- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 02-12-2022

- NZD/USD is set to finish the week with gains of 2.56%.

- The November US Nonfarm Payrolls suggested a tight labor market, so the Federal Reserve needs to keep hiking rates.

- NZD/USD Price Analysis: Daily close above 0.6400 exacerbates a rally towards 0.6570s.

The New Zealand Dollar (NZD) climbed against the US Dollar (USD) for the fourth consecutive day, spurred by a weaker USD. An upbeat employment report on the United States (US) suggested the Federal Reserve (Fed) might need to keep hiking rates to ease a contracted labor market, though it failed to underpin the US Dollar. Therefore, the NZD/USD is trading at 0.6404, above its opening price by 0.54%.

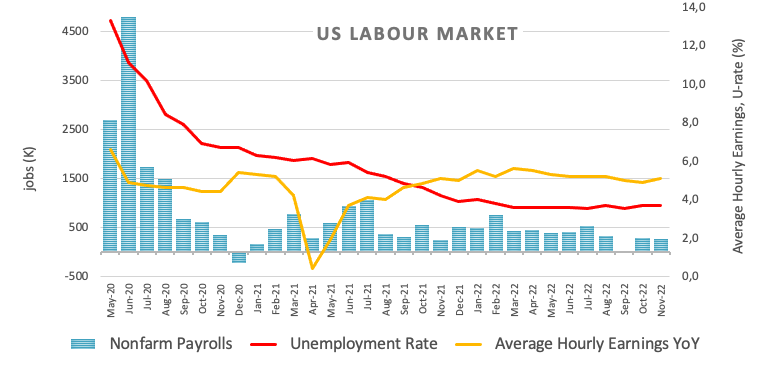

Wall Street finished the week lower. The US Department of Labor (DoL) revealed that November Nonfarm Payrolls rose 263K above estimates of 200K but trailed October’s data, revised up 284K, adding pressure on the Federal Reserve (Fed). Delving into the data, Average Hourly Earnings rose by 5.1% YoY, up from October’s 4.9%, adding to inflationary pressures, while the Unemployment Rate persisted around 3.7%.

Following the November employment report, the Federal Reserve would need to continue tightening borrowing costs, albeit on 50 bps sizes. In the last monetary policy press conference, Fed Chair Jerome Powell said that the pace of tightening it’s not as important as how high the Federal Funds rate (FFR) needs to be. Some Fed policymakers had forecasted the FFR to end at around 5% to 5.25%.

Federal Reserve’s decision to moderate hikes was justified by an Institute for Supply Management (ISM) Manufacturing PMI report for November. The index dropped to the contractionary territory at 49.0 but also portrayed conditions deteriorating. The data reignited recession fears as the US central bank continues to tighten policy. Indeed, the Federal Reserve is trying to slow the economy, accounting for below-trend growth, as the Fed Chair Powell had said.

Aside from this, an absent New Zealand (NZ) economic docket keeps NZD/USD traders adrift to US Dollar dynamics. It should be said that the Kiwi has rallied on broad US Dollar weakness. On the data front, the NZ Business Confidence report in November fell 14 points to -57.1 compared to October’s reading. Respondents foresee the economy deteriorating over the next year, while some respondents expect their business to shrink in the next 12 months.

NZD/USD Price Analysis: Technical outlook

From a technical perspective, the NZD/USD remains upward biased after surpassing the 200-day Exponential Moving Average (EMA) on Wednesday. Notably, during Friday’s session, the NZD/USD reached a daily low nearby the November 30 high of 0.6399 but bounced off and reclaimed the 0.6400 figure. After the major achieved a daily close above 0.6400, a test of the June 2022 high of 0.6576 is on the cards. The Relative Strength Index (RSI) in overbought territory suggests the NZD/USD might consolidate within the 0.6350-0.6400 range, while the Rate of Change (RoC) confirms that buyers remain in charge.

Therefore, the NZD/USD key resistance levels are the August 12 high of 0.6468, followed by the 0.6500 figure, and the June 2022 high of 0.6575.

- The USD/JPY retraced from daily highs of 120 pips, as the USD is being offered.

- USD/JPY: Daily close below the 200-DMA opens the door for a drop to 131.70s.

The US Dollar (USD) gave away its earlier gains courtesy of upbeat economic data revealed in the United States (US) and dropped 0.52% against the Japanese Yen (JPY). At the time of writing, the USD/JPY is trading at 134.63, below the 200-day Exponential Moving Average (EMA), as the JPY gets ready to finish the week with gains of 3.26%.

USD/JPY Price Analysis: Technical outlook

The USD/JPY daily chart portrays the pair as downward biased after breaking the 200-day EMA and a five-month-old upslope support trendline. Nevertheless, upbeat US data exacerbated a rally toward Friday’s high of 135.98. However, the Relative Strength Index (RSI) at bearish territory and the Rate of Change (RoC) aiming lower showed that sellers were gathering momentum. Eventually, the USD/JPY erased those gains and some more.

If the USD/JPY achieves a daily close below the 200-day EMA at 134.99, it could pave the way for further downside action. The USD/JPY key support levels would be the psychological 134.00 figure. A breach of the latter could open the door for a 220 pip drop towards the August 11 low at 131.73, followed by August’s low at 130.39.

USD/JPY Key Technical Levels

- US Dollar remains weaker, despite upbeat US Nonfarm Payrolls report.

- The USD/CHF hit a daily high following the US NFP headline but plunged in the aftermath.

- USD/CHF: Break below 0.9370 to pave the way to the 0.9300 figure.

The USD/CHF trims some of its earlier losses/gains in a volatile trading session, spurred by a buoyant US Nonfarm Payrolls report for November, which increased the likelihood that the US Federal Reserve (Fed) will keep increasing borrowing costs. Nevertheless, manufacturing activity slowing reignited recession fears in the US economy. Therefore, the USD/CHF fluctuates around 0.9370s at the time of writing.

USD/CHF Price Analysis: Technical outlook

Friday’s session witnessed the USD/CHF rallying to its daily high of 0.9439 once the NFP headline crossed newswires. However, it was used by Swiss Franc (CHF) buyers to open fresh short positions on the USD/CHF, as shown by the major erasing its earlier gains, hoovering back below the psychological 0.9400.

Oscillators like the Relative Strength Index (RSI) at bearish territory is almost flat, suggesting consolidation ahead, while the 9-day Rate of Change (RoC) portrays sellers are in charge.

Therefore, the path of least resistance is downward biased. At the time of typing, the USD/CHF tests August 11 daily low of 0.9370, which, once cleared, could pave the way towards testing the fresh 7-month low of 0.9326, followed by the 0.9300 figure.

USD/CHF Key Technical Levels

- Silver price tumbled to its daily low but rallies to six-month highs at $23.22.

- US Nonfarm Payrolls report smashed estimates through an increase in wages to pressure the Federal Reserve.

- Silver Price Analysis: Upward biased, eyeing $24.00 and beyond.

Silver price rallied back above $23.00 after the release of an upbeat US jobs report bolstered the US Dollar (USD), while US Treasury bond yields advanced. Initially, the white metal trimmed some of its gains, traveling towards its daily low of $22.59, though as the USD weakens, it is rising again. At the time of writing, XAG/USD is trading at $23.13.

Federal Reserve pressured by an upbeat US employment report

Investors sentiment remains sour as US stocks trade with losses. The US Department of Labor (DoL) revealed that November Nonfarm Payrolls had risen 263K above estimates of 200K but trailed the previous month’s upward revised 284K, exerting pressure on the Federal Reserve (Fed). Delving into the data, the Unemployment Rate persisted around 3.7%, but wages increased. Average Hourly Earnings rose by 5.1% YoY, up from October’s 4.9%, adding to inflationary pressures.

Should be noted that the employment report would keep the Federal Reserve on the path to continue tightening monetary policy, even if it signifies to do it at smaller sizes, as the Federal Reserve Chair Jerome Powell stated on Wednesday.

The Federal Reserve’s decision to moderate hikes was further justified by a weaker Institute for Supply Management (ISM) Manufacturing PMI report for November. The index dropped to the contractionary territory at 49.0 but also portrayed conditions deteriorating. The data reignited recession fears as the US central bank continues to tighten policy. Indeed, the Federal Reserve is trying to slow the economy, accounting for below-trend growth, as the Fed Chair Powell had said.

In the meantime, after reclaiming 105.000, the US Dollar Index (DXY) drops 0.12%, down to 104.610, contrary to US Treasury yields. The US 10-year T-bond is yielding 3.559%, up five bps, bolstered by traders readjusting the peak for the Federal Funds rate (FFR) at 4.94%.

What to watch

Next week, the US economic docket will feature the ISM Non-Manufacturing PMI, Initial Jobless Claims, the Producer Price Index (PPI), and the University of Michigan (UoM) Preliminary release of the Consumer Sentiment.

Silver Price Forecast: XAG/USD Technical Outlook

The daily chart shows that the XAG/USD broke to fresh six-month highs during the London fix. Traders should note that the white metal plunged, but buyers stepped around the day’s lows and lifted XAG/USD toward $23.22. Oscillators led by the Relative Strength Index (RSI) flashes signals that Silver is overbought, though the 9-day Rate of Change (RoC) shows that buyers remain in charge. Therefore, the XAG/USD bias is upwards.

XAG/USD key resistance levels lie at $24.00, followed by the $25.00 figure, ahead of the February 2022 high of $25.61.

The Mexican Peso has been rising versus the US Dollar over the last weeks. Analysts at MUFG Bank, argue the resilience of the Mexican Peso might not last long amid domestic and external risks. Their forecast is for USD/MXN to reach 19.80 by the end of the first quarter 2023 and 20.00 by the third quarter.

Key Quotes:

“The Mexican peso continued its strengthening path in November helped by improving risk sentiment and a weaker US dollar supported by expectations for a slower pace of Fed hikes.”

“Further Fed hikes albeit slower along with the resilient core inflation in Mexico leads to the expectation of further interest rate hikes in Mexico. We expect a further 50bps hike in December meeting to 10.50%, followed by a final rate hike to 11.00% early next year. Although such scenario might be favourable for MXN appreciation, we see a set of risk factors that might revert the MXN appreciation observed in the latest months.”

“The scenario of some recession in the United States affects Mexican growth path.”

“We keep our bearish forecast profile for MXN due to building fears of a sharp global economic slowdown, and domestic risks coming from potential radical AMLO policies leading to some increased fiscal imbalances. Such risks are higher in a circumstance of weaker economic growth ahead that could impact Lopez Obrador’s popularity that is currently at quite high levels (61% approval rating).”

The Indian rupee is likely to depreciate moderately due to the potential strengthening of the US dollar in the near term, according to analysts at MUFG Bank. They forecast USD/INR at 82.300 by the end of the first quarter of next year and at 80.500 by the third quarter.

Key Quotes:

“Tracking gains in most emerging Asian peers, the INR advanced mildly last month along with a mild gain in India’s stock market, with the benchmark BSE Sensex up 3.2% to 62,858 as foreigners’ net purchased USD3.11 billion worth of Indian equities in November. Easing crude oil prices also offered some support to the currency.”

“The RBI is likely to hike the benchmark repo rate by 50bps at the upcoming meeting on 7th December to further contain inflationary pressures. As inflation moderates further and falls into the central bank’s target range, the RBI will likely keep rates stable for a while and shifts some focus to growth.”

“In the near term, we see that fundamental factors including Fed rate hikes, a stronger US dollar, trade deficits and India’s soaring fiscal deficits, are likely to weigh on the INR, and China factor could also bring volatility to USD/INR movements. The strengthening of INR likely happens when Fed pivots and US dollar begins to weaken in 2Q2023. We expect USD/INR to end this year at 82.000, and next year at 79.800.

"We are probably going to have a slightly higher peak to Fed policy rate even as we slow pace of rate hikes," Chicago Fed President Charles Evans said on Friday, as reported by Reuters.

"We're on a path to getting financial conditions appropriately restrictive to bring inflation down to 2%," Evans noted and added that they are well-positioned to be evaluating some very clear improvements on inflation.

Market reaction

The US Dollar Index clings to modest recovery gains following these remarks and was last seen rising 0.32% on the day at 105.05.

On Friday, the Canadian employment report showed better-than-expected numbers. The Loonie fell against the US Dollar but rose against its other rivals. Analysts at CIBC point out that the report supports their view that the Bank of Canada will increase rates by 50 bps next week, before pausing in 2023.

Key Quotes:

“After a roller coaster few months, the Canadian labour market moved sideways in November. The 10.1K job gain was in line with consensus expectations, as gains in full-time jobs were almost fully offset by losses in part-time employment. Looking through the volatility inherent to this series, the Canadian labour market has largely stood still over the past 6 months, with average gains of just over 4K a month.”

“There were no big surprises in this report. Therefore, and given the low unemployment rate, composition of employment changes and strong and stable wage growth, we continue to expect the Bank of Canada to deliver another 50 bps hike next week, before pausing in 2023. There's not a huge difference, however, between a one-off 50 basis point move and the most likely alternative, two 25 bps hikes in succession, in terms of what it would mean for the economy.”

The US Dollar trimmed weekly losses following the release of the US employment report that showed better-than-expected numbers. Analysts at Wells Fargo, point out that employment gains were fairly broad-based across industries, including in cyclically-sensitive sectors like construction and manufacturing. They argue the labor market remains far too hot for the Fed's liking, and it will take much slower growth in employment and wages to return inflation to the central bank's 2% target on a sustained basis.

Key Quotes:

“Nonfarm payrolls once again blew past expectations, increasing by 263K in November. Employment gains were fairly broad-based across industries, including in cyclically-sensitive sectors like construction and manufacturing. Average hourly earnings growth was much stronger than anticipated, and new labor supply that might help put water on the fire was once again not forthcoming: the labor force participation rate fell by a tenth and is now below where it was in January.”

“Payroll growth of 263K is still too fast at this stage of the business cycle, and wage growth of ~5% is 1-1/2 percentage points above what would be consistent with the Fed's inflation target. A downshift to a 50 bps rate hike in December seems likely, but the Fed still has a ways to go in its tightening cycle.”

Analysts at MUFG Bank, point out that the stress on the Korean Won is unlikely to fade in a near term horizon. They forecast USD/KRW at 1330.0 by the end of the first quarter of next year and at 1270.0 in twelve months.

Key Quotes:

“The won appreciated last month on improving risk-on sentiment spurred by the prospect of a slower pace of Fed rate hikes. The performance of KRW was consistent with benchmark KOSPI Index rising more than 7% and foreign investors’ net buying of USD2 billion worth in Korean equities in the month.”

“Data-wise, South Korea’s current account balance flipped to a surplus of USD1.61 bn in September after a deficit of USD3.05 bn in August; the country’s lower-than-expected unempolyment rate (2.8% in November vs Bloomberg consenus’s 2.9%); and continuous efforts to stabilize its credit market, these helped boost sentiment. Having said that, its latest economic indictors still pointed to the weakness ahead. South Korea’s early exports (first 20 days) contracted for the third straight month in November, indicating the risk to a trade-reliant part of the economy amid softening external demand.”

“The growth deceleration, and the potential strengthening of the dollar in upcoming quarter implies a slightly weaker KRW. We expect USD/KRW to end this year at 1,320.0.”

Gold Price is set to close the week in positive territory despite Friday's pullback. XAU/USD eyes a break above $1,800 as preserves its bullish bias, FXStreet’s Eren Sengezer reports.

XAU/USD to attract additional buyers above $1,800

“On the upside, $1,800 (psychological level, 200-day Simple Moving Average (SMA) aligns as a key pivot level. Once XAU/USD stabilizes above that level by using it as support, it could target $1,830 (Fibonacci 50% retracement of the long-term downtrend) and $1,860 (static level) next.”

“If Gold price falls below $1,780 (Fibonacci 38.2% retracement) and fails to reclaim that level, sellers could show interest and drag XAU/USD lower toward $1,740 (static level) and $1,720 (Fibonacci 23.6% retracement, 50-day SMA).”

- US November’s Nonfarm Payrolls crushed estimates, and wages rose.

- The US Dollar reclaimed the 105.000 mark, underpinned by high US bond yields.

- RBA’s Lowe: “Australia’s inflation expectations well anchored.”

The Australian Dollar (AUD) dropped against the US Dollar (USD) following the release of a positive employment report in the United States (US) which showed an increase in wages, pressuring the Federal Reserve (Fed) to take action. At the time of writing, the AUD/USD is trading at 0.6771 after hitting a daily high of 0.6832.

Positive US jobs data bolstered the US Dollar

US stocks are trading with losses after November’s US Nonfarm Payrolls (NFP) report. Data showed that the economy added 263,000 new jobs, and October’s was upward revised 284,000 jobs, the Department of Labor (DoL) report showed. In the same statement, the Unemployment Rate was unchanged at 2.7%, while Average Hourly Earnings rose by 5.1% YoY, vs. 4.6% consensus, reigniting wage inflation spirals, adding further pressure on the Fed.

The US Dollar Index (DXY), which tracks the greenback’s performance against six currencies, stages a recovery, gaining 0.49%, up at 105.234, underpinned by US Treasury yields. The US 10-year Treasury bond yield rises nine bps, at 3.599%.

Thursday, the Institute for Supply Management (ISM) revealed that November’s manufacturing activity in the US shrank to 49.0 from 50.2 in the previous month. The figures reignited recession fears, as the report showed new orders are falling, demand eased, and the employment index contracted. Therefore, investors’ mood dwindled, as demonstrated by US equities finishing the session with losses.

Meanwhile, Federal Reserve Chairman Jerome Powell opened the door for lower-sized rate hikes, reinforcing the latest meeting minutes sentence that “a substantial majority of participants judged that a slowing in the pace of increase would likely soon be appropriate.” On those remarks, the AUD/USD hit a fresh three-month high, though the rally stalled, on the US ISM report.

Earlier, during the Asian session, the Australian economic docket featured the release of Retail Sales for October, which shrank 0.2% MoM, vs. 0.6% expansion, while housing data remained in negative territory but was better-than-expected. Also, the Reserve Bank of Australia (RBA) Governor Philippe Lowe said that inflation expectations in Australia are “well anchored.” He added that domestic spending remains resilient amidst higher interest rates, and the RBA’s decision to moderate rate hikes reflects monetary policy lags.

AUD/USD Key Technical Levels

The Canadian Dollar is the third-best performing G10 currency year-to-date behind the safe havens Swiss Franc and US Dollar. Economists at Rabobank expect the USD/CAD pair to surge higher toward 1.38 by the end of the year.

CAD to outperform on the crosses in the coming months

“We still expect CAD to outperform on the crosses in the coming months despite seeing upside for USD/CAD.”

“USD/CAD has been volatile and will likely continue trading in wide ranges.”Our base case is for “USD/CAD to trade back to 1.38 by year-end.”

- US economy creates 263K jobs in November against 200K of market consensus.

- Canadian job markets adds 50.7K full time jobs in November.

- Loonie falls versus US dollar but strengthens against other rivals.

The USD/CAD jumped after the release of the employment reports from Canada and the US and peaked at 1.3520, the highest level in two days. It then pulled back to the 1.3450 area. It is still positive for the day but off highs.

Loonie gains on data…

Despite the spike in USD/CAD, the Canadian Dollar rose versus most of its rivals boosted by job market figures. The net change in employment in Canada in November was positive by 10.1K, against expectations of 5K. Full-time jobs increased by more than 50K. Wages rose 5.6% y/y.

“Some early signs that broader inflation pressures have started to ease, and indications that domestic demand is softening, mean the BoC could be close to the end of the current interest rate hiking cycle. But we expect another 25 basis point hike to the overnight rate at next week's central bank policy decision”, explained analysts at RBC Capital Markets.

But Dollar gains more on data

In November, the US economy added 263K jobs above the 200K of markets consensus. The Department of Labor announced the unemployment rate stood at 3.7%. Average Hourly Earnings put upward pressure on inflation, by rising 5.1% y/y.

The US Dollar jumped across the board as equity prices slide and US Treasury yields rose. The numbers keep the door open to more interest rate hikes. “The labor market remains far too hot for the Fed's liking, and it will take much slower growth in employment and wages to return inflation to the central bank's 2% target on a sustained basis”, mentioned analysts at Wells Fargo.

USD/CAD up but off highs

The pair is hovering around 1.3470, up for the day but far from the daily high. The same situation applies to the daily chart. On Tuesday, the pair peaked at 1.3646 but then pulled back 250 pips, finding support around the 1.3400 zone.

The 4-hour chart still shows a bullish bias supported by the 1.3400 area, a horizontal level and also where an uptrend line stands. A break lower should strengthen the Loonie.

Gold rose above $1,800 for the first time in four months. However, economists at TD Securities expect the buying appetite for the yellow metal to fade.

Positioning risks are no longer tilted to the upside

“After yesterday's sharp rally sent Gold prices above several key triggers catalyzing trend follower short covering, CTA trend followers are set to start adding shorts again this session.”

“At this juncture, positioning risks are no longer tilted to the upside in gold, and we see the first signs of buying exhaustion in gold as a rally north of $1,830 only points to marginal CTA buying from current positioning levels.”

In the last month, we have had a sharp sell-off in the US Dollar. Economists at Nordea expect the greenback to remain supported in the near-term, however, EUR/USD is set to edge higher next year.

Dollar’s rise on increasing recession risks to be brief

“In the short-term, we believe EUR/USD is bound for a slight pullback, rather than a quick trend reversal for a higher EUR/USD. Key to our thinking is that downside risks prevail in financial markets, which will benefit the safe haven USD.”

“Looking ahead, the USD is likely to rise initially in response to rising recession risks in the US and Europe, but not substantially unless we end up in a severe recession, which we do not expect.”

“We expect the USD to keep its shine in the short-term, but once investors focus on weakening growth and its impact on inflation, we expect EUR/USD to rise from historical low levels this year.”

- The Pound Sterling nosedived to 1.2133 once the headline crossed newswires.

- US November’s Nonfarm Payrolls crushed estimates, and wages rose.

- Traders focus on Chicago Fed Charles Evans’s speech around 15:00 GMT.

The GBP/USD dived from around 1.2290s close to 100 pips following a better-than-foreseen labor market report in the United States (US), suggesting that further central bank tightening is needed. However, in the aftermath of the US employment report, the GBP/USD is trading around 1.2210s, after traveling towards its daily low of 1.2133, on the market’s reaction to US headline data.

US equity futures remain downbeat after the November US Nonfarm Payrolls rose by 263,000 following an upward revision of 284,000 jobs added in October, the Department of Labor (DoL) report showed. Delving into the information, the Unemployment Rate stood at 3.7%, while Average Hourly Earnings put upward pressure on inflation, jumping 5.1% YoY, vs. 4.6%, consensus. Given that Federal Reserve (Fed) policymakers agreed that moderating the pace of rate hikes is appropriate, it would be interesting to see Fed officials’ postures, led by the Chicago Fed President Charles Evans, crossing newswires around 15:00 GMT.

The US Dollar Index (DXY), a gauge of the buck’s value against a basket of six currencies, after hitting six-month lows around 104.377, stages a mild recovery, reclaimed the 105.000 figure up 0.32%.

Aside from this, a weaker Institute for Supply Management (ISM) Manufacturing PMI report for November on Thursday flashed signs of activity contraction, shifted sentiment sour, spurring flows towards safety, except for the US Dollar (USD). On the inflation side, the Fed’s preferred gauge for inflation, the core Personal Consumption Expenditure (PCE) for October, rose by 5% YoY, below the previous month’s 5.2%, aligned with estimates.

An absent UK economic calendar leaves the GBP/USD pair adrift to the US Dollar dynamics. Given that the GBP/USD reached a fresh 5-month high at 1.2311, it was achieved on a soft USD after the Federal Reserve Chair Jerome Powell said that moderation on the speed of rate increases was “appropriate” Wednesday.

Ahead in the calendar, the US economic docket will feature the Chicago Fed President Charles Evans, ahead of the Fed’s blackout period, at the upcoming December monetary policy meeting.

GBP/USD Key Technical Levels

The Canadian labour market added another 10K jobs in November to match the market consensus. Economists at TD Securities think there is scope for CAD underperformance to come to an end, at least tactically.

A bang-on consensus expectations result does little for the CAD

“The November employment report showed job growth slowing to 10.1K, matching the market consensus, as weaker labour force participation helped pull the unemployment rate to 5.1%.”

“Today's report fits with our call for the Bank of Canada to hike by 25 bps next week, as there was little in the report to support a more aggressive move.”

“This number does little to impact the CAD. That said, we think there is scope for CAD underperformance to come to a tactical end on the crosses following much stronger US Nonfarm Payrolls and wage data.”

- US Dollar soars across the board after NFP.

- Better-than-expected numbers trigger a decline in US Treasuries.

- USD/JPY rises by almost 200 pips, finds resistance below 136.00.

The USD/JPY jumped from 134.10 to 135.95, after the release of the US official employment report that showed better-than-expected numbers. The pair then pulled back toward 135.00 after the initial reaction.

Jobs market still healthy, so is the Dollar?

Nonfarm Payrolls rose by 263K in November, the smallest since April 2021 but the number surpassed expectations and showed positive signs about the health of the labor market.

The US Dollar jumped after the report, while equity prices tumbles and US Treasury yields soared. The economic figures mean a go-ahead for the Federal Reserve to keep raising rates in order to control inflation. “This means that the labor market is hardly cooling off and remains stronger than the Fed would like”, said analysts at Commerzbank.

The combination of a stronger US Dollar and higher US yields sent the Japanese Yen to the downside across the board. It is still among the top performers of the day, but off highs.

The USD/JPY peaked at 135.95 and then pulled back. After the opening bell at Wall Street the pair is hovering at 135.10/30, as volatility remains elevated with market participants still digesting the NFP and its impact.

On a weekly basis, USD/JPY is headed toward the lowest close since mid-August, about to post the sixth weekly decline out of the last seven weeks.

Technical levels

Gold price surged by more than 8% in November. But the current rally on the Gold market could run out of steam ahead of the central bank meetings scheduled to take place the following week, according to strategists at Commerzbank.

Prospect of slower US rate hikes lends buoyancy to precious metals

“Precious metals have profited recently – partly thanks to the weaker US Dollar – from the prospect of more moderate rate hikes by the Fed. It is questionable whether the buoyancy will last until the end of the year, however.”

“Gold could shed some of its gains again in the run-up to the central bank meetings that are to take place the week after next.”

“It is above all long-term-oriented financial investors who still appear hesitant, though at least no further selling from the ETFs tracked by Bloomberg has been reported since mid-November.”

- The index bounces off multi-month lows post-NFP.

- The US economy added more jobs than expected in November.

- A 50 bps rate hike remains favoured despite robust Payrolls.

The Greenback, in terms of the USD Index (DXY), quickly reclaimed the area above the 105.00 mark following another strong result for US Nonfarm Payrolls on Friday.

USD Index appears supported near 104.40

The index manages to regain strong upside traction following solid prints from November’s Payrolls, which showed both the job creation and wage growth remained far from mitigated.

Indeed, the US economy added 263K jobs during last month (vs. 200K expected) and the Unemployment Rate remained at 3.7%, while Average Hourly Earnings rose more than expected 0.6% MoM and 5.1% from a year earlier. The Participation Rate, however, deflated marginally to 62.1% (from 62.2%).

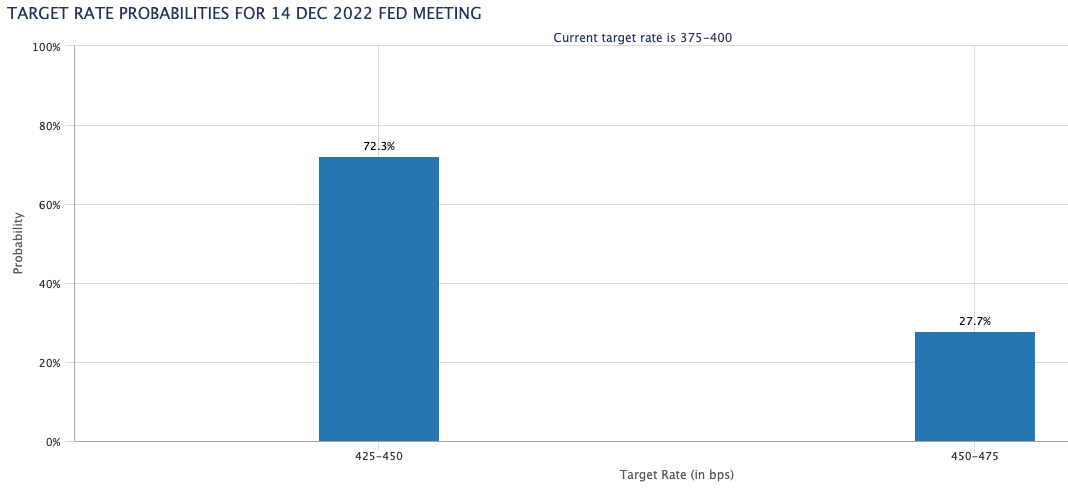

Following the release of the jobs report, the probability of a 75 bps rate hike at the next Fed’s gathering (December 14) improved to nearly 30%, according to CME Group's FedWatch Tool.

Next on tap in the US docket comes the speech by Chicago Federal Reserve President Charles Evans (2023 voter, centrist).

What to look for around USD

The US Dollar seems to have met some decent contention around 104.30 for the time being.

While hawkish Fedspeak maintains the Fed’s pivot narrative in the freezer, upcoming results in US fundamentals would likely play a key role in determining the chances of a slower pace of the Fed’s normalization process in the short term.

Key events in the US this week: Nonfarm Payrolls, Unemployment Rate (Friday).

Eminent issues on the back boiler: Hard/soft/softish? landing of the US economy. Prospects for further rate hikes by the Federal Reserve vs. speculation of a recession in the next months. Fed’s pivot. Geopolitical effervescence vs. Russia and China. US-China persistent trade conflict.

USD Index relevant levels

Now, the index is gaining 0.58% at 105.33 and faces the next up barrier at 105.55 (200-day SMA) followed by 107.19 (weekly high November 30) and then 107.99 (weekly high November 21). On the other hand, the breakdown of 104.37 (weekly low December 2) would open the door to 103.41 (weekly low June 16) and finally 101.29 (monthly low May 30).

- Gold price retreats sharply from a multi-month top in reaction to upbeat US jobs data.

- Rising US Treasury bond yields prompt aggressive US Dollar short-covering and weigh.

- The risk-off impulse fails to impress bulls or lend support to the safe-haven XAU/USD.

Gold price struggles to find acceptance above a technically significant 200-day Simple Moving Average (SMA) and retreats from a nearly four-month high touched earlier this Friday. The intraday downtick picks up pace in reaction to the upbeat US jobs report and drags the XAU/USD to sub-$1,780 levels during the early North American session.

US employment details beat market expectations

The closely-watched Nonfarm Payrolls (NFP) from the United States showed that the economy added 263K new jobs in November, beating consensus estimates pointing to a reading of 200K. Adding to this, the previous month's print was also revised higher to show an addition of 284K vacancies as compared to the 261K reported originally. Meanwhile, the unemployment rate held steady at 3.7% during the reported month, as was anticipated.

Aggressive US Dollar short-covering weighs on Gold price

Additional details of the report showed that Average Hourly Earnings grew 0.6% in November and 5.1% YoY rate, suggesting a further rise in inflationary pressures. The data validates Federal Reserve Chair Jerome Powell's forecast that the peak rate will be higher than expected, which triggers a sharp rise in the US Treasury bond yields. This, in turn, prompts an aggressive US Dollar short-covering move and weighs heavily on the Dollar-denominated Gold price.

Risk-off impulse fails to lend support to safe-haven XAU/USD

Traders, meanwhile, seem rather unaffected by a sell-off in the equity markets, which tends to drive flows towards the safe-haven precious metal. Nevertheless, Gold price, for now, seems to have snapped four days of the winning streak, though remains on track to post strong weekly gains. Hence, it will be prudent to wait for strong follow-through selling before confirming that the XAU/USD has topped out and positioning for a deeper corrective pullback.

Gold price technical outlook

From a technical perspective, failure to find acceptance above the very important 200-day SMA and the subsequent downfall could be seen as the first sign of bullish exhaustion. That said, any further decline is likely to find some support near the $1,770 horizontal zone. A convincing break below should pave the way for a fall towards the next relevant support near the $1,755-$1,753 region.

On the flip side, the $1,800 round-figure mark now seems to act as an immediate hurdle ahead of the multi-month top, around the $1,804-$1,805 region. This is closely followed by the August 2022 swing high, around the $1,808 area, above which Gold price could climb to the $1,820 resistance zone.

Key levels to watch

- Unemployment Rate in Canada declined modestly in November.

- USD/CAD trades in positive territory at around 1.3500.

The data published by Statistics Canada revealed on Friday that the Unemployment Rate declined to 5.1% in November from 5.2% in October. This reading came in better than the market expectation of 5.3%.

Further details of the publication showed that the Net Change in Employment was +10.1K, slightly higher than analysts' estimate of +5K.

"The number of people employed on a full-time basis increased by 51,000 (+0.3%) in November," Statistics Canada noted. "Since November 2021, when full-time employment first surpassed its pre-COVID-19 pandemic level, full-time work has grown by 460,000 (+2.9%), concentrated among core-aged men (+212,000; +3.5%) and women (+169,000; +3.4%)."

Market reaction

USD/CAD rose sharply in the early North American session as the upbeat November jobs report from the US provided a boost to the US Dollar. As of writing, the pair was up 0.5% on the day at 1.3500.

- EUR/USD now looks offered well below 1.0500 on NFP.

- US Non-farm Payrolls surprised to the upside in November.

- The unemployment rate held steady at 3.7%.

EUR/USD comes under further downside pressure and rapidly breaks below the 1.0500 in the wake of the US jobs report on Friday.

EUR/USD: Gains appear capped near 1.0550 so far

EUR/USD picks up extra selling pressure after the release of the Nonfarm Payrolls showed the US economy added 263K jobs during November, surpassing initial estimates for a gain of 200K jobs. In addition, the October reading was also revised up to 284K (from 261K).

Further data saw the Unemployment Rate unchanged at 3.7% and the key Average Hourly Earnings – a proxy for inflation via wages – rise 0.6% MoM and 5.1% from a year earlier. Additionally, the Participation Rate eased a tad to 62.1% (from 62.2).

What to look for around EUR

EUR/USD’s upside momentum faltered ahead of 1.0550, or multi-month peaks, amidst persistent optimism in the risk complex and intense weakness in the dollar ahead of US Payrolls.

In the meantime, the European currency is expected to closely follow dollar dynamics, the impact of the energy crisis on the region and the Fed-ECB divergence. In addition, markets repricing of a potential pivot in the Fed’s policy remains the exclusive driver of the pair’s price action for the time being.

Back to the euro area, the increasing speculation of a potential recession in the bloc emerges as an important domestic headwind facing the euro in the short-term horizon.

Key events in the euro area this week: ECB Lagarde, Germany Balance of Trade (Friday).

Eminent issues on the back boiler: Continuation of the ECB hiking cycle vs. increasing recession risks. Impact of the war in Ukraine and the persistent energy crunch on the region’s growth prospects and inflation outlook. Risks of inflation becoming entrenched.

EUR/USD levels to watch

So far, the pair is losing 0.82% at 1.0440 and a breach of 1.0365 (200-day SMA) would target 1.0330 (weekly low November 28) en route to 1.0222 (weekly low November 21). On the upside, there is an initial hurdle at 1.0548 (monthly high December 2) ahead of 1.0614 (weekly high June 27) and finally 1.0773 (monthly high June 27).

Nonfarm Payrolls in the US rose by 263,000 in November, the data published by the US Bureau of Labor Statistics revealed on Friday. This reading came in much higher than the market expectation of 200,000. October's reading got revised higher to 284,000 from 261,000.

Further detail of the publication revealed that the Unemployment Rate remained unchanged at 3.7% and the annual wage inflation, as measured by the Average Hourly Earnings, rose to 5.1% from 4.9% in October. Finally, the Labor Force Participation Rate edged lower to 62.1% from 62.2%.

Follow our live coverage of market reaction to the US jobs report.

Market reaction

The US Dollar gathered strength against its rivals with the initial reaction and the US Dollar Index was last seen rising 0.55% on the dayat 105.35.

GBP/USD has gained a solid 1.5% over the course of the week. A move above 1.2295 would trigger another leg higher, economists at Scotiabank report.

Momentum favours more gains

“The pause (a bull flag pattern) in the GBP rally should shortly give way to further gains on a spot move through the consolidation ceiling at 1.2295.”

“Support is 1.2225.”

“Trend signals are bullish on the shorter-term (intraday, daily) DMIs and tilting bullish on the weekly study.”

“Bullish oscillators should limit GBP losses in the short term and least and leave the GBP well-supported on minor dips – which remain a buy from a technical point of view.”

- USD/JPY plummets to a fresh multi-month low on Friday amid sustained USD selling bias.

- A break and acceptance below the 200-day SMA support prospects for additional losses.

- The bearish pressure, however, abates amid oversold conditions and ahead of the NFP.

The USD/JPY pair prolongs its bearish trend for the fifth straight day on Friday - also marking the ninth day of a negative move in the previous ten and dives to its lowest level since August 16. The pair now seems to have entered a bearish consolidation phase and is seen hovering around the 134.00 mark as traders await the US NFP report for a fresh impetus.

The relentless US Dollar selling remains unabated amid growing acceptance that the Fed will slow the pace of its rate-hiking cycle. Apart from this, the recent sharp decline in the US Treasury bond yields narrows the US-Japan rate differential, which benefits the Japanese Yen. This, along with the overnight hawkish signals by the Bank of Japan board member Asahi Noguchi contributes to the heavily offered tone surrounding the USD/JPY pair.

From a technical perspective, this week's downfall took confirmed a breakdown through an upward sloping trend-line extending from late March. A subsequent slide below the 137.65-137.50 horizontal support and the 135.00 psychological mark zone is seen as a fresh trigger for bearish traders. Moreover, acceptance below the very important 200-day SMA supports prospects for an extension of the recent depreciating move for the USD/JPY pair.

That said, oscillators on short-term charts are already flashing oversold conditions and warrant some caution. Nevertheless, the USD/JPY pair seems poised to weaken further towards testing sub-133.00 levels. The downward trajectory could eventually drag spot prices below the 132.00 round figure, towards the next relevant support near the 131.50 area en route to the 131.00 mark and the August swing low, around the 130.40-130.35 zone.

On the flip side, the 200-day SMA, currently around the 134.50 region, could act as an immediate strong resistance ahead of the 135.00 mark. A sustained move beyond might trigger a short-covering rally and allow the USD/JPY pair to reclaim the 136.00 round figure. Any subsequent move up, however, is more likely to attract fresh sellers and remain capped near the 136.70 support breakpoint, which should act now act as a pivotal point.

USD/JPY daily chart

Key levels to watch

- EUR/USD advances further to fresh 6-month peaks near 1.0550.

- Further upside could put the 1.0614 level back on the radar.

EUR/USD keeps the optimism well and sound and advances to new highs near 1.0550, an area last seen back in late June.

Gains in the pair are now likely to pick up pace following the breakout of the 200-day SMA and the 10-month resistance line. Against that, there are no resistance levels of note until the June high at 1.0614 (June 27).

Further upside in EUR/USD remains on the cards while above the 200-day SMA, today at 1.0365.

EUR/USD daily chart

- The index sheds further ground and retreats to multi-month lows.

- Further weakness could force the dollar to test the 103.40 zone.

DXY loses ground for the third session in a row and re-visits the 104.30 area on Friday.

The continuation of the selling pressure could motivate the dollar to accelerate losses and challenge the weekly low at 103.67 (June 27) ahead of another weekly low at 103.41 (June 16).

Below the 200-day SMA at 105.51, the dollar’s outlook should remain negative.

DXY daily chart

USD/JPY is approaching potential support zone at 132.50/130.40. The downtrend could extend on failure to hold this support, economists at Société Générale report.

Graphical level at 145 could contain upside

“The pair is fast approaching its next potential support of 132.50, representing the 38.2% retracement of the whole uptrend since 2020. The low formed in August at 130.40 is an important support level. A test of this support could result in a short-term bounce; however, a graphical level at 145 could contain upside.”

“If the pair fails to defend support at 130.40, the downtrend is likely to extend towards 127.30 and 2015 levels of 125.85/124.00.”

European Central Bank (ECB) Vice President Luis de Guindos said on Friday that the economic deceleration in the Eurozone will not be as deep as expected a few weeks ago, as reported by Reuters.

Key takeaways

"Inflation data in November has been good news."

"Inflation in eurozone around mid-2023 will hover around 7%."

"Further interest rate increases will depend on upcoming data."

"We are seeing that inflation is starting to slow down."

Market reaction

The EUR/USD pair showed no immediate reaction to these comments and was last seen trading at 1.0535, rising 0.14% on a daily basis.

EUR/USD maintains gains above 1.05. Economists at Scotiabank expect the pair to extend its advance toward the 1.0650/1.0750 range.

Technical trend remains bullish

“EUR/USD remains well-supported near the high of the week and looks well-positioned to advance a little more at least in the near term as broader USD sentiment weakens.”

“A weekly close above 1.0517 (50% retracement of the 2022 decline) should be sufficient to push EUR gains on the 1.0650/1.0750 range.”

“Trend signals are aligned bullishly on short, medium and long-term oscillators which should limit counter-trend corrections (to the high 1.04s) and keep the EUR grind higher on track for more gains.”

Canadian employment details overview

Statistics Canada is scheduled to publish the monthly employment report for November later this Friday at 13:30 GMT. The Canadian economy is anticipated to have added 5K jobs during the reported month, down sharply from October's blockbuster reading of 108.3K. Moreover, the unemployment rate is anticipated to edge higher from 5.2% to 5.3% in November.

According to analysts at NBF: “The prior month’s report was suspiciously strong (+108.3K) given slowing growth and declining business confidence. A trend reversal would therefore not be surprising; we expect employment to have fallen 25K in the penultimate month of 2022. Such a decline would translate into a two-tick increase in the unemployment rate to 5.4%, assuming the participation rate remained steady at 64.9% and the working-age population grew at a strong pace.”

How could the data affect USD/CAD?

The data is more likely to be overshadowed by the simultaneous release of the closely-watched US jobs report - popularly known as NFP. That said, a significant divergence from the expected readings might still influence the Canadian Dollar and provide some meaningful impetus to the USD/CAD pair.

Strong domestic data should provide a goodish lift to the Canadian dollar and exert fresh downward pressure on the USD/CAD pair. Conversely, any disappointment from the Canadian jobs data is more likely to be overshadowed by the prevalent US Dollar selling bias amid bets for a less aggressive policy tightening by the Fed. This, in turn, suggests that the path of least resistance for the major is to the downside any positive reaction is more likely to get sold into.

From current levels, the 1.3400 mark is likely to protect the immediate downside ahead of a two-week-old ascending trend-line support, around the 1.3380 region. A convincing break below the latter will be seen as a key trigger for bears and expose the crucial 100-day SMA support, currently around the 1.3300-1.3290 region.

On the flip side, momentum beyond the overnight swing high, around the 1.3470 region, is likely to confront stiff resistance and remain capped near the 1.3500 psychological mark. That said, some follow-through strength might prompt some short-covering move and lift the USD/CAD pair towards the 1.3575-1.3580 hurdle en route to the 1.3600 mark.

Key Notes

• Canadian Jobs Preview: Forecasts from five major banks, more lackluster performance

• USD/CAD Outlook: Traders seem non-committed ahead of US NFP, Canadian jobs data

• USD/CAD Price Analysis: Impending bear cross keeps sellers hopeful above 1.3400

About the Employment Change

The employment Change released by Statistics Canada is a measure of the change in the number of employed people in Canada. Generally speaking, a rise in this indicator has positive implications for consumer spending which stimulates economic growth. Therefore, a high reading is seen as positive, or bullish for the CAD, while a low reading is seen as negative or bearish.

About the Unemployment Rate

The Unemployment Rate released by Statistics Canada is the number of unemployed workers divided by the total civilian labour force. It is a leading indicator for the Canadian Economy. If the rate is up, it indicates a lack of expansion within the Canadian labour market. As a result, a rise leads to weaken the Canadian economy. Normally, a decrease of the figure is seen as positive (or bullish) for the CAD, while an increase is seen as negative or bearish.

- EUR/JPY breaks below the 141.00 mark to record new 3-month lows.

- Extra losses now target the key 200-day SMA just above 139.00.

EUR/JPY remains entrenched in the negative territory and drops to new 3-month lows in the 140.80/75 band at the end of the week.

The sharp pullback breached the 4-month support line and left the cross vulnerable to a deeper decline. Against that, the next support of relevance is expected at the critical 200-day SMA, today at 139.08.

The outlook for EUR/JPY is expected to remain positive while above this region.

EUR/JPY daily chart

What will China’s reopening mean for the US? Here is what economists at Morgan Stanley think you need to know.

Fed will be able to slow and eventually pause its rate hikes in 2023

“China's restrictive COVID zero policy will be a thing of the past come spring of 2023, but there will be many fits and starts along the way. This dynamic is important to understand for its implications to the outlook for the global economy and key markets.”

“The economic growth story for Asia should be weak in the near term, but begin to improve and outperform the rest of the world from the second quarter of 2023 through the balance of the year.”

“In the US, the reopening of the China economy should help ease inflation as the supply of core goods picks up with supply chains running more smoothly. This, in turn, supports the notion that the Fed will be able to slow and eventually pause its rate hikes in 2023.”

“Look to the foreign exchange markets. China's currency should relatively benefit, particularly if reopening leads investors back to its equity markets. The US Dollar, however, should peak, as the Fed approaches pausing its interest rate hikes and, accordingly, ceasing the increase in the interest rate advantage for holding USD assets versus the rest of the world.”

Lee Sue Ann, Economist at UOB Group, sees the RBA raising the OCR by 25 bps at its event next week.

Key Takeaways

“Both consumer and business confidence have softened under the weight of high inflation and rising interest rates. This is why we think the RBA will soon pause in the current rate hiking cycle.”

“We are penciling in another 25bps hike at the final monetary policy meeting of the year on 6 Dec, which will take the OCR to 3.10%. Thereafter, we look for a hold.”

GBP/USD has risen close to the 1.2450 mark. A break above here is needed to avoid a phase of pullback, economists at Société Générale report.

Watch out for next hurdle at 1.2450

“1.2450 is the lower end of the multi-year range from which the pair broke down earlier this year and it is expected to be an intermittent resistance zone. A test and failure to cross above this hurdle could result in a phase of pullback. The October high of 1.1500, which is also the 50DMA, is expected to be first layer of support in case a decline develops.”

“If the pair establishes itself beyond 1.2450, the up move could extend towards 1.2750, the 61.8% retracement from February 2021 and 1.3250/1.3300.”

US monthly jobs report overview

Friday's US economic docket highlights the release of the closely-watched US monthly jobs data for November. The popularly known NFP report is scheduled for release at 13:30 GMT and is expected to show that the economy added 200K jobs during the reported month, down from the 261K in October. The unemployment rate is anticipated to hold steady at 3.7% in November. Apart from this, investors will take cues from Average Hourly Earnings, which could offer fresh insight into the possibility of any further rise in inflationary pressures.

Analysts at Citibank are more optimistic and offer a brief preview of the important macro data: “We expect a solid 225K jobs added in November, reflecting a slowing but still-solid pace of job growth. Average hourly earnings should rise 0.3% MoM, a slightly softer increase than last month but with upside risks. Average hourly earnings have slowed in recent months relative to other, more carefully constructed wage measures such as the Atlanta Fed’s Wage Tracker and the Fed’s preferred Employment Cost Index. After a somewhat surprising increase in October, we expect the unemployment rate to drop to 3.6%.”

How could the data affect EUR/USD?

Ahead of the key release, the US Dollar plummets to over a five-month low in the wake of a dovish pivot by the Fed and assists the EUR/USD pair to hold steady above the 1.0500 psychological mark. Weaker US employment details should be enough to trigger a fresh leg down in the USD and provide an additional boost to the major.

In contrast, any positive surprise - though could offer a temporary respite to the USD - is likely to be overshadowed by expectations that the US central bank will slow the pace of its rate-hiking cycle. This, in turn, favours the USD bears and suggests that the path of least resistance for the EUR/USD pair is to the upside.

Eren Sengezer, Editor at FXStreet, offers a brief technical overview and outlines important technical levels to trade the EUR/USD pair: “The Relative Strength Index (RSI) indicator on the four-hour chart stays within a touching distance of 70, suggesting that the pair could stage a technical correction before the next leg higher. On the upside, interim resistance seems to have formed at 1.0540. In case buyers manage to flip that level into support, additional gains toward 1.0600 (psychological level, static level) and 1.0630 (static level) could be witnessed.”

“1.0500 (former resistance, psychological level) aligns as initial support. With a four-hour close below that level, sellers could take action and drag the pair toward the 1.0410/1.0390 area, where the 20-period and the 50-period Simple Moving Averages are located,” Eren adds further.

Key Notes

• Nonfarm Payrolls Preview: Dollar selling opportunity? Low expectations to trigger temporary bounce

• US NFP Preview: Forecasts from 10 major banks, less strong, but not weak

• EUR/USD Forecast: Euro to end week on strong note on weak NFP

About the US monthly jobs report

The nonfarm payrolls released by the US Department of Labor presents the number of new jobs created during the previous month, in all non-agricultural business. The monthly changes in payrolls can be extremely volatile, due to its high relation with economic policy decisions made by the Central Bank. The number is also subject to strong reviews in the upcoming months, and those reviews also tend to trigger volatility in the forex board. Generally speaking, a high reading is seen as positive (or bullish) for the USD, while a low reading is seen as negative (or bearish), although previous month's reviews and the unemployment rate are as relevant as the headline figure.

- USD/CAD struggles for a firm direction on Friday and remains confined in a narrow range.

- Traders now await the release of the monthly employment data from the US and Canada.

- Bearish traders might wait for sustained weakness below the 1.3385 confluence support.

The USD/CAD pair extends its sideways consolidative price moves through the mid-European session and remains confined in a narrow trading band below mid-1.3400s.

The US Dollar selling remains unabated on the last day of the week amid growing acceptance that the Fed will slow the pace of its rate-hiking cycle. This, in turn, continues to cap the USD/CAD pair, though a modest downtick in oil prices undermines the commodity-linked Loonie and acts as a tailwind. Traders also seem reluctant to place aggressive bets ahead of the monthly employment reports from the US and Canada.

From a technical perspective, the USD/CAD pair, so far, has managed to hold above the 1.3400 mark and the 100-period SMA on the 4-hour chart. The latter, currently pegged around the 1.3385 area, coincides with over a two-week-old ascending trend-line extending from the November swing low and should now act as a pivotal point. A convincing break below will be seen as a key trigger for bears and set the stage for further losses.

The subsequent downfall will expose the crucial 100-day SMA support, currently around the 1.3300-1.3290 region. Some follow-through selling should pave the way for an extension of the recent sharp pullback from a 29-month peak touched in October.

On the flip side, the overnight swing high, around the 1.3470 zone, might act as an immediate barrier ahead of the 1.3500 psychological mark. A sustained strength beyond the latter could lift the USD/CAD pair towards the 1.3575-1.3580 hurdle en route to the 1.3600 mark and the multi-week high, around the 1.3645 zone set on Tuesday.

USD/CAD 4-hour chart

Key levels to watch

EUR/USD is extending its bounce. The pair could enjoy further gains on a move beyond the 1.0630/1.0690 region, economists at Société Générale report.

Graphical levels of 1.0000/0.9930 should be an important support

“A test of projections at 1.0630/1.0690, which is also the low of March 2020 and the descending trend line connecting highs of June 2021 and February 2022, is expected. This is likely to act as an interim resistance zone. In case the up-move falters near this hurdle, a short-term pullback is expected to materialise.”

“Graphical levels of 1.0000/0.9930 should be an important support zone. Failure to defend this could mean renewed downward momentum.”

USD/JPY has broken below 135.00. A dip under the 134.50 mark is set to trigger another leg lower, economists at ING report.

Markets may struggle to live with sub-3.50% rates for long

“The main risk for USD/JPY is that UST 10Y yields fail to find extra support at 3.50%: a further bond rally could force a break below the 134.50 200-Day Moving Average and unlock additional downside potential for USD/JPY.”

“Still, markets may struggle to live with sub-3.50% rates for long in the current environment.”

10-year Yields have plummeted 76 bps from their high of 4.335%. Support must come quickly to avoid yields unraveling below 3.50%, economists at Société Générale report.

Signals of a meaningful up move are not yet visible

“Signals of a meaningful up move are not yet visible; failure to reclaim the peak formed earlier this week near 3.80% can lead to continuation in pullback.”

“Below 3.50%, next objectives are located at 3.38% and the lower band of the channel at 3.25%/3.20%.”

See: US 10Y Bond Yields could move below 3.00% – Credit Suisse

EUR/USD closed above 1.0500 for the first time since June. Economists at ING note that the pair could test the 1.0600 level.

Ignoring some warning signs

“EUR/USD moves should only be a function of the market’s reaction to US payrolls today. There is a non-negligible risk we explore 1.0600, with the pair not having any clear resistance levels until the 1.0780 6-month highs. We are, however, getting the feeling that markets are ignoring at least one warning sign for the Euro.”

“TTF contracts are trading at one-month highs now and may see further upside volatility in the near term as temperatures in northern Europe are expected to fall. A significant recovery in gas prices would likely make the recent rally in EUR/USD unsustainable.”

The more nuanced approach to monetary policy going forward suggested by Fed Chair Powell’s speech means the jobs reports in the coming months will be even more important. Economists at MUFG Bank note that impressively strong Nonfarm Payrolls figures are needed to lift the US Dollar.

Jobs data increasingly important

“When Fed Chair Powell talks of avoiding ‘crashing the economy’ what the Fed really wants to engineer is a soft landing that means the scale of unemployment increase is kept to the minimum required to achieve a drop in inflation back to target. Hence, the importance of NFP reports.”

“Given the momentum in the market favouring USD selling, we suspect a weaker than expected employment report would trigger a bigger market reaction than a stronger than expected report.”

“It would take less of a surprise we feel for the market to price in less tightening from the FOMC than more. So the bias feels skewed to a weaker Dollar today and a stronger jobs report would have to be impressively stronger to see the US Dollar advance notably.”

See – US NFP Preview: Forecasts from 10 major banks, less strong, but not weak

US Dollar Index (DXY) has now lost 8.5% from the top in October and is below the August low of 104.60. Economists at Société Générale highlight the next targets on the downside.

An initial bounce is on the cards

“Daily MACD is within deep negative territory pointing towards an overstretched move. An initial bounce is not ruled out, however, the recent pivot high at 107.20/108.00 could provide resistance near term.”

“Next potential supports are located at 2020 peak of 103 and 101.90/101.30, the 50% retracement from 2021.”

- GBP/USD oscillates in a narrow trading band just below its highest level since June.

- The overnight breakout above the 200-day SMA supports prospects for further gains.

- Bulls, however, prefer to wait for the crucial US NFP report before placing fresh bets.

The GBP/USD pair consolidates its recent gains to the highest level since June and oscillates in a range, below the 1.2300 mark through the first half of the European session on Friday. The technical bias, meanwhile, remains tilted in favour of bulls and supports prospects for a further near-term appreciating move.

The overnight sustained strength and acceptance above a technically significant 200-day SMA for the first time in 2022 could be seen as a fresh trigger for bullish traders. Furthermore, the recent move up since late September has been along an ascending channel, which further points to a well-established short-term positive trend.

Moreover, oscillators on the daily chart are holding comfortably in the positive territory and are still far from being in the overbought zone. The GBP/USD pair, however, remains capped near the trend-channel resistance as traders prefer to move to the sidelines ahead of the release of the closely-watched US monthly jobs report (FMP).

Hence, it will be prudent to wait for a sustained strength beyond the top end of the aforementioned channel before placing fresh bullish bets. The said barrier is currently pegged near the 1.2310 region, above which the GBP/USD pair could climb to the 1.2345-1.2350 intermediate resistance and eventually aim to reclaim the 1.2400 round-figure mark.

On the flip side, the corrective pullback might now find decent support near the 1.2200 mark. Any further downfall could be seen as a buying opportunity and remain limited near the 1.2150 region (200-DMA). The latter should act as a pivotal point for short-term traders, which if broken decisively will negate the near-term positive outlook for the GBP/USD pair.

GBP/USD daily chart

Key levels to watch

Economist at UOB Group Enrico Tanuwidjaja reviews the latest interest rate decision by the Bank of Thailand.

Key Takeaways

“BOT voted unanimously to raise the policy rate by 25bps to 1.25%. This is its third hike for 2022. Back in Aug when BOT started its hiking cycle, 1 out of a total 7 members preferred a larger 50bps hike.”

“BOT deemed that a gradual policy normalization remains an appropriate course for monetary policy given the growth and inflation outlook in today’s decision statement.”

“We revised our view for another two 25bps back-to-back rate hikes to 1.75% in 2023 Jan and Mar MPC meeting and remained at that level for the rest of next year.”

- EUR/USD clinches fresh 6-month tops near 1.0550 on Friday.

- Germany’s trade surplus widened to €6.9B in October.

- US Nonfarm Payrolls will take centre stage later in the session.

The European currency now comes under some mild pressure and motivates EUR/USD to retreat to the 1.0520 region following earlier peaks near 1.0550 on Friday.

EUR/USD alternates gains with losses ahead of US data

EUR/USD now struggles to keep the strong weekly rebound well and sound above the 1.0500 hurdle soon after hitting new 6-month highs near 1.0550.

In the meantime, the continuation of the decline in the dollar continues to underpin the upbeat momentum in the pair, which gathered extra steam after surpassing the critical 200-day SMA (1.0365) and the 10-month line around 1.0410.

The daily improvement in the pair is also accompanied by another decline in the German 10-year bund yields, this time breaking below the 1.80% level, an area last seen back in early October.

Earlier in the domestic docket, Germany’s trade surplus increased to €6.9B in October (from €3.7B).

Moving forward, the release of the US Nonfarm Payrolls for the month of November (200K exp.) will take centre stage seconded by the Unemployment Rate (3.7% exp.). In addition, Chicago Fed C.Evans is also due to speak.

What to look for around EUR

EUR/USD manages to extend the rally to the vicinity of 1.0550, or multi-month peaks, amidst persistent optimism in the risk complex and intense weakness in the dollar ahead of US Payrolls.

In the meantime, the European currency is expected to closely follow dollar dynamics, the impact of the energy crisis on the region and the Fed-ECB divergence. In addition, markets repricing of a potential pivot in the Fed’s policy remains the exclusive driver of the pair’s price action for the time being.

Back to the euro area, the increasing speculation of a potential recession in the bloc emerges as an important domestic headwind facing the euro in the short-term horizon.

Key events in the euro area this week: ECB Lagarde, Germany Balance of Trade (Friday).

Eminent issues on the back boiler: Continuation of the ECB hiking cycle vs. increasing recession risks. Impact of the war in Ukraine and the persistent energy crunch on the region’s growth prospects and inflation outlook. Risks of inflation becoming entrenched.

EUR/USD levels to watch

So far, the pair is losing 0.05% at 1.0520 and a breach of 1.0365 (200-day SMA) would target 1.0330 (weekly low November 28) en route to 1.0222 (weekly low November 21). On the upside, there is an initial hurdle at 1.0548 (monthly high December 2) ahead of 1.0614 (weekly high June 27) and finally 1.0773 (monthly high June 27).

With a larger yield top now threatening in the US 10-year Bond Yield, economists at Credit Suisse downgrade their tactical objective further to 3.045/00%.

10yr US Bond Yields to confirm a large top on a break below 3.56%

“10yr US Bond Yields need to break below 3.56% to confirm a larger top. Of course, Nonfarm Payrolls data represents a key event risk, however, short-term momentum continues to accelerate to the downside, suggesting a break is more likely than not.”

“Even if yields were to rebound from current levels on an upside NFP surprise, the completion of a larger top would still be our base case, as long as the market holds below support at 4.00/03%.”

“Assuming the top is confirmed, the potential ‘measured top objective’ suggests a move below 3.00% is possible, however, the rising 200-Day Average at 3.045% should provide a formidable barrier beforehand.”

See – US NFP Preview: Forecasts from 10 major banks, less strong, but not weak

UOB Group’s Economist Lee Sue Ann and Markets Strategist Quek Ser Leang note a deeper decline in USD/CNH could see the 7.000 level revisited in the near term.

Key Quotes

24-hour view: “We highlighted yesterday that USD ‘could test 7.0200 first before the risk of a rebound increases’. Our expectations did not materialize as USD traded within a range of 7.0256/7.0919 before closing slightly lower at 7.0390 (-0.11%). The price movement is likely part of a consolidation phase and we expect USD to trade within a range of 7.0300/7.0800 today.”

Next 1-3 weeks: “We continue to hold the same view as yesterday (01 Dec, spot at 7.0400). As highlighted, the recent outsized drop in USD is likely to extend to 7.0200, possibly below 7.0000. The downside risk is intact as long USD does not move above 7.1250 (‘strong resistance’ level was at 7.1400 yesterday).”

GBP/USD has gone into a consolidation phase at around 1.2250. Economists at ING expect the pair to plummet toward 1.1500 by year-end.

Cable nearing the peak?

“US Nonfarm Payrolls may fail to invert the bearish Dollar trend and GBP/USD may find a bit more support around 1.2300-1.2350.”

“However, Cable is not factoring in the negative implications of rebounding gas prices and weak economic fundamentals. A return to 1.1500 around the turn of the year seems appropriate in our view.”

See – US NFP Preview: Forecasts from 10 major banks, less strong, but not weak

- AUD/USD gains some positive traction for the fourth straight day amid sustained USD selling.

- The Fed’s dovish pivot continues to drag the US bond yields lower and weigh on the greenback.

- A softer risk tone seems to act as a headwind for the risk-sensitive Aussie ahead of the NFP report.

The AUD/USD pair reverses an intraday dip to sub-0.6800 levels and turns positive for the fourth successive day on Friday. The steady intraday ascent extends through the first half of the European session and lifts spot prices to the 0.6835 region, back closer to the highest level since September 13 touched on Thursday.

The US Dollar selling remains unabated amid rising bets for a less aggressive policy tightening by the Fed, which, in turn, acts as a tailwind for the AUD/USD pair. The dovish-sounding comments by Fed Chair Jerome Powell, along with signs of easing inflationary pressures, reaffirmed expectations that the US central bank will slow the rate-hiking cycle. This is evident from slugging US Treasury bond yields and continues to weigh on the greenback.

Furthermore, hopes of more stimulus from China and the easing of stringent COVID-19 restrictions in the world's second-largest economy offer additional support to the China-proxy Australian Dollar. That said, the cautious market mood could act as a headwind for perceived riskier currencies and keep a lid on any further gains for the AUD/USD pair. Traders also seem reluctant to place aggressive bets ahead of the US monthly employment details.

The popularly known NFP report is due later during the early North American session and will provide fresh insight into the US labour market. This might influence the Fed's policy outlook and drive the USD demand ahead of the next FOMC meeting on December 13-14. Apart from this, the broader market risk sentiment should provide some impetus to the AUD/USD pair. Nevertheless, spot prices seem poised to post gains for the second straight week.

Technical levels to watch

- The index drops to 6-month lows near 104.50 on Thursday.

- Further losses remain likely after a breakdown of the 200-day SMA.

- US Nonfarm Payrolls are expected at 200K in November.

The USD Index (DXY), which tracks the greenback vs. a bundle of its main competitors, remains well on the defensive and revisits multi-month lows around 104.50 at the end of the week.

USD Index looks at Payrolls

The index loses ground for the third session in a row on Friday and drops to levels last seen back in late June near 104.40, always in response to the increasingly deteriorated outlook for the greenback and the pick-up in the sentiment surrounding the risk-associated universe.

The rapid decline in the index has been exacerbated as of late and especially in response to Chair Powell’s speech on Wednesday, where he once again reiterated that a moderation in the pace of future interest rate hikes looks appropriated.

The march lower in the dollar comes in tandem with the absence of direction in US yields across the curve, which seem to have met some initial contention in recent multi-week lows.

Later in the NA session, all the attention will be on the release of the Nonfarm Payrolls for the month of November (200K exp.) and the Unemployment Rate (3.7% exp.), all ahead of the speech by Chicago Fed C.Evans (2023 voter, centrist).

What to look for around USD

The dollar extends the downside and revisits multi-month lows near 104.30 ahead of the key release of the US jobs report for the month of November.

While hawkish Fedspeak maintains the Fed’s pivot narrative in the freezer, upcoming results in US fundamentals would likely play a key role in determining the chances of a slower pace of the Fed’s normalization process in the short term.

Key events in the US this week: Nonfarm Payrolls, Unemployment Rate (Friday).

Eminent issues on the back boiler: Hard/soft/softish? landing of the US economy. Prospects for further rate hikes by the Federal Reserve vs. speculation of a recession in the next months. Fed’s pivot. Geopolitical effervescence vs. Russia and China. US-China persistent trade conflict.

USD Index relevant levels

Now, the index is retreating 0.24% at 104.48 and the breakdown of 103.41 (weekly low June 16) would pave the way for a test of 101.29 (monthly low May 30) and finally 100.00 (psychological level). On the other hand, the immediate resistance emerges at 105.55 (200-day SAM) followed by 107.19 (weekly high November 30) and then 107.99 (weekly high November 21).

The Bank of Japan (BoJ) bought JPY70.1 billion ($523.37 million) of exchange-traded funds (ETFs) on Friday, according to the central bank data.

The BoJ stepped into the market for the first time in six months afte the Japanese indices fell roughly 2% on Friday.

Irish Minister for Foreign Affairs and Defence, Simon Coveney, said on Friday, “trust is growing in protocol negotiations between the UK and Northern Ireland.”

“Landing zone on the protocol is possible in the next few weeks,” Coveney added.

His comments come a day after the European Commission's President Ursula von der Leyen said she has had "encouraging" meetings with Rishi Sunak over the Northern Ireland Protocol and is "very confident" a solution can be found.

Market reaction

GBP/USD is benefiting from the renewed selling in the US Dollar and the upbeat Brexit headlines, adding 0.26% on the day to trade at 1.2283, at the press time.

Today, the Bank of Canada will gain further important insight for next week’s rate decision with the labour market report for November. If the data surprises on the upside, the Loonie could surge higher, economists at Commerzbank report.

Continued constraints on the labour market?

“If today’s data remains within the framework of expectations (unemployment rate 5.3%; employment +10K) it should not impress the Loonie much. With a view to the BoC meeting next week the market seems to be expecting a smaller rate step of 25 bps.”

“The analysts polled by Bloomberg are divided. Whereas one half also expects BoC to switch down a gear, the other half expects it to hike its key rate by a further 50 bps. Against this background, a surprisingly strong labour market might well drive rate expectations up again, which would support the Loonie.”

See – Canadian Jobs Preview: Forecasts from five major banks, more lackluster performance

Further decline in USD/JPY is predicted to meet the next solid support at 134.00, comment UOB Group’s Economist Lee Sue Ann and Markets Strategist Quek Ser Leang.

Key Quotes

24-hour view: “Yesterday, we indicated that ‘The strong downward momentum in USD is likely to continue’. We added, ‘The support levels to monitor are at 136.40 and 135.50’. USD took out both support levels as it plunged to a low of 135.20 in NY trade. While further weakness is not ruled out, the massive drop over the past couple of days is overextended and it remains to be seen if USD could challenge the next support at 134.00 today. Resistance is at 135.90, a breach of 136.50 would indicate that the weakness in USD has stabilized.”

Next 1-3 weeks: “We indicated yesterday (01 Dec, spot at 137.20) that the strong surge in downward momentum is likely to lead to further USD weakness to 136.40, as low as 135.50. While our view was correct, we did not quite expect 135.50 to come view so soon as USD nose-dived to a low of 135.20. Downward momentum is unsurprisingly, still strong but it is left to be seen if USD could maintain the frenetic pace of decline. The next level to watch is at 134.00. On the upside, a breach of 137.05 (‘strong resistance’ level was at 138.55 yesterday) would indicate that the weakness in USD has stabilized.”

- USD/JPY drops to a fresh multi-month low on Friday amid sustained USD selling bias.

- The Fed’s dovish pivot and sliding US bond yields continue to weigh on the greenback.

- Technical selling below the 135.00 mark also contributes to the downward trajectory.

- Oversold conditions on short-term charts could help limit losses ahead of the US NFP.

The USD/JPY pair remains under some selling pressure for the fifth straight day and drops to its lowest level since August 17 during the early part of the European session on Friday. The pair is currently trading just below mid-134.00s, down over 0.50% for the day, with bears awaiting a convincing break through the very important 200-day SMA.

The prevalent bearish sentiment surrounding the US Dollar - amid expectations that the Fed will soften its policy stance - is seen as a key factor dragging the USD/JPY pair lower. The prospects for a less aggressive policy tightening by the Fed were reaffirmed by dovish-sounding remarks by Fed Chair Jerome Powell and signs of easing inflationary pressures. This, in turn, keeps the US Treasury bond yields depressed and continues to weigh on the greenback.

In fact, the yield on the benchmark 10-year US government drops to a nearly two-month low, narrowing the US-Japan rate differential. Apart from this, the overnight hawkish-sounding comments by Bank of Japan (BoJ) board member Asahi Noguchi continue to underpin the Japanese Yen and exert additional downward pressure on the USD/JPY pair. Noguchi hinted at the possibility of the pre-emptive withdrawal of stimulus if inflation overshoots expectations.