- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 26-03-2023

- US Dollar Index pares recent gains with mild losses amid cautious optimism, downbeat yields.

- Fears of US recession, challenges to hawkish Fed concerns probe DXY bulls.

- US Core PCE Price Index, risk catalysts are the key for fresh impulse.

US Dollar Index (DXY) teases sellers around 103.00, following a two-day winning streak, amid market’s consolidation during early Monday. In doing so, the greenback’s gauge versus six major currencies remain pressured after two-week downtrend as the US Treasury bond yields remain pressured.

US 10-year Treasury bond yields struggle to defend the late Friday’s corrective bounce off the lowest levels since September 2022 amid mixed concerns about the banking sector and the US Federal Reserve’s (Fed) next move. However, the dovish comments from Minneapolis Fed President Neel Kashkari and headlines surrounding Silicon Valley Bank (SVB) weigh on the US Dollar of late, mainly due to a mild rebound in the market’s sentiment.

Fed’s Kashkari said on the CBS show Face the Nation that recent stress in the banking sector and the possibility of a follow-on credit crunch brings the US closer to recession. On the other hand, headlines from Bloomberg also contributed to the risk-on mood and weighed on the US Dollar. “First Citizens BancShares Inc. is in advanced talks to acquire Silicon Valley Bank after its collapse earlier this month, according to people familiar with the matter,” said Bloomberg.

Previously, Reuters’ news about Russia allowed the US Dollar to grind higher before the latest fall. “The North Atlantic Treaty Organization (NATO) NATO on Sunday criticised Vladimir Putin for what it called his ‘dangerous and irresponsible’ nuclear rhetoric, a day after the Russian president said he planned to station tactical nuclear weapons in Belarus,” per Reuters.

It’s worth noting that mostly upbeat data and hawkish Fedspeak triggered the US Dollar’s rebound during late Friday. That said, US Durable Goods Orders for February dropped by 1.0% versus January's fall of 5% (revised from -4.5%) and the market expectation for an increase of 0.6%. Details suggested that the figure for Durable Goods Orders ex Defense and ex Transportation were also downbeat but Nondefense Capital Goods Orders ex Aircraft came in firmer-than-expected 0.0% to 0.2%, versus 0.3% prior. Moving on, the preliminary readings of the US S&P Global PMIs for March came in firmer as the Manufacturing gauge rose to 49.3 from 47.3 in February, versus 47.0 expected, while Services PMI rose to 53.8 from 50.6 prior and 50.5 expected. With this, the S&P Global's Composite PMI increased to 53.3 from 50.1 in February, versus 50.1 market forecasts.

Following the data, Atlanta Fed President Raphael Bostic told NPR that it was not an easy decision to raise the policy rate while also adding that he is not expecting the economy to fall into recession. Further, St. Louis Federal Reserve President James Bullard, a policy hawk, said on Friday that the response to the bank stress was swift and appropriate, allowing the monetary policy to focus on inflation, per Reuters. The policymaker also added that the projections suggest one more rate hike that could be at the next FOMC meeting or soon after.

Against this backdrop, S&P 500 Futures trace Wall Street’s mild closing while the US Treasury bond yields remain pressured.

Looking ahead, Fed talks and second-tier US data may entertain DXY traders ahead of the Fed’s preferred inflation gauge, namely the Core Personals Consumption Expenditure (PCE) Price Index. Should the inflation numbers print strong outcomes, the greenback has scope for recovery.

Technical analysis

A three-week-old bearish channel keeps US Dollar Index sellers hopeful unless the quote rises past 103.65 hurdle.

- NZD/USD is building a cushion near the lower end of the Rising Channel around 0.6200.

- A responsive buying for the New Zealand Dollar is highly expected as the US Dollar has shown correction.

- Fewer chances of continuation of ongoing increases by the Fed have heavily impacted US Treasury yields.

The NZD/USD pair is displaying a back-and-forth action in a narrow range of 0.6191-0.6212 continuously since Friday. The Kiwi asset has turned sideways and signs of recovery are solidifying as the US Dollar Index (DXY) has shown some correction.

The USD Index (DXY) has corrected to near 103.00 after failing to extend recovery above 103.36. S&P500 futures have generated solid gains in the morning session on hopes that more financial support to mid-size United States lenders from the Federal Reserve (Fed) would infuse confidence among investors and in households for making more deposits.

Fewer chances of continuation of ongoing increases in the interest rate by the Federal Reserve (Fed) after the banking fiasco have heavily impacted US Treasury yields. The return offered on 10-year US Treasury bonds has dropped sharply to near 3.37%. Contrary, economists at Goldman Sachs believe that the Fed will announce two more rate hikes in May and June by 25 basis points (bps).

NZD/USD is demonstrating a small inventory adjustment near the lower edge of the Rising Channel chart pattern formed on a two-hour scale. In a Rising Channel chart pattern corrective moves are considered as buying opportunities by the market participants.

The Kiwi asset is auctioning below the 20-period Exponential Moving Average (EMA) at 0.6222, which indicates that the short-term bias is still on the downside.

Meanwhile, the Relative Strength Index (RSI) (14) has slipped into the bearish range of 20.00-40.00, which also favors a downside bias.

An extension of recovery above March 07 high at 0.6223 will drive the asset toward March 13 high at 0.6265 followed by the upper end of the chart pattern around 0.6325.

On the flip side, a breakdown of March 21 low at 0.6167 will drag the asset toward March 15 low at 0.6139. A slippage below the latter will expose the asset for more downside toward the round-level support at 0.6100.

NZD/USD two-hour chart

- AUD/USD picks up bids to pare weekly losses amid sluggish markets.

- News of a deal for Silicon Valley Bank joins dovish comments from Fed’s Kashkari to lure Aussie pair buyers.

- Absence of data/events on Monday allow pair to consolidate previous fall ahead of the key inflation numbers scheduled during the week.

AUD/USD grinds near an intraday high surrounding 0.6650 amid Monday’s sluggish Asian session, portraying a mildly positive sentiment after a week of pessimism and volatility. In doing so, the Aussie pair cheers hopes of easing banking fears while also cheering news suggesting the challenges for the Federal Reserve’s (Fed) rate hikes.

That said, comments from Minneapolis Fed President Neel Kashkari on the CBS show Face the Nation seem to weigh on the US Dollar of late as the policymaker said, that recent stress in the banking sector and the possibility of a follow-on credit crunch brings the US closer to recession.

Previously, Atlanta Fed President Raphael Bostic told NPR that it was not an easy decision to raise the policy rate while also adding that he is not expecting the economy to fall into recession. "Fed has to get inflation under control,” said Fed’s Bostic. Further, St. Louis Federal Reserve President James Bullard, a policy hawk, said on Friday that the response to the bank stress was swift and appropriate, allowing the monetary policy to focus on inflation, per Reuters. The policymaker also added that the projections suggest one more rate hike that could be at the next FOMC meeting or soon after.

It’s worth noting that the headlines from Bloomberg also contributed to the risk-on mood and allowed the AUD/USD price to remain firmer after a loss-making week. “First Citizens BancShares Inc. is in advanced talks to acquire Silicon Valley Bank after its collapse earlier this month, according to people familiar with the matter,” said Bloomberg.

Talking about the data, US Durable Goods Orders for February dropped by 1.0% versus January's fall of 5% (revised from -4.5%) and the market expectation for an increase of 0.6%. Details suggested that the figure for Durable Goods Orders ex Defense and ex Transportation were also downbeat but Nondefense Capital Goods Orders ex Aircraft came in firmer-than-expected 0.0% to 0.2%, versus 0.3% prior. Moving on, the preliminary readings of the US S&P Global PMIs for March came in firmer as the Manufacturing gauge rose to 49.3 from 47.3 in February, versus 47.0 expected, while Services PMI rose to 53.8 from 50.6 prior and 50.5 expected. With this, the S&P Global's Composite PMI increased to 53.3 from 50.1 in February, versus 50.1 market forecasts.

Amid these plays, S&P 500 Futures trace Wall Street’s mild closing while the US Treasury bond yields remain pressured.

Moving on, AUD/USD traders may witness further consolidation on Monday amid a lack of major data/events. However, the cautious mood ahead of this week’s Aussie Retail Sales, monthly inflation and the Fed’s preferred inflation gauge, namely the Core Personals Consumption Expenditure (PCE) Price Index, could test the pair’s upside momentum. It’s worth noting that the Reserve Bank of Australia officials have mostly been cautious of late and hence softening the inflation signals could keep the sellers in the driver’s seat.

Technical analysis

A clear downside break of a two-week-old ascending support line, now immediate resistance near 0.6675, keeps the AUD/USD pair on the bear’s radar.

- Silver price snaps three-day uptrend on breaking a fortnight-old support line.

- Nearly overbought RSI adds strength to the pullback moves targeting 61.8% Fibonacci retracement.

- Convergence of 50-DMA, 50% Fibonacci retracement acts as an important support, XAG/USD bulls need validation from $23.50.

Silver price (XAG/USD) prints the first daily loss in four as the bright metal drops to $23.15 during early Monday in Asia. In doing so, the bright metal remains depressed after two consecutive weekly losses while justifying Friday’s downside break of a short-term key support line.

Not only a downside break of the two-week-old ascending support line, now resistance near $23.50, but the RSI (14) line’s placement near the oversold territory also teases the XAG/USD sellers.

As a result, the bright metal appears well-set to drop towards the 61.8% Fibonacci retracement level of its February-March downside, near $22.85.

However, the 50% Fibonacci retracement and the 50-DMA, around $22.30-20, could together challenge the Silver bears afterward.

It’s worth noting that the XAG/USD weakness past $22.20 makes it vulnerable to drop toward the early-month swing high of around $23.20 while the 200-DMA support of $21.00 could restrict the commodity’s further downside.

On the flip side, recovery moves remain elusive unless the quote stays beyond the previous support line, now resistance around $23.50.

Following that, multiple hurdles around $24.00 and $24.20 can test the Silver buyers before challenging the yearly high of around $24.65.

Overall, the Silver price flags the risk of further downside but the room towards the south appears limited.

Silver price: Daily chart

Trend: Pullback expected

European Central Bank (ECB) Vice President Luis de Guindos said during the weekend that the banking sector is “going through a period of very high uncertainty” that dictates a meeting-by-meeting approach on interest rate policy, per an interview posted on the ECB website.

More comments

Appropriate not to pre-commit to outcomes of monetary policy meetings.

The question now is how the events in the US banking system and Credit Suisse will impact the euro-area economy.

Over the next weeks and months, we need to assess whether they will give rise to an additional tightening of financing conditions.

EUR/USD grinds higher

EUR/USD struggles to justify the news amid mixed concerns, making rounds to 1.0780-90 during early Monday.

Also read: EUR/USD eases below 1.0800 despite hawkish ECB talks, EU/US inflation cues eyed

- USD/CHF is aiming to reclaim the 0.9200 resistance amid a firm recovery by the USD Index.

- Expansion of financial support to US lenders and upbeat US PMI strengthened the US Dollar appeal.

- The SNB is ready to tighten monetary policy further if inflation continues to remain persistent.

The USD/CHF pair is aiming to recapture the immediate resistance of 0.9200 in the early Asian session. The Swiss franc asset is being supported by a recovery in the US Dollar Index (DXY). Easing United States banking fears and solid preliminary US Global PMI (March) bolstered confidence for the USD Index last week.

Bloomberg reported on Saturday the U.S. authorities are considering the expansion of an emergency lending facility that would offer banks more support, in an effort that could give First Republic Bank more time to shore up its balance sheet. The expression of further support to lenders to dodge vulnerable times infuses confidence among investors.

S&P500 futures ended the week on a promising note as more support to lenders would also result in more deposits to mid-size US banks, which have dropped firmly after their debacle, portraying an improvement in investors’ risk appetite.

Reuters reported on Friday that the data from Federal Reserve (Fed) shows that deposits at small U.S. banks dropped by a record amount following the collapse of Silicon Valley Bank (SVB). Now wider blanket of support to US mid-size banks might provide support to US mid-side banks in the longer term.

The US Dollar Index (DXY) was supported by solid S&P Global PMI data. Manufacturing PMI is still in the declining phase as a figure below 50.0 is considered as contracting. Although the figure rebounded firmly to 49.3 from the consensus of 47.0. Also, Services PMI accelerated to 53.8 against the estimates of 50.5 and the prior release of 50.6.

On the Swiss franc front, an interest rate hike by 50 basis points (bps) by the Swiss National Bank (SNB) to tackle galloping inflation has trimmed Fed-SNB rate divergence. SNB Chairman Thomas J. Jordan cited that the central bank is ready to hike rates further if inflation continues to remain persistent.

- USDJPY rebounds from 129.50 after US authorities intervene to stabilize the market.

- Deutsche Bank's credit default swap surges, sparking investor panic and risk.

- Fed's Bullard and Barkin emphasize the need to tackle inflation despite financial stability concerns.

The USDJPY experienced a significant rebound from the 129.50 level after US authorities intervened to address market challenges stemming from rising credit default swaps among various banks. On Wednesday, the Federal Reserve (Fed) implemented a 25-basis point rate hike, and Fed Chair Jerome Powell reassured the market that all necessary steps would be taken to alleviate the liquidity crisis in the banking sector.

However, panic ensued as Deutsche Bank's credit default swap began to surge, leading to investor unease and increased risk in the market.

On Friday, Fed's Bullard emphasized the importance of reducing inflation despite current financial stability concerns. He acknowledged that the Committee could use macroprudential policy to mitigate financial distress if necessary. Fed's Barkin shared a similar view, noting tight labor markets and high inflation, and agreed that this week's rate hikes were justified.

In economic data, February's US Durable Goods experienced a 1.0% decline, contrary to the anticipated 0.6% increase. The US S&P Global Flash PMI for March exceeded expectations for both Manufacturing and Services, pushing the Composite Index to 53.3 from 50.1. Manufacturing remains in contraction, while services continue to expand.

Market focus now shifts to the upcoming US Personal Consumption Expenditures Price Index (PCE), Personal Income, and Spending data for Friday. Core PCE is expected to rise by 0.4% MoM in February, slower than January's 0.6% increase. The annual rate of core PCE is predicted to moderate to 4.3% YoY from 4.7%. US Personal Income is anticipated to increase by 0.3% MoM in February, slowing down compared to the 0.6% MoM growth in January. Personal Spending is also expected to rise by 0.3% MoM, a more moderate pace compared to the previous 1.8% increase.

Developments in the global banking sector will be crucial to monitor, as they may significantly impact market sentiment and trends. The efforts made by the Fed and other authorities to stabilize financial markets and address inflation concerns will play a key role in shaping future economic conditions.

Levels to watch

Riksbank Governor Erik Thedeen said on Sunday, “The Swedish central bank might have underestimated inflationary pressure and will likely have to stick to its forecasts of another interest rate hike in April,” per Reuters.

“It could be that the inflation process is worse than we thought,” Riksbank Governor told SVT television.

Additional comments

The main scenario remained a hike of 25 or 50 basis points in April and added that inflation outcomes since the monetary policy decision in February had been worse than expected.

It is in our forecasts that inflation will come down quite quickly. The problem is that it has been in our forecasts all through 2022 and it has yet to happen.

Market implications

The news can weigh on the USD/KRW price that grinds higher of late around 1,296 during early Monday. It’s worth noting that the Riksbank will announce its next monetary policy decision on April 26.

- GBP/USD picks up bids to refresh intraday high after two-week uptrend.

- Fears of US recession underpin latest fall of the greenback amid downbeat yields.

- Hopes of more soothing economic measures for the UK energy companies from PM Sunak help Cable buyers.

- Speech from BoE Governor Bailey, US Core PCE Price Index eyed.

GBP/USD begins the week on a positive footing, renewing its intraday high near 1.2250 while extending the previous two-week uptrend, as fears of US recession join positive headlines from the UK. However, the cautious mood ahead of this week’s key data/events seems to test the Cable pair buyers.

That said, the quote managed to cheer the Bank of England’s (BoE) 0.50% rate hike with mostly positive economics, as well as the downbeat US Treasury bond yields. However, Friday’s risk-negative headlines tested the GBP/USD buyers before the latest run-up, backed by the weekend news.

During the weekend, Minneapolis Fed President Neel Kashkari said on the CBS show Face the Nation that recent stress in the banking sector and the possibility of a follow-on credit crunch brings the US closer to recession. His comments joined the Financial Times (FT) headlines suggesting more relief to the UK’s energy companies to favor the GBP/USD prices. “Britain’s oil and gas companies are next week expected to be offered the prospect of windfall tax relief, as prime minister Rishi Sunak looks to boost investment and improve the country’s energy security,” said FT.

Previously, UK Retail Sales offered an upside surprise for February by marking 1.2% MoM growth versus 0.2% expected and 0.9% previous. Further, the Core Retail Sales, which excludes the auto motor fuel sales, rose 1.5% MoM compared to 0.1% market forecasts and 0.9% previous. It’s worth noting, however, that the UK’s preliminary S&P Global/CIPS Services PMI for March came in at 52.8 compared to February’s 53.5 final print and 53.0 expected. On the same line, the first readings of Manufacturing PMI dropped to 48.0 for the said month compared to 49.8 expected and February’s 49.3 final readout. With this, the Composite PMI eased to 52.2 versus 52.8 market forecasts and 53.1 previous readings.

Following the mixed UK data, Bank of England (BoE) Governor Andrew Bailey spke during a BBC interview while saying, “There is evidence of encouraging progress on inflation, we have to be vigilant.” The policymaker also added that the risk of recession this year has gone down quite a lot. Further, BoE Monetary Policy Committee (MPC) member Catherine Mann said on Friday that she voted for a 25 basis point (bp) rate hike instead of a bigger increase, motivated in part by the fact that inflation expectations began to moderate, reflecting that monetary policy is having an effect.

On the other hand, US Durable Goods Orders for February dropped by 1.0% versus January's fall of 5% (revised from -4.5%) and the market expectation for an increase of 0.6%. Details suggested that the figure for Durable Goods Orders ex Defense and ex Transportation were also downbeat but Nondefense Capital Goods Orders ex Aircraft came in firmer-than-expected 0.0% to 0.2%, versus 0.3% prior. Moving on, the preliminary readings of the US S&P Global PMIs for March came in firmer as the Manufacturing gauge rose to 49.3 from 47.3 in February, versus 47.0 expected, while Services PMI rose to 53.8 from 50.6 prior and 50.5 expected. With this, the S&P Global's Composite PMI increased to 53.3 from 50.1 in February, versus 50.1 market forecasts.

Following the data, Atlanta Fed President Raphael Bostic told NPR that it was not an easy decision to raise the policy rate while also adding that he is not expecting the economy to fall into recession. "Fed has to get inflation under control,” said Fed’s Bostic. Further, St. Louis Federal Reserve President James Bullard, a policy hawk, said on Friday that the response to the bank stress was swift and appropriate, allowing the monetary policy to focus on inflation, per Reuters. The policymaker also added that the projections suggest one more rate hike that could be at the next FOMC meeting or soon after.

Elsewhere, the fears of Russia’s nuclear usage in its war with Ukraine and political chaos surrounding Brexit probes the GBP/USD bulls.

Looking ahead, a speech from BoE Governor Bailey can entertain intraday traders of the GBP/USD pair but major attention will be given to the Fed’s preferred inflation gauge, namely the Core Personals Consumption Expenditure (PCE) Price Index.

Technical analysis

Unless rising back beyond the previous support line from early March, around 1.2325 by the press time, GBP/USD remains vulnerable to retesting the 50-DMA support around 1.2150.

- USD/CAD is gauging an intermediate cushion near 1.3700 as USD Index looks firm.

- A recovery in retail demand could force the BoC to resume hiking rates again.

- The upside bias for the loonie asset is still solid as it is holding auction above the downward-sloping trendline from 1.3862.

The USD/CAD pair is looking for an intermediate cushion around 1.3700 in the early Tokyo session. The Loonie asset is juggling in a narrow range below 1.3740 following the footprints of the US Dollar index (DXY). The major slipped firmly on late Friday after the release of a jump in the Canadian Retail Sales data.

Monthly Canadian Retail Sales (Feb) jumped to 1.4%, higher than the consensus of 0.7%, and a flat performance was observed earlier. A recovery in retail demand could force the Bank of Canada (BoC) to resume hiking rates again.

The US Dollar Index (DXY) extended its recovery above 103.00 after S&P Global reported upbeat preliminary PMI (March) data. Manufacturing and Services PMI recovered to 49.3 and 53.8 respectively. Although a figure below 50.0 is still considered as a contraction for an economic indicator.

On an hourly scale, USD/CAD has corrected to near the demand zone placed in a narrow range of 1.3737-1.3746. The upside bias for the loonie asset is still solid as it is holding auction above the downward-sloping trendline plotted from March 10 high at 1.3862.

Also, the major is still above the 50-period Exponential Moving Average (EMA) at 1.3727, which indicates that the short-term upside bias has not faded yet.

The Relative Strength Index (RSI) (14) has slipped below 60.00 but is likely to find support around 40.00 initially.

A confident recovery above March 14 high at 1.3773 would drive the major toward March 09 high at 1.3835 and the round-level resistance at 1.3900.

In an alternate scenario, a decisive breakdown of March 14 low at 1.3652 would drag the loonie asset toward March 07 low at 1.3600, followed by March 03 low at 1.3555.

USD/CAD hourly chart

Reserve Bank of New Zealand (RBNZ) said on Monday that the capital ratios of the country's banks will remain resilient during most severe weather events though more studies were needed to understand how they could potentially compound with other risks to the financial system, per Reuters.

"As flood risk increases, the financial system is likely to face simultaneously a broader range of climate-related risks," the Reserve Bank of New Zealand (RBNZ) Deputy Governor Christian Hawkesby said in a statement per Reuters.

RBNZ’s Hawksby also said, “RBNZ's climate stress test, due out later this year, will help identify the combination of these risks to the balance sheets of banks.”

Markets remain resilient

NZD/USD struggles for clear direction near 0.6200 during early Monday, following a positive weekly close.

- Gold price has shifted its business below $1,980.00 after solid preliminary US PMI data.

- Solid PMI numbers could force the Fed to continue to hike rates further.

- Fed Kashkari cited recent stress in the banking sector could bring the US closer to recession.

Gold price (XAU/USD) has shifted its auction below $1,980.00 in the early Asian session. The precious metal is not showing any signs of a rebound, therefore, more downside is anticipated further. Bearish bets for Gold price soared after S&P Global reported upbeat preliminary United States PMI figures (March) on Friday. Manufacturing PMI jumped to 49.3 vs. the consensus of 47.0 and the former release of 47.3. While Services PMI accelerated to 53.8 against the estimates of 50.5 and the prior release of 50.6.

A vertical jump in the overall economic activities indicates that overall demand is robust and the road ahead for pushing US inflation lower would be full of challenges for the Federal Reserve (Fed). Last week, Fed chair Jerome Powell hinted that few rates are in pipeline now to avoid a banking crisis. And now solid PMI numbers could force the Fed to continue to hike rates further.

Meanwhile, Minneapolis Fed president Neel Kashkari cited on Sunday, “Recent stress in the banking sector and the possibility of a follow-on credit crunch brings the US closer to recession. It definitely brings us closer." It would be a tough call from the Fed to bring more interest rates if recession fears are potential.

Meanwhile, the US Dollar Index (DXY) is juggling in a narrow range below 103.20 after a solid recovery. The USD Index is looking to add gains further despite potential fears of further banking turmoil. S&P500 futures settled on a positive note last week despite sheer volatility inspired by the Fed policy. The impact of dovish interest rate guidance by the Fed was witnessed in US Treasury yields. The 10-year US Treasury yields dropped to 3.37%.

Gold technical analysis

Gold price has shown a break of higher highs and higher lows structure below $1,982.70 after forming a Double Top chart pattern on an hourly scale. The chart pattern indicates a re-test of prior highs with less buying interest, which allows aggressive selling interest to penetrate. The asset has slipped below the 20-period Exponential Moving Average (EMA) at $1,985.00, which indicates that the short-term trend is bearish now.

Meanwhile, the Relative Strength Index (RSI) (14) is defending the 40.00 cushion. A break below the same would drag Gold price further as a bearish momentum will get triggered.

Gold hourly chart

- EUR/USD fades late Friday’s corrective bounce amid sour sentiment.

- Headlines surrounding banking sector, nuclear fears from Russia weigh on risk appetite.

- Mostly upbeat EU data, hawkish ECB talks previously allowed Euro to pare some losses.

- Inflation numbers from EU/Germany, US Core PCE Price Index will be crucial to watch for fresh impulse.

EUR/USD retreats towards 1.0750 as it consolidates the previous weekly gains amid a cautious mood in the market ahead of the key inflation data from Europe and the US. That said, the Euro pair eases from its intraday high to 1.0765 during early Monday in Asia while fading the late Friday’s corrective bounce.

Fears of more banking sector fallout and Russia’s likely usage of nuclear weapons in its war with Ukraine join the hawkish central bank talks to challenge the risk profile. It’s worth noting, however, that the US Dollar managed to pare some of its latest losses despite the downbeat Treasury bond yields. The recent rebound in the greenback could be linked to the slightly positive US data and hopes of faster rate hikes by the Federal Reserve (Fed). However, the hawkish tone of the European Central Bank officials and an absence of disappointing numbers from the bloc allowed the EUR/USD pair to post weekly gains in the last.

The North Atlantic Treaty Organization (NATO) NATO on Sunday criticised Vladimir Putin for what it called his "dangerous and irresponsible" nuclear rhetoric, a day after the Russian president said he planned to station tactical nuclear weapons in Belarus, per Reuters.

Elsewhere, the preliminary readings of Eurozone S&P Global PMIs for March showed that the Manufacturing gauge arrived at 47.1 versus 49.0 expected and 48.5 prior but the Services PMI rose to a fresh 10-month high of 55.6 while rising from 52.7 prior and 52.5 expected. As a result, the Composite PMI also rose to a 10-month top of 54.1 versus 51.9 market forecasts and 52.0 previous readings.

On the same line were the first readings of Germany’s S&P Global/BME PMIs for March as the Manufacturing gauge dropped to a two-month low of 44.4 versus 47.0 expected and 46.3 prior but the Services PMI rose to 53.9 during the stated month from 50.9 prior and 51.1 expected. Further, the Composite PMI refreshed a 10-month high with the 52.6 figure for March versus 51.0 expected and February’s 50.7.

On the other hand, US Durable Goods Orders for February dropped by 1.0% versus January's fall of 5% (revised from -4.5%) and the market expectation for an increase of 0.6%. Details suggested that the figure for Durable Goods Orders ex Defense and ex Transportation were also downbeat but Nondefense Capital Goods Orders ex Aircraft came in firmer-than-expected 0.0% to 0.2%, versus 0.3% prior.

Further, the preliminary readings of the US S&P Global PMIs for March came in firmer as the Manufacturing gauge rose to 49.3 from 47.3 in February, versus 47.0 expected, while Services PMI rose to 53.8 from 50.6 prior and 50.5 expected. With this, the S&P Global's Composite PMI increased to 53.3 from 50.1 in February, versus 50.1 market forecasts.

Talking about the central bankers’ comments, On Friday, Atlanta Fed President Raphael Bostic told NPR that it was not an easy decision to raise the policy rate while also adding that he is not expecting the economy to fall into recession. "Fed has to get inflation under control,” said Fed’s Bostic.

Further, St. Louis Federal Reserve President James Bullard, a policy hawk, said on Friday that the response to the bank stress was swift and appropriate, allowing the monetary policy to focus on inflation, per Reuters. The policymaker also added that the projections suggest one more rate hike that could be at the next FOMC meeting or soon after. It should be noted that the latest comments from Minneapolis Fed President Neel Kashkari seem to weigh on the US Dollar as he said during CBS show Face the Nation that recent stress in the banking sector and the possibility of a follow-on credit crunch brings the US closer to recession.

In the case of the ECB officials, ECB President Christine Lagarde told EU leaders on Friday that the Euro area banking sector is resilient with strong capital and liquidity positions, Reuters reported citing EU officials. “ECB is determined to bring back inflation to 2%, will decide on future rates based on incoming data,” added ECB’s Lagarde. On the same line was Eurogroup President Paschal Donohoe who said that European banks have enough capital and liquidity. Further, ECB policymaker Joachim Nagel said on Friday, “It will be necessary to raise policy rates to sufficiently restrictive levels in order to bring inflation back down to 2% in a timely manner.” During the weekend, ECB Board Member Isabel Schnabel said that while headline inflation has begun falling, the core is sticky.

Amid these plays, Wall Street closed with mild gains after late Friday’s losses while the yields bounce off weekly lows.

Looking ahead, IFO numbers for Germany will join the comments from the ECB and the Fed officials to direct the EUR/USD pair’s intraday moves. However, major attention will be given to the inflation data from Germany and Europe. On the other hand, the Fed’s preferred inflation gauge, namely the Core Personals Consumption Expenditure (PCE) Price Index, will be important to track for clear direction.

Technical analysis

Although a downside break of a short-term support line, now resistance around 1.0855, teases EUR/USD bears, the 50-DMA support around 1.0725 challenges the quote’s further downside.

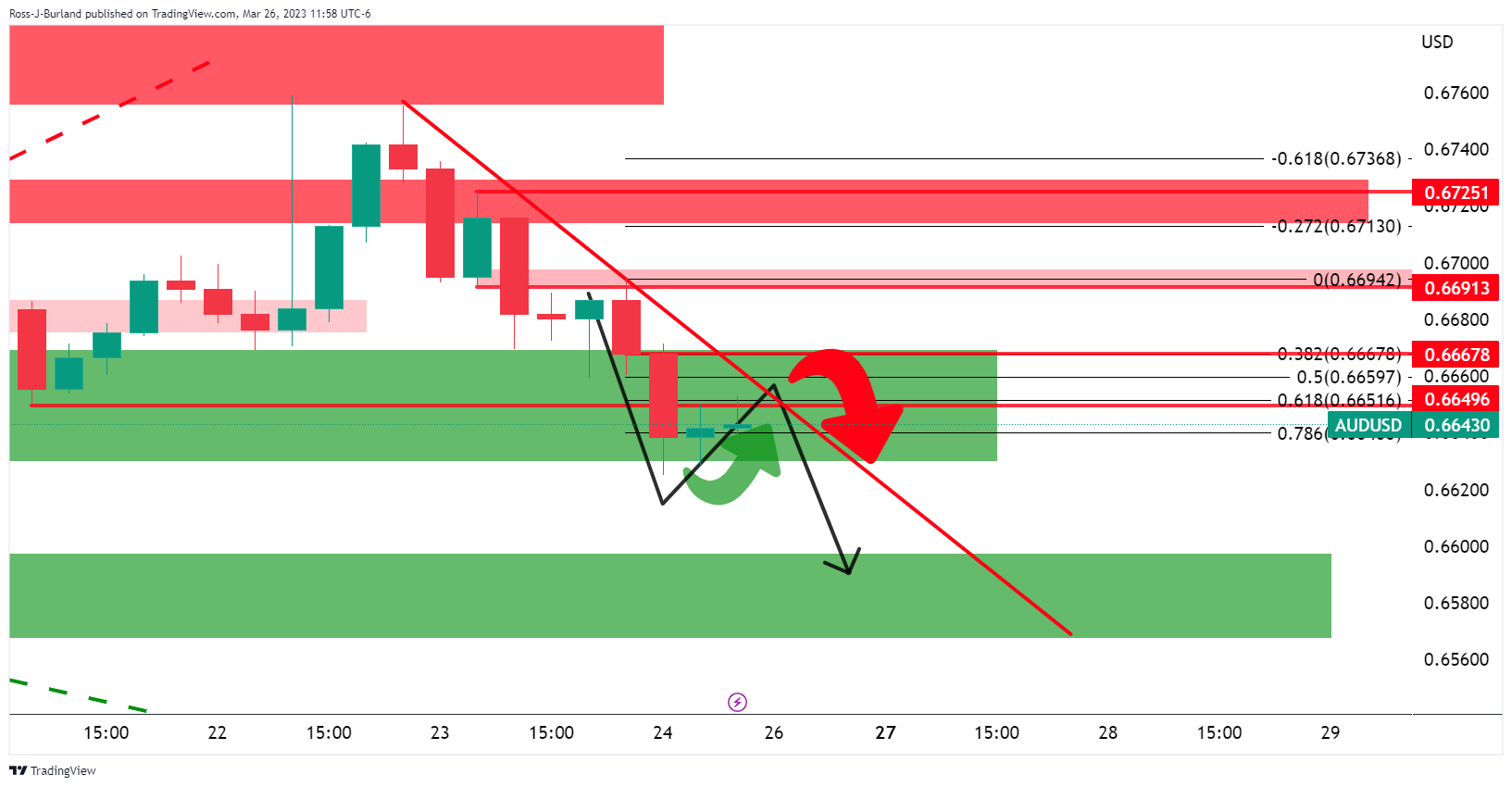

- AUD/USD is on the front side of the bear trend, potentially leading to a bearish start to the week.

- AUD/USD bears lurking below the Fibo scale.

As per the prior analysis, AUD/USD Price Analysis: Bears in the market, chipping away into key support, where the focus was on the downside, we have indeed seen a deeper move into support.

AUD/USD prior support

There is an emphasis on the downside for the meanwhile on the lower time frames:

Zoomed in, we could see that AUD/USD had left an M-formation on the 4-hour chart. A correction into the neckline would meet a 38.2% Fibonacci of the prior bearish leg.

Either way, below there, the bias was to the downside for a deeper test into the support area. 0.6725 is an upside resistance that guards a continuation higher subsequent of the bullish breakout.

AUD/USD update

The price action followed the forecasted trajectory as illustrated above.

With the recent break of the structure of 0.6650, there is a bias to the downside still while on the front side of the bear trendline.

The European Union´s foreign minister Josep Borrell said that Belarus hosting Russian nuclear weapons would mean an irresponsible escalation and a threat to European security.

He said Belarus can still stop it, it is their choice but the EU stands ready to respond with further sanctions.

-

Putin: Russia plans to station tactical nuclear weapons in Belarus

Reuters reported that Minneapolis Fed president Neel Kashkari was speaking on Sunday in comments to CBS show Face the Nation.

´´Recent stress in the banking sector and the possibility of a follow-on credit crunch brings the US closer to recession. It definitely brings us closer," Kashkari said.

"What's unclear for us is how much of these banking stresses are leading to a widespread credit crunch. That credit crunch ... would then slow down the economy. This is something we are monitoring very, very closely."

US Dollar update

The US Dollar rose on Friday as banking stocks plunged in Europe with heavyweights Deutsche Bank and UBS Group pummelled by worries that the worst problems to hit the sector since the 2008 financial crisis have not yet been contained. The dollar index, or DXY, rose 0.51% ands printed a high at 103.350,

Isabel Schnabel, Member of the ECB's Executive Board, crossed the wires and has said headline inflation has begun to decrease although said core inflation remains sticky.

She added that energy contributions are declining quickly yet financial turbulence has notable effects on markets.

EUR/USD update

The euro fell sharply against a strengthening US Dollar on Friday amid lingering nervousness over banks.

Banking stocks plunged in Europe with heavyweights Deutsche Bank and UBS Group pummelled by worries that the worst problems to hit the sector since the 2008 financial crisis have not yet been contained. EUR/USD was down 0.71% to 1.0753.

´´With so much tension gathering in the banking sector we are reluctant to alter our call that the USD may yet see further strength in the coming weeks on the back of safe haven demand,´´ analysts at Rabobank argued. ´´We still forecast at EUR/USD1.05 in 3 months, though we have tweaked our 6 to 12 mth EUR/USD forecasts.´´

President Vladimir Putin said Saturday that Russia plans to station tactical nuclear weapons in neighboring Belarus.

A special storage facility for tactical nuclear weapons in Belarus is to be built and installed by the beginning of July, Putin told state broadcaster Russia 1.

Putin said Russia had helped Belarus convert 10 aircraft to make them capable of carrying tactical nuclear warheads and would start training pilots to fly the re-configured planes early next month.

Putin said that the placement of nuclear weapons in Belarus will not violate nuclear non-proliferation accords.

´´We're not transferring our nuclear weapons to Belarus but will station them there, like the US does in Europe.´´

´´We have found no reason to change our own strategic nuclear posture, nor have we seen any signals that Russia is planning to use a nuclear weapon,´´ the US Department of Defense said in a statement.

In prior communications, Washington made clear to Putin that there will be consequences to any use of nuclear weapons in Ukraine.

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers