwhile, the US Dollar was set for a third straight weekly gain on Friday. The US Dollar index DXY, which tracks the currency against six major counterparts, was last at 104.23%.

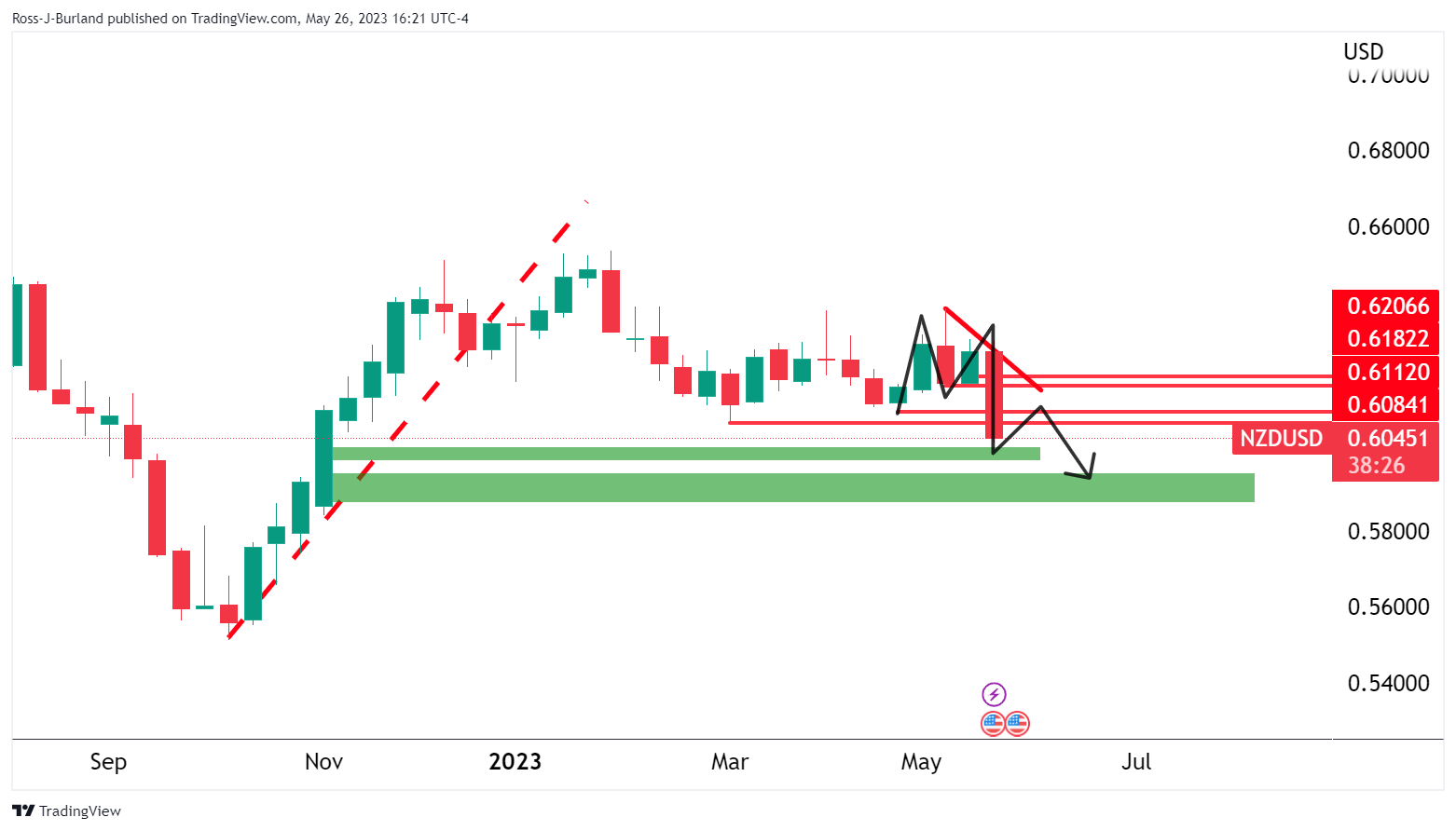

- NZD/USD bears eye a continuation below structure.

- Bulls could be lurking at a key area of potential support.

NZD/USD remains on the backfoot following the Reserve Bank of New Zealand confirming it would ease mortgage loan-to-value ratio (LVR) restrictions from June 1. The technical outlook is bearish for the meanwhile, but there could be prospects of a bullish correction for the week ahead as the following illustrates.

NZD/USD weekly chart

The weekly chart shows the M-formation´s last leg penetrating prior lows that might be regarded as stucture and such a move signifies a market that is breaking down. However, in the meanwhile, a correction could be coming up.

NZD/USD daily chart

The market is headed toward a support structure but should the bulls turn up, a correction towards 0.6080-0.6112 could be on the cards.

- WTI crude oil closes higher, settling at US$72.67 per barrel, driven by mixed signals from OPEC+ regarding production cuts.

- Ongoing talks between the Biden Administration and House Republicans bring relief as a deal to raise the US debt ceiling nears completion.

- US inflation surges as consumer spending exceeds expectations, with the personal consumption expenditures index rising by 4.4% annually.

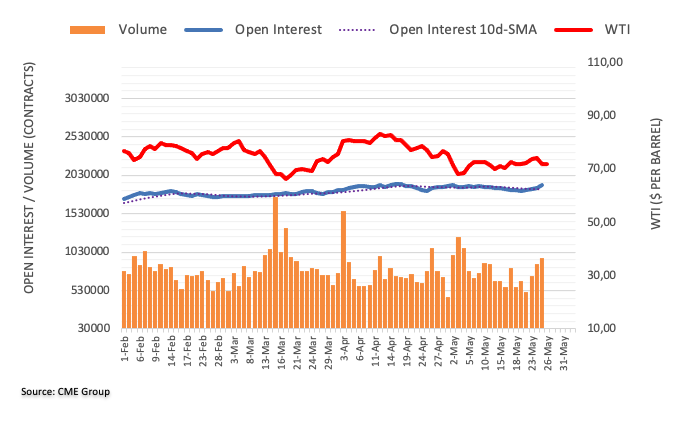

Western Texas Intermediate (WTI), the US crude oil benchmark, recovered some lost ground during the week, driven by factors like mixed signals from OPEC+ regarding potential output cuts, ongoing discussions between US politicians about the debt ceiling, and higher-than-expected US inflation.

Mixed signals from OPEC+, progress in US debt-ceiling talks, and higher inflation are impacting the rise of WTI crude oil prices

WTI crude oil trades with gains of $0.99 or 1.35% after hitting a daily low of $71.54, exchanging hands at $72.75 per barrel.

The rise in oil prices comes as conflicting statements emerged from OPEC+'s significant producers. Russia expressed its expectation that there would be no alteration to production quotas during the cartel's meeting, citing the voluntary cuts of over one million barrels per day implemented at the beginning of May. Conversely, Saudi Arabia's oil minister cautioned short sellers to remain vigilant.

The upward trajectory of oil prices also corresponds with reports of progress in negotiations between the Biden Administration and House Republicans concerning a deal to raise the US debt ceiling for two years. This development alleviates concerns that the country would face an unprecedented default on its debt payments.

However, recent data from the US reveals stronger-than-expected consumer spending in the previous month, which increased by 0.5% following a stagnant performance in March. Additionally, the Personal Consumption Expenditures (PCE) index, the Federal Reserve's preferred inflation gauge, rose by 4.4% annually, surpassing the 4.2% growth reported in March.

WTI Technical Levels

- EUR/JPY maintains a bullish outlook, on its weekly high around 150.80.

- Tokyo Consumer Price Index (May) came in below consensus as well as previous values.

- Gross Domestic Product figures from Q1 from Germany came in surprisingly weaker than expected.

The EUR/JPY pair maintains its gains, continuing its upward trajectory for the third consecutive day. Currently, it is oscillating above the significant 150.00 level, signaling a strong bullish sentiment. Despite the recent weakness in Germany's Q1 Gross Domestic Product figures, the pair maintains a positive outlook, even reaching its weekly high around 150.80. However, it is essential to consider the impact of the Tokyo Consumer Price Index (May), which has recently disappointed, falling below both consensus expectations and previous values. Consequently, bond yields have declined, on expectations the Bank of Japan (BoJ) will maintain its age-old ultra-loose stance on interest rates.

Declining German and Japanese yields

German yields have weakened across the curve. The 10-year bond yield experienced a decline to 2.52%, resulting in losses of 0.72% for the day. Similarly, the 2-year yield stands at 2.96% with losses of 0.6%, while the 5-year yield is at 2.54%, showing losses of 0.72%.

In addition, the Japanese yields have also weakened across the curve. The 10-year bond yield dropped to 0.41%, resulting in significant losses of 1.66% for the day. Furthermore, the 2-year yield stands at -0.07% with losses of 3.91%, and the 5-year yield is at 0.10%, showing substantial losses of 8.02% respectively.

Levels to watch

The EUR/JPY has a bullish outlook for the short term, as per the daily chart. The Relative Strength Index (RSI) and Moving Average Convergence Divergence (MACD) are both in positive territory and the pair trades above its main moving averages, indicating that the buyers are in charge.

In case the EUR/JPY exchange rate continues to gain traction, the following resistance levels line up at the psychological mark of 151.00, followed by the monthly high at 151.60 and the 152.00 zone. On the other hand, immediate support for EUR/JPY is seen at the 150.00 level, followed by the 149.20 zone and the 20-day Simple Moving Average at 148.97.

-638207290495151122.png)

- USD/CAD bulls run into a wall of resistance.

- USD/CAD bears are moving in with 1.3570 eyed.

USD/CAD is on track to post a weekly gain as the recent rise in US bond yields helped underpin the greenback. However, a correction is taking place as the following will illustrate.

The price has come up to test a resistance zone but is starting to correct:

A 50% mean reversion comes in near prior resistance near 1.3570.

On the hourly chart above, we can see that the price is capped in resistance and is making lower highs as the rally decelerates. The market is breaking down on the backside of the prior bullish rally with 1.3570 eyed.

- USD/JPY leaps past the 140.00 mark, despite US economic data suggesting a potential Fed rate hike.

- Japanese Finance Minister Shunichi Suzuki encourages market-determined currency rates, stating that he’s closely monitoring exchange-rate movements.

- USD/JPY, poised to challenge 142.00 once it clears 141.00, finds support at 139.89/140.00, with a deeper fallback to 137.26.

USD/JPY rallied sharply past the 140.00 figure on Friday late in the New York session, after traveling towards its daily low of 139.49, before making a U-turn. Solid economic data from the United States (US) bolstered the odds for another rate hike by the Federal Reserve (Fed), as shown by the market reaction. US Treasury bond yields rose before reversing their course, while the US Dollar weakened. At the time of writing, the USD/JPY is trading at 140.60.

USD/JPY Price Analysis: Technical outlook

After hitting a new year-to-date (YTD) high of 140.72, the USD/JPY retraced somewhat but remains upward biased. Once the USD/JPY cracked the November 30 swing high of 139.89, buyers piled in to break the 140.00 figure despite Japanese Finance Minister Shunichi Suzuki saying that markets should set currency rates based on economic fundamentals. He stated that he’s watching exchange-rate moves closely.

During Friday’s session, USD/JPY continued and extended its gains, but the pair lost momentum as the New York session began to wind down. However, if USD/JPY extends its gains past 141.00, the next resistance would be the 142.00 figure, ahead of testing the November 22 High at 142.24.

Conversely, the USD/JPY first support would be the 140.00 mark, ahead of falling to November 30 previous resistance turned support at 139.89. A dip below could clear the way for the pair to fall toward December 15 daily high at 138.17 before reaching the 20-day Exponential Moving Average (EMA) At 137.26.

USD/JPY Price Action – Daily chart

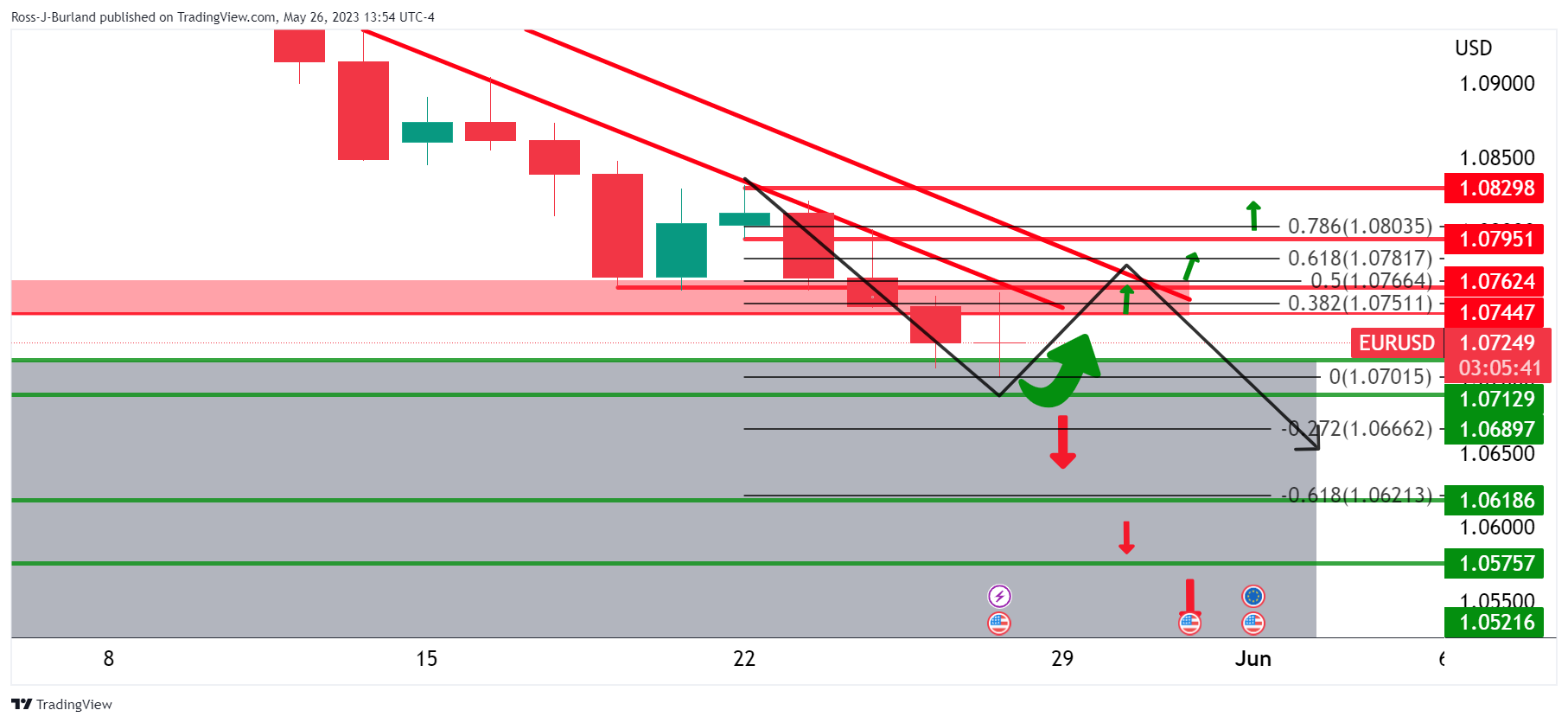

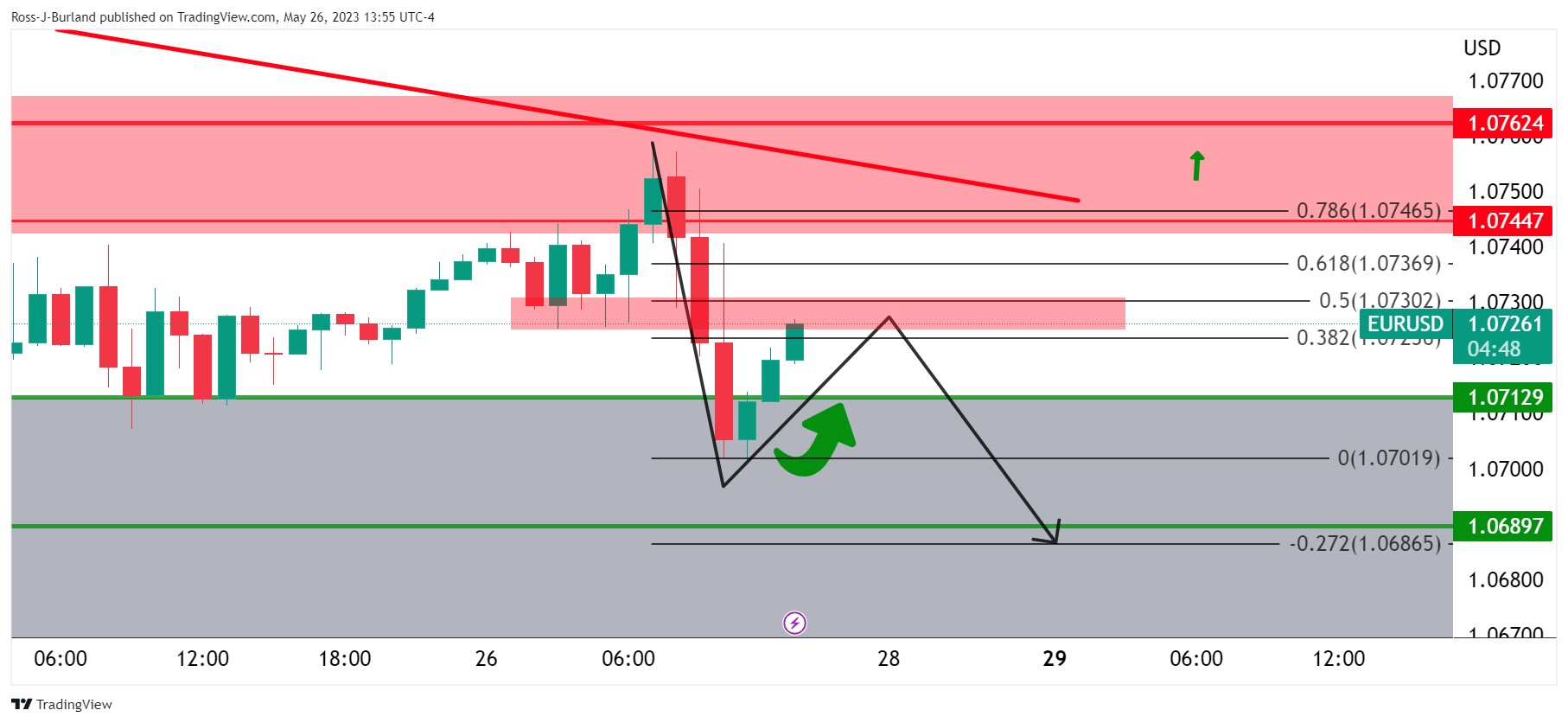

- EUR/USD is on the front side of the bearish trend, submerged in the low 1.07s.

- Bears eye a downside extension for the coming days while below 1.0800.

EUR/USD hit a 9-week low of 1.0701 on the US Dollar´s strength as expectations increased that the US Federal Reserve will deliver another rate hike. The market is penetrating into a key area of potential support as the following will illustrate:

EUR/USD daily charts

As illustrated in the above daily charts, the price is submerged below the trendline resistance and touching into a space that could give way to a move even lower in the coming days.

On the hourly chart, the price has broken structure on the left and has found demand around 1.0700. However, if resistance holds, we could see the start of the downside extension.

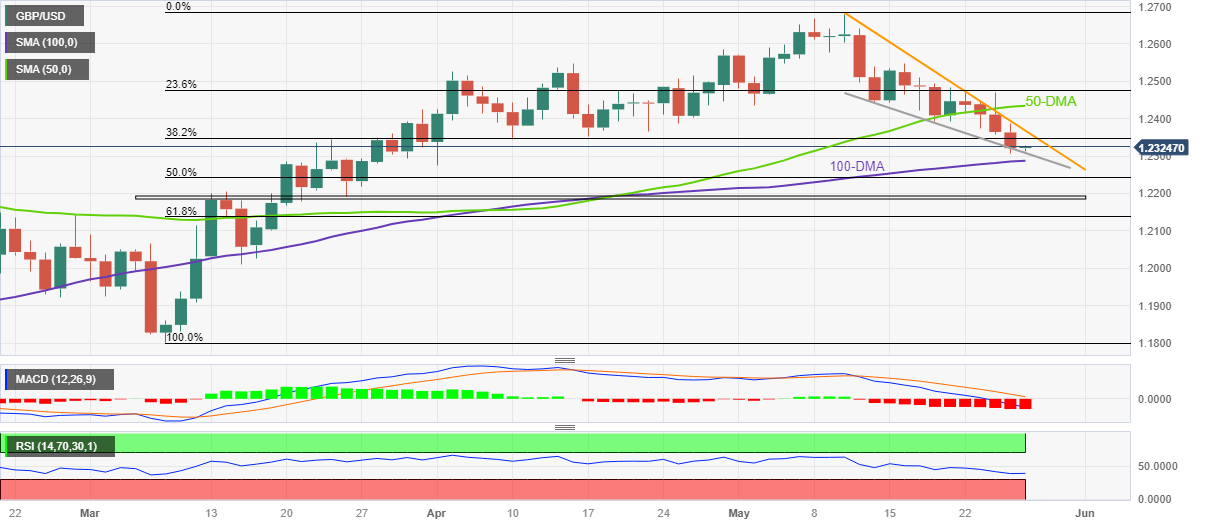

- GBP/USD recovered from weekly lows, maintaining a position above the 1.2300 figure, while US Treasury bond yields reached their highest since March.

- The Core PCE, Fed’s preferred inflation measure, climbed to 4.7% YoY in April, pushing the odds of a 25 bps rate increase in June to 65.4%.

- Retail sales in the UK skyrocket, reaching their fastest pace in nearly two years, fueling market expectations of a significant bank rate increase, potentially up to 5.50%.

GBP/USD regained some composture past the mid-North American session and bounced off the weekly lows, clinging above the 1.2300 figure amidst a week that witnessed solid US and UK data. Therefore, the GBP/USD stays positive in the day, gains 0.19%, and trades around 1.2340s.

Solid economic data set the stage for possible Fed’s June rate hike, UK Retail Sales at its fastest pace in almost two years

US equities continue to run the Artificial Intelligence (AI) frenzy underpinned by NVIDIA and Maxwell Technologies. The latest tranche of US economic data, with the Fed’s preferred gauge for inflation, the Core PCE rising to 4.7% YoY in April, and headline PCE hitting 4.4% YoY, has increased the odds for additional tightening by the Federal Reserve, with both figures exceeding estimates and previous data. Odds for a 25 bps increase at the June meeting stand at 65.4%, higher than the 17.4% a week before solid data from the US derailed the Fed’s plan to keep rates unchanged.

At the same time, Durable Good Orders printed a positive reading of 1.1% MoM in March, exceeding estimates but showing signs of slowing down, as trailed by March’s 3.3%. Later, the University of Michigan (UoM) Consumer Sentiment exceeded estimates of 57.7 at 59.2 but trailed the 63.5 previous data. Americans inflation expectations cooled down for a one-year horizon is expected at 4.1%, less than the 4.5% revealed in the last report, while for the 5-year horizon, it came at 3.1%, above April’s 3.0%.

Given the backdrop, US Treasury bond yields advance, with the 10-year benchmark note rate at 3.851%, its highest level since March 10, a headwind for the GBP/USD exchange rate. The greenback strengthened, as shown by the US Dollar Index (DXY), up 0.04%, at 104.255. If the DXY achieves a daily close above the 103.752 area, that would confirm the buck’s bullish bias.

Recently, the Cleveland Fed President Loretta Mester stood to her hawkish stance and confirmed that inflation is too high in an interview on CNBC. She said that she would revise her forecast for inflation and that more data would help her to decide on the June meeting while emphasizing that “everything is on the table” for the next FOMC decision.

Aside from this, US debt ceiling talks continued and will resume over the weekend, with both sides confident of achieving a deal before the US Treasury runs out of cash by June 1.

On the UK front, Retail Sales rose to its highest pace in almost two years. That, alongside high inflation data revealed during the week, spurred a reaction in the swaps markets, with most traders expecting at least 100 bps of increase to the bank rate, which would reach 5.50%.

GBP/USD Technical Levels

- USD/CHF surpasses the 0.9050 zone, marking a breakthrough in this resistance.

- The RSI remains in positive territory, approaching the 58.20 level, sustaining a bullish momentum.

- The currency pair is making efforts to reach the 0.9100 level, following three days of gains.

The USD/CHF pair has maintained a neutral stance on Friday but with a positive outlook as it recently surpassed the resistance at the 0.9050 zone and maintains its bullish momentum for the short term. On the daily chart, the Relative Strength Index (RSI) remains in positive territory and is approaching the 58.20 level, while the Moving Average Convergence Divergence (MACD) continues to print green bars. Over the past four days, the pair has shown consistent gains and is striving to reach the 0.9135 level (100-day Simple Moving Average). In that sense, the USD/CHF holds a neutral to bullish bias outlook for the short term.

Levels to watch

If the pair continues to gain momentum, the following resistance levels come into play: first, at the 0.9080 zone, followed by the 0.9100 level, and at the mentioned 0.9135 level. Conversely, immediate support for USD/CHF can be found at the 0.9050 zone level, followed by the 0.9000 level and the 20-day Simple Moving Average (SMA) at 0.8950.

Kristalina Georgieva, Managing Director of the International Monetary Fund, has crossed the wires with the following comments:

- US economy has proven resilient in face of significan fiscal and monetary tightening -article iv review statement.

- Expects US growth to be around 1.2% in 2023, picking up momentum later in 2024.

- US unemployment to rise slowly to close to 4.5% by end-2024.

- Strength in US demand and labor market means a persisten inflation problem.

- Core US inflation will continue to fall during 2023, but remain 'materially above' 2% fed target throughout 2023 and 2024.

- Will be essential for fed to communicate carefully on policy path.

- US interest rates will need to be higher for longer.

- US needs to do more to lower the public debt.

- We are very keen to see a u.s. debt ceiling resolution as soon as possible

- Silver price returns from two-month lows, crosses the 200-day EMA and $23 threshold and ends the week with a 2.89% loss.

- Despite US data supporting another Fed rate hike and subsequent rise in Treasury bond yields, silver price sustains an upward trajectory, targeting the 100-day EMA.

- With the Relative Strength Index indicating potential silver weakness, downside risk remains.

Silver price bounces off two-month-lows hit at $22.68, rallies sharply, and claims the 200-day Exponential Moving Average (EMA) at $22.82 and the $23.00 psychological figure on Friday’s mid-North American session. Although the white metal is gaining more than 1.90%, it is set to finish the week with losses of 2.89%. At the time of writing, XAG/USD is trading at $23.15.

Silver Price Analysis: XAG/USD technical outlook

Even though economic data from the United States (US) justifies another rate hike by the US Federal Reserve (Fed). Therefore, US Treasury bond yields are rising, underpinning the greenback. However, the XAG/USD ignored most factors that could drag the price low and rip higher, eyeing the 100-day Exponential Moving Average (EMA) at $23.47.

Nevertheless, the Relative Strength Index (RSI) is in bearish territory, warranting further Silver weakness, while the 3-day Rate of Change (RoC) has yet to reach neutral levels. Therefore, additional downside could be expected.

However, if XAG/USD clears the 100-day EMA, it would face sold resistance at the confluence of the 20 and 50-day EMAs at around $23.97-24.00. Once broken, the next supply zone would be the $25.00 mark.

On the flip side, and the path of least resistance in the near term, the XAG/USD first support would be $23.00, followed by $22.68, the current week’s low. A beach of the latter will expose the March 21 swing low of $22.14.

Silver Price Action – Daily chart

- AUD/USD sustains bearish momentum, hovers near the psychological level of 0.6500.

- Core PCE from the US rose to 4.7% in April.

- Australia’s Retail Sales rose 0.0% in April, falling short of expectations.

The AUD/USD continues its downward trend, currently trading at its year-low. However, this decline occurs amidst positive economic developments and hot Core PCE inflation from the US which made the market’s discount a higher likelihood of the Federal Reserve (Fed) hiking in the next meeting in June. On the other hand, the Australian Retail Sales from April data indicated no variation in sales levels compared to the previous period. Hence, the current data reported a stagnation.

Australia Retail Sales fall below expectations and markets price in a higher likelihood of a Fed rate hike

In April, the growth of Australian Retail Sales failed to meet expectations, remaining unchanged from March. This lackluster performance reflects the challenges faced by consumers due to the impact of rising interest rates and persistent inflation. With retail turnover falling short of the anticipated 0.2% increase, it indicates a period of stagnation in consumer spending over the past six months. Furthermore, the ongoing rise in the cost of living adds additional strain to consumers' budgets.

Adding to these challenges, the strength of the US Dollar has further contributed to the decline in the AUD/USD currency pair. Core PCE inflation from the US, an important gauge of inflation for the Federal Reserve (Fed), from April came in at 4.7% (YoY) vs the 4.6% expected and from its previous figure of 4.6%.

In that sense, following yesterday’s strong economic data and the hot inflation figures, the CME FedWatch Tool currently indicates a greater likelihood of the Federal Reserve raising interest rates by 0.25% on June 14 giving further support to the US Dollar.

Levels to watch

According to the daily chart, the AUD/USD maintains a bearish outlook in the short term, as indicated by the Relative Strength Index (RSI) and Moving Average Convergence Divergence (MACD), both suggesting that sellers are in control while the pair trades below its main moving averages.

In the event of a decline in the Aussie, immediate support levels are identified at the psychological level of 0.6500, followed by the zone around 0.6545 and the 0.6400 level. Conversely, if the AUD/USD manages to climb higher, the next resistance levels to monitor are at the 0.6540 zone, followed by the psychological level of 0.6600 and the 20-day Simple Moving Average at 0.6650.

-638207164541137858.png)

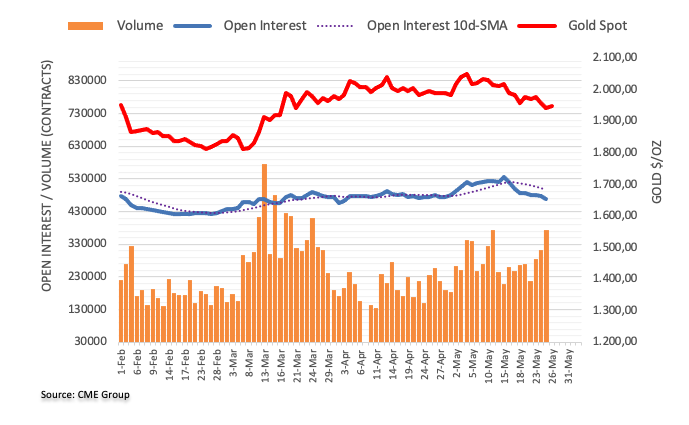

- US economic strength shown by the latest round of data raises prospects of a June Fed rate hike, boosting the US Dollar.

- Wall Street climbs despite a rise in Fed’s gauge for inflation, with Core PCE hitting 4.7% YoY.

- Rising US Treasury bond yields and Fed hawkish commentary could hurt Gold’s recovery.

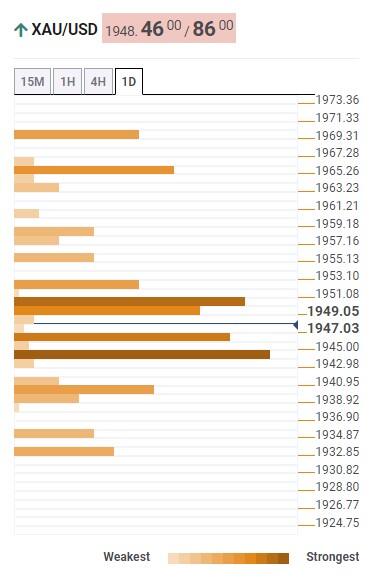

Gold price recovers some ground but remains shy of reclaiming the $1950 figure after solid economic data in the United States (US) suggests the Federal Reserve (Fed) could opt to hike again in June. Consequently, US Treasury bond yields are rising, while the US Dollar (USD) hits new two-month highs vs. a basket of peers. The XAU/USD is trading at $1940.21, still up by a minuscule 0.03%.

Wall Street rides high despite inflationary concerns; consumer and business spending showcase resilience

Wall Street registered solid gains, even though the Federal Reserve’s (Fed) preferred gauge for inflation, the Core Personal Consumption Expenditure (PCE), which strips volatile items like food and energy, exceeded estimates of 4.6% and rose by 4.7% YoY in April. Following suit, headline inflation climbed from 4.2% to 4.4% YoY after the Fed released its May meeting minutes, which showed the US central bank’s openness to pause its tightening cycle.

In another data, the final reading of the University of Michigan Consumer Sentiment for May, beat estimates of 57.7 at 59.2 but trailed the 63.5 prior’s reading. The same poll revealed that American citizens’ inflation expectations for one year eased from 4.5% to 4.1% by year’s end, while for a 5-year horizon, they came at 3.1% above April’s 3.0%.

Earlier, Durable Good Orders in April rose by 1.1% MoM, above estimates of a 1% plunge but trailed the staggering March’s 3.3%, indicating that consumer and business spending remains resilient, another reason that justifies Jerome Powell and Co. to continue to lift rates, as the economy opposes resistance to higher interest rates.

Consequently, US Treasury bond yields continued to rise, with the 10-year benchmark note rate at 3.851%, its highest level since March 10, putting a lid on Gold recovery. Another factor that could dent appetite for XAU/USD is US real yields, which stand at 1.60%, higher than Thursday’s close of 1.57%.

Recently, the Cleveland Fed President Loretta Mester stood to her hawkish stance and confirmed that inflation is too high in an interview on CNBC. She said that she would revise up her forecast for inflation and that more data would help her to decide on the June meeting while emphasizing that “everything is on the table” for the next FOMC.

XAU/USD Price Analysis: Technical outlook

XAU/USD is neutral to downward biased, though it remains trading within the boundaries of important support and resistance levels. As support, the 100-day Exponential Moving Average (EMA) at $1933.85 keeps cushioning God’s fall while the psychological price level of $1950 keeps price action restricted in a $17 range. If XAU/USD sellers claim the former, that could open the door to test the $1900 figure before threatening the 200-day EMA at $1883.27. On the other hand, if XAU/USD buyers conquer the $1950 figure, the yellow metal could be on its way to challenge the $1973.32 area, where the 50-day EMA rests.

In an interview with CNBC on Friday, Federal Reserve Bank of Cleveland President Loretta Mester said that the Personal Consumption Expenditures (PCE) Price Index released on Friday underscored the slow progress on inflation.

Breaking: US Core PCE inflation increases to 4.7% vs. 4.6% anticipated.

“It’s probably not wise to sort of pre-guess what the meeting outcome will be,” Mester said when asked whether another rate increase is warranted at the upcoming FOMC meeting.

Key takeaways

"Tighter monetary policy is still feeding into the economy."

"I may have to revise up my inflation forecast."

"Everything is on the table for the June FOMC meeting."

"Fed is very committed to lowering inflation in timely way."

"Fed still has more data to see ahead of the June FOMC meeting."

"Have not sees much sign of banking stress affecting credit conditions."

"Economy has slowed quite a bit relative to last year."

"Important for the Fed not to under tighten monetary policy."

"Right now is the hard part for monetary policy decisions."

Market reaction

The US Dollar Index stays in positive territory above 104.30 following these comments.

Gold price is under pressure amid dwindling rate cut expectations. Nonetheless, economists at Commerzbank see only limited further downside potential.

Development of physical demand in Asia is hardly likely to influence prices

“Hopes of any rate cuts in the US in the near future have been dampened this week, thereby weighing on the Gold price. A new US labour market report will be published at the end of next week. If it shows a further cooling, as many observers anticipate, this would likely reduce rate expectations, especially if a compromise were to be reached in the US debt dispute, allowing economic indicators to determine the interest rate trajectory again.”

“By contrast, the development of physical demand in Asia, as evidenced by Swiss Gold exports and Chinese Gold imports from Hong Kong, is hardly likely to influence prices, especially as exports and imports will probably turn out to be somewhat weaker given the high price level.”

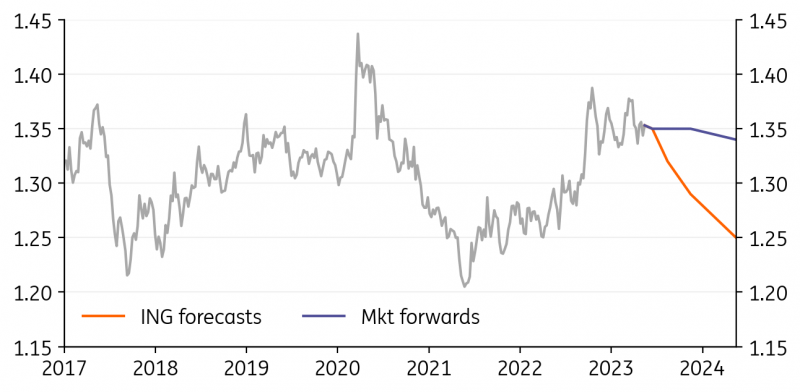

Economists at ING expect the USD/CAD to move below the 1.30 level by the end of the year.

Short-term headwinds for CAD remain non-negligible

“Short-term headwinds for CAD remain non-negligible, starting from the US banking troubles (Canada is quite exposed), Oil’s uncertain performance and risk instability.”

“In line with our call for USD accelerating its decline in the second half of the year and oil prices to be supported, we think USD/CAD can move sustainably below 1.30 by the end of 2023.”

Source: Refinitiv, Macrobond, ING

Economists at Commerzbank discuss EUR/USD outlook.

Upside potential for EUR/USD in the coming months

“In the coming months, EUR/USD is likely to strengthen because the ECB's monetary policy is likely to be more hawkish in the near future and therefore more attractive from a currency market perspective than that of the Fed. Initially, this apparent advantage will come from the fact that the ECB is likely to continue raising interest rates while the Fed is not, and later from the fact that the ECB is sticking to its maximum interest rate level while the Fed is likely to start cutting rates.”

“In the medium term, however, the ECB is probably not really more hawkish than the Fed. On the contrary, the EUR strength we expect in the short term is therefore unlikely to be sustainable. We suspect that the turnaround in the EUR/USD exchange rate could come around the turn of the year.”

Source: Commerzbank Research

- Silver stages a solid rebound from over a two-month low touched this Friday.

- The setup warrants some caution before positioning for any further recovery.

- A sustained move beyond the $24.00 mark could negate the bearish outlook.

Silver gains strong positive traction on Friday and snaps a four-day losing streak to the $22.70-$22.65 area, or over a two-month low touched earlier today. The white metal maintains its bid tone through the early North American session and currently trades around the $23.20-$23.25 zone, up over 2% for the day.

A slightly oversold Relative Strength Index (RSI) on the daily chart turns out to be a key factor that prompts aggressive short-covering around the XAG/USD. That said, this week's convincing break through the 100-day Simple Moving Average (SMA) support and the overnight slide below the 50% Fibonacci retracement level of the March-May rally favour bearish traders. This, in turn, suggests that any subsequent move up might still be seen as a selling opportunity and runs the risk of fizzling out rather quickly.

The 100-day SMA support breakpoint, currently pegged around the $23.35 region, is likely to act as an immediate hurdle. This is followed by 38.2% Fibo. level, near the $23.75 zone, above which the XAG/USD could climb to the $24.00 mark. The latter should act as a pivotal point, which if cleared decisively might trigger a fresh wave of a short-covering move and lift the commodity further beyond the $24.20-$24.25 hurdle. The recovery momentum could get extended towards the $24.50-$24.60 strong support breakpoint.

On the flip side, the monthly low, around the $22.70-$22.65 region, now seems to protect the immediate downside ahead of the 61.8% Fibo. level, near the $22.25 area. Some follow-through selling, leading to a subsequent slide below the $22.00 mark should pave the way for an extension of the recent downfall from over a one-year top touched earlier this month. The XAG/USD might then accelerate the fall towards the $21.55-$21.50 intermediate support before eventually dropping to the $21.00 round-figure mark.

Silver daily chart

Key levels to watch

- GBP/USD bounces off lows near 1.2300 the figure on Friday.

- The greenback regains composure following US data releases.

- UK Retail Sales surprised to the upside in April.

The British pound regains poise and motivates GBP/USD to reclaim ground lost and advance to the vicinity of the 1.2400 mark at the end of the week.

GBP/USD appears supported near 1.2300

Following an earlier uptick to the boundaries of 1.2400 the figure, GBP/USD now comes under some selling pressure on the back of the rebound in the greenback, which was particularly exacerbated higher US inflation figures tracked by the PCE.

Indeed, further resilience from key US fundamentals motivates the resurgence of the buying interest in the greenback, prompting at the same time the USD Index (DXY) to trim initial losses.

In the meantime, better-than-expected UK Retail Sales for the month of April lent initial legs to the quid and accompanied the move higher in Cable, all in line with rising speculation of further tightening by the BoE at the June 22 event.

GBP/USD levels to consider

As of writing, the pair is gaining 0.19% at 1.2345 and the surpass of 1.2668 (2023 high May 8) would open the door to 1.2864 (200-week SMA) and then 1.3000 (psychological level). On the downside, the next support emerges at 1.2308 (monthly low May 25) seconded by 1.2274 (monthly low April 3) and finally 1.2010 (weekly low March 15).

In the recent period there has been a completely counterintuitive mechanism: the Dollar is a safe haven currency and appreciates, even when difficulties arise in the United States, analysts at Natixis report.

In the spring of 2023, all ingredients are normally in place for the USD to weaken

“In the spring of 2023, all the ingredients are normally in place for the Dollar to weaken: Very weak growth prospects in the United States; Risk of default on US public debt due to the debt ceiling; Banking crisis affecting more and more regional banks; Consumer confidence indices down in April.”

“However, the Dollar is not depreciating but, on the contrary, appreciating against all currencies: the USD is a safe haven even when the United States is in trouble, which is paradoxical.”

GBP/USD has found firm support in the low 1.23 zone over the past 24 hours. Economists at Scotiabank analyze the pair’s technical outlook.

Intraday performance looks solid

“Steady gains so far today suggest a mild improvement in its technical tone at least.”

“Short-term trend momentum is positive but that is overshadowed by bearish-leaning signals on the longer run studies. Still, the intraday performance looks solid and regaining the mid-1.23 area (formerly support) gives the technical tone a further (short-term, at least) lift.”

“Resistance is 1.2395/00 and (stronger) at 1.2425. Gains through the latter point would be more generally constructive.”

- USD/JPY attracts some dip-buying on Friday and climbs to a fresh YTD top in the last hour.

- The USD pares modest intraday losses after stronger US PCE data and acts as a tailwind.

- The Fed-BoJ policy divergence favours bulls and supports prospects for additional gains.

The USD/JPY pair reverses an intraday dip to the 139.50 area and climbs to a fresh YTD peak in reaction to the stronger US PCE Price Index. The pair is currently placed just above the 140.00 psychological mark and seems poised to prolong its recent upward trajectory witnessed over the past two weeks or so.

The US Dollar (USD) reverses a part of its modest intraday profit-taking slide after the US Bureau of Economic Analysis (BEA) reported that the headline PCE Price Index rose 0.4% in April as compared to 0.1% in the previous month. Adding to this, the yearly rate accelerated to 4.4% against expectations for a fall to 3.9% from 4.2% in March. Additional details revealed that the Core PCE Price Index - the Fed's preferred inflation gauge - edged higher to 4.7% from 4.6%, beating consensus estimates.

The data reaffirmed market expectations that the Federal Reserve (Fed) will keep interest rates higher for longer, which, in turn, lends some support to the Greenback and acts as a tailwind for the USD/JPY pair. In fact, the markets are now pricing in over a 50% chance of another 25 bps lift-off at the June FOMC meeting. This is reinforced by a fresh leg up in the US Treasury bond yields, widening the US-Japan rate differential and contributing to driving flows away from the Japanese Yen (JPY).

Apart from this, a more dovish stance adopted by the Bank of Japan (BoJ) might continue to undermine the JPY and suggests that the path of least resistance for the USD/JPY pair is to the upside. Even from a technical perspective, the emergence of some dip-buying on Friday and acceptance above the 140.00 mark add credence to the constructive setup. Hence, some follow-through strength towards the next relevant hurdle, around the 140.45-140.50 region, looks like a distinct possibility.

Technical levels to watch

- Durable Goods Orders in the US rose unexpectedly in April.

- US Dollar Index stays in daily range at around 104.00.

Durable Goods Orders in the US increased by 1.1%, or $3.1 billion, in April to $283 billion, the US Census Bureau announced on Friday. This reading followed the 3.3% increase recorded in March and came in better than the market expectation for a decrease of 1%.

"Excluding transportation, new orders decreased 0.2%," the publication further read. "Excluding defense, new orders decreased 0.6%. Transportation equipment, also up two consecutive months, drove the increase, $3.5 billion or 3.7% to $97.6 billion."

Market reaction

This report failed to trigger a noticeable reaction in the US Dollar Index, which was last seen losing 0.15% on the day at 104.05.

EUR/USD gains modestly as support in the low 1.07 area holds. Economists at Scotiabank analyze the pair’s technical outlook.

Not out of the woods just yet

“Gains are marginal and are not – yet– indicative of a firm technical base in place.”

“Price could be consolidating ahead of another push lower. Still, if the 1.0726 point can hold on a weekly close basis, the EUR may have the technical chops to push a little higher still next week.”

“Gains through 1.0755/65 would be technically positive. A clear push under the low 1.07s would, on the other hand, pave the way for a drop to 1.05.”

Economist at UOB Group Lee Sue Ann comments on the upcoming monetary policy meeting by the BoE.

Key Takeaways

“Headline CPI inflation eased to 8.7% y/y in Apr, from 10.1% y/y in Mar. The reading was above estimates of 8.2% y/y. Core CPI inflation, however, surprised on the upside, climbing 6.8% y/y from 6.2% y/y in Mar.”

“While the unemployment rate unexpectedly rose to 3.9% in the three months to Mar, as more people sought to get back into the jobs market; pay growth, which is at the heart of the Bank of England (BOE)’s debate about whether to raise rates further, remained strong by historical standards.”

“Taking into account the BOE’s guidance and the latest slew of economic data releases, we now look for a 25bps rate hike at the next BOE monetary policy meeting on 22 Jun.”

- AUD/USD trims a part of its intraday recovery gains from a fresh YTD low touched on Friday.

- The USD bounces off the daily low in reaction to the stronger US PCE data and caps the pair.

- The fundamental backdrop favours bearish traders and supports prospects for further losses.

The AUD/USD pair stages a goodish rebound from sub-0.6500 levels, or the lowest level since November 2022 and maintains its bid tone through the early North American session on Friday. Spot prices, however, remain below mid-0.6500s and retreat a few pips from the daily peak following the release of the US macro data.

The US Dollar (USD) trims a part of its intraday losses in reaction to the stronger Personal Consumption Expenditure (PCE) Price Index data and acts as a headwind for the AUD/USD pair. The US Bureau of Economic Analysis (BEA) reported that the headline PCE Price Index rose 0.4% in April as compared to 0.1% in the previous month and the yearly rate accelerated to 4.4% against expectations for a fall to 3.9% from 4.2% in March. Furthermore, the Core PCE Price Index - the Fed's preferred inflation gauge - also came in higher than consensus estimates and reaffirms speculations that the Federal Reserve (Fed) will keep interest rates higher for longer, which, in turn, lends some support to the Greenback.

Hawkish Fed expectations, meanwhile, trigger a fresh leg up in the US Treasury bond yields, which, along with the caution mood, further benefits the safe-haven buck and contributes to capping the risk-sensitive Aussie. This, to a larger extent, helps offset the disappointing release of US Durable Goods Orders data, which fell by 0.6% in April vs. a modest 0.1% rise estimated and the 3.2% (revised down from 3.5%) strong growth recorded in the previous month. With the USD bulls looking to seize back control, speculations that the Reserve Bank of Australia (RBA) might refrain from hiking interest rates in June suggest that the path of least resistance for the AUD/USD pair is to the downside.

Bearish traders, however, might prefer to wait for a sustained break and acceptance below the 0.6500 psychological mark before placing fresh bets. Nevertheless, spot prices remain on track to register heavy weekly losses and record the lowest weekly close since October 2022.

Technical levels to watch

- EUR/USD attempts a bounce to the 1.0750 region on Friday.

- The resumption of the selling bias could challenge 1.0700 once again.

EUR/USD remains under pressure despite the ongoing bounce off recent multi-week lows in the proximity of the 1.0700 neighbourhood.

The loss of the so far decent contention area around 1.0700 could force the pair to extend the bearish move to the March low of 1.0516 (March 15), just ahead of the 2023 low of 1.0481 (January 6).

Looking at the longer run, the constructive view remains unchanged while above the 200-day SMA, today at 1.0481.

EUR/USD daily chart

- Oil price recovers after the steep sell-off on Thursday due to mixed messaging from OPEC+ members.

- Russia’s Novak says production cuts are unlikely whilst Saudi Oil Minister seems to imply the opposite.

- US Dollar corrects after strong rally, giving Oil a backdraught.

Oil price steadies on Friday after the previous day’s tumble, as traders weigh conflicting messages from two of the largest members of OPEC+ and the US Dollar weakens. Russia’s Deputy Prime Minister Alexander Novak said that he did not think further cuts would be announced, when only a few days earlier, the Saudi Oil Minister, Prince Abdulaziz bin Salman, seemed to suggest the opposite. The next OPEC+ meeting is on June 4.

At the time of writing, WTI Oil is trading in the upper $72s and Brent Crude Oil in the upper $76s.

Oil news and market movers

- Russia’s Novak plays down the idea of production cuts, saying, “I don't think that there will be any new steps, because just a month ago certain decisions were made regarding the voluntary reduction of oil production by some countries..."

- This seems to contradict comments from Saudi Oil Minister, Prince Abdulaziz bin Salman, who said on Tuesday speculators (interpreted as short-sellers by the media) should “watch out”, seeming to imply OPEC+ may announce cuts.

- Abdulaziz defended OPEC’s decision to cut production by 2 million barrels per day (bpd) at its meeting in October 2022. Given the Oil price is at similar levels to October, it further suggests a possible supply cut in June.

- The US Dollar weakens on Friday as traders take profit after the recent rally and cautiously await Core Personal Consumption Expenditure (PCE) data – the US Federal Reserve’s preferred inflation gauge – and Durable Goods data out at 14:30 GMT.

- A lack of traction in US debt-ceiling talks weighs on the Oil price as it raises the specter of the US defaulting, triggering a global recession.

- That said, past experience points to a high likelihood of the two parties agreeing a last minute deal which will act as a bullish catalyst for Oil.

Crude Oil Technical Analysis: Triangle formation hinting end of downtrend?

WTI Oil is in a long-term downtrend from a technical perspective, making successive lower lows. Given the old adage that the trend is your friend, this favors short positions over long positions. WTI Oil is trading below all the major daily Simple Moving Averages (SMA) and all the weekly SMAs except the 200-week, which is at $66.90.

-638207004306282806.png)

WTI US Oil: Daily Chart

A right-angled triangle has probably finished forming since price recovered from the May 4 YTD lows, as shown by the dotted lines on the chart above.

There is a chance the triangle might break out in either direction, but it is biased to break higher because the top border is very flat (it is right-angled). A breakout higher could see price rise in a volatile rally to a potential target in the $79.70s, calculated by using the usual technical method, which is to take 61.8% of the height of the triangle and extrapolate it from the breakout point higher. Oil price could even go as far as a 100% extrapolation in bullish cases, however, the 61.8% level roughly coincides with the 200-day SMA and the main trendline for the bear market, heightening its importance as a key resistance level.

Assuming Oil price reaches its target, a bullish break would also signify that price had surpassed the $76.85 lower high of April 28, thereby, bringing the dominant bear trend into doubt.

The three green bars in a row that represent the rally this week and the tentative breakout above the topside of the triangle, that accompanied Wednesday’s rally, are a bullish sign. It suggests there is still a chance price could recover after Thursday’s sell-off and eventually continue breaking out higher.

As well as the triangle, the long hammer Japanese candlestick pattern that formed at the May 4 (and year-to-date) lows is a sign that it could be a key strategic bottom.

Further, the mild bullish convergence between price and the Relative Strength Index (RSI) at the March and May 2023 lows – with price making a lower low in May that is not matched by a lower low in RSI – is a sign that bearish pressure is easing.

That said, until Oil price actually climbs above the $76.85 mark, the downtrend is dominant, and there is still a possibility WTI Oil price could break out lower. A decisive piercing below the triangle’s lower border would be required for confirmation, targeting $67.27, which is just above where the 200-week SMA is located and likely to offer good support. Traders might even wish to wait for a break below the lows of the triangle’s Wave B at $69.40 for added confirmation.

-638207004822323375.png)

WTI US Oil: Weekly Chart

A break below the year-to-date (YTD) lows of $64.31 would be required to re-ignite the downtrend, with the next target at around $62.00 where trough lows from 2021 will come into play, followed by support at $57.50.

WTI Oil FAQs

What is WTI Oil?

WTI Oil is a type of Crude Oil sold on international markets. The WTI stands for West Texas Intermediate, one of three major types including Brent and Dubai Crude. WTI is also referred to as “light” and “sweet” because of its relatively low gravity and sulfur content respectively. It is considered a high quality Oil that is easily refined. It is sourced in the United States and distributed via the Cushing hub, which is considered “The Pipeline Crossroads of the World”. It is a benchmark for the Oil market and WTI price is frequently quoted in the media.

What factors drive the price of WTI Oil?

Like all assets, supply and demand are the key drivers of WTI Oil price. As such, global growth can be a driver of increased demand and vice versa for weak global growth. Political instability, wars, and sanctions can disrupt supply and impact prices. The decisions of OPEC, a group of major Oil-producing countries, is another key driver of price. The value of the US Dollar influences the price of WTI Crude Oil, since Oil is predominantly traded in US Dollars, thus a weaker US Dollar can make Oil more affordable and vice versa.

How does inventory data impact the price of WTI Oil

The weekly Oil inventory reports published by the American Petroleum Institute (API) and the Energy Information Agency (EIA) impact the price of WTI Oil. Changes in inventories reflect fluctuating supply and demand. If the data shows a drop in inventories it can indicate increased demand, pushing up Oil price. Higher inventories can reflect increased supply, pushing down prices. API’s report is published every Tuesday and EIA’s the day after. Their results are usually similar, falling within 1% of each other 75% of the time. The EIA data is considered more reliable, since it is a government agency.

How does OPEC influence the price of WTI Oil?

OPEC (Organization of the Petroleum Exporting Countries) is a group of 13 Oil-producing nations who collectively decide production quotas for member countries at twice-yearly meetings. Their decisions often impact WTI Oil prices. When OPEC decides to lower quotas, it can tighten supply, pushing up Oil prices. When OPEC increases production, it has the opposite effect. OPEC+ refers to an expanded group that includes ten extra non-OPEC members, the most notable of which is Russia.

Economists at Société Générale expect the EUR/USD pair to race higher driven by relative natural rates.

Do ‘natural’ interest rate trends suggest a stronger Euro ahead?

“The New York Fed has now updated its estimates of natural rates and its work suggests that the European natural (real) rate has risen from a low of 38 bps in mid-2020 to 83 bps now, while the US rate has fallen from 0.9% to 0.7%. This isn’t going to do anything to help the Euro in the short run, but it raises the possibility that when (if) the Fed and ECB can get rates back to a neutral setting, we should see ECB rates move higher than Fed rates, which hasn’t happened since 2011.”

“EUR/USD almost broke above 1.50 in that cycle and while that seems inconceivable, we’re more optimistic than we have been for a while, that we’ll see EUR/USD above 1.30 again, once the war in Ukraine and Europe’s energy troubles are behind us.”

Economists at Commerzbank discuss BCB’s policy outlook and its implications for the USD/BRL pair after yesterday’s inflation figures.

Interest rate cuts in Brazil getting closer

“Yesterday's weaker-than-expected inflation data for mid-May boosted expectations of a rate cut in Brazil and weakened the real. We also see room for a rate cut.”

“Critically, the government continues to call for interest rate cuts. In order to maintain credibility in the market and ensure the stability of the BRL, the Brazilian central bank must make it clear that rate cuts, if they come, are fundamentally justified and not the result of pressure from the government.”

“We expect the BCB to initiate the rate cut cycle cautiously in order to avoid speculation about government influence. Accordingly, the Real depreciated yesterday, but is still trading at high levels against the US Dollar. We see confirmation of our view that the lows for USD/BRL are in the 4.90-5.00 range.”

Senior Economist at UOB Group Alvin Liew assesses the latest GDP figures for the January-March period in Singapore.

Key Takeaways

“Singapore’s final 1Q23 GDP growth coming in at 0.4% y/y (-0.4% q/q SAAR) revised up from the prelim estimate of 0.1% y/y (-0.7% q/q SA), compared to the 2.1% y/y (+0.1% q/q) growth in 4Q22. Despite the revision, 1Q’s y/y growth was still the weakest since 1Q 2021. It was, however, higher than our and Bloomberg median estimate of 0.2% y/y, -0.6% q/q.”

“Growth was dragged by manufacturing sector (-4.8% q/q, -5.6% y/y) in 1Q with all major sectors within manufacturing recording declines in output except transport engineering. Services supported growth with aviation- and tourism related sectors outperforming but trade-related services weighed on growth. Construction activity supported growth although its 1Q pace was revised lower.”

“The MTI in their outlook, was more downbeat about the US and Europe but more positive on China (seeing its recovery to be stronger than expected while noting the downside risks). MTI also warned of a more prolonged and deeper electronics downturn and highlighted two increasing downside risks to the global economy: 1) tightening of global financial conditions and 2) escalations in the Russia-Ukraine war and geopolitical tensions among major global powers. The MTI maintained its previous forecast for the Singapore economy to grow by 0.5-2.5% in 2023, adding that growth will likely be in the mid-point of the range (i.e. 1.5%). In comparison, we still expect full year GDP growth at 0.7% in 2023 (lower end of the official growth forecast range) reflecting our more cautious external outlook. There is a substantial risk Singapore may enter a technical recession in 1H 2023, largely driven by the weakness in manufacturing.”

“Singapore’s headline inflation rose to 5.7% y/y in Apr from 5.5% y/y in Mar. The core inflation remained elevated at 5.0% y/y (unchanged from Mar). The MAS kept its inflation forecasts (that were first made in the 14 Oct 2022 MPS) unchanged in the Apr CPI report and said core inflation rate will remain ‘elevated in the next few months’ but ‘will remain on a broad moderating path’ and ‘to slow more discernibly in the second half of the year’. However, the MAS omitted the previous mention that ‘MAS Core Inflation is projected to reach around 2.5% y-o-y by the end of 2023’.”

“MAS Outlook – Keeping Our View Of Status Quo For Oct 2023: While inflation concerns remained in the latest Apr inflation print, it was also evident that the growth outlook has been also subject to greater uncertainty and biased to the weaker side. That said, it is also too soon to expect monetary policy to reverse part of its restrictive stance given the stickiness of core inflation. On the balance of sticky Apr inflation and a weaker growth outlook, we keep the view that the tightening cycle to have ended in Apr and the MAS to maintain this pause in the next Oct meeting. If there is another off-cycle announcement before Oct, we think it will likely be due to a sudden worsening in external conditions leading to a sharp downgrade in growth outlook, so the MAS will likely shift to a more accommodative policy rather than further tightening in its next move, but that is not our base case to expect an off-cycle policy announcement for now.”

- DXY meets some resistance around the 104.30 region so far.

- Extra upside should face the key 200-day SMA near 105.70.

DXY retreats for the first session after four consecutive daily gains, putting the 104.00 region to the test at the end of the week.

Further upside appears on the cards in the near term. That said, the next resistance level of note is expected at the key 200-day SMA, today at 105.69 ahead of the 2023 top of 105.88 (March 8).

Looking at the broader picture, while below the 200-day SMA the outlook for the index is expected to remain negative.

DXY daily chart

UK rate pricing is heading into recession-inducing Subsequently, Sterling is set to suffer, Kit Juckes, Chief Global FX Strategist at Société Générale, reports.

Sterling’s last hurrah?

“Jeremy Hunt, the UKL’s Chancellor told Sky News that ‘It’s not a trade-off between tackling inflation and recession, in the end the only path to sustainable growth is to bring down inflation’ as he expressed support for tighter monetary policy even if the economy suffers.”

“If the K does raise rates by another 1%, as is priced by markets, and all that talk of long and variable lags between monetary policy implementation and when it takes effect on the economy are ignored, yet again, recession seems certain. How high will Sterling climb from here before it starts falling? Given how much is priced into the curve, this is surely the last leg of the GBP rally.”

- EUR/JPY extends the upside past the 150.00 hurdle.

- Extra gains could see the 2023 peak near 151.60 revisited.

EUR/JPY climbs for the third session in a row and briefly surpasses the key 150.00 barrier on Friday.

While the likeliness of further consolidation appears a plausible near-term scenario, a convincing breakout of the key round level at 150.00 could encourage the cross to dispute the 2023 top at 151.61 (May 2) in the not-so-distant future.

So far, further upside looks favoured while the cross trades above the 200-day SMA, today at 143.62.

EUR/JPY daily chart

- USD/CAD pulls back from a nearly one-month high and is pressured by a combination of factors.

- A pickup in Oil prices undermines the Loonie and weighs on the pair amid a modest USD slide.

- Hawkish Fed expectations should help limit the downside ahead of the US Core PCE Price Index.

The USD/CAD pair retreats from a nearly one-month high, around the 1.3655 region touched earlier this Friday and remains on the defensive through the mid-European session. The pair languishes near the lower of the daily trading range and is pressured by a combination of factors, though manages to hold its neck above the 1.3600 round-figure mark.

Crude Oil prices gain some positive traction and recover a part of the previous day's slump, which, in turn, is seen underpinning the commodity-linked Loonie. The US Dollar (USD), on the other hand, pulls back from over a two-month high set on Thursday amid a modest downtick in the US Treasury bond yields and further contributes to a mildly offered tone surrounding the USD/CAD pair. That said, the uncertainty over OPEC’s plans for future production cuts, along with worries that a global economic slowdown will dent fuel demand, keep a lid on any meaningful upside for Oil prices.

Apart from this, expectations that the Federal Reserve (Fed) will keep interest rates higher for longer favour the USD bulls and should help limit the downside for the USD/CAD pair, at least for the time being. In fact, the markets started pricing in the possibility of another 25 bps lift-off at the June FOMC meeting following the recent hawkish comments by a slew of US central bank officials. Furthermore, Thursday's better-than-expected US macro data pointed to a resilient US economy and should allow the Fed to stick to its hawkish stance to combat stubbornly high inflationary pressures.

Hence, the market focus will remain glued to the release of the US Core PCE Price Index - the Fed's preferred inflation gauge - due later during the early North American session. Friday's US economic docket also features Durable Goods Orders, which, along with the US bond yields and the US debt ceiling crisis, will drive the USD demand. Apart from this, Oil price dynamics might provide some impetus to the USD/CAD pair. Nevertheless, spot prices remain on track to register strong weekly gains, though bulls might wait for a move beyond the 1.3665-1.3670 area before placing fresh bets.

Technical levels to watch

Since the beginning of May, the SEK has depreciated significantly again. The weakness of the Krona may become too much for the Riksbank and may act, economists at Commerzbank report.

Rate hikes should be the Riksbank's first choice against currency weakness

“Rate hikes should be the Riksbank's first choice against currency weakness, as intervening in the currency market (in this case in favor of its own currency) would be a ‘leaning against the wind’ strategy with questionable chances of success. Therefore, it will be particularly interesting to see whether the Riksbank's last rate hike really comes at the end of June or not.”

“As long as the US debt crisis continues to unsettle the markets, even strong words from the Riksbank will have little effect and the SEK will remain under pressure for the time being.”

See – EUR/SEK: Krona’s near-term outlook remains grim – ING

Economists at Société Générale analyze USD/JPY technical outlook.

Defending 138/137.20 an lead to continuation in up move

“USD/JPY broke out above the upper end of its range since December and has achieved the earlier highlighted target of 140.30 representing projections. An initial pullback is not ruled out however the 200-DMA near 138/137.20 should be an important support zone. Defending this can lead to continuation in up move.”

“Beyond 140.30, next potential hurdles are located at the upper limit of a multi-month channel near 141.60 and 142.50/142.80.”

- GBP/USD stages a goodish recovery from its lowest level since April amid modest USD weakness.

- The British Pound draws additional support from the better-then-expected UK Retail Sales figures.

- The divergent BoE-Fed expectations could cap the upside ahead of the key US Core PCE Price Index.

The GBP/USD pair gains some positive traction on Friday and snaps a three-day losing streak to the 1.2300 neighbourhood, or its lowest level since early April touched the previous day. Spot prices stick to intraday gains through the first half of the European session and currently trade around the 1.2360 region, up over 0.30% for the day.

A modest pullback in the US Treasury bond yields prompts traders to lighten their US Dollar (USD) bullish bets, especially after the recent move up to over a two-month high, which, in turn, lends support to the GBP/USD pair. The British Pound (GBP), meanwhile, gets an additional lift following the better-than-expected release of the UK Retail Sales figures, which rose 0.5% in April as compared to the 0.3% expected and the 1.2% decline registered in the previous month.

The upside for the GBP/USD pair, however, seems limited amid expectations that fewer rate increases by the Bank of England (BoE) will be needed in the coming months to bring down inflation. The bets were reaffirmed by the fact that the UK CPI decelerated sharply from the 10.1% YoY rate in March to 8.7% in April. Furthermore, speculations that the Federal Reserve (Fed) will keep interest rates higher for longer favour the USD bulls and might cap the major.

In fact, the markets started pricing in the possibility of another 25 bps lift-off at the June FOMC policy meeting in the wake of the recent hawkish comments by several Fed officials. Adding to this, the upbeat US macro data released on Thursday could allow the Fed to stick to its hawkish stance. This should act as a tailwind for the US bond yields, which supports prospects for the emergence of some USD dip-buying and contribute to keeping a lid on the GBP/USD pair.

Traders might also refrain from placing aggressive bets and prefer to wait on the sidelines ahead of the release of the US Core PCE Price Index - the Fed's preferred inflation gauge - later during the early North American session. Friday's US economic docket also features the release of Durable Goods Orders, which, along with the US bond yields and the US debt ceiling talks, will influence the USD and provide some meaningful impetus to the GBP/USD pair.

Technical levels to watch

- US Dollar stabilizes after big rally, awaits next market-moving event..

- US debt-ceiling talks continue into Friday, Biden mentions possible spending freeze and denies default..

- US Dollar Index holds just above 104 and awaits US macroeconomic data for a sense of direction.

The US Dollar (USD) is in wait-and-see mode early on Friday as traders await more economic data out of the US to assess which way to take. The US debt ceiling keeps making headlines, with more details being released about a possible deal, although an agreement this week looks almost close to impossible. US President Joe Biden gave more details about the talks and reiterated that there will be no default on his watch.

On the macroeconomic data front, a big slew of important data is about to hit the markets. At 12:30 GMT, the Fed’s preferred inflation metric is being published – the Personal Consumption Expenditure (PCE) inflation numbers, both core and overall for monthly and yearly performances. These numbers have the potential to shift market expectations for the next Federal Reserve interest rate decision in June, thus being an important market-mover for US Dollar traders.

Personal Spending and Income figures, together with Durable Goods Orders and Inventories data, will be hitting the wires at that same time. To close off the batch of macroeconomic data for the US, the University of Michigan is set to issue its May Final reading for Consumer Sentiment and Inflation Expectations. These numbers could help round-up moves on US Dollar, Treasury yields and other assets.

Daily digest: US Dollar to be data-driven this Friday

- US President Joe Biden commented after the last debt-ceiling meeting that a proposal is on the table for a spending freeze for two years, and reiterated again there will be no default. Meanwhile GOP debt negotiators gave ground on defence spending demands.

- Negotiator Garret Graves said that finding a debt-limit deal this Friday will be hard.

- US Credit Default Swaps (CDS) eases a touch to 163.875 after peaking at 165.83 on Thursday. The peak was last week on Monday at 177.62 when concerns for a default were at the highest.

- Fitch places Fannie Mae and Freddie Mac ratings on watch.

- US Treasury Cash balance dropped to $49.5 billion on Wednesday.

- US equity futures are mixed to unchanged at the start of this Friday, while the Chinese Hang Seng Index closed nearly 2% lower.

- The CME Group FedWatch Tool shows that markets are pricing in a 82% chance of rate hike for July and even June is now at a 41% chance for a hike. The data coming out this Friday could lock in that rate hike for July and see a more than 50% chance for the June rate hike.

- The benchmark 10-year US Treasury bond yield trades at 3.79% and are holding at that level after briefly hitting 3.82%, awaiting further guidance from the data later this Friday.

US Dollar Index technical analysis: USD bulls pause their attack

The US Dollar Index (DXY) has taken out both the 55-day and the 100-day Simple Moving Averages (SMA), respectively, at 102.43 and 102.85 on the upside. The US Dollar safe-haven status keeps seeing bids for the DXY, with 104 having been broken early on Thursday and now eases a touch as a debt-ceiling deal takes some shape.

On the upside, 105.73 (200-day SMA) still acts as long-term price target to hit, as the next upside key level for the US Dollar Index is at 104.00 (psychological, static level), and acts as an intermediary element to cross the open space.

On the downside, 102.85 (100-day SMA) aligns as the first support level to confirm a change of trend. In the case that breaks down, watch how the DXY reacts at the 55-day SMA at 102.48 in order to assess any further downturn or upturn.

US Dollar FAQs

What is the US Dollar?

The US Dollar (USD) is the official currency of the United States of America, and the 'de facto' currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022.

Following the second world war, the USD took over from the British Pound as the world's reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

How do the decisions of the Federal Reserve impact the US Dollar?

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed's 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

What is Quantitative Easing and how does it influence the US Dollar?

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed's weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

What is Quantitative Tightening and how does it influence the US Dollar?

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

The Australian Dollar was one of the biggest losers this week. Economists at Commerzbank discuss AUD/USD outlook for the next week.

Aussie under pressure

“Next week's data will likely determine whether AUD/USD will remain below the 0.66 level for the time being, or whether it will be able to return to its range. This is because in addition to the monthly inflation data, the housing market and private sector credit growth data are likely to influence the RBA's overall picture.”

“The Chinese PMIs will also play an important role. After all, China's economic momentum has a significant impact on the outlook for the Australian economy via expected commodity demand and may have contributed to the recent AUD weakness.”

Economist at UOB Group Ho Woei Chen, CFA, reviews the latest BoK monetary policy meeting.

Key Takeaways

“In line with consensus and our expectation, Bank of Korea (BOK) extended its interest rate pause… keeping the benchmark 7-day repo rate at 3.50% for the third consecutive meeting. However, BOK’s tone turned out to be more hawkish than expected.”

“The central bank also updated its economic forecasts today as it sees higher core inflation and slower growth in 2023.”

“For now, we think BOK’s hands are tied but it should start to tone down its relatively more hawkish rhetoric as US’ Fed rate peaks and provide early signals for interest rate cuts that are likely to materialize nearly next year as inflationary pressure eases sufficiently. We maintain our call for the BOK to start cutting interest rate in 1Q24.”

Today, it is all about the release of the US Core PCE deflator. Unless we see a soft figure, the Dollar is set to stay bid, economists at ING report.

USD Index to rally toward the 105.88 high on a weekly close above the 104.00/20 area

“Today is all about the April US Core PCE deflator. Expectations are for another firm 0.3% month-on-month / 4.6% year-on-year figure which will feed into the narrative that core inflation is not falling as quickly as the Fed would like. Unless this surprises on the downside, expect the Dollar to stay bid.”

“A DXY close above the 104.00/104.20 area opens up a run at the 105.88 high next week.”

See – US Core PCE Preview: Forecasts from four major banks, inflation to stay elevated in April

The continuation of the upside momentum in USD/CNH could challenge the 7.1200 level in the next weeks, comment UOB Group’s Economist Lee Sue Ann and Markets Strategist Quek Ser Leang.

Key Quotes

24-hour view: “We highlighted yesterday that USD could break above 7.0960 but it might not be able to hold above this level. USD rose to a high of 7.0945 in NY trade before rising briefly above 7.0960 in early Asian trade. Conditions are deeply overbought and USD is unlikely to advance much further. Today, we expect USD to trade in a range, likely between 7.0700 and 7.1000.”

Next 1-3 weeks: “We turned positive USD two weeks ago. As USD rose, in our latest narrative two days ago (24 May, spot at 7.0780), we highlighted that USD ‘is likely to break above 7.0960’. We added, ‘a breach of this level will shift the focus to 7.1200’. While USD rose above 7.0960 in early Asian trade today, conditions are deeply overbought and 7.1200 may not come into view so soon. Overall, only a break of the ‘strong support’ level at 7.0500 (level previously at 7.0280) would indicate the USD is not advancing further.”

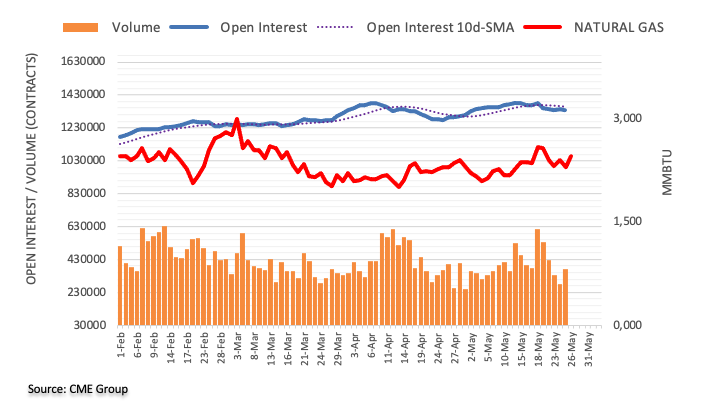

Considering advanced prints from CME Group for natural gas futures markets, open interest resumed the downtrend and shrank by nearly 6K contracts on Thursday. On the other hand, volume rose by around 93.1K contracts after four daily drops in a row.

Natural Gas: No changes to the consolidative theme

Prices of natural gas remained choppy on Thursday and traded on the back foot amidst diminishing open interest and rising volume. That said, while a rebound seems likely in the very near term, the broader consolidation scenario remains unchanged for the time being.

European Central Bank (ECB) Chief Economist, Philip Lane, said on Friday, “food inflation will reverse later this year.”

Additional quotes

“Energy price fall will feed into core prices but timeframe is uncertain.”

“There are some upside risks to wage growth.”

“Real wage growth correction has to be a gradual process.”

“Uncertainty in models high.“

“No sense of certainty in terminal rate.”

Market reaction

At the time of writing, EUR/USD is trading modestly flat at 1.0730, awaiting the US PCE inflation data for fresh trading impetus.

- AUD/USD bounces off a multi-day low touched on Friday amid a modest USD pullback.

- Economic woes and US debt ceiling concerns cap the upside for the risk-sensitive Aussie.

- Investors now look to the US Core PCE Price Index before placing fresh directional bets.

The AUD/USD pair stages a modest recovery from sub-0.6500 levels, or its lowest since November 2022 touched this Friday and sticks to its intraday gains through the first half of the European session. The pair is currently placed around the 0.6525-0.6530 region, up over 0.20% for the day, and for now, seems to have snapped a three-day losing streak.

The US Dollar (USD) bulls opt to take some profits off the table following the recent rally to over a two-month high and turn out to be a key factor lending some support to the AUD/USD pair. The downside for the USD, meanwhile, seems cushioned amid growing acceptance that the Federal Reserve (Fed) will keep interest rates higher for longer to combat sticky inflation. Apart from this, the prevalent cautious mood could benefit the Greenback's relative safe-haven status and contribute to capping the upside for the risk-sensitive Aussie.

Against the backdrop of the recent hawkish remarks by several Fed officials, Thursday's better-than-expected US macro data reaffirms market expectations that the US central bank will continue to tighten its monetary policy. In fact, the markets have started pricing in the possibility of another 25 bps lift-off at the June FOMC meeting. This, in turn, pushed the yield on the rate-sensitive two-year US government bond to a two-and-half-month high on Thursday and supports prospects for the emergence of some dip-buying around the USD.

The market sentiment, meanwhile, remains fragile amid worries about a global economic slowdown and the US debt ceiling impasse. It is worth mentioning that both Democrats and Republican negotiators flagged little progress towards reaching a deal to raise the borrowing limit ahead of the early-June deadline when the federal government could run out of money. Moreover, Fitch placed its top-level "AAA" rating of the US on negative watch, while credit rating agency DBRS Morningstar put the US on review for a downgrade on Thursday.

Apart from this, speculations that the Reserve Bank of Australia (RBA) might refrain from hiking in June, bolstered by softer domestic data, suggests that the path of least resistance for the AUD/USD pair is to the downside. Hence, any subsequent move up might still be seen as a selling opportunity and runs the risk of fizzling out rather quickly. Traders now look to the US economic docket, highlighting the release of the Core PCE Price Index - the Fed's preferred inflation gauge - and Durable Goods Orders, later during the early North American session.

Technical levels to watch

Inflation rises in Japan. Economists at Commerzbank discuss BoJ's policy outlook and its implications for the Yen.

Prices in Japan are rising

“Prices in Japan are rising. As a result, some analysts expect another increase in the 10-year Japanese government bond yield target as early as this summer, effectively pushing up long-term interest rates in Japan. However, USD/JPY levels around 140 suggest that this is (still) a minority view.”

“As long as the BoJ continues to signal a wait-and-see approach to gain more certainty about the sustainability of inflation dynamics, high inflation will erode the Yen's purchasing power. As a result, we see limited upside potential for the Yen in the near term.”

ECB policymaker, Boris Vujčić, said on Friday, “inflation momentum is still persistent.”

“It is questionable if we will be able to get to 2% in the next two years.”

Market reaction

At the time of writing, EUR/USD is treading water at around 1.0730, modestly flat on the day.

USD/BRL is back above 5.00. Economists at Société Générale analyze the pair’s technical outlook.

Downtrend could resume on a break under 4.93

“USD/BRL broke below the consolidation since last August however the downward momentum has not regained. The pair has formed an interim support near April low of 4.89 resulting in an initial bounce towards the 50-DMA. Recent pivot high at 5.10 is a short-term resistance. This must be overcome to affirm an extended rebound.”

“In case the pair fails to defend low formed this week at 4.93, the downtrend could resume.”

Economists at ING discuss EUR/USD outlook.

1.05/1.07 to prove the base for a push towards 1.15 in the third quarter

“There were reports in the market yesterday of some upside interest in EUR/USD going through the FX options market. We can see why. 1.0700 is a decent support area for EUR/USD and we do see the outside risk of a break to 1.0500. However, the eurozone terms of trade story is so much better than it was last summer and that is why our medium-term models identify EUR/USD as very under-valued.”

“Our view is that 1.05/1.07 proves the base for a push towards 1.15 in the third quarter, once clearer signs of US disinflation and slowing activity become a lot clearer.”

“Expect EUR/USD to stay soft near 1.0700/0720 and perhaps take a decisive turn on the release of the US inflation data.”

See – US Core PCE Preview: Forecasts from four major banks, inflation to stay elevated in April

- USD/JPY retreats from the YTD peak amid a modest USD pullback from over a two-month high.

- A softer risk tone benefits the safe-haven JPY and further contributes to the intraday downfall.

- The Fed-BoJ policy divergence should help limit losses ahead of the US Core PCE Price Index.

The USD/JPY pair comes under some selling pressure on the last day of the week and extends its steady intraday slide through the first half of the European session. Spot prices drop to mid-139.00s in the last hour, reversing the previous day's positive move to the highest level since November 2022.

The US Dollar (USD) pulls back from over a two-month high touched on Thursday and turns out to be a key factor dragging the USD/JPY pair lower. The Japanese Yen (JPY), on the other hand, attracts some heaven flows amid growing worries of a global economic slowdown and US debt ceiling woes. This further contributes to the offered tone surrounding the major, though any meaningful corrective decline still seems elusive.

A more dovish stance adopted by the Bank of Japan (BoJ), along with the softer domestic data, could act as a headwind for the JPY and lend some support to the USD/JPY pair. In fact, BoJ Governor Kazuo Ueda had reiterated recently that the central bank will continue easing with yield curve control. Furthermore, the Tokyo CPI released this Friday showed that inflation in Japan’s capital city eased more than expected in May.

The Federal Reserve (Fed), on the other hand, is expected to keep interest rates higher for longer to combat stick inflation. In fact, the markets have started pricing in the possibility of another 25 bps lift-off at the June FOMC policy meeting and the bets were lifted by the recent comments by a slew of Fed officials. Adding to this, Thursday's upbeat US macro data could allow the US central bank to stick to its hawkish stance.

This has been pushing the US Treasury bond yields higher recently, widening the US-Japan rate differential and supporting prospects for the emergence of some dip-buying around the USD/JPY pair. The USD bulls, however, seem reluctant to place aggressive bets and await the release of the Core PCE Price Index - the Fed's preferred inflation gauge - later during the early North American session for a fresh impetus.

Technical levels to watch

- EUR/USD attempts a mild bounce from recent lows near 1.0700.

- There seems to be dome renewed optimism around the US debt ceiling.

- Markets’ attention will be on the US PCE/Core PCE in April.

The single currency manages to regain some composure and encourages EUR/USD to put some distance from Thursday’s multi-week lows near the 1.0700 region.

EUR/USD looks at US docket, debt ceiling

EUR/USD trades with humble gains in the wake of the opening bell in Euroland at the end of the week against the backdrop of some selling pressure in the dollar and fresh optimism around the US debt ceiling.