- Phân tích

- Tin tức và các công cụ

- Tin tức thị trường

- 3 Reasons Why This European Banking Crisis Won't Hurt The Euro - Credit Suisse

3 Reasons Why This European Banking Crisis Won't Hurt The Euro - Credit Suisse

"The G10 market has pirouetted away from its extreme JPY focus last week to consider the potential FX impact of European banking frailties. With a notable German lender under the microscope due to concerns about capital adequacy in light of potential fines and related problems, European equities and credit have come under a degree of pressure. This has spilled over to some extent to the FX market via a widening of the EUR basis towards the widest levels this year, though still far from the lofty levels seen in genuine crises such as 2008 or 2012

Historically, banking crises and widening basis would have quickly led to a weaker EUR and much higher realised and implied volatility. But so far, the latest stresses have had almost no discernable impact on these vol metrics despite starting points that were already very low.

We see three key reasons for this mild response as follows:

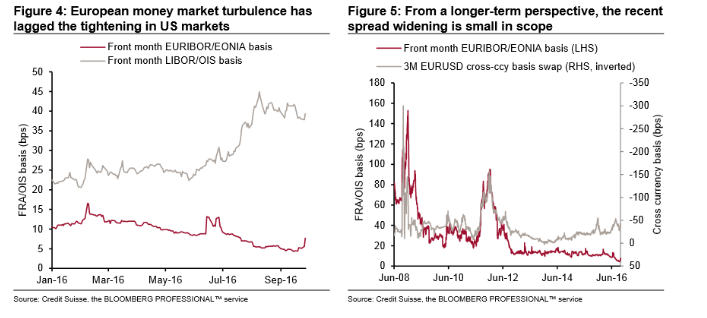

1. ECB liquidity and systemic stability: unlike 2012, many more ECB mechanisms with a range of acronyms are in play to support the wider system and provide easy access to liquidity. These range from OMT to TLTRO to QE among others, but also factors such as negative rates and excess deposits from other sources help too. This can be seen in Figure 4 and Figure 5. European money markets are not showing material signs of idiosyncratic stress. Dec IMM Euribor minus Eonia spreads have moved a touch higher but are easily lagging the move that money market reforms in the US prompted earlier in similar US LIBOR minus OIS spreads. And from a longer-term perspective, the spread widening in both Euribor minus OIS and the EUR basis is trivial. Also, the USD funding requirement of European banks is much lower than before 2012 due to lower operational requirements for USD-funded balance sheets

2. German policy: markets suspect the German government would not allow a major lender to fail, even if significant losses are imposed on shareholders and some creditors. This limits the capacity to generate systemic risk.

3. EUR is now a funding currency: unlike the period up to 2012, the euro area now systematically runs a large current account surplus, which both adds to excess liquidity and means that euro area investors provide rather than need capital flow funding on a net basis. This limits exposure to risk-off situations - indeed those that could trigger repatriation flows could even be helpful.

In this context, we take a relatively benign view of these events and maintain our EURUSD 1.15 three month target".

Copyright © 2016 Credit Suisse, eFXnews™

© 2000-2026. Bản quyền Teletrade.

Trang web này được quản lý bởi Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

Thông tin trên trang web không phải là cơ sở để đưa ra quyết định đầu tư và chỉ được cung cấp cho mục đích làm quen.

Giao dịch trên thị trường tài chính (đặc biệt là giao dịch sử dụng các công cụ biên) mở ra những cơ hội lớn và tạo điều kiện cho các nhà đầu tư sẵn sàng mạo hiểm để thu lợi nhuận, tuy nhiên nó mang trong mình nguy cơ rủi ro khá cao. Chính vì vậy trước khi tiến hành giao dịch cần phải xem xét mọi mặt vấn đề chấp nhận tiến hành giao dịch cụ thể xét theo quan điểm của nguồn lực tài chính sẵn có và mức độ am hiểu thị trường tài chính.

Sử dụng thông tin: sử dụng toàn bộ hay riêng biệt các dữ liệu trên trang web của công ty TeleTrade như một nguồn cung cấp thông tin nhất định. Việc sử dụng tư liệu từ trang web cần kèm theo liên kết đến trang teletrade.vn. Việc tự động thu thập số liệu cũng như thông tin từ trang web TeleTrade đều không được phép.

Xin vui lòng liên hệ với pr@teletrade.global nếu có câu hỏi.

ngân hàng