- Analiza

- Novosti i instrumenti

- Vesti sa tržišta

Forex-novosti i prognoze od 17-08-2022

- AUD/USD remains pressured around weekly low after breaking one-month-old bullish channel to the south.

- Sour sentiment, China-linked fears and downbeat Aussie Wage Price Index have already put a floor for bears.

- Fed Minutes failed to impress USD bears amid recession woes.

- Australia employment numbers for July, and second-tier US data will be important for fresh impulse.

AUD/USD holds lower grounds near 0.6930, after falling to the weekly low, as traders await Australia’s monthly employment data during Thursday’s Asian session. In doing so, the Aussie pair portrays the market’s risk-off mood, as well as justifies the previous day’s downbeat wage numbers.

Market sentiment soured after the US 10-year Treasury yields rose the most in a week while refreshing the monthly high near 2.90%. In doing so, the benchmark bond coupons ignored downbeat Federal Open Market Committee (FOMC) meeting Minutes, while also ignoring risk-positive news from China Securities.

The Fed Minutes stated that the policymakers strongly supported the 75 bps rate increase in August while seeing a slowing pace of hikes at some point. The Minutes also signaled that Fed officials saw the hazard the Fed could tighten more than necessary.

On the other hand, “China may issue 1.5trln yuan in additional debt as part of an investment push,” mentioned china securities news.

It should be noted that the softer-than-expected Aussie Wage Price Index for the second quarter (Q2) also exerted downside pressure on the AUD/USD prices the previous day. That said, Aussie wages grew 0.7% QoQ in Q2 to mark the faster pace of growth since September 2014. However, the figures remain dismal when compared to the inflation data and the Reserve Bank of Australia’s (RBA) economic fears.

In the case of the US, Retail Sales flashed 0.0% growth during July, versus 0.1% expected and a downwardly revised 0.8% prior. The Retail Sales Control Group figures, however, rose to 0.8% compared to 0.6% market consensus and 0.7% prior (revised from 0.8%).

Following the mixed data and Fed Minutes, Federal Reserve Governor Michelle Bowman mentioned, “High inflation and strong employment will likely create some pressure on labor and employment.”

Moving on, AUD/USD traders should pay close attention to the Aussie jobs report for July amid recent challenges for the Reserve Bank of Australia’s (RBA) further rate hikes. That said, the headline Employment Change is likely to register 25K figure versus 88.4K prior while the Unemployment Rate is expected to remain unchanged at 3.5%. Following that, the weekly prints of the US Initial Jobless Claims and Philadelphia Fed Manufacturing Survey for August could entertain the pair traders.

Also read: Australian Employment Preview: No surprises on solid job creation

Technical analysis

A clear downside break of the one-month-old bullish channel, directs AUD/USD prices towards the yearly low of 0.6678. However, 50-DMA and May’s low, respectively around 0.6900 and 0.6825, could act as buffers to the south. Meanwhile, recovery remains elusive until the quote stays below the 200-DMA level around 0.7120.

- NZD/USD remains under pressure despite a phase of consolidaiton.

- The bulls are making hard work of a bid through 0.6300.

NZD/USD is trading at 0.6276 and flat for the day having ranged between 0.6274 and 0.6282 so far following some comments from the Reserve Bank of New Zealand's governor, Adrian Orr.

Reserve Bank of New Zealand Governor Adrian Orr answered questions from members of the New Zealand parliamentary Finance and Expenditure Committee. He said that the central bank was confident domestic inflation was now tracking lower.

"We are at the low end globally and we are tracking in the right direction."

On Wednesday, the RBNZ increased the cash rate by 50 basis points to 3.0% as it seeks to get inflation under control. New Zealand inflation is currently at three-decade highs having hit 7.3% in the second quarter.

Nevertheless, as analysts at ANZ Bank noted, ''FX markets have been quick to move on from local themes in favour of global ones. That’s been the case over the past 24hrs. So, we’re back to watching what’s happening offshore, which is mixed, with stocks lower but bond yields higher after a double-digit UK Consumer Price Index print.''

Meanwhile, the release of the Federal Open Market Committee (FOMC) policy decision that took place over the July 26-27 policy meeting sparked a little bit of a flurry in the markets, albeit short-lived.

''The post-minutes reaction was likely driven by 'many FOMC members' flagging that 'it likely would become appropriate at some point to slow the pace of policy rate increases while assessing the effects of cumulative policy adjustments on economic activity and inflation,'''analysts at TD Securities explained.

''This suggested to investors that the pace of rate hikes should slow, which pushed the pricing for a 75bp hike in September from 58% prior to the minutes to 47% and the terminal rate to 3.69% from 3.73% prior to the minutes,'' analysts added.

As a consequence, the DXY dropped 37 points to 106.385. The 10-year yield was under pressure, dropping 0.8% to 2.888% and well off the 2.919% highs for the day. The 2-year yield dropped by nearly 1.4%. This all enabled the Aussie to rally initially, however, as analysts at TD Securities argued, who believe the dovish reaction to the dated minutes may be unwarranted, ''markets should be taking their cue from hawkish Fed rhetoric in recent weeks rather than the minutes.''

- GBP/USD holds lower grounds after a volatile day that ended on a negative note.

- UK’s 40-year high inflation propelled recession woes, yields.

- Hopes of BOE’s aggression fail to impress buyers.

- Second-tier US data can entertain traders ahead of UK Retail Sales for July.

GBP/USD bears flex muscles around 1.0250, after retaking control following a brief bounce after the Fed Minutes. That said, the cable pair’s inaction could be attributed to the lack of major data/events during Thursday’s initial Asian session. It’s worth noting that the quote poked weekly top after the UK inflation data but failed to remain firmer amid fears that higher price pressure could lead to recession.

The Federal Open Market Committee (FOMC) meeting Minutes mentioned that the policymakers strongly supported the 75 bps rate increase in August while seeing a slowing pace of hikes at some point. The Minutes also signaled that Fed officials saw the hazard the Fed could tighten more than necessary.

On the other hand, fears of economic slowdown escalated after the UK inflation jumped to a 40-year high. The economic fears fuelled the rush towards risk safety, which in turn fuelled the UK 2-year Treasury yields to the highest since October 2008.

It should be noted that the firmer inflation also pushes the Bank of England (BOE) towards faster rate hikes but the market’s lack of confidence over the “Old Lady”, as it is informally called, seem to exert downside pressure on the GBP/USD prices. “The potential loss of independence by the BoE could also hurt sterling with Foreign Secretary Liz Truss, poll leader in the Tory leadership contest promising to review the BoE's remit,” said Reuters.

That said, UK Consumer Price Index (CPI) rose to 10.1% YoY in July versus 9.8% expected and 9.4% previous readings while the Core CPI, which excludes volatile food and energy items, rose to 6.2% versus 5.9% market consensus and 5.8% previous readouts.

Elsewhere, US Retail Sales flashed 0.0% growth during July, versus 0.1% expected and a downwardly revised 0.8% prior. The Retail Sales Control Group figures, however, rose to 0.8% compared to 0.6% market consensus and 0.7% prior (revised from 0.8%).

The firmer US data and the Fed Minutes’ inability to please bears seem to have helped Federal Reserve Governor Michelle Bowman to mention, per Reuters, “High inflation and strong employment will likely create some pressure on labor and employment.”

Amid these plays, the US 10-year Treasury yields rose the most in a week while refreshing the monthly high near 2.90%, which in turn weighed on the Wall Street benchmarks and helped the US dollar to reverse the fall marked after the Federal Open Market Committee (FOMC) meeting minutes.

Given the fears of economic slowdown in the UK, GBP/USD is likely to remain pressured ahead of Friday’s Retail Sales for July, the key component of the British Gross Domestic Product (GDP), expected -3.3% YoY versus -5.8% prior.

Technical analysis

GBP/USD remains on the way to June’s low around 1.1930 unless crossing a two-month-ols downward sloping resistance line, at 1.2260 at the press time. It’s worth noting that the 21-DMA and 100-DMA, respectively near 1.2110 and 1.2385, are extra filters to the north.

- The AUD/JPY moderately advances as the Asian session begins.

- From a daily chart perspective, the pair is neutral biased, but the 4-hour chart portrays an upward bias.

- AUD/JPY Price Analysis: Break above 94.47 clears the way toward 96.00; otherwise, it could fall to 93.00.

The AUD/JPY crept lower on Wednesday session spurred by a risk-off impulse on worries of China’s economic slowdown. In the meantime, US Retail Sales showed consumers resilience, while “dovish” FOMC minutes put into play a possible Fed “put” in the scene. At the time of writing, the AUD/JPY is trading at 93.67.

AUD/JPY Price Analysis: Technical outlook

The AUD/JPY is in a consolidation phase, unable to crack the top/bottom of the 93.08-94.47 range for the last few days. It is worth noting that the 20, 50, and 100-day EMAs hover around that area, while the Relative Strength Index (RSI) at 48.98 is almost flat. Therefore, the AUD/JPY is neutral biased.

In the near term, the AUD/JPY 4-hour chart illustrates the cross-currency pair as upward biased, trading within the boundaries of an ascending channel. AUD/JPY buyers reclaimed the 200-EMA and reached a daily high at 94.47 on Wednesday. However, solid resistance at the 20-EMA, sliding towards the confluence of the 100 and 200-EMAs, around 93.65-68. If AUD/JPY sellers clear the latter, then a fall towards the confluence of the S1 daily pivot and the bottom of the ascending channel, around 93.50-60, is on the cards.

If that scenario plays out, the AUD/JPY’s next support will be the August 15 low at 93.07. Once cleared, it will expose the August 4 low at 92.25 and 92.00. However, if AUD/JPY buyers remain in control, a break above the August 17 high at 94.47 to open the door for further gains. Hence, the first resistance would be the top of descending channel at 94.97. Once cleared, the next supply zone will be the July 27 daily high at 95.69, followed by the 96.00 figure.

AUD/JPY 4-hour chart

AUD/JPY 4-hour chart

AUD/JPY Key Technical Levels

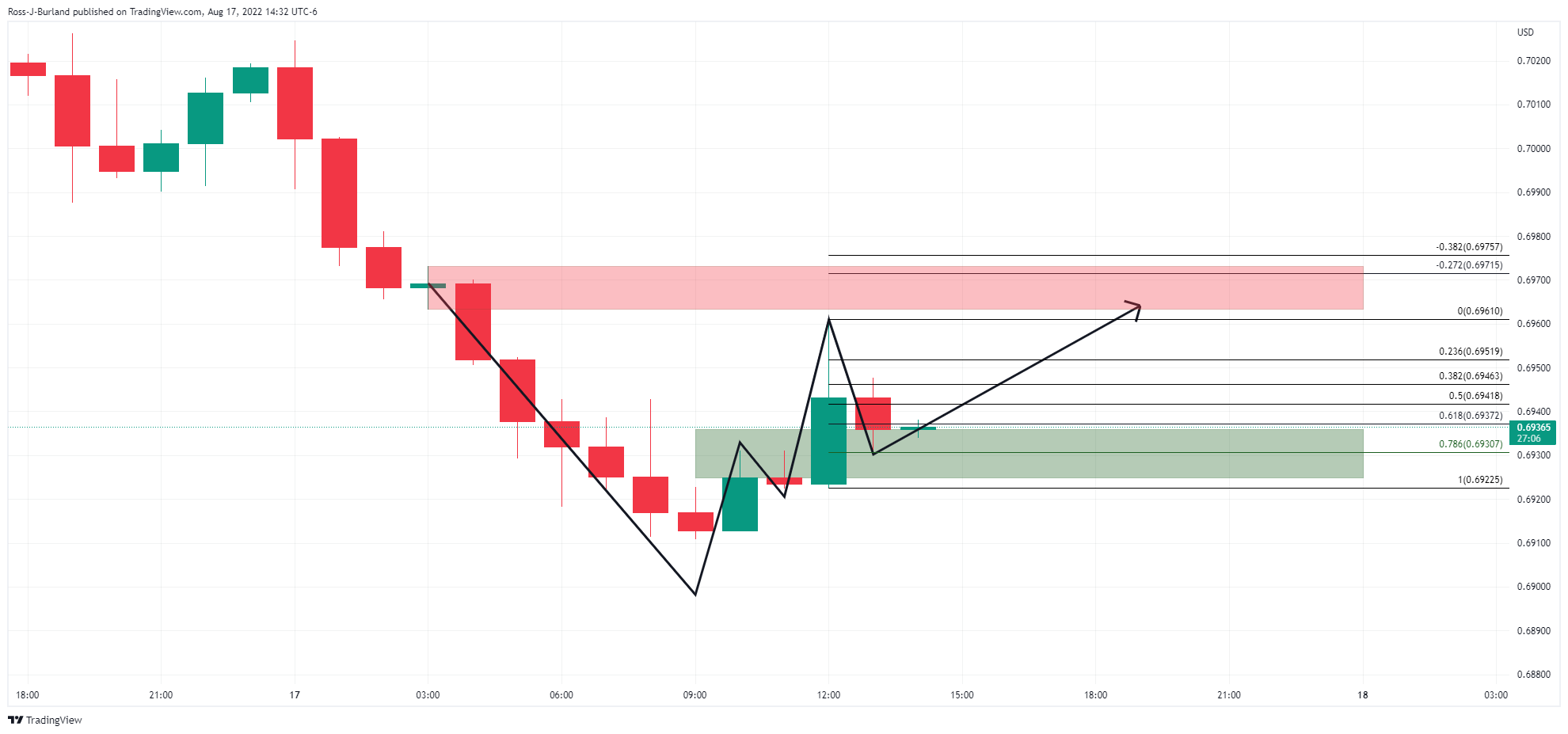

- EUR/USD struggles to extend corrective pullback from monthly low.

- Three-week-old support line restricts immediate downside amid steady RSI.

- Previous support line, 50-DMA adds to the upside filters.

- MACD teases bear cross, buyers to remain cautious below 1.0370.

EUR/USD recovery remains sluggish at around 1.0180 as bulls approach the short-term key hurdles during Thursday’s Asian session. Even so, steady RSI and an upward sloping support line from late July challenge the bears.

That said, an impending bear cross on the MACD, as well as the 21-DMA surrounding 1.0210 questions the major currency pair’s immediate upside.

Following that, the support-turned-resistance from mid-July and the 50-DMA, respectively near 1.0260 and 1.0290, will act as extra hurdles for the EUR/USD bulls to cross.

It’s worth noting that the pair buyers remain unconvinced below the upward sloping resistance line from mid-May, around 1.0370 by the press time.

Alternatively, pullback moves need to break the aforementioned support line from July 27, close to 1.0165 at the latest, to recall the EUR/USD bears.

In that case, the south-run could quickly poke the 1.0100 and parity levels before challenging the yearly bottom surrounding 0.9950.

Overall, the EUR/USD pair’s run-up remains elusive even as the bears are likely losing their grip of late.

EUR/USD: Daily chart

-637963736779472434.png)

Trend: Limited upside expected

- Gold remains pressured around two-week low, down for the fourth consecutive day.

- Fed Minutes signalled policymakers’ support for restrictive rates despite suggesting a retreat from faster rate hike before long.

- US data, economic fears added to the market’s favor for the US dollar, weighing on XAU/USD.

Gold price (XAU/USD) remains on the back foot around a two-week low, taking rounds to $,1761 at the start of Thursday’s Asian session. The precious metal’s latest inaction could be linked to a lack of major data/events. However, mixed US data and rejection of Fed Minutes, after a brief dovish play, join the broad pessimism surrounding the US economy and Fed moves to weigh on the XAU/USD prices, not to forget strong yields and geopolitical fears.

US 10-year Treasury yields rose the most in a week while refreshing the monthly high near 2.90%, which in turn weighed on the Wall Street benchmarks and helped the US dollar to reverse the fall marked after the Federal Open Market Committee (FOMC) meeting minutes. That said, the US Dollar Index (DXY) ended Wednesday’s North American trading session with 0.18% daily gains around 106.70.

The Fed Minutes mentioned that the policymakers strongly supported the 75 bps rate increase in August while seeing a slowing pace of hikes at some point. The Minutes also signaled that Fed officials saw the hazard the Fed could tighten more than necessary.

Elsewhere, US Retail Sales flashed 0.0% growth during July, versus 0.1% expected and a downwardly revised 0.8% prior. The Retail Sales Control Group figures, however, rose to 0.8% compared to 0.6% market consensus and 0.7% prior (revised from 0.8%).

It should be noted that Federal Reserve Governor Michelle Bowman recently mentioned, “High inflation and strong employment will likely create some pressure on labor and employment.”

Elsewhere, China’s Premier Li Keqiang recently crossed wires, via the Communist Party’s flagship newspaper People’s Daily, while urging local officials from six key provinces that account for about 40% of the country’s economy to bolster pro-growth measures. Previously, President Xi Jinping and state planner National Development and Reform Commission (NDRC) showed readiness for more measures to combat the recession fears.

Moving on, second-tier US data may entertain XAU/USD traders with eyes on the central banks and growth concerns, not to forget China.

Technical analysis

Confirmation of the rising wedge bearish chart pattern precedes the yellow metal’s sustained trading below the 50-DMA and 21-DMA to direct XAU/USD bears towards the previous resistance line from April 18, around $1,735 by the press time.

However, a clear downside break of $1,735 won’t hesitate to refresh the yearly low surrounding $1,680 by the press time.

Alternatively, 21-DMA and 50-DMA guard the quote’s immediate upside around $1,765 and $1,776 in that order. Following that the aforementioned wedge’s lower line, near $1,809 at the latest, appears the last defense of the XAU/USD bears.

Gold: daily chart

Trend: Further downside expected

“(We are) At low end globally of inflation level, tracking in the right direction,” said Reserve Bank of New Zealand Governor Adrian Orr to New Zealand (NZ) Parliament's Finance and Expenditure Select Committee.

Additional comments

Labor constraint key reason to “consciously” slow demand to match supply capacity.

There is and will be financial stress in many households.

At times monetary policy was overly loose.

Market reaction

NZD/USD traces RBNZ Governor’s attempt to justify the latest moves, while also matching the previous cautious remarks, as the quote drops back to 0.6275 by the press time.

- USD/JPY is advancing some 0.03% as the Asian session begins on cooler-than-estimated FOMC minutes.

- The USD/JPY retraced towards the 50% Fibonacci retracement, before

- The major might extend its uptrend once buyers reclaim 135.50.

The USD/JPY grinds high as Wall Street closes, though retraced from weekly highs reached just above the 50-day EMA, at around 135.49, but FOMC’s minutes tumbled the pair towards the 135.00 figure before the NY close. At the time of writing, the USD/JPY is trading at 135.06.

US equities were lower on Wednesday, portraying risk aversion. The greenback weakened but held to gains against its counterpart’s safe-haven peers, and per the US Dollar Index, recorded modest gains of 0.16%, at 106.645.

Also read: FOMC minutes: Rate would have to reach a ‘sufficiently restrictive’ level to control inflation

USD/JPY Price Analysis: Technical outlook

The USD/JPY remains upward biased, despite retracing from daily highs. The break above the confluence of a downslope-trendline and the 20-day EMA opened the door for additional gains, further reinforced by the Relative Strength Index (RSI) just crossing above 50, a bullish signal. A decisive break above the 50-day EMA at 135.38 would open the door for further upside, being the first target, the July 27 daily high at 137.46.

In the shorter time-frame, as I wrote in yesterday’s article, “ … the major might print a leg down before resuming the higher-time frame uptrend towards 135.00 and beyond.” On Wednesday, the USD/JPY printed a leg down, towards the 200-hour EMA, just above the 50% Fibonacci retracement around 133.90, and resumed the uptrend. However, it faced sold resistance at 135.49 and consequently fell towards the 135.00 figure, ahead of Thursday’s Asian session open.

However, the USD/JPY is neutral-to-upward biased, and the first resistance will be the August 17 high at 135.49. Break above will expose 136.00, followed by the July daily high at 136.57.

USD/JPY Hourly chart

Also read: USD/JPY Price Analysis: Soars and reclaims 134.00, eyeing 135.00

USD/JPY Key Technical Levels

- AUD/USD came under pressure again despite benign FOMC minutes.

- There could be some sideways action ahead of Thursday's Aussie jobs data.

- 0.6980 eyed as a resistance area and 0.7020 thereafter. Bears will need to break 0.6910 daily lows ahead of 0.6870.

AUD/USD is trading down 1.2% on the day despite a benign set of minutes of the Federal Open Market Committee (FOMC) policy decision that took place over the July 26-27 policy meeting. There was a knee-jerk reaction to the minutes that took the value of the US dollar lower but the dip was bought back shortly afterwards resulting in a turnover in the commodity-fx arena.

At the time of writing, AUD/USD is trading around 0.6937 and has travelled within a 0.6910 and 0.7026 range on the day so far. There was not an explicit message that rate hikes will be as aggressive in Sepement. ''The post-minutes reaction was likely driven by 'many FOMC members' flagging that 'it likely would become appropriate at some point to slow the pace of policy rate increases while assessing the effects of cumulative policy adjustments on economic activity and inflation,''' analysts at TD Securities explained.

''This suggested to investors that the pace of rate hikes should slow, which pushed the pricing for a 75bp hike in September from 58% prior to the minutes to 47% and the terminal rate to 3.69% from 3.73% prior to the minutes,'' analysts explained. For that reason, US futures are pricing in a higher probability of a 50 bps hike for Sep after these minutes to around a 60% chance.

As a consequence, the DXY dropped 37 points to 106.385. The 10-year yield was under pressure, dropping 0.8% to 2.888% and well off the 2.919% highs for the day. The 2-year yield dropped by nearly 1.4%. This all enabled the Aussie to rally initially, however, as analysts at TD Securities argued, who believe the dovish reaction to the dated minutes may be unwarranted, ''markets should be taking their cue from hawkish Fed rhetoric in recent weeks rather than the minutes.''

The analysts explained that the Fed also discussed its desire to tighten financial conditions and the tightening that has occurred so far. ''However, financial conditions have recently eased and data has remained strong.''

Meanwhile for the day ahead, Aussie jobs data will be a critical feature of the Asian session. ''July is a seasonally strong month for job gains and we look for the unemployment rate to trend lower. Another strong labour print should give the RBA the assurance that the economy can withstand a cash rate of 3% by end-2022,'' the analysts at TDS said ahead of the data on Thursday.

AUD/USD technical analysis

AUD/USD came under pressure again and met the neckline on the W-formation on the hourly chart. This is holding as a support so far with a perfect touch of the 78.6% Fibonacci level. Should this continue to hold, there could be some sideways action ahead of Thursday's data with 0.6980 eyed as a resistance area and 0.7020 thereafter. Bears will need to break 0.6910 daily lows ahead of 0.6870.

What you need to take care of on Thursday, August 18:

The American dollar finished Wednesday higher against most major rivals on Wednesday, despite suffering a near-term setback following the release of the FOMC Meeting Minutes.

The greenback suffered a short-lived setback following the release of the Federal Reserve document, which showed that US policymakers unanimously agreed to hike rates by 75 bps, seeing a slowing pace of hikes at some point. It also read that many Fed officials saw the hazard the Fed could tighten more than necessary. Furthermore, some participants said the policy rate would have to reach a “sufficiently restrictive” level to control inflation and remain there “for some time.”

The EUR/USD pair managed to post modest intraday gains and settled around 1.0180, although the local GDP was downwardly revised. The GBP/USD pair, on the other hand, remained under pressure and finished the day at around 1.2050.

Commodity-linked currencies were among the weakest, with AUD/USD now trading around 0.9630 and USD/CAD just above 1.2900. The NZD/USD is down to 0.6270, as the New Zealand dollar retained its strength despite RBNZ Governor Orr saying they did not consider a 75 bps rate hike and lifted the main rate by 50 bps.

The greenback posted modest advances against safe-haven currencies, with USD/CHF trading around 0.9510 and USD/JPY at 135.00.

Gold trades at $1,765 a troy ounce, extending its weekly slide, while crude oil prices spent the day consolidating losses. WTI is changing hands at $87.60 a barrel.

Australia employment data coming up next.

Dogecoin Price Prediction: A $0.02 DOGE by 2023

Like this article? Help us with some feedback by answering this survey:

- Gold has spiked on the back of the FOMC minutes.

- Bears, however, have moved in fading the kneee-jerk reaction.

- The Jackson Hole symposium presents an additional avenue for the Fed to push back against the dovish narrative.

The gold price has rallied on the minutes from the Federal Reserve's July 26-27 policy meeting that, while not shedding much light on just how aggressive they expect to be, there was not an explicit message that rate hikes will be as aggressive in Sepement. For that reason alone, US futures are pricing in a higher probability of a 50 bps hike for Sep after these minutes to around a 60% chance.

The US dollar was lower as a consequence with the DXY dropping 37 points to 106.385. The 10-year yield was under pressure, dropping 0.8% to 2.888% and well off the 2.919% highs for the day. The 2-year yield dropped by nearly 1.4%. This enabled the yellow metal to recover some ground in a knee-jerk reaction.

Key notes from the Fed minutes

- Fed minutes: All participants at July 26-27 policy meeting agreed 75-basis-point interest rate hike was appropriate.

- Some participants said the policy rate would have to reach a 'sufficiently restrictive' level to control inflation and remain there 'for some time.

- Participants 'concurred' that future rate hikes would depend on incoming information, and judged that 'at some point' it would be appropriate to slow the pace of increases.

- Participants agreed there was 'little evidence inflation pressures were subsiding and that it would take a considerable time for the situation to be resolved.

- Participants 'emphasized' that slowdown in demand would 'play an important role in reducing inflation.

- Participants noted recent readings on inflation expectations were 'consistent' with long-run expectations anchored at 2%.

- Participants said the strength of the labour market suggests economic activity is stronger than implied by weak Q2, raising the possibility of upward GDP revision.

Is this the start of the pain trade in gold?

Analysts at TD Securities explained that ''while money manager length in gold hovering near multi-year lows, we are still anticipating a capitulation event in gold driven by the unwind of a massively bloated position held by a few proprietary trading shops and family offices.''

''A small breadth of these traders is holding nearly twice their average position size, accumulated during the pandemic, which does not appear to be associated with a Fed narrative or a recessionary view. As gold prices trade towards their pandemic-era entry levels, this complacent length is increasingly at risk for capitulation.''

''The Jackson Hole symposium presents an additional avenue for the Fed to push back against the dovish narrative.''

Gold technical analysis

Gold is retracing some of the rally in the aftermath of the minutes. It has broken the trendline resistance but a retest of the neckline of the W-formation is a high probability for traders fading the rally on lower time frames such as the 5 and 1 minute charts. The neckline aligns with the 61.8% Fibonacci retracement level of the hourly spike.

- The EUR/USD rallied close to 50 pips after the release of the July minutes.

- All Fed members agreed to hike 75 bps in the July meeting.

- Fed members acknowledge they would slow the pace of tightening at “some point.”

The EUR/USD jumped during the last hour due to the release of July’s Federal Reserve Open Market Committee (FOMC) minutes, which lifted the shared currency near the highs of the day, reached earlier, at 1.0198, though stabilized around the highs 1.0180s. At the time of writing, the EUR/USD is trading at 1.0190.

Summary of the FOMC minutes

The US Federal Reserve revealed in its minutes that all the participants agreed to hike rates by 75 bps, while many of them saw the Fed could tighten more if necessary. Fed officials added that future hikes would depend on incoming data while acknowledging that it would be appropriate to slow the pace of increases at some point.

Regarding inflation, Fed members said that there was “little evidence” of inflation subsiding and recognized it would take “considerable” time for the situation to be resolved. Concerning economic conditions, policymakers expressed that a strong labor market suggests economic activity is stronger than implied by the weak Q2 reading, raising the possibility of an upward GDP revision.

EUR/USD reaction

The EUR/USD rallied sharply, as shown by the 5-minute chart below. Even though the pair dipped towards 1.0185, buying pressure lifted the pair towards the daily high at 1.0202. Market participants’ interpretation of the minutes is perceived as dovish, despite pushing back efforts by Fed speakers in the last couple of weeks.

EUR/USD 5-minute chart

EUR/USD 5-minute chart

In the meantime, the US Dollar Index trimmed earlier gains and edged up 0.02% at 106.511, while the US 10-year bond yield rose seven bps at 2.884%, following the release of the minutes.

Aside from this, earlier US data revealed by the Department of Commerce reported that Retail sales for July increased by 10.3% YoY, exceeding forecasts of 8.3%, while the monthly reading was unchanged, missing expectations. Excluding autos and gasoline, sales jumped 0.4% YoY, vs. -0.1%.

EUR/USD Key Technical Levels

Reuters reports Federal Reserve Governor Michelle Bowman saying on Wednesday that a strong US labour market, the recovery of the service sector, and more fully open schools and childcare centres will likely bring more women back to the workforce.

"We continue to see strong employment gains and low unemployment rates—the kind of labour market that historically has pulled in more workers," Bowman said in remarks prepared for delivery to the Arkansas Women's Commission in Russellville, Arkansas.

"There are still plenty of jobs available even if we see the number of job openings reduced."

Key quotes

- Fed's Bowman: Labour market continues to be strong.

- Fed's Bowman: Future of labor supply is uncertain.

- Fed's Bowman: Some retirees may feel compelled to return to work due to inflation.

- Fed's Bowman says he sees potential for greater job opportunities for women in the future.

- Fed's Bowman: High inflation and strong employment will likely create some pressure on labour and employment.

Meanwhile, US futures are pricing in a higher probability of a 50 bps hike for Sep after the release of the FOMC minutes to around a 60% chance.

As a consequence, the US dollar is lower. The DXY index, that measure the greenback vs. a basket of currencies fell 30 points to 106.44. The 10-year yield is under pressure, dropping 0.8% to 2.888% and well off the 2.919% highs for the day. The 2-year yield dropped by nearly 1.4%.

- EUR/JPY rallies as buyers eye a break above the 100-day EMA at 138.10.

- A risk-off impulse was no excuse for EUR buyers to propel the shared currency higher.

- EUR/JPY buyers faltering to crack the 138.39 level would expose the pair to selling pressure.

The EUR/JPY climbs towards solid resistance around the 100-day EMA at 138.10 after clearing the 20-day EMA at 137.29, despite a risk-off impulse, which usually benefits safe-haven peers. Nevertheless, in the FX space, the only safe haven up in the day are the greenback and the Swiss franc. At the time of writing, the EUR/JPY is trading at 137.51, registering gains of 0.72%.

EUR/JPY Price Analysis: Technical outlook

The EUR/JPY daily chart portrays the pair as neutral-to-upward biased, further cemented by the Relative Strength Index (RSI) pushing above the 50-midline, signaling buyers are gaining impulse. However, unless they break above the August 10 daily high at 138.39, risks of sellers stepping in remain. If EUR/JPY reclaims the latter, the first resistance would be the 139.00 figure, followed by the50-day EMA at 139.36 and a downslope trendline drawn from the YTD highs around 144.00.

On the flip side, the EUR/JPY first support would be the August 16 high previous resistance-turned-support at 136.91. Once cleared, the next support will be the August 17 low at 136.26, followed by the August 16 daily low at 134.94. EUR/JPY Daily chart

EUR/JPY Daily chart

EUR/JPY Key Technical Levels

The Minutes of the Federal Open Market Committee (FOMC) policy decision that took place over the July 26-27 policy meeting that may shed light on just how aggressive they expect to be have been released as follows:

- Fed minutes: All participants at July 26-27 policy meeting agreed 75-basis-point interest rate hike was appropriate.

- Some participants said the policy rate would have to reach a 'sufficiently restrictive' level to control inflation and remain there 'for some time.

- Participants 'concurred' that future rate hikes would depend on incoming information, and judged that 'at some point' it would be appropriate to slow the pace of increases.

- Participants agreed there was 'little evidence inflation pressures were subsiding and that it would take a considerable time for the situation to be resolved.

- Participants 'emphasized' that slowdown in demand would 'play an important role in reducing inflation.

- Participants noted recent readings on inflation expectations were 'consistent' with long-run expectations anchored at 2%.

- Participants said the strength of the labour market suggests economic activity is stronger than implied by weak Q2, raising the possibility of upward GDP revision.

Market reaction

US futures are pricing in a higher probability of a 50 bps hike for Sep after these minutes to around a 60% chance. The US dollar is lower as a consequence with the DXY dropping 25 points to 106.48. The 10-year yield is under pressure, dropping 0.8% to 2.888% and well off the 2.919% highs for the day. The 2-year yield dropped by nearly 1.4%.

About the FOMC minutes

Investors look for clues regarding the policy outlook in this publication alongside the vote split. A bullish tone would be expected to provide a boost to the greenback while a dovish stance would be seen as USD-negative. It needs to be noted that the market reaction to FOMC Minutes could be delayed as news outlets don’t have access to the publication before the release, unlike the FOMC’s Policy Statement.

FOMC stands for The Federal Open Market Committee organizes 8 meetings in a year and reviews economic and financial conditions, determines the appropriate stance of monetary policy and assesses the risks to its long-run goals of price stability and sustainable economic growth. FOMC Minutes are released by the Board of Governors of the Federal Reserve and are a clear guide to the future US interest rate policy.

- GBP/USD bulls are stepping in ahead of the FOMC minutes.

- This leaves a 38.2% ratio and the 50% mean reversion level vulnerable for the immediate future.

- On the 4-hour chart, the key structure on the upside is around 1.2150, 1.2280 and to the downside, around 1.2020 and then 1.1965.

GBP/USD is under pressure in midday New York trade. Cable was last down 0.39% on the day at 1.2046 and has fallen from a high of 1.2142 and met a low of 1.2027 from where it is correcting currently.

Markets have been digesting plenty of data this week in the build-up to the Federal Reserve's minutes from its July meeting. The Us dollar had been under demand following data that showed US consumer spending was steady in July. US Retail Sales were unchanged due to declining gasoline prices that weighed on receipts at service stations but, overall, consumer spending appeared to hold up. This was seen to assuage fears that the US economy was already in recession.

However, the Fed is expected to continue to hike rates aggressively to battle inflation although softer-than-expected inflation in July had eased some concerns. On the other hand, looser financial conditions as benchmark 10-year Treasury yields hold below 3% has also increased the probability that the Fed may need to be more aggressive in hiking rates to make an impact. In any case, the release of the minutes from the Fed's July 26-27 policy meeting may shed light on just how aggressive they expect to be. Fed funds futures traders are currently pricing in a 48% chance of a 50 basis points increase and a 52% probability of a 75 basis points hike.

As for domestic inflation, the UK's July Consumer Price Index data came in hot. The headline came in at 10.1% YoY vs. 9.8% expected and 9.4% in June, core came in at 6.2% YoY vs. 5.9% expected and 5.8% in June, and CPIH came in at 8.8% YoY vs. 8.6% expected and 8.2% in June.

Analysts at Brown Brothers Harriman explained that, of note, ''the Bank of England sees headline inflation peaking near 13% in October. Market expectations have risen sharply on the realization that the bank is set to continue tightening as inflation spirals ever higher.''

''WIRP suggests a 50 bp hike on September 15 is fully priced in, with 25% odds now seen of a larger 75 bp move. The swaps market is now pricing in 200 bp of tightening over the next 12 months which would see the policy rate peak near 3.75% vs. 3.25-3.50% at the start of this week and 3.0-3.25% at the start of last week.''

GBP/USD technical analysis

The hourly chart, above, shows that the price could be on the verge of a downside extension. However, it is in a corrective phase currently. The 15-minute charts identify areas of price imbalance, as per the greyed-out areas below:

This leaves a 38.2% ratio and the 50% mean reversion level vulnerable for the immediate future.

On the 4-hour chart, the key structure on the upside is around 1.2150, 1.2280 and to the downside, around 1.2020 and then 1.1965:

- WTI is trimming some of its Tuesday’s losses, up by 0.80% in the North American session

- US EIA stockpiles shed 7.06 million barrels last week, spurring a jump in oil prices.

- China’s slower-than-expected growth pace, and Iran’s nuclear deal agreement, put a lid on higher oil prices.

Western Texas Intermediate (WTI) prices seesaw in a thin trading session after a US stockpile inventory spurred an uptick in oil prices when the US EIA revealed its weekly report illustrating that demand remains strong. At the same time, the US assesses Iran’s proposals for a nuclear deal.

In the meantime, WTI is trading at $87.84 PB, above its opening price, registering gains of 0.85% after hitting a daily low of $85.90.

WTI rises on lower US stockpiles

Sentiment deteriorated since the beginning of the European session. European bourses ended in the red, while US equities are dropping. The greenback rises, underpinned by Investors’ appetite for safe-haven assets, with the US Dollar Index hitting fresh three-week highs around 106.943, but at the time of writing, is at 106.752, up 0.27%.

The US EIA report showed that inventories fell by 7.06 million last week, while exports increased due to European buyers replacing Russia’s oil. Meanwhile, the Organization of the Petroleum Exporting Countries (OPEC) new Secretary Haitham Al Ghais said that he was confident that global oil demand would increase by almost 3 million barrels a day, in 2022, via Bloomberg.

Aside from this, worries that China’s economy might grow at a slower pace keep oil participants uneasy. China’s Premier Li Kequiang demanded local officials, that account for 40% of China’s economy, to bolster growth measures following softer-than-expected Industrial Production and Retail sales.

Therefore, the WTI outlook is slightly tilted to the downside, as further news points to lower demand but increasing offers, exacerbating downward pressure on oil prices.

WTI Key Technical Levels

- USD/CAD climbs above the 20/50-DMA, up by 0.64% in the day.

- US Retail Sales beat estimations but were ignored by market players focused on FOMC minutes.

- According to TDS analysts, a cooler-than-expected Canadian inflation report would not deter the Bank of Canada (BoC) of hiking 75 bps.

USD/CAD breaks above the 20 and 50-day EMAs, refreshing weekly highs around 1.2936 in the North American session, triggered by modestly positive US Retail Sales data, while a risk-off impulse in the markets added to overall US dollar strength, to the detriment of the Canadian dollar.

The USD/CAD is trading above its opening price at 1.2916 after reaching a daily low of 1.2827 during the European session.

The US Department of Commerce reported that Retail sales for July rose by 10.3% YoY, beating estimates of 8.3%, while the monthly reading was unchanged, missing expectations. Excluding autos and gasoline, sales jumped 0.4% YoY, vs. -0.1%. Albeit the report was positive, market participants’ focus is still on the July Federal Reserve Open Market Committee (FOMC) minutes.

In the meantime, the US Dollar Index, rises 0.33%, at 106.825, while US crude oil prices, also known as WTI, is slightly down, trading at $87.01 PB, down 0.07%. The previously mentioned factors exerted upward pressure on the USD/CAD, with buyers reclaiming the 1.2900 figure.

On the Canadian side, on Tuesday, inflation figures for July were mixed, with the plain vanilla Consumer Price Index at 7.6% YoY, unchanged. Still, core figures were skewed to the upside, mainly CPI Trimmed-mean and CPI Median, at 5.4% and 5% year-over-year, respectively.

Analysts at TDS commented, “With core inflation averaging 5.3% y/y and CPI-common sitting at 5.5%, we do not expect the Bank of Canada to draw much comfort from the moderation in headline CPI and continue to look for a 75bp hike in September.”

All that said, the USD/CAD inched higher, boosted by expectations that US FOMC minutes would be leaning towards the hawkish side, consequently bolstering US bond yields, which may underpin the US dollar.

What to watch

The US economic docket will feature Fed Governor Michelle Bowman’s speech, alongside July’s FOMC minutes. The Canadian economic calendar will reveal the Producer Price Index (PPI) for July, alongside Retail Sales.

USD/CAD Key Technical Level

According to analysts from Danske Bank, dollar weakness is likely to be transitory. They forecast EUR/USD at 0.99 in one month, 0.98 in three months and at 0.95 in twelve months.

Key Quotes:

“The large negative terms-of-trade shock to Europe vs US, a further cyclical weakening among trading partners, the coordinated tightening of global financial conditions, broadening USD strength and downside risk to the euro area makes us keep our focus on EUR/USD moving still lower (targeting 0.95) – a view not shared by the consensus.”

“The key risk to shift EUR/USD towards 1.15 is seeing global inflation pressures fade and industrial production increase. However, ‘transitory’ has substantially lost credibility and European industrial production continues to be weak. This will continue as manufacturing PMIs heads below 50. The upside risk also include a renewed focus on easing Chinese credit policy and a global capex uptick but neither appear to be materialising, at present.”

Retail sales were flat in July (against expectations of a 0.1% increase), but after adjusting for sharply lower prices of some goods, particularly gasoline, real retail sales actually rose 0.6%, the first volume gain in three months, point out analysts at Wells Fargo. They expect the staying power of the consumer to last into August before a sharp spending retrenchment takes hold this autumn.

Key Quotes:

“Amid constant headlines about the highest inflation in 40 years, there is an overlooked and counterintuitive fact that puts the July retail sales report into context: goods prices were actually down 0.5% in July, according to the already-released CPI report. Today, we learned that July retail sales were flat for the month, but the fact that goods prices were down means people actually got a little more for their money in July. By our accounting, real retail sales were actually up 0.6%.”

“We forecast real personal consumption expenditures to rise at a 2.0% annualized pace in the third quarter before contracting 0.5% in the fourth. This retail sales report does not change that expectation. But with notable crosscurrents beneath the surface, the trajectory for spending may be a bit bumpier in the second half of the year than we presently expect.”

“Supply chains are thawing, which may finally give way to some normalization in the auto sector specifically. Consumers are transitioning away from goods purchases to services, but this is happening at a very gradual pace. The staying power of consumers has been quite robust, but it's showing signs of running out. How these factors evolve from here will determine the trajectory for spending, and thereby the overall economy.”

The Swiss National Bank will likely raise the key rate by 05 basis points again in September and December according to analysts at Danske Bank. They see the EUR/CHF cross at 0.96 in one month, at 0.95 in three months and at 0.93 in twelve months.

Key Quotes:

“EUR/CHF has moved sharply lower and is currently trading around 0.96. This comes after a month of global yields moving lower and consequently rising recession fears."

“We expect the SNB to hike by 50bp again in September and December to curtail underlying inflation pressures bringing the policy rate to 0.75%. With the SNB broadly following the ECB, we see relative rates as an inferior driver for the cross. We continue to forecast the cross to move lower on the back of fundamentals and a tighter global investment environment. We thus lower our overall forecast profile and now forecast EUR/CHF at 0.93 in 12M.”

“The key upside risks to our forecast are global yield curves steepening amid a shift in the global investment environment and/or the SNB falling behind the curve.”

Analysts at Danske Bank expected the pressure on the Japanese yen will wear off but not in the short term. They forecast the USD/JPY pair at 134 (1M), 134 (3M), 133 (6M) and 125 (12M).

Key Quotes:

“With the economic recovery in Japan still hampered by COVID, domestic price pressures are likely to remain modest. Thus, the key driver of USD/JPY remains the outlook for the global economy and the energy crunch. With the US labour market still in top shape, we are not convinced global inflation pressures are yet turning and expensive natural gas over the winter will keep JPY headwinds in place.”

“Upside risks to USD/JPY come from a new surge in commodities and energy prices driving inflation and global yields higher. If global slowdown turns into a real recession, flatter yield curves and cheaper energy will drive USD/JPY lower. The risk of Tokyo intervening in FX markets has declined as JPY pressures have eased and BoJ has demonstrated a strong will to keep aiming for the inflation target without politicians interfering.”

- EUR/USD spikes to 1.0198 and quickly pulls back to 1.0160.

- US dollar and euro among top performers on Wednesday.

- Market participants await FOMC minutes.

The EUR/USD continues to move sideways on Wednesday around 1.0160/70 ahead of the release of the FOMC minutes. The pair made a run to 1.0198, hitting the highest level in two days but it quickly pulled back toward 1.0160.Economic data released in the US showed retail sales stagnated in July, against expectations of a 0.1% increase. The details of the report were above market consensus. Later on Wednesday, the Federal Reserve will release the minutes of its latest meeting when it raised the Fed Funds rate by 75 basis points. Market participants will look for clues about the next steps of the central bank.

Analysts at Brown Brothers Harriman expect the minutes to come in very hawkish. “It wasn’t until Chair Powell’s post-decision press conference that markets saw what they believed was a dovish pivot, when he acknowledged the pace of future rate hikes will depend on incoming data (…) Because the Fed has embarked on a corrective communication effort since that meeting, the minutes should reveal more about the Fed’s hawkish thinking then”. Such a scenario could be bullish for the US dollar.

The DXY is up by 0.22% on Wednesday, supported by higher yields and risk aversion. The euro is also gaining ground. EUR/CHF is up sharply for the second day in a row, recovering almost a hundred pips from record lows, approaching 0.9700. EUR/GBP is at two-day highs near 0.8450 despite higher-than-expected UK inflation data.

Short-term outlook

The EUR/USD continues to move sideways under the 20-day Simple Moving Average, today at 1.0210 and also still looking at the 1.0100/10 critical support. A break under 1.0100 should clear the way to more weakness. On the flip side above 1.0210, the euro could strengthen. Still a consolidation above 10.270 is needed for a test of the 55-day SMA that capped the rally last week, currently at 1.0335.

Technical levels

- AUD/USD slides more than 1.40% on Wednesday due to cooler-than-expected Australia’s Wage Price Index (WPI).

- Risk aversion keeps investors leaning towards safe-haven assets, bolstering the greenback.

- AUD/USD Price Analysis: Break below 0.6900 to extend losses towards 0.6869 before clearing the way towards 0.6681.

AUD/USD tumbles below the 20/50-day EMA on Wednesday, on a risk-off impulse spurred by recession fears lingering on investors’ minds, while US Retail Sales crushed expectations on a yearly basis, ahead of the release of July’s FOMC monetary policy minutes. At the time of writing, the AUD/USD is trading at 0.6915.

Global bourses reflect a deterioration in sentiment. A report by the US Department of Commerce revealed that Retail Sales on a monthly basis for July finished flat at 0%, missing estimates of 0.1%, undermined by declines in auto purchases and gas prices. Compared to one year before, sales rose by 10.3%, higher than the 8.3% estimates.

Even though the news was positive, traders’ reaction was muted, as they remained focused on the July FOMC minutes.

Additional factors weighing on the AUD/USD are the greenback, with the US Dollar Index, a gauge of the buck’s value against a basket of six peers, advancing 0.22% at 106.708. Further, Iron Ore prices drop 1.73% to $105.51 a ton, down from the August peak at $114.31.

Meanwhile, in the Asian session, the Australia Wage Price Index increased less than estimations, so traders priced in less aggressive rate hikes by the RBA, a headwind for the Aussie, which tumbled from 0.7026 daily highs below the 0.7000 figure. The quarter-on-quarter figure rose 0.7%, less than 0.8% expected, while on a yearly basis, it jumped 2.6%, lower than 2.7%.

What to watch

The US economic docket will feature the FOMC minutes release alongside Fed’s Governor Michell Bowman, crossing newswires on Wednesday. In the Australian calendar, traders will get cues from employment data.

Also read: Australian Employment Preview: Forecasts from four major banks, solid job creation

AUD/USD Price Analysis: Technical outlook

In the last three days, AUD/USD’s price action witnessed a fall of almost 3%, from monthly highs reached at 0.7136. Losses extended below the 100, 50, and 20-day EMAs, with sellers aggressively in charge. Further confirmation of the previously mentioned is the Relative Strength Index (RSI) with a steeper fall from 64.39, below the 50-midline, but with enough room to spare before reaching oversold conditions. Therefore, the AUD/USD next support will be the 0.6900 figure. Once cleared, it will expose crucial support levels, at 0.6869 August 5 low, followed by the YTD low at 0.6681.

Australia is set to report its July employment figures on Thursday, August 19 at 01:30 GMT and as we get closer to the release time, here are forecasts from economists and researchers at four major banks regarding the upcoming employment data.

Australia is expected to have added 25K positions in the month, while the Unemployment Rate is set to remain at the current 3.5%. Additionally, the Participation Rate is also seen as stable, at 66.8%.

ANZ

“For July, we expect another solid rise in employment of 40K which should see the unemployment rate edging down to 3.4%, even with a small rise in participation, on its way to sub-3%.”

Westpac

“We have an around trend forecast of 50K. We look for a further 0.1% increase in participation to 66.9% limiting the fall in unemployment to 0.1ppt to 3.4%.”

TDS

“July is a seasonally strong month for job gains and we look for the unemployment rate to trend lower. Another strong labour print (we forecast 50K) should give the RBA the assurance that the economy can withstand a cash rate of 3% by end-2022.”

NAB

“We look for employment growth of 20K and for the unemployment rate to be unchanged at 3.5%.”

- Gold turns lower for the third straight day and drops to over a one-week low on Wednesday.

- Hawkish Fed expectations, rising US bond yields underpin the USD and exert some pressure.

- The risk-off mood fails to lend support to the safe-haven XAU/USD ahead of FOMC minutes.

Gold attracts fresh selling near the $1,782 region on Wednesday and turns lower for the third straight day. The intraday selling bias remains unabated through the early North American session and drags the XAU/USD to a one-and-half-week low, around the $1,765-$1,764 area in the last hour.

The US dollar ticks higher, back closer to the monthly top touched the previous day, which turns out to be a key factor denting demand for the dollar-denominated gold. Despite signs of easing US inflation, investors seem convinced that the Fed would stick to its policy tightening path. Wednesday's mostly upbeat US Retail Sales data reaffirms market bets and continues to act as a tailwind for the buck.

Hawkish Fed expectations, meanwhile, trigger a fresh leg up in the US Treasury bond yields. This offers additional support to the greenback and further contributes to driving flows away from the non-yielding yellow metal. That said, growing recession fears, along with the risk-off impulse, could extend some support to the safe-haven gold and help limit any further losses, at least for the time being.

Worries about a global economic downturn temper investors' appetite for perceived riskier assets, which is evident from a generally weaker tone around the equity markets. This might hold back bearish traders to place aggressive bets ahead of the FOMC meeting minutes, scheduled for release later during the US session. Market players will look for clues about the possibility of a 75 bps rate hike in September.

The Fed's policy outlook would play a key role in influencing the near-term USD price dynamics and provide a fresh directional impetus to gold. From a technical perspective, the recent repeated failures to find acceptance, or build on the momentum beyond the $1,800 mark supports prospects for a further near-term depreciating move. Hence, any attempted recovery could still be seen as a selling opportunity.

Technical levels to watch

- EUR/USD comes under pressure once again near 1.0150.

- The 1.0370/80 band caps the upside for the time being.

EUR/USD returns to the lower end of the weekly range near 1.0150 and fades at the same time Tuesday’s shy advance.

While below the 1.0370/80 band, a region where the August high and the 6-month resistance line converge, the pair is expected to remain under downside pressure. That said, the lower end of the recent range in the 1.0100 zone should hold the downside ahead of a potential challenge of the psychological parity level.

In the longer run, the pair’s bearish view is expected to prevail as long as it trades below the 200-day SMA at 1.0873.

EUR/USD daily chart

- GBP/USD witnesses an intraday turnaround and retreats nearly 100 pips from the daily high.

- The USD stands tall near the monthly peak and turns out to be a key factor exerting pressure.

- The US Retail Sales fail to provide any impetus as the focus remains on the FOMC minutes.

The GBP/USD pair extends its intraday retracement slide from the vicinity of mid-1.2100s and continues losing ground through the early North American session. Spot prices drop to the 1.2050-1.2045 region, or a fresh daily low in the last hour, reversing a major part of the overnight recovery gains from the monthly low.

The US dollar regains some positive traction and inches back closer to its highest level since late July touched the previous day. This overshadows hotter-than-expected UK consumer inflation figures and attracts fresh selling around the GBP/USD pair. Expectations that the Fed would stick to its policy tightening path, along with a fresh leg up in the US Treasury bond yields and the risk-off impulse, continue to underpin the safe-haven buck.

The USD holds on to its modest intraday gains after the US Census Bureau reported that US Retail Sales remained flat in July, missing expectations for a modest 0.1% increase. A slight disappointment, however, was largely offset by unexpected growth in sales excluding autos, which rose 0.4% during the reported month. Adding to this, Control Group sales climbed 0.8% during the reported month against consensus estimates pointing to a 0.6% rise.

The data might have lifted bets for a larger Fed rate hike move at the September meeting, which remains supportive of elevated US Treasury bond yields. That said, traders seem reluctant to place aggressive bets and prefer to wait for the FOMC meeting minutes, due for release later during the US session. This, in turn, suggests that the GBP/USD pair is more likely to find decent support and stall the intraday slide near the 1.2000 pivotal support.

Technical levels to watch

Is this the start of the pain trade in gold? As gold prices trade towards their pandemic-era entry levels, some traders’ complacent length is increasingly at risk for capitulation, economists at TD Securities report.

FOMC minutes to reinforce a hawkish stance

“While money manager length in gold hovering near multi-year lows, we are still anticipating a capitulation event in gold driven by the unwind of a massively bloated position held by a few proprietary trading shops and family offices.”

“The FOMC minutes today are likely to reinforce a hawkish stance, and considering the strength in financial conditions observed over the past weeks, the Jackson Hole symposium presents an additional avenue for the Fed to push back against the dovish narrative.”

“The margin of safety for trend follower short covering is rising, while Shanghai traders are also likely to join in on the offer after having accumulated nearly 14 tonnes of gold ahead amid Taiwan tensions with lockdowns and a depreciating CNY denting Chinese demand.”

- USD/JPY gains strong follow-through traction for the second successive day on Wednesday.

- Hawkish Fed expectations, rising US bond yields underpin the USD and remain supportive.

- The markets react little to the US Retail Sales figures as the focus remains on FOMC minutes.

The USD/JPY pair prolongs its one-week-old ascending trend and gains traction for the second straight day on Wednesday. The pair maintains its strong bid tone through the early North American session and is currently placed just below mid-135.00s, or over a one-week high.

The US dollar regains positive traction and inches back closer to the monthly peak touched the previous day, which turns out to be a key factor acting as a tailwind for the USD/JPY pair higher. The recent hawkish remarks by several Fed officials fueled speculations that the Fed would stick to its policy tightening path. This, along with a fresh leg up in the US Treasury bond yields, continues to underpin the buck.

The USD holds steady after the US Census Bureau reported that the US Retail Sales remained flat MoM in July, missing estimates for a modest 0.1% increase. The slight disappointment, however, was largely offset by unexpected growth in sales excluding autos, which rose 0.4% during the reported month. Adding to this, Control Group sales climbed 0.8% during the reported month against market expectations for a 0.6% rise.

The data reaffirms hawkish Fed expectations and remains supportive of elevated US bond yields, widening the US-Japan rate differential. This, in turn, weighs on the Japanese yen and pushes the USD/JPY pair higher. That said, the risk-off impulse, as depicted by a generally weaker tone around the equity markets, seems to offer some support to the JPY and might keep a lid on any meaningful upside for the pair, at least for now.

Traders might also refrain from placing aggressive bets and prefer to wait on the sidelines ahead of the FOMC meeting minutes, due later during the US session. Investors will look for clues about the possibility of a larger 75 bps Fed rate hike move in September, which would play a key role in influencing the near-term USD price dynamics. This, in turn, should help determine the next leg of a directional move for the USD/JPY pair.

Technical levels to watch

- Retail Sales in the US stayed unchanged on a monthly basis in July.

- US Dollar Index continues to push higher toward 107.00.

Retail Sales in the US stayed virtually unchanged at $682.8 billion in July, the data published by the US Census Bureau showed on Wednesday. This reading followed June's increase of 0.8% and came in slightly weaker than the market expectation of +0.1%.

"Total sales for the May 2022 through July 2022 period were up 9.2% from the same period a year ago," the publication further read. "The May 2022 to June 2022 percent change was revised from up 1.0% to up 0.8%."

Market reaction

The greenback continues to outperform its rivals after this data with the US Dollar Index rising nearly 0.4% on the day at 106.87.

- DXY keeps the weekly bounce well in place near 106.80.

- Extra upside appears likely once 107.00 is surpassed.

DXY quickly fades Tuesday inconclusive price action and resumes the upside to the upper end of the recent range near 106.80.

The continuation of the upside momentum could extend to the August high near the 107.00 mark (August 5). The breakout of this level should motivate the index to challenge the post-FOMC meeting high at 107.42 (July 27).

Looking at the broader scenario, the bullish view in the dollar remains in place while above the 200-day SMA at 100.22.

DXY daily chart

- EUR/JPY extends further north of 137.00 its weekly recovery.

- Immediately to the upside comes the August high at 138.40.

EUR/JPY adds to Tuesday’s gains and reclaims the area beyond the 137.00 yardstick on Wednesday.

In case the recovery becomes more serious, then the cross should meet the next barrier at the 100-day SMA at 138.10 ahead of the more relevant August high at 138.39 (August 10).

While above the 200-day SMA, today at 133.98, the prospects for the pair should remain constructive.

EUR/JPY daily chart

Trend signals in gold have deteriorated further. As strategists at TD Securities note, the downtrend in gold is still gaining steam.

Gold distrusts Fed pivot

“Trend signals in the yellow metal are pointing to a strengthening downtrend, which clashes against market hopes of a Fed pivot amid cooling inflation.”

“As long as gold remains below $1,890 before year-end, participants should distrust a regime change in gold prices associated with a pivot in Fed policy.”

Economists at Commerzbank have significantly lowered their EUR/USD forecast. The reason is that the euro is likely to continue to suffer from the risk of a halt to Russian gas supplies and from the relatively hesitant European Central Bank (ECB) monetary policy.

A recession in the euro area will increase pressure on EUR/USD

“We now expect a recession for the euro area, triggered by high energy prices, in turn, a consequence of reduced gas supplies from Russia.”

“For 2023, we expect a partial recovery of EUR/USD when it becomes clear that Europe can meet its energy needs without Russian gas, when energy prices settle down again and when it becomes clear that the ECB resumes its rate hike cycle.”

“EUR/USD: Sep-22 1.00 Dec-22 0.98 Mar-23 0.98 Jun-23 1.02 Sep-23 1.06.”

US Monthly Retail Sales Overview

Wednesday's US economic docket highlights the release of monthly Retail Sales figures for July, due later during the early North American session at 12:30 GMT. The headline sales are estimated to register a modest 0.1% growth during the reported month, down sharply from the 1% increase in June. Excluding autos, core retail sales probably shrunk by 0.1% in July against the 1% rise in the previous month.

Analysts at ING offer a brief preview of the report and explain: “Retail sales at the headline level will be modestly depressed (0.3%) due to falling gasoline prices weighing on gas station sales as it is a nominal dollar figure. However, this frees up cash to spend on other goods and services so the ‘core’ rate of retail sales growth should rebound and help to translate into rising real consumer spending.”

How Could it Affect EUR/USD?

Ahead of the key release, the US dollar stands tall near the monthly peak touched the previous day and continues to draw support from hawkish Fed expectations. A surprisingly stronger consumer spending data would reaffirm speculations that the Fed would stick to its aggressive policy tightening path and lift the greenback. Conversely, a weaker-than-expected report could prompt some USD selling and lend support to the EUR/USD pair. That said, any immediate market reaction is more likely to be short-lived ahead of the FOMC meeting minutes, scheduled to be released later during the US session.

Eren Sengezer, Editor at FXStreet, offers a brief technical outlook and writes: “EUR/USD faces strong resistance in the 1.0200/1.020 area, where the 100-period and the 200-period SMAs on the four-hour chart are located. Unless buyers reclaim that level, the bearish bias should stay intact. Meanwhile, the Relative Strength Index (RSI) indicator stays below 50 and the 20-period SMA crossed below the 50-period and 100-period SMAs, supporting the view that sellers look to dominate the pair's action.”

Eren also outlines important technical levels to trade the EUR/USD pair: “On the downside, 1.0150 (static level) aligns as first support. Although the pair dropped below that level on Tuesday, it managed to rise back above it. If this level is confirmed as resistance, additional losses toward 1.0100 (static level, psychological level) and 1.0050 (static level) could be witnessed.”

“Above 1.0200, resistance are located at 1.0230 (Fibonacci 38.2% retracement, 50-period SMA) and 1.0300 (Fibonacci 50% retracement),” Eren adds further.

Key Notes

• US Retail Sales Preview: Forecasts from six major banks, losing speed in July

• EUR/USD Forecast: Euro could test 1.0100 with key resistances staying intact

• EUR/USD: Break below support at 1.01 to open up a move towards parity – ING

About US Retail Sales

The Retail Sales released by the US Census Bureau measures the total receipts of retail stores. Monthly per cent changes reflect the rate of changes in such sales. Changes in Retail Sales are widely followed as an indicator of consumer spending. Generally speaking, a high reading is seen as positive (or bullish) for the USD, while a low reading is seen as negative (or bearish).

In the view of economists at Scotiabank, the USD/CNH pair is set to trade within a 6.70-6.80 range in the weeks ahead.

China’s economy to revive further in the second half

“We expect China’s economy to revive further in the second half with more fiscal stimulus to be rolled out.”

“We believe China’s central bank will not flood the economy with excessive liquidity and a weaker yuan that makes imports into China more expensive is not in the monetary authority’s interest at this stage.”

“USD/CNH is expected to trade between 6.70 and 6.80 with downside potential in the weeks ahead.”

The S&P 500 Index now face a key test of technical resistance at the 200-day moving average (DMA), potential downtrend and 61.8% retracement at 4327/70, with Credit Suisse’s bias for a potentially important top here.

Weekly MACD momentum maintains its bullish cross

“Although weekly MACD momentum has crossed higher, we continue to look for a potentially important top at the falling 200-DMA, potential downtrend from the beginning of the year and 61.8% retracement of the 2022 fall at 4327/70.”

“Near-term support is seen at 4177, with a break below 4117/07 seen as needed to add weight to our view for a fall back to the 63-day average, now at 3974.”

“A close above 4370 would suggest strength can extend further, with resistance seen next at 4513, then the 78.6% retracement of the 2022 fall at 4566.”

Norges Bank meets on Thursday, August 18 at 08:00 GMT and as we get closer to the release time, here are the expectations forecast by the economists and researchers of six major banks regarding the upcoming central bank's Interest Rate Decision.

Markets are pricing in a 50 basis points (bps) rate hike to 1.75%. Furthermore, investors will be even more focused on the wording of the statement and on the press conference by Norges Bank Governor Ida Wolden Bache.

Danske Bank

“We now expect NB to hike policy rates by 50 bps instead of 25 bps after the recent high inflation numbers. However, there will be no press briefing as this is an intermediary meeting. We still believe that the policy rate will peak in December this year at 2.25% by hiking 50 bps this week, 25 bps in September, and 25 bps in December. If we are right in our call on NB, NOK FX is not expected to be much affected.”

TDS

“We look for a 50 bps hike from Norges Bank, in line with market pricing and the consensus, and despite the Norges Bank's most recent forecast of a 25 bps hike at this meeting. Inflation has been much stronger than expected, with headline and underlying inflation running 1.7ppts and 1.3ppts above the Bank's latest forecasts, respectively.”

ING

“Having hiked rates by 50 bps in June, on paper there are good reasons for Norway’s central bank to do the same again. Crucially the latest inflation readings have come in above the bank’s forecasts again. While the bank will be nervous about inflation, its models will also be acknowledging the fact that global market rates have fallen since June, which in isolation would be interpreted as a dovish factor. Bottom line: it’s a close call, though we narrowly favour a 25 bps move. As other central banks have found in recent weeks, Norges Bank faces a choice between sticking to its ‘forward guidance’, or adapting to the latest economic data.”

Commerzbank

“The fact that Norges Bank will raise the policy rate by 50 bps to 1.75% is likely to be largely priced in. Inflation is higher than expected by Norges Bank in June. It will therefore in all likelihood have to adjust its inflation forecasts upward again in the new monetary policy report in September. As a result, the basis for Wednesday’s interest rate hike is likely to be higher-than-expected inflation. I see a good chance that, on the basis of new, higher inflation forecasts that will be published in September with the new monetary policy report, it will then also raise the policy rate by another 50 bps and adjust the interest rate path accordingly. Hence, if Norges Bank plans to raise the policy rate by 50 bps in September also, it will in any case have to adjust the interest rate path upward once again. It would at least have to hint at that. What does that mean for the NOK? If the Norges Bank sounds restrictive and signals another juicy move for September, the NOK should be able to appreciate against the euro.”

Credit Suisse

“We anticipate nuance from the Norges Bank, where a 50 bps hike might still not be seen as a clearly hawkish development.”

Swedbank

“We expect Norges Bank to hike by 50 bps at the upcoming August meeting and in September, followed by 25 bps in both November and December. This should leave the policy rate at 2.75% by year-end, which we deem to be the peak.”

- Silver witnesses some selling for the third successive day on Wednesday.

- Acceptance below the 50 DMA supports prospects for additional losses.

- Any attempted recovery move might now be seen as a selling opportunity.

Silver struggles to capitalize on the previous day's late rebound and meets with a fresh supply near the $20.25-$20.30 region on Wednesday. The white metal remains depressed for the third straight day and slips back below the $20.00 psychological mark during the first half of the European session.

The XAG/USD is currently hovering around over a one-week low touched on Tuesday and now seems to have found acceptance below the 50-day SMA. Bulls now look to the 38.2% Fibonacci retracement level of the $22.52-$18.15 downfall, near the $19.80 region, to offer some support. A convincing break below would expose the next relevant support near the $19.55 area (last week's swing low).

The latter should now act as a key pivotal point, which if broken decisively would be seen as a fresh trigger for bearish traders and make the XAG/USD vulnerable. Spot prices could then accelerate the fall towards the 23.6% Fibo. level, around the $19.20-$19.15 region, en route to the $19.00 mark. The downward trajectory could further get extended towards the $18.45-$18.40 area.

On the flip side, the 50% Fibo. level, around the $20.35 region, now becomes an immediate strong hurdle. Any subsequent move up could be seen as a selling opportunity near the $20.65 horizontal zone and remain capped near the 61.8% Fibo. level, around the $20.85 region. That said, some follow-through buying beyond the $21.00 mark could negate the negative outlook for the XAG/USD.

Silver daily chart

-637963279129018048.png)

Key levels to watch

Gold remains in a range. However, a major “double top” continues to threaten, as strategists at Credit Suisse note.

Sustained break above 55 DMA to confirm further ranging

“A convincing break above the 55-day average, currently seen at $1,786, would confirm further ranging in the two-year range, with next resistance then seen at the even more important 200-day average, currently at $1,842.”

“We continue to stress that a closing break below $1,691/77 would be sufficient to complete a large ‘double top’, which would turn the risks lower over at least the next one-three months. We note that the next support should this top be triggered is seen at $1,618/16, then $1,560.”

- EUR/GBP bounces off earlier lows near 0.8380.

- UK CPI rose 10.1% YoY in July, 0.6% MoM.

- EMU advanced Q2 GDP is seen expanding 3.9% YoY.

Following a knee-jerk to the vicinity o 0.8380, EUR/GBP regains some composure and now manages to retake the 0.8400 barrier and beyond on Wednesday.

EUR/GBP remains supported by the 0.8350 region

EUR/GBP so far leaves behind three consecutive daily retracements, including a monthly peak just shy of 0.8500 the figure on August 12, although the breach of the key 200-day SMA – today at 0.8430 – has opened the door to fresh weakness in the upcoming periods.

The cross thus reverses the initial knee-jerk to the 0.8385/80 band following the bout of strength in the British pound in the wake of the release of UK inflation figures for the month of July.

According to the latter, headline inflation rose 10.1% in the year to July and 0.6% from a month earlier, while the Core CPI also rose above expectations 6.2% over the last twelve months.

The initial reaction post-CPI release saw investors penciling in further (and larger?) rate hikes by the BoE in its next meetings, which in turned morphed into further legs for the quid. However, the latest dovish tilt at the BoE event and the prospects of a 15-month recession in the UK economy warns against sustainable strength in the sterling ahead.

Closer to home, another revision of the EMU Q2 GDP now sees the region’s economy expanding 3.9% YoY.

EUR/GBP key levels

The cross is gaining 0.03% at 0.8409 and faces the next hurdle at 0.8434 (200-day SMA) followed by 0.8492 (monthly high August 12) and then 0.8584 (weekly high July 21). On the flip side, a breach of 0.8386 (weekly low August 17) would expose 0.8339 (monthly low August 2) and finally 0.8249 (monthly low April 14).

In the view of Kit Juckes, Chief Global FX Strategist at Société Générale, EUR/USD is unlikely to break below 0.95. Nonetheless, the pair is set to trade under parity in the coming weeks.

Europe has tapped into global LNG supplies

“The good news, that Europe has tapped into global LNG supplies and is doing a better job of weaning itself off Russian gas, is enough to provide some kind of a cushion for EUR/USD and makes a break below 0.95 less likely now unless the conflict with Russia escalates dramatically.”

“However, the drag of higher prices on European growth seems sure to get EUR/USD below parity for a while in the coming weeks.”

Haitham Al Ghais, the new Secretary-General of the Organization of the Petroleum Exporting Countries (OPEC), said on Wednesday that he doesn't see a major global recession.

Additional quotes

Open to dialogue with the US.

Spare capacity about 2m-3m bpd, running on thin ice.

It is too early to call the outcome of the September 5 meeting.

See the likelihood of an oil-supply squeeze this year.

Market reaction

The WTI recovery from six-month lows of $85.47 gains momentum on these above comments. The US oil erases losses to trade flat at $86.65, as of writing.

- USD/CAD remains supported by USD rebound and falling WTI prices.

- Recession fears continue to dent the market sentiment.

- Bulls look to recapture 50 DMA ahead of the FOMC minutes.

USD/CAD is heading back towards the critical 50-Daily Moving Average (DMA) at 1.2901, having found buyers once again near the 1.2830 region.

In doing so, the major is capitalizing on the renewed weakness in WTI prices amid recession fears, which has dragged the black gold to fresh six-month lows near $85.50.

Additionally, risk-aversion-driven safe-haven flows into the US dollar have also aided the rebound in the major. On Tuesday, USD/CAD incurred sizeable losses after softer Canadian inflation data failed to dissuade the Bank of Canada’s (BOC) commitment to combat inflation. BOC Governor Tiff Macklem said, “our job is not done yet,” adding that “we're determined to eliminate high inflation and return to our 2% target.”

Will the Fed minutes throw a dovish surprise? Investors are eagerly awaiting the Fed July meeting minutes to gain fresh insight on the size of the rate increments in the coming months. The US dollar could potentially see a fresh leg up if the world’s most powerful central bank maintains its hawkish rhetoric in its fight against inflation.

From a short-term technical perspective, USD/CAD is looking to retest the 100 DMA barrier but acceptance above the latter is crucial to initiate a meaningful recovery towards the monthly highs of 1.2985.

Ahead of that bulls will be probed by the 1.2950 psychological hurdle.

The 14-day Relative Strength Index (RSI) is edging higher gradually above the midline, supporting the case for the bullish potential.

USD/CAD: Daily chart