- Phân tích

- Tin tức và các công cụ

- Tin tức thị trường

- EUR/USD bulls tread around with caution in a field of land mines and disruptive Russian headlines

EUR/USD bulls tread around with caution in a field of land mines and disruptive Russian headlines

- EUR/USD stabilising despite Russian invasion angst and weakness in Asian equities.

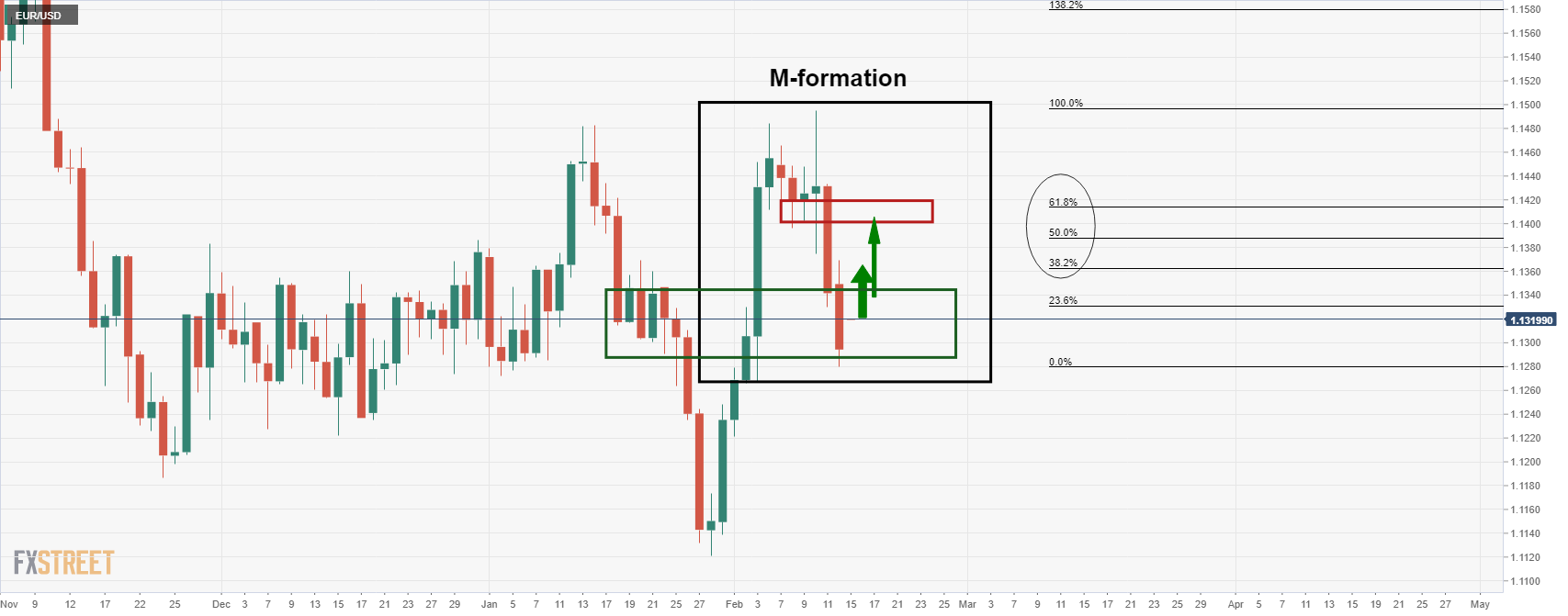

- Daily M-formation neckline has a confluence with the 50% and 61.8% ratios.

- Bears in anticipation of a disruptive Russian headline to put 1.11's in focus.

EUR/USD is trading higher by some 0.12% in Asia with the euro catching a bid as it attempts to correct vs the greenback in what appears to be 'wait and see' market conditions unfolding. The bulls moved on the lows of Monday's trade and stay in control through Asia, despite Russian invasion jitters and a wobble in Asian equities.

Asian share benchmarks have fallen on Tuesday as investors contemplated the implications of a potential imminent Russian invasion of Ukraine. There were plenty of headlines swirling over financial markets at the start of the week that caused a tense atmosphere in both European and US sessions.

Asia is feeling some of that today. The MSCI's broadest index of Asia-Pacific shares outside Japan was down 0.4% in early regional trade, tracking lost ground on Monday in the West. Overnight, the Dow Jones Industrial Average lost 0.49%, the S&P 500 (SPX) fell 0.38%. Japan's Nikkei was down 0.5% at the time of writing and while in Australia, the S&P/ASX200 was off 0.14%. Hong Kong's Hang Seng Index (HSI) slid 0.67% early in the session, although China's CSI300 Index (399300) bucked the trend and was up 0.41%.

The ebbs and flows of Russian tensions in markets

Washington had said Russia could invade Ukraine "any day now," and British Prime Minister Boris Johnson on Monday called the situation "very, very dangerous." The US Secretary of State Antony Blinken said the US embassy would be relocated from Kyiv to Lviv, citing the "dramatic acceleration of the buildup of Russian forces," and this was accompanied by what was perceived as a confirmation from the Ukraine president that there would be an invasion on the 16th Feb.

Ukraine President Volodymyr Zelenskiy urged Ukrainians to fly the country's flags from buildings and sing the national anthem in unison on Feb. 16, a date some Western media have cited as the possible start of a Russian invasion. However, a Ukrainian official said that Zelenskiy was not predicting an attack on that date, but instead responding with scepticism to foreign media reports.

This caused some two-way knee-jerk reaction in markets overnight but the dust settled as the more dominant theme is one of diplomacy considering Russia's president, Vladimir Putin, had signalled that there would be continued efforts to find a diplomatic solution to the standoff. Additionally, in a 40-minute call, Joe Biden and Boris Johnson agreed a deal was still possible despite a chorus of warnings of imminent Russian military action.

Trapped between a rock, (war) and a hard place, (inflation)

Meanwhile, besides the threat of world war 3, one eye is still being pointed at central bank divergences and the futures markets are portraying the likelihood of the Federal Reserve raising interest rates at its March meeting. St. Louis Federal Reserve President James Bullard was calling, again, for faster US Federal Reserve interest rate hikes.

Fed fund futures sold off again and continued to price in a high risk of a 50bp move in March. ''Meanwhile,'' analysts at ANZ bank said, ''the European Central Bank faces a challenging communication hurdle having recently pivoted in its assessment of inflation.''

The analysts warn that id If sanctions were to be imposed on Russia, ''that would hurt European exports as Russia is the EU’s fifth-largest trading partner. Any exacerbation of energy supply tightness would also hurt EU growth while raising inflationary pressures in the short run.''

In response to the threat of rising inflation in the eurozone as a consequence, the ECB President, Christine Lagarde, has reiterated that the central bank will act when appropriate and with due regard to the volatility in prices. She also stressed the ECB’s gradual approach.

Meanwhile, for the calendar, there will be a slew of important data and we will have another look at the ZEW survey of expectations that has recently rebounded firmly above average. Analysts at Westpac say that this is ''indicating that omicron disruptions are expected to only temporarily slow growth prospects.''

The other key release will come in the form of the second estimate for Q4 Gross Domestic Product that the analysts at Westpac say ''will confirm the slowing of year-end activity for the region (market f/c: 0.3%).''

EUR/USD technical analysis

As for the daily chart, the euro has room to correct, so long as the media keeps a lid on the Russian invasion angst and does not misinterpret statements from global officials such as what happened in New York's trade on Monday.

With price stabilising in a familiar support area, the M-formation is compelling especially as the neckline has a confluence with the 50% and 61.8% ratios. With that being said, markets can turn on a dime at the drop of a disruptive Russian headline, and the 1.11 area is by no means a distant possibility.

© 2000-2026. Bản quyền Teletrade.

Trang web này được quản lý bởi Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

Thông tin trên trang web không phải là cơ sở để đưa ra quyết định đầu tư và chỉ được cung cấp cho mục đích làm quen.

Giao dịch trên thị trường tài chính (đặc biệt là giao dịch sử dụng các công cụ biên) mở ra những cơ hội lớn và tạo điều kiện cho các nhà đầu tư sẵn sàng mạo hiểm để thu lợi nhuận, tuy nhiên nó mang trong mình nguy cơ rủi ro khá cao. Chính vì vậy trước khi tiến hành giao dịch cần phải xem xét mọi mặt vấn đề chấp nhận tiến hành giao dịch cụ thể xét theo quan điểm của nguồn lực tài chính sẵn có và mức độ am hiểu thị trường tài chính.

Sử dụng thông tin: sử dụng toàn bộ hay riêng biệt các dữ liệu trên trang web của công ty TeleTrade như một nguồn cung cấp thông tin nhất định. Việc sử dụng tư liệu từ trang web cần kèm theo liên kết đến trang teletrade.vn. Việc tự động thu thập số liệu cũng như thông tin từ trang web TeleTrade đều không được phép.

Xin vui lòng liên hệ với pr@teletrade.global nếu có câu hỏi.

ngân hàng