- Phân tích

- Tin tức và các công cụ

- Tin tức thị trường

- USD Index appears side-lined around 106.60, focus is on Fed, NFP

USD Index appears side-lined around 106.60, focus is on Fed, NFP

- The index trades without direction around 106.60.

- Cautiousness should prevail ahead of the FOMC event.

- Nonfarm Payrolls will be the salient release later in the week.

The USD Index (DXY), which tracks the greenback vs. a bundle of its main competitors, extends the consolidative mood around the 106.60 at the beginning of the week.

USD Index remains capped by 107.00

The index trades in a vacillating mood on Monday on the back of increasing prudence among investors in light of key upcoming events in the US economy, namely: the Federal Reserve’s interest rate decision (Wednesday) and the publication of October’s Nonfarm Payrolls (Friday).

In the meantime, US yields navigate in an equally directionless pattern in the upper end of the recent range, particularly in the belly and the short end of the curve vs. some loss of momentum in the short end.

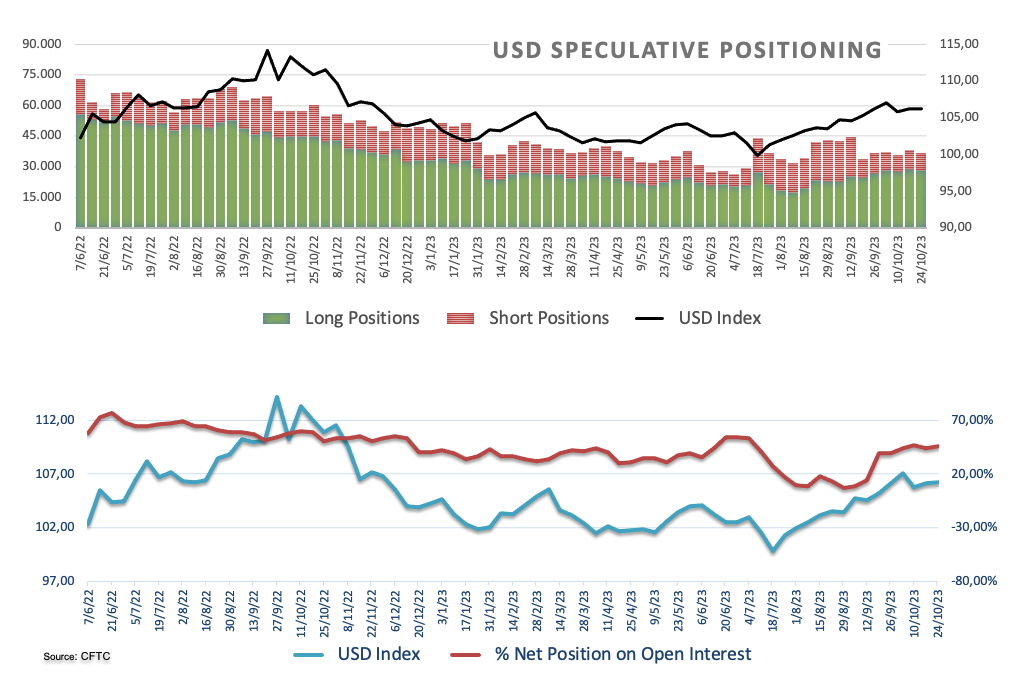

On another front, speculators increased their USD net longs positions to the highest level since mid-December 2022 during the week ended on October 24, as per the CFTC report. During this period, the greenback remained side-lined amidst speculation that the Fed might extend its restrictive stance for longer than anticipated, a view that appeared propped up by auspicious results from US fundamentals.

There will be no scheduled data releases on Monday in the US calendar.

What to look for around USD

The upside momentum in the index seems to have met some initial obstacle just below the 107.00 barrier so far this week.

In the meantime, support for the dollar keeps coming from the good health of the US economy and still elevated inflation, which morphs into higher yields and underpins the renewed tighter-for-longer narrative from the Federal Reserve.

Key events in the US this week: Employment Cost, FHFA House Price Index, CB Consumer Confidence (Tuesday) – MBA Mortgage Applications, ADP Report, Final Manufacturing PMI, ISM Manufacturing, Construction Spending, FOMC Interest Rate Decision, Powell press conference (Wednesday) - Initial Jobless Claims, Factory Orders (Thursday) – Nonfarm Payrolls, Unemployment Rate, Services PMI, ISM Services PMI (Friday).

Eminent issues on the back boiler: Persistent debate over a soft or hard landing for the US economy. Speculation of rate cuts in late 2024. Geopolitical effervescence vs. Russia and China. Potential spread of the Middle East crisis to other regions.

USD Index relevant levels

Now, the index is up 0.06% at 106.64 and the breakout of 106.88 (weekly high October 26) could expose 107.34 (2023 high October 3) and finally 107.99 (weekly high November 21 2022). On the downside, initial contention aligns at 105.36 (monthly low October 24) ahead of 104.42 (weekly low September 11) and then 103.41 (200-day SMA).

© 2000-2026. Bản quyền Teletrade.

Trang web này được quản lý bởi Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

Thông tin trên trang web không phải là cơ sở để đưa ra quyết định đầu tư và chỉ được cung cấp cho mục đích làm quen.

Giao dịch trên thị trường tài chính (đặc biệt là giao dịch sử dụng các công cụ biên) mở ra những cơ hội lớn và tạo điều kiện cho các nhà đầu tư sẵn sàng mạo hiểm để thu lợi nhuận, tuy nhiên nó mang trong mình nguy cơ rủi ro khá cao. Chính vì vậy trước khi tiến hành giao dịch cần phải xem xét mọi mặt vấn đề chấp nhận tiến hành giao dịch cụ thể xét theo quan điểm của nguồn lực tài chính sẵn có và mức độ am hiểu thị trường tài chính.

Sử dụng thông tin: sử dụng toàn bộ hay riêng biệt các dữ liệu trên trang web của công ty TeleTrade như một nguồn cung cấp thông tin nhất định. Việc sử dụng tư liệu từ trang web cần kèm theo liên kết đến trang teletrade.vn. Việc tự động thu thập số liệu cũng như thông tin từ trang web TeleTrade đều không được phép.

Xin vui lòng liên hệ với pr@teletrade.global nếu có câu hỏi.

ngân hàng