- Analiza

- Novosti i instrumenti

- Vesti sa tržišta

Forex-novosti i prognoze od 08-03-2023

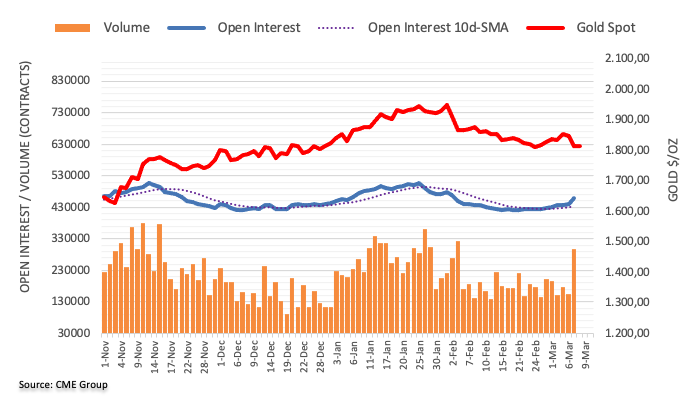

- Gold price seesaws around the key Fibonacci retracement level after Wednesday’s sluggish performance.

- Market players take a breather amid absence of any major surprise.

- United States Treasury bond yield curve inversion, hawkish Federal Reserve bias keep XAU/USD bears hopeful.

- US employment report for February is the key catalyst for Gold price, Nonfarm Payrolls gain major attention.

Gold price (XAU/USD) stretches Wednesday’s boring moves around $1,815 as it seeks more clues during early Thursday, amid a firmer bearish bias due to the hawkish Federal Reserve (Fed) concerns and recession woes.

That said, the yellow metal’s latest inaction could be linked to an absence of major surprise from the market’s, as well as cautious mood ahead of Friday’s key United States employment report for February. However, the widest yield curve inversion since 1981 joins the hawkish rhetoric from Fed Chair Jerome Powell to keep the XAU/USD bears hopeful.

Gold price stays dicey on Federal Reserve Chairman Powell’s repetitive remarks

Despite refreshing a one-week low, the Gold price failed to portray any major moves on Wednesday as Federal Reserve Chairman Jerome Powell repeated his hawkish remarks in front of the House Financial Service Committee. The policymaker highlighted the data-dependency of the Fed while also signaling that they have underestimated the resilience of growth and inflation. The news defends the hawkish Fed bias as market players expected 50 bps rate hike in March, versus 0.25% expected in the last week. With this, the XAU/USD remains depressed near the key Fibonacci retracement level.

United States data, Treasury bond yields favor XAU/USD bears

Although repeated comments from Fed’s Powell allowed Gold traders to catch a breather on Wednesday after the volatile Tuesday, upbeat United States data and strong Treasury bond yields exert downside pressure on the XAU/USD price.

On Wednesday, the US ADP Employment Change rose to 242K in February versus 200K market forecasts and 119K prior (revised). Further, the US Goods and Services Trade Balance dropped to $-68.3B from the $-67.2B previous reading (revised) and $-68.9B analysts’ estimations. It should be noted that the US JOLTS Job Openings for January improved to 10.824M versus 10.6M expected but eased from 11.234M revised prior.

It should be noted that the benchmark US Treasury bond yields rose in the last three consecutive days and raised recession fears via the widest difference between the two-year and 10-year bond coupons.

Elsewhere, the US removed testing restrictions on the travelers from China and joined a light calendar to allow the traders to lick their wounds after a volatile Tuesday.

Amid these plays, Wall Street closed mixed and the S&P 500 Futures also remains sidelined after a dicey day.

Moving on, China’s China’s monthly Consumer Price Index (CPI) and the Producer Price Index (PPI) for February could direct immediate Gold price moves ahead of the United States employment report, up for publishing on Friday.

Also read: Gold Price Forecast: Bulls losing the battle, $1,800 at sight

Gold price technical analysis

Gold price seesaws around the 61.8% Fibonacci retracement of its late November 2022 to the early last month’s run-up as bears await the key United States data to extend the weekly fall.

However, a clear downside break of the 3.5-month-old ascending trend line joins impending bear cross on the Moving Average Convergence and Divergence (MACD) indicator to keep the XAU/USD sellers hopeful.

It should be noted that the 100-DMA, around $1,805 by the press time, acts as an immediate downside support for the Gold price, a break of which could quickly fetch the XAU/USD toward testing the 200-DMA support of $1,775. That said, the $1,800 threshold may act as an intermediate halt durng the anticipated fall.

Meanwhile, corrective bounce needs to cross the previous support line from late November 2022, now resistance around $1,820.

Even so, the 50% Fibonacci retracement level and a two-month-long horizontal area, respectivelty near $1,840 and $1,858-62, could challenge the Gold buyers before giving them control.

It’s worth mentioning that the nearly oversold condition of the Relative Strength Index (RSI), placed at 14, suggests limited downside room for the metal.

Gold price: Daily chart

Trend: Further downside expected

- Silver price stabilizes after sliding close to 5% on Tuesday.

- XAG/USD Price Analysis: To resume its downward bias after dropping below $21.00.

Silver price reached a multi-month low of around $19.92, but buyers stepped in, dragging the XAG/USD price above the $20.00 figure.

Wall Street finished the session mixed. The US Federal Reserve Chair Jerome Powell rattled the US equities market after commenting that to testify against the US Congress with a consistent hawkish tone. Therefore, the US Dollar (USD) consolidates yesterday’s gains, as shown by the US Dollar Index up 0.09%, at 105.710.

XAG/USD Price Action

After dropping almost 5% on Tuesday, the XAG/USD collapse appears to have found a temporal bottom. The XAG/USD printed a new YTD low at $19.92. Wednesday’s price action formed a doji, indicating that buyers and sellers are at equilibrium. The Relative Strength Index (RSI) is at oversold conditions as sellers take a breather, while the Rate of Change (RoC) suggests that sellers are gathering momentum.

If the XAG/USD tumbles below the YTD low at $19.92, the next line of defense for XAG bulls would be $19.00, ahead of sliding toward November’s 3 low at $18.84.

In an alternate scenario, the XAG/USD first resistance would be February’s 28 daily low turned resistance at $20.43. A breach of the latter will clear the pave toward March’s 2 low at $20.68, before testing the $21.00 psychological level.

XAG/USD Daily chart

XAG/USD Technical levels

Japan's Gross Domestic Product has been released by the Cabinet Office as follows:

- Japanese GDP Annualised SA (QoQ) Q4 F: 0.1% (exp 0.8%; prev 0.6%).

- GDP SA (Q/Q) Q4 F: 0.0% (exp 0.2%; prev 0.2%).

- GDP Nominal SA (QoQ) Q4 F: 1.2% (exp 1.3%; prev 1.3%) .

USD/JPY is flat and hovers around 137.20 while the US Dollar paused its advance following Federal Reserve Jerome Powell's second day on Capitol Hill where he repeated his hawkish message that key interest rates could be raised faster than previously anticipated.

About Japan's Gross Domestic Product

The Gross Domestic Product released by the Cabinet Office shows the monetary value of all the goods, services and structures produced in Japan within a given period of time. GDP is a gross measure of market activity because it indicates the pace at which the Japanese economy is growing or decreasing. A high reading or a better than expected number is seen as positive for the JPY, while a low reading is negative.

US president Joe Biden and EU's Ursula Von der Leyen are expected to agree on Friday to work toward a trade deal and it is said the US will give the EUR a free-trade agreement-like status.

More to come...

- GBP/JPY is marching towards 163.00 on expectations of a dovish BoJ policy.

- According to a Reuters poll, the BoJ will tweak its YCC in April-June.

- It is expected that UK’s Manufacturing sector has contracted in January.

The GBP/JPY pair has witnessed a mild correction after a perpendicular upside move to near 162.80 in the early Asian session. The cross is approaching the critical resistance of 163.00 as investors are expecting the maintenance of ultra-loose monetary policy by the Bank of Japan (BoJ), which is scheduled for Friday.

BoJ Governor Nominee Kazuo Ueda has already confirmed that current inflationary pressures in Japan are backed by higher import prices. Japan’s labor cost index is still struggling to get on its feet and contribute to overall inflation. Also, domestic demand is insufficient to fuel the Consumer Price Index (CPI). Therefore, BoJ Ueda favored for the continuation of expansionary monetary policy.

The last monetary policy dictation by BoJ Governor Haruhiko Kuroda is expected to have an absence of a roadmap for an exit from prolonged easy policy.

According to a Reuters poll, April’s monetary policy, the first one by BoJ Ueda will be full of surprises. A Reuters poll indicates BoJ will start unwinding its ultra-easy policy in April. Also, the market participants are expecting further tweaks in the Yield Curve Control (YCC) in April-June.

Going forward, Japan’s Gross Domestic Product (GDP) (Q4) data will be keenly watched. The quarterly GDP is expected to remain steady at 0.2%. While the annualized figure is expected to improve to 0.8% from the former release of 0.6%.

On the United Kingdom front, investors are awaiting the release of the manufacturing sector data, scheduled for Friday. Monthly Manufacturing production (Jan) is expected to contract by 0.1% and the Industrial Production is seen contracting by 0.2% in the same period.

Dovish commentary from Bank of England (BoE) policy maker Swati Dhingra could put the Pound Sterling on the tenterhooks. BoE Dhingra has warned against further interest rate increases by citing “Overtightening poses a more material risk at this point.” She further added, “Many tightening effects are yet to fully take hold.”

Britain’s finance ministry said on Wednesday it will launch a review into how investor research on companies could be improved to attract more listings, a step that follows a decision by UK chip designer Arm Ltd to only list in New York, reported Reuters.

The Ministry also mentioned that the Investment Research Review will be launched next Monday and chaired by Rachel Kent, a veteran financial services lawyer at Hogan Lovells, who will report back to City minister Andrew Griffith within three months.

Also read: BCC: UK to avoid recession this year but outlook still weak

Key quotes

It seeks to develop concrete steps the government can take to enhance London’s status as Europe’s leading listings destination, and only second globally.

Investors use research from analysts at banks and brokers for picking stocks, but concerns have been raised about the quality and quantity of research produced in Britain, particularly for tech and life sciences.

GBP/USD stays pressured

The news fails to improve the Cable’s conditions amid a light calendar in Asia. That said, the quote remains depressed near 1.1850 as the US Dollar bulls occupy the driver’s seat.

Also read: GBP/USD retreats from 1.1850 as risk-off mood rebounds amid tight US labor market

- US Dollar Index retreats from three-month high within an ascending trend channel from February.

- Sour-sentiment, 100-DMA and upbeat oscillators allow DXY bulls to stay hopeful.

- 200-DMA acts as an extra filter to the north; bears need validation from 104.30.

US Dollar Index (DXY) grinds near the highest levels since early December 2022, making rounds to 105.65-70 during early Thursday. In doing so, the greenback’s gauge versus the six major currencies remains inside a one-month-old bullish channel, as well as keeping the previous day’s corrective bounce off the 100-DMA.

Apart from the 100-DMA support, the bullish MACD signals also keep the DXY buyers hopeful. However, the RSI (14) line approaches the overbought territory as the US Dollar Index (DXY) nears the aforementioned trend channel’s top line, close to 106.15, which in turn suggests limited upside room for the greenback’s gauge.

Adding strength to the 106.15 hurdle is the 38.2% Fibonacci retracement level of the DXY’s fall from the last September to the previous month.

Even if the quote crosses the 106.15 resistance confluence, the 200-DMA hurdle surrounding 106.70 appears a tough nut to crack for the US Dollar Index bulls.

On the flip side, a clear break of the 100-DMA support of 105.25 isn’t an open invitation to the DXY bears as the previously mentioned bullish channel’s support line could test the quote’s further downside near 104.30.

In a case where the DXY remains bearish past 104.30, the odds of witnessing a slump toward the previous monthly low of 100.80 can’t be ruled out.

US Dollar Index: Daily chart

Trend: Limited upside expected

- AUD/JPY remains depressed around six-week low, fading the previous day’s corrective bounce.

- Sour sentiment joins pre-data anxiety to weigh on the risk barometer pair.

- Dovish comments from RBA’s Lowe, hopes of an end to BoJ’s ultra-easy monetary policy weigh on prices.

- Japan’s final readings of Q4 GDP, China inflation data for February will be crucial for immediate direction.

AUD/JPY renews its intraday low near 90.45 while posting mild losses on a day during the early hours of Thursday morning in Asia. In doing so, the cross-currency pair portrays the dicey markets ahead of the key data/events.

Traders appear cautious amid fears of the Bank of Japan’s (BoJ) exit from its multi-year low ultra-easy monetary policy once Haruhiko Kuroda bid adieu in April. On the same line are the dovish expectations from the Reserve Bank of Australia (RBA), mainly after downbeat comments from RBA Governor Philip Low.

On Wednesday, RBA’s Lowe said that the RBA was closer to pausing its aggressive cycle of rate increases as the policy was now in the restrictive territory and there were signs the economy was responding. It should be noted that Lowe also mentioned, “China reopening is positive for our economy,” while also adding that no particular implications for inflation from China reopening.

On the other hand, BoJ announced one more unplanned bond market move and teased readiness for a hawkish stunt after April. That said, Reuters’ poll mentioned, "The Bank of Japan (BoJ) will end its long-term yield control policy this year." The February 28 to March 6 survey of 26 respondents also anticipated that academic Kazuo Ueda's new leadership will dismantle the complex easing scheme and restore bond market functionality.

Elsewhere, the US removed testing restrictions on travelers from China and joined a light calendar to allow the traders to lick their wounds after a volatile Tuesday.

Amid these plays, Wall Street closed mixed and the US Treasury bond yields remained firmer with minor moves and keeping the yield curve inversion the widest since 1981.

Looking ahead, the final readings of Japan’s fourth quarter (Q4) Gross Domestic Product (GDP), expected to confirm the 0.2% QoQ initial estimate, will join China’s monthly Consumer Price Index (CPI) and the Producer Price Index (PPI) for February to direct immediate AUD/JPY moves. Above all, risk catalysts are the key for cross-currency pair traders to watch for clear directions.

Technical analysis

A 1.5-month-old horizontal support zone near 90.25-15 precedes an ascending support line from early January, close to 90.10, as well as the 90.00 round figure, to challenge immediate AUD/JPY downside.

- USD/CHF is constantly auctioning above 0.9400 and is expected to extend its upside journey amid the overall risk-off mood.

- The upside bias for the USD index is intact amid expectations of more resilience in the US labor market.

- An increase in US Average Hourly Earnings data might fuel inflationary pressures ahead.

The USD/CHF pair is holding its auction above the critical support of 0.9400 in the early Asian session. The Swiss Franc asset is expected to resume its upside journey later as solid United States labor market data indicates that the fears of persistent inflation in the sentiment of Federal Reserve (Fed) policymakers are real and bigger rates are in pipeline to squeeze galloping inflation.

S&P500 futures settled Wednesday’s session with modest gains despite mounting recession fears in the United States on expectations that the Federal Reserve (Fed) is considering a higher terminal rate due to renewed fears of a higher Consumer Price Index (CPI). The US Dollar Index (DXY) has shifted into a volatility contraction phase and the upside bias is still intact amid expectations of more resilience in the labor market.

Meanwhile, the overall risk-aversion theme has failed to infuse fresh blood into the US Treasury yields. The alpha delivered on 10-year US Treasury bonds has failed to sustain above 4.0%.

Fed chair Jerome Powell continued his hawkish remarks on Wednesday citing "Costs of not getting inflation down will be extremely high." He further added, "Costs of failure to control inflation would be much higher than costs of controlling it." Fed’s Powell also discussed the positive impact of China’s reopening to the prices of commodities, which will also propel price pressures. However, the reopening measures will also trim supply chain disruptions.

After an upbeat US Automatic Data Processing (ADP) Employment Change data, investors are shifting their focus toward US Nonfarm Payrolls (NFP) data, which is scheduled for Friday. The economic data is seen at 203K lower than the former bumper release of 517K. The Unemployment Rate is seen steady at 3.4%. Investors would be worried about Average Hourly Earnings data, which is expected to increase to 4.8% vs. the prior release of 4.4% on an annual basis.

On the Swiss Franc front, Swiss National Bank (SNB) Chairman Thomas J. Jordan stated the inflation in Switzerland is low in international comparison but above the handling capacity of the SNB. He further explained that the appreciation of the Swiss Franc has protected them from imported inflation.

“The country's economy is on track to shrink less than expected this year and avoid the two quarters of negative growth which mark a technical recession,” the British Chambers of Commerce (BCC) forecast on Wednesday per Reuters.

Key findings

Gross Domestic Product (GDP) would fall by 0.3% this year, a smaller decline than its previous forecast of a 1.3% fall, after stronger activity at the end of 2022.

On a quarterly basis GDP is forecast to fall 0.3% in the first quarter of 2023, before showing zero growth in the second quarter and rising by 0.2% in each of the third and fourth quarters of 2023.

The BCC expects the economy to grow 0.6% next year, while the Bank of England (BoE) predicted a quarter percent contraction for 2024 last month.

Britain is the only Group of Seven economy that has yet to rebound to its pre-pandemic size and the BCC forecast it would not return to that level until the final quarter of 2024.

While consumers and businesses still face a hit from double-digit inflation, the BCC expects inflation to drop to 5% in the fourth quarter and 1.5% by late 2024.

The BCC expects BoE rates to be a quarter-point higher at the end of the year than they are now - taking rates to 4.25% - and then for rates to be cut to 3.5% by late 2024.

Also read: GBP/USD retreats from 1.1850 as risk-off mood rebounds amid tight US labor market

- NZD/USD fades bounce off the lowest levels since late November 2022 inside one-month-old descending trend channel.

- Failure to cross previous support line from early January, bearish MACD signals keep sellers hopeful.

- Recovery remains elusive below 200-SMA, 0.6215-20 acts as an additional upside filter.

NZD/USD retreat towards the multi-day low marked the previous day while staying with a one-month-old descending trend channel, pressured around 0.6105 during the early Thursday morning in the Asia-Pacific zone.

In doing so, the Kiwi pair portrays the inability to cross the two-month-long previous support line, now immediate resistance near 0.6130. Adding strength to the downside bias are the bearish MACD signals.

It’s worth noting, however, that the lower line of the aforementioned bearish channel, around 0.6070 by the press time, as well as the lows marked during mid-November 2022 near 0.6060, can act as crucial supports to watch during the NZD/USD pair’s further downside.

Should the Kiwi pair remains bearish past 0.6060, the odds of witnessing a slump toward the 0.6000 psychological magnet can’t be ruled out.

Alternatively, recovery moves remain elusive unless the quote stays below the support-turned-resistance line near 0.6130.

Even so, a convergence of the 100-SMA and the stated channel’s top line, close to 0.6215-20 at the latest, will be important for the NZD/USD buyers to break before retaking control.

Above all, the Kiwi pair remains on the bear’s radar unless it successfully trades above the 200-SMA hurdle surrounding 0.6315.

NZD/USD: Four-hour chart

Trend: Further downside expected

- GBP/USD has sensed selling interest after a less confident recovery to near 1.1850 amid the risk-off mood.

- Fed’s Powell has reiterated the need for bigger rates to bring down persistent US inflation.

- BoE Dhingra cited that overtightening poses a more material risk at this point.

The GBP/USD pair is observing selling pressure around 1.1850 in the early Tokyo session after remaining sideways on Wednesday. The Cable might deliver sheer losses after surrendering the immediate support of 1.1800. The downside bias for the Cable looks favored as Federal Reserve (Fed) chair Jerome Powell has reiterated the need for bigger rates to bring down persistent United States inflation.

S&P500 futures are showing modest gains, however, the recovery move looks less confident, which could be capitalized as a selling opportunity by the market participants. The US Dollar Index (DXY) settled above 105.20 after a volatile day inspired by upbeat United States Employment data reported by Automatic Data Processing (ADP) agency.

The release of the fresh payrolls addition at 242K vs. the consensus of 200K and the prior release of 119K has confirmed that the US labor market is extremely tight and investors should be prepared to face the extreme stubbornness of inflation. It is highly expected that firms will offer higher wages to fetch talent onboard amid a shortage of labor. This will deliver more funds to households for disposal, which will increase resilience in overall consumer spending.

Also, upbeat Job Openings data added fuel to the fire. The economic data landed at 10.824 million vs. the consensus of 10.6K. Higher job openings demonstrate the overall demand, which is going to propel the Consumer Price Index (CPI).

Later this week, the official labor market data will be keenly watched by the street. As per the estimates, the US Nonfarm Payrolls (NFP) (Feb) is expected to land at 203K lower than the former bumper release of 517K.

On the United Kingdom front, falling odds of more restrictive monetary policy is expected to keep the Pound Sterling on the tenterhooks. Bank of England (BoE) policy maker Swati Dhingra warned against further interest rate increases by citing “Overtightening poses a more material risk at this point.” She further added, “Many tightening effects are yet to fully take hold.”

- EUR/USD has carved out an M-formation with a 50% mean reversion eyed.

- 1.0520 guards 1.0480 while bulls will need to get above 1.06 to open risk to 1.0700.

EUR/USD was little changed at 1.0547 but it fell to 1.0524 was trading just above this year's low of 1.04820 reached on Jan. 6. after Federal Reserve Chairman Jerome Powell offered no major surprises on his second day of testimony before Congress and as investors waited for jobs data on Friday.

The Fed's decisions will be hinging on data to be issued before the US central bank's policy meeting in two weeks which makes this week's US nonfarm Payrolls event key for EUR/USD. The price is rested above key structural support ahead of the event as the following illustrates:

EUR/USD daily charts

The price has carved out an M-formation which is a pattern that tends to see a retest of the neckline near a 50% mean reversion in this particular case. 1.0520 guards 1.0480 while bulls will need to get above 1.06 to open risk to 1.0700.

- AUD/USD reverses early Wednesday’s corrective bounce, remains pressured at four-month low.

- Sour sentiment, dovish comments from RBA’s Lowe joined upbeat US data to weigh on Aussie price.

- Inactive markets restrict AUD/USD moves ahead of key data.

- China CPI/PPI can entertain traders before Friday’s US jobs report.

AUD/USD holds its place on the bear’s radar, after an initial attempt to leave the zone, as it stays depressed near 0.6590 amid early Thursday morning in Asia.

The Aussie pair tried paring weekly losses at the lowest levels in four months during early Wednesday amid sluggish markets. However, dovish comments from Reserve Bank of Australia (RBA) Governor Philip Lowe joined upbeat US data and repetition of the hawkish statements from Federal Reserve Chairman Jerome Powell confirmed the bear’s dominance. It should be noted that the cautious mood ahead of today’s China inflation numbers seems to probe the risk barometer, due to its ties with the dragon nation.

On early Wednesday, the US removed testing restrictions on the travelers from China and joined a light calendar to allow the traders to lick their wounds after a volatile Tuesday. However, RBA’s Lowe said that the RBA was closer to pausing its aggressive cycle of rate increases as the policy was now in the restrictive territory and there were signs the economy was responding. It should be noted that Lowe also mentioned, “China reopening is positive for our economy,” while also adding that no particular implications for inflation from China reopening.

Elsewhere, Fed’s Powell repeated his hawkish calls of readiness to lift the rate while highlighting stronger-than-expected inflation pressure. The same bolstered calls for the Fed’s 50 bps rate hike but the Testimony 2.0 didn’t have anything new from what’s already heard on Tuesday and hence traders were mostly afraid of taking any major steps.

Talking about the data, the US ADP Employment Change rose to 242K in February versus 200K market forecasts and 119K prior (revised). Further, the US Goods and Services Trade Balance dropped to $-68.3B from the $-67.2B previous reading (revised) and $-68.9B analysts’ estimations. It should be noted that the US JOLTS Job Openings for January improved to 10.824M versus 10.6M expected but eased from 11.234M revised prior.

Against this backdrop, Wall Street closed mixed and the US Treasury bond yields remained firmer with minor moves and keeping the yield curve inversion the widest since 1981, which in turn allowed the US Dollar Index (DXY) to remain firmer.

Looking ahead, China’s monthly Consumer Price Index (CPI) and the Producer Price Index (PPI) for February will be important after the latest improvements in the Aussie-China ties. However, RBA’s Lowe has already mentioned no effects of the inflation emanating from China reopening on Canberra and the same could weigh on the AUD/USD in case of a downbeat outcome. Above all, Friday’s US Nonfarm Payrolls are the key to clear directions.

Technical analysis

AUD/USD sellers appear to run out of steam amid oversold RSI (14) conditions. With this, the 0.6540-20 support zone, marked during September-November 2022, gains major attention. The recovery moves, however, remain elusive unless the quote offers a daily closing beyond the one-month-old descending trend line, previous support around 0.6615.

- USD/CAD has jumped above 1.3800 as hawkish Fed bets have strengthened the risk-off mood.

- The Canadian Dollar has been impacted by steady BoC policy and lower oil prices.

- An upbeat US ADP Employment data indicates an extension in the inflationary pressures.

The USD/CAD pair has scaled above the round-level resistance of 1.3800 in the early Asian session. The Lonnie asset has been strengthened further by unchanged monetary policy by the Bank of Canada (BoC) and hawkish remarks from Federal Reserve (Fed) chair Jerome Powell in his testimony before Congress.

S&P500 futures have shown a modest recovery but the recovery move looks insufficient in considering a decent improvement in the risk appetite of the market participants. The 10-year US Treasury yields dropped below 4.0%.

The US Dollar Index (DXY) is demonstrating volatility contraction after some volatile moves inspired by better-than-anticipated United States Employment data reported by Automatic Data Processing (ADP) agency. The economic data landed at 242K, higher than the expectations of 200K and the former release of 119K. Also, the job openings data soared to 10.824 million vs. the consensus of 10.6K. A follow-up solid labor market data indicates that the US inflation is expected to be sticky further as upbeat demand for talent will be offset by higher wages offered.

Fed’s Powell reiterated on Wednesday that the “Fed is prepared to increase the pace of interest rate hikes” to help inflation return to the 2% target. This kept the US Dollar bulls at the driving seat.

On the Canadian Dollar front, as expected the BoC Governor Tiff Macklem announced an unchanged interest rate policy. A steady interest rate decision by the BoC was highly expected as BoC’s Macklem already announced a pause in the policy tightening spell in January’s monetary policy meeting. The central bank believes that the current monetary policy is restrictive enough to tame Canada’s sticky inflation.

Meanwhile, oil prices have trimmed further amid deepening demand worries as the Fed sounds extremely hawkish on the interest rate guidance. It is worth noting that Canada is a leading exporter of oil to the United States and lower oil prices will impact the Canadian Dollar.

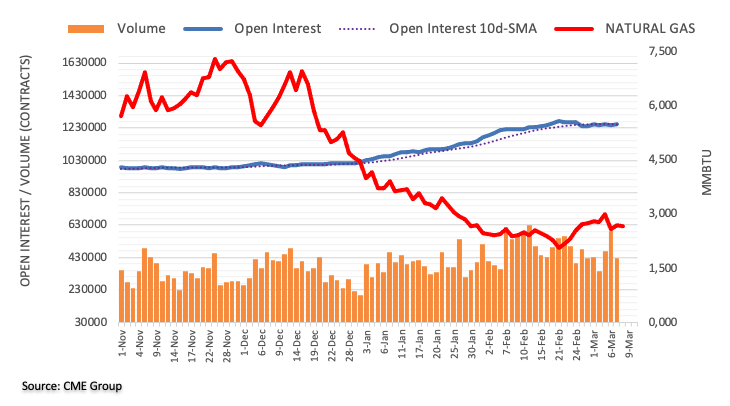

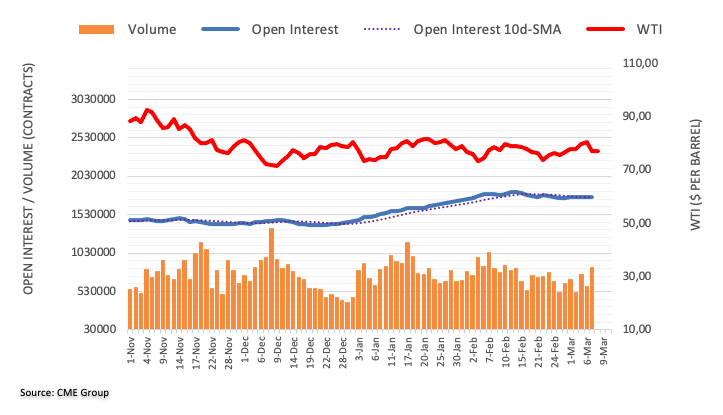

- WTI has dropped in the last two days 3% on speculations about future Federal Reserve rate hikes.

- US crude oil inventories dropped, putting a lid on WTI’s fall.

- WTI Price Analysis: Further downside is expected below $74.00.

Western Texas Intermediate (WTI), the US crude oil benchmark, falls 0.93% as Federal Reserve’s (Fed) Chair Jerome Powell’s two-day testify in the US Congress ended. The aftermath leaves the US Dollar (USD) gaining, US Treasury bond yields up, and speculations for a 50 bps rate hike at the Fed’s upcoming meeting looming. At the time of typing, WTI is trading at $76.44 PB.

Oil prices extended its losses based on hawkish commentary by Fed Chief Jerome Powell, who said that rates would peak higher than expected and at a faster pace if needed. The greenback appreciated sharply and jumped more than 1%, spurring WTI’s 3% fall.

US crude oil inventories fell 1.7 million last week, exceeding estimates for a 395K drop, according to the US Energy Information Administration (EIA) agency.

Oil demand is expected to increase based on China’s reopening. Barclays lowered its WTI forecast from $94.00 a barrel to $87.00. “(We) expect the continued recovery in civil aviation demand in China and neighboring countries, a stabilization in industrial activity, and slower non-OPEC+ supply growth to drive the oil market balance into a deficit later this year,” Barclays analysts added.

At a Houston meeting, oil officials discussed how tight the supply was. Angola’s oil and gas chief said OPEC did not have to raise production to compensate for Russia’s half-a-million-barrel-per-day reduction.

WTI Technical analysis

WTI consolidates at around the $74.00-$78.00 range, with the 20 and 50-day Exponential Moving Averages (EMAs) overlapping against each other. Contrarily, the 100 and 200-day EMAs, at 80.31 and 83.90, respectively, hover above WTI’s spot price, maintaining the bias tilted downwards. Traders should know that the Relative Strength Index (RSI) shifted bearish while the Rate of Change (RoC) followed suit.

For a bearish continuation, WTI needs to clear $74.00. Once done, the next support would be the February 22 daily low at 73.83, followed by the February 6 low at 72.30, before testing the YTD low of $70.10. Conversely, WTI needs to clear the $77.51-$78.03 area, the confluence of the 20/50-day EMAs. A breach of that area will expose the 100-day EMA at $80.31.

- Gold bears remain in play while below key resistance and eye a break of $1,800.

- US jobs market data is eyed as next key catalyst.

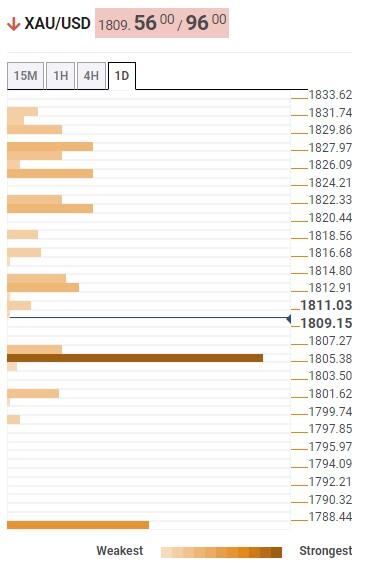

Gold prices fell for a second day on Wednesday although markets stabilised following yesterday’s rout as traders await the February Nonfarm Payrolls this week and Consumer Price Index data next week. at the time of writing, Gold price is flat near $1,1814 and has traded between $1,809.42 and $1,824.30.

Fed Chair Powell’s remarks in his repeat testimony to the House Financial Service Committee were that the Fed is data dependent, and no decision has been made yet about the size of a March hike, analysts at ANZ Bank said. ''This helped to calm price action, despite the fact that Powell’s assessment is that the Fed has underestimated the resilience of growth and inflation recently. Ahead of the March interest rate decision, Powell noted that the Fed will be watching JOLTS, CPI, PPI and the labour market report,'' they said, adding, ''we think it will require much weaker data for the FOMC to step back from Powell’s more hawkish assessment of the landscape.''

Meanwhile, Gold price is heavy due to the DXY Dollar index rising to the highest since December after Fed's Powell said in Tuesday's Senate testimony that the US economy is shrugging off higher interest rates and emphasised that the Fed was ready to raise rates higher and faster to slow growth and lower inflation. The ICE dollar index was last seen printing 105.66, making gold more expensive for international buyers. Bond yields were also higher, bearish for the metal since it offers no interest. The US 10-year note was last seen paying 3.979%.

US Nonfarm Payrolls eyed

As for the Nonfarm Payrolls, markets anticipate a still firm pace in Feb after an unexpected 517k surge in Jan and the UE rate to stay unchanged at 3.4% with wage growth printing another strong 0.4% for the month. In a deeper dive, analysts at ANZ bank said that ''last year, the US economy created 4.8m nonfarm payroll jobs. In the 2010s, the average annual jobs creation was 2.2m. Returning jobs growth to that historical average pace requires monthly jobs growth to slow to just 180k. Even that may still be too strong for inflation to return to 2.0% given ongoing labour supply issues,'' the analysts explained. ''The CBO estimates that the increase in the workforce this year will be 1.2m, and 1.1m in 2024. This would suggest that balancing the labour market requires average monthly jobs growth of 100k or less. Given strong labour market demand, such projections by the CBO imply the scarcity of skilled workers will continue, firms will continue to hoard labour and unemployment may remain at current lows. That just means a more hawkish Fed.''

Gold technical analysis

As for the technical outlook, analysts at TD Securities said, ''a potential break below the $1806/oz level would serve as the next trigger to see trend followers modestly reduce their positions.''

It was explained in the Chart of the Week article, Gold, the Chart of the Week: XAU/USD bulls ride H4 dynamic support on key week ahead that the Gold price was riding dynamic support that would be expected to hold initial tests ''but a break thereof opens the risk of a move to test the $1,825 all-important support structure. A break there will most probably see a flurry of orders triggered and a fast subsequent move lower.''

As illustrated above, we have seen that break happen which leaves $1,800 vulnerable and the $1,770s.

Here is what you need to know on Thursday, March 9:

It the second day of testimony, FOMC Chairman Jerome Powell did not surprise markets, after he left the door wide open to a 50 basis points rate hike at the March meeting, and the US Dollar jumped to monthly highs. After a brief retreat on Wednesday, the Greenback erased losses. If Dollar’s momentum holds, a test of the recent highs during the Asian session seems likely. China will report inflation, and Japan a new estimate of Q4 GDP.

In the US, Automatic Data Processing (ADP) reported that private sector employment rose by 242K in February, surpassing expectations of 200K. The US Bureau of Labor Statistics (BLS) revealed that January job openings reached 10.8 million, slightly higher than the market expectation of 10.6 million. The numbers continue to show a tight labor market, helping the US Dollar and supporting Fed’s hawkish tone. On Thursday, the weekly Jobless Claims report is due. Market participants await the Nonfarm payrolls on Friday and next week’s Consumer Price Index.

Markets stabilized somewhat following Tuesday’s sell-off, but risk aversion dominates. US Treasury yields moved in tandem with the US Dollar, falling and then rebounding toward Tuesday’s highs. The US 10-year yield settled around 3.97%, and the 2-year rose back above 5%.

EUR/USD rose to 1.0575, only to decline later below 1.0550. Despite mixed data from the Eurozone, market participants are looking to a higher terminal rate from the European Central Bank, supporting the Euro.

GBP/USD remains under pressure, although it holds near, but above, the critical 1.1800 area. EUR/GBP is hovering around 0.8900. Bank of England’s Swati Dhingra called for a no change in interest rates.

USD/JPY posted a close above 137.00 but, at the same time, far from the daily high and below the 200-day Simple Moving Average. On Friday, the Bank of Japan will announce its decision on monetary policy.

The Bank of Canada kept interest rates unchanged and signaled it will continue on pause. As a result, the Loonie fell across the board. USD/CAD rose to four-month highs above 1.3800.

Reserve Bank of Australia Governor Philip Lowe said the central bank will be guided by incoming data to decide on another hike or a pause at the next monetary policy meeting. His comments echoed Tuesday’s monetary policy meeting. AUD/USD rebounded after hitting a fresh four-month low; however, it failed to hold above 0.6600 and remains under pressure.

Gold showed a strong negative correlation to Treasury yields and the DXY. XAU/USD remained above the critical $1,800, unable to stage a recovery. Silver settled around $20.00 after testing levels below that psychological mark.

Gold Price Forecast: Bulls losing the battle, $1,800 at sight

Crude oil prices kept going south, hitting fresh weekly lows. Cryptocurrencies oscillated between gains and losses on Wednesday. Bitcoin is moving around $22,000, while Ethereum around $1,560.

Like this article? Help us with some feedback by answering this survey:

Reuters reported on the Federal Reserve's Beige Book and noted that the report said that the US economic activity increased slightly from January through late February and price increases remained widespread, but businesses reported a moderation in inflation that they expect to continue this year.

- This report was prepared at the federal reserve bank of new york based on information collected on or before February 27, 2023.

- Overall economic activity increased slightly in early 2023.

- Inflationary pressures remained widespread, though price increases moderated in many districts.

- Amid heightened uncertainty, contacts did not expect economic conditions to improve much in the months ahead.

- Six districts reported little or no change in economic activity since the last report, while six indicated economic activity expanded at a modest pace.

- On balance, loan demand declined, credit standards tightened, and delinquency rates edged up.

US Dollar update

The US dollar was steady near 105.70 as per the DXY index following the release but it was down from three-month highs reached earlier on Wednesday after Federal Reserve Chairman Jerome Powell offered no major surprises on his second day of testimony before Congress. eyes are now on the US Nonfarm Payrolls at the end of the week.

- AUD/USD bears stay in charge with eyes on a downside extension.

- The pair have made a correction and bears have moved in again.

As per the prior analysis, AUD/USD falls heavily as bears move in towards the 0.6580s target area, AUD/USD moved in on the target and holds within the region with a bearish bias ahead of the US Nonfarm Payrolls this Friday.

AUD/USD H4 & H1 charts

Prior analysis:

AUD/USD update

AUD/USD has already made a recovery that came in close contact with the 38.2% ratio which leaves prospects of a move to the downside with 0.6520 eyed.

- USD/CHF is almost flat, retraces 0.04% at around 0.9410s.

- A USD/CHF bullish continuation would trigger if the major cracks the 200-day EMA, with 0.9500 up for grabs.

- Otherwise, the USD/CHF falling below 0.9400 will expose the 100-day EMA.

The USD/CHF is firm above 0.9400, shy of the 200-day Exponential Moving Average (EMA), after rallying 1.21% on Tuesday. Also, it’s forming a doji around current exchange rates, trading at 0.9414 at the time of typing.

Wall Street continues to trade with losses. The US Federal Reserve Chair Jerome Powell continues to testify against the US Congress with a consistent hawkish tone. Therefore, the US Dollar (USD) consolidates yesterday’s gains, as shown by the US Dollar Index up 0.09%, at 105.710.

USD/CHF Price action

The USD/CHF remains sideways, trapped within the 100 and the 200-day EMAs, at 0.9384 and 0.9449, respectively. The Relative Strength Index (RSI) turned bullish, aimed north on Tuesday, indicating buyers are moving in. However, as of late turned flat, consistent with the USD/CHF price action. The Rate of Change (RoC) portrays buyers taking a breather before attempting to attack the 200-day EMA.

If the USD/CHF resumes upwards, the first resistance would be the 200-day EMA. A breach of the latter will send the pair rallying toward 0.9500. Once buyers reclaimed the 0.95 figure, the seller’s following line of defense would be the November 30 daily high at 0.9547. That could pave the way towards the November 21 high at 0.9598 before challenging 0.9600.

As an alternate scenario, the USD/CHF first demand area would be the 0.9400 psychological barriers, followed by the 100-day EMA at 0.9384. Once cleared, sellers could drag prices toward the 20-day EMA at 0.9331.

USD/CHF Daily chart

USD/CHF Technical levels

- NZD/USD consolidates the US Dollar's strength and sits at key support

- The Kiwi is tucked in below horizontal and trendline resistance that has a confluence with the 38.2% ratio.

NZD/USD is flat on the day during the late lunch hour of the US session with the US Dollar's rally slowing up after reaching 105.88 vs. a basket of currencies, the highest since December 1. NZD/USD has ranged between a low of 0.6084 and 0.6137 thus far.

On Tuesday, Fed's chairman surprised markets with a more hawkish rate outlook by saying that the board would likely need to raise interest rates more than expected in response to recent strong data and is prepared to move in larger steps if the "totality" of incoming information suggests tougher measures are needed to control inflation.

This has led the Fed funds futures markets to price in a 66% probability of a 50 basis-point hike at the Fed’s March 21-22 meeting, up from around 22% before Powell spoke on Tuesday. The rate is now expected to peak at 5.62% in September. ''Looking ahead, 25 bp hikes in May and June are priced in that would take Fed Funds to 5.50-5.75%, with nearly 30% odds of a last 25 bp hike in Q3 that would move the range up to 5.75-6.0%,'' analysts at Brown Brothers Harriman said.

''After all this, an easing cycle is still expected to begin in Q4, albeit at much lower odds. Eventually, it should be totally and unequivocally priced out into 2024 during the next stage of Fed repricing. For now, we believe the uptrends in US yields and the dollar remain intact,'' the analysts added.

Looking ahead, investors are now focused on February jobs data in Nonfarm Payrolls that is due on Friday. ''US payrolls likely mean-reverted to a still firm pace in Feb after an unexpected 517k surge in Jan. We also look for the UE rate to stay unchanged at 3.4%, and wage growth to print a strong 0.4% MoM,'' analysts at TD Securities said.

RBNZ outlook

Meanwhile, analysts at ANZ Bank said that they continue to see the reserve Bank of New Zealand hiking the OCR to a peak of 5.25% by May 2023, and holding it there until at least the end of 2024. ''But the tight labour market and uncertain cyclone impacts represent upside risks to the outlook for both inflation and the OCR.''

NZD/USD technical analysis

NZD/USD is tucked in below horizontal and trendline resistance that has a confluence with the 38.2% ratio with prospects of a firmer correction as it holds in support near 0.61 the figure.

- EUR/USD meanders slightly above the 200-day EMA, a magnet for EUR/USD bears.

- Hotter-than-expected US labor market data warrants further rate hikes by the Fed.

- ECB’s policymakers split by tightening aggressively or gradually.

- EUR/USD Price Analysis: If the pair tumbles below the 200-DMA, that would pave the way towards 1.0400.

EUR/USD remains unchanged at 1.0545, below the 200-day Exponential Moving Average (EMA) as Fed Chair Jerome Powell testifies before the US Congress. Meanwhile, US equities continued to fluctuate, portraying a mixed sentiment, while the US Dollar turned positive. At the time of writing, the EUR/USD is trading at 1.0545.

EUR/USD stays firm around familiar levels amidst the lack of a catalyst

The EUR/USD has failed to gain traction either way after US economic data backed the latest commentaries by Jerome Powell. Although January’s JOLTs report showed a decrease In openings at 10.8M, it exceeded estimates of 10.5M.

Earlier, the February US ADP Employment Change report revealed that the US private sector added 242,000 jobs, more than the expected 200,000. That said, figures from both reports reinforced what Federal Reserve officials have commented about a tight labor market, which would warrant further tightening by the Federal Reserve. That could weigh on the Euro (EUR); therefore, a further downside in the EUR/USD is expected.

Before Wall Street opened, the Richmond Fed President Thomas Barkin commented that inflation is still high and that the Fed stills have work to do. Later at the US House of Representatives, Fed Chief Jerome Powell said that the Fed had not decided yet about the upcoming March meeting. Powell added that China’s reopening could spur another round of inflation due to higher commodity prices.

In the Euro area (EU), European Central Bank (ECB) policymakers have remained hawkish. Earlier in the week, ECB’s Knot said that the central bank needs to keep hiking rates for some time, echoing Robert Holzmann’s words to raise rates by 50 bps due to stubborn inflation.

Ignazio Visco, ECB’s Governing Council (GC) member, commented that monetary policy must remain cautious and driven by economic data, favoring gradual rate increases. In the meantime, an ECB survey showed that EU consumers expect inflation to moderate and wages to rise. Meanwhile, Citigroup expects the ECB to raise rates to 4% by mid-2023.

EUR/USD Technical levels

The EUR/USD is neutral biased, though about to test the 200-day EMA. Tuesday’s fall below the 100-day EMA at 1.0554 exacerbated a fall toward the 200-day EMA, viewed as a trendsetter level for EUR/USD traders. A decisive break below 1.0536, the 200-day EMA would accelerate the EUR/USD pair fall toward 1.0500. Once cleared, the following support would be the YTD low at 1.0482, followed by the November 30 low at 1.0290.

What to watch?

- US Dollar dips modestly from three-month highs.

- USD/JPY sits tight as investors now focus on February jobs data in Nonfarm Payrolls.

USD/JPY is flat near 137 the figure and within the day's range of between 136.47 and 137.91 while the greenback dips modestly from three-month highs reached earlier on Wednesday following Federal Reserve Chairman Jerome Powell on Tuesday.

The US Dollar index, DXY, was reaching 105.88, the highest since Dec. 1 as the Fed chair surprised markets with a more hawkish rate outlook. Powell said that the Fed will likely need to raise interest rates more than expected in response to recent strong data and is prepared to move in larger steps if the "totality" of incoming information suggests tougher measures are needed to control inflation.

This has led the Fed funds futures markets to price in a 66% probability of a 50 basis-point hike at the Fed’s March 21-22 meeting, up from around 22% before Powell spoke on Tuesday. The rate is now expected to peak at 5.62% in September. ''Looking ahead, 25 bp hikes in May and June are priced in that would take Fed Funds to 5.50-5.75%, with nearly 30% odds of a last 25 bp hike in Q3 that would move the range up to 5.75-6.0%,'' analysts at Brown Brothers Harriman said.

''After all this, an easing cycle is still expected to begin in Q4, albeit at much lower odds. Eventually, it should be totally and unequivocally priced out into 2024 during the next stage of Fed repricing. For now, we believe the uptrends in US yields and the dollar remain intact,'' the analysts added.

Looking ahead, investors are now focused on February jobs data in Nonfarm Payrolls that is due on Friday. Another 280k increase would be unambiguously strong following a 517k increase in January, analysts at Societe Generale said. ''There is room for potentially greater giveback on the January increase, which was likely aided by warm weather. We see readings above a 150,000-175,000 threshold as strong, since over time such a pace would contribute to further declines in the unemployment rate.''

On Wednesday, the Bank of Canada (BoC), as expected kept its key interest rate unchanged at 4.50% as expected and made small changes to its forward guidance. Analysts at CIBC point out the BoC will keep their focus on the Canadian economy after showing no concern over a larger gap to US rates.

Bank of Canada keeps its eyes on the home front

“Markets were reminded that the Bank of Canada is going to keep its eyes on the home front, as the central bankers showed no tendency to follow the increasing hawkish tone from their counterparts in Washington.”

“The absence of any stated concern over a larger gap to US rates, or the resultant recent weakening in the Canadian dollar, adds weight to our view that rates can stay on hold north of the border even as the Fed has signalled another 75 basis points to come.”

“Other than a reference to the US dollar strengthening (i.e. against other currencies in general), the Bank didn't highlight any concerns about a pass through to Canadian inflation from a weaker loonie. Canadian short term rates had drifted up in recent days as markets judged that a more hawkish Fed, and the resulting foreign exchange rate moves, might drag the Bank of Canada back to the rate hiking table, and today's statement could see a bit of that unwind.”

“A no-surprise statement from the Bank of Canada relative to our expectations naturally implies no change to our view that we're done with rate hikes on this side of the border.”

- GBP/USD trims Tuesday’s losses after hitting a YTD low of 1.1802.

- Labor market data in the United States portrays a tight labor market; focus shifts to Friday’s Nonfarm Payrolls.

- BoE’s Mann: The Pound Sterling could be vulnerable to weakening based on other central banks’ outlooks.

GBP/USD stays firm at around 1.1840s, following hawkish remarks by the US Federal Reserve (Fed) Chair Jerome Powell. Powell’s two-day meeting with the US Congress would conclude today at the US House o Representatives, with market participants expecting him to remain hawkish. Therefore, the GBP/USD is exchanging hands at 1.1843, gaining 0.10%.

Federal Reserve Chair Powell testifies at the US House of Representatives

The GBP/USD would likely remain at familiar levels, as the market has priced in Powell’s hawkishness on Tuesday. On Wednesday, labor market data revealed in the United States (US) economic docket reinforced the Federal Reserve’s worries about the tightness of the labor market. February’s ADP report revealed that the US private sector added 242,000 jobs, more than the expected 200,000.

Later, job openings for January in the United States dropped less than estimates, as shown by the JOLTS report. Job openings, a measure of labor demand, decreased to 10.8M. However, data came above forecasts of 10.5M. Given the backdrop, Jerome Powell and Co. could justify higher rates, which could be confirmed by next Friday’s US Nonfarm Payrolls report.

The US Dollar Index (DXY) has trimmed some of its losses and is down 0.08%, at 105.535, after diving to 105.365. US Treasury bond yields, namely the 10-year, is still pressured, falling two and a half bps to 3.942%.

At the time of typing, Fed Chair Jerome Powell is testifying at the US House of Representatives and has managed to stay hawkish as his previous appearance in the US Senate.

On the United Kingdom (UK) front, Bank of England (BoE) policymakers had been crossing the wires. Swati Dhingra said on Wednesday that risks of overtightening “pose a more material risk at this point, through potential negative impacts from increased borrowing costs and reduced supply capacity going forwards.” Of note, she voted for no change in the last two meetings.

Contrarily, Catherine Mann, one of the hawks at the BoE, commented that the Pound Sterling (GBP) could be vulnerable to other central banks’ outlooks. That could hurt the Pound’s prospects if the Federal Reserve and the Europen Central Bank (ECB) continued their tightening cycles.

What to watch?

GBP/USD Technical levels

FOMC Chairman Jerome Powell testifies on the Semi-annual Monetary Policy Report before the US House Financial Services Committee.

Key quotes

"We are aware of lags of monetary policy effects."

"They are highly uncertain in timeframe though."

"Slowing down pace of rate hikes this year is a way to better watch for those effects."

"Data we've seen so far suggests that ultimate level of rates will need to be higher."

"Still more data to analyze though."

"Will do everything I can to bring people into consensus on any change to bank capital requirements."

Market reaction

The US Dollar Index continues to fluctuate in its daily range at around 105.50 after these comments.

FOMC Chairman Jerome Powell testifies on the Semi-annual Monetary Policy Report before the US House Financial Services Committee.

Key quotes

"US Dollar is only serious candidate for world's reserve currency."

"We can pay bills when we have negative income."

"Inflation is coming down but it's very high."

"Some part of the high inflation we have is likely related to extremely tight labor market."

"Every forecaster is baking in lower rent increases this year."

"Costs of not getting inflation down will be extremely high."

"Costs of failure to control inflation would be much higher than costs of controlling it."

"Committed to bringing prices down."

"A faster reopening from China could have offsetting effects on inflation."

"China's faster reopening could put upward pressure on commodities prices but also quicker healing of supply chains."

"We expect China's impact to be moderate overall."

Market reaction

The US Dollar stays under modest bearish pressure during Powell's testimony and the US Dollar Index was last seen posting small daily losses at 105.50.

Gold Price has dipped below its 55-Day Moving Average of $1,864. Strategists at Credit Suisse expect the yellow metal to challenge the 200-DMA at $1,775

Break above $1,890/1900 needed to clear the way for a retest of $1,973/98

“Gold has broken below its 55-DMA, currently seen at $1,864 and with the USD strengthening is seen at risk to a test of the long-term 200-DMA, currently seen at $1,775. We continue to look for this to remain a floor and for the broader risk to turn higher again from here in due course.”

“A close below $1,775 though would warn of further weakness in the broader range to test the ‘neckline’ to the September/November 2022 base at $1,729.”

“Above $1,890/1900 is needed to clear the way for a retest of $1,973/98. Beyond here stays seen needed to reassert an upward bias for a test of long-term resistance from the $2,070/72 record highs of 2020 and 2022.”

FOMC Chairman Jerome Powell testifies on the Semi-annual Monetary Policy Report before the US House Financial Services Committee.

Key quotes

"We have important data before March meeting."

"I haven't seen JOLTS data yet."

"We have not made any decision yet about March meeting, it's data-dependent."

"We will be guided by incoming data."

"Terminal rate is likely to be higher than we expected."

"Extraordinarily strong jobs report and inflation reports pointed in the same direction."

Market reaction

The US Dollar came under modest bearish pressure following these comments and the US Dollar Index was last seen losing 0.15% on the day at 105.45.

The Norwegian Krone has weakened significantly after Fed Chairman Powell’s hawkish remarks yesterday. Economists at Nordea believe the NOK will remain under severe pressure in the short-term.

Will Norges Bank come NOK to the rescue?

“We believe the NOK will remain under severe pressure in the coming weeks and moves in EUR/NOK to 11.50 and USD/NOK to 11.15 are far from unlikely.”

“With the ECB, Riksbank, and now Fed as well expect to increase rates by 50 bps in the upcoming weeks, Norges Bank’s expected 25 bps rate hike will be overshadowed. Thus, Norges Bank would have to move back to a 50 bps rate hike as well if it wants to soften the blow for the NOK from more aggressive central banks elsewhere.”

- Bank of Canada keeps interest rates unchanged, as expected.

- Loonie weakens across the board, extending daily losses.

- USD/CAD resumes upside looks at 1.3800.

The USD/CAD rose after the Bank of Canada meeting, reaching the highest intraday level since early November at 1.3793. The Loonie weakened across the board. The central bank kept rates unchanged as expected

BoC: No more 'excess demand'

The Bank of Canada (BoC) kept its key interest rate unchanged at 4.50%, as expected. “Governing Council will continue to assess economic developments and the impact of past interest rate increases, and is prepared to increase the policy rate further if needed to return inflation to the 2% target.”

According to the statement, “the latest data remains in line with the Bank’s expectation that CPI inflation will come down to around 3% in the middle of this year. Year-over-year measures of core inflation ticked down to about 5%, and 3-month measures are around 3½%. Both will need to come down further, as will short-term inflation expectations, to return inflation to the 2% target.” The BoC no longer sees “the economy in excess demand”.

The Loonie hit fresh daily lows after the report. USD/CAD moved to the 1.3790 zone, without significant impulse yet, limited by a weaker US Dollar. The Greenback is pulling back modestly amid a recovery in Treasury bonds.

Data from the US showed the Automatic Data Processing (ADP) report surpassed expectations by showing private sector employers added 242K jobs in February, above the 197K of market consensus. The JOLTS Job Openings survey came in also above expectations, at 10.82 million, down from January’s 11.23.

The US Dollar is holding onto important weekly gains after soaring Tuesday on the back of Fed Chair Jerome Powell’s testimony before the US Congress. He opened the doors to a larger rate hike at the March FOMC meeting. Powell is again at the US Congress and will take questions from lawmakers. Later, in the American session the Fed will release the Beige Book.

Jerome Powell Testimony: All about Fed Chair's second day in US Congress

The USD/CAD continues to move with a bullish bias, looking at the 1.3800 area. The next resistance might be located at 1.3825. Over the last 24 hours, the pair has risen almost 200 pips.

Technical levels

- The US ADP Employment Change report exceeded estimates but failed to boost the USD vs. the MXN.

- US Federal Reserve Chair Jerome Powell will testify in the US House of Representatives, expected to remain hawkish.

- USD/MXN Price Analysis: A break below 18.000 warrants further downside, with bears eyeing 17.4498.

The USD/MXN tumbled below the psychological $18.00 barrier on Wednesday despite hawkish remarks by US Federal Reserve’s (Fed) Chair Jerome Powell. On Tuesday, the Mexican Peso (MXN) depreciated towards the weekly high of 18.1800, but it’s staging an astonishing recovery, and dived to 5-year lows at 17.9255. At the time of writing, the USD/MXN is trading at 17.9690, down 0.76%.

US ADP employment data exceeded estimates ahead of the US NFP report

Wall Street opened in the green. The February US ADP National Employment Report showed that private hiring in the United States (US) increased by 242,000 jobs, above estimates of 200,000. That reinforces Fed Chair Jerome Powell’s stance that the labor market is tight and that there is work to do.

On Tuesday, Fed Chair Jerome Powell testified before the US Senate Finance Committee. He acknowledged that the rate peak would be higher and opened the door for significant rate hikes. Powell added that would be decided based on incoming data. Traders should be aware that the US Nonfarm Payrolls report for February and next week’s inflation data will be featured ahead of the Fed’s March meeting.

In the meantime, the US Dollar Index (DXY), a gauge of the buck’s value vs. six currencies, retraces 0.11%, down at 105.502, influenced by falling UST bond yields. The US 10-year T-note rate is at 3.913%, dropping five bps.

Aside from this, inflation in Mexico is expected to slow its pace in February, according to a Reuters poll. Seventeen analysts forecasted by Reuters expect inflation at 7.69% in February, below January’s 7.91%.

The Bank of Mexico (Banxico) central bank members expressed that rates could be raised moderately since the next monetary policy meeting, as shown by the latest meeting minutes. Even though there’s one dissenter, most of the board agreed that the tightening cycle is about to end.

That could favor a recovery of the US Dollar (USD) in the medium to long term. Therefore, the USD/MXN bias could shift upwards based on reduced interest rate differentials between the Fed and Banxico.

USD/MXN Technical analysis

The USD/MXN remains downward biased after plummeting below the 18.0000 barrier. Oscillators like the Relative Strength Index (RSI) accelerate to the downside. Meanwhile, the Rate of Change (RoC) is back below neutral, suggesting that sellers are gathering momentum. That said, the USD/MXN first support would be the July 2017 lows at 17.4498. A breach of the latter would expose April’s 2016 lows at 17.0509, ahead of $17.00.

What to watch?

- Job openings in the US declined marginally in January.

- US Dollar Index continues to fluctuate in daily range slightly above 105.50.

The data published by the US Bureau of Labor Statistics (BLS) revealed on Wednesday that the number of job openings on the last business day of January was 10.8 million, compared to 11.2 million in December. This reading came in slightly higher than the market expectation of 10.6 million.

"Over the month, the number of hires and total separations changed little at 6.4 million and 5.9 million, respectively," the BLS noted in its press release. "Within separations, quits (3.9 million) decreased, while layoffs and discharges (1.7 million) increased."

Market reaction

The US Dollar Index showed no immediate reaction to this report and was last seen trading virtually unchanged on the day at 105.58.

The US Dollar Index (DXY) remains well supported and above the 55-Day Moving Average (DMA) at 103.47. Analysts at Credit Suisse look for DXY rally to extend further to its 200-DMA and 38.2% retracement of its fall from October.

106.15/62 remains seen as key inflection point to watch

“We continue to look for a deeper recovery to 105.63 and then the 38.2% retracement of the 2022/2023 fall and 200-DMA at 106.15/62. Our bias for now remains to look for this to cap to define the top of a broader range.”

“Should a close above the 200-DMA at 106.62 be seen though this would warn of a more protracted phase of USD strength and a test of 107.80/99 next.”

“Below the 55-DMA at 103.47 would suggest the recovery may already be coming to an end but with a break below 102.59 seen needed to clear the way for a retest of the 100.82 YTD low.”

The Bank of Canada (BoC) announced on Wednesday that it left the benchmark interest rate unchanged at 4.5% following the March policy meeting. This decision came in line with the market expectation.

In its policy statement, the BoC reiterated that it expects to hold the key rate at its current level, conditional on the economy developing broadly in line with its forecasts.

Market reaction

USD/CAD edges slightly higher as investors assess the BoC's policy announcements. As of writing, the pair was trading at its highest level since early November, rising 0.2% on the day at 1.3778.

Key takeaways from the policy statement

"Latest economic data remain in line with bank's expectation that overall inflation will come down to around 3% in the middle of this year."

"Prepared to increase policy rate further if needed to return inflation to 2% target."

"Labor market remains very tight, employment growth has been surprisingly strong."

"Price increases for food and shelter remain high, causing continued hardship for Canadians."

"Restrictive monetary policy continues to weigh on household spending."

"Weak economic growth over the next couple of quarters means pressures in product and labor markets are expected to ease."

"Strength of China's recovery and impact of Russia's war in Ukraine remain key sources of upside risk to forecasts for commodity prices."

Gold fell sharply following the hawkish comments from the Fed Chair Powell. Strategists at TD Securities note that the yellow metal could suffer additional losses on a dip below the $1,806 mark.

Higher for longer narrative in rates to put more pressure on key support levels

“While central banks and physical flows have been of keen importance, and have offered support to Gold, the higher for longer narrative in rates is likely to put more pressure on key support levels.”

“A potential break below the $1,806 level would serve as the next trigger to see trend followers modestly reduce their positions.”

Ho Woei Chen, Economist at UOB Group, comments on the recently published trade balance results in the Chinese economy.

Key Takeaways

“In USD terms, exports and imports extended their declines in Jan-Feb, marking continuous declines since 4Q22.”

“China’s exports rose 29.9% in 2021 and a further 7.0% in 2022. Following the strong gains in the last two years, exports are set for a weaker trend this year as external demand slows and global semiconductor prices are pressured lower.”

“Meanwhile, imports may be boosted by China’s efforts to expand domestic consumption and an expected recovery in the economy this year.”

“Overall, we expect China’s export to register a contraction of -3.0% this year while imports may see a small gain of around +2.0% in 2023.”

- The index comes under some pressure near 105.90.

- The ADP report surpassed expectations in February.

- Powell will testify once again before Congress later in the session.

The greenback now gives away part of the initial impulse to the vicinity of the 106.00 mark and revisits the mid-105.00s when measured by the USD Index (DXY) on Wednesday.

USD Index now targets the 106.00 barrier and above

Following the earlier move to the proximity of 106.00, the dollar now faces some selling pressure as investors wait for the second semiannual testimony by Chair Powell before Congress.

The knee-jerk in the buck also comes in tandem with the now corrective drop in US yields across the curve, soon after the short end reached fresh multi-year highs past the 5% yardstick.

The recent move higher in the dollar and US yields has been propped up by the shift in investors’ sentiment towards a 50 bps rate hike by the Fed at the March event. On this, CME Group’s FedWatch Tool sees the probability of such scenario at around 75%, from nearly 9% a month ago.

In the US, MBA Mortgage Applications rose 7.4% in the week to March 3 and the ADP report showed the US private sector added 242K jobs during last month, more than initially estimated. Additionally, the Balance of Trade showed a $68.3b deficit in January. Later in the session, the JOLTs Job Openings comes next ahead of the second semiannual testimony by Chief Powell, this time before the House Financial Services Committee.

What to look for around USD

The index accelerates the upside momentum and navigate in multi-month highs following the hawkish testimony by Fed’s Powell on Tuesday.

The probable pivot/impasse in the Fed’s normalization process narrative is expected to remain in the centre of the debate along with the hawkish message from Fed speakers, all after US inflation figures for the month of January showed consumer prices are still elevated, the labour market remains tight and the economy maintains its resilience.

The loss of traction in wage inflation – as per the latest US jobs report - however, seems to lend some support to the view that the Fed’s tightening cycle have started to impact on the still robust US labour markets somewhat.

Key events in the US this week: MBA Mortgage Applications, ADP Employment Change, Balance of Trade, Powell’s Semiannual Monetary Policy Report, Fed’s Beige Book (Wednesday) – Initial Jobless Claims (Thursday) – Nonfarm Payrolls, Unemployment Rate, Monthly Budget Statement (Friday).

Eminent issues on the back boiler: Rising conviction of a soft landing of the US economy. Persistent narrative for a Fed’s tighter-for-longer stance. Terminal rates near 5.5%? Fed’s pivot. Geopolitical effervescence vs. Russia and China. US-China trade conflict.

USD Index relevant levels

Now, the index is losing 0.09% at 105.52 and the breakdown of 104.09 (weekly low March 1) would open the door to 103.50 (55-day SMA) and finally 102.58 (weekly low February 14). On the flip side, the next up-barrier emerges at 105.88 (2023 high March 8) seconded by 106.59 (200-day SMA) and then 107.19 (weekly high November 30 2022).

USD/CAD is at key breakout levels ahead of the NFP report on Friday. A weekly close above 1.3738 would trigger another leg higher, economists at Credit Suisse report.

USD/CAD is at a key inflection point at 1.3728

“A clear weekly closing break above the top of its 2-3 month range at 1.3728 would trigger a renewed trending phase to the upside, with the next levels at 1.3809, then the 1.3978/1.4000 2022 high. We note that there is also further important retracement resistance just above here at 1.4099/4100, which should be a tough barrier if reached.

“In contrast, a reversal to hold below 1.3728 on a payrolls miss would likely keep the market in the broader ~1.3300-1.3750 range.”

EUR/USD lost more than 100 pips on Tuesday and closed below 1.0550 in response to the hawkish policy signals delivered by Fed Chair Powell at semi-annual testimony to Congress. The pair could dive below the 1.05 mark, economists at MUFG Bank report.

US Dollar to rebound further in the near-term

“Powell delivered two clear hawkish policy signals over the outlook for further monetary tightening. Firstly, he stated that the latest economic data ‘suggests that the ultimate level of interest rates is likely to be higher than previously anticipated’. The second hawkish policy signal that Powell delivered was the he re-opened the door to a quick return to larger 50 bps rate hikes.”

“The developments have clearly increased upside risks for the US Dollar. While we had not been expecting the Fed to deliver such a hawkish policy update yesterday, it does support our forecast for the USD to rebound further in the near-term.”

“We had maintained our forecast for EUR/USD to fall back to the 1.05 level by the end of Q1. It could fall further still if the Fed delivers a larger 50 bps hike this month.”

Economist at UOB Group Lee Sue Ann comments on the recent decision by the RBA to lift the OCR by 25 bps to 3.60% at its event on March 7.

Key Takeaways

“The Reserve Bank of Australia (RBA) decided to increase the cash rate target by 25bps to 3.60%. This is the 10th straight meeting that the RBA has raised rates. Taking into account today’s move, the cash rate has increased by 350bps since May 2022.”

“Once again, it was highlighted in the accompanying statement that ‘the Board’s priority is to return inflation to target’, and that ‘further tightening of monetary policy will be needed to ensure that inflation returns to target and that this period of high inflation is only temporary’.”

“We are keeping our view of one more 25bps hike in Apr, which will take the OCR to 3.85%, as the RBA maintains a cautious approach. Attention will now turn to RBA Governor Philip Lowe’s speech at the AFR Business Summit in Sydney, early Wed (8 Mar) morning at 5.55am SGT.”

The S&P 500 has managed to hold 200-Day Moving Average and 38.2% retracement support at 3940/27. But a break past 4081/99 is needed to see further gains, economists at Credit Suisse report.

Close below 3927 would warn of a significant turn lower

“S&P 500 has managed to hold key support at 3940/27. Above 4081/98 though is needed to ease the pressure off this support for strength back to 4195/4203, then what we look to be tougher resistance at the 61.8% retracement of the 2022 fall and summer 2022 high at 4312/4325. We look for this to then prove a tough barrier to define the top of what we believe could be a broad and lengthy range.”

“A close below 3927 would now warn of a significant turn lower in the broader range with next support then seen at 3764/60 ahead of the long-term 200-week average at 3726.”

- EUR/USD extends the Powell-led steep drop to the 1.0520 region.

- Immediately to the downside now emerges the YTD low near 1.0480.

EUR/USD adds to Tuesday’s intense sell-off and hits new 2-month lows in the 1.0525/20 and on Wednesday.

The continuation of the selling pressure could force the pair to challenge the 2023 low at 1.0481 (January 6) ahead of the minor support at 1.0443 (weekly low December 7 2022).

Looking at the longer run, the constructive view remains unchanged while above the 200-day SMA, today at 1.0325.

EUR/USD daily chart

BoC Monetary Policy Decision – Overview

The Bank of Canada (BoC) is scheduled to announce its monetary policy decision this Wednesday at 15:00 GMT. The Canadian central bank said in January that if economic developments evolve broadly in line with the outlook, Governing Council expects to hold the policy rate at its current level while it assesses the impact of the cumulative interest rate increases. Having raised interest rates eight times since the first quarter of 2022, the BoC is now expected to leave the overnight rate unchanged at 4.5%. Investors will further take cues from the accompanying monetary policy statement in the absence of the post-meeting press conference.

Analysts at TD Securities (TDS) offer a brief preview of the event and write: “The downside surprise on Q4 GDP should allow the BoC to look past the blockbuster January jobs number and keep the overnight rate unchanged at 4.50%. The forward guidance is not expected to change too much from January, though the BoC might want to put more emphasis on the conditional nature of its pause.”

How Could it Affect USD/CAD?

Ahead of the key central bank risk, the USD/CAD pair holds steady near a four-month high touched earlier this Wednesday amid sustained US Dollar buying and a softer tone surrounding Crude Oil prices. Given that the markets have been expecting the BoC to keep rates unchanged, the announcement is unlikely to provide any meaningful impetus to the major. That said, the near-term policy outlook should infuse some volatility around the Canadian Dollar and allow traders to grab some meaningful opportunities.

From a technical perspective, the overnight sustained strength beyond the 1.3700 mark was seen as a fresh trigger for bullish traders. That said, the Relative Strength Index (RSI) on the daily chart is on the verge of breaking into the overbought territory. This makes it prudent to wait for some near-term consolidation or a modest pullback before positioning for any further appreciating move.

The USD/CAD pair, however, still seems poised to prolong the upward trajectory towards reclaiming the 1.3800 round figure. The momentum could get extended further towards an intermediate hurdle near the 1.3870-1.3880 region en route to the 1.3900 mark and the 2022 swing high, around the 1.3975-1.3980 zone.

On the flip side, the 1.3700 strong resistance breakpoint now seems to protect the immediate downside. Any subsequent pullback is more likely to attract fresh buyers and remain limited near the 1.3655-1.3650 region. The latter should act as a strong base for the USD/CAD pair.

Key Notes

• Bank of Canada Preview: Canadian Dollar set to climb on hawkish hold, market positioning

• BoC Preview: Forecasts from seven major banks, leaving rates on hold

• USD/CAD Forecast: Bulls now await BoC policy decision before placing fresh bets

About the BoC Interest Rate Decision

BoC Interest Rate Decision is announced by the Bank of Canada. If the BoC is hawkish about the inflationary outlook of the economy and raises the interest rates it is positive, or bullish, for the CAD. Likewise, if the BoC has a dovish view on the Canadian economy and keeps the ongoing interest rate, or cuts the interest rate it is seen as negative, or bearish.

- XAU/USD remains in an intraday consolidation near $1,815 after US data.

- US ADP employment reports show an increase in private payrolls above expectations.

- US Dollar holds onto recent gains, US yields retreat.