- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 13-03-2023

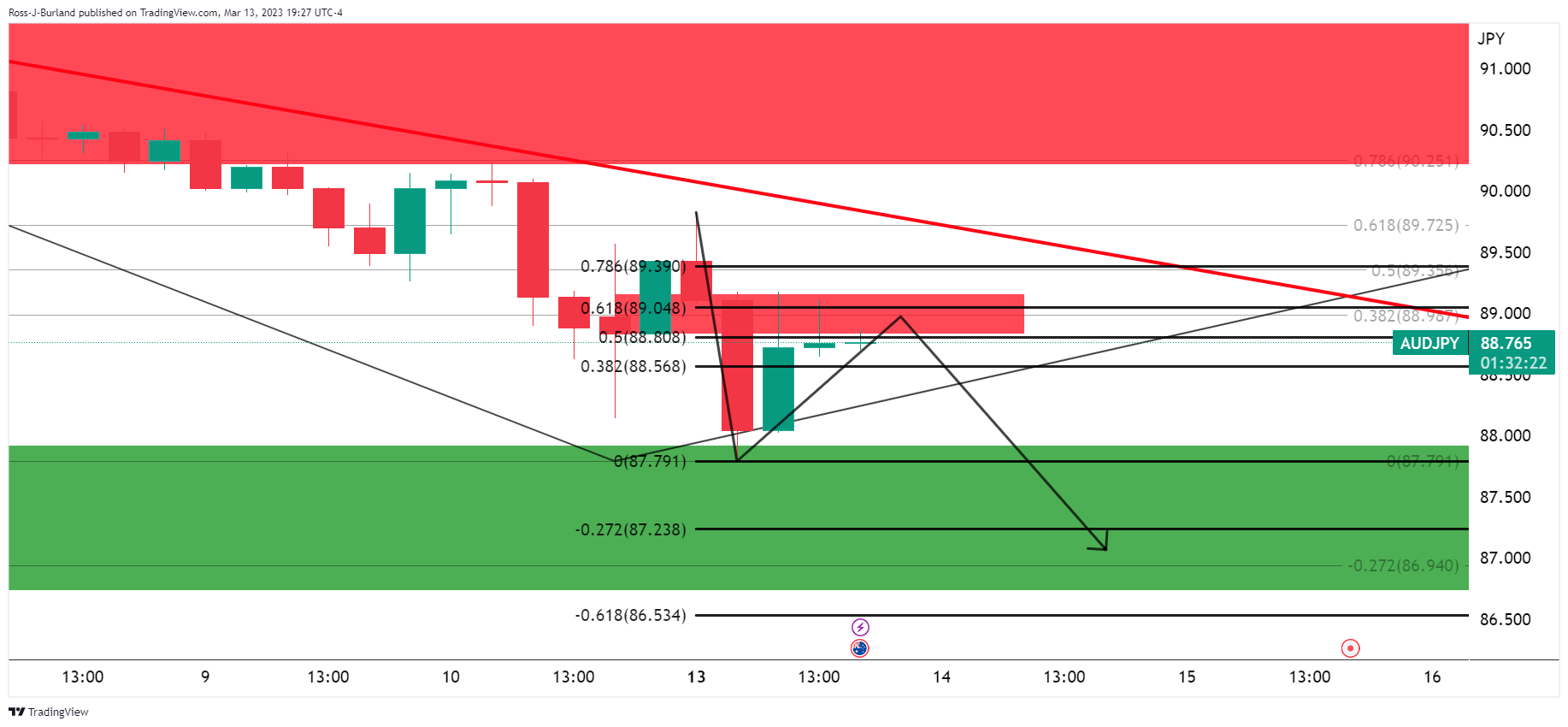

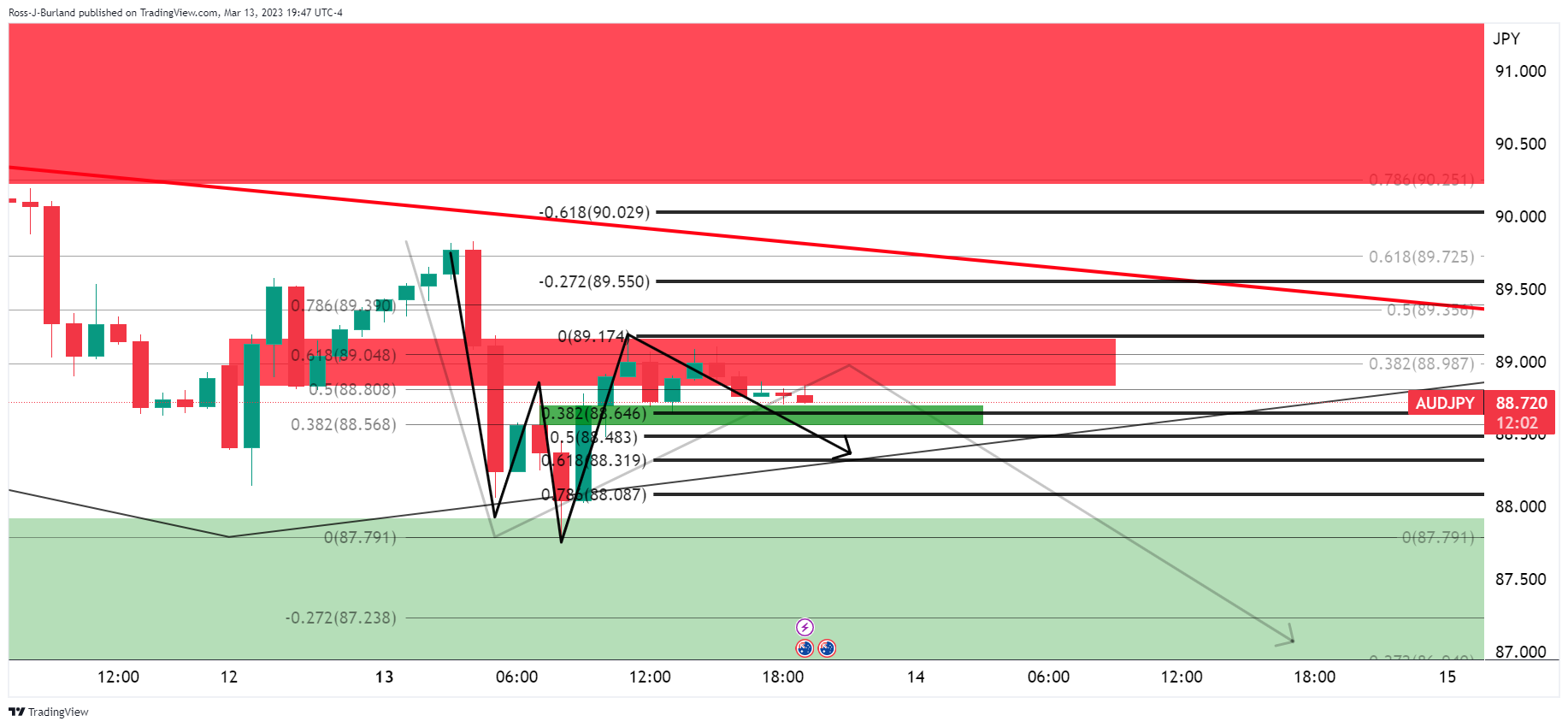

- AUD/JPY bulls are defending support on the daily chart but bears are stepping up again.

- A deeper correlation of the bullish recovery is eyed for the immediate future.

AUD/JPY is flat on the day so far approaching the Tokyo open, trading at 88.67 and sticking to a 20 pip range so far. The bulls are stepping in from daily support with prospects of a bullish correction towards prior support that would now be regarded as resistance. Pulling up the Fibonacci scale, there is an alignment with the 78.6% Fibonacci resistance near to 90.25:

AUD/JPY daily chart

AUD/JPY H4 chart

However, moving down to the 4-hour time frame, we can see plenty of resistance near 89.00 and the fact that the price is stalling here, in a confluence with the 61.8% ratio, a downside case can be built, until a break of the resistance structure. We are still on the front side of the bear trend so a bullish thesis is not as easy to make.

AUD/JPY H1 chart

The W-formation on the hourly chart sees the price drawn to the neckline and testing the 38.2% Fibonacci of the prior bullish impulse currently. A break here opens the risk of a deeper correction further into the Fibonacci scale where the 787.6% Fibo meets 88.00 the figure or thereabouts as the likely last line of defense before a bullish thesis can be made for the forthcoming sessions.

- GBP/JPY is eyeing a fresh upside above 163.00 as the focus shifts to UK labor market data.

- A decline in the UK Employment cost index and a higher Unemployment Rate would trim inflation expectations.

- BoJ Ueda is expected to scrap Yield Curve Control (YCC) and ultra-loos monetary policy gradually.

The GBP/JPY pair is gauging an intermediate cushion above 162.00 in the early Asian session after sensing restrictions in the upside momentum above 163.00. The cross is expected to resume its upside journey as investors are worried about the United Kingdom’s labor cost index, which has kept the Bank of England (BoE) busy with high inflation affairs for the past one year.

The release of the UK’s Employment data will be the key trigger for the Pound Sterling ahead. As per the consensus, the Claimant Count Change (Feb) will drop by 12.4K, lower than the former release of 12.9K. Three-month Unemployment Rate is expected to increase to 3.8% from the prior release of 3.7%.

The major catalyst will be the Average Earnings data, which is expected to decline to 5.7% vs. the prior release of 5.9%. Investors should be aware of the fact that higher employment costs and stubborn food price inflation in the UK economy have been driving inflationary pressures. And, now a decline in the labor cost index will delight BoE Governor Andrew Bailey, who is going through sleepless nights in designing a roadmap for decelerating the double-digit figure inflation.

It is worth noting that the impact of the Silicon Valley Bank (SVB) collapse is not restricted to the United States. In a joint statement from the UK Treasury and the Bank of England (BOE), the UK Finance Minister, Jeremy Hunt, said on Monday that the “deposits will be protected, with no taxpayer support.” The UK authorities confirmed that HSBC bank agreed to rescue the Silicon Valley Bank’s (SVB) UK arm. UK Hunt further added, "No other UK banks are directly materially affected by these actions."

On the Tokyo front, after an unchanged monetary policy announcement by ex-Bank of Japan (BoJ) Governor Haruhiko Kuroda, investors are shifting their focus toward the commentary from BoJ Kazuo Ueda over the Yield Curve Control (YCC) and a shift to restrictive monetary policy.

Senior Economist at UOB Group Alvin Liew is of the view that “An exit from the YCC and negative interest rates is inevitable for Japan, the question is how Ueda will execute his plan. We believe Ueda will proceed at a gradual, well-telegraphed pace, and not a sharp and sudden reversal. We see it in two broad steps, 1) Protracted adjustment to its forward guidance on YCC and interest rates (Apr to Dec 2023) and 2) Scrapping of YCC and lifting of the negative policy rate in early 2024.”

- EUR/GBP remains sidelined around the key support line after refreshing two-week low.

- Downbeat oscillators favor bears but 100-DMA acts as an extra filter towards the south.

- Double tops around 0.8925-30 appear important hurdle towards the north.

EUR/GBP portrays the pair trader's cautious mood ahead of the key UK employment data during early Tuesday. In doing so, the cross-currency pair makes rounds to 0.8900 while probing a three-day downtrend near the lowest levels in two weeks, marked the previous day.

Also read: GBP/USD grinds near one-month high below 1.2200 ahead of UK employment, US CPI

It’s worth noting that an upward-sloping support line from mid-December 2022 challenges the EUR/GBP bears as traders brace for the key UK data. However, the bearish MACD signals and the downbeat RSI (14) line, not oversold, keeps the pair sellers hopeful.

Adding strength to the downside bias is the quote’s double top formation around the 0.8930-25 area.

That said, the EUR/GBP bears need a sustained downside break of the aforementioned support line, near 0.8910 at the latest, to aim for the 100-DMA support surrounding 0.8765.

Following that, the lows marked during February and January, respectively near 0.8755 and 0.8740, will be the focus of the sellers.

On the contrary, recovery moves may initially aim for the month-start peak surrounding the 0.8900 threshold ahead of challenging the “double top” bearish formation near 0.8930.

In a case where EUR/GBP bulls surpass the 0.8930 hurdle, the odds of witnessing a fresh 2023 high, currently around 0.8980, can’t be ruled out.

EUR/GBP: Daily chart

Trend: Further downside expected

- AUD/USD looks cautious prior to the US CPI release, as the downside bias is intact.

- Fed is in a tricky situation, what next for a rate hiking plan?

- Market forecasters are abating for a massive rate hike from the Fed.

AUD/USD is treading water in the early Asian session after hitting the 0.6700 mark in the last trading session. US Dollar Index (DXY) is on the softer side in early Asian hours, as the market awaits the United States (US) Consumer Price Index (CPI) data release on Tuesday.

AUD/USD has not capitalized much on the previous trading day in wake of the backstop provided by the Federal Reserve (Fed) and US Treasury. On Silicon Valley Bank’s (SVB) fallout and to cement any dent over the US banking system, the Fed came up with a backstop plan on Sunday, which prompted milder risk on the market environment during New York (NY) session on Monday.

Looking ahead, the market is heading into US CPI data with caution due to the numerous dynamic changes that occurred on Monday after the SVB fallout event. Many key market forecasters are rolling back their 50 basis points (bps) Fed rate hike expectation for 22 March.

Given the fact that higher borrowing cost across the globe is putting pressure on high-leverage business like tech companies, which are struggling to keep on with repayments on their debt amidst higher interest rate, therefore the banking system is facing a big problem with their non-performing assets.

Moreover, a continuously rising interest rate will likely hammer the banking system as per the aforementioned analogy. Hence the market is expecting no overstretching on the rate fronts.

However, elevated inflation levels are putting central banks into a tricky situation and acting like a double whammy for central banks.

The upcoming US CPI will be interesting to watch as it's only going to add more complexity for the Federal Reserve.

Levels to watch.

- USD/CAD keeps recent bounce off one-week low after falling the most in a month.

- WTI refreshed three-month low before making rounds to $75.00.

- Market sentiment dwindles amid SVB, Signature Bank fallout but US Dollar bears the burden of the downbeat Treasury yields.

- Risk catalysts eyed closely ahead of US CPI for February.

USD/CAD licks its wounds around 1.3740, after marking the biggest daily slump in a month the previous day. In doing so, the Loonie pair portrays the market’s positioning for the US Consumer Price Index (CPI) data while struggling to cheer the latest rebound in the Oil price, Canada’s main export item.

The quote ignored the WTI crude oil’s slump towards refreshing a three-month low to $72.42, before a rebound to $74.90 at the latest, amid the broad US Dollar weakness due to the reduction in the hawkish Federal Reserve (Fed) bets.

That said, the US Dollar Index (DXY) began the week’s trading on a back foot by printing a three-day south-run while declining the most in two months on Monday, licking its wounds near 103.68 at the latest. With this, the greenback’s gauge versus the six major currencies traced the US Treasury bond yields as hawkish bets on the Federal Reserve (Fed) reverberate.

US two-year Treasury bond yields marked the biggest daily slump since October 1987 by declining more than 13.0% on a day as US banking regulators rushed to defend the Silicon Valley Bank (SVB) and the Signature Bank. Further, the US 10-year Treasury bond yields slumped to the monthly low amid a sudden shift in the market’s Fed bets due to the financial market risks emanating from the stated banks.

While portraying the latest shift in the US Fed Fund Futures, Reuters said that the US rate futures on Monday have priced in a 69% chance of a 25-bps hike at next week's Fed policy meeting, with a more than 30% probability of a pause. The market last week was poised for a 50-bps increase prior to the SVB collapse.

Looking ahead, the US inflation data for February will be important to watch for clear directions. Forecasts suggest the US CPI is likely to ease to 6.0% YoY versus 6.4% prior while CPI ex Food & Energy may slide to 5.5% YoY from 5.6% prior. It’s worth noting that Canada Manufacturing Sales for January, around 3.9% versus -1.5% prior, will also be important to better predict the USD/CAD pair’s immediate moves. However, major attention should be given to the yields and the market’s risk catalysts for better directions.

Also read: US Inflation Preview: Five scenarios for trading the Core CPI whipsaw within the SVB storm

Technical analysis

A daily closing below a one-month-old ascending support line, around 1.3705 by the press time, becomes necessary for the USD/CAD bears to take control.

- USD/CHF is gauged as an intermediate cushion around 0.9100 ahead of US Inflation.

- The Fed might look for a small rate hike to restore the confidence of US households and firms.

- Only a sheer surprise upside could provide decent support to the USD index ahead.

The USD/CHF pair has sensed an intermediate cushion near the round-level support of 0.9100 in the early Asian session. The Swiss franc asset is gathering strength to extend its recovery above the immediate resistance of 0.9127. However, the upside looks capped as the collapse of Silicon Valley Bank (SVB) has limited the expectations of a bumper pace in the policy-tightening regime by the Federal Reserve (Fed), as expected earlier, to tame the stubborn inflation.

The Fed on Sunday announced it would make additional funding available through a new Bank Term Funding Program, which would offer loans of up to one year to depository institutions, backed by Treasuries and other assets these institutions hold, as reported by Reuters.

In times, when firms and households are losing confidence in the United States banking system, the street considers that a halt or a continuation of the slowdown in the policy-tightening pace by Fed chair Jerome Powell would be prudent to restore confidence.

After the catastrophic collapse of SVB, investors are shifting their focus on the US Consumer Price index (CPI) data, which will provide direction to the FX domain ahead.

Analysts at CIBC are of the view that “A further increase in prices at the pump and continued pressure in core categories suggest that prices rose by an uncomfortably fast 0.4% in February. Looking at core (ex. food and energy) categories, shelter prices are set to peak imminently as the typical lags with new leases that are resetting at lower rates kick in, but continued pressure in core services outside of the shelter, in line with the tight labor market, will keep the Fed on a tightening path.

The US Dollar Index (DXY) has shown some tough fight after dropping to near 103.50 as bulls are reluctant to go downside further ahead of the US inflation release.

S&P500 futures have shown some decent gains after a choppy session that ended with marginal losses. This shows a recovery in the risk appetite theme but a broad-based caution cannot be ruled out. The return offered on 10-year US Treasury yields has dropped sharply to 3.54%.

On the Swiss Franc front, the monthly Producer Price Index (PPI) (Feb) is expected to show a deceleration of 0.1%, which indicates a decline in the households’ demand that has forced producers to trim prices of goods and services offered at factory gates. A decline in the monthly PPI figure will be music to the ears of the Swiss National Bank (SNB) as Swiss inflationary pressures have gone beyond its control.

“Britain's Finance Minister Jeremy Hunt announced on Monday he would create 12 ‘investment zones’ in England to spur the regional economy outside London, a scaled-back version of a policy announced under former Prime Minister Liz Truss,” reported Reuters during the initial hours of Tuesday’s Asian session.

Key quotes

Ahead of Hunt's annual budget on Wednesday, the finance ministry said each of the zones will be backed by 80 million pounds spread over five years that can be directed towards tax relief for businesses, training and infrastructure.

Hunt also announced 100 million pounds ($122 million) of funds to be shared across Glasgow, Manchester and part of central England to improve their research and development centers.

Hunt looks set to keep his grip on public finances in the budget, holding off on any big tax cuts or spending increases until the next election comes closer into view.

GBP/USD grinds

Despite the price-positive news and the broad-based US Dollar weakness, the GBP/USD pair remains sidelined near the highest levels in a month, recently around 1.2770-80, after rising the most since early January the previous day.

Also read: GBP/USD grinds near one-month high below 1.2200 ahead of UK employment, US CPI

- NZD/USD is oscillating around 0.6220, resumption in the upside is expected ahead of US CPI.

- After a responsive buying, NZD/USD has negated the breakdown of the Double Top chart pattern.

- A decent recovery from the RSI (14) into the 40.00-60.00 range indicates that the presence of responsive buyers.

The NZD/USD pair has turned sideways around 0.6220 in the early Tokyo session after a corrective move from 0.6260. A resumption in the upside momentum is expected from the Kiwi asset as the catastrophic collapse of Silicon Valley Bank (SVB) has faded the hopes of a hawkish stance on the interest rates by the Federal Reserve (Fed).

On the interest rate hike outlook, Goldman Sachs believes "In light of recent stress in the banking system, we no longer expect the FOMC to deliver a rate hike at its March 22 meeting with considerable uncertainty about the path beyond March."

A decent rebound is shown by the S&P500 futures, indicating an improvement in the risk appetite of the market participants. However, caution on a broad basis cannot be ruled out.

The US Dollar Index (DXY) has shown a less-confident recovery from 103.50 and is expected to remain volatile ahead of the release of the Consumer Price Index (CPI) ahead.

NZD/USD has negated the breakdown of the Double Top chart pattern formed on a daily scale. A responsive buying in the Kiwi asset has pushed it above the critical resistance plotted from January 06 low at 0.6190.

The asset is attempting to shift its auction above the 20-period Exponential Moving Average (EMA) at 0.6207, which will improve the short-term upside bias.

A decent recovery from the Relative Strength Index (RSI (14) into the 40.00-60.00 range indicates that the presence of responsive buyers at lower levels.

A buying opportunity in the Kiwi asset will emerge it will surpass March 1 high at 0.6276, which will drive the pair toward the round-level resistance at 0.6300 followed by February 14 high at 0.6389.

In an alternate scenario, a breakdown of January 6 low at 0.6193 will drag the asset toward November 28 low at 0.6155. A slippage below the latter will expose the asset for more downside toward the round-level support at 0.6100.

NZD/USD daily chart

- GBP/USD buyers take a breather at one-month high, probing four-day uptrend.

- Broad-based US Dollar weakness propels Cable pair despite geopolitical, Brexit uncertainty in the UK.

- US Treasury bond yields, Fed Fund Futures slumps as US regulators rescue SVB, Signature Bank.

- UK jobs report, US CPI will be crucial but risk catalysts may gain major attention.

GBP/USD prods a four-day winning streak near 1.2180, after poking the highest level in a month to 1.2199 the previous day. In doing so, the Cable pair takes a breather ahead of the key statistics from the UK and the US. Apart from the pre-data anxiety, mixed concerns surrounding UK politics and Brexit also probe the momentum traders of the pair, after witnessing the biggest daily jump in nine weeks.

That said, the quote’s previous losses could be linked to the broad-based US Dollar slump. US Dollar Index (DXY) began the week’s trading on a back foot, printing a three-day south-run while declining the most in two months on Monday. With this, the greenback’s gauge versus the six major currencies traced the US Treasury bond yields as hawkish bets on the Federal Reserve (Fed) reverberate.

It should be noted that the US two-year Treasury bond yields marked the biggest daily slump since October 1987 by declining more than 13.0% on a day as US banking regulators rushed to defend the Silicon Valley Bank (SVB) and the Signature Bank. Further, the US 10-year Treasury bond yields slumped to the monthly low amid a sudden shift in the market’s Fed bets due to the financial market risks emanating from the stated banks.

US banking regulators undertook joint actions to tame the risks emanating from SVB and Signature Bank during the weekend. While announcing the plan, US President Joe Biden noted on Monday that investors in those banks will not be protected and reminded that "no one is above the law." However, the US President also vowed to take whatever action was needed to ensure the safety of the US banking system, per Reuters.

While portraying the latest shift in the US Fed Fund Futures, Reuters said that the US rate futures on Monday have priced in a 69% chance of a 25-bps hike at next week's Fed policy meeting, with a more than 30% probability of a pause. The market last week was poised for a 50-bps increase prior to the SVB collapse.

Elsewhere, the US-China tussles escalate while the UK joins hands with the US and Australia to provide Canberra with nuclear-powered attack submarines, a major step involving an investment of hundreds of billions of dollars aimed at countering China's ambitions in the Indo-Pacific, reported Reuters. Further, Brexit optimism fades amid the broad market anxiety. While portraying the mood, Wall Street closed mixed while Gold managed to remain firmer amid broad US Dollar weakness, as well as due to the metal’s traditional safe-haven status.

It’s worth noting that news conveying Britain's Finance Minister Jeremy Hunt, as he announces a plan to create 12 "investment zones" in England also favors the GBP/USD buyers. “Ahead of Hunt's annual budget on Wednesday, the finance ministry said each of the zones will be backed by 80 million pounds spread over five years that can be directed towards tax relief for businesses, training and infrastructure,” stated Reuters.

Looking ahead, the UK employment report will be crucial to watch for immediate directions as the central bank haws retreat. Following that, the US Consumer Price Index (CPI) for February will be important to watch for clear directions. Forecasts suggest a slight reduction in the UK’s Claimant Count Change and Unemployment Rate jostling with a minor fall in the Average Earnings. On the other hand, the US CPI is likely to ease to 6.0% YoY versus 6.4% prior while CPI ex Food & Energy may slide to 5.5% YoY from 5.6% prior.

To sum up, the mixed expectations from the UK and the US data join the market’s latest attention on the financial risks and a fall in the Treasury bond yields to dim the importance of today’s economic calendar for the GBP/USD pair traders. Even so, the quote is likely to remain firmer amid broad US Dollar weakness.

Also read: US Inflation Preview: Five scenarios for trading the Core CPI whipsaw within the SVB storm

Technical analysis

The first daily closing above the 50-DMA in five weeks, enables the GBP/USD bulls to aim for the mid-February swing high surrounding 1.2270.

- EUR/USD seesaws near one-month high after rising the most in two weeks the previous day.

- US Dollar traces downbeat Treasury bond yields as SVB, Signature Bank fallout weigh on Fed bets.

- Market sentiment dwindles amid fears of looming financial market crisis.

- US inflation could offer immediate directions, firmer prints can put a floor under Euro prices.

EUR/USD grinds near the highest level in a month, after posting the biggest daily gains in a fortnight, as the US inflation data loom. That said, the Euro pair cheered the broad US Dollar strength to rally to 1.0741 the previous day before portraying the market’s cautious mood while making rounds to 1.0720-30 at the latest.

US Dollar Index (DXY) began the week’s trading on a back foot, printing a three-day south-run while declining the most in two months on Monday. In doing so, the greenback’s gauge versus the six major currencies traced the US Treasury bond yields as hawkish bets on the Federal Reserve (Fed) reverberates.

US 10-year Treasury bond yields slumped to the monthly low whereas the two-year counterpart marked above 13.0% daily slump amid a sudden shift in the market’s Fed bets due to the fallout of the Silicon Valley Bank (SVB) and the Signature Bank. “The two-year note's yield, which reflects interest rate move expectations, was on track for the biggest one-day drop since October 1987 in the wake of that fateful Black Monday stock market crash,” said Reuters.

That said, the Fed Fund Futures suggest the 80 basis points (bps) of rate cuts by the end of 2023, versus a 50 bps rate hike in the next meeting expected previously. With this, the interest rate futures seem to ignore the latest jump in the US employment data and rather bear the burden of the position unwinding amid fears of another financial market crackdown.

Elsewhere, Wall Street closed mixed while Gold managed to remain firmer amid broad US Dollar weakness, as well as due to the metal’s traditional safe-haven status.

It should be noted that the US Treasury Department, Federal Reserve and the Federal Deposit Insurance Corporation (FDIC) undertook joint actions to tame the risks emanating from SVB and Signature Bank during the weekend. While announcing the plan, US President Joe Biden noted on Monday that investors in those banks will not be protected and reminded that "no one is above the law."

Moving on, US Consumer Price Index (CPI) for February will be important to watch for clear directions. However, major attention will be on the SVB and Signature Bank updates. “Amid this financial uncertainty, US February CPI data will be out tonight. The consensus is for core CPI to slow just 0.1ppt to 5.5% y/y. That would indicate progress in bringing inflation back to target is proving very slow. Combined with a hot February Nonfarm Payrolls print, and we retain our forecast for a 25bp FFR hike next week (and a peak of 5.5% in June),” said Analysts at the ANZ ahead of the US CPI release.

Also raed: US Inflation Preview: Five scenarios for trading the Core CPI whipsaw within the SVB storm

Technical analysis

The first daily closing beyond the 50-DMA, around 1.0725 by the press time, keeps EUR/USD buyers hopeful of poking the mid-February swing high surrounding 1.0805.

- Gold price has delivered a three-day winning streak on hopes of a slowdown in the Fed’s policy tightening pace.

- Going forward, a sheer volatility is expected ahead of the US inflation data.

- A decisive break above 61.8% Fibo indicates that the asset will recapture the previous swing high ahead.

Gold price (XAU/USD) has refreshed its five-week high at $1,914.70 in the early Asian session. The precious metal has delivered a three-day winning streak and is expected to continue its upside momentum as a sudden collapse of Silicon Valley Bank (SVB) might force the Federal Reserve (Fed) to continue a lower pace of policy tightening if not halt the restrictive regime.

President Joe Biden said the administration's swift actions to ensure depositors can access their funds in Silicon Valley Bank (SVB) and Signature Bank (SBNY) should give Americans confidence that the U.S. banking system was safe, as reported by Reuters.

The US Dollar Index (DXY) has sensed an intermediate cushion around 103.50, however, sheer volatility is expected ahead as investors will keep an eye on the United States Consumer Price Index (CPI) data.

Analysts at Credit Suisse expect “Expect core CPI inflation to remain steady at 0.4% MoM in February, causing the YoY reading to tick down to 5.5%. Energy and food prices are likely to moderate, with headline inflation also coming in at 0.4% MoM. A reading in-line with our expectations would be uncomfortably high for the Fed, but still consistent with gradual disinflation this year.”

S&P500 futures are showing marginal gains after a subdued Monday, a case of a dead cat bounce, however, the risk sentiment is still negative. The 10-year US Treasury yields dropped to 3.54% as Fed chair Jerome Powell won’t go heavy on interest rates to maintain consumer confidence in the economy.

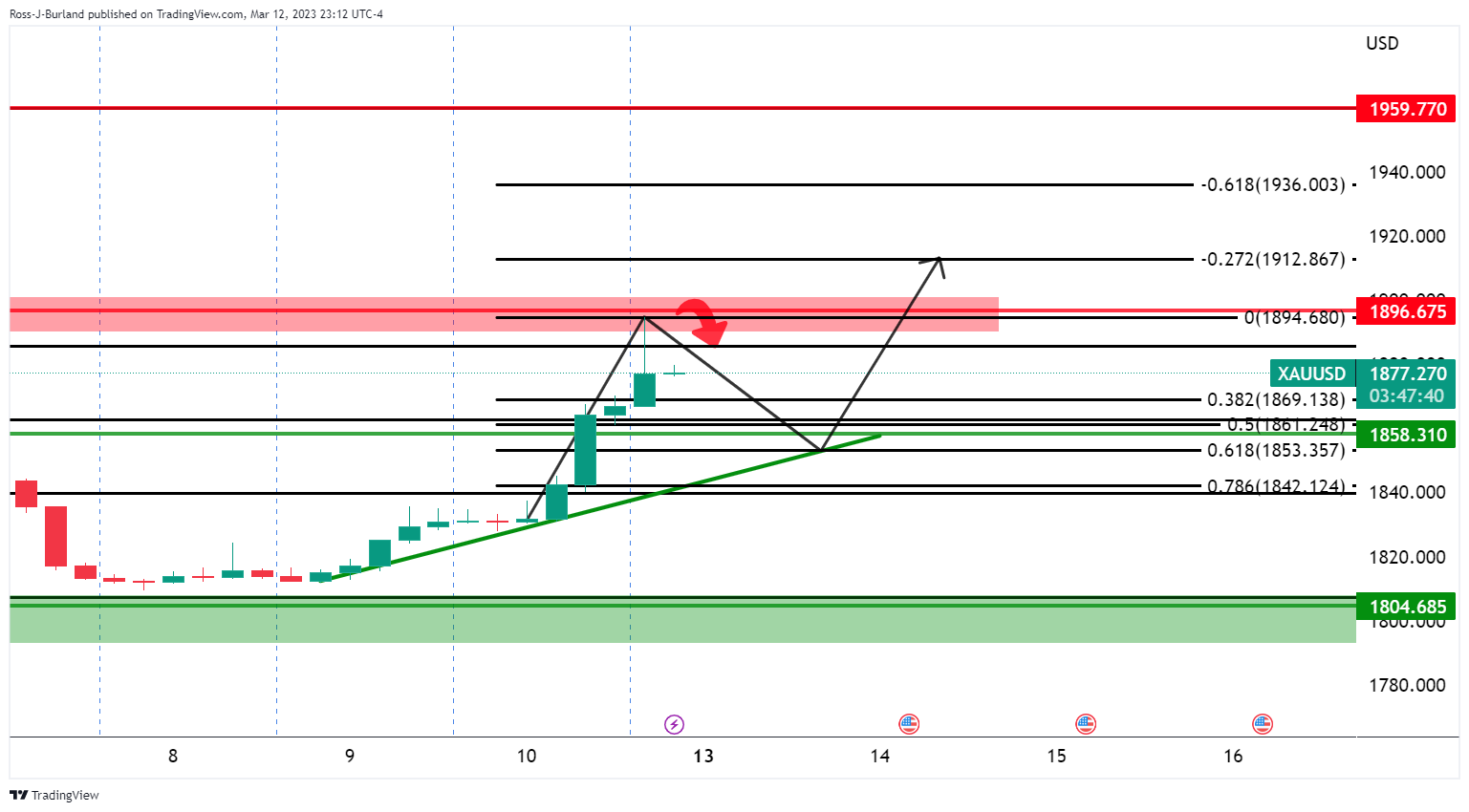

Gold technical analysis

Gold price has scaled above the 61.8% Fibonacci retracement (placed from February 2 high at $1,959.71 to February 28 low at $1,804.76) at $1.901.24. A decisive break above 61.8% Fibo indicates that the asset will recapture the previous swing high ahead.

Upward-sloping 20-and 50-period Exponential Moving Averages (EMAs) at $1,900 and $1,883.00 add to the upside filters.

The Relative Strength Index (RSI) (14) oscillates in the bullish range of 60.00-80.00, which indicates an upside momentum is already active. However, some corrections due to an overbought situation cannot be ruled out.

Gold two-hour chart

- USD/JPY is pressured to daily support near 132.90.

- All eyes are on US CPI for the day ahead.

USD/JPY is down some 1.3% on the day and has fallen from a high of 135.05 to a low of 132.28 ahead of what will be critical data in the US Consumer Price Index on Tuesday. The US Dollar was pressured at the start of the week and in a continuation to the fallout from the Nonfarm Payrolls.

While the Nonfarm Payrolls showed robust jobs growth, the rise in the Unemployment Rate and signs of cooling wage inflation sent the greenback lower as investors started to trim bets that the Federal Reserve will raise interest rates as sharply. The United States added 311,000 payrolls in February and the unemployment rate rose to 3.6%. However, a survey of economists polled by Reuters expected the United States to have added 205,000 jobs last month and the unemployment rate to hold steady at 3.4%. Average hourly earnings rose 0.2% last month after gaining 0.3% in January, below expectations of 0.3%.

On Monday, more fuel was added to the fire when markets priced in a Federal Reserve that will slow if not halt its raising of interest rates after US authorities moved to limit the fallout from the sudden collapse of Silicon Valley Bank. A new Bank Term Funding Program will offer loans from the Federal Reserve of up to one year to depository institutions, backed by United States Treasuries and other assets these institutions hold.

Consequently to all of the above, the US Dollar index, or DXY, which measures the greenback vs. a basket of major currencies, has dropped heavily benefitting the Yen. DXY has printed a fresh low of 103.484, tracking the fall in short-dated Treasury yields. The two-year note was paying as low as 3.997% at one point in New York trade early in the day. In fact, the yield dropped hard from the week´s highs of 4.534% in the biggest one-day drop since the financial crisis of 2008, on track for its biggest three-day decline since the Black Monday crash of 1987.

Also supporting the bid in the Yen is the fact that the Fed funds futures have been repriced as traders expect that the Fed's terminal rate will be lower. Investors are now expecting that to come in as low as 4.14% for December which was originally priced above 5% on Friday. Additionally, futures are showing a 21% chance of no hikes in rates from the Federal Open Market Committee when announcements will be made on March 22. A week ago futures were pricing about the same probability of a 50 basis point rate hike by policymakers.

US CPI eyed

Analysts at TD Securities explained that the US core prices likely gained momentum in February with the index rising a strong 0.5% MoM, as we look for the recent large relief from goods deflation to start normalizing. ´´Shelter inflation likely remained the key wildcard, while slowing gasoline and food prices will likely dent non-core CPI inflation. Our m/m forecasts imply 6.1%/5.5% YoY for total/core prices.´´

USD/JPY technical analysis

On a daily basis, USD/JPY is moving into a support zone that could result in a correction ahead of the US CPI data with the 134.50-70 eyed as per the daily Fibonacci scale as illustrated above. However, on a lower time frame:

There is a lot of resistance between 133.70 and 134.00 that the bulls will need to volt first.

Here is what you need to know on Tuesday, March 14:

The collapse of Silicon Valley Bank (SVB) and Signature Bank hit markets unexpectedly, creating a confidence crisis that continues to spread. The Federal Reserve announced it will make available additional funding to help assure banks have the ability to meet the needs of all their depositors. US President Biden spoke on Monday and said that no taxpayer money would be used to bail out banks. The impact has been large enough that a 50 basis point hike from the Federal Reserve at the March 21-22 meeting now seems unlikely.

The SVB collapse drove US stock markets to monthly lows. The Nasdaq managed to recover and gained 0.45%, while the Dow Jones lost 0.28% and the S&P 500 fell by 0.15%. The VIX rose 6% after pulling back during the second half of the American session.

The US Dollar dropped sharply at the beginning of the week, hit by the decline in US yields as markets consider the possibility of no interest rate hike from the Fed at the March meeting. As a result, US yields suffered the biggest three-day slide in three decades.

On Tuesday, the US Consumer Price Index (CPI) is due at 12:30 GMT (Daylight Saving Time began on Sunday, so the time of main US releases has changed). The numbers will be watched closely to see how the fight against inflation is going. Prior to the SVB crisis, the US CPI was seen as a critical report for the upcoming Fed’s monetary policy decision. At current hours, markets are seeing a softer Fed, as their focus is on the impact of the banking crisis.

USD/JPY fell for the third consecutive day, trimming losses during the American session after recovering above 133.00. EUR/USD broke above 1.0700, hitting the strongest level in a month. Reports suggest the European Central Bank will raise rates by 50 basis points on Thursday despite SVB turmoil. EUR/GBP pulled back to 0.8800. GBP/USD rose sharply from near 1.2050 toward 1.2200.

AUD/USD and NZD/USD took advantage of the weaker Dollar and rose to 0.6700 and 0.6250, respectively. The risk-off environment is not affecting commodity currencies so far. Latin American currencies dropped again, with USD/MXN hitting levels above 19.00.

Crude Oil prices fell more than 2%. WTI finished around $74.50, avoiding a daily close under January or February lows that would have increased the bearish pressure. Bitcoin surged, gaining more than 10%, surpassing $24,000.

Gold jumped above $1,900 to the highest since early February, boosted by the rally in the bond market. Silver rocketed by more than 6%, approaching $22.00.

Like this article? Help us with some feedback by answering this survey:

- GBP/USD bulls could be tiring at this juncture.

- Bears need to break the 1.2140 structure to cement the bearish case for the day ahead.

GBP/USD has run up towards an area of potential resistance area on the daily chart as the following will illustrate. This gives rise to the prospects of a significant correction over the coming week:

Drawing the Fibonacci from a presumed level where there could be resistance if the price were to continue higher over the next day or so, a 38.2% Fibonacci retracement level comes in near the 1.2080s as potential support.

At this point, however, drawing the Fib from current highs, the 38.2% comes in at 1.2050.

GBP/USD H4 chart

Drilling down to the 4-hour chart, above, there could be a pop to test 1.2200-1.2250 but a subsequent failure and break of the micro-dynamic support will possibly lay the foundations for the anticipated correction.

GBP/USD H1 chart

Meanwhile, the price is still very much on the front side of the trend. However, the hourly micro trendline is now under some pressure adding substance to the corrective bias at this point. A break of the 1.2140 structure is needed to cement the bearish case for the day ahead.

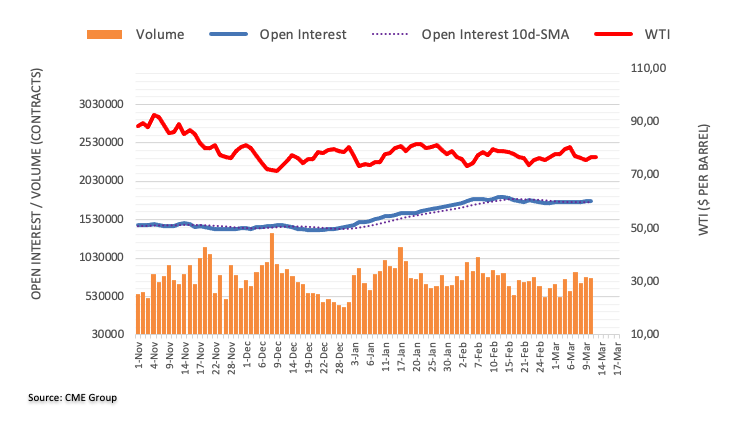

- Western Texas Intermediate drops almost 3% on possible US financial crisis risks.

- A weaker US Dollar put a lid on WTI’s price.

- WTI Price Analysis: Can test March’s lows around $72.30s.

Western Texas Intermediate (WTI), the US crude oil benchmark, dropped more than 2% on risk-off impulse, with a bank crisis in the United States (US) raising fears for a possible contagion. Nevertheless, a recovery in Chinese demand put a lid on WTI’s fall. At the time of writing, WTI is trading at $74.54 after hitting a high of $77.42.

US assets dropped in value last week due to worries about the impact of Silicon Valley Bank’s collapse, and regulators shut down another bank in New York on Sunday.

On Monday, U.S. stocks were mostly up but volatile as investors wondered if the Fed would stop raising interest rates in March. The government took urgent steps on Sunday to boost trust in the banks. [.N]

The sudden closure of SVB Financial raised questions about how other banks were affected by the Fed’s fast rate increases in the past year. It also made investors think the central bank might slow down its monetary policy.

Oil prices fluctuated on Monday as investors assessed how the news would affect the market. WTI price usually increases with a weaker US Dollar because oil becomes more affordable for people who use other currencies.

High US oil stockpiles have also pressured oil prices, which indicates weak demand.

Oil’s decline came after a positive day on Friday when US job data was better than expected. The number of jobs added in February was 311,000, much higher than the predicted 205,000 by market participants.

WTI Technical Analysis

When sentiment shifted sour, the US crude oil benchmark fell toward its daily low of $72.36. Buyers stepped in and dragged prices up, but buyers failed to reclaim the 20-day EMA at $77.01. WTI’s bias remains downward biased, and it might retest March lows, but it would need to clear support areas. The first support would be $74.00. A break below will expose the February 22 low of $73.83, followed by the $73.00, and then the YTD lows.

- NZD/USD is a touch off the highs but buoyed by US Dollar softness.

- US CPI is the next key data event with eyes on the Fed next week.

NZD/USD is higher at the start of the week, up some 1.65% at the time of writing after climbing from a low of 0.6134 and reaching a high of 0.6264 on the day so far. Risk currencies that are high beta to equities such as the antipodeans have been rebounding sharply from their four-month lows as the collapse of Silicon Valley Bank has been met by resolve from the US regulators and Federal Reserve in order to safeguard depositors.

As a consequence, the US Dollar has struggled in the face of sinking bond yields amid the SVB fallout. The two-year note was paying as low as 3.997% at one point in New York trade and fell from the start of the week´s highs of 4.534% in the most significant one-day drop since the financial crisis of 2008.

Additionally, Fed funds futures have been repriced as traders expect that the Fed's terminal rate will be lower. Markets are now pricing as low as 4.14% for December which was originally priced above 5% on Friday. Moreover, futures are showing a 21% chance of no hikes in rates from the Federal Open Market Committee when announcements will be made on March 22.

´´Contagion fears are high and bond markets have taken the view that the Fed will hike just once more, and then start cutting by September, presumably on the view that confidence and spending will hit a brick wall,´´ analysts at ANZ bank explained.

´´That’s possible, but of course, the inflation starting point is problematic. The point is there are a lot of ifs and buts, and more volatility seems likely in Consumer Price Index data tonight. New Zealand considerations have been well and truly relegated to the background, and this is the USD show. Positioning, and the need to be nimble, are likely to dominate the economics for now.´´

It is worth noting that the Reserve Bank of New Zealand raised interest rates by 50 basis points in a widely anticipated move at its February meeting. The RBNZ has hiked the OCR by a total of 450 basis points in ten consecutive meetings and the rate now stands at a 41-year record of 4.75%.

- XAG/USD advances as US Treasury bond yields undermine the US Dollar.

- The XAG/USD is testing the confluence of the 50/100/200-day EMAs.

- XAG/USD Price Analysis: To remain upwards in the short term, though the rally’s size suggests a mean reversion correction.

XAG/USD surges sharply in Monday’s session, up by more than 6% on investors flying to safety. US Treasury bond yields collapsed due to regional bank failure in the United States (US) blamed on higher rates. Therefore, US bond yields collapsing are a tailwind for the white metal prices. At the time of writing, the XAG/USD is trading at $21.76.

XAG/USD Price Action

The white metal is testing solid resistance in the confluence of the 200, 50, and 100-day Exponential Moving Averages (EMAs), each at $21.79, $21.85, and $21.87, respectively. In addition, the Relative Strength Index (RSI) broke above the 50 neutral lines, portraying buying pressure strength. The Rate of Change (RoC) suggests buyers moved aggressively, which could open the door for a mean reversion move. Therefore, traders should be careful.

With XAG/USD breaking above the 200-day EMA would pave the way toward $22.00 a troy ounce. Once done, the XAG/USD next resistance would be $23.00 before testing the February 23 high at $23.59.

In an alternate scenario, the XAG/USD first support would be the 20-day EMA at $21.16. A breach of the latter will expose the $21.00 figure, followed by the March 13 low of $20.50, before falling to YTD lows at $19.92.

XAG/USD Daily Chart

XAG/USD Technical Levels

- EUR/USD bulls are running higher into potential resistance.

- All eyes are on the Federal Reserve, European Central Bank, and Tuesday´s US Consumer Price Index, CPI.

EUR/USD is up by over 0.9% in midday trade on Wall Street aided by a weaker US Dollar and ahead of the European Central Bank's policy meeting on Thursday. Expectations call for the ECB to deliver a 50-basis point hike and hawkish rhetoric is assumed which is buoying the Single Currency which has traveled from a low of 1.0650 to a high of 1.0748 so far.

Meanwhile, the US Dollar continued to bleed heavily on Monday as markets bet the Federal Reserve will be less aggressive in raising interest rates to curb inflation. US authorities have made moves to try to lessen the damage from the recent collapse of Silicon Valley Bank.

A new Bank Term Funding Program will offer loans from the Federal Reserve of up to one year to depository institutions, backed by United States Treasuries and other assets these institutions hold.

Consequently, the US dollar index, or DXY, which measures the greenback vs. a basket of major currencies, has dropped to a fresh low of 103.484, tracking the fall in short-dated Treasury yields. The two-year note was paying as low as 3.997% at one point in New York trade and tumbled from the start of the week´s highs of 4.534% in the biggest one-day drop since the financial crisis of 2008, on track for its biggest three-day decline since the Black Monday crash of 1987. Meanwhile, Fed funds futures have been repriced as traders expect that the Fed's terminal rate will be lower. Markets are now pricing as low as 4.14% for December which was originally priced above 5% on Friday. Moreover, futures are showing a 21% chance of no hikes in rates from the Federal Open Market Committee when announcements will be made on March 22.

US Consumer Price Index will be key

This all makes for a very important red calendar event this week in the US Consumer Price Index data. This will be released on Tuesday morning in the US session and traders will use the data to speculate how the Federal Reserve will react later this month when the central bank will meet to decide on its interest rate setting.

´´The release of US CPI inflation data tomorrow is expected to show headline price pressures remains elevated at 6% YoY, well above the Fed’s 2% Inflation forecast,´´ analysts at Rabobank said. ´´If the Fed were to back away from its tightening cycle, it may have a credibility issue on its hands. Additionally, for some years Fed officials have argued that monetary policy is not the right tool to tackle financial stability,´´ the analysts noted.

´´Given the announcement that the Fed has made over the weekend in conjunction with the Treasury to stop contagion risks from the SVB crisis, the FOMC may favor continuing to hike rates next week with a focus on the inflation risks,´´ the analysts at Rabobank argued.

´´We maintain our 1- and 3-month forecasts of EUR/USD 1.06 and 1.06 respectively, though clearly, we will be watching the forward guidance at this month’s Federal Reserve (and ECB) policy meetings closely,´´ the analysts explained.

EUR/USD technical analysis

There appears to be more gas in the tank for the Euro at this stage but it is running low. EUR/USD approaches a key resistance area and has left territory behind hastily that might require a correction in order to mitigate uneven grounds in EUR/USD´s bids and offers between 1.0600-1.0650 on the daily chart:

On the EUR/USD hourly chart, a 50% mean reversion of the prior bullish impulse meets the trendline support near 1.07 the figure:

A break of the EUR/USD trendline could be the makings for the continuation of the distribution that appears to be taking place on the daily chart with the price on the backside of the prior dominant bullish trend.

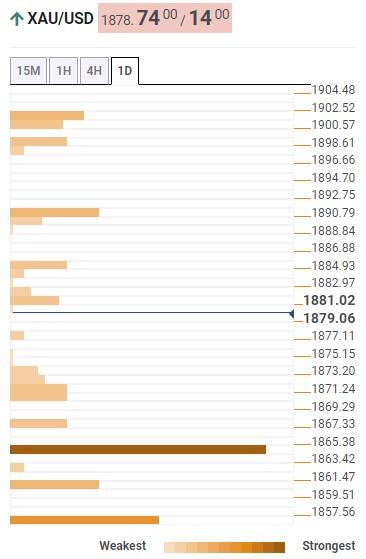

- The XAU/USD (Gold) commodity starts the week positively, trading at $1,906.70, up by 2.11% on the day.

- Increased market volatility and rising risk led to a surge in demand for safe-haven assets like Gold.

- Technical indicators, such as the daily 20-SMA and 50-SMA, suggest a potential bullish outlook for gold.

- Due to risk aversion, US yields have reached their lowest levels in recent months.

Daily price movements:

XAU/USD (Gold) commodity opens the first day of the week at $1,867.24, with an intraday high of $1,913.13 and a low of $1,867.24. Gold trades at $1,906.70 at the press time for the first time since February 3rd, 2023, up by 2.11% on Monday.

The sharp drop in US yields is considered the primary catalyst for the rise in the price of Gold. The US 10-year yield has fallen to 3.41%, approaching its year-to-date lows from its previous level above 4.0%. Meanwhile, the 2-year yield reached its highest since 2008 and fell to its lowest intraday level since October 2022, at 4.00%.

Following the collapse of Silicon Valley Bank (SVB), concerns have arisen about the state of the banking sector, which has caused a decrease in expectations for a rate hike by the Federal Reserve (Fed). Investors are watching the potential impact of this crisis on economic data.

Key economic events:

The upcoming US February Consumer Price Index (Feb) on Tuesday and US Retail Sales (Feb) on Wednesday are expected to be critical for monetary expectations and is also closely monitored.

However, following the unexpected SVB collapse, markets are now pricing in a more relaxed stance by the Fed.

Technical view:

Technical indicators suggest a potential bullish outlook for Gold in the short term. The daily 20-SMA and 50-SMA are at $1,838.83 and $1,873.21, respectively, indicating a possible bullish trend. The RSI(14) is at 64.970, indicating potential bullish momentum.

Resistance levels for Gold are at $1,884.08, $1,898.25, and $1,926.40, while support levels stand at $1,841.76, $1,813.61, and $1,799.44. The daily pivot point is $1,855.93.

Citing eurosystem sources, MNI reported on Monday that the European Central Bank was planning to go ahead with the 50 basis points (bps) rate hike at its upcoming meeting despite sliding market rate expectations amid Silicon Bank Valley turmoil.

MNI further explained that dovish policymakers were likely to argue that the changing economic environment would warrant more caution in regard to policy tightening.

Market reaction

EUR/USD showed no immediate reaction to this headline and was last seen rising 0.8% on a daily basis at 1.0725.

- USD/CAD falls amidst broad US Dollar weakness across the board.

- The SVB crisis in the United States sent ripples in the financial markets, with UST bond yields plummeting.

- USD/CAD Price Analysis: In the near term, neutral to downward biased.

USD/CAD drops from around daily highs of 1.3815, falls 0.90% on overall US Dollar (USD) weakness, spurred on an ongoing Regional Bank crisis in the US. Therefore, UST bond yields plunge; consequently, the buck is down. At the time of writing, the USD/CAD is trading at 1.3692.

USD/CAD Price Action

After rallying to YTD highs of 1.3862, the Canadian dollar (CAD) is recovering some ground, eyeing a daily close below the December 12 high at 1.3705. Even though the financial markets are punishing the US Dollar (USD), safe-haven flows would increase volatility in USD-denominated currency pairs. If the banking crisis ease, traders should expect a repricing of the Fed, meaning further upside in the USD/CAD is expected.

In the short term, the USD/CAD might fall toward 1.3600, but solid support areas would face it. The first support would be the February 20 daily high at 1.3665, followed by the 1.3600 figure. A breach of the latter will expose the 20-day Exponential Moving Average (EMA) at 1.3496 before testing the 50-day EMA at 1.3280.

In an alternate scenario, the USD/CAD first resistance would be 1.3700. Once cleared, the pair could rally towards the 1.3800 area, ahead of testing the YTD high at 1.3862.

Oscillators like the Relative Strength Index (RSI) at 58.22 aiming lower suggests that sellers are gathering momentum. The Rate of Change (RoC), shifted toward neutral territory, displaying that buying pressure is waning.

Trend: In the near term, neutral to downwards.

USD/CAD Daily Chart

USD/CAD Technical Levels

Strategists at ANZ Bank are raising Gold forecasts. They see limited downside, with a 0-3 month target of $1,800. Meanwhile, they have lifted their year-end forecast by $100 to $2,000.

Upside bias remains intact

“We see the Gold price holding above $1,800 in the short-term. Any dips below this should be short-lived, as opportunistic buying would likely emerge.”

“As the macro backdrop becomes more supportive later in the year, we see the price trending higher. We have lifted our quarterly forecasts, targeting $2,000 towards year-end.”

- The AUD/USD currency pair starts the week positively, trading at 0.6716 at the press time, up by 2.11% on the day.

- Technical indicators, such as the daily 20-SMA and 50-SMA, suggest a potential bullish outlook for AUD/USD.

- SVB banking catastrophe’s ripple effects and the consequences of the Fed’s rate hike decision support the pair.

Daily price movements:

AUD/USD currency pair opens the first day of a new week at 0.6575, with an intraday high of 0.6718 and a low of 0.6577. The pair trades at 0.6716 at the press time, up by 2.11% on the day, just below Monday’s ATH price.

The recent issues with Silicon Valley Bank (SVB) and Signature Bank have highlighted the vulnerable state of US banks, which has dampened expectations for additional interest rate increases from the Federal Reserve (Fed). As a result, Goldman Sachs now predicts a delay in rate hikes in March, and the Fed Fund futures (*) have reduced the likelihood of a 0.50% increase in the Fed rate.

Consequently, the US Dollar Index (DXY) has fallen to its lowest level in a month, trading near 103.60 at the press time.

* Fed Fund futures directly reflect collective marketplace insight regarding the future course of the Federal Reserve's monetary policy. (Source: CME Group’s website)

Key economic events:

Investors will be closely watching the US Consumer Price Index (CPI) (excluding Food and Energy) data for February, set to be released on Tuesday, to gain a better understanding of potential Federal Reserve (Fed) actions on the pace of interest rate increases, which could impact the strength of the US Dollar.

Additionally, both the Employment Change s.a. (Feb) and Unemployment Rate s.a. (Feb) released by the Australian Bureau of Statistics on Thursday will be the key economic events for AUD this week.

Technical view:

Technical indicators suggest a potential bullish outlook for the AUD/USD in the short term. The 20-day SMA and 50-day SMA are at 0.6777 and 0.6885, respectively, indicating a possible bullish trend. The daily 38.2% Fibonacci level is at 0.6593, with the 61.8% Fibonacci level at 0.6611. The RSI(14) is at 44.516, indicating potential bullish momentum. Resistance levels for AUD/USD are at 0.6623, 0.6670, and 0.6699, while support levels stand at 0.6547, 0.6517, and 0.6471. The daily pivot point is at 0.6594.

If the economy slips into a mild – but still traumatic – recession, the Yen will benefit, and so will the Euro, but the biggest winners may be the NZD and the AUD, according to Kit Juckes, Chief Global FX Strategist at Société Générale.

USD/JPY is still following yields, EUR/USD has more complicated drivers but should rise

“We may need clear evidence that the crisis won’t be contagious, and that it won’t alter the path of ECB rates, before the Euro makes new cycle highs, but USD/JPY continues to track yield differentials and history tells us that USD/JPY hit 160 in April 1990, fell to 120 as rates fell to 3%, and kept on going, falling below 80 1995.”

“Continued FX volatility is assured as the markets fret about contagion, and if that were to emerge, the Dollar can turn higher very quickly. But if this event validates the signals from the yield curve and leads to a 1990s-style mild recession, the Dollar will fall further. The Yen will benefit, and so will the Euro, but the biggest G10FX winners in the short run may be the NZD and even the AUD.”

- The USD/MXN pair depreciates close to 2%, caused by the SVB crisis

- It reached a weekly maximum of $19.1789, a level not seen since February.

- USD/MXN Price Analysis:: A close for the week above $19.00 could generate an advance towards $19.50.

The Mexican Peso (MXN) depreciates the most against the US Dollar (USD) on fears of a possible contagion after the failure of the Silicon Valley Bank (SVB). Over the weekend, the state seized New York’s Signature Bank amidst the need to stabilize the financial system. At the time of writing, the USD/MXN is trading at 18.8246, above its opening price by 1.85%.

The crisis in regional banks in the US weaken the Mexican Peso

The domestic crisis in the banking sector in the United States (USD) caused a change in market sentiment. The winner is the precious metals segment, with Gold breaking the $1900 barrier. Wall Street turned positive, except for financials, which are losing as US Treasury bond yields plummet. US Federal Reserve (Fed) interest rate expectations lie at a 25 bps hike in March at a 64.2% change, and for no change, at 35.8%. Traders speculate that the current crisis in the Regional Bank segment could keep the Fed from tightening monetary conditions.

The US 2-year Treasury bond yield has dropped 50 bps, the most since the Global Financial Crisis (GFC) in 2008, barely above the 4% threshold. The 10-year note rate sits at 3.466%, down 23 bps.

The CME FedWatch Tool has the Federal Funds Rate (FFR) peaking at 4.75% - 5.00%, with traders expecting rate cuts in June, September, and December.

As a consequence, the USD/MXN appreciates in uncertain scenarios. Large capitals, fearing a crisis, move their assets out of emerging markets and return to the US Dollar or Gold.

Let’s remember that Jerome Powell, the head of the Federal Reserve, testified before the Senate’s finance committee and the House of Representatives. Powell said that interest rates could rise to higher levels than projected. He added a faster rate increase, depending on economic data.

Given this scenario, the USD/MXN broke important technical ceilings, such as the 50 and 100-day Moving Average, at 18.6546 and 19.010, respectively. However, it has fallen below $19.00, having that barrier as the first top.

USD/MXN Technical analysis

From a technical point of view, the USD/MXN could consolidate between the 50-day and 100-day Moving Averages (MM), at 18.6549 and 19.00, respectively. The current trend has turned neutral. However, a break above $19.00 would open the way to the February 6 high at 19.2905 units. With a break of this area, the USD/MXN pair could reach the 200-day Moving Average (MM), at 19.4187.

Momentum indicators such as the Relative Strength Index (RSI) have turned bullish above 50, while the Rate of Exchange (RoC) shows increased demand for dollars.

On the other hand, a drop below the 50-day MA at 18.6555 could cause a decline toward the 20-day MA at 18.3821 before testing the $18.00 barrier.

- US yields fall dramatically pushing DXY to the downside.

- Markets attempt to stabilize amid market jitters.

- GBP/USD up for the fourth day in a row, looking at 1.2200.

The GBP/USD broke above 1.2150, reaching the highest level since mid-February, boosted by a sharp decline of the US Dollar Index (DXY). A sharp drop in US yields occurs as investors shift their bets for a softer Federal Reserve, amid market concerns about the banking industry.

DXY slumps on a new scenario

The collapse of Silicon Valley Bank and its effect are driving markets. Major US indices are mixed on Monday, with the banking sector falling sharply. The Dow Jones is at four-month lows levels.

The ongoing situation has diminished the odds of a 50 basis points rate hike from the Federal Reserve next week and sent US yields sharply to the downside. On Tuesday, the US will release February’s Consumer Price Index, a key input, now being offset by recent developments. Before the SVB collapse, larger-than-expected inflation numbers would have cemented exceptions for a 50bps rate hike, but the case now is more complex with market participants projecting a softer Fed.

US yields are falling sharply at a speed not seen in years. The US 10-year was above 4% last week and on Monday bottomed at 3.42%. The slide in yields has weakened the US Dollar against it main European competitors. The DXY is down by almost 1% at the lowest in four weeks.

The ramifications of the banking crisis in the US crossed the Atlantic. In the UK, the government and the Bank of England facilitated a deal for HSBC o buy Silicon Valley Bank UK for 1 pound. On Tuesday, before US CPI, the UK will release employment numbers.

The GBP/USD is trading at monthly highs at 1.2176, with a strong bullish momentum. On the upside, the next strong resistance area is seen at 1.2200. The pair is retaking the 20-day Simple Moving Average (SMA). The 1.2100 zone and 1.2060 have become relevant support levels.

GBP/USD daily chart

Economists at Erste Group Research expect the EUR/USD pair to hover around 1.08 in the short term. In the medium term, the US Dollar is expected to weaken.

Dollar to weaken slowly in the medium term

“Varying economic data should continue to drive rapidly changing expectations for policy rates in both economies. The environment thus remains very uncertain. However, neither currency should become more attractive.”

“EUR/USD should thus remain in a volatile sideways movement around 1.08 for the time being.”

“In the medium term, we expect a slow weakening of the Dollar, as interest rates should start to fall here earlier than in the Eurozone.”

The Federal Reserve Bank of New York's monthly Survey of Consumer Expectations showed on Monday that the US consumers' one-year inflation expectation dropped to the lowest level since May 2021 at 4.2% in February, compared to 5% in January.

Further details of the publication showed that the three-year ahead expected inflation remained unchanged at 2.7% and the five-year ahead expected inflation edged higher to 2.6% from 2.5%.

Finally, the year-ahead expected earnings growth held steady at 3%.

Market reaction

The US Dollar stays on the back foot after this report and the US Dollar Index was last seen losing 1% on the day at 103.60.

The US Dollar has continued to weaken sharply. A big upside surprise in the US Consumer Price Index (CPI) report due out tomorrow is required to lift the greenback, economists at MUFG Bank report.

Another 25 bps hike next week

“On balance we believe the latest labour market developments favour another 25 bps hike rather than a larger 50 bps hike.”

“Market attention will now shift to the release of the latest US CPI report tomorrow. It would likely take a significant upside inflation surprise now to revitalize speculation over a larger 50 bps hike at next week’s FOMC meeting and trigger a US Dollar rebound.”

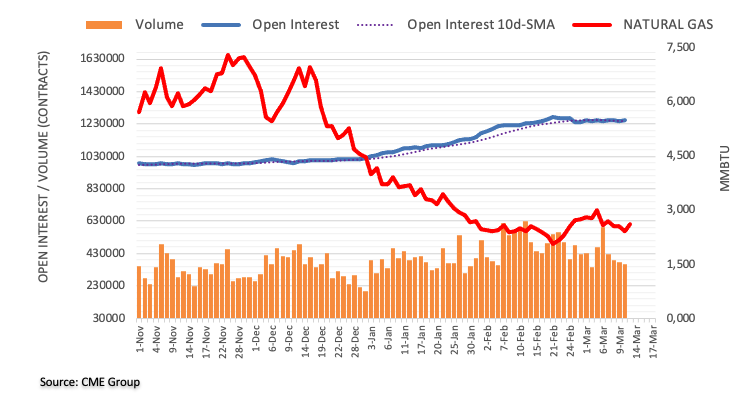

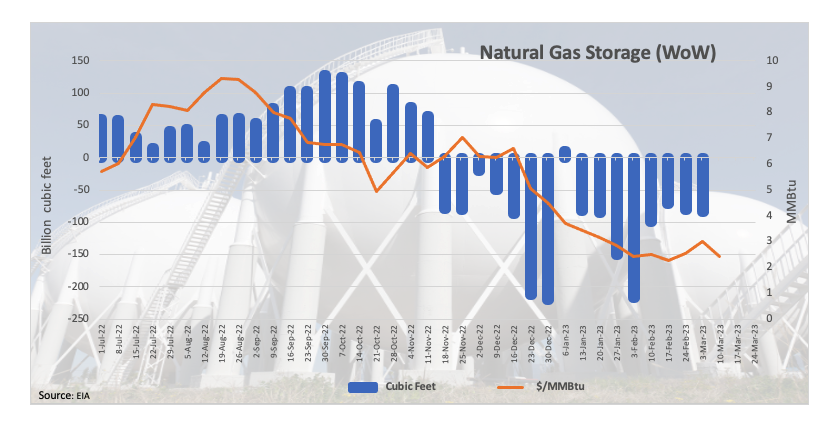

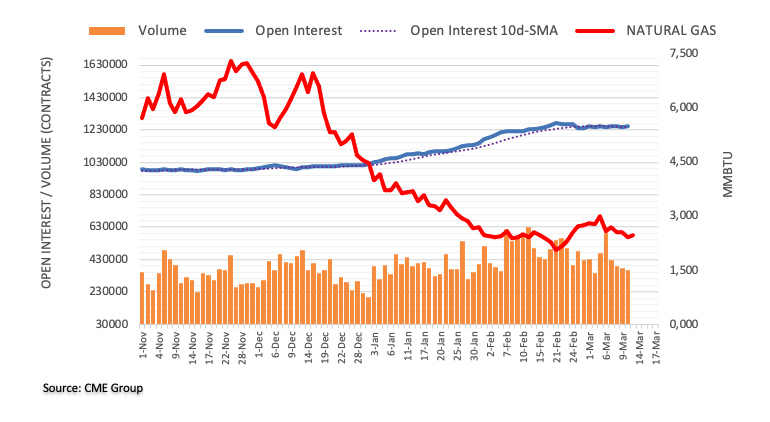

Prices of natural gas seem to have met some decent support in the $2.40 region per MMBtu and manage to leave behind three consecutive daily pullbacks at the beginning of the week.

The commodity gathers some traction on the back of colder days ahead in the US, although the broad-based outlook remains tilted to the negative side amidst the absence of a strong driver for the time being. On this, Friday’s figures in natural gas futures markets appear to support the underlying negative outlook for the commodity in the very near term at least.

Against that, another test of the 2023 low in the sub-$2.00 region should not be ruled out, while the $3.00 mark continues to cap occasional bullish attempts for the time being. Above this region, natural gas should meet temporary resistance at the 55-day SMA at $3.145, just ahead of the Fibo retracement of the December-February drop at $3.182.

Later in the week, the EIA will release its weekly report on natural gas storage.

Natural Gas levels to watch

At the moment, Natural Gas prices are advancing 6.87% at $2.594 and faces the next up-barrier at $3.009 (monthly high March 3) seconded by $3.145 (55-day SMA) and finally $3.182 (Fibo retracement). On the downside, a break below $1.967 (2023 low February 22) would expose $1.795 (monthly low September 21 2020) and then $1.605 (monthly low July 20 2020).

Silver price has plunged 16% so far this year. Economists at ANZ Bank expect the precious metal to perform better by the end of the year.

Silver price action diverges from fundamentals

“Normally, Silver outperforms Gold in a rising price environment, suggesting Silver should do well in the later part of the year.”

“From a supply-demand perspective, the market is expected to remain undersupplied for this year.”

See – Gold Price Forecast: XAU/USD bullish momentum continues, eyes on next resistance at $1,960 – ANZ

- The upside momentum in EUR/USD picks up pace on Monday.

- Next on the upside comes the 1.0800 mark.

EUR/USD extends the buying interest to fresh multi-week highs north of 1.0700 the figure at the beginning of the week.

The continuation of the uptrend appears favoured for the time being. Against that, a convincing move above Monday’s peak at 1.0737 should open the door the wekly high at 1.0804 (February 14). Further up, there are no resistance levels of note until the 2023 high at 1.1032 (February 2).

Looking at the longer run, the constructive view remains unchanged while above the 200-day SMA, today at 1.0324.

EUR/USD daily chart

Senior Economist at UOB Group Alvin Liew reviews the latest BoJ monetary policy meeting.

Key Takeaways

“The Bank of Japan (BoJ) kept its policy measures unchanged at last Monetary Policy Meeting (MPM) helmed by exiting BoJ Governor Kuroda. The decision was unanimous, and the BoJ kept steadfastly to its easing stance. Post-BoJ announcement saw a jump of the USD/JPY above 136 while the Nikkei stock index fell.”

“BoJ Outlook – To Shift Or Not To Shift YCC Policy, That Will Now Be Under The New BoJ Governor Ueda: With Kuroda’s last MPM decision now out of the way, the attention will shift to Kazuo Ueda who is likely to win approval from the Upper House of the Diet today as the new BoJ Governor. While we see an exit from the YCC and negative interest rates is inevitable for Japan, the question is how Ueda will execute his plan. We believe Ueda will proceed at a gradual, well-telegraphed pace, and not a sharp and sudden reversal. We see it in two broad steps, 1) Protracted adjustment to its forward guidance on YCC and interest rates (Apr to Dec 2023) and 2) Scrapping of YCC and lifting of the negative policy rate in early 2024.”

“The next BoJ MPM on 27-28 Apr will be widely watched event given that it will be the first BoJ decision under Ueda and the outcome of the Shunto (annual wage negotiation) will be out by then, and it will include an updated Outlook Report (The Bank's View).”

EUR/USD edges back under the 1.07 level. Economists at Scotiabank expect the world’s most popular currency pair to sustain more losses on a break below the 1.0635 mark.

EUR reversal from the highs has been quite significant

“The EUR reversal from the highs has been quite significant and suggests a failure/rejection at the 55-Day Moving Average (1.0716).”

“EUR/USD losses may extend a little more on a break under 1.0635 intraday.”

See: EUR/USD set to extend its race higher toward the 1.0780/1.0800 area – ING

- DXY intensifies the decline and breaches 104.00 on Monday.

- The 55-day SMA near 103.50 should offer initial contention.

DXY extends the strong bearish momentum and breaks below the 104.00 support to record new multi-week lows.

In case sellers push harder, then the index should face a temporary support at the 55-day SMA at 103.51 prior to the weekly low at 102.58 (February 14).

In the meantime, while below the 200-day SMA at 106.62, the outlook for the greenback is expected to remain negative.

DXY daily chart

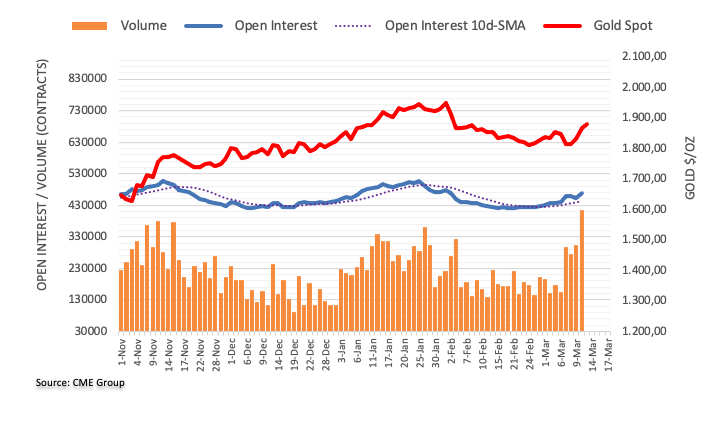

- Gold rally goes on, tests $1,900.

- Yellow metal rises 5% in three trading days.

- US Yields hit lowest levels in months amid risk aversion.

Gold price is up by more than 2% on Monday, adding to last Friday’s gains boosted by a rally in US Treasury bonds as investors fly to safety and pare Federal Reserve rate hike bets.

XAU/USD hit $1,900 for the first time since February 3. It then pulled back modestly to $1,895. The rally in gold has been dramatic, rising more than $90 since Thursday. Above $1,900 the next resistance area is seen around $1,920.

The key driver of the yellow metal rally is the sharp decline in US yields. The US 10-year has fallen from above 4.0% to 3.41%, approaching year-to-day lows; the 2-year was above 5.0% on Wednesday (highest since 2008) and a few moments ago reached the lowest intraday level since October at 4.00%.

The collapse of the Silicon Valley Bank triggered concerns about the banking sector, weighing on Fed rate hike expectations. Investors are looking at the impact of the crisis that is offsetting incoming economic data. On Tuesday, the US February Consumer Price Index is due and it was supposed to be critical for monetary expectations. After the SVB collapse, markets are pricing in a softer Fed.

Technical levels

- XAG/USD starts the week with a 5.24% intraday gain, touching a high of $21.61.

- Technical indicators, such as the RSI(14) and daily 20-SMA, suggest a potential bullish outlook for silver.

- US CPI ex Food and Energy data (Feb) is the critical economic event to be followed on Tuesday.

Daily price movements:

XAG/USD (Silver) opens the day at $20.54, with the precious metal experiencing an intraday gain of 5.24% to trade at $21.61 at the time of press. Silver hits an intraday high of $21.61, indicating a surge in bullish market sentiment.

At the start of the new week, the US Dollar faces significant selling pressure due to market reevaluation of the Federal Reserve’s (Fed) future policy actions after the recent collapse of Silicon Valley Bank (SVB). This also acts as a booster for Silver to climb higher on the day.

Key economic events:

Markets will be monitoring Tuesday’s US Consumer Price Index ex Food & Energy (MoM)(Feb) data to understand better the possible Fed actions on the speed of rate hikes decisions which will affect the US Dollar’s strength.

Technical view:

Technical indicators suggest a potential bullish outlook for XAG/USD silver in the short term. The RSI(14) is currently at 52.93, indicating bullish momentum. The daily 20-SMA is $21.03, indicating that the current price may trend higher. Daily pivot resistance levels for Silver are $20.91, $21.30, and $21.81, while support levels stand at $20.02, $19.52, and $19.13. However, the daily 50-SMA is $22.40, indicating a long-term bearish trend.

Technically, bullish momentum is continuing after breaking the range of $1,845-1,850 on Friday. Gold needs to trade high to continue this momentum, analysts at ANZ Bank report.

Cautious on false breakout

“Gold price broke the key resistance of $1,845 following rise in US unemployment number and collapse of Silicon Valley Bank on Friday. This suggests that bullish momentum is likely to continue, however, one should be cautious of a false breakout.”

“To continue the bullish momentum, Gold needs to trade above $1850 level. The next resistance is at $1,960.”

“On the downside, if XAU/USD comes back below $1,845 range, then a consolidation looks possible until it breaks the key support of $1,810. A break of this could trigger a technical sell-off, dragging prices to a low of $1,750. We see this level setting the lower bound for this year’s price range.”

US President Joe Biden said on Monday that no losses will be borne by US taxpayers following the collapse of Silicon Valley Bank and Signature Bank.

Biden further noted that investors in those banks will not be protected and reminded that "no one is above the law."

Biden also explained that the quick administration action should give Americans confidence that the US banking system is safe and added that he will ask Congress and regulators to strengthen bank rules.

Market reaction

These comments don't seem to be having a significant impact on financial markets. As of writing, the benchmark 10-year US Treasury bond yield was down 6% on the day at 3.48% and the US Dollar Index was losing 0.6% at 104.00.

SVB (Silicon Valley Bank) rattled the US financial sector and global markets last week. Economists at HSBC analyze investment implications.

USD downside to occur when the economic downturn is further advance

“In the short term, we expect continued volatility in US equities and credit and hence we stress our focus on quality. We think the backstop provided by the Fed for banks should be helpful to restore public confidence in the banking system. While tech VC may face more headwinds than before, we maintain a neutral view on IT and focus on established cash-generative industry leaders. As for financials, some banks may raise deposit rates, which could weigh on profitability but net interest margins are very healthy, causing us to keep a neutral view on the sector.”

“For fixed income investors, the increased level of uncertainty may direct the Fed to a 0.25% hike (as per our view) rather than 0.5% in March. The volatility and increased unemployment have moved the markets’ view of the peak rate from 5.69% to 5.1%, close to our 5.25%-5.5% forecast. We continue to overweight global investment grade and stay invested in senior and Basel III Tier 2 financials bonds.”

“The US Dollar should continue to consolidate. The fall in rate expectations weighed on USD last week, but on the other hand, the USD benefits from a safe haven bid. We expect further USD downside to occur when the economic downturn is further advanced and global risk appetite bounces.”

The US Bureau of Labor Statistics (BLS) will release the most important inflation measure, the US Consumer Price Index (CPI) figures, on Tuesday, March 14 at 12:30 GMT. As we get closer to the release time, here are the forecasts by the economists and researchers of 10 major banks regarding the upcoming United States inflation print for the month of February.

The annual inflation is expected to decline to 6.0% from 6.4% in January, while the Core CPI, which excludes volatile food and energy prices, is seen at 5.5% from 5.6%. On a monthly basis, the CPI is forecast at 0.4%, while the Core CPI is also expected at 0.4%.

ANZ

“We expect US core CPI inflation to increase by 0.4% MoM and headline CPI to rise by 0.5% in February.”

Commerzbank

“In February, although the headline inflation rate is likely to have fallen from 6.4% to 6.1%, the core rate probably fell only slightly from 5.6% to 5.5% and thus remains far too high. At 0.5%, the MoM rate of the core index is likely to be above average again. From the Fed's point of view, such a report would probably not provide convincing enough support for the ‘disinflation process’ identified by Fed Chairman Powell and would therefore argue in favor of stronger interest rate hikes again.”

Credit Suisse

“We expect core CPI inflation to remain steady at 0.4% MoM in February, causing the YoY reading to tick down to 5.5%. Energy and food prices are likely to moderate, with headline inflation also coming in at 0.4% MoM. A reading in-line with our expectations would be uncomfortably high for the Fed, but still consistent with gradual disinflation this year.”

Deutsche Bank

“We think the headline CPI and core CPI will both round to 0.4% MoM which is where the consensus is. This will translate to headline dropping 0.4pp to 6% YoY and core down a tenth to 5.5% YoY.”

RBC Economics

“We expect Tuesday’s report to show the YoY measure falling to 5.9% in February compared to 6.4% January (which was the lowest reading since October 2021). Much of that easing has come from lower energy prices and signs that food price growth is past its peak. Inflation pressures across other goods and services has also been edging lower, though stickier than expected in recent months. We expect the February numbers to look better with ‘core’ inflation (which excludes food and energy products) dipping to 5.4% from 5.6% in January. Robust US labour market data indicates strong economic momentum at the start of 2023, and stickier inflation suggests it may take longer to get back to the 2% target. This is bolstering the case for further interest rate hikes from the Fed.”

NBF

“The energy component may have had only a limited effect on the headline index, with prices remaining more or less flat in this segment in the month. Expected gains for shelter, used vehicles and airline fares could still result in a 0.4% monthly increase in headline prices. The core index may have seen a similar rise, which would translate into a one-tenth drop in the annual rate to 5.5%.”

TDS

“Core prices likely gained momentum in February with the index rising a strong 0.5% MoM, as we look for the recent large relief from goods deflation to start normalizing. Shelter inflation likely remained the key wildcard, while slowing gasoline and food prices will likely dent non-core CPI inflation. Our MoM forecasts imply 6.1%/5.5% YoY for total/core prices.”

CIBC

“A further increase in prices at the pump and continued pressure in core categories suggest that prices rose by an uncomfortably fast 0.4% in February. Looking at core (ex. food and energy) categories, shelter prices are set to peak imminently as the typical lags with new leases that are resetting at lower rates kick in, but continued pressure in core services outside of shelter, in line with the tight labor market, will keep the Fed on a tightening path. Moreover, the deflation in core goods prices appears to have ended, as supply chains have normalized, and used car prices as measured by industry gauges climbed in February. A consensus-matching core CPI reading will likely be good enough to keep the Fed on track for a 25 bps hike this month.”

Wells Fargo

“We look for another monthly increase of 0.4% in the overall CPI in February, which would put the YoY rate at 6.0%. We still see inflation set to grind lower, but the process is likely to be bumpy and take time. Despite some directional improvement over the past couple of quarters, prices are still growing well-above the Fed's 2% target, and the tight labor market suggests that there are still inflationary pressures that could forestall a full return to 2% inflation.”

CitiBank

“We expect a softer 0.4% MoM increase in headline CPI due to a retracement of utility gas prices in line with falling natural gas prices. Details should reveal continued strength in key services prices, although starting with February data could be the start of an expected slowing in shelter prices which comprise close to 40% of core CPI. Other non-shelter services should be strong overall, although with a continued drag from the medical insurance component in CPI which notably will not be included in PCE inflation. Prices for medical services themselves, however should remain strong, as should prices for recreation services and transportation services, including a 1.5% MoM bounce back in airfares. Rather than services which should remain consistently strong, the pick-up in core CPI relative to the previous two months should come from goods prices. Most notably, we expect recently rising wholesale measures of used car prices to start to feed through to stronger car prices in CPI.”

CAD slips from highs versus soft USD. Economists at Scotiabank expect the USD/CAD pair to challenge 1.37 if it manages to stay below the 1.38 level.

Persistent strength above 1.38 will likely prompt a retest of 1.3850/60

“Price action Friday strongly suggested that the broader USD uptrend in place over the past month or so may be stalling. But the intraday rebound in the USD from session lows – so far – looks quite constructive on the short-term charts and underlying trend momentum remains USD-bullish.”

“If USD/CAD gains are capped around 1.38 intraday, the CAD may have a shot at pushing back towards 1.37.”

“Persistent USD strength above the figure will likely prompt a retest of 1.3850/60.”

- EUR/JPY falls off the cliff and retests the 200-day SMA near 141.80.

- The next support level emerges at the February low in the mid-139.00s.

EUR/JPY debilitates further and breaks below the 142.00 to print new 4-week lows near 141.80 at the beginning of the week.

EUR/JPY breaks below the consolidative range and challenges the key 200-day SMA, today at 141.77. A sustainable breach of the latter should open the door to extra weakness to, initially, the February low at 139.54 (February 10).

Below the 200-day SMA the outlook for the cross is expected to shift to negative.

EUR/JPY daily chart

- USD/JPY opens the week on a bearish note, with the currency pair trading at 133.50, down by 1.10% on the day.

- Despite hitting an intraday high of 134.99, USD/JPY struggles to gain as bearish market sentiment prevails.

- US CPI and BoJ Monetary Meeting Minutes are critical events to follow on Tuesday.

Intraday price movements:

USD/JPY opens the day of a new week at 134.97, dropping to an intraday low of 132.96 before hitting an intraday high of 134.99. The pair continues to struggle to gain amid bearish market sentiment, trading at 133.50 above its 50-day SMA of 132.41, down by 1.10% on the day at the press time.

There is no critical economic event on the day that may affect the price of USD/JPY on Monday, the week's first and relatively silent day.

Markets will be closely monitoring the Consumer Price Index ex Food & Energy (MoM)(Feb) released by the US Department of Labor Statistics (Tue, Mar 14th, 2023 12:30 GMT) and Bank of Japan’s (BoJ) Monetary Meeting Minutes (Tue, Mar 14th, 2023 23:50 GMT).

Technical View: