- Phân tích

- Tin tức và các công cụ

- Tin tức thị trường

Tin tức thì trường

- An Inverted Flag formation is strengthening the Swiss franc bulls.

- The 50-period EMA is acting as a major resistance for the counter.

- The RSI (14) has shifted into a 40.00-60.0 range which awaits a potential trigger for volatility expansion.

The USD/CHF pair is oscillating in a narrow range of 0.9650-0.9672 in the Asian session. On a broader note, the asset is oscillating in a 0.9623-0.9732 range from the past four trading sessions after delivering a vertical downside move from a high of 1.0050 recorded last week after the Swiss National Bank (SNB) elevated its interest rates for the first time in the past 15 years. The SNB dictated a 50 basis point (bps) interest rate hike.

The formation of an Inverted Flag chart pattern is indicating more downside after the violation of the inventory re-distribution phase. An inventory re-distribution phase denotes the placement of shorts from those market participants, which prefer to enter a bearish auction after the establishment of a downside bias.

The Swiss franc bulls have defended the 50-period Exponential Moving Average (EMA) at 0.9683. Also, the 200-period EMA is trading above the asset prices at 0.9750, which weakens the greenback bulls.

Meanwhile, the Relative Strength Index (RSI) (14) is oscillating in the 40.00-60.00 range, which supports a consolidation ahead. A downside move below Friday’s low at 0.9619 will drag the asset towards May 27 low at 0.9545, followed by March 16 high at 0.9460.

On the flip side, the greenback bulls could regain control if the major overstep Friday’s high at 0.9733, which will send the asset towards June 9 high at 0.9817. A breach of the latter will drive the asset towards June 14 low at 0.9874.

USD/CHF hourly chart

-637914519474672508.png)

- NZD/USD justifies Tuesday’s Doji formation to pare weekly gains and renews intraday low of late.

- New Zealand Trade Balance widens in May, Export and Imports rise from revised down priors.

- Cautious sentiment ahead of Fed Chair Powell’s Testimony appears to weigh on previously upbeat mood.

- NZ Credit Card Spending for May could offer immediate directions.

NZD/USD refreshes intraday low around 0.6320 as traders consolidate recent gains following New Zealand’s (NZ) downbeat trade data during Wednesday’s Asian session. Also exerting downside pressure on the Kiwi pair is the market’s anxiety ahead of the key Testimony from Fed Chair Jerome Powell.

New Zealand Trade Balance dropped to $263M MoM versus $440M prior (revised from $584M). Further details suggest that the Exports and Imports came in as $6.95B and $6.69B respectively compared to $6.16B and $5.72B revised down previous figures in that order.

Other than the NZ trade data, the mild losses of S&P 500 Futures and two basis points (bps) of a downtick by the US 10-year Treasury yields also portray the market’s cautious mood and weigh on the NZD/USD prices.

That said, the Kiwi pair rose during the last two days amid receding fears of the US recession, mainly propelled by US President Joe Biden and Treasury Secretary Janet Yellen. Wall Street’s jump after witnessing the biggest weekly loss in two years also favored the NZD/USD buyers.

Additionally, downbeat US data added strength to the Kiwi pair as the US Existing Home Sales dropped to the lowest levels in two years when talking the annualized number. On the same line, the Chicago Fed National Activity Index also dropped to 0.01 in May versus a revised down 0.04 prior.

It should be noted that the hawkish Fedspeak probed the NZD/USD bulls. On Tuesday, Richmond Federal Reserve President Thomas Barkin said that there will be no rapid return for the U.S. economy to the experience of the previous decade of stable growth, jobs and inflation, Reuters reported.

To sum up, NZD/USD pair portrays the market’s anxiety as Fed Chair Powell has a tough task to justify the biggest rate hike since 1994 while also balancing the growth optimism. On an immediate basis, NZ Credit Card Spending for May, expected 2.0% versus 1.1% prior, will be important to watch.

Technical analysis

Tuesday’s Doji formation, as well as the sustained trading below the 21-day EMA level of 0.6380, keeps NZD/USD sellers hopeful to visit the yearly low surrounding 0.6200.

- The EUR/JPY is printing gains of 1.53% in the week.

- The sentiment is mixed and remains fragile due to the global economic outlook.

- EUR/JPY Price Forecast: Double top in the daily chart looms.

The EUR/JPY begins the Asian session on the wrong foot, recording decent losses of 0.13% as market sentiment deteriorates with Asian equity futures mixed. In contrast, US stocks and DAX futures start to trade in the red. At the time of writing, the EUR/JPY trades around the 143.80 area.

A mixed market mood threatens to increase appetite for safe-haven peers, meaning the Japanese yen has the upper hand. Wall Street’s skepticism that Tuesday’s rally means that equities reached a bottom opens the door for further losses. Fed speaking continued, led by Thomas Barkin, Richmond’s Fed President, who said that the Fed should raise rates as fast as it can without triggering a recession in the US.

EUR/JPY Price Forecast: Technical outlook

Daily chart

From a technical perspective, the EUR/JPY might nearly form a double top in the 143.80-144.20s area. Also, traders need to take notice of the Relative Strength Index (RSI), which, although it remains in bullish territory, illustrates that the EUR/JPY’s last two higher highs were printed on RSI’s lower peaks, suggesting that buyers were booking profits.

4-hour chart

The EUR/JPY illustrates the cross as upward biased, based on pure market structure; nevertheless, unless it breaks above the June 8 daily high at 144.25, that would leave the pair exposed to selling pressure.

1-hour chart

The EUR/JPY depicts a negative divergence between the cross-currency price action and the Relative Strength Index (RSI), which is within an overbought territory. However, the EUR/JPY might snap higher for a re-test of the YTD highs around 144.25. If the EUR/JPY buyers fail to break above 144.01, a fall towards the June 21 daily low at 142.00.

Therefore, the EUR/JPY first support would be 143.46. Once broken, the next support would be 143.00. A breach of the latter would tumble the EUR/JPY towards 142.00.

- GBP/USD fades upside momentum after two-day advances, retreats of late.

- Sustained trading beyond the key HMAs, bullish RSI formation keep buyers hopeful.

- Short-term triangle restricts immediate moves ahead of UK CPI data for May.

GBP/USD struggles to extend the weekly rebound as bulls take a breather around 1.2275 during Wednesday’s Asian session. In doing so, the cable pair funnels down to the short-term triangle break.

However, the quote’s successful trading above the 100-HMA and 200-HMA, as well as the RSI’s support to the recent higher lows on prices, keeps the pair buyers hopeful.

That said, the latest pullback remains elusive until the quote stays above the 200-HMA support of 1.2230. Before that, the stated triangle’s support line and the 100-HMA may entertain GBP/USD sellers around 1.2265 and 1.2250 respectively.

In a case where the cable pair remains weak past 1.2250, weekly horizontal support near 1.2200 and Friday’s low of 1.2172 should gain the bear’s attention.

Meanwhile, recovery moves need validation from the 1.2310 hurdle, comprising the aforementioned triangle’s resistance line.

Following that, the mid-June swing high of 1.2406 and early month bottom around 1.2430 may rest the GBP/USD pair buyers before directing the run-up towards the monthly peak of 1.2616.

It should be noted that the UK Consumer Price Index (CPI) is likely to increase to 9.1% in May from 9.0%, which in turn suggests more urgency on the part of the Bank of England (BOE) to propel rates. The same could favor the GBP/USD buyers in case of firmer data.

GBP/USD: Hourly chart

Trend: Further upside expected

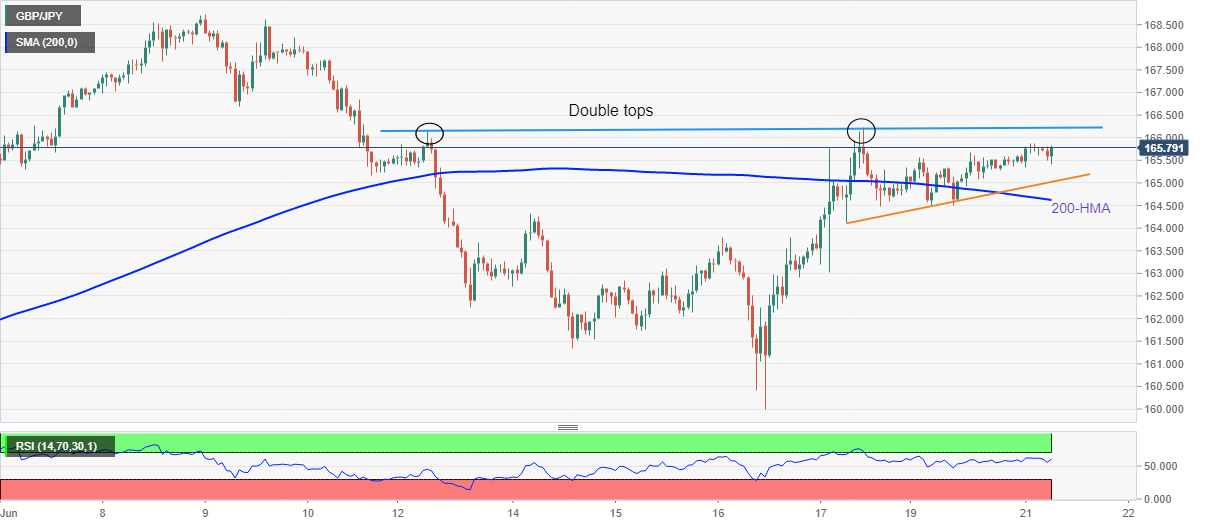

- GBP/JPY has displayed a momentum loss on higher forecasts for the UK Inflation.

- The BOJ minutes will disclose the ideology behind keeping a neutral stance on the interest rates.

- The annual inflation rate of 2.9% in Japan is majorly contributed by soaring oil and food prices.

The GBP/JPY pair has witnessed a steep fall in early Tokyo after exhaustion in the upside momentum kicked in as investors are shifting their focus towards the UK Consumer Price Index (CPI) and minutes of the Bank of Japan (BOJ)’s June monetary policy meeting. Earlier, the cross displayed a sheer upside move to near 167.86 after giving an upside break of Friday’s high at 166.22.

As per the market consensus, the annual UK CPI is seen at 9.1%, marginally higher than the prior print of 9%. In comparison with the Western leaders, the UK economy is seldom operating at a whooping above 9% inflation rate. One could get an idea from that how much the households in the UK would be facing the headwinds of depreciated paychecks.

An annual inflation rate above 9% is sufficient to advance the odds of a recession in an economy. The Bank of England (BOE) is bound to tighten its policy, however, lower growth prospects are not providing much freedom to the central bank. This is restricting the BOE not to thinking beyond a quarter-to-a-percent rate hike as a higher rate elevation will shrink liquidity from the economy at a much more rapid pace.

On the Tokyo front, investors are awaiting the release of the BOJ’s minutes, which will dictate the ideology behind sticking to an ultra-loose monetary policy despite soaring price pressures. Well, one could understand through scrutiny that the inflation rate at 2.9% is highly contributed by expensive fossil fuels and costly food prices. However, the commentary from the BJ on the same would be worth watching.

- EUR/USD remains mildly bid after two-day uptrend, sidelined of late.

- Risk-on mood, hawkish ECBspeak join downbeat US data to underpin bullish bias.

- Powell’s Testimony eyed amid talks over longevity of Fed’s 75 bps rate hike.

EUR/USD holds onto the previous two-day gains around 1.0535-40 during Wednesday’s initial Asian session. The major currency pair’s latest rebound could be linked to the softer US dollar, as well as hawkish comments from the European Central Bank (ECB) policymaker. However, cautious sentiment ahead of Fed Chair Jerome Powell’s Testimony on the bi-annual Monetary Policy Report restricts immediate moves of the quote.

European Central Bank (ECB) Governing Council member Olli Rehn said on Tuesday, “it is very likely that September rate hike is bigger than 25 bps.” His comments raised doubts about the ECB’s latest verdict suggesting a 0.25% rate hike in July and September, which in turn propels the EUR/USD prices.

On the other hand, Richmond Federal Reserve President Thomas Barkin said on Tuesday that there will be no rapid return for the U.S. economy to the experience of the previous decade of stable growth, jobs and inflation, Reuters reported. The policymaker also favored higher rates.

Furthermore, US President Joe Biden’s firm rejection of the recession fears seems to gain the market’s acceptance and underpin the firmer sentiment amid a lack of major negatives as the US traders began the trading week. Following Biden’s comments, his Economic Aide Heather Boushey also conveyed hopes of avoiding the recession. It’s worth noting that US President Biden’s readiness for the gas tax holiday and softer US data also underpinned the positive mood. Additionally, US Treasury Secretary Janet Yellen said that the traditional recession measure of two consecutive quarters of negative growth 'has typically worked' but recessions aren't all alike.

Talking about the data, US Existing Home Sales dropped to the lowest levels in two years when talking the annualized number. Further, the Chicago Fed National Activity Index also dropped to 0.01 in May versus a revised down 0.04 prior.

Against this backdrop, the US Dollar Index (DXY) dropped for the second consecutive day, to 104.40 by the press time whereas Wall Street pared the biggest weekly loss in two years. Further, the US 10-year Treasury yields also rose to 3.27% at the latest.

Looking forward, various ECB policymakers are up for speeches and may entertain EUR/USD traders. However, Powell’s art of defending the tighter monetary policies and the rate hikes will be crucial for the pair traders to watch for clear directions.

Technical analysis

The first daily closing above the 10-DMA, around 1.0500 by the press time, in nearly three weeks enables EUR/USD bulls to aim for early June’s swing low near 1.0630.

- The AUD/JPY remains boosted by a risk-on mood, though sentiment remains fragile.

- AUD/JPY Price Forecast: Negative divergence emerging in the month/weekly chart loom and might open the door for further losses.

The Australian dollar rallied 130 pips vs. the Japanese yen on Tuesday due to the stubbornness of the Bank of Japan (BoJ), which pledged to its ultra-loose monetary policy and is the only central bank in the G8 that showed no intentions of tightening policy in the near term. At 95.06, the AUD/JPY is barely up by 0.01% as the Asian session begins, though, in the last couple of days, it has been gaining 1.50%.

Asian futures are trading in the green, setting cash equity markets for a higher open. Nevertheless, sentiment remains fragile. Although China’s Covid-19 news shows that authorities remain in control, additional lockdowns could shift investors’ mood and drag the AUD/JPY down.

AUD/JPY Price Forecast: Technical outlook

Monthly chart

The AUD/JPY monthly chart shows that the exchange rate approached near the May 2015 highs but retreated 50 pips shy and printed a six-year-highs. Failure at the aforementioned kept the AUD/JPY consolidating and opened the door for a reversal towards the September 2017 highs around 90.30.

Weekly chart

The AUD/JPY weekly chart illustrates the pair as upward biased on pure market structure. Nevertheless, a negative divergence between AUD/JPY’s price action and the Relative Strength Index (RSI) suggests that the cross might be headed downwards. Traders should be aware that, albeit a negative divergence shows, the current price action opens the door for a re-test of May 2015 highs around 97.30.

Daily chart

The AUD/JPY daily chart is still upward biased, though the last two higher highs, being April 20 at 95.74 and June 8 at 96.88, were reached on RSI’s lower highs, meaning that buyers are not committing to lift the AUD/JPY to higher prices, opening the door for a shift in the trend.

Digging a little deep, if the AUD/JPY exchange rate breaks above April’s 20 swing high at 95.74, that would open the door for a test of May’s 2015 high at 97.30. Otherwise, failure to break above the 78.6% Fibonacci retracement alongside RSI’s acceleration downwards might open the door for a fall towards the September 2017 high-turned-support at 90.30.

- AUD/USD seesaws above 0.6950 after two-day rebound, paring Friday’s heavy losses.

- Market sentiment improves amid softer US data, pre-Powell consolidation and Biden’s optimism.

- RBA Minutes, Lowe’s speech added strength to the upside momentum, hawkish Fedspeak fails to propel USD.

- Australia’s Westpac Leading Index may entertain traders, Fed Chair Powell’s testimony is the key catalyst.

AUD/USD dribbles around 0.6970, after paring Friday’s heavy losses in the last two days, as buyers turn cautious ahead of Fed Chair Jerome Powell’s Testimony. However, receding fears of recession and an absence of major negatives, as well as the Reserve Bank of Australia’s (RBA) hawkish bias, keeps the Aussie bulls hopeful during the early hours of Wednesday’s Asian session.

US President Joe Biden’s firm rejection of the recession fears seems to gain the market’s acceptance and underpin the firmer sentiment amid a lack of major negatives as the US traders began the trading week. Following Biden’s comments, his Economic Aide Heather Boushey also conveyed hopes of avoiding the recession. It’s worth noting that US President Biden’s readiness for the gas tax holiday and softer US data also underpinned the positive mood.

On the same line were the recent comments from US Treasury Secretary Janet Yellen who said that the traditional recession measure of two consecutive quarters of negative growth 'has typically worked' but recessions aren't all alike.

That said, the US Existing Home Sales dropped to the lowest levels in two years when talking about the annualized number. Further, the Chicago Fed National Activity Index also dropped to 0.01 in May versus a revised down 0.04 prior.

At home, the RBA Minutes and Governor Philip Lowe both teased higher rates moving forward, while also suggesting the economic strength to avoid the pessimism.

Elsewhere, Richmond Federal Reserve President Thomas Barkin said on Tuesday that there will be no rapid return for the U.S. economy to the experience of the previous decade of stable growth, jobs and inflation, Reuters reported. The policymaker also favored higher rates.

Amid these plays, Wall Street posted the notable gains after the biggest weekly loss in years while the US 10-year Treasury yields also rose to 3.27% at the latest.

Moving on, Australia’s Westpac Leading Index for May, prior -0.15%, can offer immediate directions to the AUD/USD pair. However, major attention will be given to Fed Chair Jerome Powell’s Testimony.

Read: S&P 500 bounces back from oversold, but what’s around the corner?

Technical analysis

AUD/USD grinds inside a 40-pip trading area above 0.6940 comprising the weekly support line and the 10-DMA.

- The greenback bulls are facing barricades at the downward sloping trendline placed from 1.3079.

- A Positive Divergence signals resumption in the dominant trend after a corrective move.

- The RSI (14) is oscillating in a 40.00-60.00 range which indicates a consolidation ahead.

The USD/CAD pair is displaying back and forth moves in a narrow range of 1.2910-1.2922 in the early Tokyo session. Earlier, the greenback bulls witnessed a corrective move after failing to sustain above the 1.3050 on Friday.

On an hourly scale, the major has displayed a Positive Divergence, which indicates a resumption of an uptrend after a corrective move. A Positive Divergence was recorded after the asset made a higher low at around 1.2907 while the momentum oscillator Relative Strength Index (RSI) (14) made a lower low. This dictates an oversold situation in an uptrend which is considered a bargain buy for the market participants. The dotted downward sloping trendline placed from Friday’s high at 1.3079 will act as a major hurdle going forward.

The major is auctioning between the 50- and 200-period Exponential Moving Averages (EMAs) at 1.2952 and 1.2895 respectively, which signals a consolidation ahead.

A decisive move above the 50-period EMA at 1.2952 will trigger the Positive Divergence and eventually will active the greenback bulls for an upside move towards the psychological resistance and Friday’s high at 1.3000 and 1.3079 respectively.

Alternatively, the Positive Divergence formation could negate if the asset drops below Thursday’s low at 1.2861. This will drag the asset towards June 10 high at 1.2813, followed by May 23 low at 1.2766.

USD/CAD hourly chart

-637914474205108793.png)

“I believe there is a path to bringing down inflation while maintaining a strong labor market,” said US Treasury Secretary Janet Yellen per Reuters.

Additional comments

Traditional recession measure of two consecutive quarters of negative growth 'has typically worked' but recessions aren't all alike.

Most economists do not believe the US will enter recession because they are taking into account unique post-pandemic economic features.

To my knowledge, cutting US tariffs on Canadian lumber is not being considered by Biden as part of tariff relief deliberations.

Market reaction

The news fails to gain any major attention from the market during the generally inactive early Asian session. That said, AUD/USD remains sidelined around 0.6970 while the S&P 500 Futures track Wall Street’s gains.

Richmond Federal Reserve President Thomas Barkin said on Tuesday that there will be no rapid return for the U.S. economy to the experience of the previous decade of stable growth, jobs and inflation, Reuters reported.

Key quotes

''We're about two years into a quite unstable time.''

"It seems to me highly unlikely you go from very stable to very volatile to very stable again...continued volatility around some of these economic indicators is a more likely scenario than a return to that kind of stability."

''There could be some months, or even quarters ahead, when inflation readings will oscillate between pre-pandemic levels and higher ones.''

''There also is a real possibility that deglobalization and systemic labor market shortages could cause persistent headwinds to keeping inflation down."That's a risk I am very attuned to."

- Gold price is gauging support around $1,830.00 ahead of Fed Powell.

- Fed Powell may dictate the ideology behind announcing the 75 bps rate hike in June.

- The momentum oscillator RSI (14) is advocating a consolidative move ahead.

Gold prices (XAU/USD) are testing the waters after a strong rebound below $1,830 in the late New York session. The precious metal has displayed a firmer responsive buying action but needs more filters to confirm a bullish reversal. Broadly, a gradual downside move could be named to the recent move in the asset as investors are keeping an eye on Federal Reserve (Fed) chair Jerome Powell’s testimony.

The Fed has already elevated its interest rates by 75 basis points (bps) to 1.50-1.75% officially this month. It would be worth noting the guidance on upcoming monetary policies. Apart from that, Fed Powell in May monetary policy conference dictated that a 75 bps rate hike is not into consideration. In spite of that, Fed Powell went beyond his statement and featured a bumper rate hike. It is important to understand the ideology behind selecting the 75 bps rate hike.

Meanwhile, the US dollar index (DXY) has turned sideways ahead of Fed Powell’s testimony. On Tuesday, the DXY rebounded firmly after hitting the round-level support of 104.00. The 10-year US Treasury yields remained flat on Tuesday at around 3.30%.

Gold technical analysis

The trendline placed from June 16 high at $1,857.40, adjoining Friday’s high at $1,853.04 will act as a major resistance for the gold prices going forward. The precious metal is auctioning below the 21-period Exponential Moving Average (EMA) at $1,835.24, which signals a short-term weakness in the counter. Meanwhile, the Relative Strength Index (RSI) (14) has shifted into a 40.00-60.00 range, which signals a consolidation ahead.

Gold hourly chart

- USD/JPY bears could be about to move in and cap the rally.

- A drop below 136.57 could be the catalyst for a near term run to 136.10 and beyond.

With the divergence between the Bank of Japan and the Federal Reserve, the yen has been crushed to multi-year levels and the following illustrates the prospects of a move even lower according to the monthly structure:

USD/JPY monthly chart

As illustrated, the price is reaching for blue skies mas it clears 2002 levels and eyes the body of the monthly reversal candle from August 1998. The mid point of that candle is as high as 141.86.

USD/JPY weekly chart

However, RSI bearish divergence is playing out on the lower time frames, such as the above weekly chart and below on the daily chart.

A bearish correction could be on the cards:

USD/JPY daily chart

From a daily perspective, the prior lows near 131.50, if broken, will open the risk of a test below 130.00 and 127.00 thereafter, both of which are levels of liquidity and below areas of an imbalance in price.

From an hourly perspective, the is starting to round off. The significant downside prospects will kick in on a break of 136.10 and 135.06 respectively as midpoints of hourly order blocks.

From a 5-min chart's perspective, the price could be on the verge of a break of structure (BoS) of 136.57, resulting in a bearish head and shoulders (H&S) and a significant move to the downside as per the hourly levels identified.

- The NZD/USD remains within familiar levels, though up by 0.12%.

- Worst than expected NZ consumer sentiment, put a lid on the NZD/USD.

- An upbeat market mood kept the greenback on the defensive.

The New Zealand dollar gains some ground vs. the greenback on Tuesday as the New York session begins to wane. The NZD/USD is up by 0.12% after reaching a daily high of around 0.6363 but failed to break resistance near 0.6370, opening the door for a pullback. At the time of writing, the NZD/USD is trading at 0.6336.

NZ Consumer sentiment plunges, though the NZD/USD stayed afloat

A risk-on mood keeps the greenback heavy. US equities are set to finish the day higher, between 2.41% and 2.93%. Meanwhile, the NZD/USD struggled to push higher, courtesy of June’s dismal NZ Consumer confidence, which plummeted to the lowest level on record, falling from 92.1 to 78.7.

“The combination of rising mortgage rates and increases in living costs has already taken a large bite out of disposable incomes. And with interest rates set to rise even further, many households will find the pressure on their finances becoming more intense over the coming months,” Westpac analysts wrote.

In the meantime, the US economic docket featured some Fed officials crossing wires. Thomas Barkin, Richmond’s Fed President, said he decided on 75 bps in June on the University of Michigan (UoM) Consumer sentiment and inflation expectations reports. Furthermore, he added that 50 or 75 bps in July are reasonable and commented that inflation would go down once supply chain issues are resolved.

Earlier, the Chicago Fed National Activity Index for May came at 0.01, the lowest in eight months, trailing April’s 0.40. Of late, US Existing Home Sales dropped by 3.4% to 5.41 million in May 2022, the lowest level since June 2020.

In the week ahead, traders should prepare for Fed Chair Jerome Powell’s appearance at the US Senate Banking Committee, where senators would question him regarding the status of the US economy.

Key Technical Level

What you need to take care of on Wednesday, June 22:

US Federal Reserve chief Jerome Powell will testify before Congress. His pre-prepared remarks will be out ahead of the event. Market players will be looking for hints on future quantitative tightening. Additionally, the UK will post updates on inflation data.

The American dollar edged modestly lower against most major rivals on Tuesday amid a better market mood. The USD/JPY pair, however, soared to a fresh multi-year high of 136.61, holding nearby at the end of the US session. The yen's collapse is mostly due to the Bank of Japan's stubborn commitment to its ultra-loose monetary policy.

Global indexes edged higher, with Wall Street posting substantial gains and limiting demand for safety. US government bond yields ticked higher, but not enough to revive inflation-related concerns.

Meanwhile, central bankers keep hinting at aggressive measures. Bank of England Chief Economist Huw Pill said they would certainly be ready to act if they see evidence of persistent price pressures. Reserve Bank of Australia Governor Philip Lowe opened the door for a 50 bps rate hike in July. Finally, European Central Bank Governing Council member Olli Rehn said it is very likely that the September rate hike would be bigger than the 25 bps planned for July.

The EUR/USD pair trades around 1.0530, little changed on a daily basis. GBP/USD posted a modest advance and now trades around 1.2280. The better tone of equities helped commodity-linked currencies to advance against their American rival. AUD/USD is up to 0.6970, while USD/CAD trades in the 1.2910 price zone.

Gold is battling with the $1,830 level under pressure. Crude oil prices saw little change on Tuesday, with WTI now trading at around $109.50 a barrel.

Like this article? Help us with some feedback by answering this survey:

- GBP/USD is riding a positive wave or risk sentiment.

- The bears will need to see a break of 1.22 the figure whereas bulls have sights on a break of 1.2340.

At 1.2270, GBP/USD is trading on the bid between a low of 1.2239 and 1.2324. The price is currently higher by 0.24% and correcting from last week's dip from 1.24 the figure. Overall, the tone is risk-on and positive for sterling with a softer US dollar despite a focus on higher global rates and central banks.

However, following last week's rout in equities, there has been some bargain hunting on Wall Street in stocks as investors move in on the energy and tech sectors, dragging the benchmarks higher in line with a broader global bid in equities. MSCI's broadest index of Asia-Pacific shares outside Japan rose 1.3%, moving higher from a more than five-week low and set for its best day in around two weeks. Japan's benchmark Nikkei average gained 2.22%.

European shares also closed higher for a second consecutive day on Tuesday. The Stoxx Europe 600 gained 0.35%, London's FTSE 100 added 0.42%, France's CAC rose 0.75% and Germany's DAX edged up by 0.20%. The Swiss Market Index was off 0.06%. On Wall Street, all sectors in stocks are in the green and the Dow Jones Industrial Average jumped is now over 2% higher, with S&P 500 up 2.56% to 3,761 and the Nasdaq Composite 2.8% higher.

The risk-on mood is benefitting sterling as the greenback loses its safe-haven bid, weighed down below the 105 level as per the DXY, an index that measures the greenback vs a basket of currencies. At the time of writing, DXY is trading at 104.41 within a range of 103.938 and 104.536.

With all of the positive action in the markets, the elephant in the room stays with higher risks of a global slowdown, and specifically, UK growth fears will remain a thorn in the side of the pound. Nevertheless, net short GBP positions have dropped back for a third consecutive week in the run-up to the June 13 Bank of England policy meeting. The hawkish tone by some MPC members has been GBP supportive.

The BoE is likely to step up the intensity of its tightening, analysts at ANZ Bank argued. ''MPC member Catherine Mann has noted that demand is strong and that she voted for a 50bp rate rise at last week’s meeting.''

''The BoE has noted that the pace of rate increases may well accelerate in the months ahead as inflation is poised to move to double digits. In sum, central bank hawkishness continues to broaden, and that’s likely to keep risk markets fragile and weigh on global growth prospects in the short to medium term.''

GBP/USD technical analysis

The above bullish scenario identifies the price imbalance between the current resistance, 1.2340, and prior consolidation near 1.25 the figure that occurred before the significant price drop into test 1.19 the figure. On the downside, the bears would be in control on a break of the support zone that consists of both horizontal and dynamic support around 1.2250 and 1.2180. This could lead to mitigation of the price imbalance between 1.2172 and 1.1998:

- A risk-on market mood was no excuse for silver to advance, boosted by a soft US dollar.

- US Treasury yields fell, except for the 10-year TIPS, a headwind for silver prices.

- Silver Price Forecast (XAG/USD): In consolidation in the $21.50-$22.00 range.

Silver (XAG/USD) snaps two consecutive days of losses and edges higher by 0.50% in the mid-North American session as US traders return from a long weekend. At the time of writing, the XAG/USD is trading at $21.70, gaining $0.10.

Global equities are rallying, depicting a risk-on mood. In the meantime, the greenback is almost flat, as illustrated by the US Dollar Index, parked around 104.412, down by 0.01%. The US 10-year Treasury yield ascends three basis points, sitting at 3.298%, failing to drag the white-metal price down.

In the meantime, the US 10-year Treasury Inflation-Protected Securities (TIPS), a proxy for real yields, shifted positive and is yielding 0.696%, up by one basis point, a headwind for precious metals prices.

During the day, XAG/USD reached a daily high of around $21.94, but buyers lacked the strength to challenge the $22.00 figure, last tested on June 13. Consequently, the silver price fell, though it stayed around the $21.70 area.

Data-wise, the US economic docket featured some Fed speaking. Thomas Barkin, Richmond’s Fed President, commented that he decided on 75 bps in June on the University of Michigan (UoM) Consumer sentiment and inflation expectations reports. Furthermore, he added that 50 or 75 bps in July are reasonable and commented that inflation would go down once supply chain issues are resolved.

Earlier, the Chicago Fed National Activity Index for May came at 0.01, the lowest in eight months, trailing April’s 0.40. Of late, US Existing Home Sales dropped by 3.4% to 5.41 million in May 2022, the lowest level since June 2020.

In the week ahead, traders should prepare for Fed Chair Jerome Powell’s appearance at the US Senate Banking Committee, where he will be questioned about the US economy.

Silver Price Forecast (XAG/USD): Technical outlook

XAG/USD illustrates that the non-yielding metal is consolidating, though forming a bullish flag, within the $21.50-$22.00 range. Nevertheless, unless XAG buyers achieve a daily close above $22.00, silver bias will remain headed to the downside. Additionally, a two-month-old downslope trendline passes near the $22.00 figure, which means that any test could find some sellers lying around.

That said, the XAG/USD’s first resistance would be June 16 high at $21.96. Break above would expose the $22.00 mark, followed by the trendline mentioned above near $22.10. On the flip side, the XAG/USD first support would be $21.50. A breach of the latter would expose the May 19 swing low at $21.28, followed by a test of $21.00.

Key Technical Levels

- Gold is grappling with headwinds from either side, but technically, the price is destined lower.

- The bears have moved in following a restest of important resistance on the 4-hour chart.

At $1,833.90, the gold price is trading around flat by mid-day New York trade and has stuck to a $1,830.83 and $1,843.66 range so far in a fickle trading environment. There has been some bargain hunting on Wall Street following last week's sell of in stocks as investors move in on the energy and tech sectors, dragging the benchmarks higher with energy leading the pack.

Gold is failing to benefit from a softer US dollar and risk-on environment as the wider focus stays on the rate hike narrative. Nevertheless, all sectors in stocks are in the green and the Dow Jones Industrial Average jumped is now over 2% higher, with S&P 500 up 2.56% to 3,761 and the Nasdaq Composite 2.8% higher.

However, US 10-year Treasury yields are up over 1% which has dimmed appeal for the yellow metal, coinciding with the Federal Reserve's biggest interest rate hike since 1994 made earlier this month with more of the same expected in July from the US central bank.

Gold prices remain anchored after Chair Jerome Powell tactfully manufactured a sell-the-news rally following a 75bp hike. Additionally, and as analysts at TD Securities pointed out, ''with equity markets trading in bear-market territory, gold offers an attractive less correlated stream of returns than other traditional havens.''

''For the time being, these forces have allowed gold to avoid a large-scale liquidation event, but proprietary traders continue to hold a massive amount of potentially complacent speculative length in the yellow metal. Ultimately, this still leaves the bias to the downside under the weight of a hawkish Fed.''

In this regard, this week's main event will be Fed Chair Powell’s semi-annual monetary policy report to Congress. ''Given the dramatic breakout in inflation, we expect Powell to robustly emphasise the Fed’s inflation credentials in front of lawmakers who face mid-term elections in November,'' analysts at ANZ Bank explained.

Central banks in general are moving in line with the European Central Bank looking to soon move to incremental 50bps moves and the Bank of England singing from the same hymn sheet, seeking to step up the intensity of its tightening.

ECB President Lagarde re-iterated guidance this week that interest rates will rise 25bp in July. Analysts at ANZ Bank noted that the ECB is accelerating work on an anti-fragmentation tool and argue that the latter is ''necessary to enable the ECB to raise interest rates and meet its 2% inflation target over the medium term.''

''We think once the anti-fragmentation tool is designed and adopted, it will pave the way for a more rapid tightening in monetary policy.''

Stronger rate hikes, rising yields and strengthening currencies are a headwind for gold and the sell-off in the equity markets hasn't added any safe-haven demand.

On the other hand, investors are watchful for whether the central banks can balance out the risks of higher rates and stronger currencies vs. the gloomy economic backdrop and increasing supply risks which could ultimately serve to support gold in the longer term. Inflation and economic uncertainties usually spur safe-haven buying of gold but rising interest rates increase the opportunity cost of the non-yielding bullion.

Gold technical analysis

The 4-hour chart above illustrates that the price is starting to melt to the downside following a restest of the M-formation's neckline and a subsequent retest of an order block.

The expectations are bearish with MACD piling up in negative territory which opens the prospects of a move towards the mid-month lows. This is an area of inefficiency from where the price rallied sharply but left behind a price imbalance between there and $1,813 that is vulnerable to mitigation.

The following attempts to illustrate the market structure from a bearish bias more clearly:

- The shared currency extended its gains in the week by 0.42%.

- The US dollar falls courtesy of an upbeat market mood.

- ECB’s Rehn backs a move above 25 bps in the ECB’s September meeting.

- Fed’s Barkin supported a 50/75 bps rate hike in July and said inflation would go down once supply chain issues were resolved.

The EUR/USD climbs for the second consecutive day, though struggled to get near the 1.0600 figure, as sellers dragged the major from daily highs around 1.0582 towards the 1.0530s area during the New York session. At the time of writing, the EUR/USD is trading at 1.0529, registering a decent gain of 0.18%.

A risk-on impulse weighs on the greenback, so the euro rises

Sentiment is positive, as global equities are rallying. As risk appetite increases, safe-haven assets like the US Dollar remain on the defensive. In the meantime, on Monday, the ECB President Lagarde affirmed that the central bank would lift rates in July and remained flexible about the size of the rate hike in September.

Although Lagarde’s comments lifted the EUR/USD near the 1.0600 figure, buyers lacked the strength to push the major above it, and it fell. The interest rate differential between the ECB and the Fed would likely favor the greenback, which is almost flat, as shown by the US Dollar Index.

Additionally to Lagarde’s commentary, the ECB Chief Economist Philip Lane said that he does not see the need to revisit the plan after July’s decision on the rate increase and added that there is no preview beyond September of what will be the appropriate pace of tightening.

On Tuesday, ECB’s Rehn, one of the hawks of the central bank, said that inflation in the EU has broadened and remains stronger and added he backs up a rate increase of more than 25 bps in September.

Elsewhere, Fed speakers had been unleashed and are crossing wires. The Richmond Fed President Thomas Barkin said that the Fed would have to restrict monetary policy, but the question is how much. He emphasized that the Fed needs to be flexible and commented that after the UoM survey, he felt it was possible to go 75 bps.

Barkin added that 50 or 75 bps in July are reasonable and commented that inflation would go down once supply chain issues are resolved.

In the meantime, the US economic docket featured the Chicago Fed National Activity Index, which went down to an eight-month low of 0.01 in May from 0.40 in April. Later, Existing US Home Sales declined by 3.4% to 5.41 million in May 2022, the lowest level since June 2020.

Key Technical Levels

On Wednesday, inflation data from Canada will be released. Market consensus sees a 1% increase in the Consumer Price Index. Analysts at TD Securities expect a 0.9% increase fueled by gasoline and food prices. They consider declines in USD/CAD are likely hard to sustain.

Key Quotes:

“We look for CPI to strengthen to 7.2% y/y in May, fueled by another large contribution from gasoline and food prices. Core components should also see another strong gain, led by shelter and airfares/travel services. The BoC's core measures should firm by 0.1pp on average (to 4.3%) and we do not anticipate a significant impact from new basket weights.”

“Despite inflation, the BOC (Bank of Canada) will struggle to keep up with the Fed on tightening. Dips in USD/CAD are likely hard to sustain, especially as the impact of higher rates begins to filter into the data in the coming weeks. 1.2860/00 key support and 1.3080 notable resistance in USD/CAD.”

According to the Research Department at BBVA, Treasury yields are likely to rise further, peaking at the time when the Federal Reserve end with tightening monetary policy. They point out current Treasury yield spreads seem to continue to price in a soft landing.

Key Quotes:

“Slowing demand to bring down inflation without significant pain is “not getting any easier”; markets (still?) price in a soft landing.”

“With the Fed set to hike rates to a “modestly restrictive level” by year-end, the tightening pace is already faster than the one seen in the 1994-95 hiking cycle.”

“Market-based inflation expectations point to continued confidence that, over the longer term, the Fed will be able to bring down inflation to the 2.0% target.”

“Futures markets are currently pricing that the fed funds rate will peak above 3.5% in mid-2023 which is broadly in line with the updated fed funds rates central tendency FOMC projections.”

“With a flat yield curve ahead, we expect both 2-and 10-year yields to keep moving in sync, while shorter-term Treasury yields continue to catch up, driven by upcoming Fed hikes.”

- The AUD/USD is upward biased in the near term, boosted by RBA’s Lowe, saying that a 25-50 bps increase in the July meeting is on the cards.

- Fed’s Barkin backed a 75 bps rate hike in the July meeting.

- AUD/USD Price Forecast: Buyers struggling at 0.7000 might open the door for a fall to the 0.6900 mark.

AUD/USD edges up after beginning the week on the wrong foot, jumping from 0.6915 daily lows towards 0.6990 highs, closing to the 0.7000 threshold. At 0.6969, the AUD/USD reflects an upbeat market mood, portrayed by European and US equities recording robust gains on Tuesday.

RBA's Lowe boosts the AUD/USD

Sentiment stays positive once US traders return from a long weekend due to a holiday. The AUD/USD got a boost since the Asian session when the Reserve Bank of Australia (RBA) Governor Philip Lowe stated that rates were still “very low for an economy with low unemployment and that is experiencing high inflation.”

Lowe added that price pressures would continue building up and expects local inflation to reach 7% by the end of the year. He forward guided traders, saying that at the July 5 meeting, they would expect 50 or 25 bps by that meeting.

In the meantime, Fed speakers continue to dominate the headlines. Richmond’s Fed President Thomas Barkin said that the Fed would have to restrict monetary policy, but the question is how much. He emphasized that the Fed needs to be flexible and commented that after the UoM survey, he felt it was possible to go 75 bps.

Barkin added that 50 or 75 bps in July are reasonable and commented that inflation would go down once supply chain issues are resolved.

Data-wise, the US economic docket featured the Chicago Fed National Activity Index, which went down to an eight-month low of 0.01 in May from 0.40 in April. Later, Existing US Home Sales declined by 3.4% to 5.41 million in May 2022, the lowest level since June 2020.

AUD/USD Price Forecast: Technical outlook

The AUD/USD continues to push towards the 0.7000 figure but failed to reclaim the threshold since Monday. Tuesday’s daily high, at 0.6993, fell shy of reaching the figure and was followed by a dip towards the 0.6960 area. Traders should be aware that zooming into the 1-hour chart, the AUD/USD 200-hour simple moving average (SMA) is acting as dynamic support, and was the reason AUD buyers failed to reclaim 0.7000.

The AUD/USD 1-hour chart depicts the pair as upward biased but consolidating in the 0.6960-90 area. That said, the AUD/USD first resistance would be the R1 daily pivot at 0.6990. Break above would expose the R2 daily pivot at 0.7030, followed by last week’s daily high at 0.7069. On the flip side, the major’s first support would be the daily pivot at 0.6950. A breach of the latter would expose additional support levels like the S1 pivot at 0.6910, followed by the 0.6900 figure.

Data released on Tuesday showed retail sales in Canada rose 0.9% on April, surpassing expectations, even as March’s figures were revised higher. According to analysts at the National Bank of Canada expect retail sales to moderate amid price increases and higher interest rates.

Key Quotes:

“Consumer expenditures on goods came out a little better than expected. In addition, the prior month was upwardly revised. The monthly print was held back again by motor vehicle/part dealers as lack of supply remains characteristic. Nonetheless, core retail sales (which excludes gas and autos) rose 1.0%, marking a fourth consecutive monthly increase.”

“Retail sales were driven up in part by outsized gains in general merchandise and miscellaneous stores, which increased at their fastest pace in 10 and 14 months respectively. Perhaps the most surprising element of the report was volume retail sales which rose 0.9% in the month, suggesting a negligible price effect in the month.”

“The Statistics Canada preliminary estimate for May suggest a 1.6% increase in nominal sales. For the following months, we expect retail sales to moderate in an environment where consumers are being hit by both price increases and higher interest rates. Fortunately, the labour market remains strong, and the still high savings rate should allow consumption to continue to expand.”

The Bank of France announced on Tuesday that it cut the growth forecast for 2022 to 2.3% from 3.4%. In 2023, the central bank expects the French economy to expand by 1.2%, compared to 2% in its previous forecast.

The Bank of France raised its inflation outlook to 5.6% in 2022 and to 3.4% in 2023, from 3.7% and 1.9%, respectively.

Market reaction

EUR/USD lost its traction and erased a portion of its daily gains after this report. As of writing, the pair was trading at 1.0530, where it was still up 0.2% on a daily basis.

- USD/MXN drops for the third day, amid an improvement in market sentiment.

- Negative bias while under 20.25, next support at 20.05.

- Key resistance at the 200-day SMA at 20.42.

The USD/MXN is falling for the third consecutive day. It bottomed at 20.13, the lowest level in a week. It is hovering around 20.19, off lows. The break under 20.00 triggered more losses.

Technical indicators in the daily chart show the RSI and Momentum moving south, supporting a negative bias in the very short-term. If USD/MXN remains under 20.25, the doors for a slide to 20.05 will remain open.

A rebound back above 20.25 would alleviate the bearish pressure. The next key level is the 200-day Simple Moving Average awaits near 20.42. If it continues to rise, attention would turn again to the 20.70 area.

Last week the 20.70 zone capped the upside. A break higher would clear the way for a test of a downtrend line at 20.80. Above a visit to 21.00 and more seems likely.

USD/MXN daily chart

-637914251129102248.png)

"We need to raise rates as fast as feasible but you don't want to break things," Federal Reserve Bank of Richmond President Thomas Barkin said on Tuesday, as reported by Reuters.

Additional takeaways

"Goods demand should come back to something like normal."

"Services inflation interacts a lot with labor market."

If inflation keeps escalating, not much reason to stop raising rates."

"Our difficult task is there could be a couple of strong inflation readings interspersed with weak ones."

"I ask myself if we have real rates where we need them to have impact on the US economy we need to."

"Urgency is high on getting inflation down."

"Hard to put a timetable on when inflation will get back to 2%."

"Tweaking balance sheet reduction could be sensible but it's down the road."

"I am still sceptical on the need for central bank digital currency."

Market reaction

The US Dollar Index recovered modestly after these comments and was last seen posting small daily losses at 104.30.

- US dollar posts mixed results on Tuesday.

- Stocks rise sharply in Wall Street.

- GBP/USD holds a positive very-short term bias, but limited while under 1.2300.

The GBP/USD is rising for the second day in a row, supported by a decline of the US dollar across the board amid risk appetite. The pair peaked at 1.2323 and then pulled back after being unable to hold above 1.2300.

Cable’s slide eventually found support around the 1.2250 area and then bounced back to the upside, unable to recover 1.2300. It is hovering around 1.2270/80, up 30 pips for the day.

The US dollar is mostly lower on Tuesday as stocks rise. After the worst week in years, US indices are rising sharply with the S&P 500 up 2.52% and the Nasdaq making gains of 3.15%. US yields are marginally higher, with the US 10-year at 3.28% and the 30-year at 3.35%.

Economic data released on Tuesday in the US, showed Existing Home sales prices reached a record high in May of $407.600. The annual rate of sales declined from 5.6 to 5.41 million. It was the fourth monthly decline in a row. On Wednesday, Fed Chair Powell will deliver the semiannual testimony at Congress.

In the UK, rail workers are holding a 24-hour strike, the biggest in more than 30 years. The union rejected the latest offer from companies. The Bank of England is expected to continue to raise the key interest rate to curb inflation.

Huw Pill, Chief Economist at the BoE said the central bank is prepared to sacrifice growth to fight against inflation. “While that may seem like an obvious statement, the bank is doing a better job of addressing the tradeoffs involved than it did earlier this year, when it seemed reluctant to hike rates. Pill added that the bank was prepared to act “more aggressively.” Of note, Saunders, Mann, and Haskel dissented last week in favor of a larger 50 bp move. We suspect that 6-3 vote has already shifted to at least 5-4 in favor of a 50 bp hike at the next meeting”, explained analysts at BBH.

Technical levels

Federal Reserve Bank of Richmond President Thomas Barkin said on Tuesday that he will remain focused on actual inflation and expectations between now and the July policy meeting, as reported by Reuters.

Additional takeaways

"I supported 75 bps rate hike at June meeting."

"Inflation is high and broad-based."

"We want to get back to 2% goal as fast as we can without breaking anything."

"After Michigan survey, I felt it was possible to do a 75 bps hike."

"It was a pronounced increase in inflation last month."

"I am also watching signals on the demand side."

"I was in agreement with Powell's comments at the press conference."

"I want positive forward-looking real rates across the curve."

"You have to be flexible."

"Very hard to parse the impact of balance sheet reduction."

"Economy is normalizing."

"Lot of pressures caused by reaction to pandemic such as supply chain issues are going to settle, that will bring down pressures on inflation."

"We are going to have to restrict monetary policy, question is how much."

"We'll see how much as we get into it."

Market reaction

These comments don't seem to be having a noticeable impact on the dollar's performance against its rivals. As of writing, the US Dollar Index was down 0.13% on the day at 104.27.

German Economy Minister Robert Habeck said on Tuesday that the reduced gas supply had "another dimension" and that it was an economic attack by Russia against Germany, as reported by Reuters.

Habeck further argued that the gas supply situation could become worse than the coronavirus pandemic.

Market reaction

These comments don't seem to be having a noticeable impact on the shared currency's performance against its major rivals. As of writing, the EUR/USD pair was trading at 1.0565, where it was up 0.53% on a daily basis.

- US stocks jumped following a US bank holiday, up between 1.78% and 3.07%.

- The Nasdaq Composite leads the pack, followed by the S&P 500 and the Dow Jones.

- US Treasury yields edge up while the US Dollar Index drops.

US stocks are opening with hefty gains, following a dismal week, which dragged the SP 500 officially to a bear market after plunging more than 20% from all-time-highs, but as North American traders returned from a long weekend, US equities depict an upbeat market mood.

The S&P 500 is gaining some 2.51%, trading at 3,766.49, while the tech-heavy Nasdaq Composite (NDQ) is back above the 11,000 threshold, rallying 3.07%, at 11,130.10. The laggard in the session, but jumping more than 500 points, is the Dow Jones Industrial Average (DJIA), up 1.78%, advancing to 30,419.48.

In the meantime, the US Dollar Index extends its losses in the week and sits around 104.290, down by 0.11%. US Treasury yields remain elevated, and the US 10-year note yields 3.288%, up by two basis points.

Fundamentally nothing has changed, and some financial analysts perceive the rally as a “death cat bounce.” Last Wednesday, the US Federal Reserve hiked 75 bps rates, the biggest move since 1994, and Fed’s Chief Powell said that although those moves would not be “common,” he stated that in July, another 75 bps might be on the table.

Sector-wise, the leading gainers are Energy, up 4.85%, followed by Consumer Discretionary and Technology, each recording gains of 3.42% and 2.91%, respectively. The laggards but also positive in the day are Utilities, Consumer Staples, and Materials, up by 1.27%, 1.40%, and 1.60% each.

In the commodities complex, the US crude oil benchmark, WTI, grinds higher by 2.69%, trading at $110.88 BPD. At the same time, precious metals like gold (XAU/USD) followed suit, edging higher 0.29%, exchanging hands at $1845.65 a troy ounce.

SP 500 Chart

Key Technical Levels

- Existing Home Sales in US fell more than expected in May.

- US Dollar Index holds above 104.00 after the data.

Existing Home Sales in the United States declined by 3.4% to a seasonally adjusted annual rate of 5.41 million in May, the data published by the National Association of Realtors (NAR) showed on Tuesday. This reading came in worse than the market expectation for a decline of 0.2%.

"At $407,600, the median existing-home sales price exceeded $400,000 for the first time and represents a 14.8% increase from one year ago," the monthly publication further read. "The inventory of unsold existing homes rose to 1.16 million by the end of May, or the equivalent of 2.6 months at the current monthly sales pace."

Market reaction

The US Dollar Index largely ignored this data and was last seen losing 0.15% on the day at 104.25.

- USD/CAD witnessed some follow-through selling for the second straight day on Tuesday.

- Rising oil prices, upbeat Canadian data underpinned the loonie and exerted pressure.

- Rallying US bond yields acted as a tailwind for the USD and helped limit deeper losses.

The USD/CAD pair managed to find decent support near the 1.2900 mark on Tuesday and trimmed a part of its heavy intraday losses. The pair was seen trading around the 1.2935-1.2940 region during the early North American session, still down nearly 0.30% for the day.

Worries about tightening global supplies allowed crude oil prices to regain positive traction and move away from a one-month low, which, in turn, underpinned the commodity-linked loonie. The Canadian dollar drew additional support from upbeat domestic data, showing that Retail Sales recorded growth of 0.9% in April as against the previous month's upwardly revised reading of 0.2%. Excluding autos, core retail sales rose 1.3% during the reported month versus 0.6% anticipated.

That said, the emergence of some US dollar dip-buying offered some support to the USD/CAD pair. Expectations that the Fed would retain its aggressive policy tightening stance, along with the risk-on impulse, pushed the US Treasury bond yields higher. This, in turn, acted as a tailwind for the buck and helped limit deeper losses for the major. Spot prices, for now, seem to have stalled the recent pullback from the YTD peak, around the 1.3080 region touched last Friday.

It, however, remains to be seen if the USD/CAD pair is able to attract fresh buying as the focus now shifts to the latest Canadian consumer inflation figures, due for release on Wednesday. Investors will further take cues from Fed Chair Jerome Powell's two-day congressional testimony before placing directional bets. In the meantime, the broader risk sentiment and the US bond yields might influence the USD, which, along with oil price dynamics could provide some impetus to the pair.

Technical levels to watch

Senior Economist at UOB Group Alvin Liew and Rates Strategist Victor Yong review the latest FOMC event (June 15).

Key Takeaways

“The 14/15 Jun 2022 FOMC was hawkish as the Fed accelerated its rate hike cycle by lifting the policy Fed Funds Target rate (FFTR) by 75bps to 1.50-1.75%, and it signaled clearly that ongoing rate hikes will be appropriate with its focus on reining in inflation. This was the biggest rate hike and only the second time the Fed hiked by 75bps, since 1994. But FOMC Chair Powell’s comments in his press conference was less hawkish as he reiterated that the US economy is well-positioned to deal with higher rates and assured markets that a 75bps hike is not a “common” occurrence.”

“The other key focus was the latest Dot-plot chart which showed FOMC policymakers pivoting to an even faster pace of tightening as they now gravitate towards the view of the Fed policy rate at 3.4% by end 2022 (markedly higher from 1.9% in Mar 2022 FOMC) which implies at least three more 50bps and one 25bps rate hikes in the remaining 4 FOMC meetings in 2022 (i.e. Jul, Sep, Nov and Dec).”

“Reflecting the Fed’s underestimations about inflation, the headline PCE inflation forecasts were again adjusted materially higher to 5.2% for 2022 (from 4.3% in Mar FOMC). But it was growth revisions that caught the attention, as 2022 GDP growth outlook has been revised markedly lower to 1.7% (from 2.8% made in Mar FOMC) and growth will remain low at 1.7% in 2023 (from 2.2% in Mar FOMC), both below trend growth. Unemployment was also not spared in the latest report, likely reflecting the negative impact of the Fed’s accelerated rate hikes on the US labor market situation, with jobless rate exceeding 4% by 2024.”

“FOMC Outlook – Even Higher, CPI inflation the key determinant: Powell clearly highlighted the importance of headline CPI inflation to inflation expectations (and by that extension, to Fed policy). We will mark the Jun CPI (due on 13 Jul 2022, 8:30pm SGT) as the key determinant of whether we get a 50bps or 75bps hike for the next FOMC on 26/27 Jul. Currently, we are projecting US CPI inflation coming in at 0.8% m/m, 8.4% y/y in Jun (from 1% m/m, 8.6% y/y in May). Thus, inflation is still elevated and accelerating sequentially but the headline print will be off its peak (i.e. lower at 8.4% versus 8.6%), so that will warrant a 50bps hike for July, in our view. However, if inflation accelerates more than 0.8% m/m, and prints above 8.6% y/y for Jun, then that will mean a stronger response from the Fed is required, i.e. 75bps.”

“In addition to the move in Jul, we expect another two more 50bps rate hikes in Sep and Nov FOMC before ending the year with a 25bps hike in Dec. Including the 150bps of hikes to date, this implies a cumulative 325bps of increases in 2022, bringing the FFTR higher to the range of 3.25-3.50% by end of 2022, a range largely viewed as above the neutral stance (which is seen as 2.25-2.50%, the Fed’s long run projection of FFTR). We maintain our forecast for two more 25bps rate hikes in 2023, but likely to be brought forward to the first three months of 2023, bringing our terminal FFTR to 3.75-4.00% by end 1Q-2023.”

“Rates Outlook: Overall, the message from Jun’s FOMC has not changed our cyclical market views on the yield curvature and the SG versus US yield spreads. We continue to see the upside potential being capped on both (i.e. curve steepening and SG discount narrowing) in the near term. The updated Jun Dot plot was shifted higher, and the gap between peak FF and long-term neutral FF was widened. This was in line with what we had laid out in our May Monthly FX + Rates report. On the back of our US macro team’s FF forecast update, we recalibrate out end 2022 10Y UST forecast to 3.80% and see increases in the bond yield tapering off into 2023.”

- USD/TRY advances to new peaks north of 17.00.

- The lira depreciates more than 30% so far this year.

- The CBRT meets later in the week to decide on rates.

The Turkish lira sinks to new lows vs. the greenback and pushes USD/TRY to new highs for the year around 17.3500 on Tuesday.

USD/TRY stronger ahead of CBRT event

The selling pressure around the Turkish currency picks up pace on Tuesday and motivates USD/TRY to add to gains recorded at the beginning of the week further north of the 17.00 mark.

The move higher in spot comes despite the offered stance in the greenback and follows usual concerns around the lira and the inability of the government and/or the Turkish central bank (CBRT) to tackle inflation and somehow restore some credibility to the beleaguered currency.

On the latter, the CBRT meets on Thursday amidst consensus for another “on hold” decision despite inflation ran at more than 70% from a year earlier in May.

Furthermore, the lira has depreciated more than 30% and remains the worst EM performer so far this year. It is worth recalling that the currency lost 44% vs. the US dollar in 2021.

What to look for around TRY

USD/TRY keeps the underlying upside bias well and sound and now surpasses the 17.00 mark, an area last traded back in December 2021.

So far, price action in the Turkish currency is expected to gyrate around the performance of energy prices, the broad risk appetite trends, the Fed’s rate path and the developments from the war in Ukraine.

Extra risks facing TRY also come from the domestic backyard, as inflation gives no signs of abating, real interest rates remain entrenched in negative figures and the political pressure to keep the CBRT biased towards low interest rates remain omnipresent.

Key events in Turkey this week: Consumer Confidence (Wednesday) - CBRT interest rate decision (Thursday) – Capacity Utilization, Manufacturing Confidence (Friday).

Eminent issues on the back boiler: FX intervention by the CBRT. Progress (or lack of it) of the government’s new scheme oriented to support the lira via protected time deposits. Constant government pressure on the CBRT vs. bank’s credibility/independence. Bouts of geopolitical concerns. Structural reforms. Upcoming Presidential/Parliamentary elections.

USD/TRY key levels

So far, the pair is gaining 0.16% at 17.3433 and faces the next up barrier at 17.3499 (2022 high June 21) seconded by 18.2582 (all-time high December 20) and then 19.00 (round level). On the flip side, a breach of 16.3136 (monthly low June 3) would aim to 16.1431 (low May 27) and finally 15.6684 (low May 23).

GBP/USD gained past 1.23 before paring gains. Economists at Scotiabank expect the pair to challenge again the big figure.

Support aligns at the mid-1.22s

“The GBP is still holding relatively close to the 1.23 area and is likely to make another push above it while it holds a bullish trend from its mid-May lows.”

“Support is the mid-1.22s followed by ~1.2225 and the big figure.”

“Resistance past the daily high of 1.2324 is 1.2340/50.”

EUR/USD pushes higher. However, as markets are already positioned for a hawkish European Central Bank (ECB), the shared currency is unlikely to enjoy further gains, economists at Scotiabank report.

Strong PMI data out on Thursday could give the EUR a near-term push

“With markets already positioned for a more aggressive hiking schedule for the ECB, we spot limited immediate tailwinds for the EUR – particularly as a big hike is still two months away.”

“Strong PMI data out on Thursday could give the EUR a near-term push to extend its recovery since mid-May.”

The oil market is focused on supply constraints, so prices are likely to remain elevated. Strategists at Société Générale forecast the black gold at $130 in Q3 and $120 in Q4.

Oil prices could drop to $75-80 in a recession scenario

“With the oil industry underinvested and demand returning to normal, we expect oil prices to remain elevated: $130/bbl in Q3 and $120/bbl in Q4, with an upside risk to $150/bbl.”

“If the upside risk scenario materialises (on further supply disruption or OPEC failing to meet its production target), the subsequent demand destruction may not lead to the same downward trajectory as in 2008 (in a recession scenario, prices could drop to $75-80/bbl). The reason is the underinvestment in both upstream and downstream operations and the lack of refining capacity.”

Strategists at Société Générale do not expect to see a supply deficit in the copper market. Therefore, the metal is set to move downward over the coming months.

Copper’s long-term outlook is firmly bullish

“There is no such deficit in the copper market, where the SG Commodities strategy team sees both medium-term supply and demand being bearish.”

“Prices should remain on a downward trend over a 12-month investment horizon ($9,000/t forecasted by the end of the year and $8,500 by 2Q23), as strong mine supply floods the copper market.”

“The longer-term outlook is firmly bullish with the take-off of green transition consumption and an inexorable decrease in copper ore grade.”

AUD/USD gained traction on Tuesday and climbed toward 0.70. Economists at Rabobank expect the pair to edge higher towards the 0.73 by end-2022-

GBP/AUD to move towards the 1.73 area

“We expect AUD/USD can creep higher on a 12-month view based on Australia’s relatively sound economic outlook. However, the aussie is likely to be sensitive to risks regarding Chinese economic output and to broader concerns regarding slowing global growth.”

“We expect AUD/USD to hold close to current levels on a one-month view and rise moderately to the 0.73 area by year-end.”

“We would prefer to buy AUD vs. GBP and see scope for another move to the GBP/AUD 1.73 area.”

The S&P 500 posted its worst week since 2020. The index could tumble as low as 2525 on a 70’s stagflation backdrop, economists at Société Générale report.

S&P 500 may go to 3300 before bouncing back later in the year

“Our downbeat thesis for US Equities reflects the following factors: a) Fed hikes are taking place in a slowing growth environment, and b) we have never seen hikes and quantitative tightening in the same year.”

“We see S&P 500 fair value at 3850 points, with a volatile profile. The index may go to 3300 before bouncing back later in the year.”

“We do not factor in a recession or stagflation as a base case, but a typical recession would lead the S&P 500 down to 3200 while a 70’s style stagflation backdrop could push the index to 2525.”

- USD/JPY gained strong positive traction on Tuesday and rallied to its highest level since 1998.

- The Fed-BoJ policy divergence, the risk-on impulse weighed on the JPY and extended support.

- Weaker USD might hold back bulls from placing fresh bets amid slightly overbought conditions.

The USD/JPY pair caught aggressive bids on Tuesday and surged past the 136.00 mark, hitting its highest level since October 1998 during the early North American session. The pair was last seen trading around the 136.25 region, up over 0.85% for the day.

The Japanese yen has been the worst-performing G10 currency since March amid the ultra-loose monetary policy stance adopted by the Bank of Japan. This has resulted in a further widening of the Japan-US interest rate differential. Apart from this, the strong rally in the global equity markets weighed heavily on the safe-haven Japanese yen and acted as a tailwind for the USD/JPY pair.

The risk-on impulse, along with expectations that the Fed would retain its aggressive policy tightening stance, pushed the US Treasury bond yields higher. This was seen as another factor that impressed bullish traders and provided an additional lift to the USD/JPY pair. The strong move up could also be attributed to some technical buying above the 135.50-135.60 double-top resistance.

Furthermore, oscillators on the daily chart are hovering near the overbought territory. This, in turn, warrants caution before placing fresh bullish bets amid modest US dollar weakness. Hence, a subsequent move up is likely to confront resistance near a two-week-old ascending trend-line, currently around mid-136.00s. Nevertheless, the USD/JPY pair now seems to have confirmed a fresh bullish breakout and any meaningful corrective pullback could be seen as a buying opportunity.

Technical levels to watch

Gold remains anchored near $1,850. In the view of strategists at TD Securities the bias is still skewed to the downside under the weight of a hawkish Federal Reserve.

Risk assets attempt to stage a relief rally

“While trend followers are forced to buy their length back at higher prices, this flow is likely being met with a reversal in safe-haven length as risk assets attempt to stage a relief rally.”

“Looking forward, higher rates should again force prices and long exposure in gold lower.”

Bond yields have picked up significantly over the past month. In the view of economists at Danske Bank, yields are set to tick up further but recession fears will likely dominate over time.

Yields still likely to increase

“We forecast the US economy to tip into a mild recession in 2023. While we expect inflation – not least, underlying inflation – to remain high next year, weaker US growth indicators will likely tend to push yields down although central banks will probably not cut short rates as early as in 2023.”

“We now expect the US 10Y Treasury yields to climb to 3.75% in the course of the next three months. We previously expected an increase to 3.5% in six months.”

- Gold struggled to gain any meaningful traction and remained confined in a range below 200-DMA.

- Broad-based USD weakness offered support to the metal and helped limit any meaningful downfall.

- The risk-on impulse, rising US bond yields continued acting as a headwind and capped the upside.

Gold reversed an intraday dip to the $1,830 area, or a three-day low, though struggled to capitalize on the attempted recovery and remained below the very important 200-day SMA. Having seesawed between tepid gains/minor losses, the XAUUSD now seems to have stabilized in neutral territory and was seen trading below the $1,840 level during the early North American session.

Signs that there will not be any consensus for a 100 bps Fed rate hike move in the foreseeable future prompted fresh selling around the US dollar on Tuesday. This, in turn, was seen as a key factor that extended some support to the dollar-denominated commodity. That said, a combination of factors held back traders from placing aggressive bullish bets around gold.

The risk-on impulse - as depicted by the strong rally in the global equity markets - kept a lid on any meaningful upside for the safe-haven XAUUSD. Apart from this, expectations that the Fed would retain its aggressive policy tightening stance, pushed the US Treasury bond yields higher. This further acted as a headwind for the non-yielding gold.

The two-way/directionless price move witnessed since Monday points to indecision among traders over the next leg of a directional move for the XAUUSD. That said, the recent breakdown through a multi-week-old trading range and acceptance below a technically significant moving average (200-DMA) favours bearish traders and supports prospects for further losses.

Hence, any meaningful upside could be seen as a selling opportunity and runs the risk of fizzling out rather quickly. Traders, however, might refrain from placing aggressive bets ahead of Fed Chair Jerome Powell's testimony on Wednesday and Thursday. In the meantime, the broader risk sentiment, the US bond yields and the USD price dynamics might provide some impetus to gold.

Technical levels to watch

- Chicago Fed's National Activity Index edged lower in May.

- US Dollar Index trades with modest losses below 104.50.

The Federal Reserve Bank of Chicago's National Activity Index fell to 0.01 in May from 0.4 (revised from 0.47) in April. This data shows that the US economy expanded at its historical average in May.

"The CFNAI Diffusion Index, which is also a three-month moving average, moved down to +0.27 in May from +0.39 in April.," the Chicago Fed further noted in its publication. "Forty-seven of the 85 individual indicators made positive contributions to the CFNAI in May, while 38 made negative contributions."

Market reaction

This report doesn't seem to be having a noticeable impact on the dollar's performance against its rivals. As of writing, the US Dollar Index was down 0.15% on the day at 104.25.

- Retail Sales in Canada rose more than expected in April.

- USD/CAD trades in negative territory below 1.2950 after the data.

The monthly data published by Statistics Canada showed on Tuesday that Retail Sales in Canada rose by 0.9% in April to C$60.72 billion. This print came in better than the market expectation for an increase of 0.8% and followed March's expansion of 0.2% (revised from 0%).

The publication further revealed that Retail Sales are expected to grow by 1.6% in May.

Market reaction

With the initial reaction, the USD/CAD pair edged lower and was last seen losing 0.32% on a daily basis at 1.2938.

S&P 500 has fallen to channel support from April at 3637/33. Analysts at Credit Suisse look for this to hold for a temporary consolidation/recovery phase to emerge that could potentially extend into the 3838/3900 mid-June price gap.

A temporary and corrective consolidation/recovery phase can emerge

“Resistance is seen moving to 3728 initially, above which can add weight to our view for a recovery back to the top of the price gap from last Wednesday/Thursday at 3783/90, potentially into the more important mid-June price gap at 3838/3900. We look for this to then prove a major barrier for an eventual resumption of the core downtrend.”

“Below 3633 can see support next at the lower end of the downtrend channel, today seen at 3620, with our core support/objective still at the 50% retracement at 3505, also the location of the 200-week average.”

- Silver gained some positive traction on Tuesday, though lacked any follow-through.

- Bulls seem struggling to make it through the 200-period SMA on the 4-hour chart.

- The neutral technical setup warrants caution before placing fresh directional bets.

Silver attracted fresh buying near the mid-$21.00s region on Tuesday and inched back closer to the previous day's swing high during the first half of the European session. The white metal was last seen trading around the $21.65 region, up nearly 0.50% for the day.

Looking at the broader picture, the XAG/USD has been oscillating in a familiar range over the past four sessions and continued with its struggle to make it through the 200-period SMA on the 4-hour chart. The said barrier, currently around the $21.80 area, is closely followed by the $21-90-$22.00 supply zone, which should act as a pivotal point.

Meanwhile, technical indicators on hourly/daily charts, so far, have struggled to gain any meaningful traction and warrant caution before placing aggressive directional bets. This further makes it prudent to wait for a sustained move in either direction before traders start positioning for a firm near-term trajectory for the XAG/USD.

A convincing break through the $21.50-$21.45 horizontal support would be seen as a fresh trigger for bearish traders. The XAG/USD might then drop back to the $21.00 mark en-route the monthly low, around the $20.90 region. The depreciating move could get extended and drag spot prices to the YTD low, around the $20.45 region set in May.

On the flip side, sustained strength beyond the $22.00 mark should pave the way for a move towards an intermediate resistance near the $22.30 area en-route the $22.50-$22.60 supply zone. Some follow-through buying would shift the bias in favour of bullish traders and allow the XAG/USD to reclaim the $23.00 round-figure mark.

Silver 4-hour chart

-637914104400997207.png)

Key levels to watch

UOB Group’s Senior Economist Julia Goh and Economist Loke Siew Ting comment on the recently published May trade balance figures.

Key Takeaways